Embed Size (px)

DESCRIPTION

On January 22nd, 2013 the TBR Professional Services research team recorded a recap of vendor performance reported in TBR's 3Q12 PSBQ IT Services Vendor Benchmark, focusing on how specific vendor, go-to-market and resource management strategies impacted financial performance. TBR Senior Analyst Ramunas Svarcas and Analyst Bryan Belange shared their perspectives on the results and provided additional insight into the performance and future of the services market. This deck is from that presentation. Questions answered in the webinar included: 1. What is changing in the IT services market, and which segments are growing? 2. How is cloud impacting IT services revenue growth? 3. Is IT outsourcing disappearing?

Citation preview

TBR

TECHNOLOGY BUSINESS RESEARCH, INC.

TBR’s Professional Services Business QuarterlySM

Research Highlights and Outlook

Technology Business Research Quarterly Webinar Series

Jan. 22, 2013

TBR

2 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

PSBQ 3Q12 Research Highlights and Outlook: Webinar Presenters

Bryan BelangerAnalyst, TBR’s Professional Services [email protected] @bbelangerTBR

Ramunas SvarcasSenior Analyst and Engagement Manager, TBR’s Professional Services [email protected]@rjsTBR

TBR

3 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

• We cover, on an ongoing basis, 35 vendors in our Professional Services Practice, publishing quarterly and semiannual reports.

• Of those vendors, 30 are included in our IT Services Vendor Benchmark. TBR reports are unique due to their deep holistic

analysis of leading vendor businesses. Financial modeling and TBR insights help customers

build a better understanding of vendor business models. TBR reports and webinars are designed to be responsive

to client timelines, to be clear and concise, and to provide insights across multiple layers of an organization.

TBR’s strategic assessment provides an impartial reality check on how vendors are performing in regard to their strategic objectives and the overall market.

Clients are gaining advantages and are better understanding revenue opportunities through not only our reports, but also through their personal relationships with TBR.

PSBQ 3Q12 Research Highlights and Outlook: Webinar Overview

TBR’s IT Services Vendor Benchmark report delivers unique insight and value through in-depth analysis in a concise, consumable format

TBR

4 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

PSBQ 3Q12 Research Highlights and Outlook: Key Trends

Professional Services Vendor Trends for 3Q12

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

Emergence of Cloud: Demand continues to grow for migration and management of legacy IT infrastructure in cloud environments.

Industry Change: Adoption of cloud and shifting client IT spending priorities are challenging vendors’ near-term IT outsourcing growth.

Client Conservatism: IT services growth continues to decelerate as clients employ a “wait and see” approach to IT investment.

Migration of legacy IT to cloud and new client demands stress traditional ITO revenue streams and compel vendors to adjust business models

TBR

5 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

Emergence of Cloud: Demand continues to grow for migration and management of legacy IT infrastructure in cloud environments.

Industry Change: Adoption of cloud and shifting client IT spending priorities are challenging vendors’ near-term IT outsourcing growth.

PSBQ 3Q12 Research Highlights and Outlook: Client Conservatism

Professional Services Vendor Trends for 3Q12

Client Conservatism: IT services growth continues to decelerate as clients employ a “wait and see” approach to IT investment.

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

Migration of legacy IT to cloud and new client demands stress traditional ITO revenue streams and compel vendors to adjust business models

TBR

6 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

Enterprises are prioritizing “run the business” tactical projects over long-term “change the business” awards:•Total TTM IT services revenue growth decelerated to 4.6% in 3Q12 from 10.4% in 3Q11 and 7.9% in 2Q12.•Growth decelerated across all service lines, as well as the Americas and EMEA geographies.Long-term growth leaders will position business models to address three core objectives: (1) cost takeout (2) business outcome enablement and (3) emerging technology adoption.

Professional Services Vendor Trends for 3Q12 — Client Conservatism

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

PSBQ 3Q12 Research Highlights and Outlook: Client Conservatism

Vendors will face further revenue deceleration in 4Q12 as clients display continued conservatism in IT services spending

