Embed Size (px)

Citation preview

Important Changes to Payroll

Presenter:

Linda Pullan, Head of Payroll Alliance

Peoplesoft Day 1

Agenda

• Apprenticeship levy –avoiding the common errors

• Budget changes to Optional Remuneration Arrangements including salary sacrifice

• Proposed changes to Termination Payments

• Off payroll working in the Public Sector And

• The new Employment Status Tool

2

Apprenticeship Levy

All employers, not just large employers, are potentially liable to pay the Apprenticeship Levy

But only those whose pay bills exceed £3million over the year will pay

This is because there is an Apprenticeship Allowance which is offset against the Levy of £15,000 per annum

However, if your Apprenticeship Levy is less than £15,000 you cannot claim the rest of the Allowance in cash

Less than 2% of UK companies will be liable to pay the Levy this year

Peoplesoft Day 3

Apprenticeship Levy

Commencement date April 2017- first AL calculations made on tax week/month 1’s pay bill

First payment to HMRC was due 19th/22nd May 2017 with monthly PAYE remittance

Apprenticeship Levy is calculated each payday the AL allowance is set as an annual figure

divided into 12 equal amounts across the tax year.

Peoplesoft Day 4

Apprenticeship Levy

What is the Pay bill?

The total annual earnings that attract Class 1(secondary) NIC:- Salary/Wages/Bonuses/Commission and AllowancesPlus:

All BIKs that attract Class 1 (secondary) NICs

Exclude: All BIKs that attract Class 1A NIC PSA’s (Class1B NIC)

Fluctuating Earnings throughout the tax year could mean employers become subject to AL payments i.e. bonuses, overtime, pay increases etc.

Peoplesoft Day 5

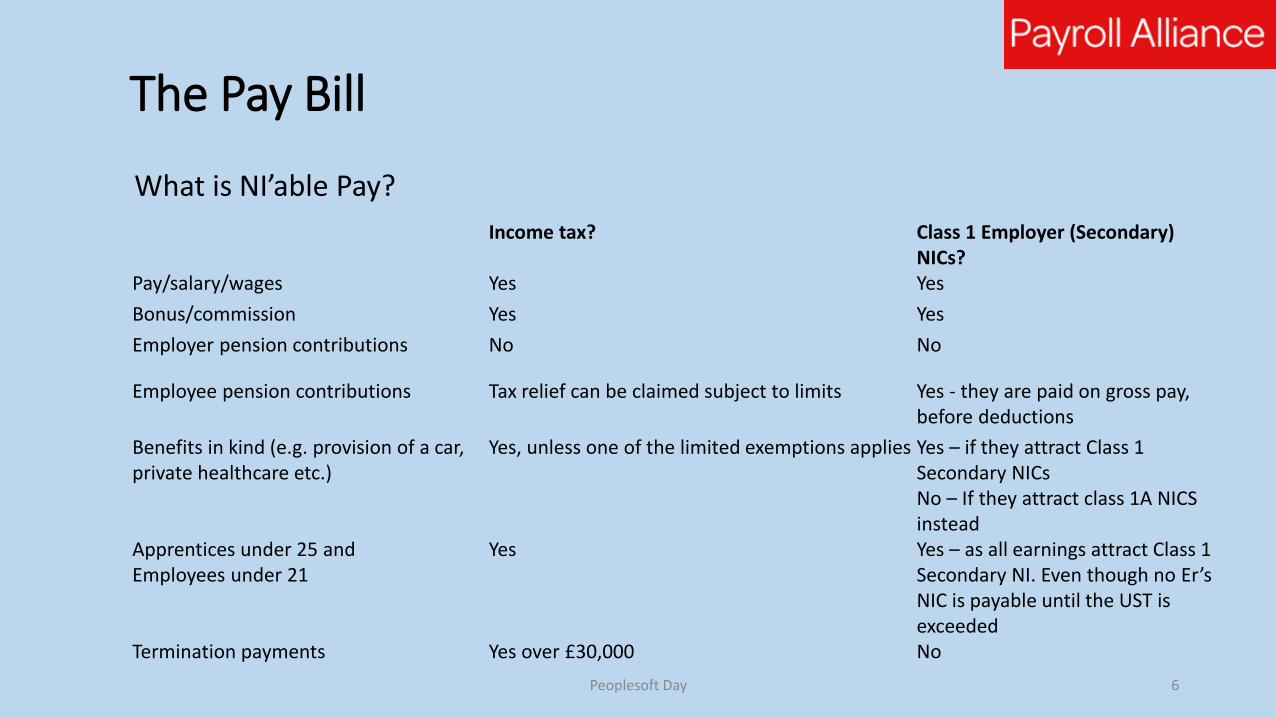

The Pay Bill

Income tax? Class 1 Employer (Secondary) NICs?

Pay/salary/wages Yes Yes

Bonus/commission Yes Yes

Employer pension contributions No No

Employee pension contributions Tax relief can be claimed subject to limits Yes - they are paid on gross pay, before deductions

Benefits in kind (e.g. provision of a car, private healthcare etc.)

