Embed Size (px)

Citation preview

2016 Global Stratecast CSP Billing - Interconnect & Settlement

Market Leadership Award

2016

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 2 “We Accelerate Growth”

Contents

Background and Company Performance ..................................................................... 3

Introduction .................................................................................................... 3

Industry Challenges .......................................................................................... 4

Stratecast End-to-End Billing Market Assessment .................................................. 6

Telarix ............................................................................................................ 9

Telarix Market Leadership ................................................................................ 13

Conclusion ..................................................................................................... 16

Significance of Market Leadership ........................................................................... 17

Understanding Market Leadership ........................................................................... 17

Key Performance Criteria ....................................................................................... 18

The Intersection between 360-Degree Research and Best Practices Awards .................. 19

About ODAM ........................................................................................................ 19

About Stratecast .................................................................................................. 19

About Frost & Sullivan .......................................................................................... 20

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 3 “We Accelerate Growth”

Background and Company Performance

Introduction

The interconnect & settlement segment of communications service provider (CSP) billing

emerged nearly 30 years ago to address the transport of fixed-line voice calls from one

carrier’s network to another. It has evolved to handle new services such as mobile voice,

mobile roaming, text messaging, and data services.

Interconnect is a wholesale connection between network operators. An interconnect

agreement defines the business and technical terms a carrier accepts for transporting

network traffic with another carrier. In most cases, this involves international carriers

working with other international carriers. In the United States, interconnection also occurs

locally and regionally.

Wholesale carrier services are bought and sold by nearly every network operator

throughout the world, and are supported by a range of interconnect agreements

composed of at least three parts:

First, a technical agreement defines the connection pathway with associated

operational attributes, and specifies the needed protocol definition to allow diverse

types of network traffic to flow between carriers. These technical ―pathways‖ are

generally established once, and then held in place.

The second part pertains to the business relationship of the interconnect

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 4 “We Accelerate Growth”

agreement—the high level contract specifications concerning how network traffic

will be processed and managed. Again, this part of an interconnect agreement is

essential, and is also generally static.

Finally, a pricing agreement is the business contract that defines the pricing and ―in

effect‖ timing of the agreement, along with any other specific terms and conditions

about how network traffic from one carrier will be routed across another carrier’s

network. The pricing agreement is dynamic and an essential part of all wholesale

connections.

Pricing agreements change quickly, sometimes daily. Profitability in the wholesale space

for a network operator comes with routing traffic appropriately to maintain the highest

margin, while balancing volume commitments, quality of service (QoS), and similar

factors. Automated agreement management, especially for pricing agreements, is now an

essential requirement for the end-to-end interconnect partner management process.

Due to the sheer number of CSPs in the world—in excess of four thousand—that must

exchange agreements, price lists, and invoices, an automated, auditable, business

information exchange service has considerable merit. Stratecast believes that an

automated pricing agreement function must be integrated with the interconnect &

settlement solution.

Industry Challenges

The CSP billing segments of interconnect & settlement and partner management share

many similarities. Interconnect is broadly defined as a carrier-to-carrier wholesale

agreement for handling a voice or data connection from one operator by another when the

terminating point of the connection falls outside the original operator’s network. An

interconnect agreement defines the business and technical terms with which a carrier

accepts and transports such connections.

Settlement addresses the financial aspects of these transactions; for example, how much

does Carrier A owe Carrier B for transporting and delivering its traffic? How much does

Carrier B owe Carrier A? The amounts charged or owed in the forward direction do not

always equate to the reverse direction, due primarily to traffic patterns and rate

agreements. A settlement payment is usually initiated on a 30-day cycle between CSPs,

often using a financial clearinghouse supplier to complete the settlement process.

A new source of interconnect is tied to network transport agreements involving the

wholesale delivery of content partner service capabilities for inclusion in complex CSP

service offerings. Another need involves application programming interface (API)

connectivity between partners. This API-to-API association can be facilitated through a

partner-focused orchestration platform provided by a CSP, or it could be provided by other

suppliers within the global communications marketplace. Both of these new requirements

are driving growth.