TBR

7 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

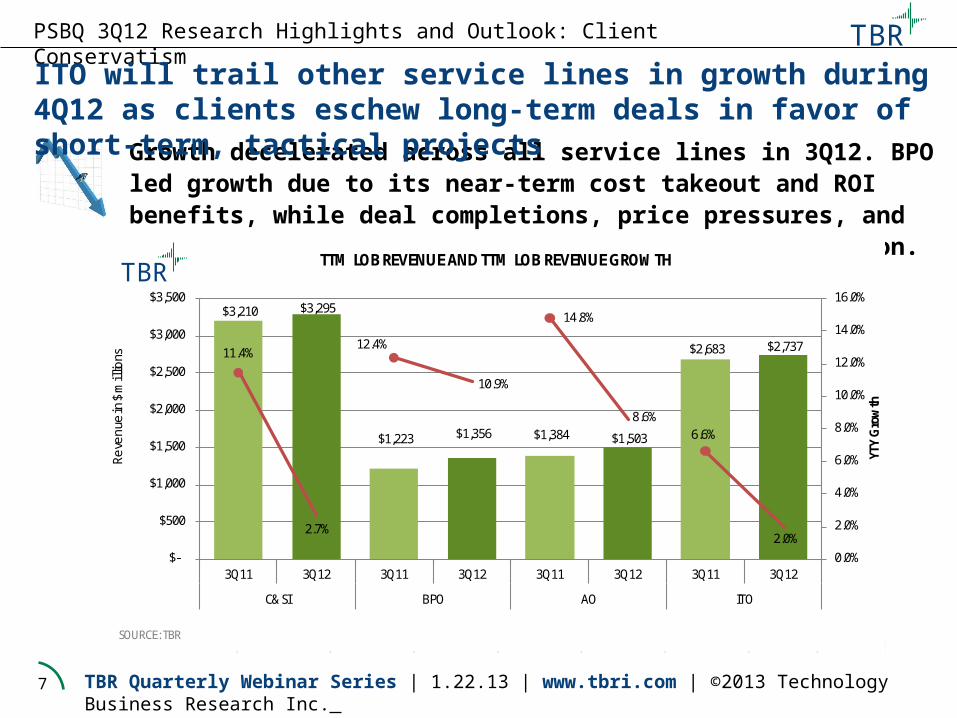

Growth decelerated across all service lines in 3Q12. BPO led growth due to its near-term cost takeout and ROI benefits, while deal completions, price pressures, and demand for shorter-term projects plagued ITO expansion.

PSBQ 3Q12 Research Highlights and Outlook: Client Conservatism

$3,210 $3,295

$1,223 $1,356 $1,384 $1,503

$2,683 $2,737 11.4%

2.7%

12.4%

10.9%

14.8%

8.6%6.6%

2.0%0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

3Q11 3Q12 3Q11 3Q12 3Q11 3Q12 3Q11 3Q12

C&SI BPO AO ITO

YTY

Gro

wth

Reve

nue

in $

mill

ions

TTM LOB REVENUE AND TTM LOB REVENUE GROWTH TBR

SOURCE: TBR

ITO will trail other service lines in growth during 4Q12 as clients eschew long-term deals in favor of short-term, tactical projects

TBR

8 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

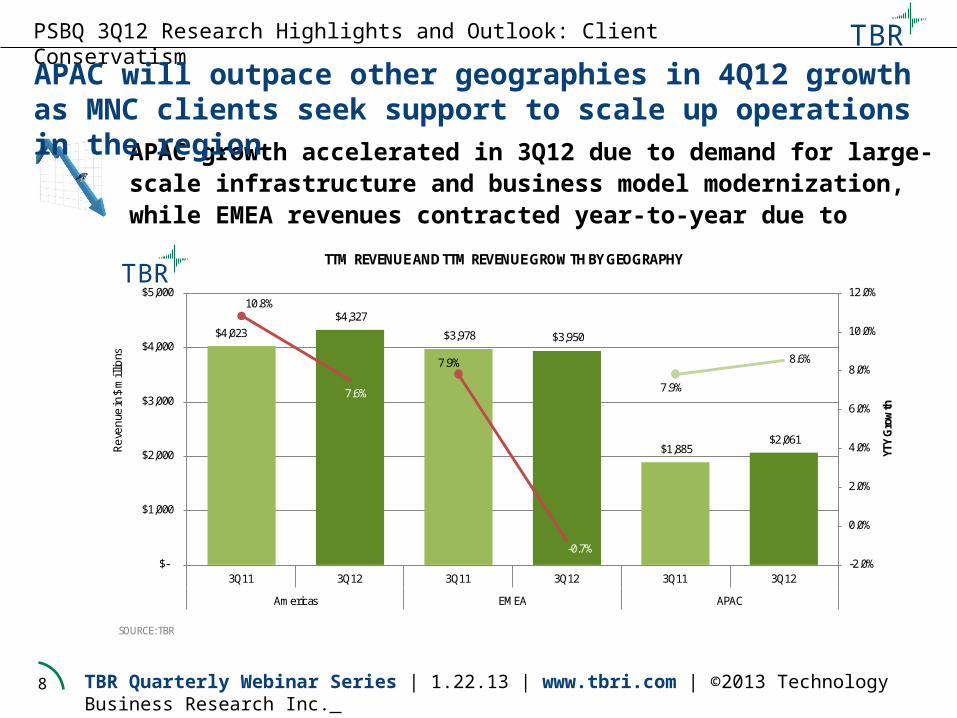

APAC growth accelerated in 3Q12 due to demand for large-scale infrastructure and business model modernization, while EMEA revenues contracted year-to-year due to persistent regional uncertainty and soft discretionary spending.

