Embed Size (px)

Citation preview

Building Your Roadmap To Better Compliance And Customer ExperiencePresented by Mike Gardner, Hosted by Karen Webster

June 25th, 2015

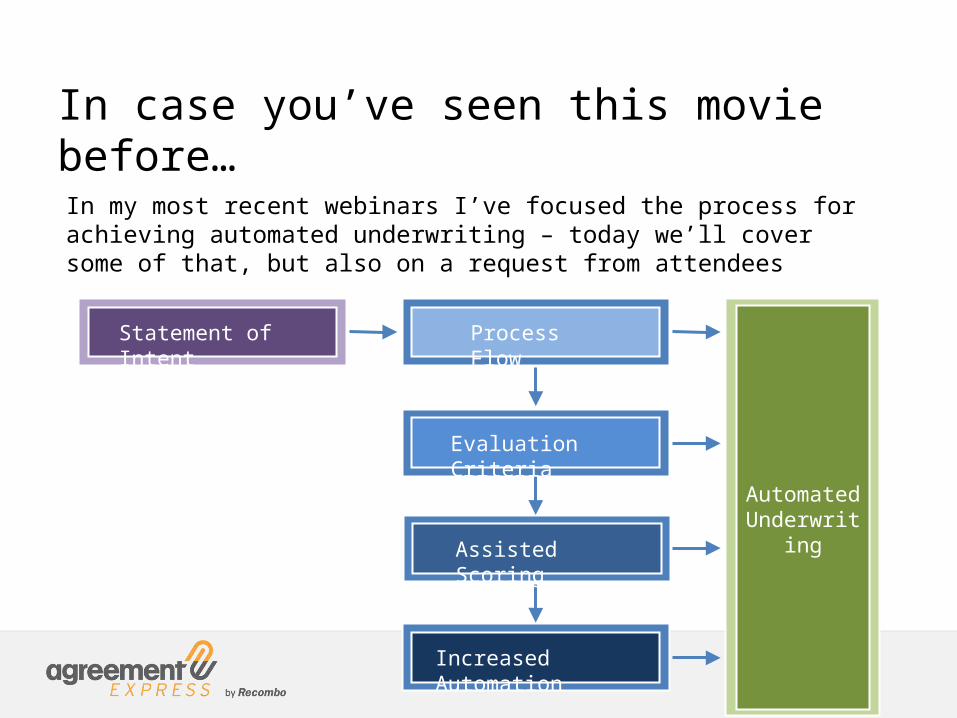

In case you’ve seen this movie before…

In my most recent webinars I’ve focused the process for achieving automated underwriting – today we’ll cover some of that, but also on a request from attendees

Statement of Intent Process Flow

Evaluation Criteria

Assisted Scoring

Increased Automation

Automated Underwriting

THE CUSTOMER EXPERIENCE

In merchant onboarding an extraordinary client experience begins with a great underwriting process