Partner management is similar to interconnect & settlement, but has emerged more

recently, and has evolved quickly. This segment includes supplier agreements: the

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 5 “We Accelerate Growth”

business terms and technical interoperability details that define the conditions pertaining

to content or services delivered via a CSP network. Partner management also includes a

financial settlement function: the details of who gets paid, how payments are defined, and

how often they are made. The figure below provides a summary of the differences

between the interconnect and partner management functions.

Source: Stratecast

Both types of wholesale relationships involve business-to-business (B2B) interaction; but,

while the interconnect segment focuses exclusively on CSP-to-CSP agreements, partner

management is more far-reaching: CSPs to multiple other organizations. In addition,

traditional interconnect focuses on network connectivity services (voice, text, and data),

while the partner management side covers a wider spectrum of needs.

Interconnect & settlement and partner management share many similarities, and some

suppliers now blend functionality from both domains within their solution offerings. While

practical on many levels, there is still strong resistance to combining them at the solution

implementation and process level for the CSPs that use these tools—often due to historical

preferences and organizational opposition, but also due to the specialized needs of each

domain.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 6 “We Accelerate Growth”

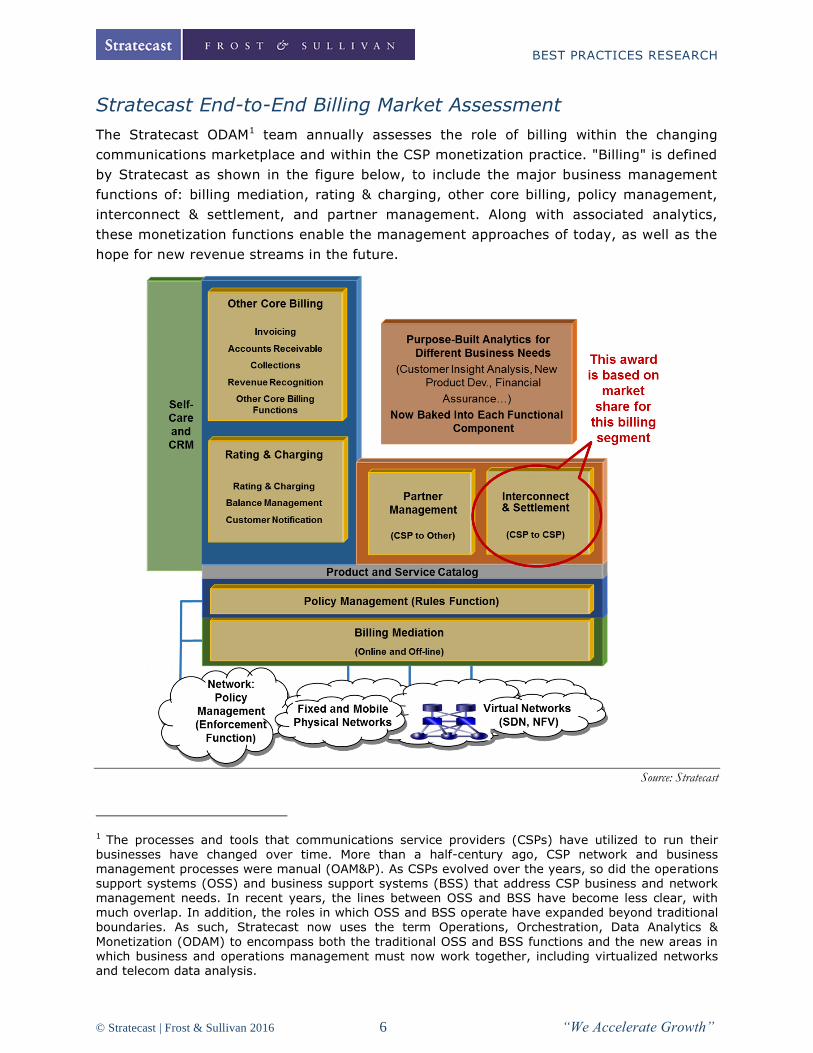

Stratecast End-to-End Billing Market Assessment

The Stratecast ODAM1 team annually assesses the role of billing within the changing

communications marketplace and within the CSP monetization practice. "Billing" is defined

by Stratecast as shown in the figure below, to include the major business management

functions of: billing mediation, rating & charging, other core billing, policy management,

interconnect & settlement, and partner management. Along with associated analytics,

these monetization functions enable the management approaches of today, as well as the

hope for new revenue streams in the future.