PSBQ 3Q12 Research Highlights and Outlook: Client Conservatism

$4,023 $4,327

$3,978 $3,950

$1,885 $2,061

10.8%

7.6%

7.9%

-0.7%

7.9%

8.6%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

$-

$1,000

$2,000

$3,000

$4,000

$5,000

3Q11 3Q12 3Q11 3Q12 3Q11 3Q12

Americas EMEA APAC

YTY

Gro

wth

Reve

nue

in $

mill

ions

TTM REVENUE AND TTM REVENUE GROWTH BY GEOGRAPHY TBR

SOURCE: TBR

APAC will outpace other geographies in 4Q12 growth as MNC clients seek support to scale up operations in the region

TBR

9 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

15.0%

16.0%

17.0%

18.0%

19.0%

20.0%

21.0%

22.0%

23.0%

24.0%

25.0%

3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12

Ope

rati

ng M

argi

n (%

)

COGNIZANT OPERATING MARGIN VERSUS INDIA-CENTRIC PEERS

Cognizant Operating Margin Peer Average Operating Margin*

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12

Year

-to-

year

Rev

enue

Gro

wth

(%

)

COGNIZANT YTY REVENUE GROWTH VERSUS INDIA-CENTRIC PEERS

Peer Average YTY Revenue Growth* Cognizant YTY Revenue Growth

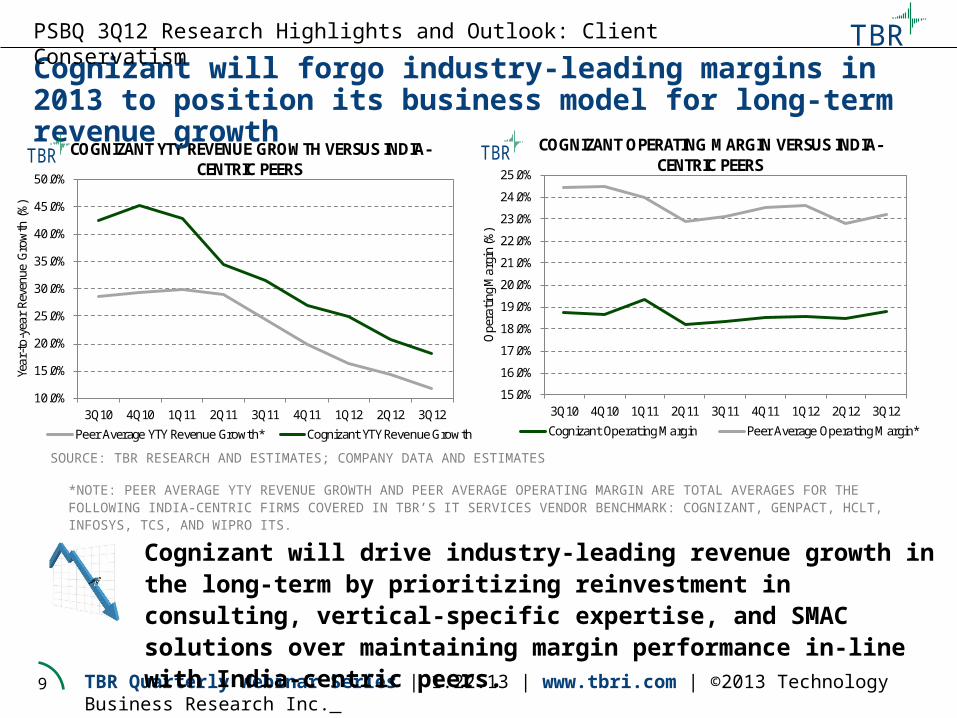

Cognizant will forgo industry-leading margins in 2013 to position its business model for long-term revenue growth

Cognizant will drive industry-leading revenue growth in the long-term by prioritizing reinvestment in consulting, vertical-specific expertise, and SMAC solutions over maintaining margin performance in-line with India-centric peers.

*NOTE: PEER AVERAGE YTY REVENUE GROWTH AND PEER AVERAGE OPERATING MARGIN ARE TOTAL AVERAGES FOR THE FOLLOWING INDIA-CENTRIC FIRMS COVERED IN TBR’S IT SERVICES VENDOR BENCHMARK: COGNIZANT, GENPACT, HCLT, INFOSYS, TCS, AND WIPRO ITS.

PSBQ 3Q12 Research Highlights and Outlook: Client Conservatism

TBR

TBR

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR

10 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

Emergence of Cloud: Demand continues to grow for migration and management of legacy IT infrastructure in cloud environments.

