Embed Size (px)

Citation preview

Preventing Tax Evasion & Combating Fraud through Predictive Analytics Evert Voorn | Thought leader, Tax & Welfare, Capgemini Seminar Digital Transformation

May 12th, 2015 | Stockholm (SE)

2 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

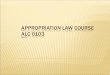

The world is changing and this drives the need for a different model of risk management

External trends

Push to online applications/change of circumstances and renewals; use of mobile apps / text; voluntary sector support for “needs help” segment

Make it simpler for customers so that they comply with the need to inform of change of circumstances and make fewer genuine errors. Design out contact; simplify online forms & guidance and processes

Welfare administrations are leveraging new data sources and more sophisticated modelling tools and data mining to improve targeting of high risk cases, detection of fraud and retrieval of debt

Segmented approach to fraud investigations; graduated range of interventions; moving upstream (prevention)

Process standardisation across benefits; re-platforming; shared services, performance KPIs to drive productivity

Outsourcing /JVs of selected functions e.g. IT, debt recovery, analytics; new commercial models

Growing use of internet to research and buy private sector products and services – fuelling 24/7 and e/mobile app service expectations

Explosion in the use of social media – ability to build customer insight but reputational risks

Internal Trends

(government e.a.)

Digital by default

Improve customer experience

Data analytics to better target risk

Re-inventing government

administrations

Growing use of digital

Globalisation

Industrialisation of fraud

Tax competition between states - large business tax domiciles; inward investment; key skills Rapid growth of emerging economies and middle class – demand for welfare state

Financial austerity in the West

Stagnating or declining real incomes in the West; fiscal deficits and levels of debt Political pressure to address tax non-compliance and welfare fraud

Increasing sophistication of banks and insurance companies are driving criminals to attack tax & welfare authorities; testing defences; insider fraud

Technological developments

Big data - new data sources e.g. Social media, smart grid; processing power e.g. Hadoop; High performance analytics e.g. SNA, voiceprints – shorter analytical timescales Internet transparency

3 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

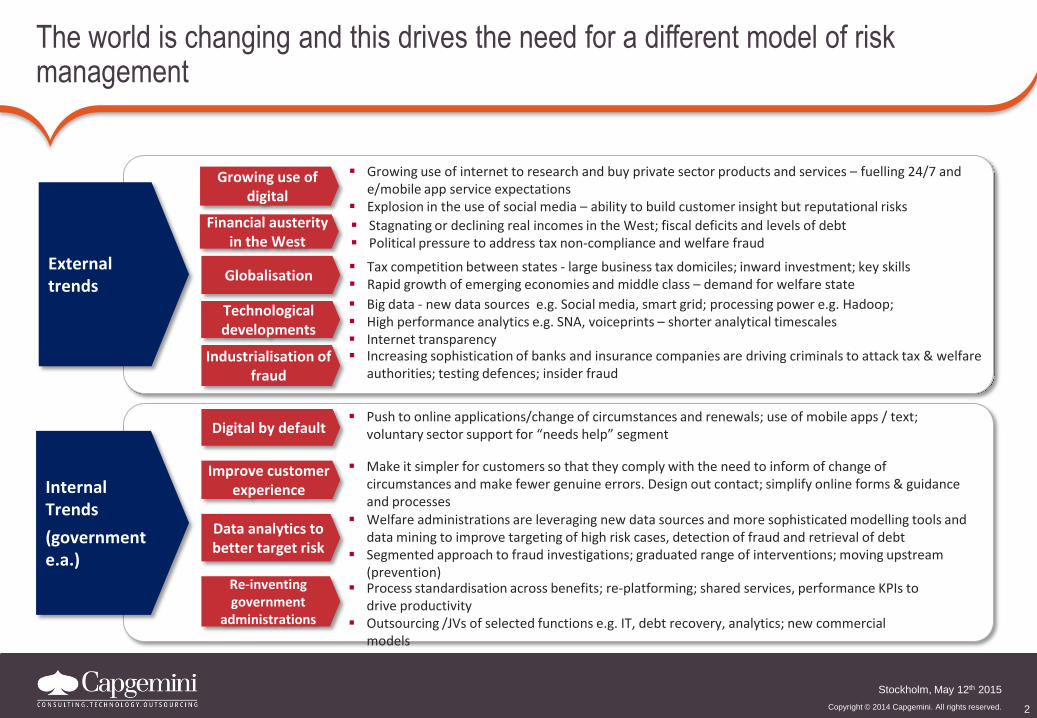

Is there really a fraud problem?