Source: Stratecast

1 The processes and tools that communications service providers (CSPs) have utilized to run their businesses have changed over time. More than a half-century ago, CSP network and business management processes were manual (OAM&P). As CSPs evolved over the years, so did the operations support systems (OSS) and business support systems (BSS) that address CSP business and network management needs. In recent years, the lines between OSS and BSS have become less clear, with much overlap. In addition, the roles in which OSS and BSS operate have expanded beyond traditional boundaries. As such, Stratecast now uses the term Operations, Orchestration, Data Analytics &

Monetization (ODAM) to encompass both the traditional OSS and BSS functions and the new areas in which business and operations management must now work together, including virtualized networks and telecom data analysis.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 7 “We Accelerate Growth”

Additional Billing Functions

The monetization needs of today’s complex services require an increasingly real-time

business support process that involves interaction with various network technologies,

computing capabilities, external partners, and suppliers. The end-to-end billing process

consists of the six primary functions previously noted and shown in the figure above, in

addition to others including:

Customer Relationship Management (CRM) solutions have long been adjacent to

CSP billing, which is used by CSPs to communicate with their end-customers. Self-

care is a function that has gained importance in recent years, to allow end-

customers to address most business issues interactively with automated systems

rather than with a customer care agent. Stratecast delineates self-care as part of

Other Core Billing.

Analytics, in particular what Stratecast refers to as purpose-built analytics, is now

part of each of the major billing segments.

Product and service catalogs are an integral part of a CSP billing system, acting as

business logic "glue" to define what customers pay for and what they are provided

by the technology that renders a service offering. As a whole, the product catalog

does not fit neatly into any of the billing segments. However, because product and

service catalogs describe what defines a service, what the role is for each sub-

system delivering a service, and lays out the business rules for how customers are

charged when they use a service, the product and service catalog function is

counted as part of Other Core Billing.

Policy management, as depicted in the figure above, consists of a rules function,

which Stratecast includes as part of billing, and an enforcement function, which

Stratecast views as network capabilities mostly beyond the scope of billing.

Stratecast Billing Report Series

The recently completed Stratecast assessment of the global billing marketplace involves

over 100 global suppliers. The findings are delivered in a multi-part report series

consisting of:

Global CSP Billing 2016 Edition Part 1: End-to-End CSP Billing Market

Forecast and Market Share Analysis provides a market share analysis and five-

year market forecast for the overall, end-to-end global CSP billing market. Recently

released,2 this report identifies the overall billing industry leaders, and highlights

billing solution leaders by revenue within the various global regions.

Global CSP Billing 2016 Edition Part 2: Billing Mediation Market Forecast

and Market Share Analysis assesses the billing mediation sector, provides a

global market share analysis, and establishes a five-year forecast for this market.

2 See OSSCS 17-05, Global CSP Billing 2016 Edition Part 1: End-to-End CSP Billing Market Forecast and Market Share Analysis, June 2016.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 8 “We Accelerate Growth”

This recently published report3 provides a market share analysis of approximately

50 suppliers that deliver mediation solutions to the global CSP market, along with a

five-year revenue forecast.

Global CSP Billing 2016 Edition Part 3: Rating & Charging and Other Core

Billing Market Forecast and Market Share Analysis assesses the rating &

charging and other core billing sectors, both individually and in combination. For

each, the report delivers a five-year market forecast, and a global market share

analysis of approximately 90 suppliers that operate within one or both of these

billing domains. The report is scheduled for publication in August 2016.4

Global CSP Billing 2016 Edition Part 4: Policy Management Market Forecast

and Market Share Analysis. Global CSP Billing Part 4 assesses the policy

management sector—in particular, what is known as the rules function. It provides

a market share analysis of approximately 55 suppliers that deliver policy

management rules function solutions, along with a five-year global forecast. The

report will be published during third quarter 2016.