Industry Change: Adoption of cloud and shifting client IT spending priorities are challenging vendors’ near-term IT outsourcing growth.

PSBQ 3Q12 Research Highlights and Outlook: Emergence of Cloud

Professional Services Vendor Trends for 3Q12

Client Conservatism: IT services growth continues to decelerate as clients employ a “wait and see” approach to IT investment.

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

Migration of legacy IT to cloud and new client demands stress traditional ITO revenue streams and compel vendors to adjust business models

TBR

11 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

Cloud computing continues to gain market acceptance as a cost-efficient, secure alternative to investments in on-premise IT, driving fundamental change in vendors’ legacy ITO and AO business models.

“Cloud and less is our motto used during managed services discussions, as cloud drives managed services sales opportunities.” – Wim Los, Atos VP of Cloud Services, Atos Managed Services Industry Analyst Day, December 2013

Professional Services Vendor Trends for 3Q12 — Emergence of Cloud

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

PSBQ 3Q12 Research Highlights and Outlook: Emergence of Cloud

Cloud computing will drive vendors’ long-term outsourcing growth as demand expands for end-to-end cloud managed services

TBR

12 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

SOURCE: TBR 2012 CLOUD PROFESSIONAL SERVICES STUDY

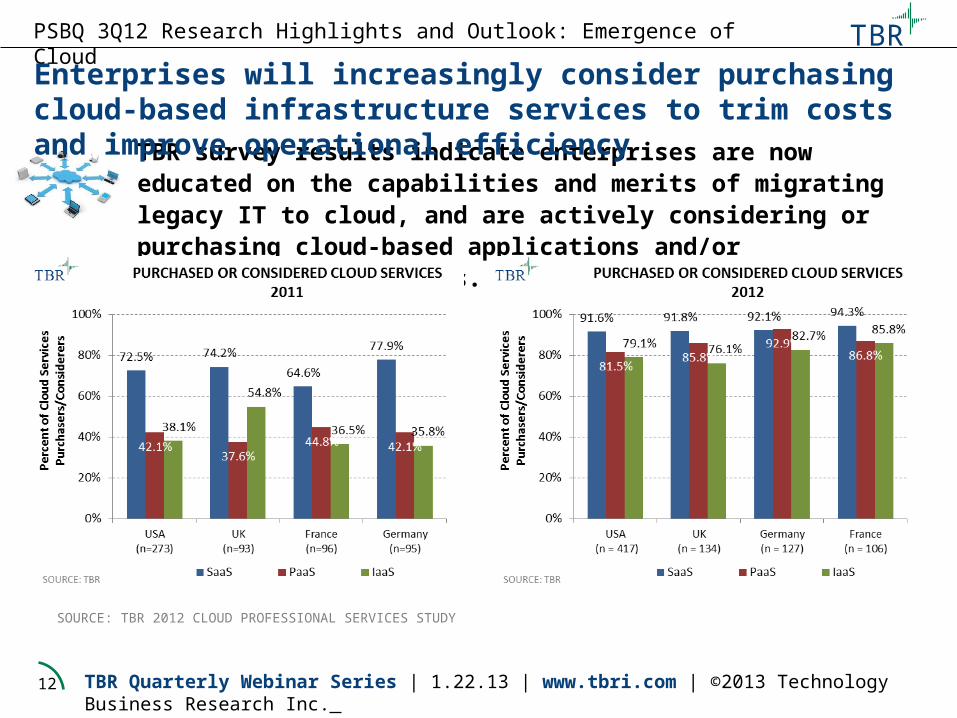

TBR survey results indicate enterprises are now educated on the capabilities and merits of migrating legacy IT to cloud, and are actively considering or purchasing cloud-based applications and/or infrastructure services.

PSBQ 3Q12 Research Highlights and Outlook: Emergence of Cloud

Enterprises will increasingly consider purchasing cloud-based infrastructure services to trim costs and improve operational efficiency