Yes, unless one of the limited exemptions applies Yes – if they attract Class 1 Secondary NICsNo – If they attract class 1A NICS instead

Apprentices under 25 and Employees under 21

Yes Yes – as all earnings attract Class 1 Secondary NI. Even though no Er’sNIC is payable until the UST is exceeded

Termination payments Yes over £30,000 No

What is NI’able Pay?

Peoplesoft Day 6

Peoplesoft Day

Apprenticeship Levy

A new group Apprenticeship Levy has been added to the EPS.

These fields should only be completed when an AL payment is due.

oData item 187 – Apprenticeship Levy due year to date (net)

oData item 188 – Tax month

oData item 189 – Annual Apprenticeship Levy allowance amount allocated to that PAYE scheme.

7

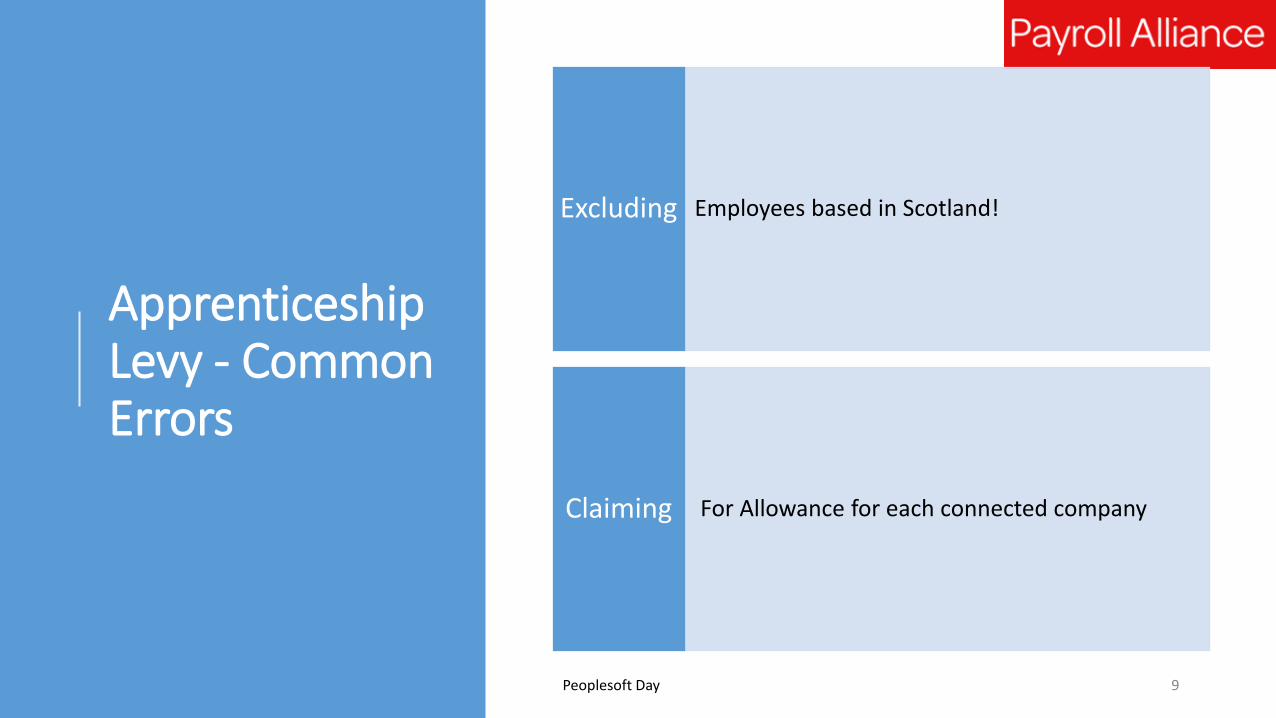

Apprenticeship Levy - Common Errors

Under 21 year old’s and apprentices under 25 in the calculationExcluding

Overseas employees who are subject to Class 1 NICs Excluding

Peoplesoft Day 8

Apprenticeship Levy - Common Errors