Now that I’ve got your attention, let’s begin

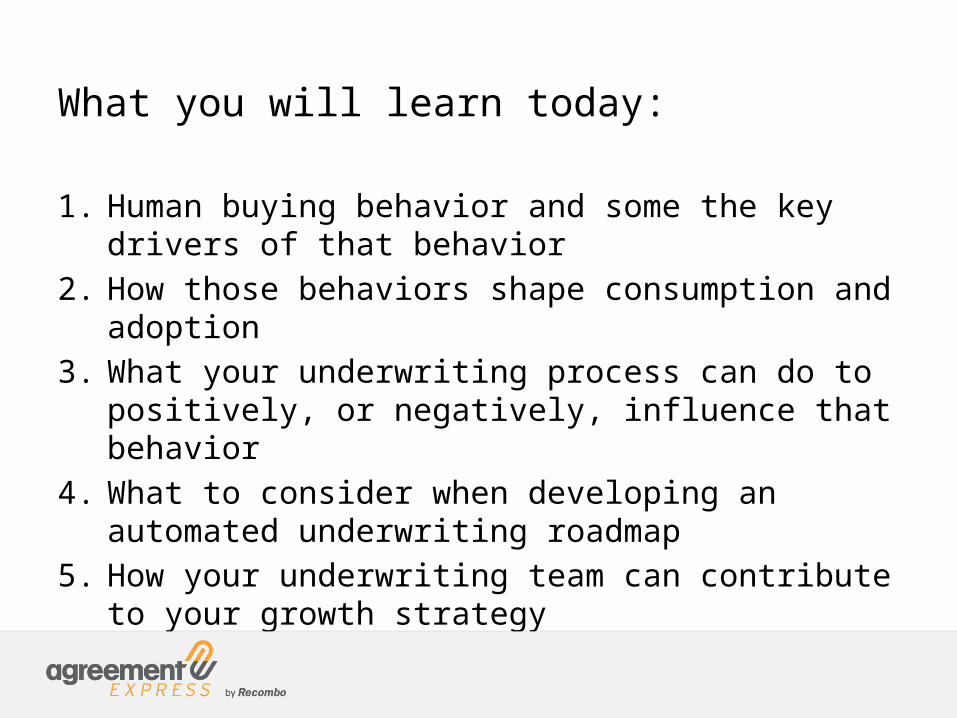

What you will learn today:

1. Human buying behavior and some the key drivers of that behavior

2. How those behaviors shape consumption and adoption3. What your underwriting process can do to positively, or

negatively, influence that behavior4. What to consider when developing an automated

underwriting roadmap5. How your underwriting team can contribute to your

growth strategy

What I think of when I hear “buying behavior”

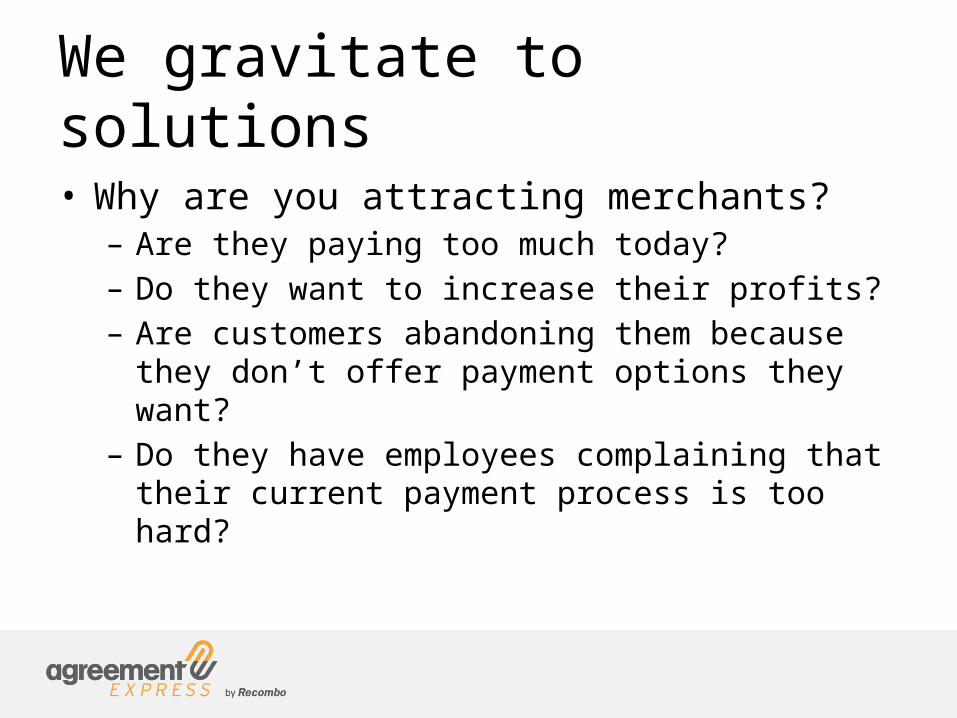

• Why are you attracting merchants?– Are they paying too much today?– Do they want to increase their profits?– Are customers abandoning them because they don’t offer

payment options they want?– Do they have employees complaining that their current

payment process is too hard?

