Embed Size (px)

Citation preview

Monitor signals in large companies, anticipate structural changes

– and provide leaders the intelligence to drive agility

(Feb 1, 2013 - April 30, 2015) www.genpact.com/home/volatility-adaptation-index

Volatility and Adaptation Index (VAI)

DESIGN ∙ TRANSFORM ∙ RUN

DESIGN • TRANSFORM • RUN 2 © 2015 Copyright Genpact. All Rights Reserved.

CONTENTS

Introduction: Genpact Volatility and Adaptation Index (VAI) 03

Why Volatility and Adaptation Index (VAI)? 03

Methodology 04

Section 1: Overall insights 06

Recurring themes for volatility and adaptation 09

Main drivers of VAI 10

Analysis of 3 months covering Feb‘15-Apr’15

Section 2: Industry specific analysis 13

Comparison across industries 14

27 month historical trend across industries

Comparison of VAI across industries in the last 3 months

Retail banking 22

Commercial banking 23

Capital markets 24

Insurance 25

Healthcare 26

Life sciences 27

Consumer goods 28

Manufacturing 29

High tech 30

DESIGN • TRANSFORM • RUN 3 © 2015 Copyright Genpact. All Rights Reserved.

Insight into global enterprises’ environment and structural moves facilitates strategy and organizational alignment

• Unprecedented economic volatility leads global

companies to adapt, often through transformed

business operations

• Events like profit warnings, cost-cutting initiatives,

M&A, change of senior leadership signal volatility,

and adaptation measures

• Genpact Volatility and Adaptation Index (VAI) is a

directional measure based on monitoring of large

data sets across a sample of 800 companies

• It provides senior leaders with the intelligence to

inform structural decisions and facilitate

organizational alignment

Why volatility and adaptation index (VAI)?

DESIGN • TRANSFORM • RUN 4 © 2015 Copyright Genpact. All Rights Reserved.

Volatility and Adaptation Index - sample

Methodology

Heathcare

Others

High tech

Manufacturing

Life sciences

Insurance

Consumer goods

Capital markets

Retail banking

Commercial banking

9%

5% 7%

10%

11%

21%

9%

12%

7%

9%

Europe Asia-Pacific and Japan

North America

63%

16% 21%

By Industry By Geography

DESIGN • TRANSFORM • RUN 5 © 2015 Copyright Genpact. All Rights Reserved.

Volatility and Adaptation Index (VAI) - methodology

800 global

companies

with sizeable

operations

63% North

America

21% Europe

16% Asia

Pacific and

Japan

Identified

“events” that

signal current

or future

volatility

correlated to

changes in

operating

strategy-

restructuring,

change in

leadership,

regulatory etc.

Monitoring of

online media,

newswires,

publications,

financial

statements,

databases and

social media to

screen content

Analytics to

filter the news,

attribute

relevance and

salience

Volatility and

Adaptation

Index =

[% of companies

displaying

events]

X

[average number

of volatility

events per

company]

• This release covers 27 months with data updated till April 30, 2015

• Events include both macro industry-wide events such as regulations and company

level events like financial underperformance or cost cutting

• Industries - Banking, Insurance, Capital Markets, Healthcare, Life Sciences,

Manufacturing, Consumer goods, etc.

Quarterly Index Analytics Definition

Methodology

Section 1

Overall insights

DESIGN • TRANSFORM • RUN 7 © 2015 Copyright Genpact. All Rights Reserved.

Executive Summary

Financial pressure rising again amidst relatively stable enterprise volatility. Time for CEOs action

• Future still uncertain, and temporary

stability is a good time to prepare

• Heed agility imperative: Comparative speed

of adaptation might determine success against

competitors and has implications for

shareholders as performance is scrutinized

• Enhance ability to change enterprise-wide

direction fast: speed of strategy formation and

organizational alignment can be shortened by

• Observing practices adopted by early

movers-some monitored by VAI

• Creating a burning platform internally by

communicating those competitors’ moves

• Utilizing lean-management principles to:

Align strategy with execution; sustain the

pace of change by discovering better ways

of working and enabling people to

contribute fully; generate material impact by

delivering value efficiently to customers

• Total index flat at moderate levels in the

last 12 months* compared to highs of 2013;

