Embed Size (px)

Citation preview

Telco data networks in Africa: Enablers of value added services or just cheap

access to OTT applications?

Zwana UnicomJune 2011

_______________________________________________________

Background• African mobile voice revenues to peak in 2012 *• Downward pressure on interconnect prices (e.g. leading

to presidential intervention in Kenya in June 2011)• African mobile data revenues will rise from $4.45bn in

2009 to $10.64bn in 2014 *• IP has changed the game for telcos as they move from

voice-centric to data-centric• Customers turn to OTT applications like Skype to meet

their needs_______________________________________________________

* Informa

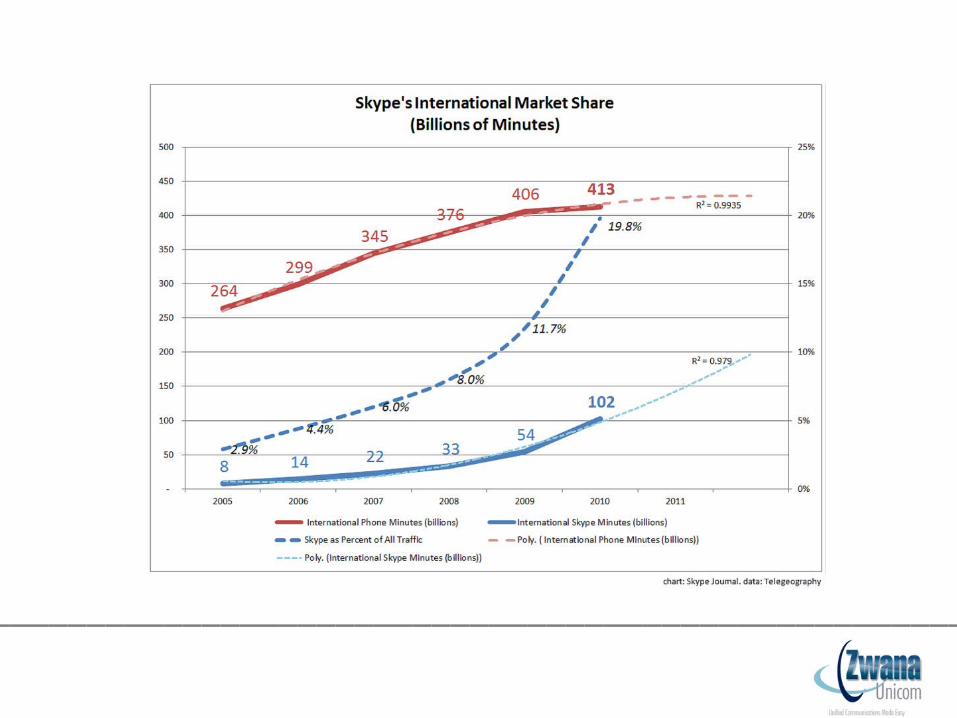

Challenges• With 600 million users, Microsoft Skype is now a

major player in the telco space

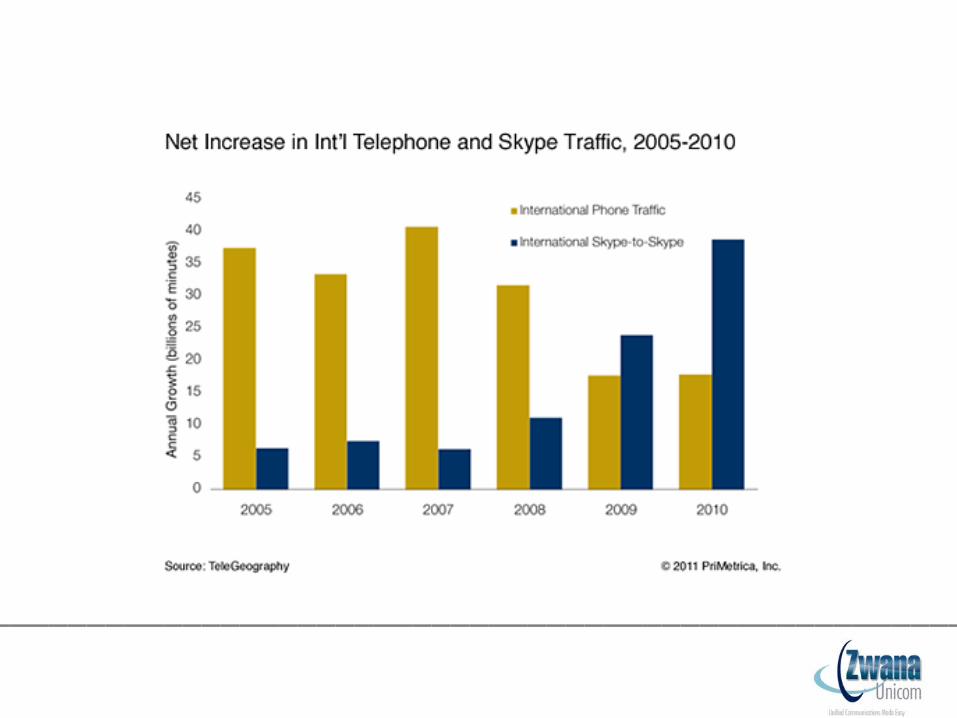

• Skype users made 207 billion minutes of voice and video calls in 2010, approximately 50% of which was international, most of which bypassed the PSTN.

• Skype international traffic is growing at more than 2x that of international phone traffic.

_______________________________________________________

_______________________________________________________

_______________________________________________________

Challenges (contd.)• Although Skype’ volumes are small compared to total

