Embed Size (px)

Citation preview

www.ovum.com

© Copyright Ovum 2015. All rights reserved.

Telco/OTT partnerships for affordable Internet access

Matthew Howett, Practice Leader, Regulation & Policy

16 April 2015, Victoria Falls, Zimbabwe

2© Copyright Ovum 2015. All rights reserved.

The rise of the OTT

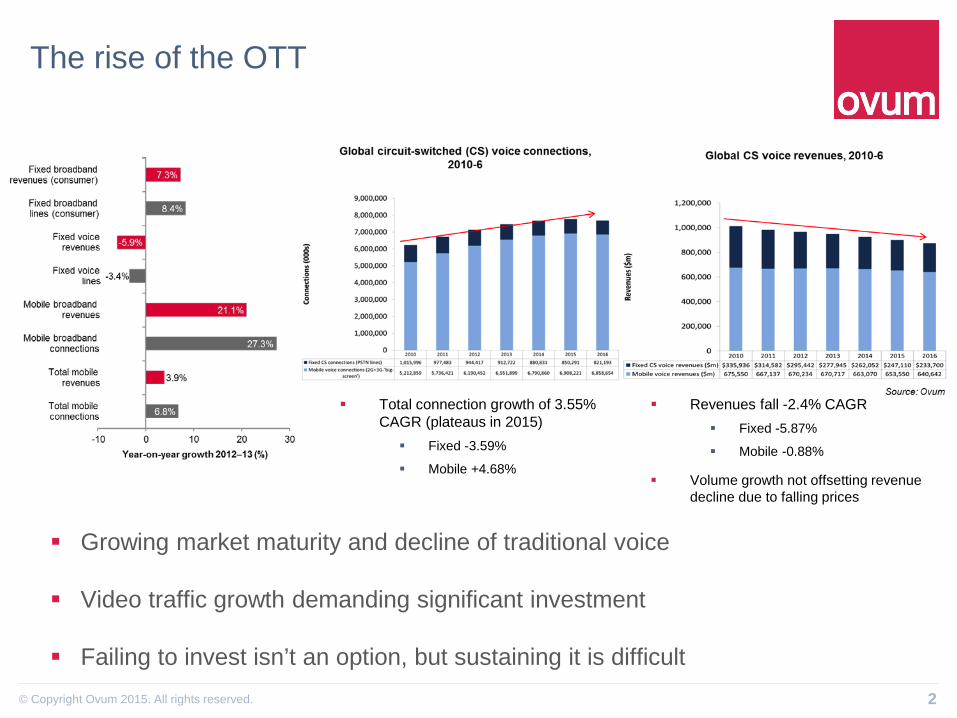

Growing market maturity and decline of traditional voice

Video traffic growth demanding significant investment

Failing to invest isn’t an option, but sustaining it is difficult

Total connection growth of 3.55% CAGR (plateaus in 2015) Fixed -3.59%

Mobile +4.68%

Revenues fall -2.4% CAGR Fixed -5.87%

Mobile -0.88%

Volume growth not offsetting revenue decline due to falling prices

3© Copyright Ovum 2015. All rights reserved.