It is estimated that

approximately €100 billion

in total is involved in the

wrongful

non-payment of VAT

within the EU Member

States each year

Source: EU MTIC Report

Shadow economies are

estimated to have

accounted for £880 billion

in lost tax in the EU

between 1999 and 2007

Source: tax justice network

It is estimated that MTIC

VAT fraud contributed

between £0.5 billion

and £1.0 billion to the

UK VAT gap in 2010-11.

Source: HMRC report (2012)

Measuring tax gaps 2012; Tax gap

estimates for 2010-11.

4 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

The fraud landscape spreads from simple opportunistic non-compliance to organized crime

4

Opportunistic Premeditative

Casual

Avoiders

Purposeful

Criminals

Organised

Crime

High Volume/Low Value Low Volume/High Value

Systemic Game

Playing Opportunistic

Level of Sophistication of Fraud

Taxpayer

Segment

Fraud

Type

5 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

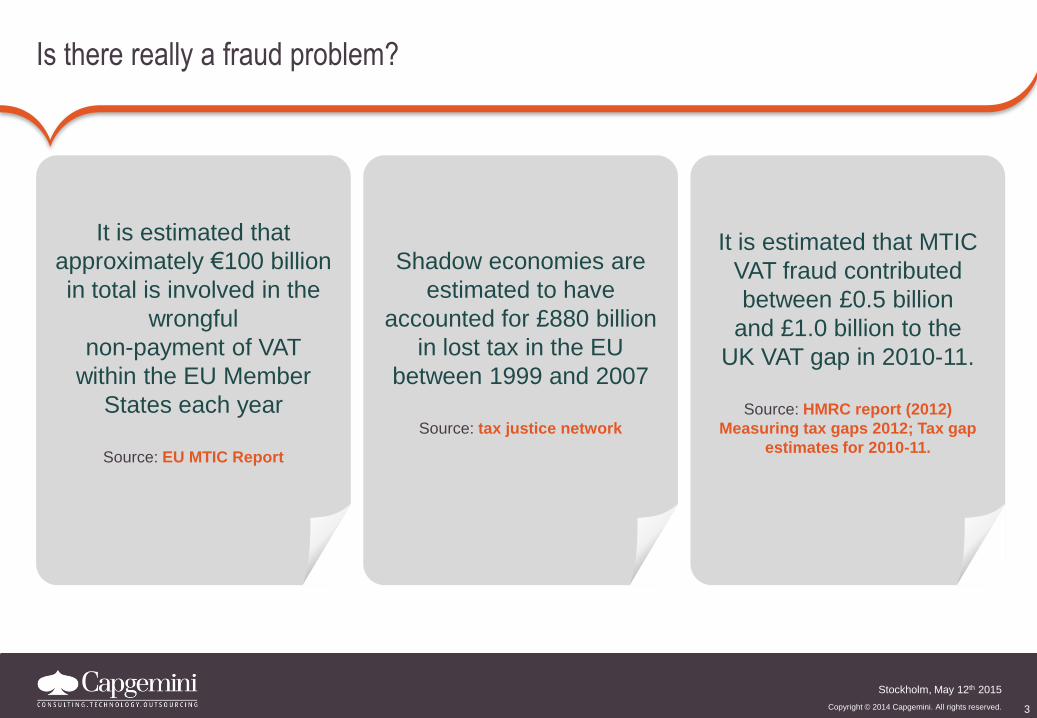

In response, a differentation to type and impact of fraud patterns is needed to determine which counter measures must be applied (and at different point of the business process)

