Embed Size (px)

Citation preview

How FinTech is Disrupting &

Partnering with our Industry

…a story in three parts.

- Mark Zmarzly, Founder & CEO of

2

Our Changing

Industry

11+ Years working with 100s

of Banks & CUs

@BankMarketing, ABA, BAI,

JD Power, Stonier

I saw the change as more

than just a move to Digital

Hip Pocket/Money33

4

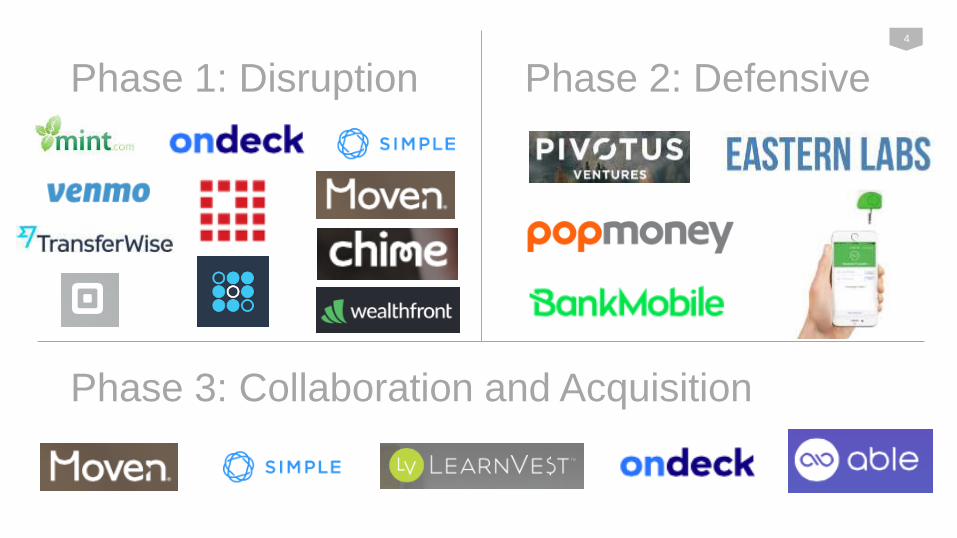

Phase 1: Disruption Phase 2: Defensive

Phase 3: Collaboration and Acquisition

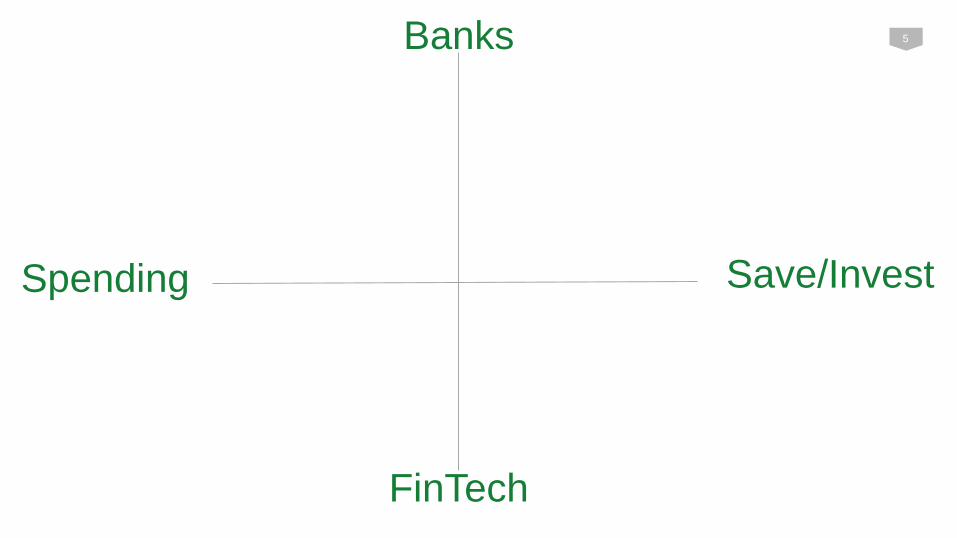

Banks

Spending Save/Invest

FinTech

5

6Banks

Spending

FinTech

Save/Invest

6

Natural Pairings are Happening in FinTech

7

“Northwestern Mutual wanted to be at the center of their clients’ financial lives,” chief technology officer Karl Gouverneur. “Are my kids going to buy life insurance from a person? I don’t think so. I think my son will be allergic to that type of interaction.”