Global CSP Billing 2016 Edition Part 5: Interconnect & Settlement and

Partner Management Market Forecast and Market Share Analysis. Global

CSP Billing Part 5 assesses the interconnect & settlement and the partner

management sectors, both individually and in combination. This report is the

source for this award. The report establishes a five-year market forecast for

these two markets, and a market share analysis of the more than 60 suppliers that

operate within them. This report will be published during third quarter 2016.

These five reports constitute what Stratecast refers to as our ―numbers‖ reports, providing

market forecast and market share data for the CSP end-to-end billing market and the six

billing sub-sectors. These five reports are delivered annually.

Global CSP Billing - Interconnect & Settlement Market Share Analysis

The first report in this billing series, OSSCS 17-05, Global CSP Billing 2016 Edition Part 1:

End-to-End CSP Billing Market Forecast and Market Share Analysis, June 2016, provides a

market share analysis for the end-to-end billing market, utilizing a base year of 2015. As

in previous Stratecast forecasts, this analysis is based on the sum of revenue generated

by supplier offerings in six related global billing segments including:

Billing Mediation

Rating & Charging

Other Core Billing functions

Policy Management (Rules Function)

3 See OSSCS 17-06, Global CSP Billing 2016 Edition Part 2: Billing Mediation Market Forecast and

Market Share Analysis, July 2016. 4 See OSSCS 17-07, Global CSP Billing 2016 Edition Part 3: Rating & Charging and Other Core Billing Market Forecast and Market Share Analysis, August 2016.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 9 “We Accelerate Growth”

Interconnect & Settlement

Partner Management

The source report for this award, Global CSP Billing 2016 Edition Part 5: Interconnect &

Settlement and Partner Management Market Forecast and Market Share Analysis, provides

a market share analysis for the interconnect & settlement and partner management

market segments, both individually and in combination.

The findings, as published in this report, show that Telarix leads in market share

for the global CSP billing interconnect & settlement market. Stratecast believes

that Telarix addresses approximately 20% of the interconnect & settlement

market based on revenue collected from the sale of these solution capabilities.

The next four competitors address approximately 19%, 14%, 10%, and 8% of

the market respectively by revenue.

For this report series, Stratecast contacted more than 100 billing suppliers that address

one or more of the above mentioned market segments, including approximately 56

suppliers that offer interconnect & settlement solutions. Stratecast revenue estimates

include vendors with software solution offerings that obtain revenue from license fees,

maintenance fees, services associated with the initial installation and configuration of a

solution, service bureau fees, cloud services fees, and installed solutions managed by a

supplier. Internal CSP spending attributed to internal work teams or assistance from

professional services consulting resources is not included. In addition, hardware-related

revenue and revenue generated by systems integrators or companies without their own

billing solutions are not included. The professional services fees for integration of new

solutions with existing systems, and updates to CSP business processes are also not

included in the market share analysis.

The market share analysis is developed by analyzing multiple sources including

information supplied to Stratecast through a market questionnaire, information from

public sources, direct interviews, and raw market data. The analysis is developed from

2015 company-level revenues, projections of future earnings, global financial market

insights, as available, and our strategic acumen concerning billing functions.

To obtain estimated revenues and associated market share, Stratecast used a modified

Delphi method for revenue analysis. Factors such as known deployments, publicly and

privately reported revenue, customers served, press releases, financial reports, and

related information were analyzed by a multi-person analyst team, each working

independently, to estimate each vendor’s 2015 revenues, where such was not specifically

provided. Final estimates were iterated to reach a consensus using a 90% confidence

interval.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 10 “We Accelerate Growth”

Telarix

Telarix is a privately held independent software supplier headquartered in Vienna, Virginia.

Telarix was founded in 1996, with a global customer base including CSPs in Asia, Europe,

North America, and South America. All of the company’s offerings fall within the CSP

billing segment of interconnect & settlement.

Interconnect & Settlement

Telarix focuses on Interconnect Business Optimization, shown in the figure below,

which provides efficient carrier-to-carrier relationships through its portfolio of wholesale

solutions. The portfolio includes two complementary, patented interconnect & settlement

solution suites: iXTools and iXLink.

