Embed Size (px)

Citation preview

BNEF WIND ENERGY BRIEFING

Yiyi Zhou

28 April 2016

1

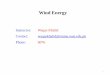

LEVERAGING THE POWER OF BLOOMBERG

Since 1981

Over 15,000 employees

in 192 locations

Generating 5,000 news stories

per day from 150 bureaus

320,000 global clients

Since 2004

200 employees

in 15 locations on six continents

Generating over 700 Insight

reports annually

2,500 global clients

2

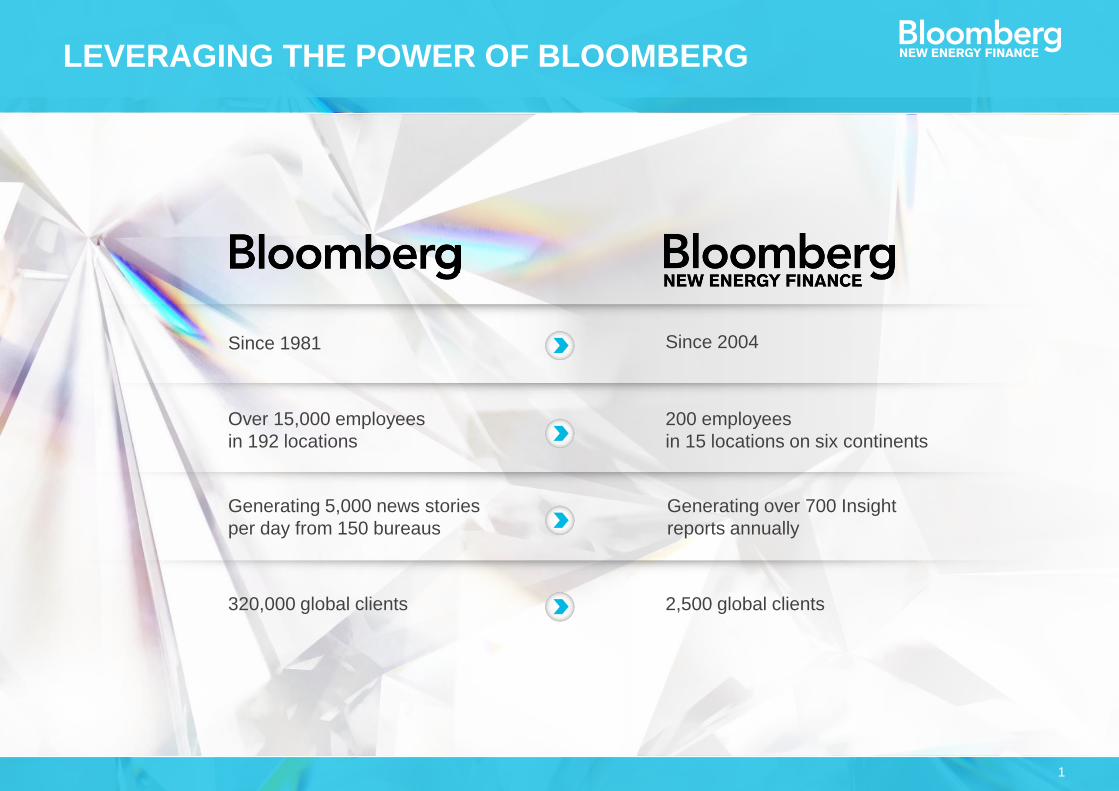

200 ENERGY EXPERTS WITH STRONG KNOWLEDGE AND NETWORK ACROSS SIX CONTINENTS

San

Francisco

Washington DC

Sao Paulo

Cape Town Sydney

Singapore

Zurich

Munich

London

New DelhiHong

Kong

Tokyo

Beijing

Seoul

New York

North America

40

SouthAmerica

5

Europe90

Africa30

AsiaPacific

40

3

Europe, Middle East

& Africa

Asia PacificAmericas

PRODUCTS TO HELP YOU UNDERSTAND THE FUTURE OF ENERGY

Solar WindOther

Renewables

Advanced

Transport

Energy Smart

TechnologiesGas

Carbon &

RECs Markets

4

Source:

http://cn.bing.com/images/search?q=wind+turbine+community&view=detailv2&&id=8ED992341002389CDFE3EAF7E77E

924D489175F6&selectedIndex=363&ccid=LzDANnOJ&simid=607996095383866982&thid=OIP.M2f30c03673890ab014df

cc2d8db46760o0&ajaxhist=0

Insert Date (go to Insert Tab, Header & Footer and Apply to All)

COMMUNITY SCALE WIND TURBINE

5

Source: Bloomberg New Energy Finance

Insert Date (go to Insert Tab, Header & Footer and Apply to All)