Employees based in Scotland! Excluding

For Allowance for each connected companyClaiming

Peoplesoft Day 9

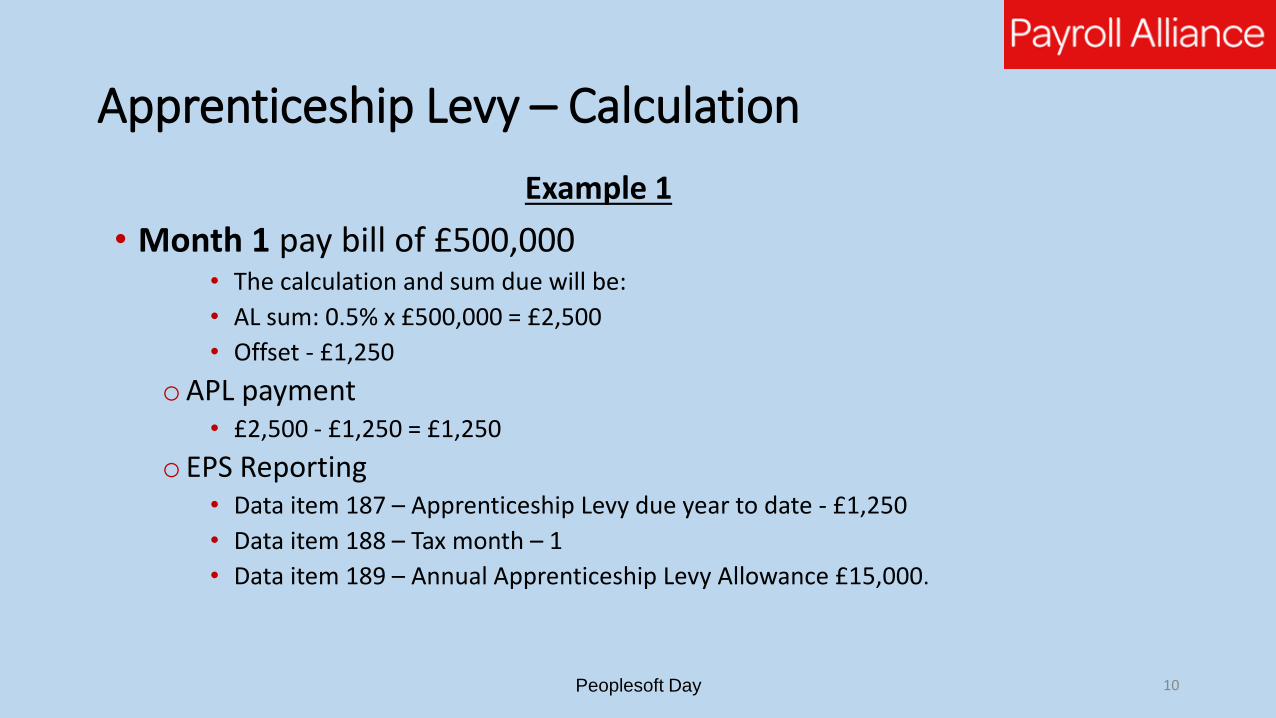

Apprenticeship Levy – Calculation

Example 1

• Month 1 pay bill of £500,000• The calculation and sum due will be:

• AL sum: 0.5% x £500,000 = £2,500

• Offset - £1,250

oAPL payment• £2,500 - £1,250 = £1,250

o EPS Reporting• Data item 187 – Apprenticeship Levy due year to date - £1,250

• Data item 188 – Tax month – 1

• Data item 189 – Annual Apprenticeship Levy Allowance £15,000.

Peoplesoft Day 10

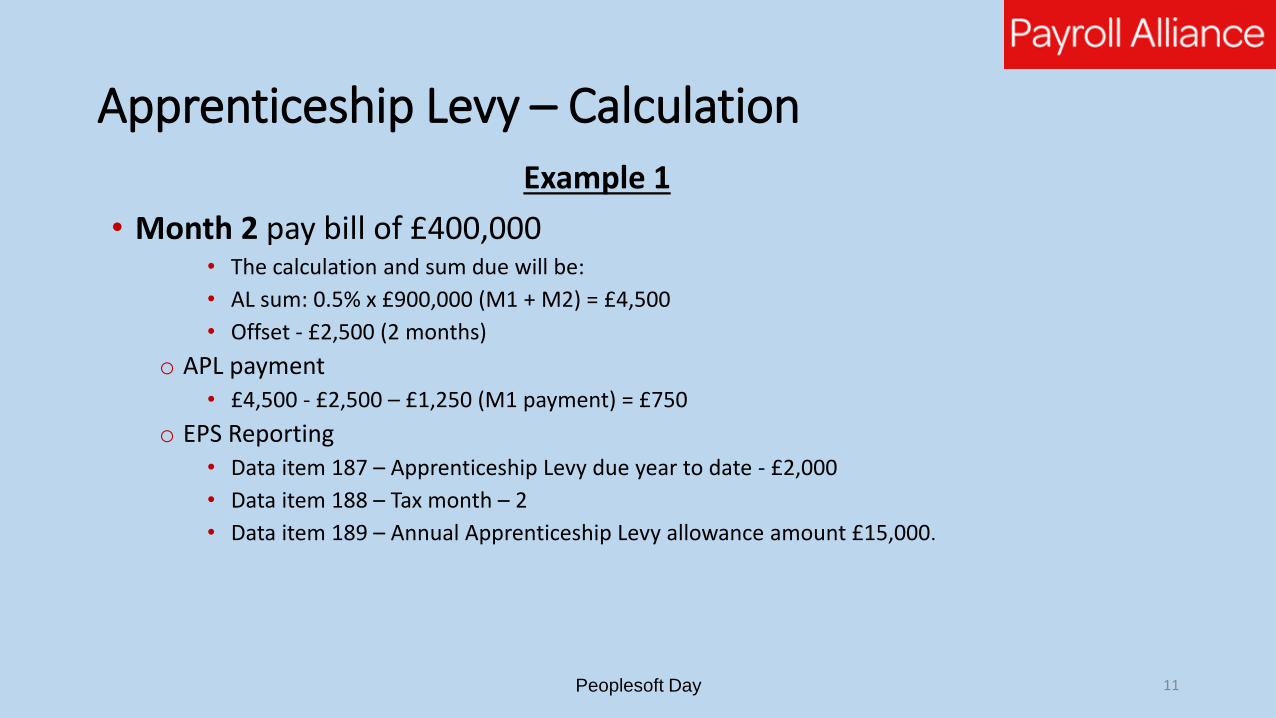

Apprenticeship Levy – Calculation Example 1

• Month 2 pay bill of £400,000• The calculation and sum due will be:

• AL sum: 0.5% x £900,000 (M1 + M2) = £4,500

• Offset - £2,500 (2 months)

o APL payment• £4,500 - £2,500 – £1,250 (M1 payment) = £750

o EPS Reporting• Data item 187 – Apprenticeship Levy due year to date - £2,000

• Data item 188 – Tax month – 2

• Data item 189 – Annual Apprenticeship Levy allowance amount £15,000.

