Embed Size (px)

Citation preview

27th Aug, 2010

Indian Software Product Markets,

VAS Offerings: Some Insights

This presentation is based on both publicly available data and interviews of key players in the

industry. Browne & Mohan takes no responsibility for any incorrect information supplied to us

by ISV, product vendors or users.

Browne & Mohan reports are limited publications containing valuable insights for CEO, policy

makers and analysts. Academic institutions (including Open Universities in UK and others) are

restricted from distributing this presentation as background material for any course work

without formal approval. Furthermore, no part may be reproduced, stored in a retrieval system,

or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or

otherwise, without the permission of Browne & Mohan.

Disclaimer

© Browne & Mohan, 2009

1

2 Indian Software Industry

3 VAS Product companies

Background

Content

4 Conclusions

Background

India has emerged as a major player in software services and

development. Most of the world‟s leading software companies have

established their subsidiaries and R&D centers in the country.

From self-doubt and bureaucratic apathy, they have grown in revenues,

stature and acquiring companies in India and abroad.

The number of software product firms is on the rise and is expected to

contribute to the economy through increased employment generation

and intellectual wealth creation. Their multiplier effect on augmenting

industrial growth and increased entrepreneurial activities are a few of

the compelling factors that warrant a focused study of this sector.

1

1

2 Indian Software Industry

3 VAS Product companies

Background

Content

4 Conclusions

© Browne & Mohan, 2009

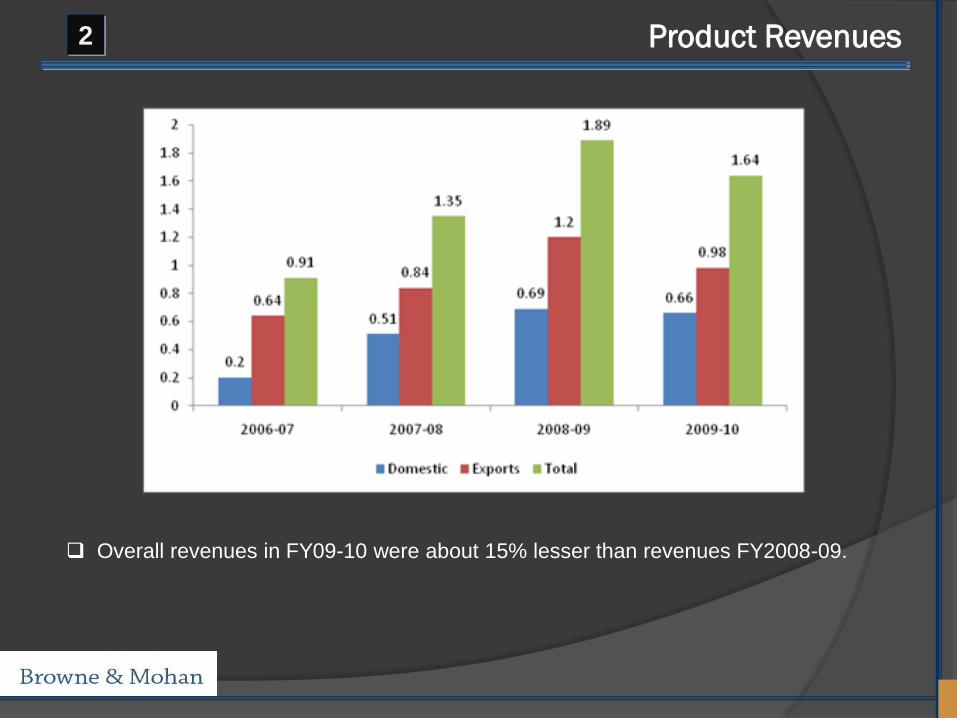

Product Revenues2

Overall revenues in FY09-10 were about 15% lesser than revenues FY2008-09.