telco minutes, calls made by Skype users all used up telco bandwidth without bringing the telcos any revenue.

• As an example, KPN, which has a 48% market share in the Netherlands has blamed the increasing use of OTT applications for a 8.1% drop in Dutch service revenue in April 2011 , resulting in a profit warning and plans to axe 20% to 25% of the company's workforce in the Netherlands between 2011 and 2015.

• African operators face drop in voice and SMS revenues as users turn to VoIP_______________________________________________________

“Demand for international communications remains strong, but ever more people are discovering that they can communicate without the services of a telco.”

TeleGeography Analyst Stephan Beckert

_______________________________________________________

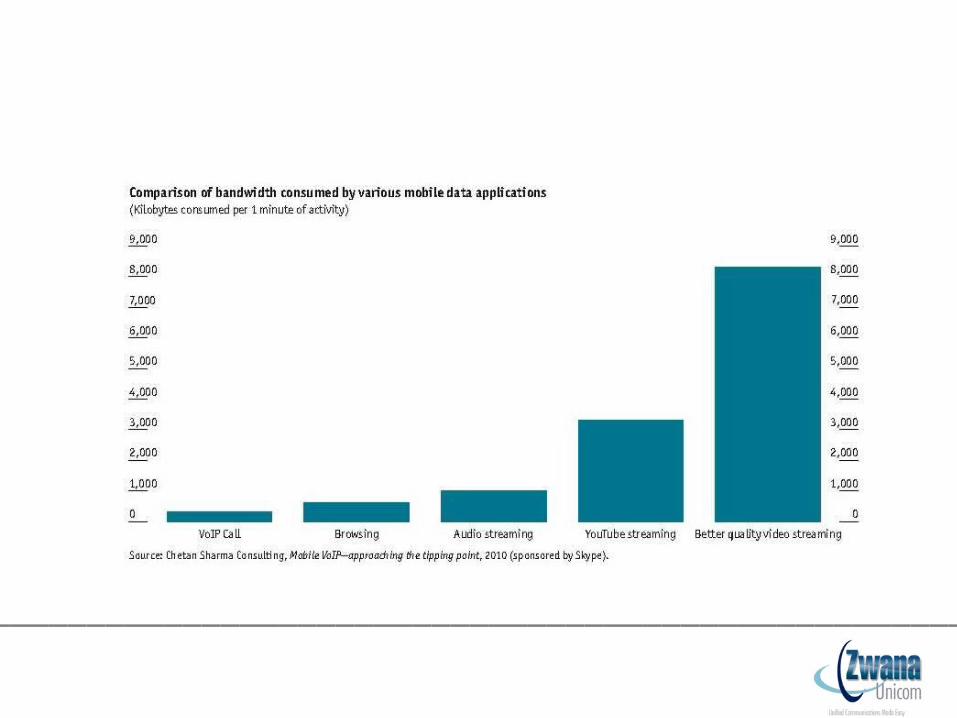

Challenges (contd.)• Operators’ battles are not just with traditional

competitors anymore but also with OTT providers:– mVoIP can kill mobile operators’ roaming charge cash cow

– VoIP user can talk for 22,222 minutes before exceeding a 5 GB data cap – there are only about 43,000 minutes in a month*

