Embed Size (px)

Citation preview

#DATAVERSITY

You

r Sp

eak

ers

John LadleyPresident

IMCue Solutions@jladley

Tony ShawCEO & FounderDATAVERSITY@tonyshaw

#DATAVERSITY

• A new webinar series on the first Tuesday of each month (mostly)• Upcoming Topics:

- Data Governance- Advanced Analytics- Roles, Function and Hiring of CDOs- Risk Management- Data Business Models- New Technologies you cannot ignore

…and much more!

#DATAVERSITY

• Metrics and Measurement• John Ladley, President of IMCue

- 30 years experience. Former Meta Group Analyst- Author of two major books on EIM and Data Governance- Data Strategy, Information Risk, Organizational Structure, Analytics- Practical reputation

All content copyright 2013 IMCue Solutions LLC 0

Metrics for Information

Management

Discussion

Can data or information cost your company

or organization $$$$$?

Is there a broad economic impact of data and

information?

If you answered “yes”, show me how much?

1

Accounting reasons:

• Information is an asset

• It has a probability of generating future value

• It is distinct from financial and material

assets

• Compliance with Financial Accounting

Standards Board Statement No. 142 —

measuring intangible assets

Practical reasons:

• Information affects the organization in visible

and most likely measurable ways

• Information assets are rapidly becoming a

significant business element

Why worry about information metrics?

Objective

Leave with some new views

about measuring tools

to sell and sustain

information asset

management (IAM)

3

Presenter / co-author

John Ladley

– 35 years EIM experience in various capacities

– @jladley

Doug Laney

– Currently heads thought leadership, and

advisory services with Gartner Analytics

– Authored 100+ articles and

research pieces, and

speaks now-and-again.

– Initiated Infonomics as a

formal approach to information

management in the 1990’s

4

Agenda Terminology

Measuring Information – Information as an asset

– What is an asset

– What do you need to measure?

Measuring assets

– Metric taxonomy

– What types of metrics are there? There is a lot more to measuring than common ROI

Value, effectiveness, income statement and balance sheet

Samples

5

Terminology

Information – ALL enterprise content that can

be used to further the survival and

achievement of business goals– Data = information = content (for this discussion)

Information Asset Management

– The treatment of data, information and content as

an asset in the true, business sense

Enterprise Information Management (EIM)

– The program that executes IAM

6

Terminology

Infonomics

– The economics of information and principles of

information asset management

Doug Laney of Gartner Group

– The accounting and measuring aspect of

information asset management

John Ladley

Data Governance

– The oversight of IAM; sets rules of engagement ,

i.e. policy, roles, accountability, responsibilities for

EIM and IAM

7

What does Information Asset really mean?

Metaphor

– Example from Thomas C. Redman, Ph. D.

8

9

Real asset Goodwill is intangible, appears on the balance sheet,

and can certainly be ‘used up’

Electricity is “used,” but there is always more in the wire. We buy and sell kilowatts

Ideas can be copyrighted, bought and sold

We trade information every day for something. Do you have a Twitter™ or Facebook™ account?You are worth $101.70!