The impact of OTT on telcos

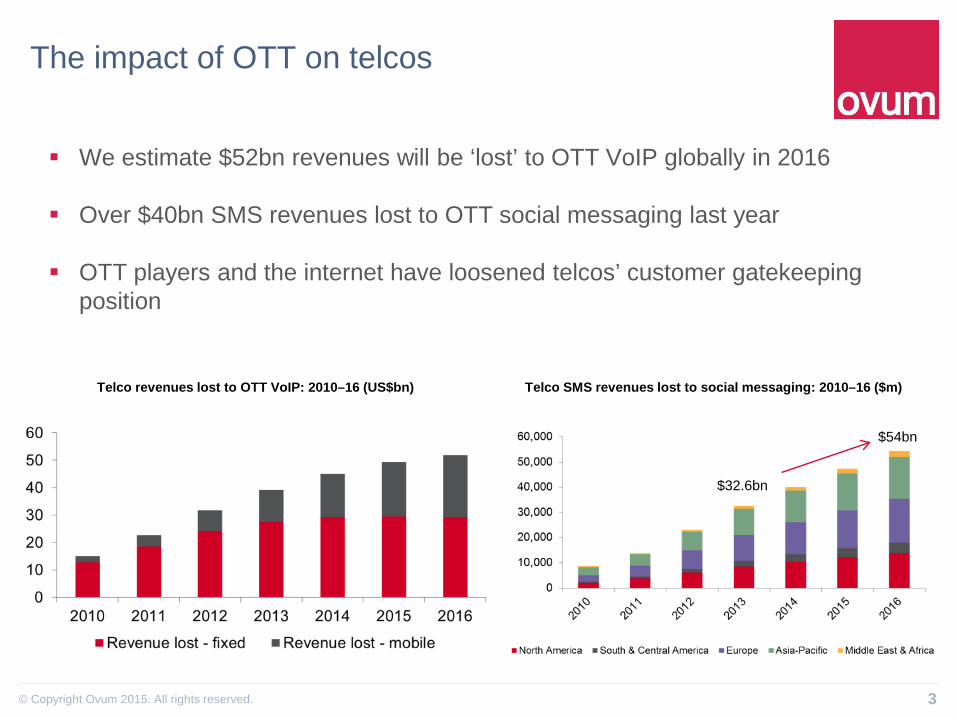

We estimate $52bn revenues will be ‘lost’ to OTT VoIP globally in 2016

Over $40bn SMS revenues lost to OTT social messaging last year

OTT players and the internet have loosened telcos’ customer gatekeeping position

Telco SMS revenues lost to social messaging: 2010–16 ($m) Telco revenues lost to OTT VoIP: 2010–16 (US$bn)

$32.6bn

$54bn

4© Copyright Ovum 2015. All rights reserved.

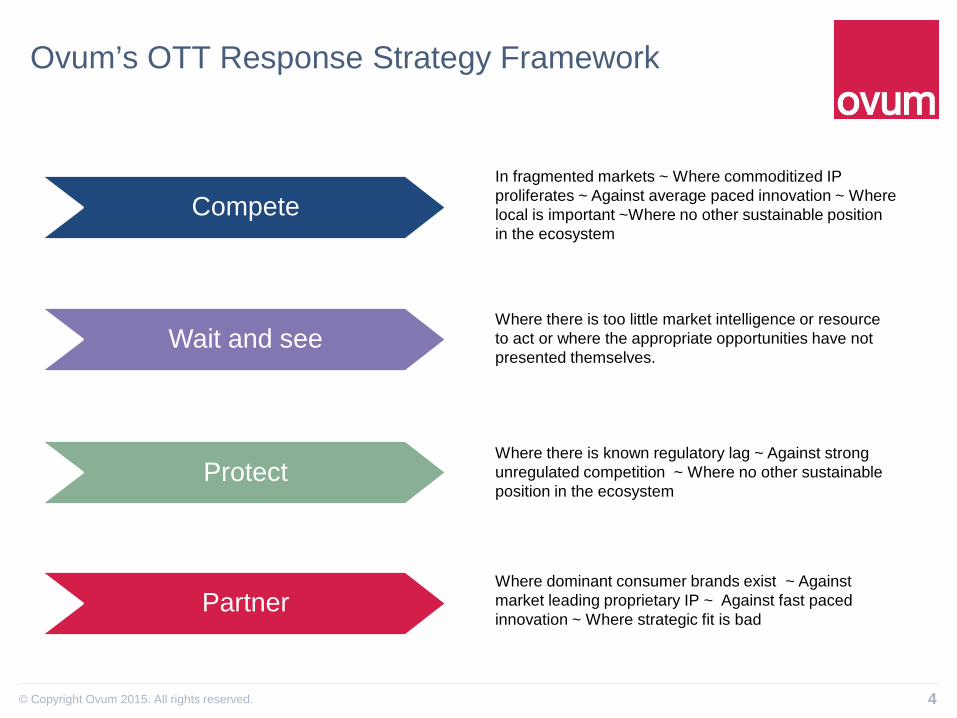

Partner

Compete

Protect

Wait and see

In fragmented markets ~ Where commoditized IP proliferates ~ Against average paced innovation ~ Where local is important ~Where no other sustainable position in the ecosystem

Where dominant consumer brands exist ~ Against market leading proprietary IP ~ Against fast paced innovation ~ Where strategic fit is bad

Where there is known regulatory lag ~ Against strong unregulated competition ~ Where no other sustainable position in the ecosystem

Where there is too little market intelligence or resource to act or where the appropriate opportunities have not presented themselves.

