Embed Size (px)

Citation preview

Hotel Investment Forum India

Elizabeth Winkle

Managing Director, STR Global

13th January 2015

Global Hotel Industry Performance

Let the Good Times Roll November 2014 YTD RevPAR % Change, Constant Currency USD, Europe in EUR

+8.1% +4.9%€ +3.5%

+0.8%

+5.1% +17.2%

+14.1%

+2.7%

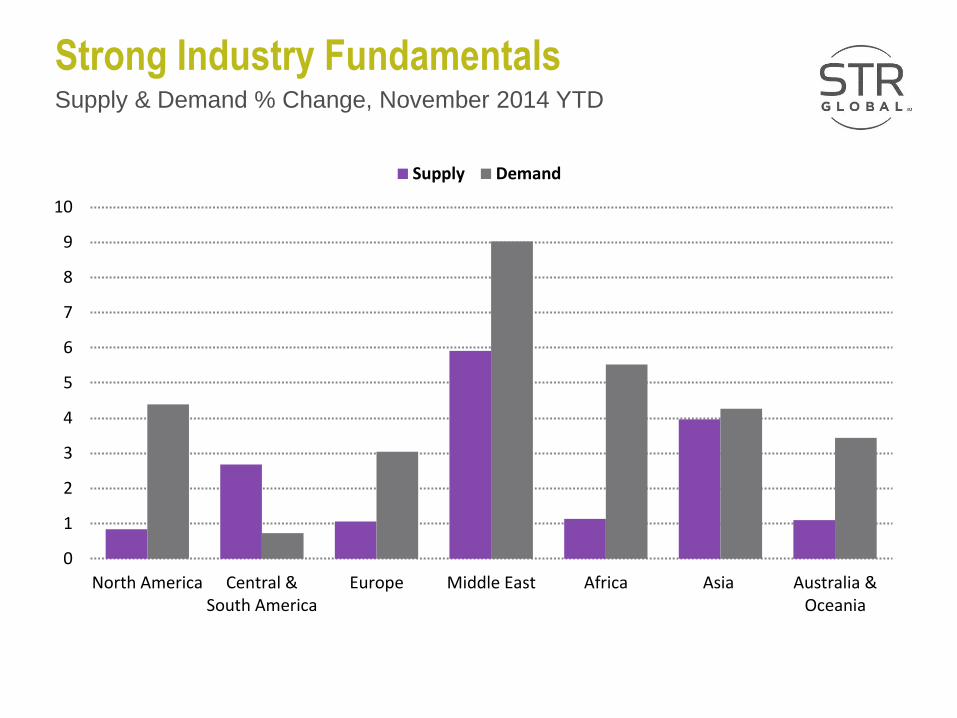

Strong Industry Fundamentals

0

1

2

3

4

5

6

7

8

9

10

North America Central &South America

Europe Middle East Africa Asia Australia &Oceania

Supply Demand

Supply & Demand % Change, November 2014 YTD

Countdown: 14 from 2014

#14 Demand: +10% from Previous Peak

12MMA Demand; Nov 2007 – Nov 2014 (indexed at Nov 2007)

0.90

1.00

1.10

1.20

Nov 14Nov 13Nov 12Nov 11Nov 10Nov 09Nov 08Nov 07

EU + UK US

#13 US: 57 months of RevPAR Growth

RevPAR Percent Change January 2001 – November 2014

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Hu

nd

red

s 57 months of growth

9/11

SARS Global

Financial crisis

56 months of growth

#12 US: Record Setting Year

#11 Europe: 16 Consecutive Growth Months

RevPAR Percent Change January 2001 – November 2014

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Hu

nd

red

s 16 months of growth

9/11

SARS Global

Financial crisis

#10 US: Pricing Power; EU Opportunity

12MMA ADR; Nov 2007 – Nov 2014 (indexed at Nov 2007)

0.80

0.90

1.00

1.10

1.20

Nov 14Nov 13Nov 12Nov 11Nov 10Nov 09Nov 08Nov 07

EU + UK (EUR) US (USD)