TWO TYPES OF UTILITY SCALE WIND ENERGY

Offshore wind farmOnshore wind farm

6

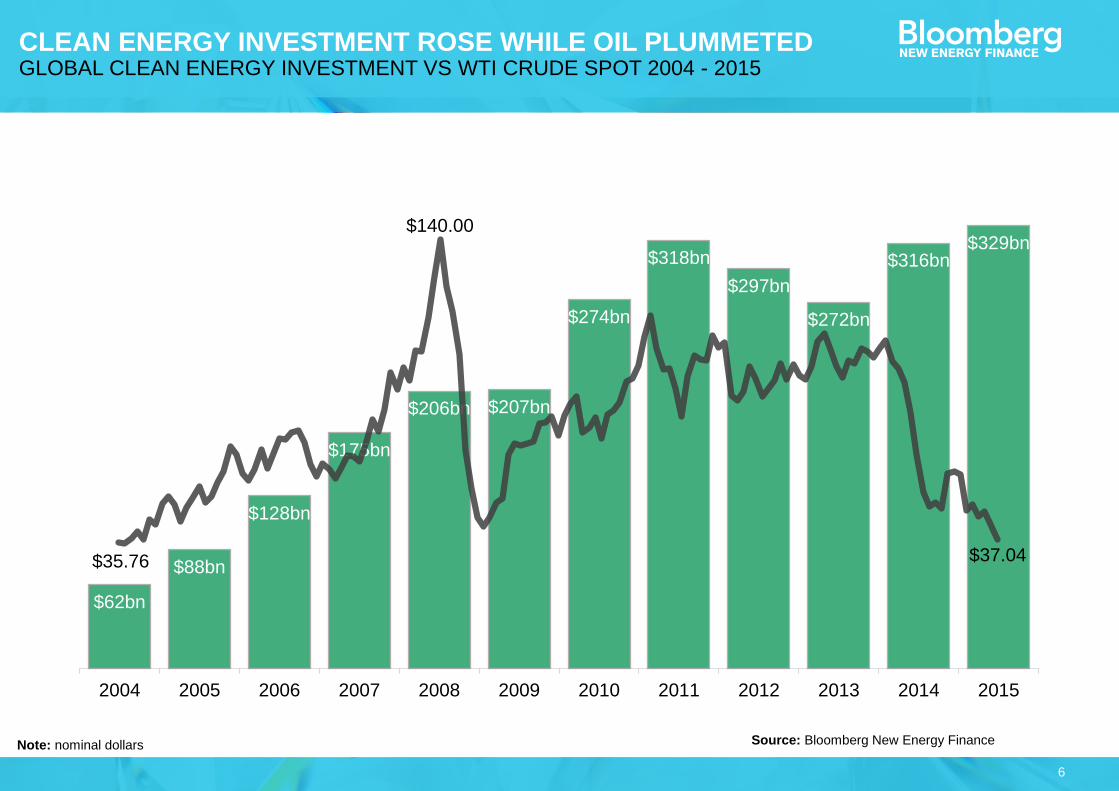

CLEAN ENERGY INVESTMENT ROSE WHILE OIL PLUMMETEDGLOBAL CLEAN ENERGY INVESTMENT VS WTI CRUDE SPOT 2004 - 2015

$62bn

$88bn

$128bn

$175bn

$206bn $207bn

$274bn

$318bn

$297bn

$272bn

$316bn$329bn

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$37.04

$140.00

$35.76

Source: Bloomberg New Energy FinanceNote: nominal dollars

7

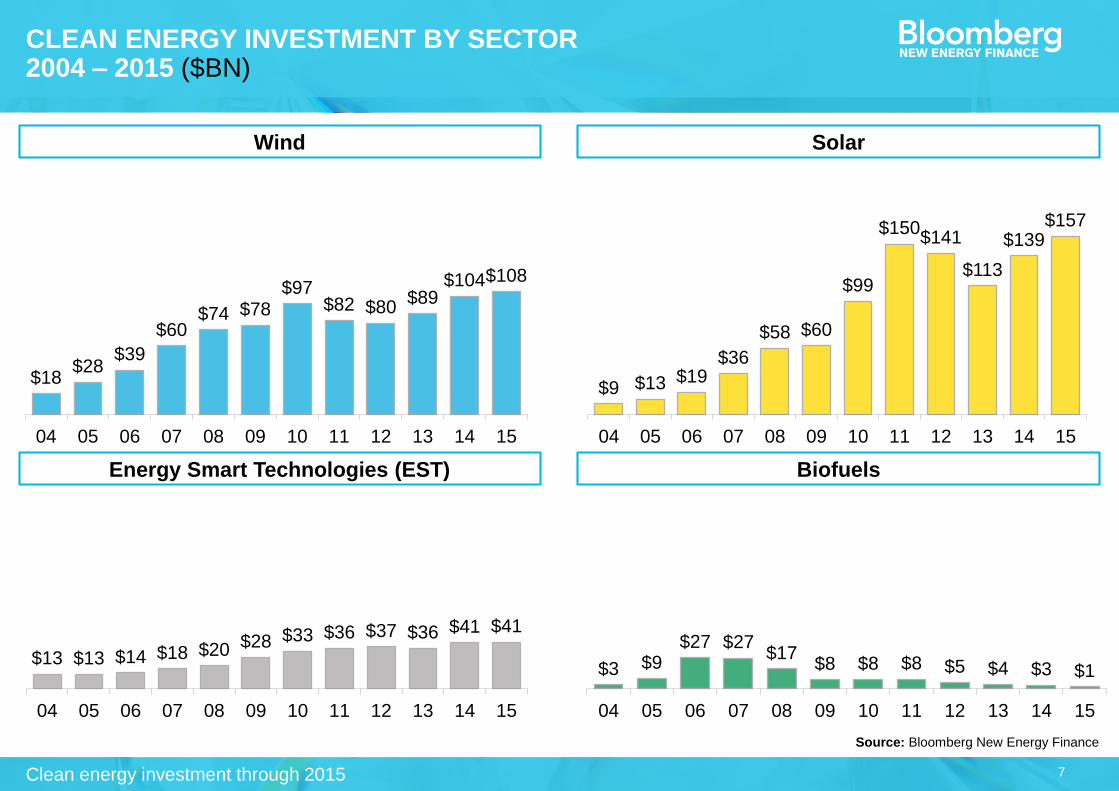

CLEAN ENERGY INVESTMENT BY SECTOR2004 – 2015 ($BN)