45% companies manifest some volatility and

change

• Financial conditions, M&A increase; fewer

companies reported cost cutting and

restructuring

• Retail banking (leadership changes, financial

conditions most widespread), followed by life

sciences have highest VAI in last 3 months

• Largest reduction in VAI for high tech

followed by insurance

• Results corroborated by Genpact’s own

operational measurements e.g. Mortgage

operations in banks; Consumer goods, life

sciences’ keen interest in operations

transformation services

* May 2014 – April 2015

Insights Implications for C-suite

DESIGN • TRANSFORM • RUN 8 © 2015 Copyright Genpact. All Rights Reserved.

DESIGN • TRANSFORM • RUN 9 © 2015 Copyright Genpact. All Rights Reserved.

Overview ► Main themes ► Feb’15–Apr‘15

Recurring themes for volatility and adaptation*

*Data from Feb’1, 2015 to Apr’30, 2015

WORD CLOUD ANALYSIS ALL INDUSTRIES

Feb’15-Apr‘15 Word cloud illustrates frequency of text observed. Size of word corresponds to the

number of times the word was used across all data sources.

DESIGN • TRANSFORM • RUN 10 © 2015 Copyright Genpact. All Rights Reserved.

Overview ► Main drivers ► Last 3 months (Feb’15–Apr’15) vs. trailing 12 months

Financial pressures, M&A and leadership changes account for much of VAI in the last 3 months

Vo

latilit

y a

nd

Ad

ap

tatio

n In

de

x

M&A activity picked up

in last 3 months

compared to trailing 12

months

Leadership changes

reduced in last 3

months compared to

trailing 12 months

Pressure on financial

condition increased in

the last 3 months

compared to trailing 12

months

ALL INDUSTRIES

Feb’15– Apr‘15

Ove

rall

Ind

us

try,

reg

ula

tory

or

geo

gra

ph

ic

ch

an

ge

Fin

an

cia

l

co

nd

itio

n

Re

str

uc

turi

ng

Lea

ders

hip

ch

an

ge

Ac

qu

isit

ion

or

ge

og

rap

hic

ex

pan

sio

n

Volatility events

Adaptation responses

+42%

Feb’15-

Apr’15

Trailing

12

Months

-33%

Feb’15-

Apr’15

Trailing

12

Months

+57%

Feb’15-

Apr’15

Trailing

12

Months

DESIGN • TRANSFORM • RUN 11 © 2015 Copyright Genpact. All Rights Reserved.

Overview ► Main drivers ► Historical trend (Feb’13–Apr’15)

VAI flat compared to trailing 12 months average; share of volatility events increases

Vo

lati

lity

an

d A

dap

tati

on

In

dex

ALL INDUSTRIES

Feb’13–Apr‘15 Adaptation responses Volatility events

Feb’13–

Apr‘13

May’13–

Jul'13

Aug’13–

Oct‘13

Nov’13–

Jan‘14

Feb’14–

Apr‘14

May’14–

Jul’14

Trailing

12 months

average

43 39 21 26 19 25 22 34 22 27

Restructuring

Industry, regulatory or geography changes

Financial condition

Acquisition or geographical expansion

Leadership change

Aug’14–

Oct’14

Nov’14–

Jan’15

Feb’15–

Apr’15

DESIGN • TRANSFORM • RUN 12 © 2015 Copyright Genpact. All Rights Reserved.

Overview ► Main drivers ► Historical trend (Feb’13–Apr’15)

VAI flat compared to trailing 12 months average; share of volatility events rises

Vo

lati

lity

an

d A

dap

tati

on

In

dex

ALL INDUSTRIES

Feb’13–Apr‘15 Adaptation responses Volatility events

Feb’13–

Apr‘13

May’13–

Jul'13

Aug’13–

Oct‘13

Nov’13–

Jan‘14

Feb’14–

Apr‘14

May’14–

Jul’14

Trailing

12 months

average

Aug’14–

Oct’14

Nov’14–

Jan’15

27

22

34

25

21 22

43

39

19

26

Industry, regulatory or geography changes

Financial condition

Acquisition or geographical expansion

Leadership change

Restructuring

Feb’15–

Apr’15

Section 2

Industry specific analysis

DESIGN • TRANSFORM • RUN 14 © 2015 Copyright Genpact. All Rights Reserved.