We gravitate to solutions

Price

Why you?

Product Place

Promotion

Price

Why you?

Product Place

Promotion

Convenience

• The variety store in your lobby

• The mobile phone that already has your music, contacts, and your apps

• The transit option closest to your departure and destination

Convenience

• Consumers and users fall into two broad groups– Those with choice– Those without choice (or minimal choices)

• The group your target clients fall into will dictate which of the 3 possible adoption profiles will be in play

Adoption Drives Growth

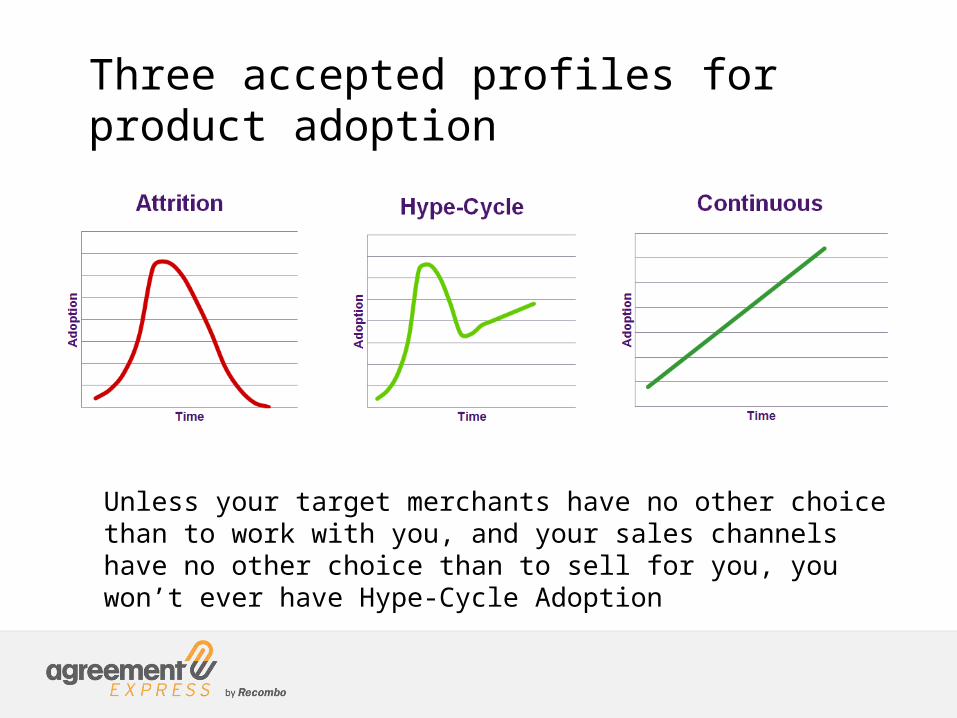

Three accepted profiles for product adoption

Unless your target merchants have no other choice than to work with you, and your sales channels have no other choice than to sell for you, you won’t ever have Hype-Cycle Adoption

But what does this have to do with Underwriting?

Underwriting governs your client experience

Most organizations today are underwriting with people, doing a largely manual assessment, to determine if merchants fall into a “bucket” of Pass, Fail or Monitor.

As organizations move to more advanced, rigorous and automated underwriting, they risk adding more hurdles for the merchant.

The more complex your underwriting requirements, the more your on-boarding

experience will reflect that complexity

Complexity Drives Inconvenience

You’re not working in a vacuumAs you design your underwriting process you are designing your customer experience

• Nice to have instead of necessary

• Difficult to gather instead of at hand

• Challenging to execute instead of easy

• Hard to sell

Hang on - We’ve got rules to follow here!