Peoplesoft Day 11

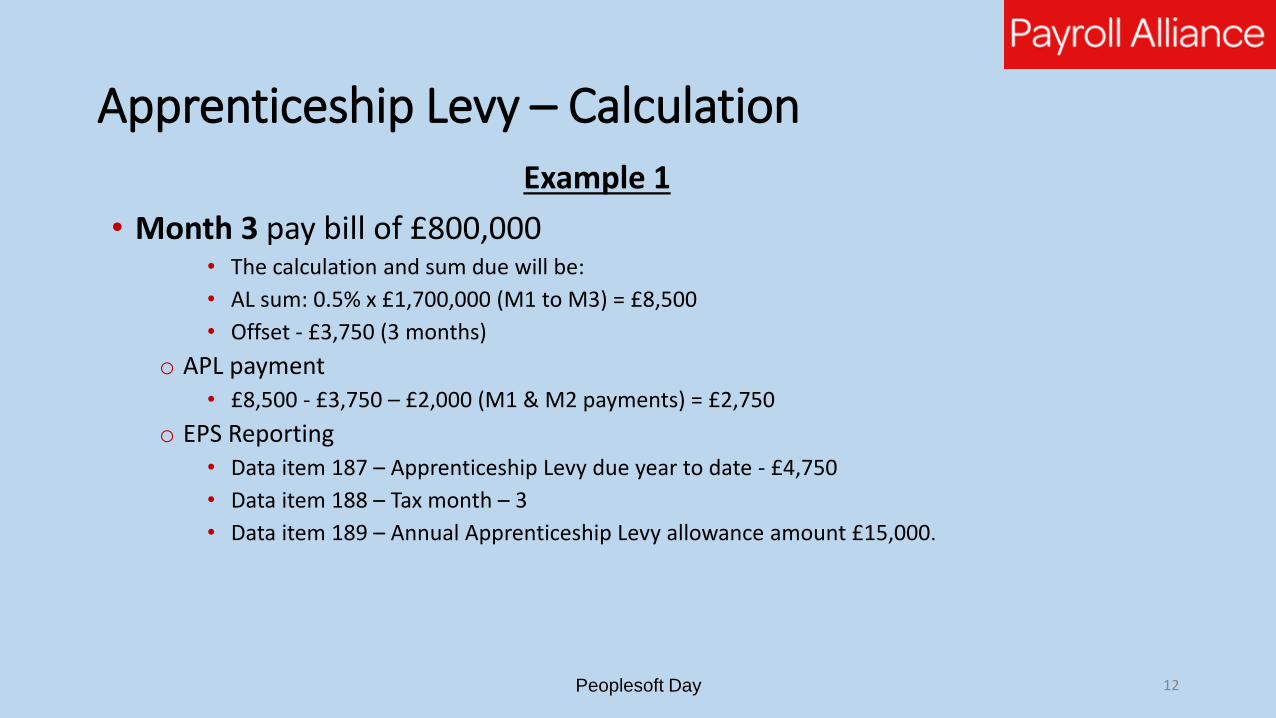

Apprenticeship Levy – Calculation Example 1

• Month 3 pay bill of £800,000• The calculation and sum due will be:

• AL sum: 0.5% x £1,700,000 (M1 to M3) = £8,500

• Offset - £3,750 (3 months)

o APL payment• £8,500 - £3,750 – £2,000 (M1 & M2 payments) = £2,750

o EPS Reporting• Data item 187 – Apprenticeship Levy due year to date - £4,750

• Data item 188 – Tax month – 3

• Data item 189 – Annual Apprenticeship Levy allowance amount £15,000.