Wind Solar

Energy Smart Technologies (EST) Biofuels

Source: Bloomberg New Energy Finance

Clean energy investment through 2015

$18$28

$39

$60$74 $78

$97$82 $80

$89$104$108

04 05 06 07 08 09 10 11 12 13 14 15

$9 $13 $19$36

$58 $60

$99

$150$141

$113

$139$157

04 05 06 07 08 09 10 11 12 13 14 15

$13 $13 $14 $18 $20 $28 $33 $36 $37 $36 $41 $41

04 05 06 07 08 09 10 11 12 13 14 15

$3 $9$27 $27

$17$8 $8 $8 $5 $4 $3 $1

04 05 06 07 08 09 10 11 12 13 14 15

8

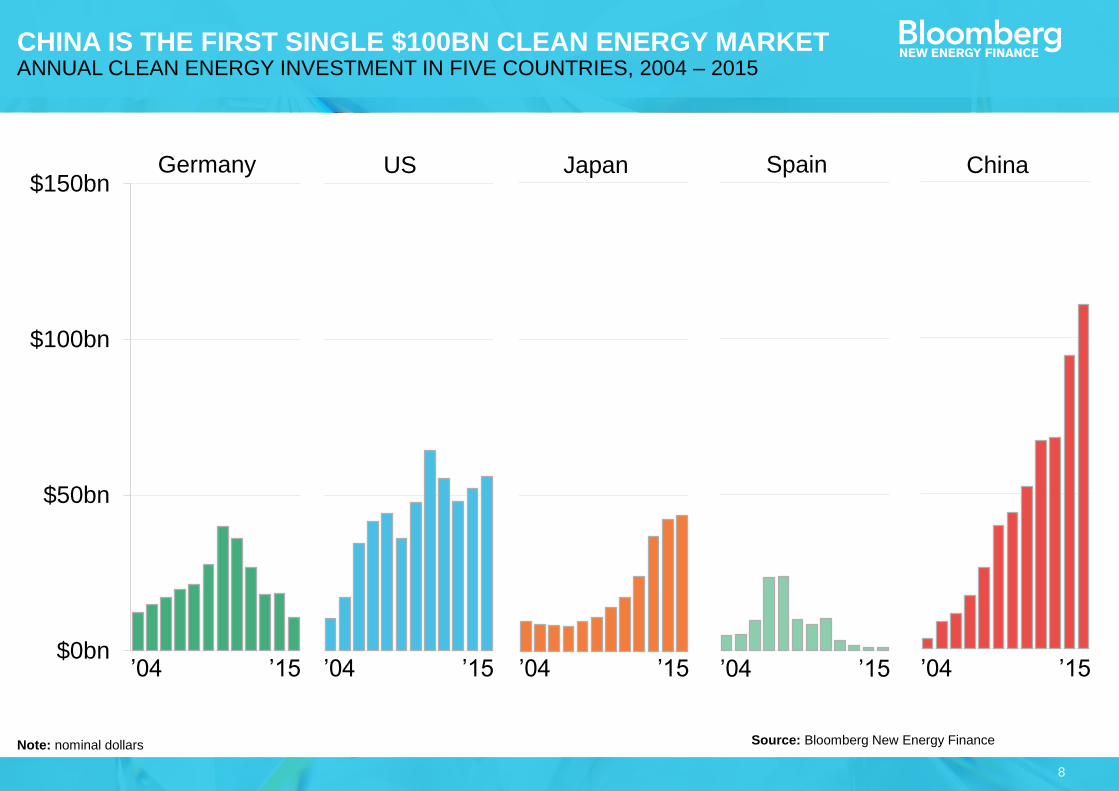

CHINA IS THE FIRST SINGLE $100BN CLEAN ENERGY MARKETANNUAL CLEAN ENERGY INVESTMENT IN FIVE COUNTRIES, 2004 – 2015

$0bn

$50bn

$100bn

$150bn

$0bn

$50bn

$100bn

$150bn

$0bn

$50bn

$100bn

$150bn

$0bn

$50bn

$100bn

$150bn

$0bn

$50bn

$100bn

$150bnGermany US Japan Spain China

’04 ’15 ’04 ’15 ’04 ’15 ’04 ’15 ’04 ’15

Source: Bloomberg New Energy FinanceNote: nominal dollars

9

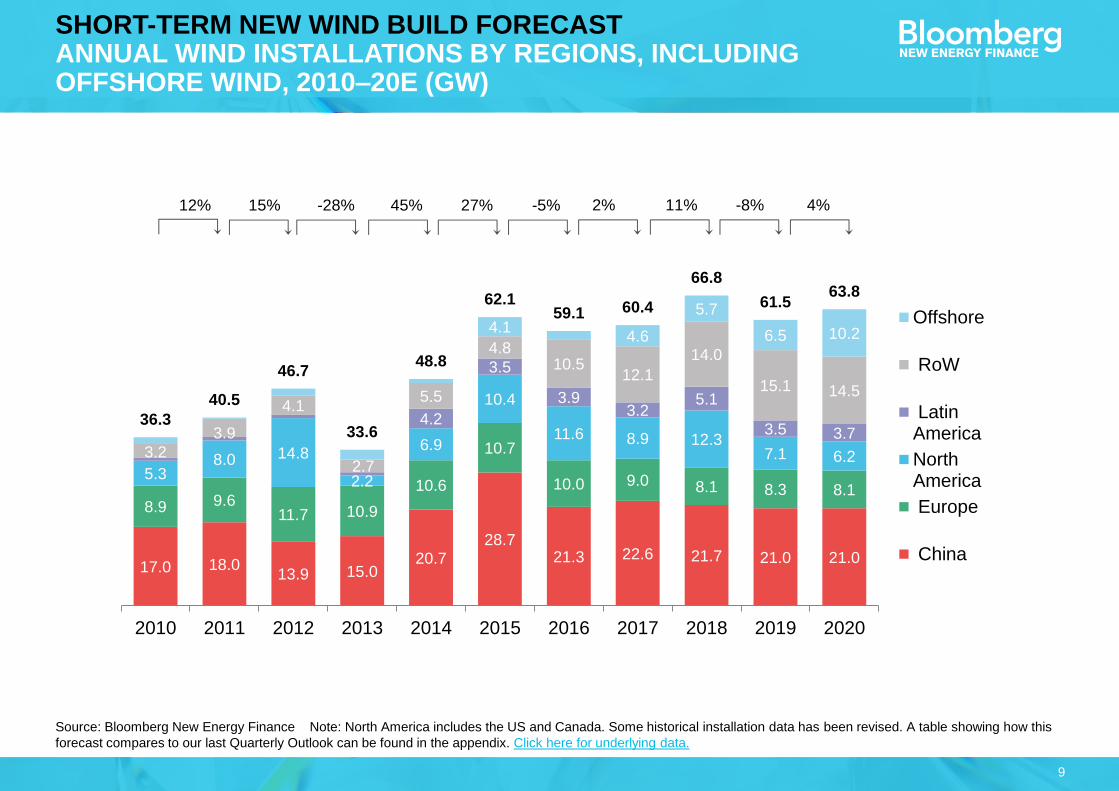

Source: Bloomberg New Energy Finance Note: North America includes the US and Canada. Some historical installation data has been revised. A table showing how this

forecast compares to our last Quarterly Outlook can be found in the appendix. Click here for underlying data.