• The ETA (Electronic Transactions Association) is the trade association representing the payments market. In 2014 they published a 109 page document providing guidelines for merchant and ISO underwriting. It is important to note that the ETA does not set policy for its members, it provides recommendations. Members are not required to adhere to the guidelines provided.

The ETA Risk Guidelines

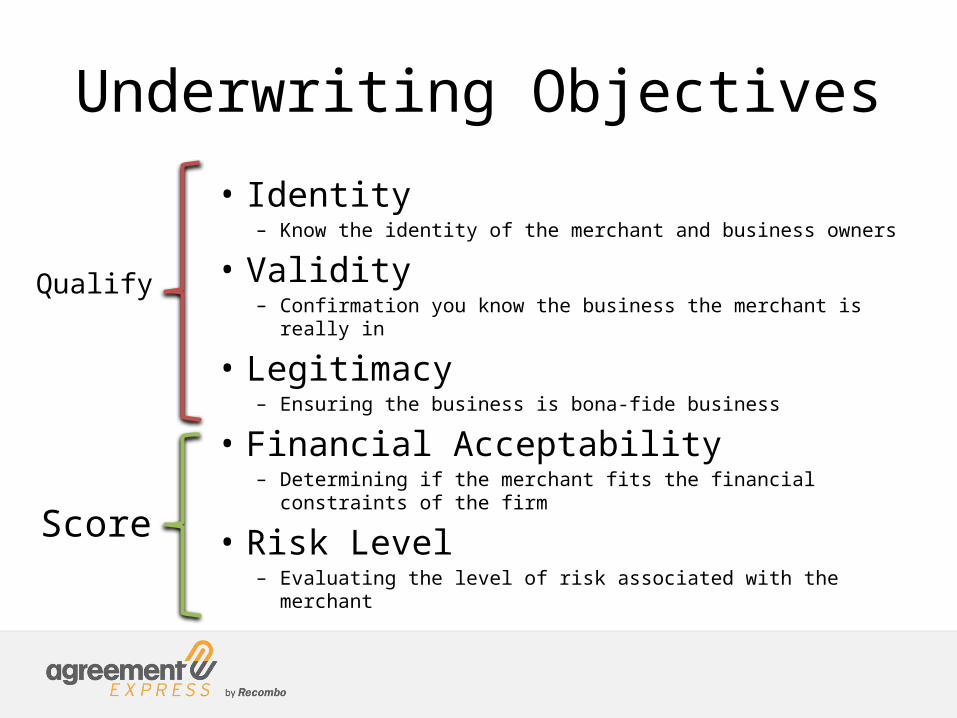

Underwriting Objectives

• Identity – Know the identity of the merchant and business owners

• Validity– Confirmation you know the business the merchant is really in

• Legitimacy– Ensuring the business is bona-fide business

• Financial Acceptability– Determining if the merchant fits the financial constraints of the