Northwestern Mutual + LearnVest

Natural Pairings are Happening in FinTech

8

Affirm + Sweep

“Max Levchin, co-founder and CEO of Affirm, acknowledged that users will most likely never be using Affirm’s loan products on a daily basis. So, the company wants to expand into services outside of lending, with the goal that users would use these services more often than they use Affirm’s loan product – maybe even on a daily basis.”

First: Peer-to-Peer Comparisons

Second: Mobile & Millennial

Anti-Status Quo: We attacked the

big banks via Kickstarter.

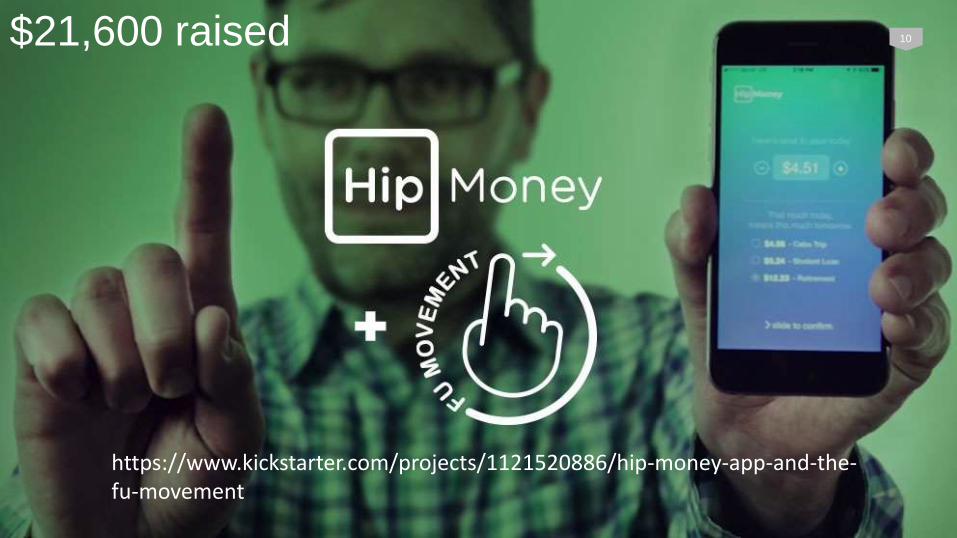

Hip Pocket/Money99

https://www.kickstarter.com/projects/1121520886/hip-money-app-and-the-fu-movement