SHORT-TERM NEW WIND BUILD FORECASTANNUAL WIND INSTALLATIONS BY REGIONS, INCLUDING OFFSHORE WIND, 2010–20E (GW)

17.0 18.013.9 15.0

20.728.7

21.3 22.6 21.7 21.0 21.0

8.9 9.611.7 10.9

10.6

10.7

10.0 9.0 8.1 8.3 8.15.3

8.0 14.8

2.2

6.9

10.4

11.6 8.9 12.37.1 6.2

4.2

3.5

3.93.2

5.1

3.5 3.7

3.2

3.9

4.1

2.7

5.5

4.810.5

12.1

14.0

15.1 14.5

4.14.6

5.7

6.5 10.2

36.3

40.5

46.7

33.6

48.8

62.159.1 60.4

66.8

61.563.8

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Offshore

RoW

LatinAmerica

NorthAmerica

Europe

China

12% 15% -28% 45% 27% -5% 2% 11% -8% 4%

10

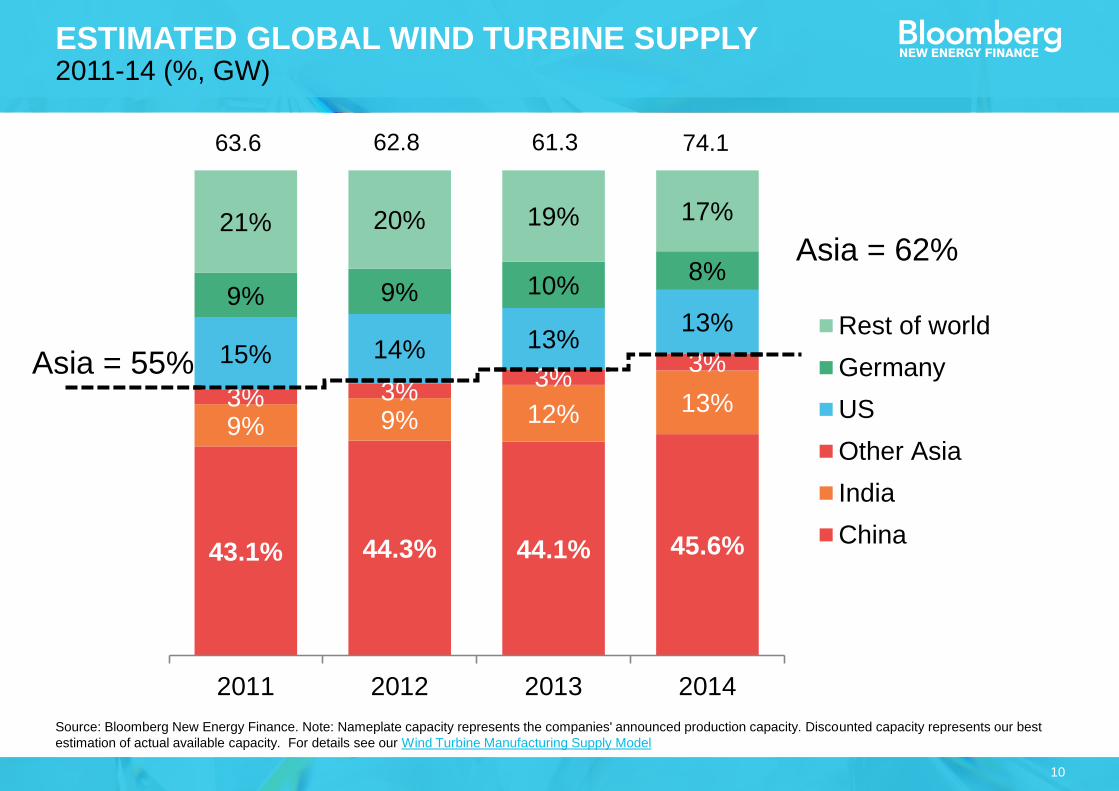

Source: Bloomberg New Energy Finance. Note: Nameplate capacity represents the companies' announced production capacity. Discounted capacity represents our best

estimation of actual available capacity. For details see our Wind Turbine Manufacturing Supply Model

ESTIMATED GLOBAL WIND TURBINE SUPPLY2011-14 (%, GW)