firm

• Risk Level– Evaluating the level of risk associated with the merchant

Qualify

Score

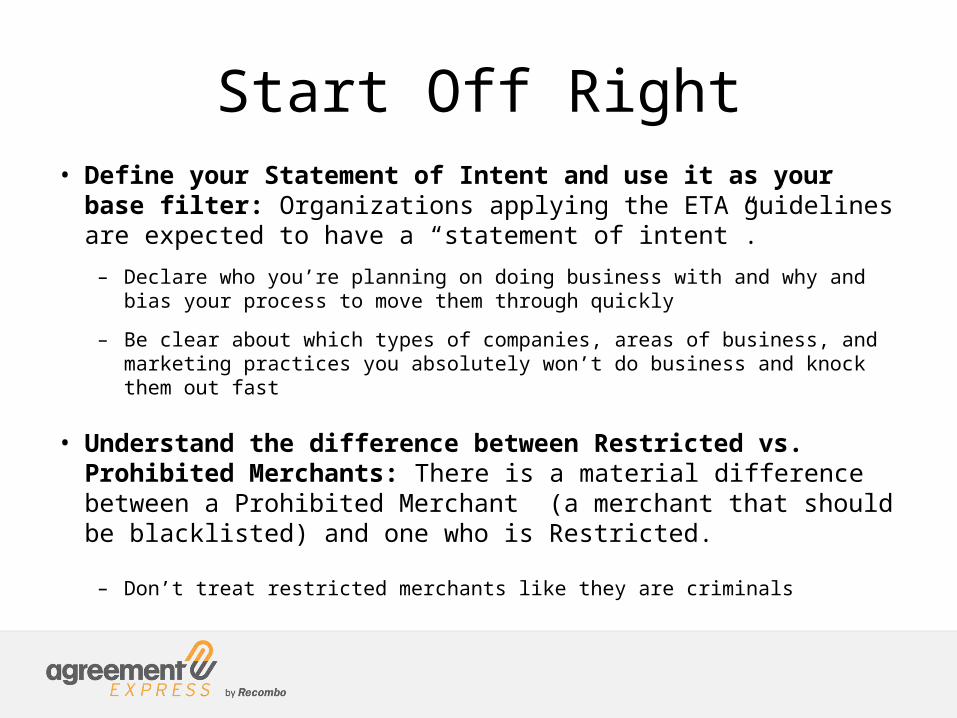

Start Off Right• Define your Statement of Intent and use it as your base filter:

Organizations applying the ETA guidelines are expected to have a “statement of intent”.

– Declare who you’re planning on doing business with and why and bias your process to move them through quickly

– Be clear about which types of companies, areas of business, and marketing practices you absolutely won’t do business and knock them out fast

• Understand the difference between Restricted vs. Prohibited Merchants: There is a material difference between a Prohibited Merchant (a merchant that should be blacklisted) and one who is Restricted.

– Don’t treat restricted merchants like they are criminals

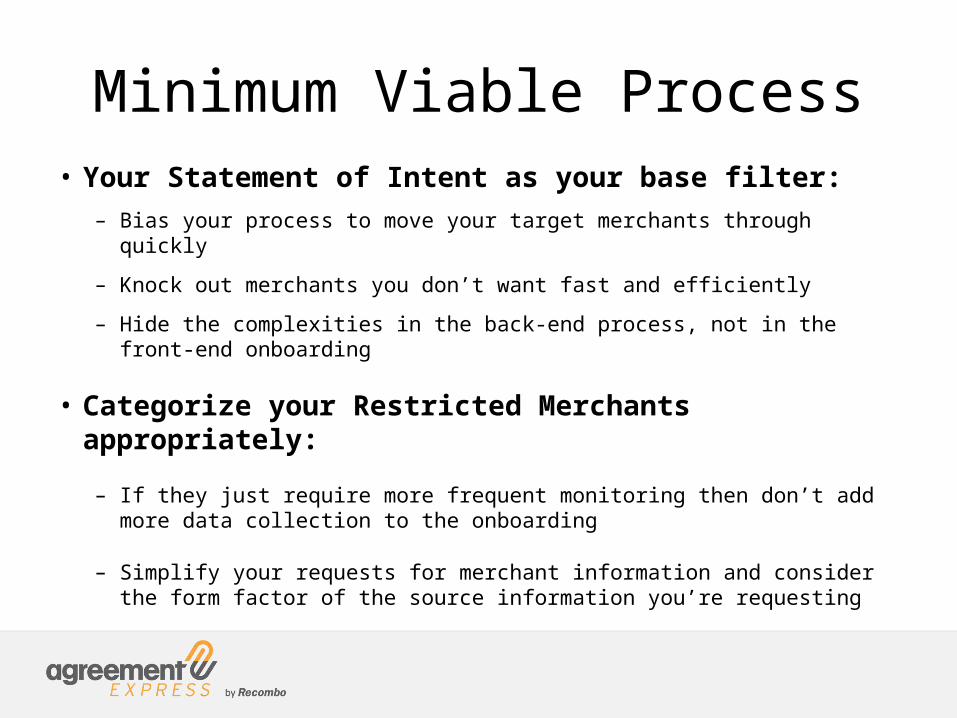

Minimum Viable Process• Your Statement of Intent as your base filter:

– Bias your process to move your target merchants through quickly

– Knock out merchants you don’t want fast and efficiently

– Hide the complexities in the back-end process, not in the front-end onboarding

• Categorize your Restricted Merchants appropriately:

– If they just require more frequent monitoring then don’t add more data collection to the onboarding

– Simplify your requests for merchant information and consider the form factor of the source information you’re requesting

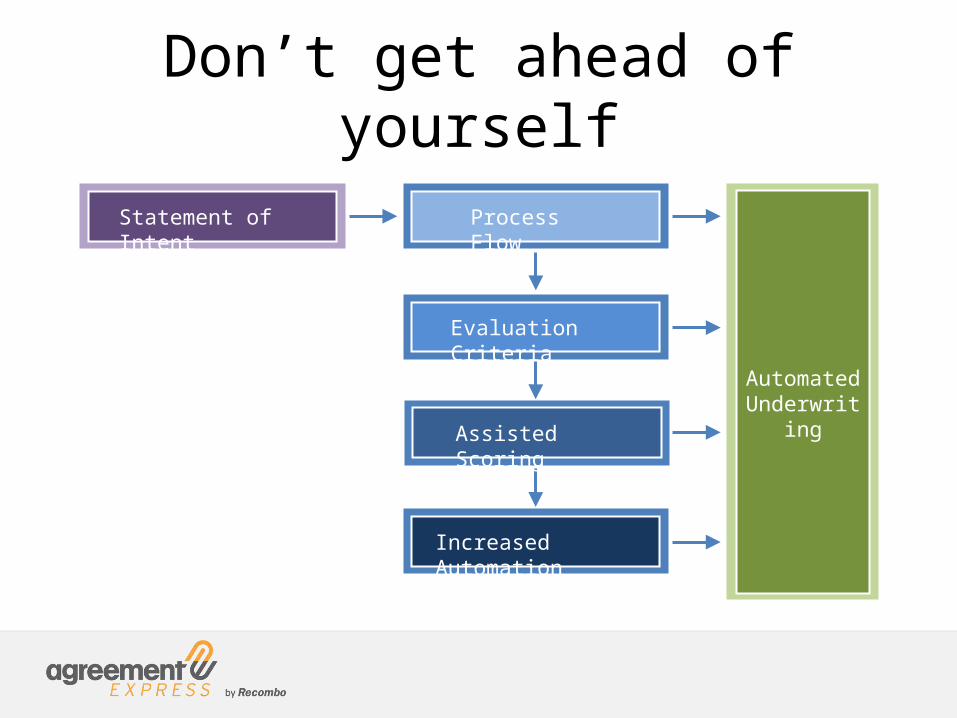

Don’t get ahead of yourself

Statement of Intent Process Flow

Evaluation Criteria

Assisted Scoring

Increased Automation

Automated Underwriting

Get to process flow and evaluate

Process Flow

Evaluation Criteria

Assisted Scoring

Increased Automation

Automate the flow to create a consistent, auditable process

Codify each data-point into a weighted numeric value

Tune and adjust automated score values to match manual evaluations

Monitor and adjust while replacing manual feeds with automatic

Good Process Flow Hygeine

• The ETA recommends firms employ and underwriting process that has the following attributes:

• Timelines (SLA’s) for underwriting evaluation are established• High Risk or Restricted Merchants are evaluated by more

senior staff (escalation) as appropriate• Title and/or Position of ALL approvers are captured during

underwriting• Escalation processes/criteria are documented• The underwriting process is documented and auditable, as

well standardized as much as possible.