Source: Telarix

The Telarix iXTools suite can be offered in a licensed, hosted, or Software as a Service

(SaaS) model. The company reports that the suite provides CSPs with a comprehensive

management, optimization, and settlement solution in support of their interconnect

business. The five business modules that define the iXTools solution suite include:

iXConnect – The core module for the iXTools suite, iXConnect, serves as a

―business intelligence platform,‖ collecting and managing all business information.

This includes network elements, products, route plans, rates, and agreements. This

business information forms the main data repository for all other modules.

iXConnect also defines and manages agreements between CSPs and partners, and

applies rates to different types of traffic within the scope of each agreement.

Finally, iXConnect provides near real-time access to business information via its

reporting capabilities, including dashboards with drill-down functionality.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 11 “We Accelerate Growth”

iXRoute – The module enables CSPs to identify and implement optimal routing

strategies, to keep the network profitable. By incorporating volume commitments

and margins, termination costs, network capacity, quality of service requirements,

and other user-defined criteria, Telarix explained to Stratecast that iXRoute can

produce ―the optimal commercial and technical route guides‖ by leveraging the

company’s patented routing algorithms.

iXTrade – iXTrade is an offer management and decision support solution, which

allows CSPs to simplify and automate the buying, pricing and selling processes

within the wholesale interconnect business. This includes managing international

interconnect complexities resulting from non-standardized numbering plans for

country, city, and mobile terminations, and allows rating of calls based on each

partner’s specific numbering plan, to give CSPs the ability to gain near real-time

margin visibility.

iXBill – This module ensures that all billable activities are captured, rated, and

billed. iXBill leverages its integration with other iXTools to provide embedded

revenue assurance capabilities. It allows CSPs to support a variety of agreement

types and rating scenarios, including multi-party settlement and revenue sharing

partnerships.

iXAudit – iXAudit is an end-to-end audit and dispute management system

designed to streamline the validation of interconnect invoices, reconcile charges,

and manage settlement. It serves as the data repository for all carrier invoices.

iXAudit automatically reconciles invoice data with internal traffic and cost

management information. The solution matches a CSP’s interconnect agreements

with invoice data, traffic usage, and cost data, to determine if discrepancies exist.

This process includes auditing and reconciling incoming interconnect invoices, in

addition to tracking and managing disputes of incoming invoices from vendors, and

outgoing invoices to customers.

Telarix provides an additional interconnect & settlement solution associated with

interconnect agreement management. Branded iXLink, the solution is an information

exchange platform that enables CSPs to automate the exchange of business documents

for the interconnect processes, and to electronically share documents; i.e., pricing quotes,

rate and dial code changes, numbering plans, invoices, and declarations. iXLink has over

4,000 members with 40 million transactions monthly. The iXLink exchange service allows

members to apply business rules that are specific to each partner and/or service to

validate transactions, meet internal business objectives, and capture errors so that the

sender can be notified immediately.

iXLink reduces risks and costs associated with the manual exchange of business

information relating to interconnect & settlement, by automating and assuring the

process. Initiated in 2007, iXLink has become the de facto standard business information

exchange for the interconnect space, with a large majority of global service providers

participating.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 12 “We Accelerate Growth”

Stratecast Insights

As the Internet of Things (IoT) continues to gain solution focus for all industries, so do the

interconnect needs of this evolving environment. The machine-to-machine (M2M)

interactions of IoT and the human-to-machine (H2M) interactions, through devices like

consumer wearables or advanced healthcare monitoring, make the IoT marketplace ripe

for new wholesale connectivity agreements between carriers and between a carrier and its

large business or enterprise customers. Wholesale agreement management for IoT

solutions, with likely pricing agreement requirements similar to wholesale carrier

interconnect today, will become the norm of the future.

Source: Stratecast

Other partner relationship requirements involving CSP connectivity are tied to the new

level of capabilities that will come from augmented reality (AR) and virtual reality (VR). In

addition, the high data volume processing capacity and low latency needs that 5G mobile

will bring to light, add substantially to the growing opportunity window for companies such

as Telarix in satisfying the accountability needs of wholesale network capacity

management. Finally, the world of wholesale virtual network functions (VNFs) traded,

sold, or shared between CSPs, and between a CSP and possible VNF development

factories, will keep both the partner management and interconnection markets far from

becoming stagnant in the months ahead.