– Demand for mobile broadband will outstrip supply as bandwidth improves and users use more bandwidth accessing VoIP and Video services from OTT providers

_______________________________________________________

* In-Stat

_______________________________________________________

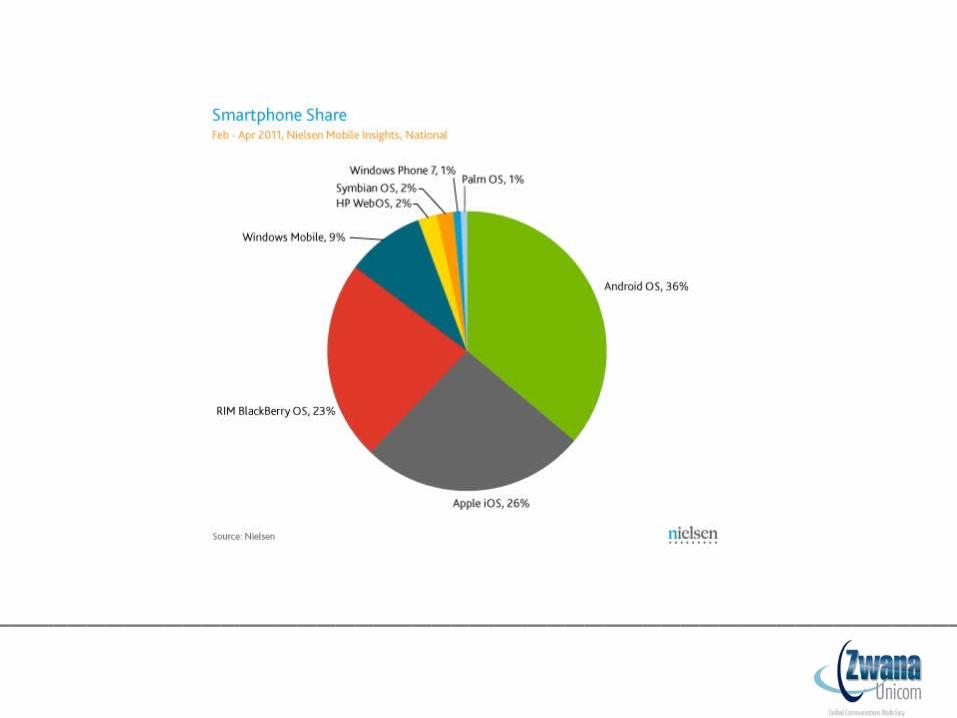

Challenges (contd.)• Android’s share of the smartphone market now exceeds

Apple’s• Fortunately for operators, smartphones still have a small

share of the market• But smartphone usage in developing regions like Africa

will increase with cheap Chinese smartphone imports and Android’s share increasing even more