5

Opportunistic Premeditative

Average Insurance

Fraud

Criminal Offender Organised

Crime

High

Volume/

Low Loss

Low

Volume

/High

Loss

Systemic Game

Playing Opportunistic

Taxpayer

Segment

Fraud

Type

Anomaly detection

Predictive Modelling

Social Network Analysis

Text mining

Database Searching

Business rules

Complexty of Fraudulent patterns

6 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

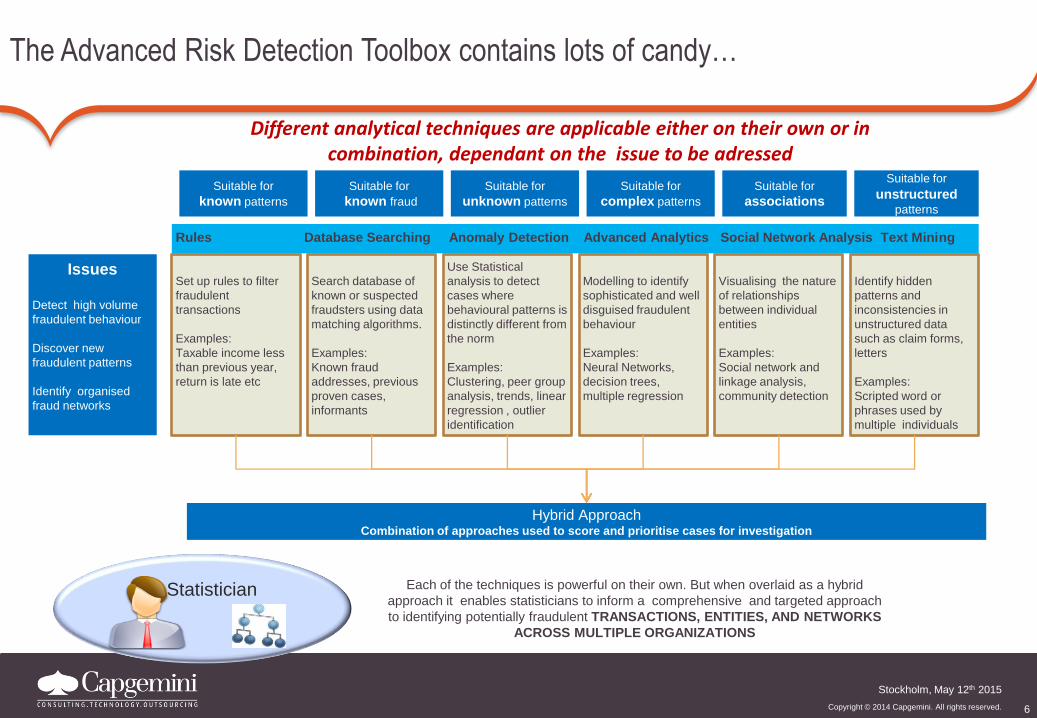

6

Issues

Detect high volume

fraudulent behaviour

Discover new

fraudulent patterns

Identify organised

fraud networks

Set up rules to filter

fraudulent

transactions

Examples:

Taxable income less

than previous year,

return is late etc

Search database of

known or suspected

fraudsters using data

matching algorithms.

Examples:

Known fraud

addresses, previous

proven cases,

informants

Use Statistical

analysis to detect

cases where

behavioural patterns is

distinctly different from

the norm

Examples:

Clustering, peer group

analysis, trends, linear

regression , outlier

identification

Modelling to identify

sophisticated and well

disguised fraudulent

behaviour

Examples:

Neural Networks,

decision trees,

multiple regression

Visualising the nature

of relationships

between individual

entities

Examples:

Social network and

linkage analysis,

community detection

Identify hidden

patterns and

inconsistencies in

unstructured data

such as claim forms,

letters

Examples:

Scripted word or

phrases used by

multiple individuals

Suitable for

known patterns

Suitable for

known fraud

Suitable for

unknown patterns

Suitable for

complex patterns

Suitable for

associations

Suitable for

unstructured patterns

Rules Database Searching Anomaly Detection Advanced Analytics Social Network Analysis Text Mining

Hybrid Approach Combination of approaches used to score and prioritise cases for investigation

Statistician Each of the techniques is powerful on their own. But when overlaid as a hybrid

approach it enables statisticians to inform a comprehensive and targeted approach

to identifying potentially fraudulent TRANSACTIONS, ENTITIES, AND NETWORKS

ACROSS MULTIPLE ORGANIZATIONS

Different analytical techniques are applicable either on their own or in combination, dependant on the issue to be adressed