Industry comparison ► Historical trends (Feb’13–Apr’15)

Sharp differences in trend across industries; volatility and adaptation picks ups in life sciences, CPG and banking

100

80

120

60

40

20

ALL INDUSTRIES

Feb’13–Apr‘15

Vo

lati

lity

an

d A

dap

tati

on

In

dex

Feb’13–

Apr‘13

May’13–

Jul'13

Aug’13–

Oct‘13

Nov’13–

Jan‘14

Feb’14–

Apr‘14

May’14–

Jul’14

Aug’14–

Oct’14

Nov’14–

Jan’15

Capital markets

Retail banking

Commercial banking

Healthcare

Consumer goods

Manufacturing

Life sciences

Insurance

High tech

Feb’15–

Apr’15

DESIGN • TRANSFORM • RUN 15 © 2015 Copyright Genpact. All Rights Reserved.

60

40

20

High tech

Capital markets

Manufacturing

Healthcare

Consumer goods

Life sciences

Insurance

Commercial banking

Retail banking

Industry comparison ► Historical trends (Feb’13–Apr’15) ► Volatility & Adaptation

Splitting VAI in its components shows increasing volatility in banking and capital markets; adaptation rises in life sciences

ALL INDUSTRIES

Feb’13–Apr‘15 Volatility events Adaptation responses

Feb’14-

Jan’15

Feb’15-

Apr’15

Feb’13-

Jan’14 Feb’14-

Jan’15

Feb’15-

Apr’15

Feb’13-

Jan’14

Vo

lati

lity

an

d A

dap

tati

on

In

dex

Retail banking, commercial

banking, capital markets

and CPG show sharp

increase in volatility

Life sciences shows

highest increase in

adaptation

DESIGN • TRANSFORM • RUN 16 © 2015 Copyright Genpact. All Rights Reserved.

0

5

10

15

20

25

30

35

Capital markets

High tech

Manufacturing

Healthcare

Consumer goods

Life sciences

Insurance

Commercial banking

Retail banking

Industry comparison ► Historical trends (Feb’13–Apr’15) ► Financial conditions

Increasing financial pressures in commercial and retail banking, capital markets and CPG in the last 3 months

ALL INDUSTRIES

Feb’13–Apr‘15

Feb’14-

Jan’15

Feb’15-

Apr’15

Feb’13-

Jan’14

Vo

lati

lity

an

d A

dap

tati

on

In

dex

(Fin

an

cia

l co

nd

itio

n c

om

po

nen

t)

DESIGN • TRANSFORM • RUN 17 © 2015 Copyright Genpact. All Rights Reserved.

Industry comparison ► Feb’15–Apr‘15

2726

2

91015

55

646569

79

Insu

rance

Vo

lati

lity

an

d A

da

pta

tio

n I

nd

ex

All

Ind

ustr

ies

Ma

y’1

4-A

pr’

15

All

Ind

ustr

ies

Fe

b’1

5–A

pr’

15

Re

tail

ba

nkin

g

He

alth

ca

re

Life

scie

nce

s

Ma

nu

factu

rin

g

Ca

pita

l m

ark

ets

Co

mm

erc

ial b

an

kin

g

Co

nsu

me

r g

oo

ds

Hig

h te

ch

Highest levels of volatility and adaptation in retail banking, followed by life sciences

Feb’15-Apr'15

Retail banking showed highest volatility and

adaptation index between Feb’15-Apr’15 (explained

by leadership change, financial conditions and M&A)

DESIGN • TRANSFORM • RUN 18 © 2015 Copyright Genpact. All Rights Reserved.

Retail Banking

Industry comparison ► Feb’15–Apr‘15

Retail banking and life sciences show most volatility and adaptation; leadership change main trigger across industries

Commercial

Banking

Life sciences

Overall

Index

Number of

events

% of

companies

impacted Main volatility themes

1. Financial condition

2. Restructuring

3. Acquisition or geographic

expansion

1. Leadership change

2. Acquisition or geographic

expansion

3. Regulatory changes

1. Financial conditions

2. Acquisition or geographic

expansion

3. Leadership change

Feb'15-Apr'15

DESIGN • TRANSFORM • RUN 19 © 2015 Copyright Genpact. All Rights Reserved.