43.1% 44.3% 44.1% 45.6%

9% 9% 12% 13%3% 3%3%

3%15% 14% 13%13%

9% 9% 10%8%

21% 20% 19% 17%

2011 2012 2013 2014

Rest of world

Germany

US

Other Asia

India

China

63.6 62.8 61.3 74.1

Asia = 62%

Asia = 55%

11

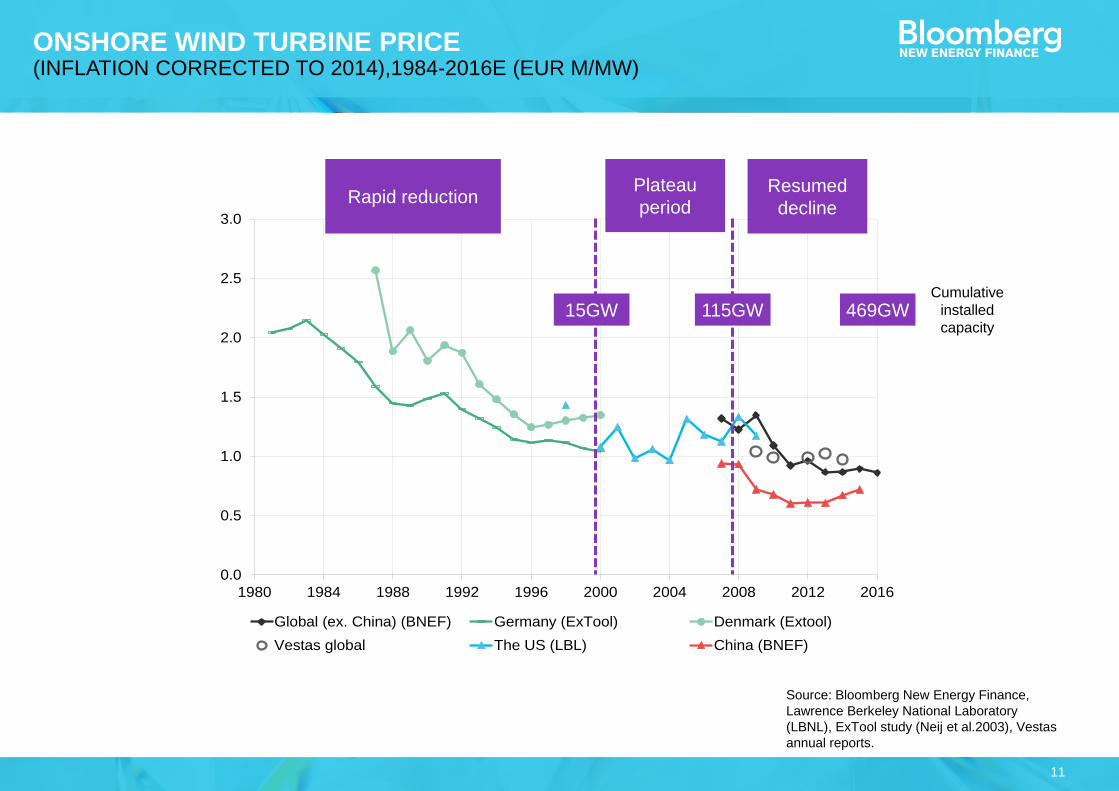

Source: Bloomberg New Energy Finance,

Lawrence Berkeley National Laboratory

(LBNL), ExTool study (Neij et al.2003), Vestas

annual reports.

ONSHORE WIND TURBINE PRICE(INFLATION CORRECTED TO 2014),1984-2016E (EUR M/MW)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Global (ex. China) (BNEF) Germany (ExTool) Denmark (Extool)

Vestas global The US (LBL) China (BNEF)

Rapid reductionPlateau

periodResumed

decline

15GW 115GW 469GWCumulative

installed

capacity

12

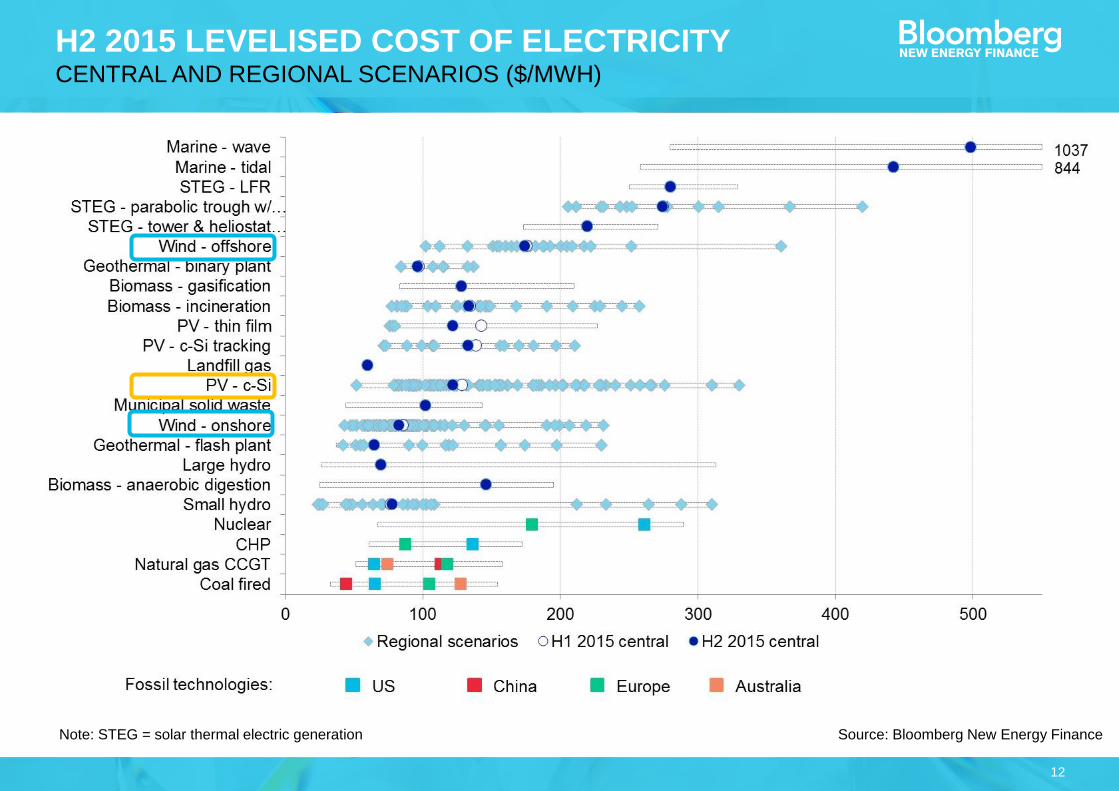

H2 2015 LEVELISED COST OF ELECTRICITYCENTRAL AND REGIONAL SCENARIOS ($/MWH)

Source: Bloomberg New Energy FinanceNote: STEG = solar thermal electric generation