The Advanced Risk Detection Toolbox contains lots of candy…

7 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

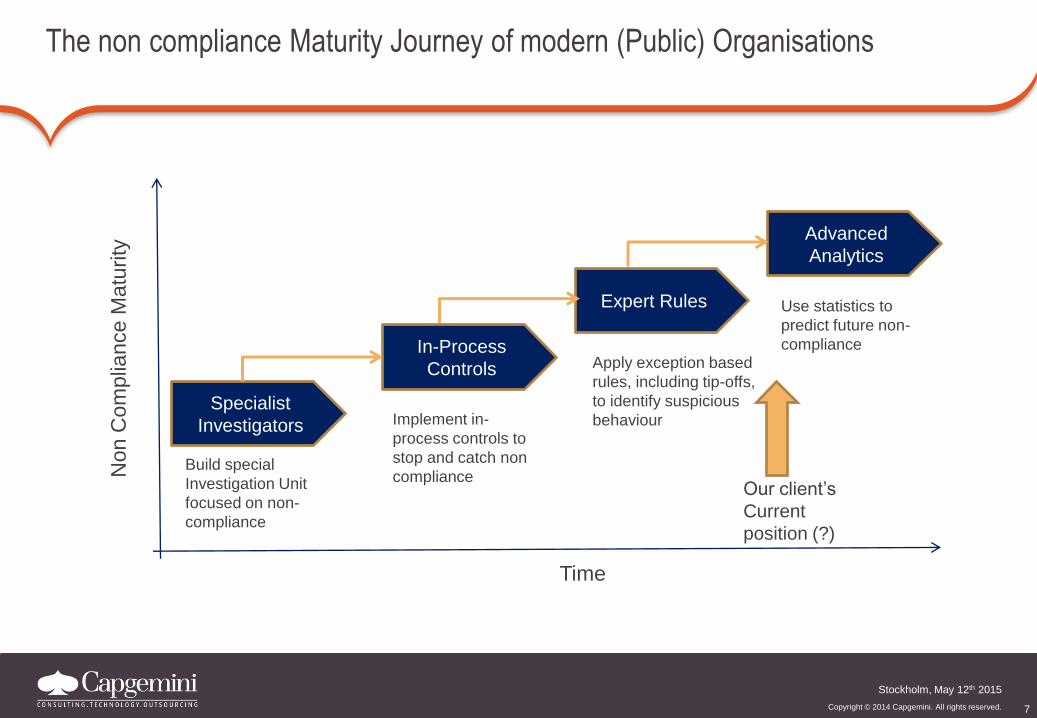

The non compliance Maturity Journey of modern (Public) Organisations

Specialist

Investigators

In-Process

Controls

Expert Rules

Advanced

Analytics

Build special

Investigation Unit

focused on non-

compliance

Implement in-

process controls to

stop and catch non

compliance

Apply exception based

rules, including tip-offs,

to identify suspicious

behaviour

Use statistics to

predict future non-

compliance

Time

Non C

om

plia

nce M

atu

rity

Our client’s

Current

position (?)