© Browne & Mohan, 2009

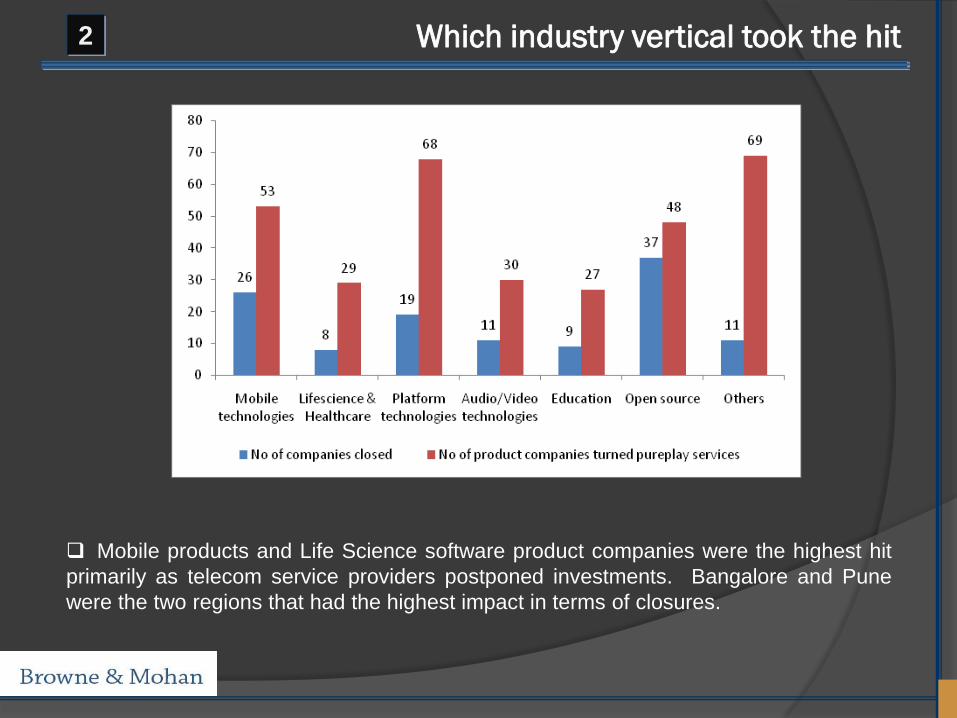

Which industry vertical took the hit2

Mobile products and Life Science software product companies were the highest hit

primarily as telecom service providers postponed investments. Bangalore and Pune

were the two regions that had the highest impact in terms of closures.

© Browne & Mohan, 2009

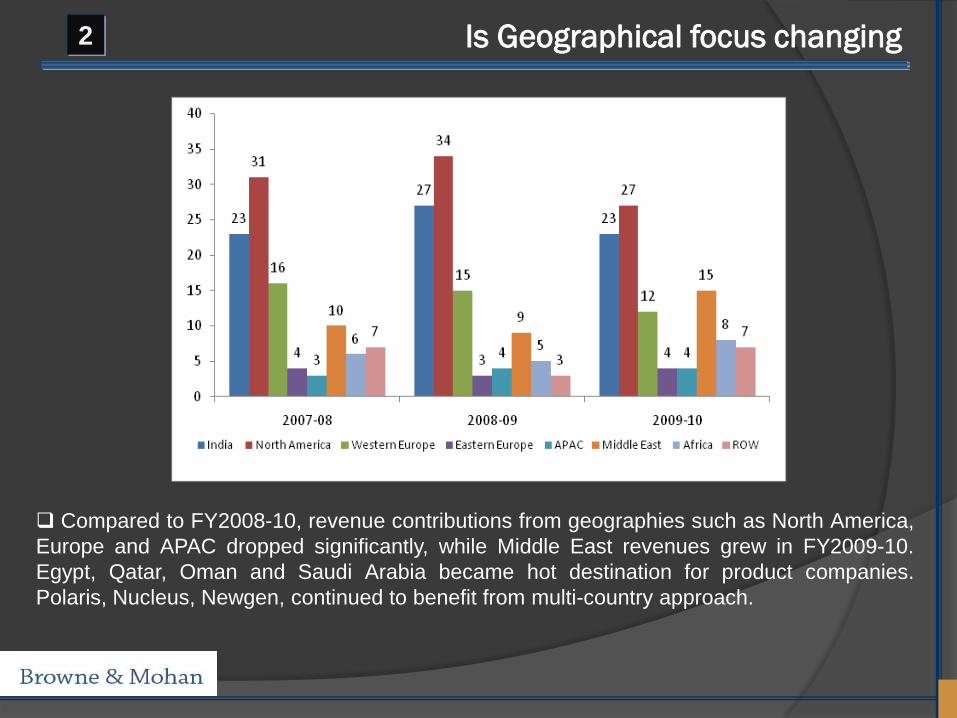

Is Geographical focus changing 2

Compared to FY2008-10, revenue contributions from geographies such as North America,

Europe and APAC dropped significantly, while Middle East revenues grew in FY2009-10.

Egypt, Qatar, Oman and Saudi Arabia became hot destination for product companies.

Polaris, Nucleus, Newgen, continued to benefit from multi-country approach.