TBR

13 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

Cover Use, Build,

integrate, Operate Cycle

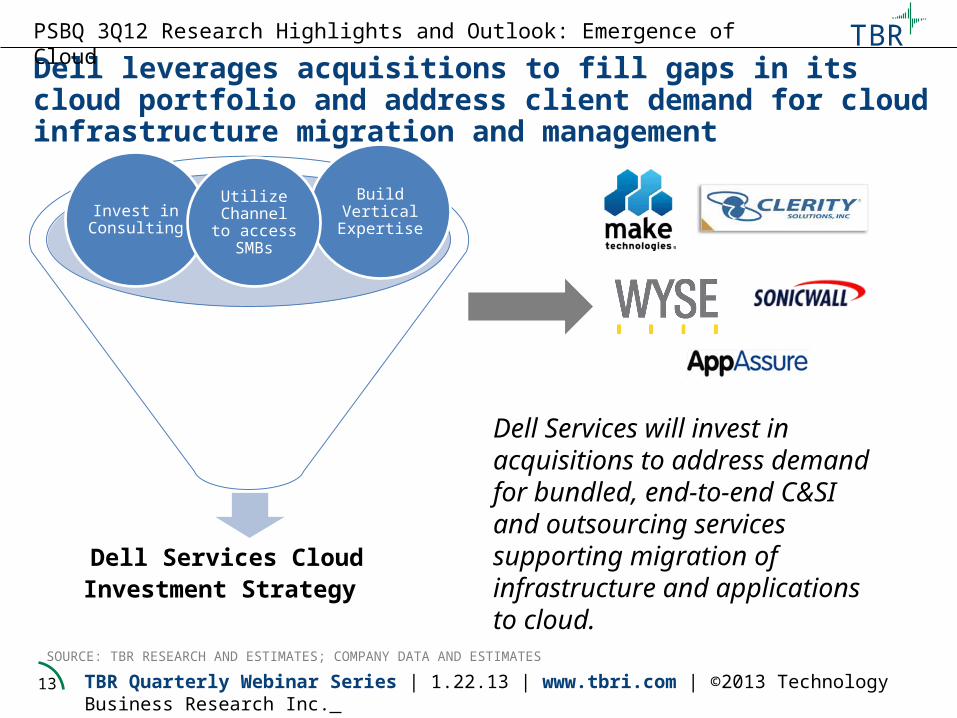

Dell leverages acquisitions to fill gaps in its cloud portfolio and address client demand for cloud infrastructure migration and management

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

PSBQ 3Q12 Research Highlights and Outlook: Emergence of Cloud

Dell Services Cloud Investment Strategy

Dell Services will invest in acquisitions to address demand for bundled, end-to-end C&SI and outsourcing services supporting migration of infrastructure and applications to cloud.

Leverage Hardware

Base

Invest in Consulting

Build Vertical Expertise

Utilize Channel to

access SMBs

TBR

14 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

Emergence of Cloud: Demand continues to grow for migration and management of legacy IT infrastructure in cloud environments.

PSBQ 3Q12 Research Highlights and Outlook: Industry Change

Professional Services Vendor Trends for 3Q12

Client Conservatism: IT services growth continues to decelerate as clients employ a “wait and see” approach to IT investment.

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

Migration of legacy IT to cloud and new client demands stress traditional ITO revenue streams and compel vendors to adjust business models

Industry Change: Adoption of cloud and shifting client IT spending priorities are challenging vendors’ near-term IT outsourcing growth

TBR

15 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

ITO providers are at a crossroads, as client demands and technology changes are challenging traditional revenue streams and requiring new go-to-market approaches:•Emergence of cloud computing •Demand for outcome-based services •Emphasis on smaller deals •Increased pricing structure flexibility/innovation•Demand for blended offshore and onshore delivery capabilities•Vertical-specific sales and delivery expertise

Professional Services Vendor Trends for 2012 — Industry Change

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

PSBQ 3Q12 Research Highlights and Outlook: Industry Change

Client demand for smaller ITO deals addressing cloud adoption and innovation will precipitate changes in vendors’ ITO strategies during 2013

TBR

16 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

$80.5 $80.7$81.5

$83.4

$85.2

$85.6 $86.0

$85.4

$84.2$83.9

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

$77.0

$78.0

$79.0

$80.0

$81.0

$82.0

$83.0

$84.0

$85.0

$86.0

$87.0

3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 Est.

TTM

Yea

r-to

-yea

r Re

venu

e G

row

th (

%)

TTM

Rev

enue

(In

$ Bill

ions

)

TTM ITO REVENUE, GROWTH, AND OVERALL INDUSTRY GROWTH

TTM ITO Revenue TTM YTY ITO Revenue Growth TTM YTY IT Services Revenue Growth

TBR

TBR

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATESNOTE: INCLUDES TOTAL TTM ITO REVENUE FROM TBR’S IT SERVICES VENDOR BENCHMARK, NOT REPRESENTATIVE OF A TOTAL GLOBAL MARKET VIEW.

Total benchmark TTM ITO growth has decelerated rapidly since 1Q12, as clients continue to pass on large-scale, traditional ITO engagements in favor of short-term, tactical deals focused on migrating elements of IT infrastructure to managed private or hybrid cloud environments.