8 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

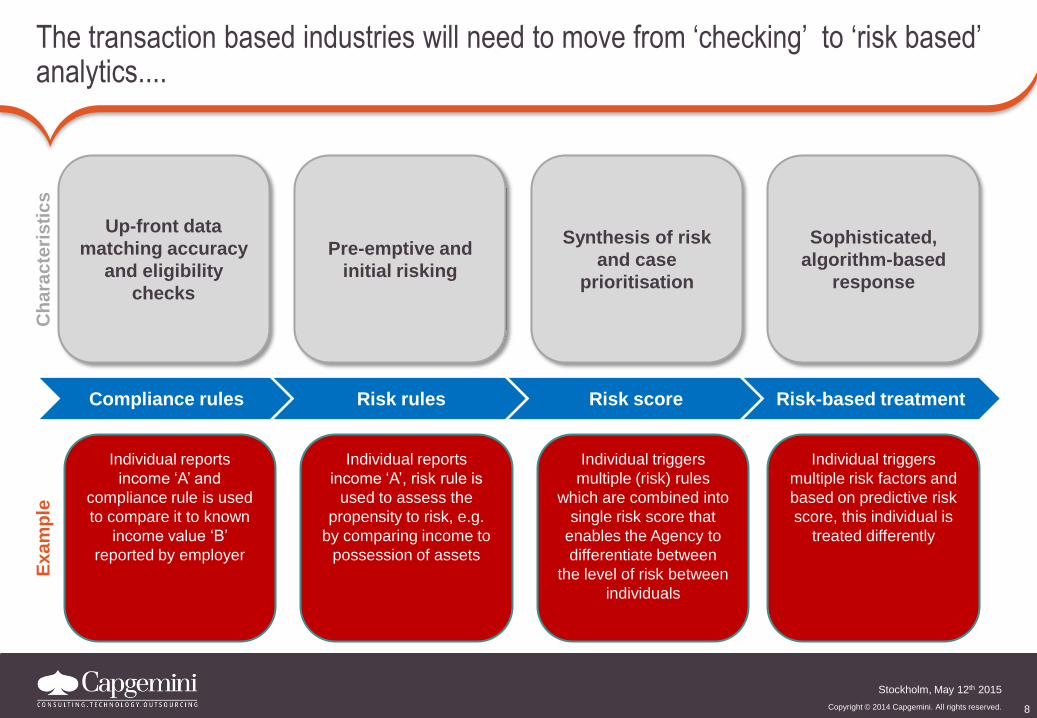

The transaction based industries will need to move from ‘checking’ to ‘risk based’ analytics....

Up-front data

matching accuracy

and eligibility

checks

Pre-emptive and

initial risking

Synthesis of risk

and case

prioritisation

Sophisticated,

algorithm-based

response

Compliance rules Risk rules Risk score Risk-based treatment

Individual reports

income ‘A’ and

compliance rule is used

to compare it to known

income value ‘B’

reported by employer

Individual reports

income ‘A’, risk rule is

used to assess the

propensity to risk, e.g.

by comparing income to

possession of assets

Individual triggers

multiple (risk) rules

which are combined into

single risk score that

enables the Agency to

differentiate between

the level of risk between

individuals

Individual triggers

multiple risk factors and

based on predictive risk

score, this individual is

treated differently

Ch

ara

cte

ris

tic

s

Ex

am

ple

9 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

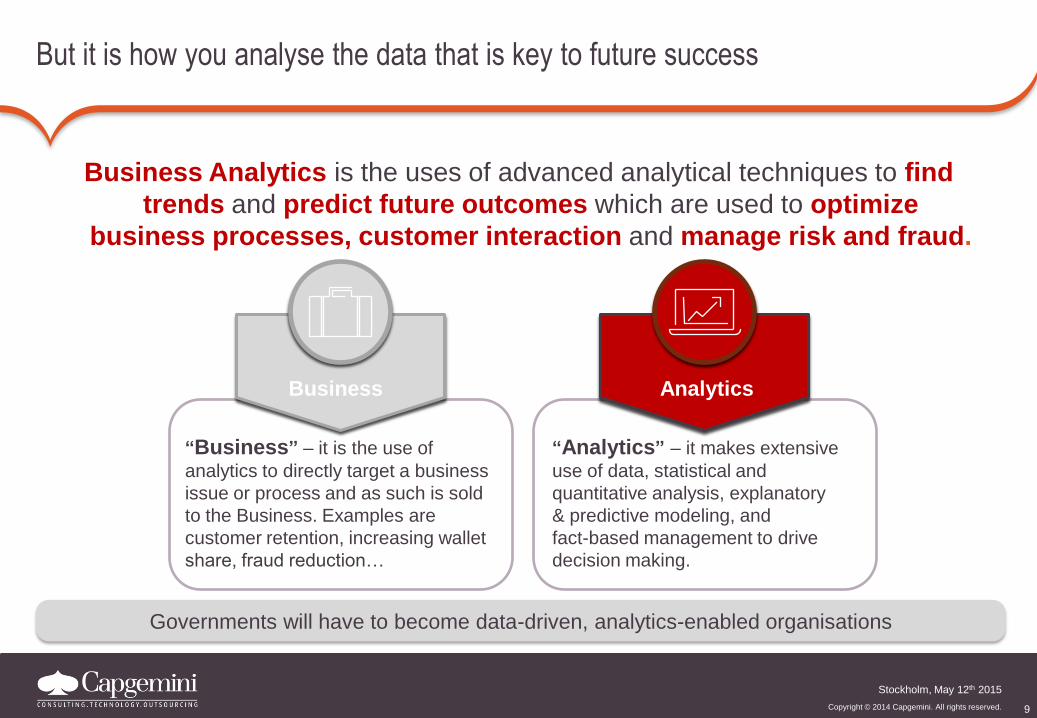

But it is how you analyse the data that is key to future success

Business

“Business” – it is the use of

analytics to directly target a business

issue or process and as such is sold

to the Business. Examples are

customer retention, increasing wallet

share, fraud reduction…

Business Analytics is the uses of advanced analytical techniques to find

trends and predict future outcomes which are used to optimize

business processes, customer interaction and manage risk and fraud.