13

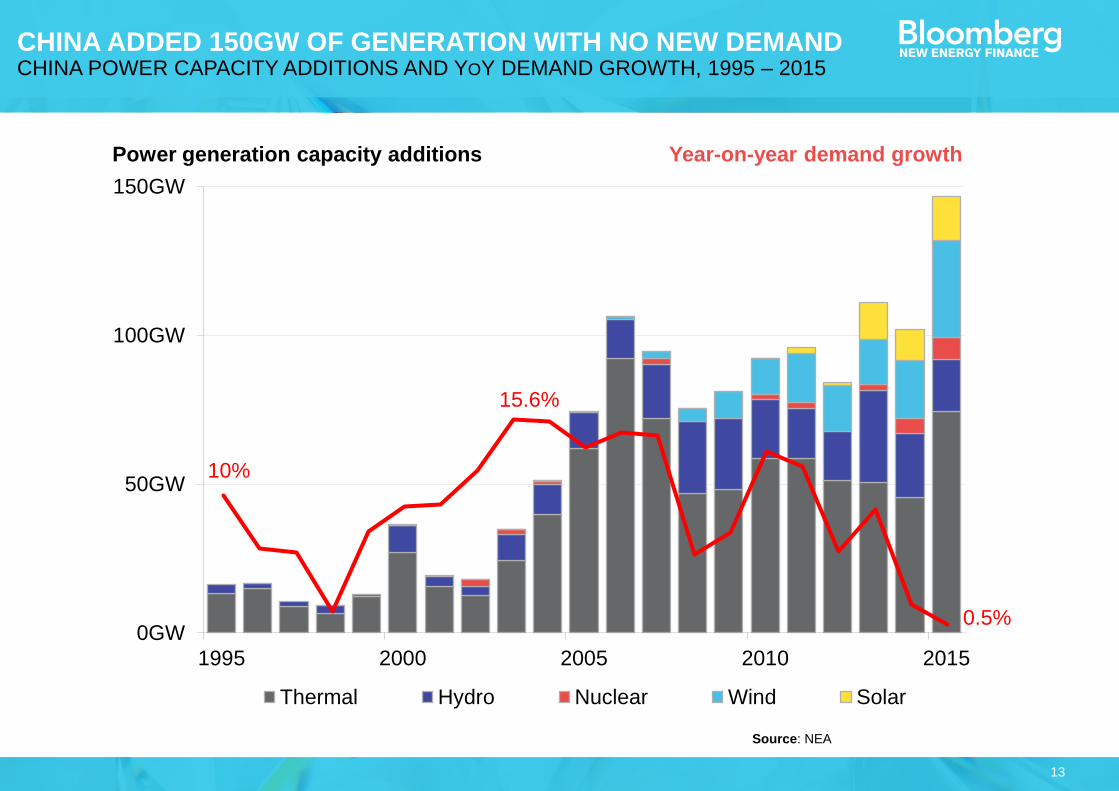

CHINA ADDED 150GW OF GENERATION WITH NO NEW DEMANDCHINA POWER CAPACITY ADDITIONS AND YOY DEMAND GROWTH, 1995 – 2015

Source: NEA

0GW

50GW

100GW

150GW

1995 2000 2005 2010 2015

Thermal Hydro Nuclear Wind Solar

10%

15.6%

0.5%

Power generation capacity additions Year-on-year demand growth

14

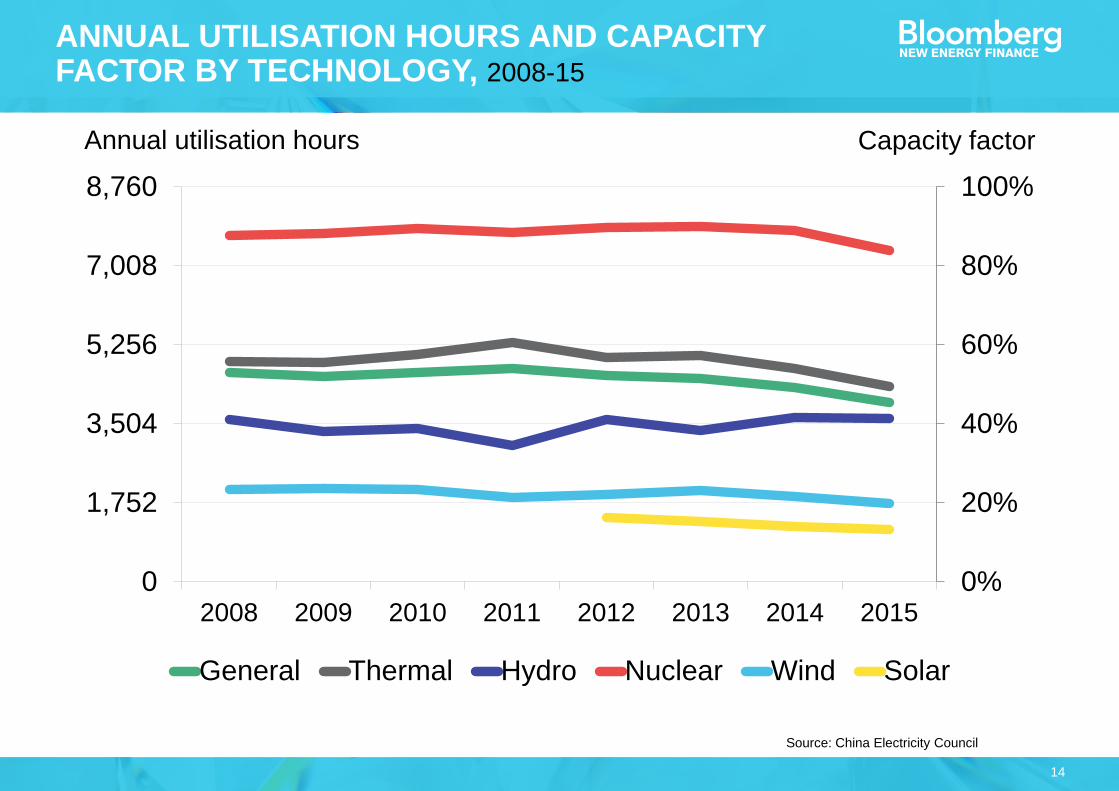

0%

20%

40%

60%

80%

100%

0

1,752

3,504

5,256

7,008

8,760

2008 2009 2010 2011 2012 2013 2014 2015

General Thermal Hydro Nuclear Wind Solar

Source: China Electricity Council

ANNUAL UTILISATION HOURS AND CAPACITY FACTOR BY TECHNOLOGY, 2008-15

Annual utilisation hours Capacity factor

15

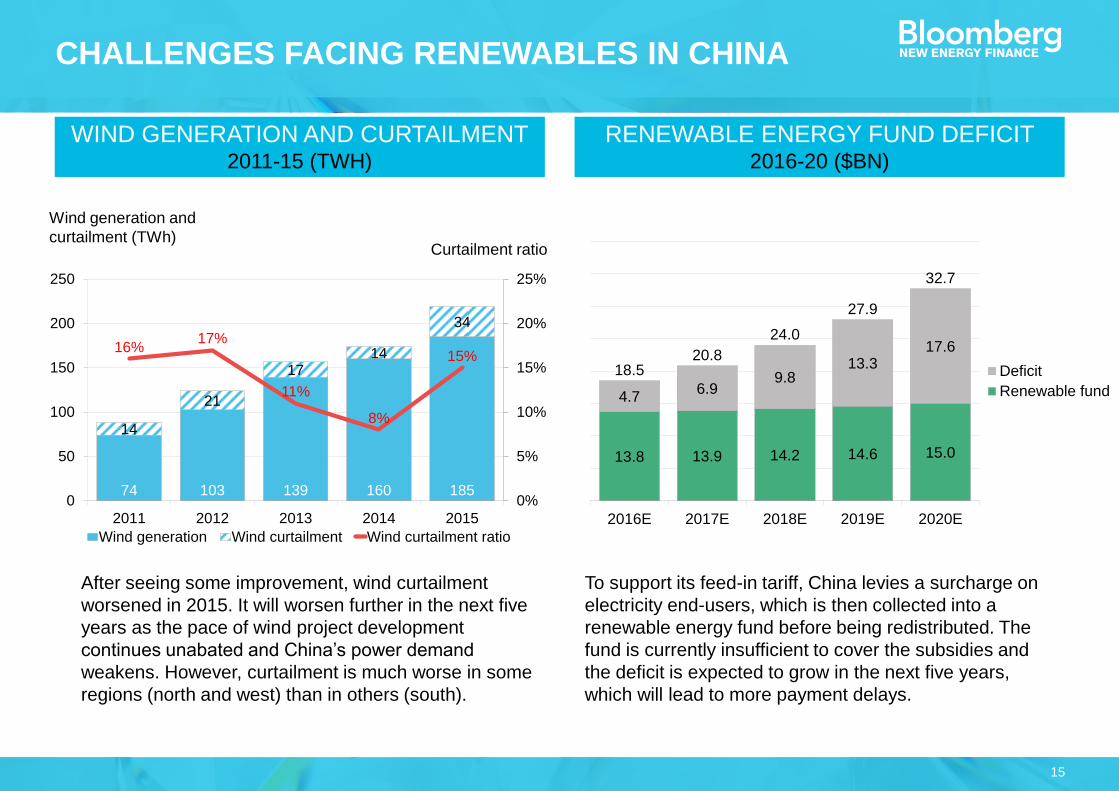

CHALLENGES FACING RENEWABLES IN CHINA

WIND GENERATION AND CURTAILMENT 2011-15 (TWH)

RENEWABLE ENERGY FUND DEFICIT 2016-20 ($BN)

74 103 139 160 185

14

21

1714

34

16%17%

11%

8%

15%

0%

5%

10%

15%

20%

25%

0

50

100

150

200

250

2011 2012 2013 2014 2015