Peoplesoft Day 12

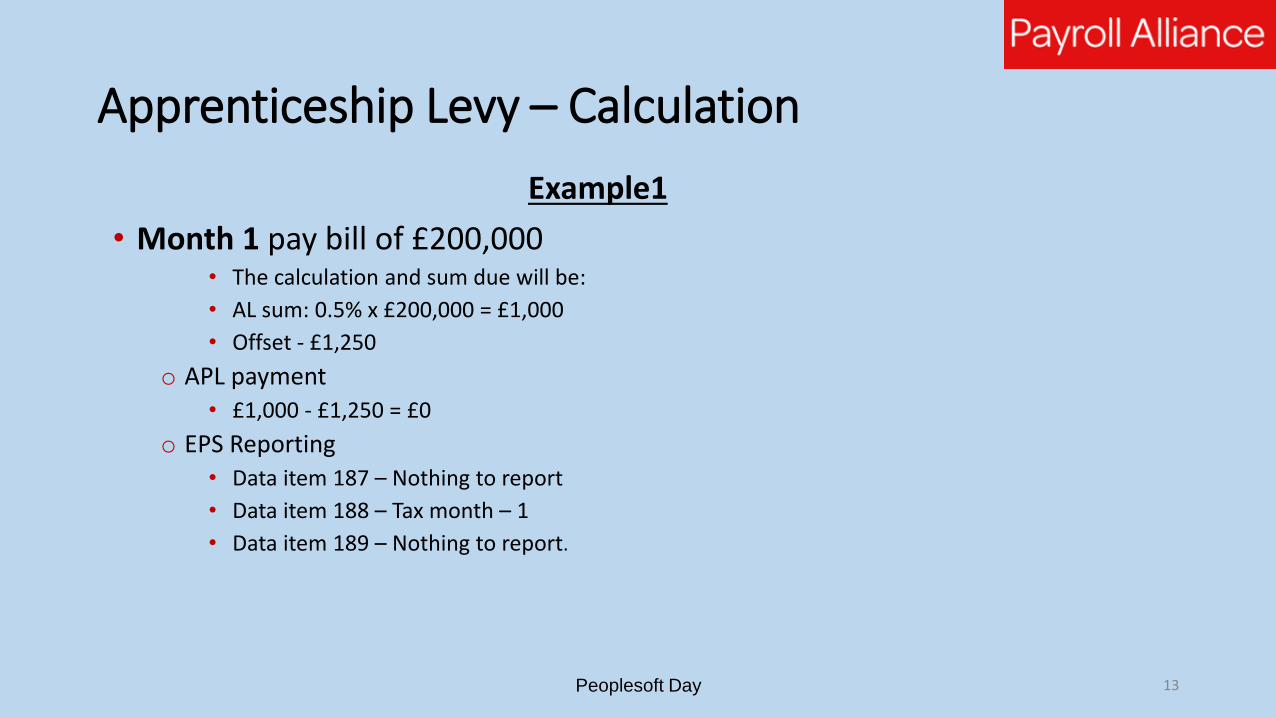

Apprenticeship Levy – Calculation

Example1

• Month 1 pay bill of £200,000• The calculation and sum due will be:

• AL sum: 0.5% x £200,000 = £1,000

• Offset - £1,250

o APL payment• £1,000 - £1,250 = £0

o EPS Reporting• Data item 187 – Nothing to report

• Data item 188 – Tax month – 1

• Data item 189 – Nothing to report.

Peoplesoft Day 13

Apprenticeship Levy – Calculation Example 2

• Month 2 pay bill of £200,000• The calculation and sum due will be:

• AL sum: 0.5% x £400,000 (M1 + M2) = £2,000

• Offset - £2,500 (2 months)

o APL payment• £2,000 - £2,500 – £0

o EPS Reporting• Data item 187 – Nothing to report

• Data item 188 – Tax month – 2

• Data item 189 – Nothing to Report.