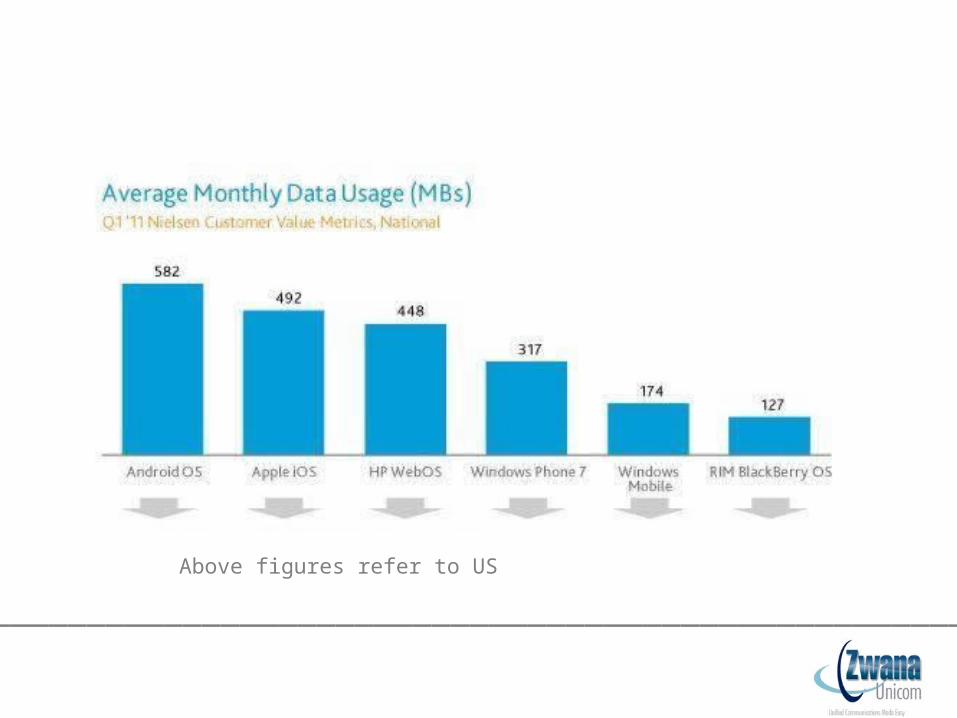

• Android data usage per user has already overtaken that of iPhones

_______________________________________________________

_______________________________________________________

_______________________________________________________

Above figures refer to US

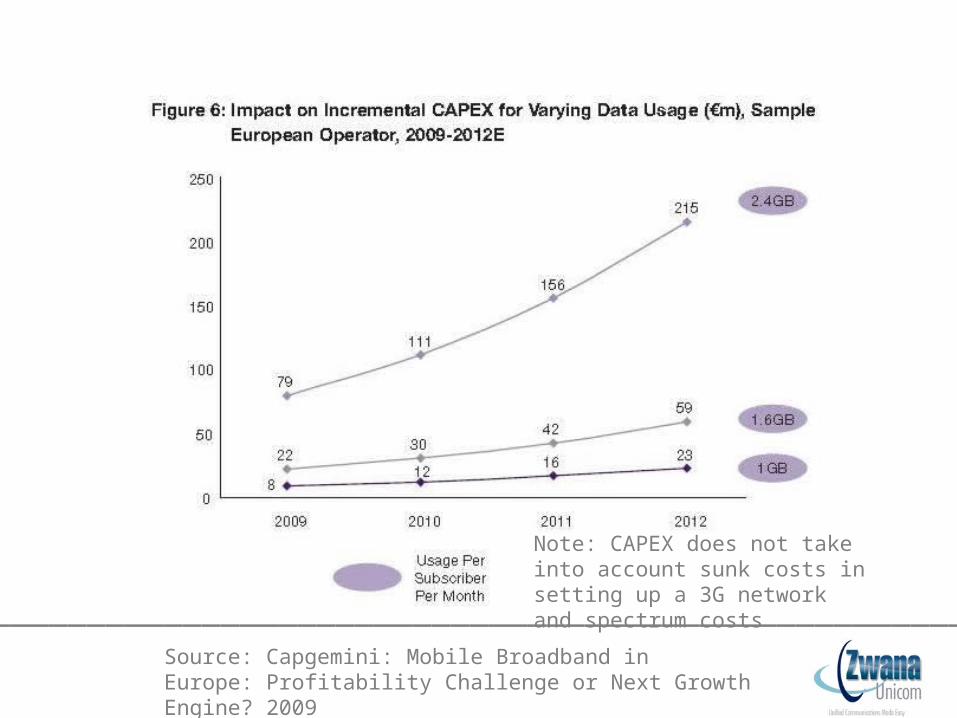

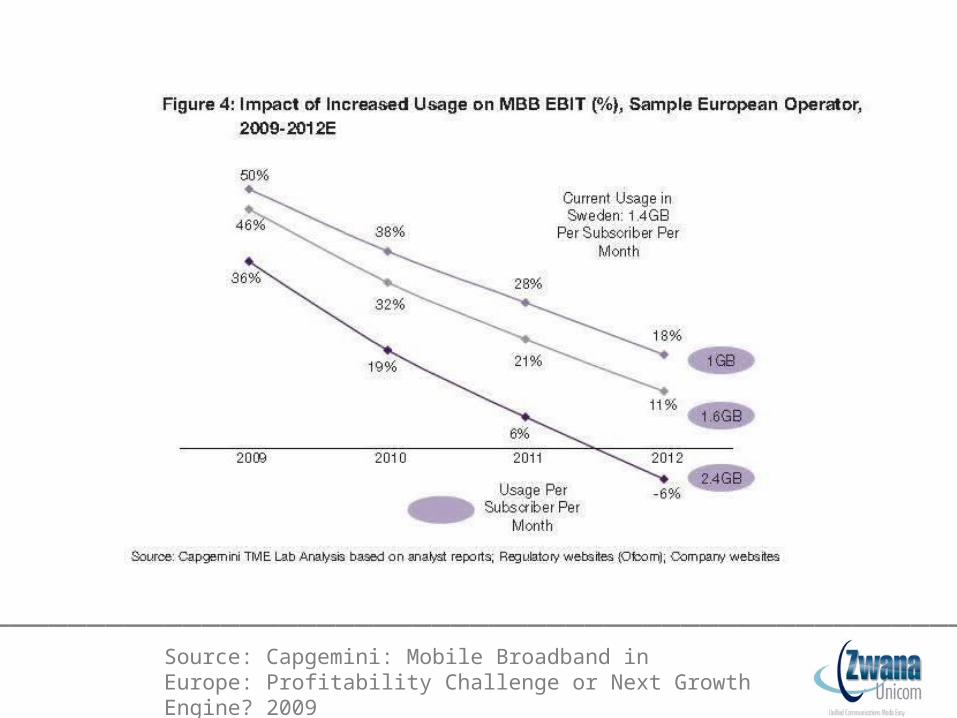

Challenges (contd.)• As data usage increases, operators CAPEX and OPEX

costs increase substantially threatening profits

• The situation is now so acute that some commentators predict that typical operators will reach the end of profitability by 2015 if continued erosion of traditional revenues continues and nothing emerges to replace them.

_______________________________________________________

_______________________________________________________Source: Capgemini: Mobile Broadband inEurope: Profitability Challenge or Next Growth Engine? 2009

Note: CAPEX does not take into account sunk costs in setting up a 3G network and spectrum costs

_______________________________________________________Source: Capgemini: Mobile Broadband inEurope: Profitability Challenge or Next Growth Engine? 2009

Challenges (contd.)• Telcos/ISPs can’t prevent their users from accessing

the services of OTT providers *• And they can’t charge users extra for accessing such

services either*• So Telco and ISP clients will access more and more

OTT applications from more and more OTT startups• So operators will lose control of their clients• While paying for the bandwidth they use!

_______________________________________________________* The Dutch Parliament voted to approve net neutrality legislation on 22/6/2011. This sets a precedent for other countries.

“Do (you) want to continue providing just commercial products or do (you) want to move up higher in the value chain in order to compete against companies

such as Facebook or Skype?”

Dr Ulrich Hammerschmidt

VP Innovation Projects

Deutsche Telekom ICSS *

_______________________________________________________

* CommuniGate Systems’ Executive Summit, Bodrum, Turkey 2010

Operators’ Strengths• Relationships with their customers

– Brand