1

2 Indian Software Industry

3 VAS Product companies

Background

Content

4 Conclusions

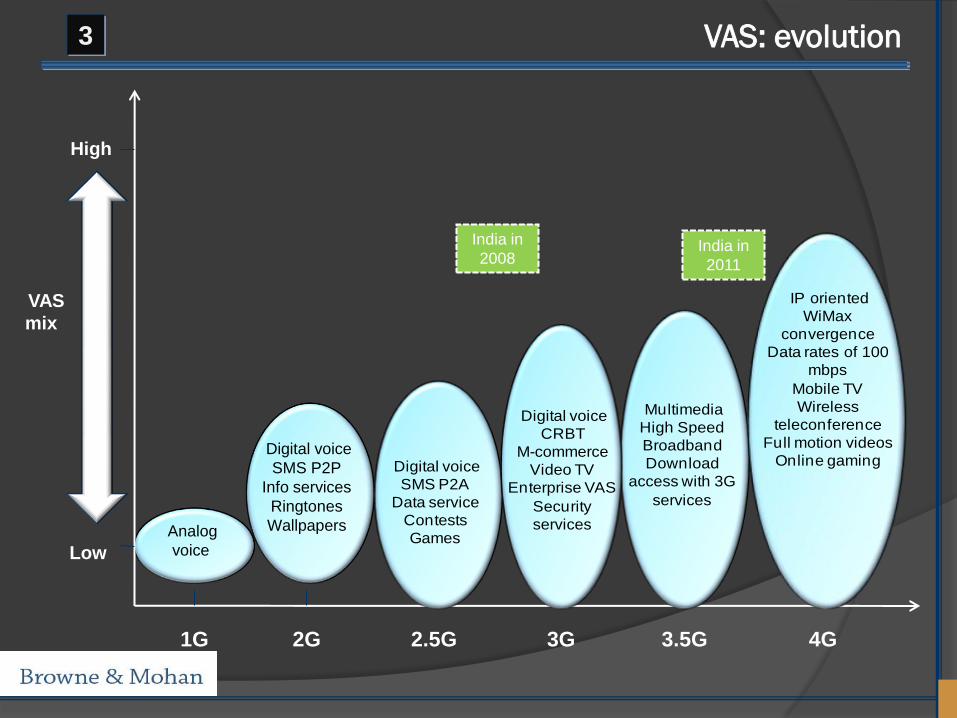

Low

Analog

voice

Digital voice

SMS P2P

Info services

Ringtones

Wallpapers

1G 2G 2.5G 3G 3.5G 4G

India in

2008

High

VAS

mix

India in

2011

Digital voice

SMS P2A

Data service

Contests

Games

Digital voice

CRBT

M-commerce

Video TV

Enterprise VAS

Security

services

Multimedia

High Speed

Broadband

Download

access with 3G

services

IP oriented

WiMax

convergence

Data rates of 100

mbps

Mobile TV

Wireless

teleconference

Full motion videos

Online gaming

VAS: evolution3

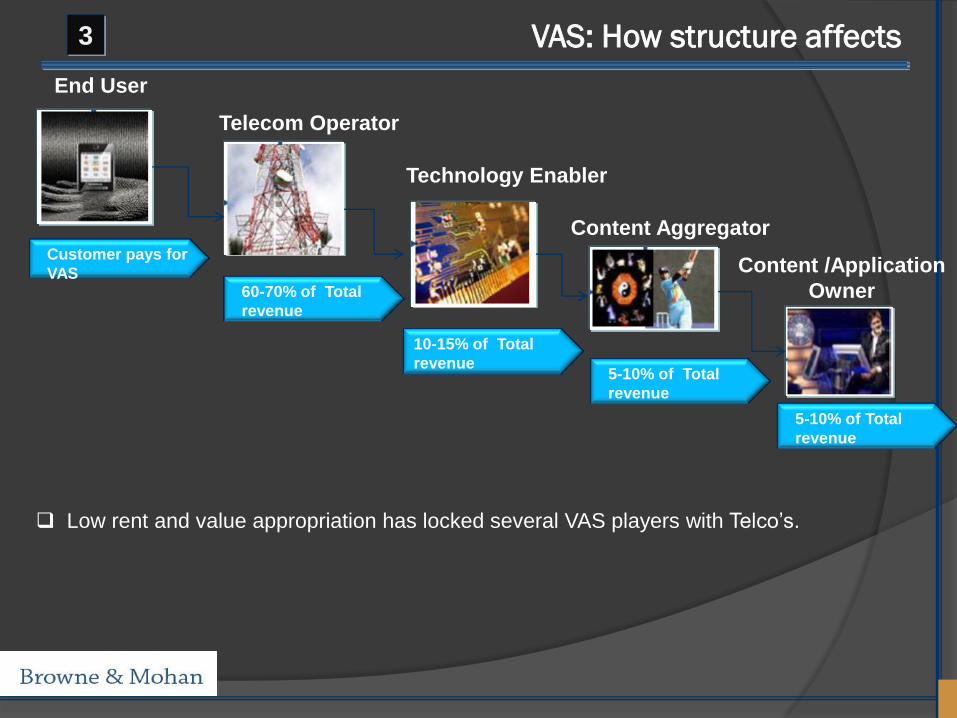

Customer pays for

VAS

Telecom Operator

Technology Enabler

Content Aggregator

Content /Application

Owner60-70% of Total

revenue

10-15% of Total

revenue5-10% of Total

revenue

5-10% of Total

revenue

End User

VAS: How structure affects 3

Low rent and value appropriation has locked several VAS players with Telco‟s.