Ovum’s OTT Response Strategy Framework

5© Copyright Ovum 2015. All rights reserved.

Type 1: Unilateral bundling• One party uses the other brand simply as a marketing tool• Often no relationship between the two companies• No direct investment

Type 2: Marketing• Main purpose is to increase the marketing of each product• Some level of cooperation between the two companies• None-to-small investment

Type 3: Revenue agreement• Either commercial agreement or revenue sharing• Usually co-branded products• Small-to-mid investment

Type 4: Joint venture / Strategic Partnership• From an announced strategic agreement between the two parties up to

the creation of an independent joint-venture company• Mid-to-significant investment

We have identified 4 types of partnership

6© Copyright Ovum 2015. All rights reserved.

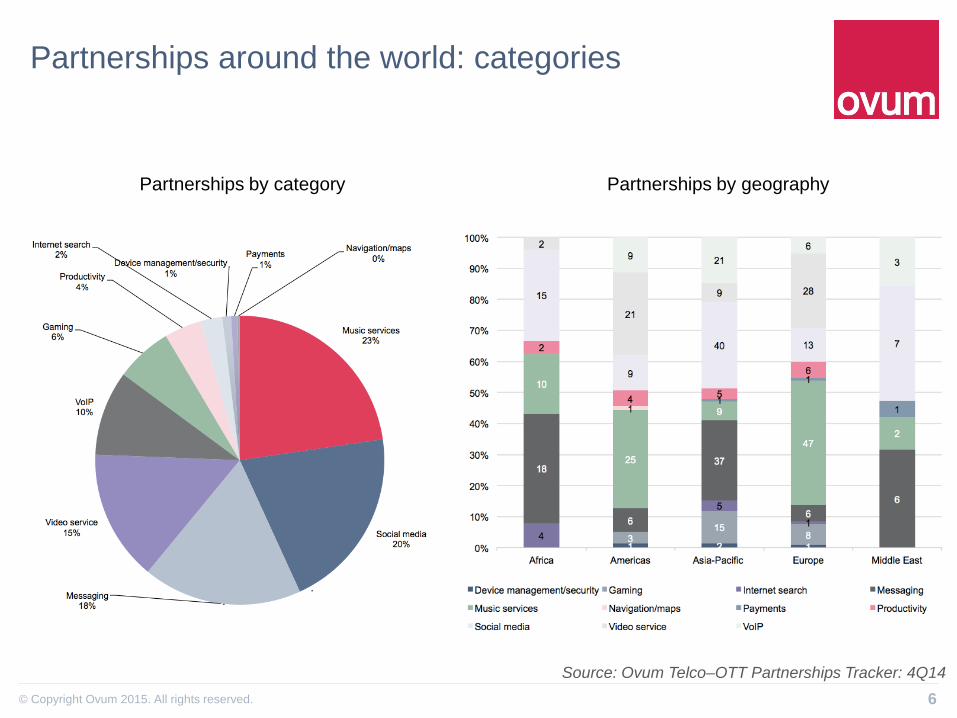

Partnerships around the world: categories

Partnerships by category Partnerships by geography

Source: Ovum Telco–OTT Partnerships Tracker: 4Q14

7© Copyright Ovum 2015. All rights reserved.