PSBQ 3Q12 Research Highlights and Outlook: Industry Change

Benchmark ITO revenues will contract further in 4Q12 as shifting market dynamics pressure traditional revenue streams in the space

TBR

17 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

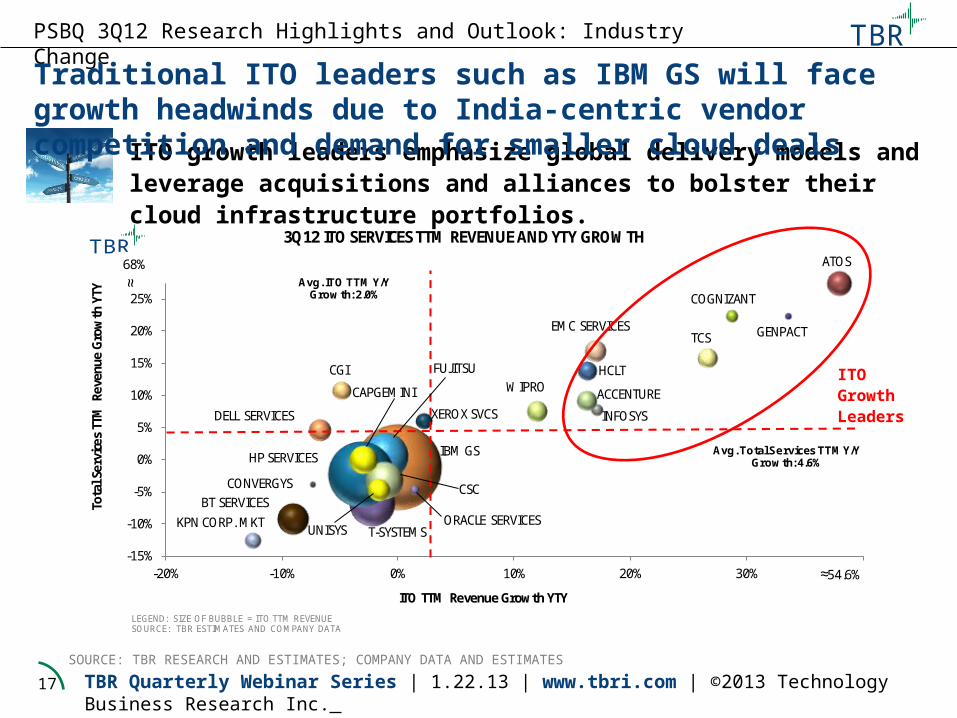

IBM GS

XEROX SVCS

GENPACT

COGNIZANT

TCS

INFOSYS

EMC SERVICES

HCLT

ACCENTUREWIPROCGI

T-SYSTEMS

FUJITSU

HP SERVICES

CSC

CAPGEMINI

UNISYSORACLE SERVICES

DELL SERVICES

CONVERGYSBT SERVICES

KPN CORP. MKT

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

-20% -10% 0% 10% 20% 30% 40%

Tota

l Ser

vice

s TT

M R

even

ue G

row

th Y

TY

ITO TTM Revenue Growth YTY

3Q12 ITO SERVICES TTM REVENUE AND YTY GROWTH TBR

LEGEND: SIZE OF BUBBLE = ITO TTM REVENUESOURCE: TBR ESTIMATES AND COMPANY DATA

Avg. Total Services TTM Y/Y Growth: 4.6%

Avg. ITO TTM Y/Y Growth: 2.0%

≈54.6%

68%

≈

ATOS

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

ITO growth leaders emphasize global delivery models and leverage acquisitions and alliances to bolster their cloud infrastructure portfolios.

ITO Growth Leaders

PSBQ 3Q12 Research Highlights and Outlook: Industry Change

Traditional ITO leaders such as IBM GS will face growth headwinds due to India-centric vendor competition and demand for smaller cloud deals