Wind generation Wind curtailment Wind curtailment ratio

Wind generation and

curtailment (TWh)Curtailment ratio

13.8 13.9 14.2 14.6 15.0

4.76.9

9.813.3

17.6

18.520.8

24.0

27.9

32.7

2016E 2017E 2018E 2019E 2020E

Deficit

Renewable fund

To support its feed-in tariff, China levies a surcharge on

electricity end-users, which is then collected into a

renewable energy fund before being redistributed. The

fund is currently insufficient to cover the subsidies and

the deficit is expected to grow in the next five years,

which will lead to more payment delays.

After seeing some improvement, wind curtailment

worsened in 2015. It will worsen further in the next five

years as the pace of wind project development

continues unabated and China’s power demand

weakens. However, curtailment is much worse in some

regions (north and west) than in others (south).

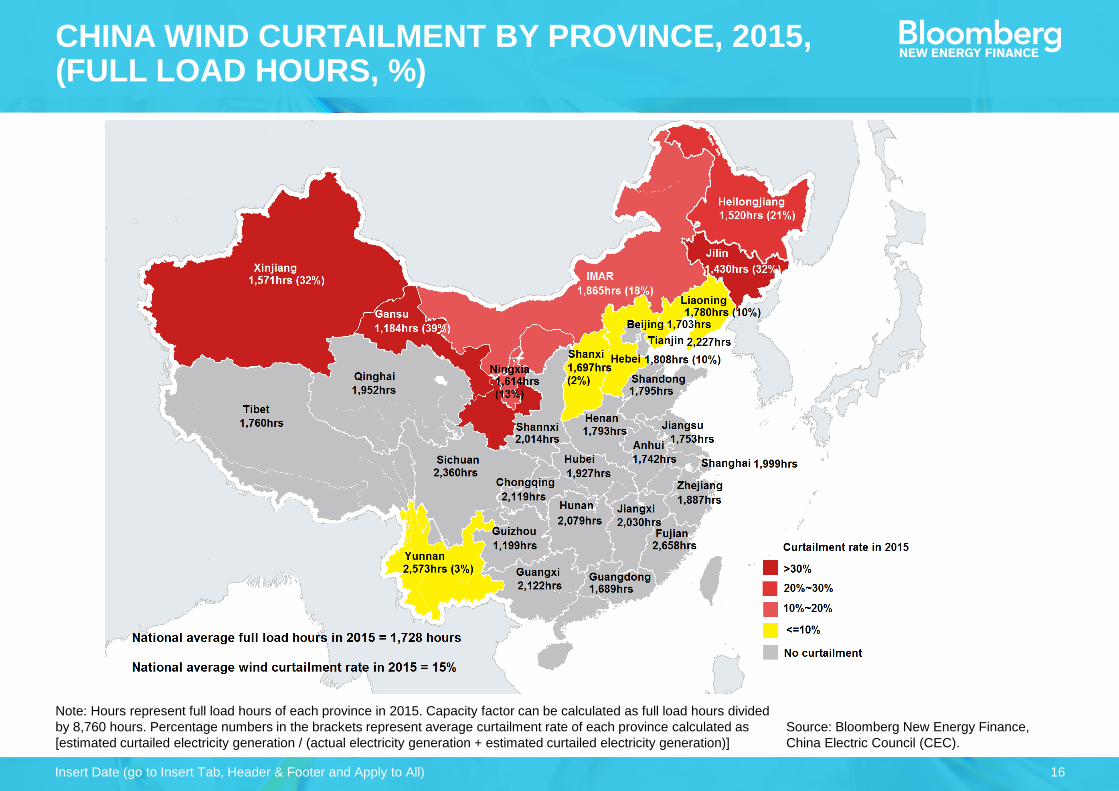

16

Note: Hours represent full load hours of each province in 2015. Capacity factor can be calculated as full load hours divided