Why follow the ETA Guidelines?

• What’s really good about the guidelines– Comprehensive– Create a defensible framework– Safety in numbers

• What’s the challenge with the guidelines– Not easy to fully automate– Directional in nature but not prescriptive– Danger of over specification of risk model

How do you know it’s working?

29

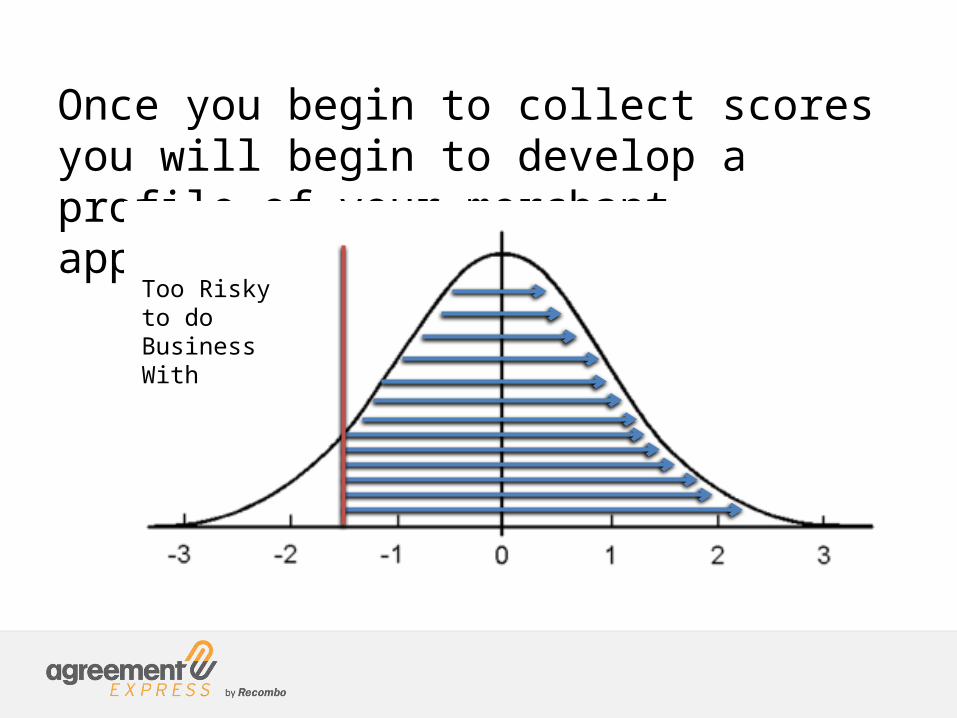

Once you begin to collect scores you will begin to develop a profile of your merchant applicants

Too Risky to do Business With

Just measuring rates of pass or fail simply isn’t good enough

You must monitor and understand the distribution of your underwriting

Risk Tolerance is set too highOR

Sales are being too conservative

Risk Tolerance is set too lowOR

Sales are being too aggressive

But when we use lots and lots of data sources in our underwriting, you increase the probability that your data potentially “overlaps.”

This is a “specification error” and I can almost guarantee that if you’re scoring, you’re over specifying.

Summary:• Refine your Statement of Intent so that it is clear who

you are after and who you are not• Determine if your targets have abundant choice or

limited choice• Define the Minimum Viable Process for underwriting

the various target groups• Minimize the complexities and eliminate any over

specification • Continuously monitor the shape and distribution your

scores, not just the rate of pass or fail

To learn more about Rapid Customer Onboarding, and how it impacts and shapes underwriting in the payments market, visit us at www.recombo.com , follow us @agreexp on Twitter, or contact me directly at [email protected]

Download Your Advanced Copy of Our Digital Guide: Building Your Roadmap to Underwriting Automation

Download The Digital Guide