Analytics

“Analytics” – it makes extensive

use of data, statistical and

quantitative analysis, explanatory

& predictive modeling, and

fact-based management to drive

decision making.

Governments will have to become data-driven, analytics-enabled organisations

10 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

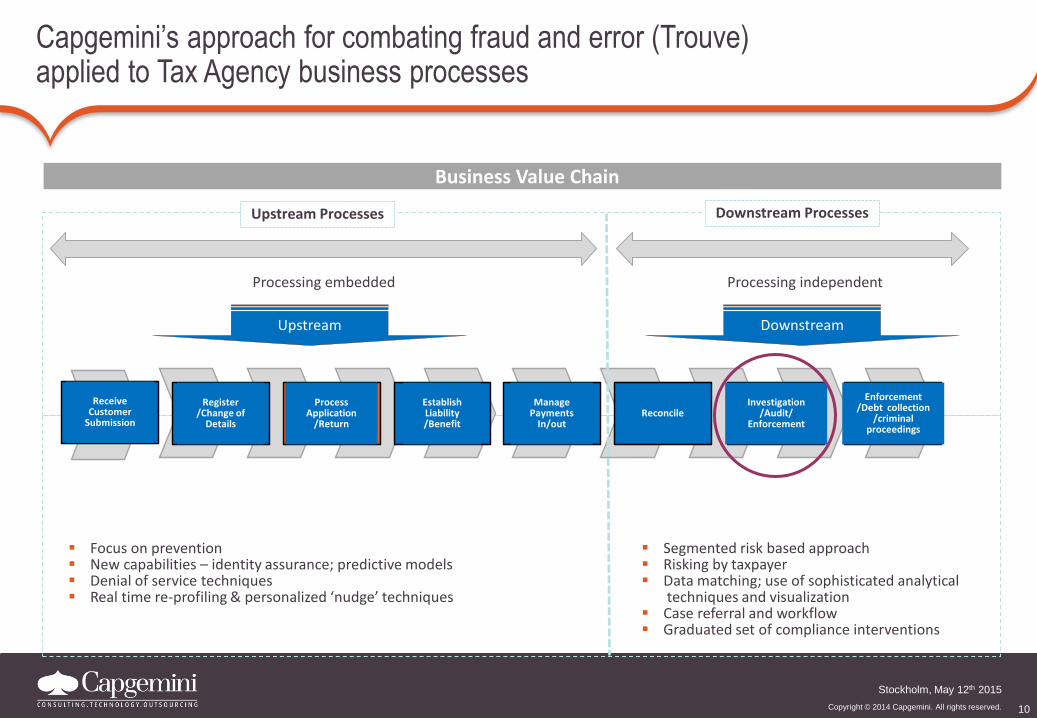

Capgemini’s approach for combating fraud and error (Trouve) applied to Tax Agency business processes

Business Value Chain

Register /Change of

Details

Process Application

/Return

Establish Liability /Benefit

Manage Payments

In/out Reconcile

Investigation /Audit/

Enforcement

Enforcement /Debt collection

/criminal proceedings

Receive Customer

Submission

Downstream Processes Upstream Processes

Upstream Downstream

Processing embedded Processing independent

Segmented risk based approach Risking by taxpayer Data matching; use of sophisticated analytical techniques and visualization Case referral and workflow Graduated set of compliance interventions

Focus on prevention New capabilities – identity assurance; predictive models Denial of service techniques Real time re-profiling & personalized ‘nudge’ techniques