TBR

18 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

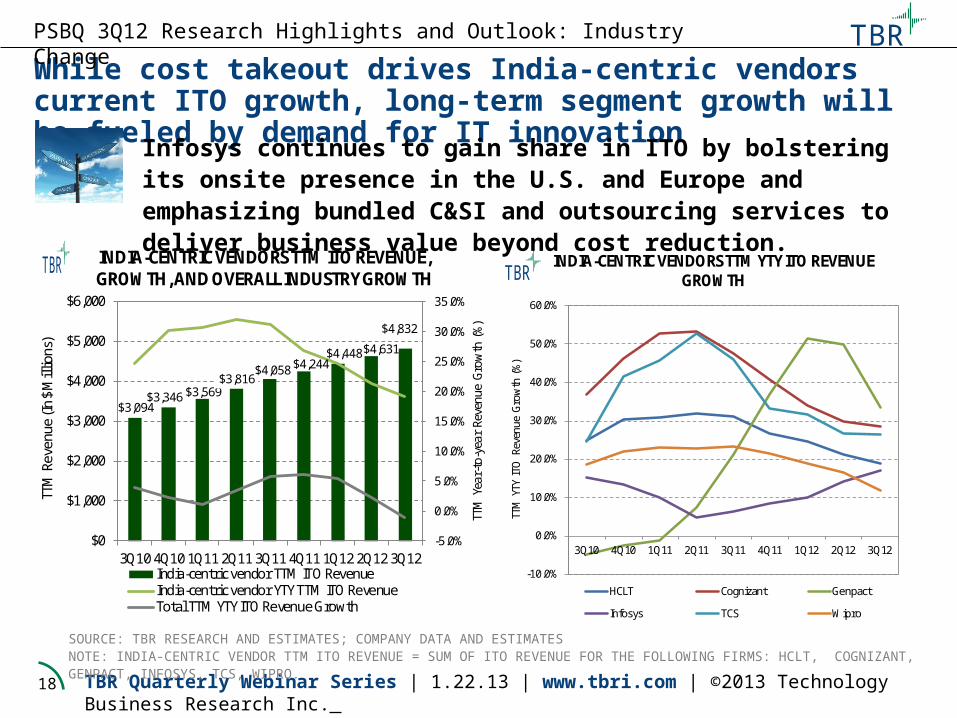

While cost takeout drives India-centric vendors current ITO growth, long-term segment growth will be fueled by demand for IT innovation

PSBQ 3Q12 Research Highlights and Outlook: Industry Change

$3,094$3,346 $3,569

$3,816$4,058 $4,244

$4,448$4,631

$4,832

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12

TTM

Yea

r-to

-yea

r Re

venu

e G

row

th (

%)

TTM

Rev

enue

(In

$ Mill

ions

)

INDIA-CENTRIC VENDORS TTM ITO REVENUE, GROWTH, AND OVERALL INDUSTRY GROWTH

India-centric vendor TTM ITO RevenueIndia-centric vendor YTY TTM ITO RevenueTotal TTM YTY ITO Revenue Growth

TBR

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12

TTM

YTY

ITO

Rev

enue

Gro

wth

(%

)

INDIA-CENTRIC VENDORS TTM YTY ITO REVENUE GROWTH

HCLT Cognizant Genpact

Infosys TCS Wipro

TBR

Infosys continues to gain share in ITO by bolstering its onsite presence in the U.S. and Europe and emphasizing bundled C&SI and outsourcing services to deliver business value beyond cost reduction.

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATESNOTE: INDIA-CENTRIC VENDOR TTM ITO REVENUE = SUM OF ITO REVENUE FOR THE FOLLOWING FIRMS: HCLT, COGNIZANT, GENPACT, INFOSYS, TCS, WIPRO.

TBR

19 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

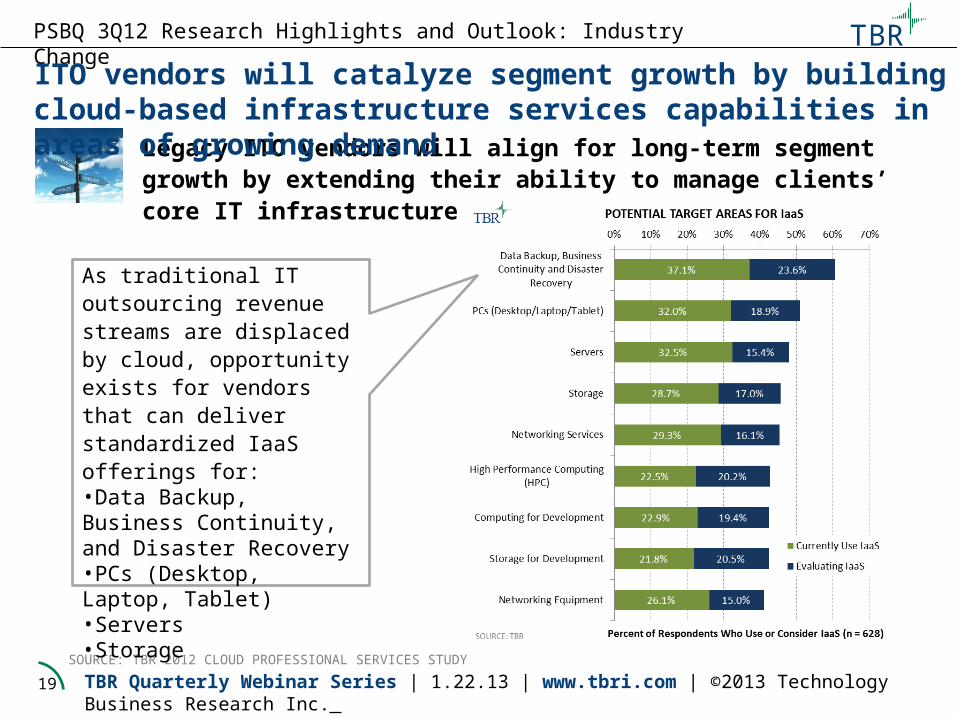

Legacy ITO vendors will align for long-term segment growth by extending their ability to manage clients’ core IT infrastructure in private or hybrid clouds.