© Browne & Mohan, 2009

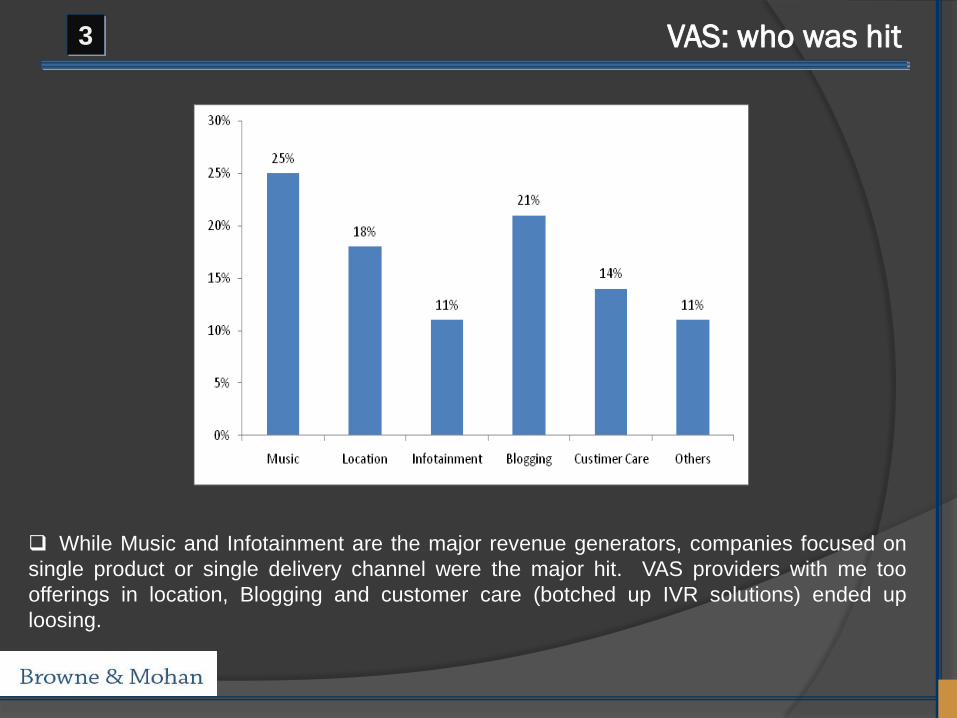

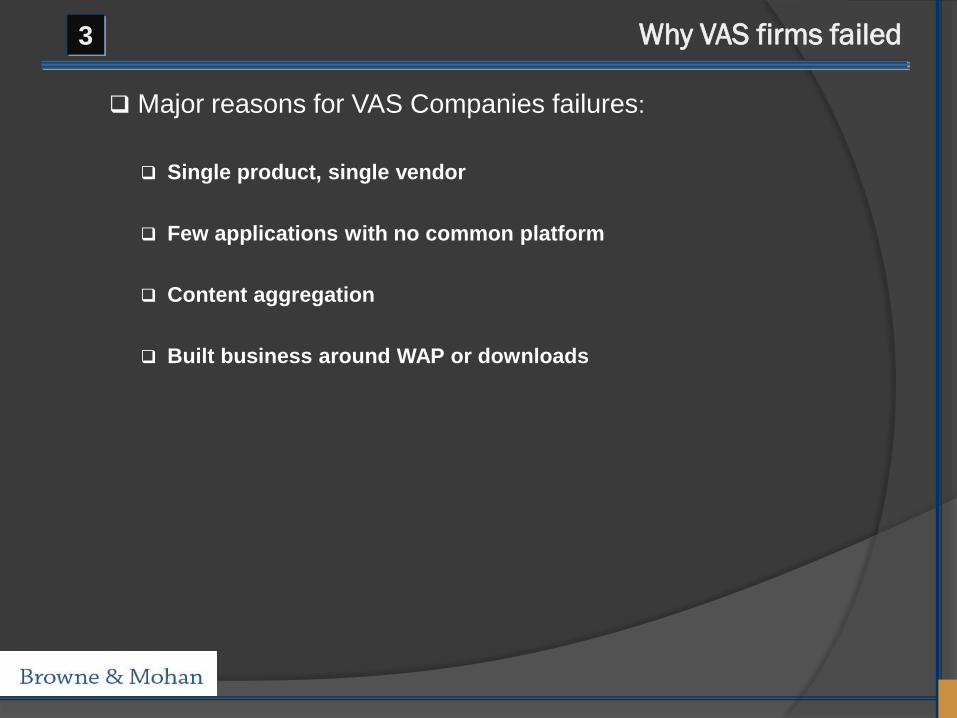

VAS: who was hit3

While Music and Infotainment are the major revenue generators, companies focused on

single product or single delivery channel were the major hit. VAS providers with me too

offerings in location, Blogging and customer care (botched up IVR solutions) ended up

loosing.

Major reasons for VAS Companies failures:

Single product, single vendor

Few applications with no common platform

Content aggregation

Built business around WAP or downloads

Why VAS firms failed3

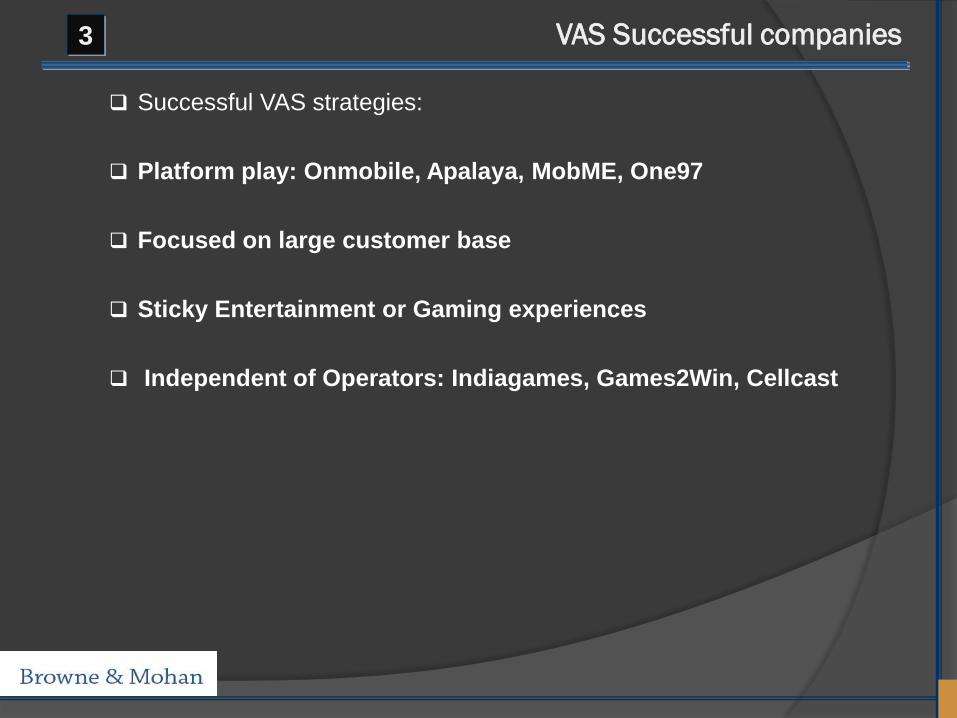

Successful VAS strategies:

Platform play: Onmobile, Apalaya, MobME, One97

Focused on large customer base

Sticky Entertainment or Gaming experiences

Independent of Operators: Indiagames, Games2Win, Cellcast

VAS Successful companies3

1

2 Indian Software Industry

3 VAS Product companies

Background

Content

4 Conclusions

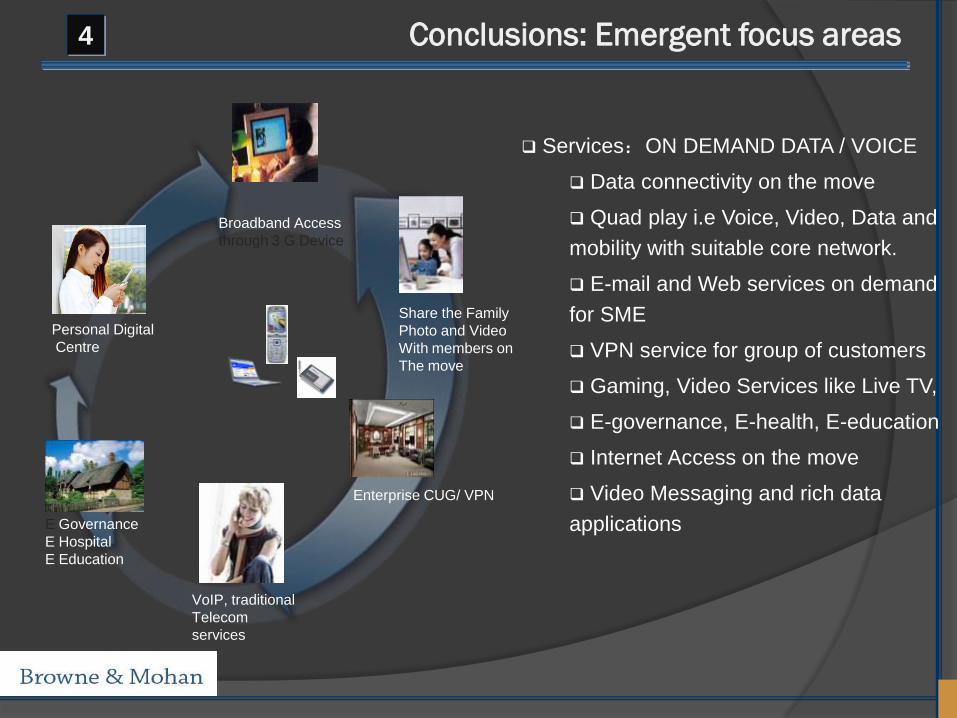

Services:ON DEMAND DATA / VOICE

Data connectivity on the move

Quad play i.e Voice, Video, Data and

mobility with suitable core network.