Stratecast views Telarix as the market leader within the wholesale interconnect

& settlement sector as defined today, with an entrenched focus on this space

through its Interconnect Business Optimization strategy. With both the iXTools

suite of interconnect & settlement solutions and its iXLink carrier-to-carrier

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 13 “We Accelerate Growth”

information exchange, Stratecast expects the company to remain at, or near, the

top of this market segment for addressing the needs of wholesale carrier-to-

carrier connectivity management.

With the same types of business solutions as what iXTools and IXLink bring the

carrier-to-carrier market, Telarix is well-positioned to address the upcoming

business connectivity needs of related markets including IoT, AR, VR, 5G, and

virtual network management.

Telarix Market Leadership

The 2016 Stratecast Global Market Leadership Award in CSP Billing for the Interconnect &

Settlement Market is judged based on ten criteria detailed later in this document. Telarix

was compared against two other leading suppliers in the CSP interconnect & settlement

space.

The following details a selection of the comparisons from the ten criteria. The data behind

the comparisons comes from Stratecast report: Global CSP Billing 2016 Edition Part 5:

Interconnect & Settlement and Partner Management Market Forecast and Market Share

Analysis, which will be released in the coming weeks.

Growth Strategy Excellence

Stratecast assesses the end-to-end CSP billing market every year, which involves analysis

of over 100 suppliers of billing solution functionality. This market, and most of its

components, have each grown over the last six years with some segments growing faster

than others. Stratecast forecasts the five-year compound annual growth rate

(CAGR) for the interconnect & settlement market to continue to climb at a single-

digit rate from 2016-2020. This growth comes from a number of sources, each

relating to changing business needs and customer expectations. Today,

interconnect & settlement accounts for approximately 4% of the overall CSP

billing market.

In a marketplace that has been expanding such as the end-to-end CSP billing market, in

general, and for interconnect & settlement in particular, growth is essential to maintain

market position. For the 2016 version of the Stratecast end-to-end billing market

assessment, we identified 56 billing solution suppliers that deliver some level of

interconnect & settlement functionality for the communications market. Telarix continues

to grow at a year-over-year rate higher than the overall market, with a share of

approximately 20%. This is up from the 19% share identified by our last assessment of

the interconnect & settlement market.

With the potential growth opportunities that are coming for the wholesale revenue

management billing segment, Telarix is poised to grow even more as the opportunities

relative to the IoT, AR, VR, and 5G markets begin to take shape.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 14 “We Accelerate Growth”

Implementation Excellence

Stratecast recognizes that to be a leader in CSP billing, in an individual segment of CSP

billing, or in any of the areas of CSP ODAM, a supplier must be able to implement the

solutions they have sold; each and every time. This process has become easier recently,

with the growing number of cloud-enabled solutions directed to every segment of the end-

to-end billing market. As Telarix continues to expand its SaaS business model strategy for

all of its solution offerings, implementation complexity for its customers will diminish. In

addition, the fast turn-around of new solution functionality characteristic of SaaS-based

solution offerings will surely spawn new ways for service providers to look at business

challenges, which will eventually create new business management needs.

Stratecast's knowledge of the excellence in implementation with regard to Telarix is well

founded based on several customer testimonials, continued press from Telarix that

identifies CSPs by name, and the ongoing discussions Stratecast has with both Telarix and

its competitors. Together, these actions indicate that the company is keeping its existing

customers happy as it continues to gain new ones in all aspects of its current and

developing business strategy.

Brand Strength

Brand is of great importance to a customer when choosing a product for purchase. This is

true of consumer goods and it holds for CSPs when they choose their ODAM systems with

price tags that usually reach into the millions of dollars. In the area of CSP end-to-end

billing, and in the billing segment of interconnect & settlement, CSPs are trusting their

ability to generate revenue, and even in their ability to stay in business, on a vendor—

trust in a company and in a brand is of utmost importance.

The company’s brand strength is greatly increased by the Telarix iXLink exchange service,

now used by almost all (more than 4000) service providers globally. With the de facto

standard agreement exchange service, the Telarix brand is of great value when offering its

iXTools solution.