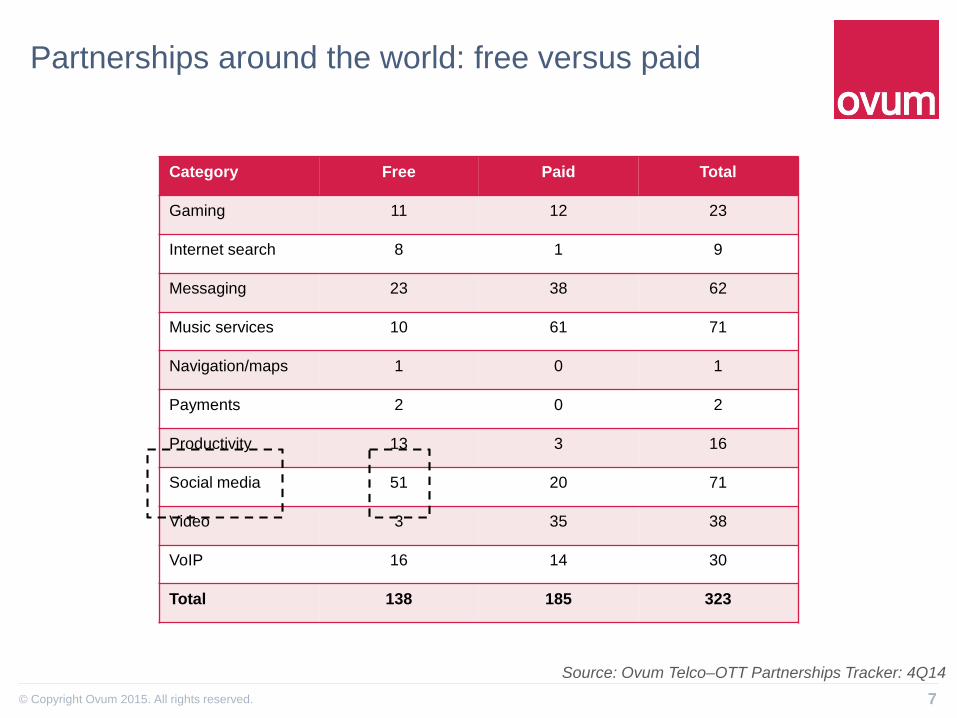

Partnerships around the world: free versus paid

Category Free Paid Total

Gaming 11 12 23

Internet search 8 1 9

Messaging 23 38 62

Music services 10 61 71

Navigation/maps 1 0 1

Payments 2 0 2

Productivity 13 3 16

Social media 51 20 71

Video 3 35 38

VoIP 16 14 30

Total 138 185 323

Source: Ovum Telco–OTT Partnerships Tracker: 4Q14

8© Copyright Ovum 2015. All rights reserved.

internet.org is probably the best known example of a partnership offering internet access and services

India (Feb 2015)Reliance customers in six Indian states (Tamil Nadu, Mahararashtra, Andhra Pradesh, Gujarat, Kerala, and Telangana) now have access to more than three dozen services ranging from news, maternal health, travel, local jobs, sports, communication, and local government information.

Tanzania (Oct 2014)Provides people with free access to basic internet services so they can browse useful health, education, finance, employment, communication and local information and services without data charges.

Colombia (Jan 2015)First time the Internet.org app is available in Latin America, and it’s also the first to include government services as part of the other free basic services in the areas of education, health, communication, jobs, finance, and local information.

Zambia (Jul 2014)Airtel customers in Zambia were the first to access services in the Internet.org Android app, at internet.org, or within the Facebook for Android app.

Kenya (Nov 2014)

Ghana (Jan 2015)The fifth country to connect with Internet.org, after Zambia, Tanzania, Kenya and Colombia. People use the internet for free to find jobs, read books, and stay connected.

9© Copyright Ovum 2015. All rights reserved.