10

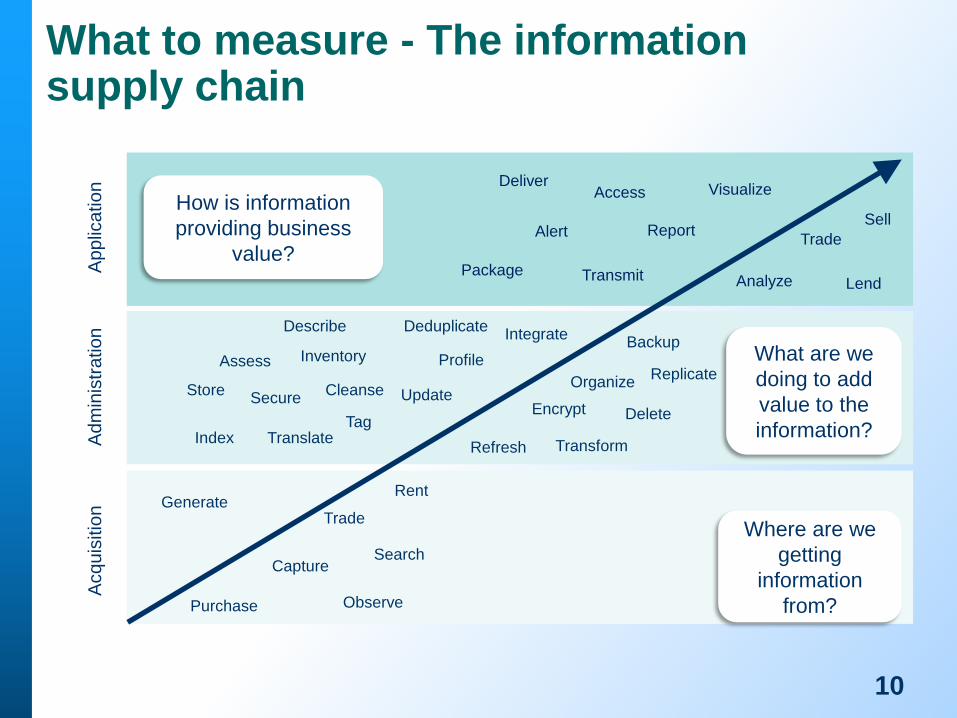

What to measure - The information supply chain

Ap

plic

atio

nA

dm

inis

tra

tio

nA

cq

uis

itio

n

How is information

providing business

value?

What are we

doing to add

value to the

information?

Where are we

getting

information

from?

Generate

Purchase

Trade

Capture

Observe

Search

Rent

StoreSecure

Assess

IndexTag

Inventory

Integrate

Organize

Encrypt

Backup

Transform

Delete

UpdateCleanse

ProfileReplicate

Describe

RefreshTranslate

Deduplicate

Package

Access

Alert

Transmit

Sell

TradeReport

Visualize

Analyze

Deliver

Lend

11

How to measure – core concept

The “algebra” of R

Where C= Create, U= Update, D = Delete, R = Read

If Value = Usage , and Usage = R, then Value = R

Therefore Information Value = R

– Then Information Costs = C + U + D

Unless information is used (read) it has no value other than the sunk cost to produce the data (transactions)

The IAM business case happens where data is used – just like “normal” assets

IAM business case: Rbenefit > Ccost + Ucost + Dcost + Rcost

How to look at information value measures

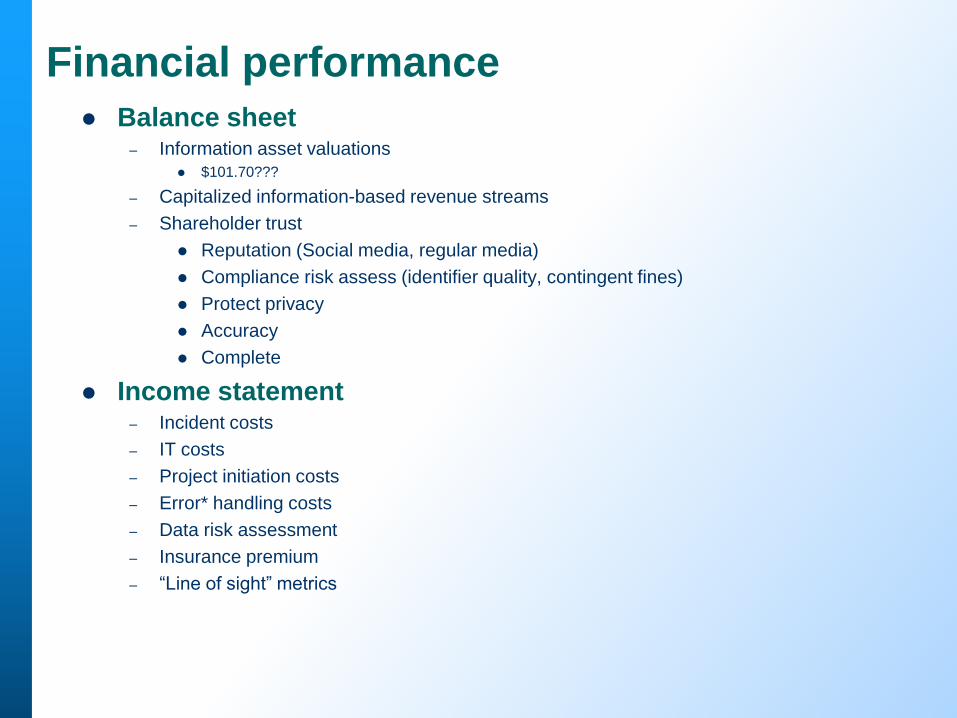

Financial performance Balance sheet

– Information asset valuations

$101.70???