Industry comparison ► Feb’15–Apr‘15

Fewer events observed in high tech and manufacturing in the last quarter; more in banking and life sciences

% of

companies

impacted

Avg.

number of

volatility events

per company

Life sciences, Consumer goods

High tech, Manufacturing

Life sciences, Consumer goods

High tech, Manufacturing

Acquisition or expansion

Leadership changes

Financial conditions

Vo

lati

lity

an

d A

dap

tati

on

In

de

x

% delta from last 12 months average

0

10

20

30

40

50

60

70

80

-100 -50 0 50 100

Manufacturing

Life sciences

Insurance

High tech

Healthcare

Capital markets

Consumer goods

Commercial banking

Retail banking

Feb'15-Apr'15

DESIGN • TRANSFORM • RUN 20 © 2015 Copyright Genpact. All Rights Reserved.

Almost 50% of companies reported at least one volatility or adaptation events in the last quarter

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90

1.0

3.0

2.5

2.0

1.5

0.5

Trailing 12 months

Healthcare

Consumer goods

High tech

Avera

ge n

um

ber

of vola

tilit

y e

vents

per

com

pany

% of companies impacted

Retail banking

Life sciences

Insurance

Commercial banking

Overall - Last 3 months

Capital markets

Manufacturing

Feb’15-Apr’15

Industry comparison ► Feb’15–Apr‘15

DESIGN • TRANSFORM • RUN 21 © 2015 Copyright Genpact. All Rights Reserved.

H L

H

# o

f ev

en

ts p

er

co

mp

an

y

% companies impacted

Industry analysis summary ► Trailing 12 months (May’14–Apr’15)

Determinants of volatility and adaptation vary widely by industry

Retail banking Commercial banking Insurance Consumer goods Capital markets

Life sciences Manufacturing High tech

Adaptation responses

A R L Restructuring/

Cost cutting

Acquisitions or

geo expansion

Leadership

changes

Volatility events

F I Financial

pressures

Industry, regulatory or

geography changes

A

L

R I

F

A

L

R

I

F

A L

R I

F

A

L

R I

F A

L

R

I

F

A L

R

I

F A

L

R I

F

A

L

R

I

F

A

L

R

I

F

May'14-Apr'15

Healthcare

DESIGN • TRANSFORM • RUN 22 © 2015 Copyright Genpact. All Rights Reserved.

Industry analysis ► Retail banking ► Feb’15–Apr‘15

Volatility and adaptation index - Retail banking Last 3 months (Feb’15-Apr’15) vs. trailing 12 months (May’14-Apr’15)

Increase in financial stress

29%

Trailing 12

months*

.

Last 3

months#

25%

Decrease in leadership churn

0.40.3

Trailing 12

months*

Last 3

months#

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Last 3

months#

16%

Trailing 12

months*

29% 0.3

0.6

Trailing 12

months*

Last 3

months#

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Ad

ap

tatio

n

Vo

latilit

y

Last 3 Months#

78.8

Trailing 12

months*

69.8

Industry, Regulatory or Geography Changes

Financial Condition

Acquisition or Geographical Expansion

Leadership Change

Restructuring

Vo

latilit

y a

nd

Ad

ap

tatio

n In

de

x

*Data covering May1, 2014 to April 30, 2015 #Data covering Feb 1, 2015 to April 30, 2015

DESIGN • TRANSFORM • RUN 23 © 2015 Copyright Genpact. All Rights Reserved.