E-mail and Web services on demand

for SME

VPN service for group of customers

Gaming, Video Services like Live TV,

E-governance, E-health, E-education

Internet Access on the move

Video Messaging and rich data

applications

Personal Digital

Centre

Broadband Access

through 3 G Device

Share the Family

Photo and Video

With members on

The move

E Governance

E Hospital

E Education

VoIP, traditional

Telecom

services

Enterprise CUG/ VPN

4 Conclusions: Emergent focus areas

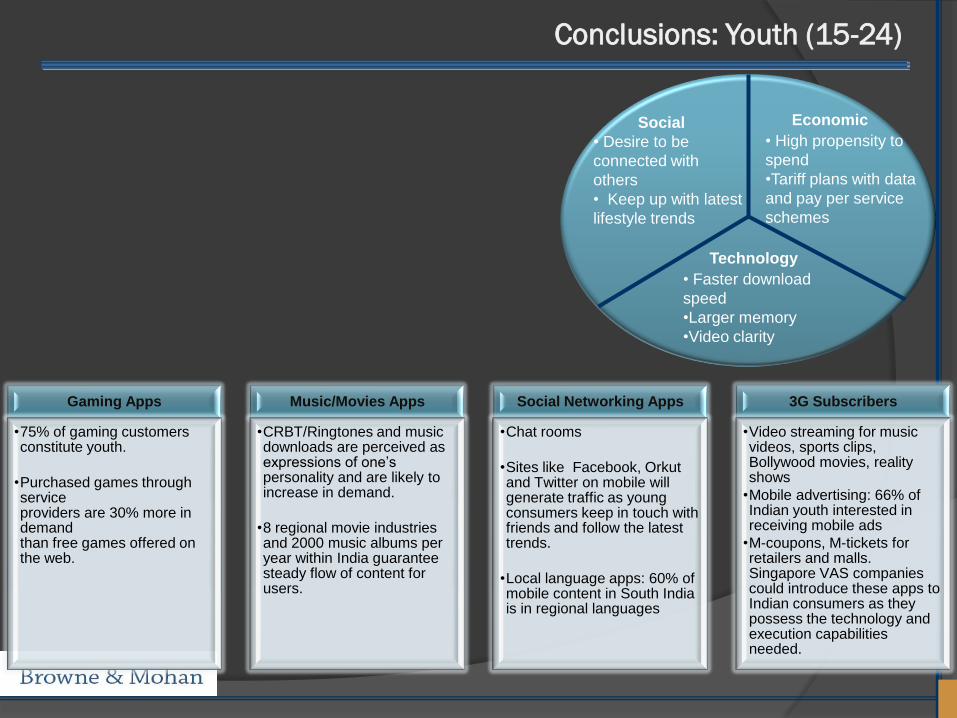

Gaming Apps

•75% of gaming customers constitute youth.

•Purchased games through service providers are 30% more in demand than free games offered on the web.

Music/Movies Apps

•CRBT/Ringtones and music downloads are perceived as expressions of one‟s personality and are likely to increase in demand.

•8 regional movie industries and 2000 music albums per year within India guarantee steady flow of content for users.

Social Networking Apps

•Chat rooms

•Sites like Facebook, Orkutand Twitter on mobile will generate traffic as young consumers keep in touch with friends and follow the latest trends.

•Local language apps: 60% of mobile content in South India is in regional languages

3G Subscribers

•Video streaming for music videos, sports clips, Bollywood movies, reality shows

•Mobile advertising: 66% of Indian youth interested in receiving mobile ads

•M-coupons, M-tickets for retailers and malls. Singapore VAS companies could introduce these apps to Indian consumers as they possess the technology and execution capabilities needed.

Technology

• Faster download

speed

•Larger memory

•Video clarity

Social

• Desire to be

connected with

others

• Keep up with latest

lifestyle trends

Economic

• High propensity to

spend

•Tariff plans with data

and pay per service

schemes

Conclusions: Youth (15-24)

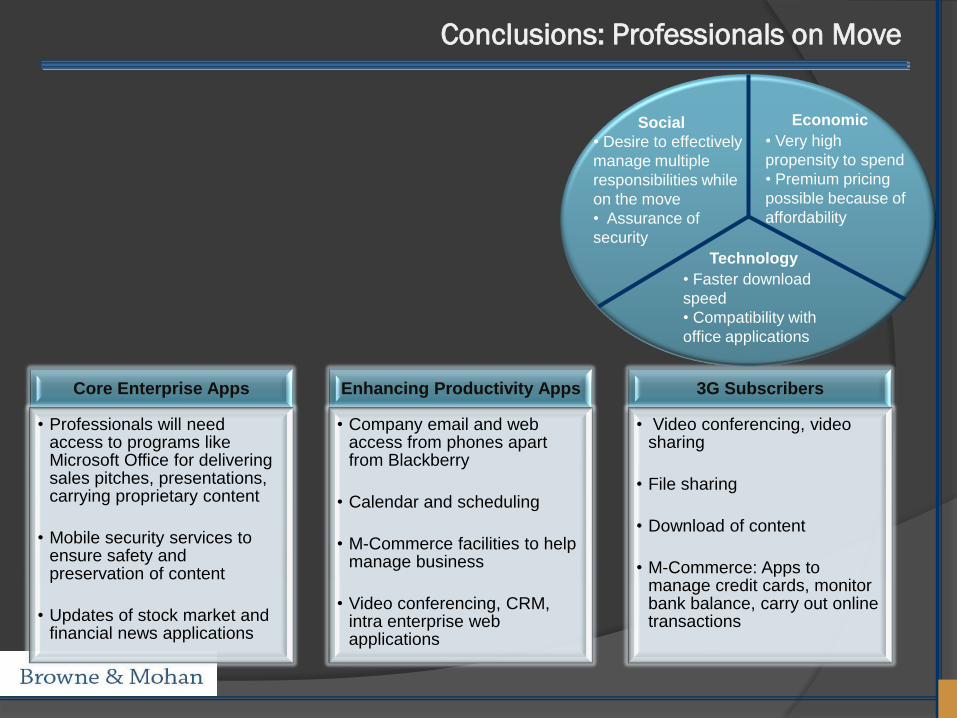

Core Enterprise Apps

• Professionals will need access to programs like Microsoft Office for delivering sales pitches, presentations, carrying proprietary content

• Mobile security services to ensure safety and preservation of content

• Updates of stock market and financial news applications

Enhancing Productivity Apps

• Company email and web access from phones apart from Blackberry

• Calendar and scheduling

• M-Commerce facilities to help manage business

• Video conferencing, CRM, intra enterprise web applications

3G Subscribers

• Video conferencing, video sharing

• File sharing

• Download of content

• M-Commerce: Apps to manage credit cards, monitor bank balance, carry out online transactions