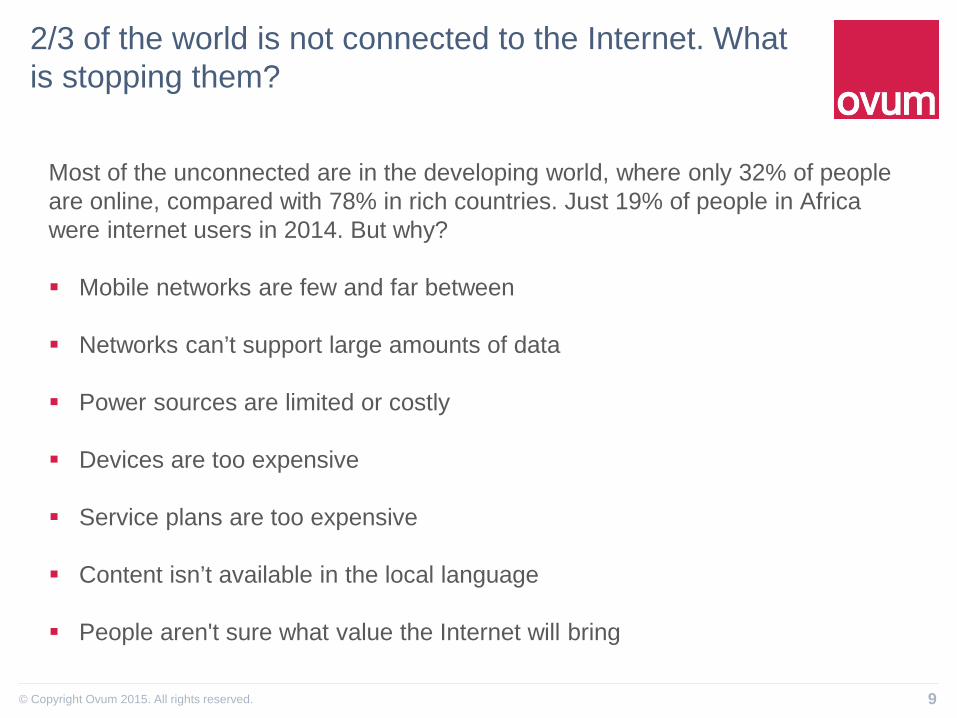

2/3 of the world is not connected to the Internet. What is stopping them?

Most of the unconnected are in the developing world, where only 32% of people are online, compared with 78% in rich countries. Just 19% of people in Africa were internet users in 2014. But why?

Mobile networks are few and far between

Networks can’t support large amounts of data

Power sources are limited or costly

Devices are too expensive

Service plans are too expensive

Content isn’t available in the local language

People aren't sure what value the Internet will bring

10© Copyright Ovum 2015. All rights reserved.

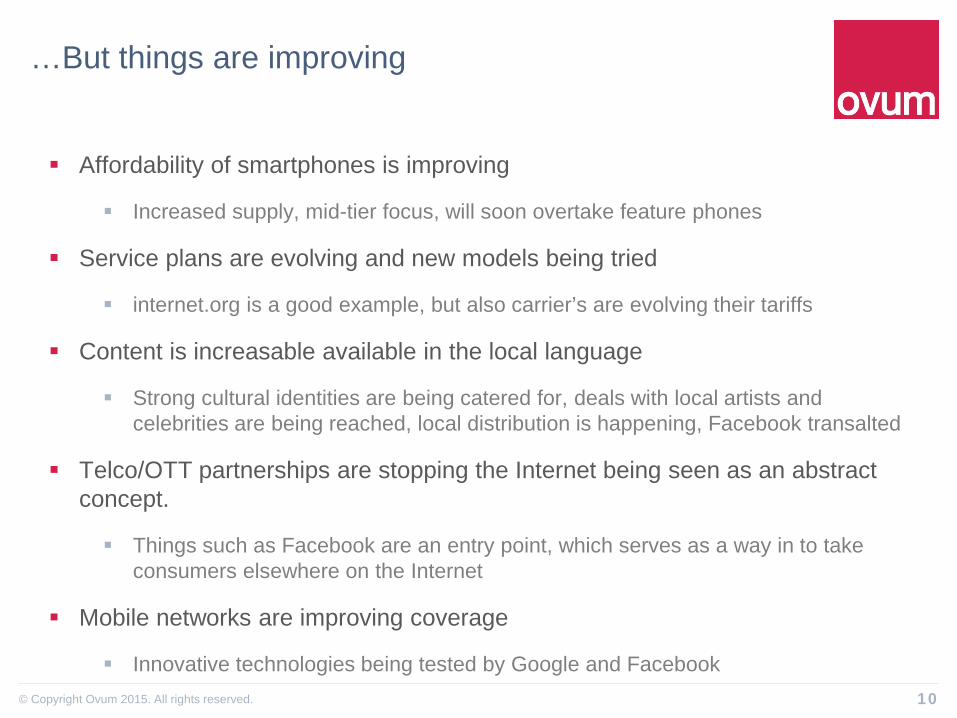

…But things are improving

Affordability of smartphones is improving

Increased supply, mid-tier focus, will soon overtake feature phones

Service plans are evolving and new models being tried

internet.org is a good example, but also carrier’s are evolving their tariffs

Content is increasable available in the local language

Strong cultural identities are being catered for, deals with local artists and celebrities are being reached, local distribution is happening, Facebook transalted

Telco/OTT partnerships are stopping the Internet being seen as an abstract concept.