11 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

B

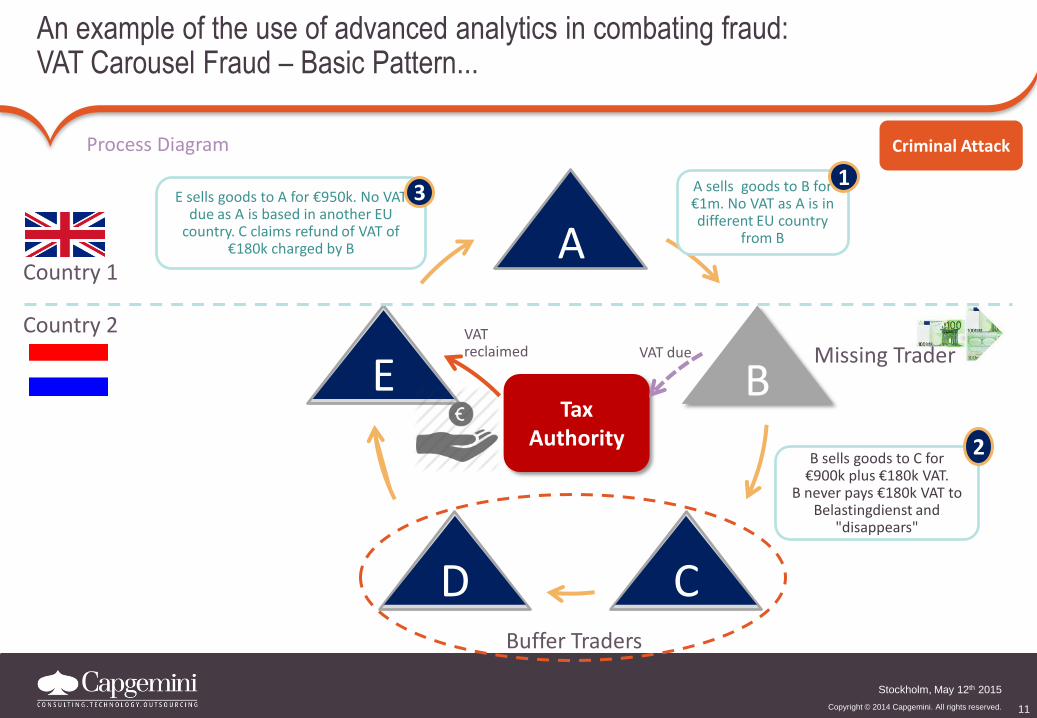

An example of the use of advanced analytics in combating fraud: VAT Carousel Fraud – Basic Pattern...

Process Diagram

A

C C D D

E E

Country 1

Country 2

Tax Authority

VAT due VAT reclaimed

Buffer Traders

Missing Trader

Criminal Attack

A sells goods to B for €1m. No VAT as A is in different EU country

from B

E sells goods to A for €950k. No VAT due as A is based in another EU

country. C claims refund of VAT of €180k charged by B

1

B sells goods to C for €900k plus €180k VAT.

B never pays €180k VAT to Belastingdienst and

"disappears"

2

3

12 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

VAT Carousel Fraud – Presented Pattern

12

13 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

VAT Carousel Fraud – A network after investigation

13

14 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

VAT Carousel Fraud – Getting the picture…

14

15 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

15

Then: moving from Investigating networks…

16 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

..... To event oriented risk assessment (predictive analytics)

16

Am

ou

nt

2 - 4 months Current

situation

SAS Fraude Framework

Preventive

First

verification

First ICA Tax Return

Payment

Subject Time

17 Copyright © 2014 Capgemini. All rights reserved.

Stockholm, May 12th 2015

Results: Breaking News! - Revolution within Tax Agency in combating fraud

17

Secretary of State for the Treasury stated in parliament 8 october 2014: “there is a small revolution going on, apllying data-anlysis and automated profiling”

The information contained in this presentation is proprietary.

Copyright © 2014 Capgemini. All rights reserved.

Rightshore® is a trademark belonging to Capgemini.

www.capgemini.com/bim

About Capgemini

With more than 130,000 people in over 40 countries, Capgemini

is one of the world's foremost providers of consulting, technology

and outsourcing services. The Group reported 2013 global

revenues of EUR 10.1 billion.

Together with its clients, Capgemini creates and delivers

business and technology solutions that fit their needs and drive

the results they want. A deeply multicultural organization,

Capgemini has developed its own way of working, the

Collaborative Business Experience™, and draws on Rightshore®,

its worldwide delivery model.