Peoplesoft Day 14

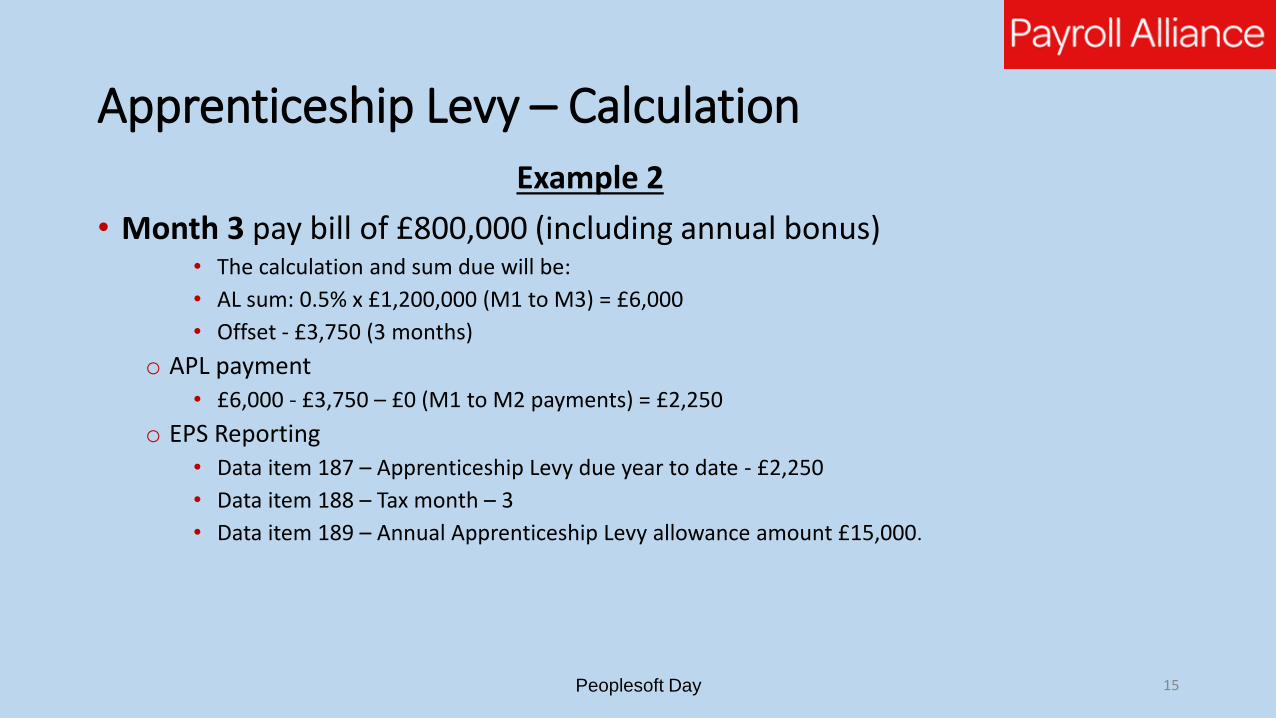

Apprenticeship Levy – Calculation Example 2

• Month 3 pay bill of £800,000 (including annual bonus)• The calculation and sum due will be:

• AL sum: 0.5% x £1,200,000 (M1 to M3) = £6,000

• Offset - £3,750 (3 months)

o APL payment• £6,000 - £3,750 – £0 (M1 to M2 payments) = £2,250

o EPS Reporting• Data item 187 – Apprenticeship Levy due year to date - £2,250

• Data item 188 – Tax month – 3

• Data item 189 – Annual Apprenticeship Levy allowance amount £15,000.

Peoplesoft Day 15

HMRC Official Guidance

• HMRC has published their own internal manual on Apprenticeship Levy at:

https://www.gov.uk/hmrc-internal-manuals/apprenticeship-levy

Peoplesoft Day 16

The Apprenticeship Service (formerly DAS)

• Registration for Digital Bank Account commenced January 2017

• April 2018 full roll out to all companies in England whether levy paid or not

• Apprenticeships commencing May 2017 will be funded by this scheme.

Peoplesoft Day 17

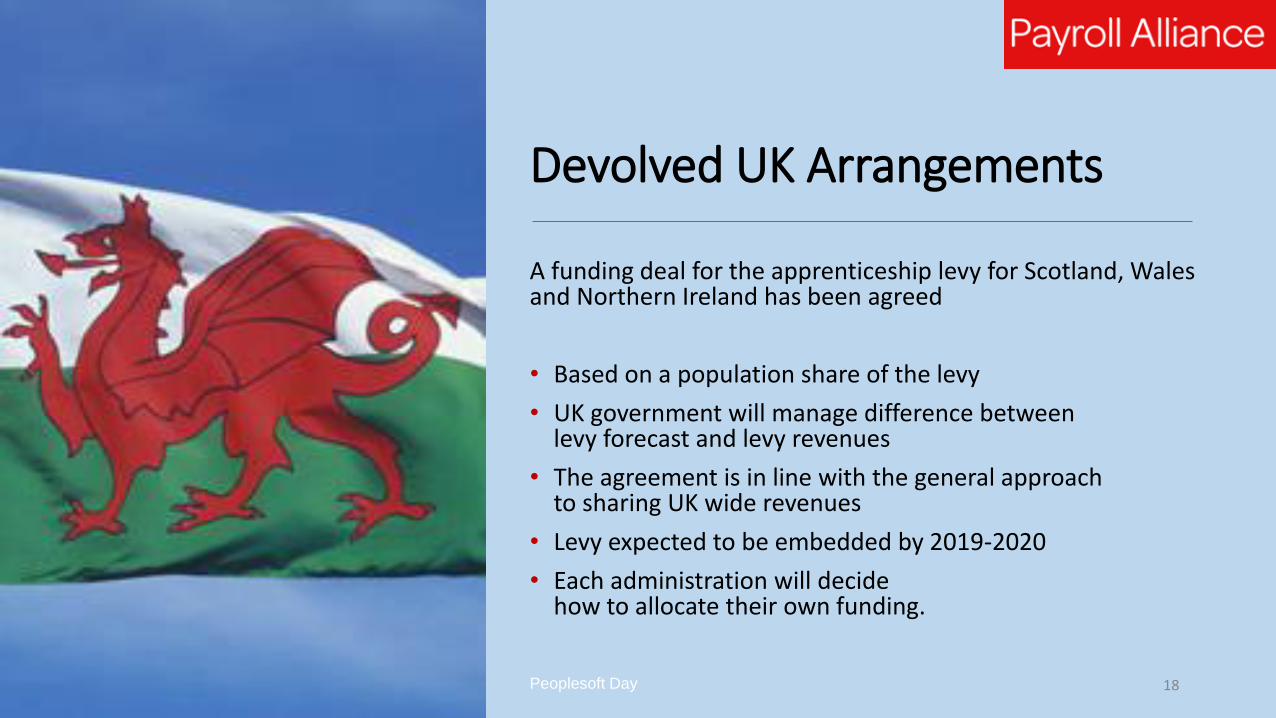

Devolved UK Arrangements

A funding deal for the apprenticeship levy for Scotland, Wales and Northern Ireland has been agreed

• Based on a population share of the levy

• UK government will manage difference between levy forecast and levy revenues

• The agreement is in line with the general approach to sharing UK wide revenues

• Levy expected to be embedded by 2019-2020

• Each administration will decide how to allocate their own funding.