Industry analysis ► Commercial banking ► Feb’15–Apr‘15

Volatility and adaptation index - Commercial banking Last 3 months (Feb’15-Apr’15) vs. trailing 12 months (May’14-Apr’15)

Leadership churn decreases

Last 3

months#

16%

Trailing 12

months*

29%

M&A activity picks up

0.0

0.1

Last 3

months#

Trailing 12

months*

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Trailing 12

months*

17%

Last 3

months#

29% 0.30.2

Last 3

months#

Trailing 12

months*

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Ad

ap

tatio

n

Vo

latilit

y

Last 3 Months#

65.0

Trailing 12

months*

50.2

Industry, Regulatory or Geography Changes

Financial Condition

Acquisition or Geographical Expansion

Leadership Change

Restructuring

Vo

latilit

y a

nd

Ad

ap

tatio

n In

de

x

*Data covering May1, 2014 to April 30, 2015 #Data covering Feb 1, 2015 to April 30, 2015

DESIGN • TRANSFORM • RUN 24 © 2015 Copyright Genpact. All Rights Reserved.

Industry analysis ► Capital markets ► Feb’15–Apr‘15

Volatility and adaptation index - Capital markets Last 3 months (Feb’15-Apr’15) vs. trailing 12 months (May’14-Apr’15)

Decrease in leadership churn

Last 3

months#

17%

Trailing 12

months*

27%

Financial stress increases

0.30.6

Last 3

months#

Trailing 12

months*

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Last 3

months#

27%

Trailing 12

months*

24% 0.40.4

Trailing 12

months*

Last 3

months#

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Ad

ap

tatio

n

Vo

latilit

y

55.8

Trailing 12

months*

55.1

Last 3 Months#

Restructuring

Leadership Change

Acquisition or Geographical Expansion

Financial Condition

Industry, Regulatory or Geography Changes

Vo

latilit

y a

nd

Ad

ap

tatio

n In

de

x

*Data covering May1, 2014 to April 30, 2015 #Data covering Feb 1, 2015 to April 30, 2015

DESIGN • TRANSFORM • RUN 25 © 2015 Copyright Genpact. All Rights Reserved.

Industry analysis ► Insurance ► Feb’15–Apr‘15

Volatility and adaptation index – Insurance Last 3 months (Feb’15-Apr’15) vs. trailing 12 months (May’14-Apr’15)

Increase in financial stress

Last 3

months#

10%

Trailing 12

months*

5%

M&A activity picks pace

0.00.1

Last 3

months#

Trailing 12

months*

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Last 3

months#

11%

Trailing 12

months*

9% 0.10.1

Last 3

months#

Trailing 12

months*

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Ad

ap

tatio

n

Vo

latilit

y

Last 3 Months#

8.9

Trailing 12

months*

5.5

Industry, Regulatory or Geography Changes

Financial Condition

Acquisition or Geographical Expansion

Leadership Change

Restructuring

Vo

latilit

y a

nd

Ad

ap

tatio

n In

de

x

*Data covering May1, 2014 to April 30, 2015 #Data covering Feb 1, 2015 to April 30, 2015

DESIGN • TRANSFORM • RUN 26 © 2015 Copyright Genpact. All Rights Reserved.