Things such as Facebook are an entry point, which serves as a way in to take consumers elsewhere on the Internet

Mobile networks are improving coverage

Innovative technologies being tested by Google and Facebook

11© Copyright Ovum 2015. All rights reserved.

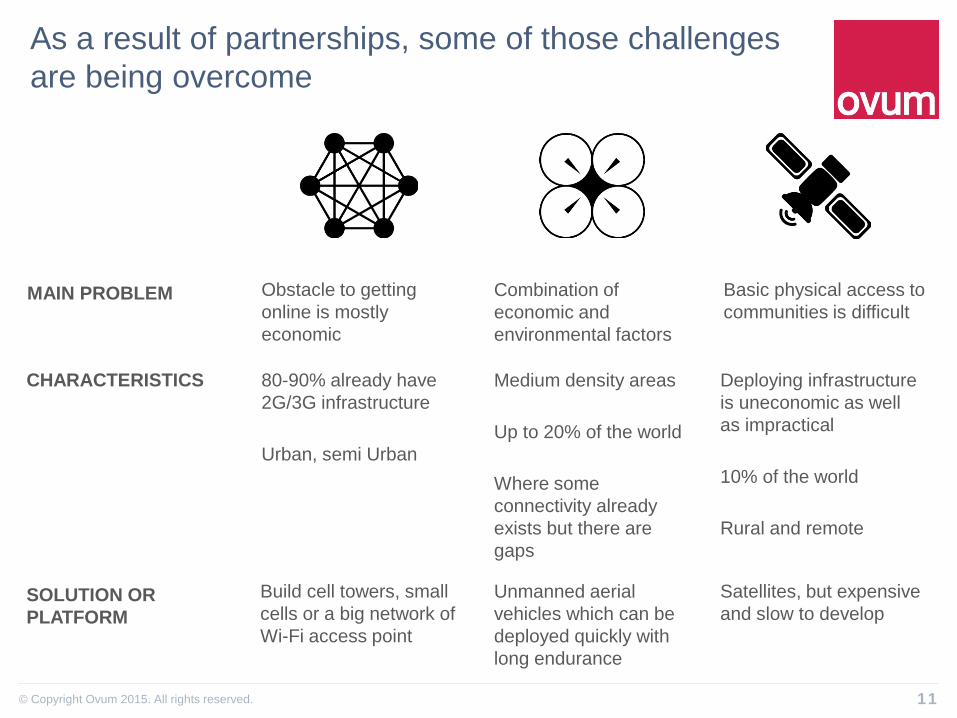

As a result of partnerships, some of those challenges are being overcome

MAIN PROBLEM

CHARACTERISTICS

SOLUTION OR PLATFORM

Obstacle to getting online is mostly economic

80-90% already have 2G/3G infrastructure

Urban, semi Urban

Build cell towers, small cells or a big network of Wi-Fi access point

Basic physical access to communities is difficult

Deploying infrastructure is uneconomic as well as impractical

10% of the world

Rural and remote

Satellites, but expensive and slow to develop

Medium density areas

Up to 20% of the world

Where some connectivity already exists but there are gaps

Unmanned aerial vehicles which can be deployed quickly with long endurance

Combination of economic and environmental factors

12© Copyright Ovum 2015. All rights reserved.

But questions remain…

Are the apps included in internet.org the right ones?

They are mostly low bandwidth and not contentious, not things such as YouTube, VoIP within Facebook and WhatsApp which would present real challenges for the network. This risks creating a further digital divide.

Who eventually owns the relationship with the end-user?

In developed markets, OTTs have stolen the gatekeeping position of the telco. internet.org believe it should be those deploying the network to become the face

Does regulation prohibit Google and Facebook plans for balloons and drones?

Some countries heavily restrict the use of such aircraft and time-wise these are still some time away

Let’s not forget the importance

160m+ jobs, reduced child mortality, empowerment