Peoplesoft Day 18

Off Payroll Working

in the Public Sector

Peoplesoft Day 19

Off Payroll Working in the Public Sector

• Public sector, agencies & third parties supplying workers to public sector are affected by new rules from 6 April 2017

• The new measure will apply to contracts entered into prior to 6 April 2017

• Where applicable workers will be paid net of tax & NI via engager’s payroll

• Services provided via an intermediary (Personal Service Co.) are affected. If the worker had contracted directly with the client, the worker would have been an employee

Peoplesoft Day 20

Off Payroll Working in the Public Sector

Where the worker is paid via the engager’s payroll it will not be necessary for the engager to:

• Pay statutory payments

• Auto enrol the worker

• Deduct a student loan

• Or provide a payslip – but must provide a statement of payment and deductions

Peoplesoft Day 21

Off Payroll Working in the Public Sector

• The new rules will not impact on direct hiring via agencies (where worker is employed by an agency or umbrella and in PAYE & NIC)

• The new rules do not apply if under IR35 rules the contract would come out as self employed

• Does not impact on Managed Service Companies

Or

• Where whole service is contracted out

Peoplesoft Day 22

Off Payroll Working in the Public Sector

• The new rules apply to work completed prior to 6 April 2017 where payment is made after 6 April 2017

• They also take precedence over CIS

• Updated guidance:

https://www.gov.uk/guidance/off-payroll-working-in-the-public-sector-reform-of-intermediaries-legislation

Peoplesoft Day 23

HMRC Online Employment Status Tool

• HMRC launched the new Employment Status Service in March 2017

• It provides users with HMRC’s view of employment status

• The new Employment Status Tool will deal with all types of workers not just public sector

• Users are encouraged to go into the Status Tool several times if necessary during a period of 30 days

• The outcome can be saved as a PDF and customised

• New online Employment Status Service

https://www.gov.uk/guidance/check-employment-status-for-tax

Peoplesoft Day 24

Salary Sacrifice and Flexible Benefits

Peoplesoft Day 25

Salary Sacrifice and Flexible Benefits

• Many tax/ employer NI savings removed from 6 April 2017

• Exempted benefits:o Pensions and pension adviceo Childcareo Cycle to worko Ultra-low emission cars

• Schemes in place prior to April 2017 protected ………until April 2018

• Cars, accommodation, school fees protected ………until April 2021

• Unless there is a change or renewal of the arrangement

Peoplesoft Day 26

Peoplesoft Day

Salary Sacrifice and Flexible Benefits

Schemes no longer in scope:

1. Salary sacrifice / exchange

2. Flexible benefits where an employee can choose between a tangible benefit or cash

3. Where the employer provides benefits over and above their salary and offers a cash alternative

Where employees are offer a benefit or cash alternative, the employee must be taxed on the higher of the two

27

Peoplesoft Day

Salary Sacrifice and Flexible Benefits

Schemes in scope:

1. Pensions including pension’s advice

2. Childcare voucher or workplace nurseries

3. Directly employer contracted childcare

4. Cycle to work including accessories

5. Cars with emissions at or under 75 CO2/km

Flexible Benefits where intangible benefits can be purchased, such as:

Annual Leave

Flexible working.