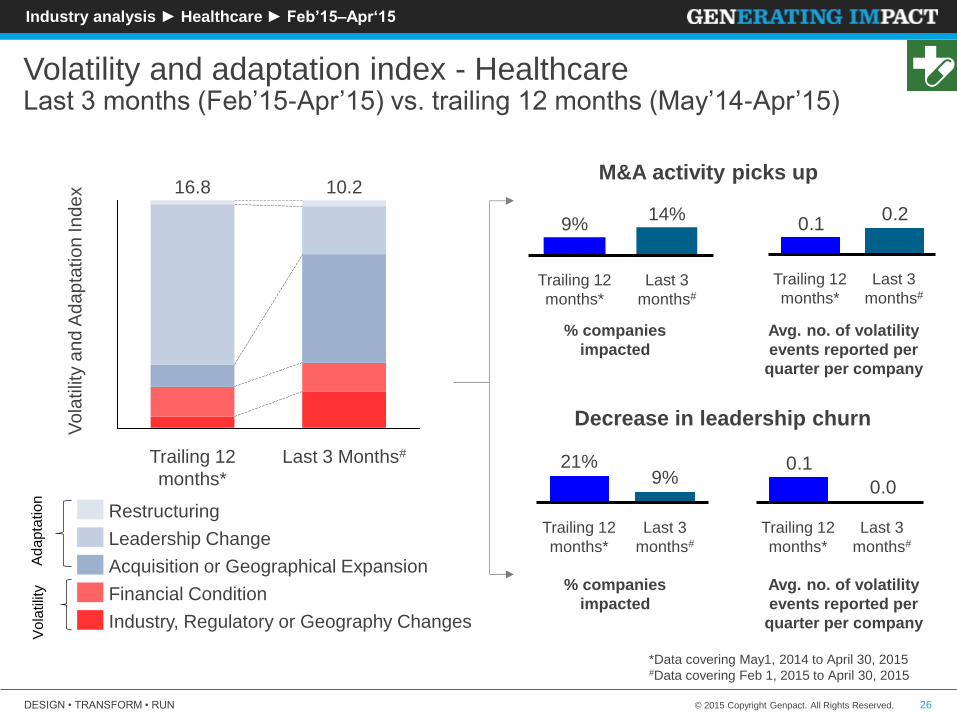

Industry analysis ► Healthcare ► Feb’15–Apr‘15

Volatility and adaptation index - Healthcare Last 3 months (Feb’15-Apr’15) vs. trailing 12 months (May’14-Apr’15)

M&A activity picks up

Last 3

months#

14%

Trailing 12

months*

9%

Decrease in leadership churn

0.20.1

Last 3

months#

Trailing 12

months*

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Last 3

months#

9%

Trailing 12

months*

21%

0.0

0.1

Last 3

months#

Trailing 12

months*

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Ad

ap

tatio

n

Vo

latilit

y

Last 3 Months#

10.2

Trailing 12

months*

16.8

Industry, Regulatory or Geography Changes

Financial Condition

Acquisition or Geographical Expansion

Leadership Change

Restructuring

Vo

latilit

y a

nd

Ad

ap

tatio

n In

de

x

*Data covering May1, 2014 to April 30, 2015 #Data covering Feb 1, 2015 to April 30, 2015

DESIGN • TRANSFORM • RUN 27 © 2015 Copyright Genpact. All Rights Reserved.

Industry analysis ► Life sciences ► Feb’15–Apr‘15

Volatility and adaptation index - Life sciences Last 3 months (Feb’15-Apr’15) vs. trailing 12 months (May’14-Apr’15)

Increase in regulatory changes

Last 3

months#

21%

Trailing 12

months*

6%

Increase in leadership churn

0.30.1

Last 3

months#

Trailing 12

months*

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Last 3

months#

38%

Trailing 12

months*

16% 0.30.2

Last 3

months#

Trailing 12

months*

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Ad

ap

tatio

n

Vo

latilit

y

Last 3 Months#

68.8

Trailing 12

months*

35.3

Industry, Regulatory or Geography Changes

Financial Condition

Acquisition or Geographical Expansion

Leadership Change

Restructuring

Vo

latilit

y a

nd

Ad

ap

tatio

n In

de

x

*Data covering May1, 2014 to April 30, 2015 #Data covering Feb 1, 2015 to April 30, 2015

DESIGN • TRANSFORM • RUN 28 © 2015 Copyright Genpact. All Rights Reserved.

Industry analysis ► Consumer Goods ► Feb’15–Apr‘15

Volatility and adaptation index – Consumer goods Last 3 months (Feb’15-Apr’15) vs. trailing 12 months (May’14-Apr’15)

M&A activity picks up

Last 3

months#

37%

Trailing 12

months*

23%

Financial stress increases

0.50.3

Last 3

months#

Trailing 12

months*

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Last 3

months#

37%

Trailing 12

months*

23% 0.5

0.3

Last 3

months#

Trailing 12

months*

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Ad

ap

tatio

n

Vo

latilit

y

Last 3 Months#

64.4

Trailing 12

months*

42.7

Industry, Regulatory or Geography Changes

Financial Condition

Acquisition or Geographical Expansion

Leadership Change

Restructuring

Vo

latilit

y a

nd

Ad

ap

tatio

n In

de

x

*Data covering May1, 2014 to April 30, 2015 #Data covering Feb 1, 2015 to April 30, 2015

DESIGN • TRANSFORM • RUN 29 © 2015 Copyright Genpact. All Rights Reserved.