by 8,760 hours. Percentage numbers in the brackets represent average curtailment rate of each province calculated as

[estimated curtailed electricity generation / (actual electricity generation + estimated curtailed electricity generation)]

Source: Bloomberg New Energy Finance,

China Electric Council (CEC).

Insert Date (go to Insert Tab, Header & Footer and Apply to All)

CHINA WIND CURTAILMENT BY PROVINCE, 2015, (FULL LOAD HOURS, %)

17

● High capital investment

● Complicated development and construction

process

● Limited types of wind farm developers and

financing model

Source: Bloomberg New Energy Finance

Insert Date (go to Insert Tab, Header & Footer and Apply to All)

KEY BARRIERS FOR COMMUNITY LEVEL INVESTOR TO ENTER WIND MARKET

18

Source: Bloomberg New Energy Finance

Insert Date (go to Insert Tab, Header & Footer and Apply to All)

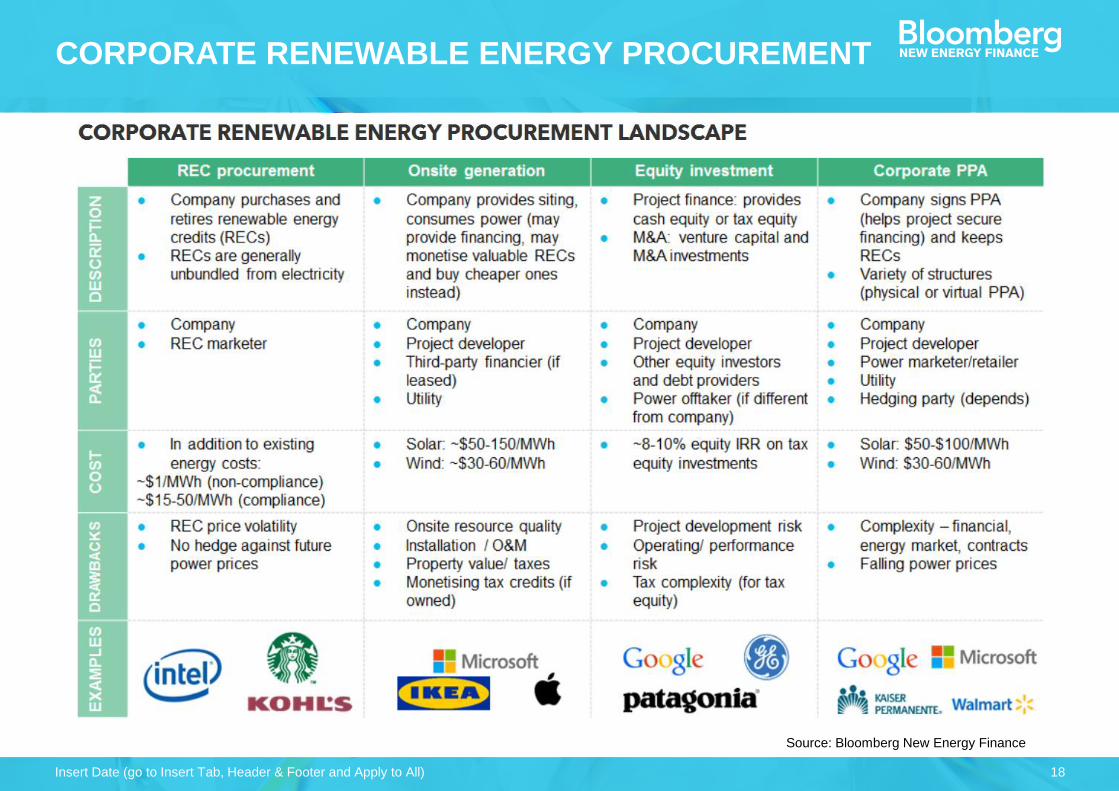

CORPORATE RENEWABLE ENERGY PROCUREMENT

19

This publication is the copyright of Bloomberg New Energy Finance. No portion of this document may be photocopied,

reproduced, scanned into an electronic system or transmitted, forwarded or distributed in any way without prior consent of

Bloomberg New Energy Finance.

The information contained in this publication is derived from carefully selected sources we believe are reasonable. We do

not guarantee its accuracy or completeness and nothing in this document shall be construed to be a representation of such

a guarantee. Any opinions expressed reflect the current judgment of the author of the relevant article or features, and does

not necessarily reflect the opinion of Bloomberg New Energy Finance, Bloomberg Finance L.P., Bloomberg L.P. or any of

their affiliates ("Bloomberg"). The opinions presented are subject to change without notice. Bloomberg accepts no

responsibility for any liability arising from use of this document or its contents. Nothing herein shall constitute or be

construed as an offering of financial instruments, or as investment advice or recommendations by Bloomberg of an

investment strategy or whether or not to "buy," "sell" or "hold" an investment.

COPYRIGHT AND DISCLAIMER

Insert Date (go to Insert Tab, Header & Footer and Apply to All)

Unique analysis, tools and data for decision-makers

driving change in the energy system

MARKETS Renewable Energy

Energy Smart Technologies

Advanced Transport

Gas

Carbon and RECs

SERVICESAmericas Service

Asia Pacific Service

EMEA Service

Applied Research

Events and Workshops

Yiyi Zhou