Embed Size (px)

DESCRIPTION

Presented by Informa and Ovum. Opportunities and threats for Telcos taking them beyond 2020. For more information on the event please visit: http://bit.ly/1AKUIwe

Citation preview

© Copyright Ovum. All rights reserved. Ovum is an Informa business. 1

Growth Opportunities for the 2020 Telecoms Service Provider

David Kennedy

Ovum 2020 Summit

30 October 2014

© Copyright Ovum. All rights reserved. Ovum is an Informa business. 2

We are experiencing a major structural change

Source: Perez, C. “Technological revolutions and Financial Capital”, 2002

© Copyright Ovum. All rights reserved. Ovum is an Informa business. 3

GFC and demand side change

Recession? Yes, but also some permanent changes.

in consumer behaviour.

In economic structure.

Implications for consumption patterns: “thrifty not frugal”.

Households are saving more, and this will not change for many years. Enterprises are seeking value for money.

A smaller revenue pie will accelerate disruption and economic restructuring.

This is the new normal for the next decade.

There’s still a market there! (but telecommunications carriage is the new utility).

© Copyright Ovum. All rights reserved. Ovum is an Informa business. 4

New pressure on the supply-side economy New ways of doing things are needed:

New institutional arrangements are required to fully exploit new technologies.

Major verticals impacted so far: media and advertising, transport & logistics, retail

Health, education, finance and government are in the pipeline for disruption.

Long term change in service industry structure: true “convergence”

Drive for cost control and productivity.

“The valley of death”: things will get worse before they get better.

This is disruptive, and favours new entrants: Sensis vs Google, Uber vs taxis.

Legacy revenues

Digital revenues

© Copyright Ovum. All rights reserved. Ovum is an Informa business. 5

A more complex telecommunications value chain

Source: Ovum SMART = Services, Management, Applications, Relationships, and Technology LEAN = Low-cost Enablers of Agnostic Networks OEM = Original equipment manufacturer (system vendor); SI = system integrator.

© Copyright Ovum. All rights reserved. Ovum is an Informa business. 6

SMART players versus LEAN operators In 2020, there will be two main player types in the broader market of

which telecoms will be part:

1. LEAN operators – focused on infrastructure ownership and wholesaling services to other operators who serve retail customers (possibly including their own retail arms).

2. SMART players – operators and other players who offer platforms for device management, technical support, backup/security/storage etc., for the whole home or business.

But these are limit cases:

Many operators will combine aspects of SMART and LEAN through commercial functional separation models.

Many operators will instinctively flock towards SMART strategies, but there will be a lot of competition in all categories leading to more consolidation, possibly global consolidation.

© Copyright Ovum. All rights reserved. Ovum is an Informa business. 7

SMART players are part of an ecosystem Building a successful SMART platform means exposing operator assets

– the network and value-added capabilities – to third parties.

This is done through carefully controlled, secured and monetised APIs and other interfaces.

The primary benefit of this process is internal exposure of APIs, then external exposure to partners.

It has two major benefits, for both telco and other SMART players:

Outsources a measure of innovation along with the risk.

Enables a much better experience for consumers and content partners when using “over the top” content – a key value generator.

Overall, it turns the network into an asset that multiple parties can innovate on, not just the operator:

An ecosystem, not just a service.

© Copyright Ovum. All rights reserved. Ovum is an Informa business. 8

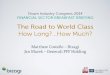

Maturity & sophis.ca.on

of ICT capabili.es

Lower

Higher

Time

Open cloud-‐based pla;orms

• opera/onal scale • focused R&D & skills • mul/-‐tenancy • business con/nuity • itera/ve evolu/on • SOA & open APIs • social & mobile • Internet-‐age security • user self service • usage-‐based charging • vendor ecosystems

Cloud pla;orm innova.on edge

Tradi.onal internal IT capabili.es • legacy complexity

• diversity & fragmenta/on • budget cuts • ageing assets • staff turnover & skill shortages • project failures

Open platforms generate both scale and innovation

Aim to get big, get connected

© Copyright Ovum. All rights reserved. Ovum is an Informa business. 9

M2M service will give way to an IoT ecosystem

Source: Ovum

Open platforms shift the locus of innovation up to the SMART layer, opening the market to third-party innovation and accelerating growth.

© Copyright Ovum. All rights reserved. Ovum is an Informa business. 10

Resultant issues in telecommunications operator strategy Core service revenues are already being disrupted by OTT players and

fixed mobile substitution.

Revenue loss of $13.9 billion in 2011 and $54 billion in 2016 to social messaging, revenue loss of $22 billion in 2011 and $52 billion in 2016 to OTT VoIP.

Any new opportunities will arise from incremental substitution of traditional service sector offerings by digital platforms and applications.

Shift away from vertical integration and towards horizontal integration.

Network and platform sharing for scale.

Outsourcing of network management for cost savings and optimisation.

Growing separation between infrastructure provision (LEAN) and platform/application (SMART) provision.

© Copyright Ovum. All rights reserved. Ovum is an Informa business. 11

Telcos need to be very clear about which strategy they want to pursue, and where

There are differences between the SMART and LEAN models, in terms of:

The skill set required.

The investments that need to be made.

The relationships between platform vendors, device vendors, content providers.

Potential clashes with regulators.

Decisions need to be made now in order to start down one of these two paths:

Investment, acquisition, and partnering strategies.

The key issue: positioning within the emerging ecosystem for innovation.

A global perspective is required.

© Copyright Ovum. All rights reserved. Ovum is an Informa business. 12

Thank you