Stratecast is certain increasing revenues correlate strongly with CSP brand trust. Telarix

increased its revenue, and CSP customer base over the past year, and therefore its brand

strength since Stratecast’s previous assessment of the CSP billing market.

Product Quality

Similar to the previous two criteria, product quality is very important to CSPs, who expect

any solution they purchase to not only work as promised, but to meet their specific

business needs within the timeframe of delivery they agree to with the software supplier.

Poor quality solutions immediately cause issues with the CSP customer and, bad news

travels fast, which is hard to overcome within the communications marketplace.

Stratecast is certain revenue growth indicates that CSP customers continue to put trust in

a supplier, the quality of their products, and in the supplier's ability to satisfy all needed

business change needs in order for the new solution to operate effectively. The continued

growth Telarix has experienced in the carrier-to-carrier interconnect space over the last

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 15 “We Accelerate Growth”

few years is a strong indicator that its CSP customers find the company's products and

solution delivery capabilities to either meet or exceed expectations.

Product Differentiation

Telarix faces many global competitors, some of which offer solutions that share similarities

to the Telarix iXTools product suite. Telarix would argue that its IXTools is a superior

solution—and its continued growth in revenue and customers backs this argument—what

truly differentiates Telarix is its unique iXLink offering. iXLink, which the company explains

is ―an open, secure, global business information exchange designed by carriers for

carriers,‖ is the de facto standard in interconnect & settlement pricing agreement

information exchange. Telarix reports that more than 4000 iXLink members generate in

excess of 40 million iXLink-facilitated transactions per month.

The iXLink solution gives Telarix a huge competitive advantage when selling its iXTools

solution set to almost every CSP already using iXLink. Telarix was recently acquired by

Vista Equity Partners, the largest software and data-focused investor in the world, that

emphasizes that the SaaS business model is the future for the industry. Telarix is finding

it’s iXLink experience and customer successes are accelerating the decision by iXTools

license customers, to move their IXTools implementations from an on-premise license

model to the iXTools SaaS model. As this shift occurs, both iXLink and iXTools are

becoming shining differentiators for independent solutions representative of all categories

of the CSP marketplace.

Technology Leverage

Much of the above discussion concerning product differentiation directly relates to Telarix

leveraging technology to gain a competitive advantage. Creating an information exchange

solution through its iXLink offering solved a fundamental business problem within the

interconnect & settlement domain. Using its in-depth knowledge of the interconnect

and settlement space, combined with the company's technology know-how and

extremely effective marketing, Telarix essentially has every global CSP as an

iXLink member, giving it a huge and ongoing advantage in this market space.

Stratecast believes that this same level of success will be an accelerator for Telarix to

bring its existing iXTools customers and new customers to its new iXTools cloud-based

solution service.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 16 “We Accelerate Growth”

Conclusion

Stratecast recently concluded its annual assessment of the end-to-end global CSP billing

market. Stratecast specifically evaluated the role of billing within the CSP business

support system and monetization operations. In so doing, Stratecast reached out to and

analyzed the insights from over 100 suppliers, covering various aspects of the end-to-end

CSP billing marketplace.

Stratecast analysis of the global interconnect & settlement segment revealed that Telarix

leads in market share for this sector based on 2015 supplier revenue. Stratecast analysis

also concluded that Telarix presently addresses approximately 20% of this market by

earned revenue.

In recognition of Telarix' superior ability to lead in market share and address

communications service provider’s key challenges, Stratecast awards the 2016

Global Market Leadership Award in CSP Billing for the Interconnect & Settlement

Market to Telarix.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 17 “We Accelerate Growth”

Significance of Market Leadership

Ultimately, growth in any organization depends upon customers purchasing from your

company, and then making the decision to return time and again. Loyal customers

become brand advocates; brand advocates recruit new customers; the company grows;

and then it attains market leadership. To achieve and maintain market leadership, an

organization must strive to be best-in-class in three key areas: understanding demand,

nurturing the brand, and differentiating from the competition.

Understanding Market Leadership

As discussed on the previous page, driving demand, strengthening the brand, and

competitive differentiation all play a critical role in a company’s path to market leadership.