#9 RevPAR: 3 of 4 Back to Peak

12MMA ADR; Nov 2007 – Nov 2014 (indexed at Nov 2007)

0.60

0.70

0.80

0.90

1.00

1.10

1.20

Nov 14Nov 13Nov 12Nov 11Nov 10Nov 09Nov 08Nov 07

Europe Eastern Europe Northern Europe Southern Europe Western Europe

#8 RevPAR +>5% in 11/22 Capitals

Nov 2014 YTD % Change Demand and RevPAR, Lux & UpperUp

-38% -28% -18% -8% 2% 12% 22% 32%

AthensBucharest

Greater MadridLisbon

SofiaGreater Amsterdam

Greater BerlinBrussels

BudapestPrague

RomeGreater London

HelsinkiDublin

ParisMonacoWarsawVienna

BratislavaMoscow

Kiev

Hundreds

Demand Nov YTD RevPAR Nov YTD LC

12 months moving average Jan 2006 to November 2014

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

2010 2011 2012 2013 2014

Supply % Chg Demand % Chg

#7 MEA: Demand Pickup

+6.6%

+2.7%

November 2014 YTD, in local currency

-8%

-4%

0%

4%

8%

12%

16%

Occupancy ADR

#6 MEA: Egypt Summer Recovery

# of international tourist arrivals in millions; Global & APAC

234 APAC

2012

Global 1.035

260 APAC

2014 f

Global 1.132

219

APAC

2011

Global

995

248 APAC

2013

Global 1.087

Source: UNWTO

#5 APAC: Int’l Arrivals +12m YOY

Market performance – RevPAR % Growth, Nov 2014 YTD, USD (CC)

North-

Eastern

Central

& South

South- Eastern

Australia

Oceania

+1.0%

-0.6%

-0.8%

+4.9%

%

%

$

$ and %

#4 APAC: Performance Improvement

November 2014 YTD, in local currency

-4%

0%

4%

8%

12%Occupancy ADR Thailand O -13% A +3%

#3 APAC Performance: Mostly Positive

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Bangladesh

Mongolia

Myanmar

Sri Lanka

…+235%

+76%

+72%

+45%

Pipeline as a % of existing supply

#2 Pipeline: Ones to Watch

Pipeline by Room Count November 2014

54%

12% 11%

Malaysia 4%

Japan 3%

Philippines 2%

Thailand 3%

Australia 2%

Vietnam 2%

Myanmar 1%

Others 6%

#1 APAC: Pipeline by Country

2015 Resolutions

RevPAR growth 2015, November 2014 edition

Forecast: 32/37 Markets Set to Rise

Takeaways

Strong Demand: Outpacing supply in most regions

Supply Growth: Slower than previous years

Stable Occupancies: Creates ADR opportunities

Recovery or Growth: Most global markets

International Arrivals: More travelling and ease of

travel improving (airlift, visa)

2015 Outlook: Positive

Threats

Economic Instability

Political Instability

Real & Perceived Security Threats

Cost of Oil (+ and -)

FX

STR Global

www.strglobal.com You can follow us on LinkedIn, Twitter, Facebook

STR Global, Ltd is the exclusive owner of all rights in this presentation and its content. Reproduction of all or a portion of this presentation for any purpose without prior approval of STR Global is strictly prohibited. This presentation is based on information compiled by STR Global Ltd. No strategic or marketing recommendations or advice are intended or implied.

Global Hotel Industry Performance

Elizabeth Winkle

![[XLS] · Web viewSTR 20015 STR 30105 STR 30115 STR 30123 STR 30125 STR 30130 STR 40090 ORİ STR 40115 STR 41090 ORİ STR 44115 STR 45111 STR 50020 STR 50103A STR 50112 STR 50113A](https://img.pdfslide.us/doc/110x75/5ad04b0c7f8b9a1d328e1e93/xls-viewstr-20015-str-30105-str-30115-str-30123-str-30125-str-30130-str-40090.jpg)