$21,600 raised 10

11

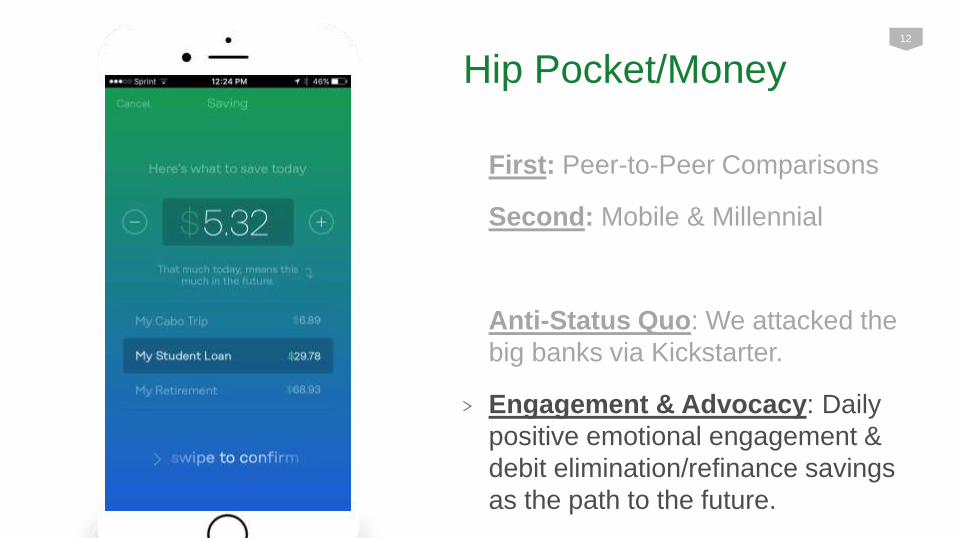

First: Peer-to-Peer Comparisons

Second: Mobile & Millennial

Anti-Status Quo: We attacked the

big banks via Kickstarter.

Engagement & Advocacy: Daily

positive emotional engagement &

debit elimination/refinance savings

as the path to the future.

Hip Pocket/Money1212

Underneath most effective #FinTech is advocacy!

13

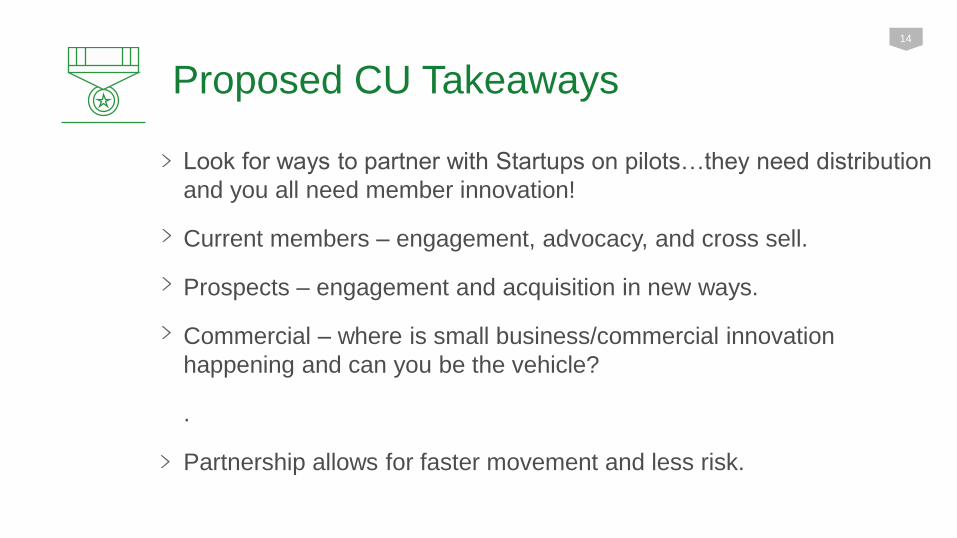

Proposed CU Takeaways

Look for ways to partner with Startups on pilots…they need distribution

and you all need member innovation!

Current members – engagement, advocacy, and cross sell.

Prospects – engagement and acquisition in new ways.

Commercial – where is small business/commercial innovation

happening and can you be the vehicle?

.

Partnership allows for faster movement and less risk.

14

15

In Summary

1 2

How does this new

FinTech collaboration

movement fit with your

current strategies?

How will your credit union

adapt to technology and

change in the future?

- What’s the future of

member engagement?

15

Questions?

Some Resources:

Goldman Sachs: We're in the 'second wave' of fintech: http://www.businessinsider.com/goldman-sachs-global-head-of-fintech-

on-the-three-waves-of-fintech-development-2016-9

Fintech's 'Third Wave' Is Coming, And It Will Change Everything: http://www.forbes.com/sites/chrismyers/2016/10/03/fintechs-

third-wave-is-coming-and-it-will-change-everything/2/#61461ba138e7

Mark Zmarzly 402-802-1005