This three-fold focus, however, is only the beginning of the journey and must be

complemented by an equally rigorous focus on the customer experience. Best-practice

organizations therefore commit to the customer at each stage of the buying cycle and

continue to nurture the relationship once the customer has made a purchase. In this

manner, such companies build a loyal, ever-growing customer base and methodically add

to their market share over time.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 18 “We Accelerate Growth”

Key Performance Criteria

For the Market Leadership Award, Stratecast | Frost & Sullivan analysts focused on

specific criteria to determine the areas of performance excellence that led to the

company’s leadership position. The criteria that were considered include (although not

limited to) the following:

Criterion Requirement

Growth Strategy Excellence Demonstrated ability to consistently identify,

prioritize, and pursue emerging growth opportunities

Implementation Excellence

Processes support the efficient and consistent

implementation of tactics designed to support the

strategy

Brand Strength The possession of a brand that is respected,

recognized, and remembered

Product Quality

The product or service receives high marks for

performance, functionality and reliability at every

stage of the life cycle

Product Differentiation

The product or service has carved out a market niche,

whether based on price, quality, uniqueness of

offering (or some combination of the three) that

another company cannot easily duplicate

Technology Leverage

Demonstrated commitment to incorporating leading

edge technologies into product offerings, for greater

product performance and value

Price/Performance Value Products or services offer the best value for the price,

compared to similar offerings in the market

Customer Purchase Experience

Customers feel like they are buying the most optimal

solution that addresses both their unique needs and

their unique constraints

Customer Ownership Experience

Customers are proud to own the company’s product

or service, and have a positive experience throughout

the life of the product or service

Customer Service Experience Customer service is accessible, fast, stress-free, and

of high quality

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 19 “We Accelerate Growth”

The Intersection between 360-Degree Research and Best Practices Awards

Stratecast | Frost & Sullivan’s 360-degree

research methodology represents the

analytical rigor of our research process. It

offers a 360-degree-view of industry

challenges, trends, and issues by integrating

all 7 of Stratecast | Frost & Sullivan's

research methodologies. Too often,

companies make important growth decisions

based on a narrow understanding of their

environment, leading to errors of both

omission and commission. Successful growth

strategies are founded on a thorough

understanding of market, technical,

economic, financial, customer, best

practices, and demographic analyses. The

integration of these research disciplines into

the 360-degree research methodology

provides an evaluation platform for

benchmarking industry players and for identifying those performing at best-in-class levels.

About ODAM

The processes and tools that communications service providers (CSPs) have utilized to run

their businesses have changed over time. More than a half-century ago, CSP network and

business management processes were manual (OAM&P). As CSPs evolved over the years,

so did the operations support systems (OSS) and business support systems (BSS) that

address CSP business and network management needs. In recent years, the lines between

OSS and BSS have become less clear, with much overlap. In addition, the roles in which

OSS and BSS operate have expanded beyond traditional boundaries. As such, Stratecast

now uses the term Operations, Orchestration, Data Analytics & Monetization (ODAM) to

encompass both the traditional OSS and BSS functions and the new areas in which

business and operations management must now work together, including virtualized

networks and telecom data analysis.

About Stratecast

Stratecast collaborates with our clients to reach smart business decisions in the rapidly

evolving and hyper-competitive Information and Communications Technology markets.

Leveraging a mix of action-oriented subscription research and customized consulting

engagements, Stratecast delivers knowledge and perspective that is only attainable

through years of real-world experience in an industry where customers are collaborators;

today’s partners are tomorrow’s competitors; and agility and innovation are essential

360-DEGREE RESEARCH: SEEING ORDER IN

THE CHAOS

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 20 “We Accelerate Growth”

elements for success. Contact your Stratecast Account Executive to engage our experience

to assist you in attaining your growth objectives.

About Frost & Sullivan

Frost & Sullivan, the Growth Partnership Company, enables clients to accelerate growth

and achieve best in class positions in growth, innovation and leadership. The company's

Growth Partnership Service provides the CEO and the CEO's Growth Team with disciplined

research and best practice models to drive the generation, evaluation and implementation

of powerful growth strategies. Frost & Sullivan leverages over 50 years of experience in

partnering with Global 1000 companies, emerging businesses and the investment

community from 40 offices on six continents. To join our Growth Partnership, please visit

http://www.frost.com.