– Billing

– Subscriber information

• The ability to do complex things at great scale• Expertise in voice• Their control of the network and QoS• Ownership of numbering pools____________________________________________________

The Way Forward for Operators• Leverage your strengths

• Encourage MVNOs on your networks by taking advantage of non-telco niche brands in your market

• Provide New Generation telco services to your own clients

• Become an OTT provider yourself!

_______________________________________________________

The Way Forward (contd.)• Target the SME/SOHO market through SaaS/’Cloud

Computing’ offerings :– Gartner estimates that 20% of businesses will own no IT

assets by 2012

– Quick time to value with minimum capital outlay

– Meet the needs of SME/SOHO Generation Y/Millennial employees

_______________________________________________________

How?• Provide ‘BlackBerry like’ services to your business

users who don’t use BlackBerry devices using from CommuniGate Systems

• Provide nomadic ‘2nd phone number’ services using

• Visit CommuniGate Systems at www.communigate.com or Zwana Unicom at www.zwana.net for further information_______________________________________________________

About CommuniGate Systems• Based on open standards, CommuniGate Systems

(www.communigate.com) provides industry leading, world class Unified Communication products

• Since 1991, CommuniGate Systems has powered the worlds' leading telecommunication companies, including Verizon, British Telecom, Deutsche Telecom, Softbank BB and Tele2

_______________________________________________________

About Zwana Unicom• Distributor for Sub Saharan Africa for CommuniGate

Systems• Provides hosted white label and OTT ‘2nd phone

number’ services through associate 1toGo (www.1togo.net )

• Visit our website www.zwana.net for more information.

_______________________________________________________

AcknowledgementsScott Stonham, VP Marketing, CommuniGate Systems,

“Operators can retake the initiative and get back in the game”, 2011

https://www.communigate.com/external/ads/FierceWireless/April2011/HDCloudTelephony/

_______________________________________________________