SOURCE: TBR 2012 CLOUD PROFESSIONAL SERVICES STUDY

PSBQ 3Q12 Research Highlights and Outlook: Industry Change

As traditional IT outsourcing revenue streams are displaced by cloud, opportunity exists for vendors that can deliver standardized IaaS offerings for:•Data Backup, Business Continuity, and Disaster Recovery•PCs (Desktop, Laptop, Tablet)•Servers•Storage

ITO vendors will catalyze segment growth by building cloud-based infrastructure services capabilities in areas of growing demand

TBR

20 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

Emergence of Cloud: Demand continues to grow for migration and management of legacy IT infrastructure in cloud environments.

Industry Change: Adoption of cloud and shifting client IT spending priorities are challenging vendors’ near-term IT outsourcing growth.

PSBQ 3Q12 Research Highlights and Outlook: Key Trends

Professional Services Vendor Trends for 3Q12

Client Conservatism: IT services growth continues to decelerate as clients employ a “wait and see” approach to IT investment.

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

Migration of legacy IT to cloud and new client demands stress traditional ITO revenue streams and compel vendors to adjust business models

TBR

21 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

PSP Research Current Topics 4Q12 Report Key Themes• Vendor Reports:o Accenture o Atoso Capgeminio Cognizanto CSCo Dell Serviceso Fujitsuo HP Serviceso IBM Global

Serviceso Infosyso TCSo Wipro ITS

• Benchmarks: Management Consulting, HITS, Public Sector, Software Alliance

How are vendors leveraging alliances, acquisitions and/or R&D investments to bolster healthcare-specific solutions breadth and capture opportunity in the space?

What strategies and approaches (R&D, alliances, and/or acquisitions) are vendors employing to develop and integrate IP assets into their services portfolios? Who are the leaders/laggards in building IP?

How are leading/lagging vendors investing in and repositioning their delivery models and portfolios to accommodate cloud IT services demand?

• What vendors are leading/lagging in expansion into the Middle East and Africa? What markets are leaders targeting for regional development?

• What are the predominant IT services demand trends and growth drivers for leading vendors in the Middle East and Africa?

Vertical Growth

Strategy: Healthcare

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

Vendor IP and Asset

Investment Strategy

ITO as-a-Service

Emerging Markets Growth

Strategy: Middle East and Africa

PSBQ 3Q12 Research Highlights and Outlook: 4Q12 Key Topics

Vendors will counter further revenue deceleration in 4Q12 by aligning portfolios to high-growth verticals, technologies, and emerging markets

TBR

22 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

Questions?

PSBQ 3Q12 Research Highlights and 2012 Outlook

TBR

23 TBR Quarterly Webinar Series | 1.22.13 | www.tbri.com | ©2013 Technology Business Research Inc.

For further information, please contact:

Lindy Hanson James McIlroyDirector, Professional Services Practice Vice President, [email protected] [email protected]

Bryan BelangerAnalyst, Professional Services [email protected] @bbelangerTBR

Ramunas SvarcasSenior Analyst and Engagement Manager, Professional Services [email protected]@rjsTBR

@TBRincwww.slideshare.net/TBR_Market_Insightwww.youtube.com/user/TBRIChannel

TBR

TECHNOLOGY BUSINESS RESEARCH, INC.

About TBR

Technology Business Research (TBR) is a leading independent technology market research and consulting firm specializing in the business and financial analyses of hardware, software, networking equipment, wireless, portal and professional services vendors.

Serving a global clientele, TBR provides timely and accurate market research and business intelligence in formats that are tailored to clients’ needs. Our analysts are available to further address client-specific issues or information needs on an inquiry or proprietary consulting basis.

TBR has been empowering corporate decision makers since 1996.

To learn how our analysts can address your unique business needs, please visit our website or contact us today.

Contact Us

[email protected] Merrill DriveHampton, NH 03842USA

This report is based on information made available to the public by the vendor and other public sources. No representation is made that this information is accurate or complete. Technology Business Research will not be held liable or responsible for any decisions that are made based on this information. The information contained in this report and all other TBR products is not and should not be construed to be investment advice. TBR does not make any recommendations or provide any advice regarding the value, purchase, sale or retention of securities. This report is copyright-protected and supplied for the sole use of the recipient. Contact Technology Business Research, Inc. for permission to reproduce.