– Capitalized information-based revenue streams

– Shareholder trust

Reputation (Social media, regular media)

Compliance risk assess (identifier quality, contingent fines)

Protect privacy

Accuracy

Complete

Income statement– Incident costs

– IT costs

– Project initiation costs

– Error* handling costs

– Data risk assessment

– Insurance premium

– “Line of sight” metrics

1414

Measuring program effectiveness

Efficiency

– Measure how well

governance applies its

resources

Risk

– Delta of risk

Improvement

– Amount of improvement /

delta from a “state”

15

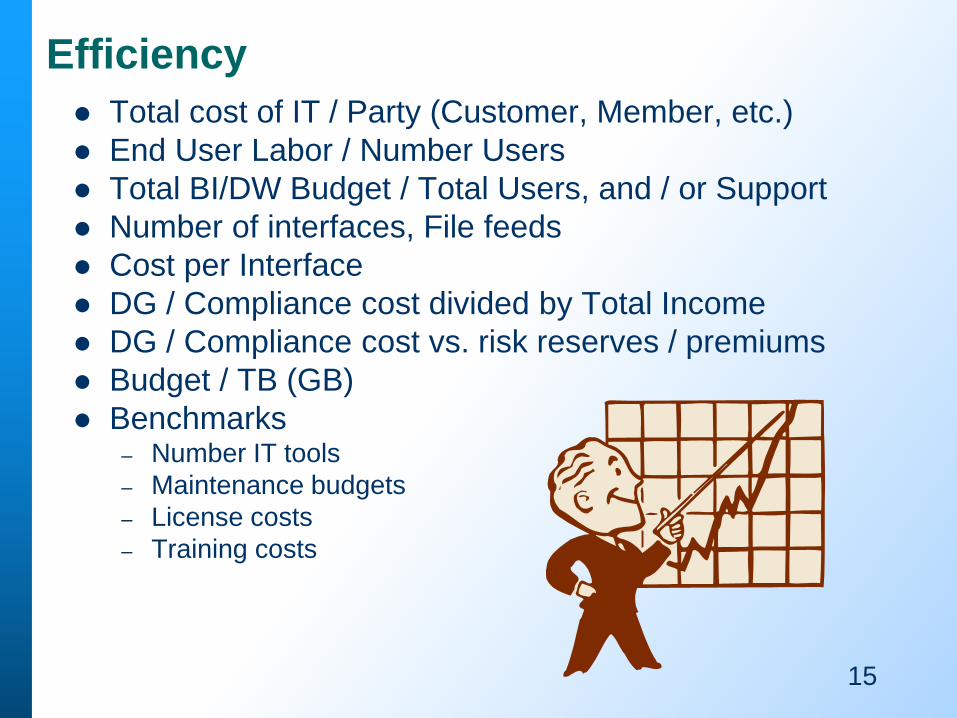

Efficiency

Total cost of IT / Party (Customer, Member, etc.)

End User Labor / Number Users

Total BI/DW Budget / Total Users, and / or Support

Number of interfaces, File feeds

Cost per Interface

DG / Compliance cost divided by Total Income

DG / Compliance cost vs. risk reserves / premiums

Budget / TB (GB)

Benchmarks – Number IT tools

– Maintenance budgets

– License costs

– Training costs

16

Risk

Threat metrics

– Cost per downtime event

– Loss of customer confidence

Financial Risk

– Liquidity

– Operational costs

– Equity / market value reduction

Data Governance Compliance

– “Hits” on web-based tools

– Access counts on repositories

Legal Compliance

– Potential penalties per subject area

– Litigation fees over time

Improvement

Operating Income by Knowledge Worker

– Operating Income for year divided by number of

Knowledge Workers

– Knowledge worker is defined as someone who uses

information to make decisions and take actions that cause

the fulfillment of objectives, reads information

IM Project NPV

– The net present value of the cash flow expected from IM

projects over 5 year planning horizon

IM Portfolio NPV

– Net present value of the current information assets

expressed as pro-rated portion of free cash flow

17

Summary

Measurements of

information value and

effectiveness are

viable

There are many many

options to present the

value of an

information program

Saying it cannot be

measured is not an

option

18

All content copyright 2013 IMCue Solutions LLC 19

Building Value Through Information Asset Management™

314-422-9076

19