Industry analysis ► Manufacturing ► Feb’15–Apr‘15

Volatility and adaptation index - Manufacturing Last 3 months (Feb’15-Apr’15) vs. trailing 12 months (May’14-Apr’15)

M&A activity slightly up

Last 3

months#

13%

Trailing 12

months*

9%

Decrease in leadership churn

0.20.1

Last 3

months#

Trailing 12

months*

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Last 3

months#

13%

Trailing 12

months*

19% 0.1

0.3

Last 3

months#

Trailing 12

months*

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Ad

ap

tatio

n

Vo

latilit

y

Last 3 Months#

14.7

Trailing 12

months*

18.8

Industry, Regulatory or Geography Changes

Financial Condition

Acquisition or Geographical Expansion

Leadership Change

Restructuring

Vo

latilit

y a

nd

Ad

ap

tatio

n In

de

x

*Data covering May1, 2014 to April 30, 2015 #Data covering Feb 1, 2015 to April 30, 2015

DESIGN • TRANSFORM • RUN 30 © 2015 Copyright Genpact. All Rights Reserved.

Industry analysis ► High tech ► Feb’15–Apr‘15

Volatility and adaptation index - High tech Last 3 months (Feb’15-Apr’15) vs. trailing 12 months (May’14-Apr’15)

Financial stress increases

2%

Trailing 12

months*

4%

Last 3

months#

Increase in regulatory changes

0.10.0

Trailing 12

months*

Last 3

months#

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

1%

Trailing 12

months*

4%

Last 3

months#

0.10.0

Trailing 12

months*

Last 3

months#

% companies

impacted

Avg. no. of volatility

events reported per

quarter per company

Ad

ap

tatio

n

Vo

latilit

y

Vo

latilit

y a

nd

Ad

ap

tatio

n In

de

x 3.4

Trailing 12

months*

2.2

Last 3 Months#

Restructuring

Leadership Change

Acquisition or Geographical Expansion

Financial Condition

Industry, Regulatory or Geography Changes

*Data covering May1, 2014 to April 30, 2015 #Data covering Feb 1, 2015 to April 30, 2015

DESIGN • TRANSFORM • RUN 31 © 2015 Copyright Genpact. All Rights Reserved.

About Genpact

Genpact (NYSE: G) stands for “generating business impact.” We design, transform, and run intelligent business operations including those that are complex

and specific to a set of chosen industries. The result is advanced operating models that support growth and manage cost, risk, and compliance across a

range of functions such as finance and procurement, financial services account servicing, claims management, regulatory affairs, and industrial asset

optimization. Our Smart Enterprise Processes (SEPSM) proprietary framework helps companies reimagine how they operate by integrating effective

Systems of EngagementTM, core IT, and Data-to-Action AnalyticsSM. Our hundreds of long-term clients include more than one-fourth of the Fortune Global

500. We have grown to over 68,000 people in 25 countries with key management and a corporate office in New York City. Behind our passion for process

and operational excellence is the Lean and Six Sigma heritage of a former General Electric division that has served GE businesses for more than 16 years.

For more information, visit www.genpact.com.

Follow Genpact on Twitter, Facebook, LinkedIn, and YouTube.

© 2015 Copyright Genpact. All Rights Reserved.

Genpact Research Institute

The Genpact Research Institute is a

specialized think tank harnessing the

collective intelligence of Genpact – as

the leading business process service

provider worldwide - its ecosystem of

clients and partners, and thousands of

process operations experts. Its

mission is to advance the “art of the

possible” in our clients’ journey of

business transformation and adoption

of advanced operating models.

www.genpact.com/research-institute

www.genpact.com/home/volatility-adaptation-index

www.genpact.com

Thank You

![Trading Strategy with Stochastic Volatility in a Limit Order ...arXiv:1602.00358v1 [q-fin.TR] 1 Feb 2016 Trading Strategy with Stochastic Volatility in a Limit Order Book Market Wai-Ki](https://img.pdfslide.us/doc/110x75/5fac60723d15eb669b515c71/trading-strategy-with-stochastic-volatility-in-a-limit-order-arxiv160200358v1.jpg)