Social Economic

TechnologyTechnology

• Faster download

speed

• Compatibility with

office applications

Social

• Desire to effectively

manage multiple

responsibilities while

on the move

• Assurance of

security

Economic

• Very high

propensity to spend

• Premium pricing

possible because of

affordability

Conclusions: Professionals on Move

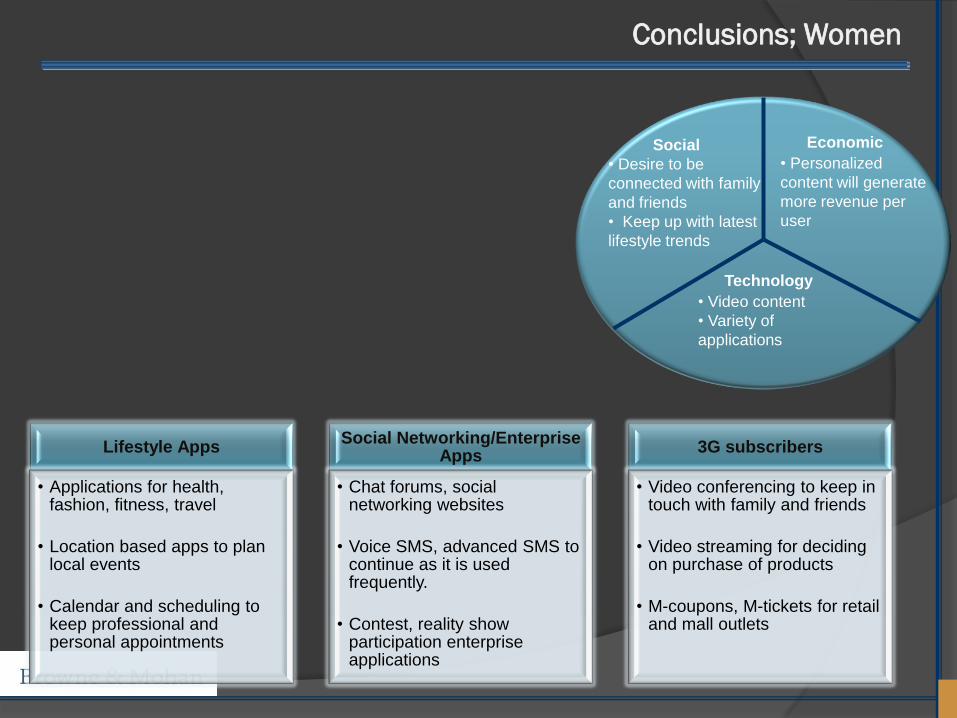

Lifestyle Apps

• Applications for health, fashion, fitness, travel

• Location based apps to plan local events

• Calendar and scheduling to keep professional and personal appointments

Social Networking/Enterprise Apps

• Chat forums, social networking websites

• Voice SMS, advanced SMS to continue as it is used frequently.

• Contest, reality show participation enterprise applications

3G subscribers

• Video conferencing to keep in touch with family and friends

• Video streaming for deciding on purchase of products

• M-coupons, M-tickets for retail and mall outlets

Technology

• Video content

• Variety of

applications

Social

• Desire to be

connected with family

and friends

• Keep up with latest

lifestyle trends

Economic

• Personalized

content will generate

more revenue per

user

Conclusions; Women

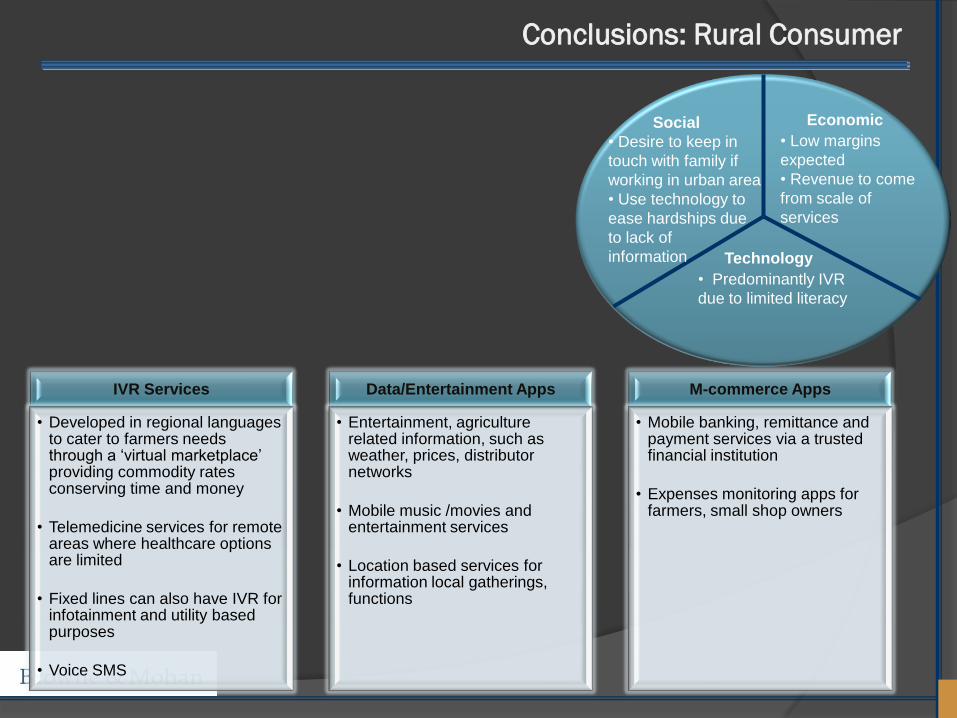

IVR Services

• Developed in regional languages to cater to farmers needs through a „virtual marketplace‟ providing commodity rates conserving time and money

• Telemedicine services for remote areas where healthcare options are limited

• Fixed lines can also have IVR for infotainment and utility based purposes

• Voice SMS

Data/Entertainment Apps

• Entertainment, agriculture related information, such as weather, prices, distributor networks

• Mobile music /movies and entertainment services

• Location based services for information local gatherings, functions

M-commerce Apps

• Mobile banking, remittance and payment services via a trusted financial institution

• Expenses monitoring apps for farmers, small shop owners

Technology

• Predominantly IVR

due to limited literacy

Social

• Desire to keep in

touch with family if

working in urban area

• Use technology to

ease hardships due

to lack of

information

Economic

• Low margins

expected

• Revenue to come

from scale of

services

Conclusions: Rural Consumer

Consumer segments in India that are likely to demand an increase in VAS are:

Youth (ages 15-34)

gaming, music/movies, social networking, 3G services

Professionals on-the-move

core enterprise VAS, M-commerce, 3G services, productivity apps

Women

lifestyle VAS, social networking, 3G services

Rural subscribers

IVR, data services, entertainment and M-commerce

The most applicable VAS capabilities that can be leveraged in the Indian market to fit

the needs of these consumer segments are:

3G services

M-commerce applications

Entertainment/Enterprise VAS

Mobile Security Services

© Browne & Mohan, 2009 21

Conclusions: Product Focus

Thank You

For any query please contact

Ms Harmeet Kaur

Associate Consultant

157/A, 2nd Floor, 10th A Main

Jayanagar 1 Block

Bangalore. 560 01

91-80-26565164

9.1

References Adachi F. Wireless Past and Future- Evolving Mobile Communication Systems. IECE Trans. Fundamentals.

2001; E84(A): 55-60.

Annual Report 2007-08. Telecom Regulatory Authority of India. October 2008.

Boston Analytics. A Study of the Mobile Value Added Services (MVAS) Market in India. 2007.

Chitkara N. Market Entry Strategy for Indian Telecom Market As Mobile Virtual Network Operator (MVNO).

December 2007. <

http://insightory.com/view/202//market_entry_strategy_for_indian_telecom_market__:_as_mobile_virtual_network

_operator > Accessed July 24, 2009.

Economic Times. MTNL calls global telcos for 3G bids. July 16, 2009. <

http://economictimes.indiatimes.com/LATEST-NEWS/MTNL-calls-global-telcos-for-3G-

bids/articleshow/4782648.cms. > Accessed on August 17, 2009.

FICCI and BDA 3G & BWA: The Next Frontier.. January 2009.

IAMAI and eTechnology Group at IMRB. Mobile Value Added Services in India. August 2008.

Infocomm Development Authority of Singapore. Annual Survey on Infocomm Industry 2008. June 2009.

Kosnik T, Gundecha M, Bajaj K. Future of Mobile VAS in India. Stanford University & BDA. December 2007.

Livemint.com . BSNL revenue arrears. August 6, 2009. < http://www.livemint.com/2009/08/06150630/BSNL-

revenue-arrears-stand-at.html>. Accessed August 10, 2009.

© Browne & Mohan, 2009 23

9.2

References Mathew L, Mysore J, Nair V. Is the Indian Market Ready to go “Virtual” for Mobile? Diamond Management and

Technology Consultants. 2006.

Members List, Mobile Alliance. < http://mobilealliance.sg/memberlist.html>. Accessed July 25, 2009.

Medianama. Airtel mobile VAS revenues. July 27, 2008. < http://www.medianama.com/2008/07/223-airtel-mobile-vas-

revenues-at-rs-23555-crores-non-sms-57-of-vas-at-rs-13356-crores/> . Accessed on August 4, 2009.

Medianama. Rcom VAS Revenues. August 1, 2008. < http://www.medianama.com/2008/08/223-rcom-vas-revenues-at-

rs-109-crmonth-non-sms-vas-at-rs-91-crmonth-60-pc-of-data-card-market/>. Accessed August 10, 2009.

Mobile Europe. Freemium model to predominate in mobile apps. 13 May, 2009. <

http://www.mobileeurope.co.uk/news_wire/114806/'Freemium'_model_to_predominate_in_mobile_apps_with_VAS_reve

nues_reaching_$14bn_by_2014,_says_report.html>. Accessed July 31, 2009.

NDTV Profit. Bharti gears up for 3G leap. August 17, 2009. < http://profit.ndtv.com/2009/08/17233801/Bharti-gears-up-

for-a-3G-leap.html >. Accessed on August 17, 2009.

Press Release No 54. Telecom Regulatory Authority of India. June 2009. <

http://www.trai.gov.in/WriteReadData/trai/upload/PressReleases/687/pr1june09no54.pdf> Accessed July 15, 2009.

Times of India. Only 4 New Operators in 3G spectrum bid. August 19, 2009. < http://www.varindia.com/Mobility1.asp >.

Accessed August 19, 2009.

VARIndia. Indian Telcos Aggressive on Value Added Services. < http://www.varindia.com/Mobility1.asp >. Accessed

August 19, 2009.

VAS. TelecomLIVE. June 2009. < http://www.kirusa.com/press/2009/06-01-09a.pdf> Accessed July 20, 2009.

© Browne & Mohan, 2009 24