28

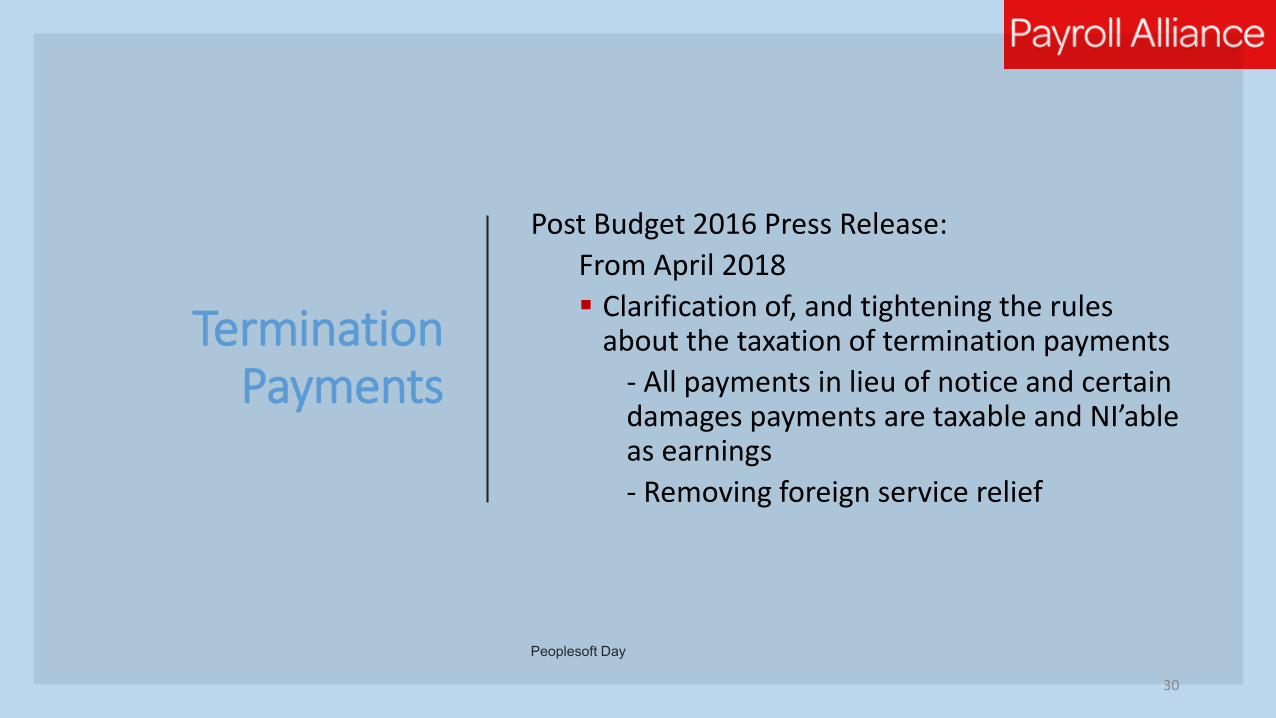

Termination Payments

Peoplesoft Day 29

Termination Payments

Post Budget 2016 Press Release:

From April 2018

Clarification of, and tightening the rules about the taxation of termination payments

- All payments in lieu of notice and certain damages payments are taxable and NI’able as earnings

- Removing foreign service relief

30

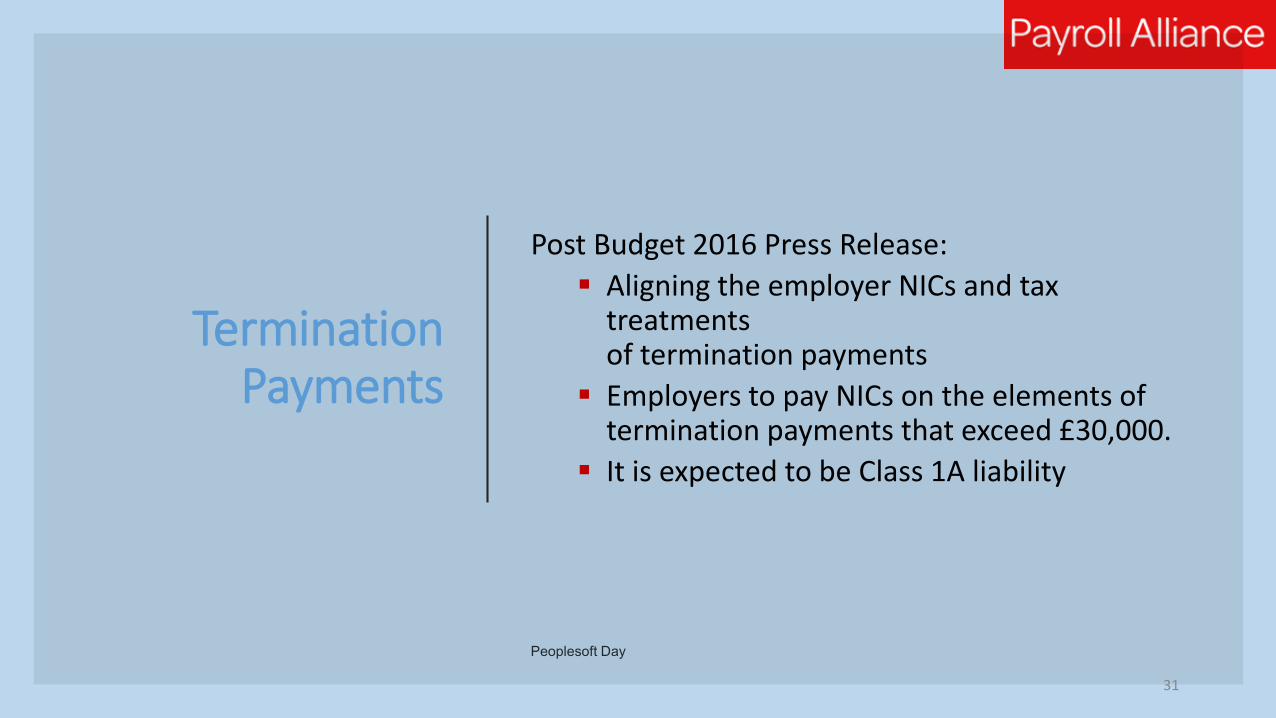

Termination Payments

Post Budget 2016 Press Release:

Aligning the employer NICs and tax treatments of termination payments

Employers to pay NICs on the elements of termination payments that exceed £30,000.

It is expected to be Class 1A liability

31

Peoplesoft Day

The General Election

Effect

32

General Election effect

As a result of the ‘snap’ General Election the Finance Bill 2017 had to be reduced

The “slimmed down” bill had to be enacted on the 27th April

The reduction meant; 72 of 135 clauses were removed

18 of 29 schedules were removed

The final act dropped from 762 to 148 pages!

Allows Parliament to review removed items in detail through more debates after the election.

Peoplesoft Day 33

General Election effect

Some of the clauses removed, temporarily Making Tax Digital

Highly contentious – possibly pushed back to April 2018 at the earliest

Pensions Advice tax free limit due to be increased to £500

- Employers may have offered advice expecting the increase

Changes to the taxation of termination payments

- Tax and NI on PILON, Class 1A on Payments over £30k.

Peoplesoft Day 34

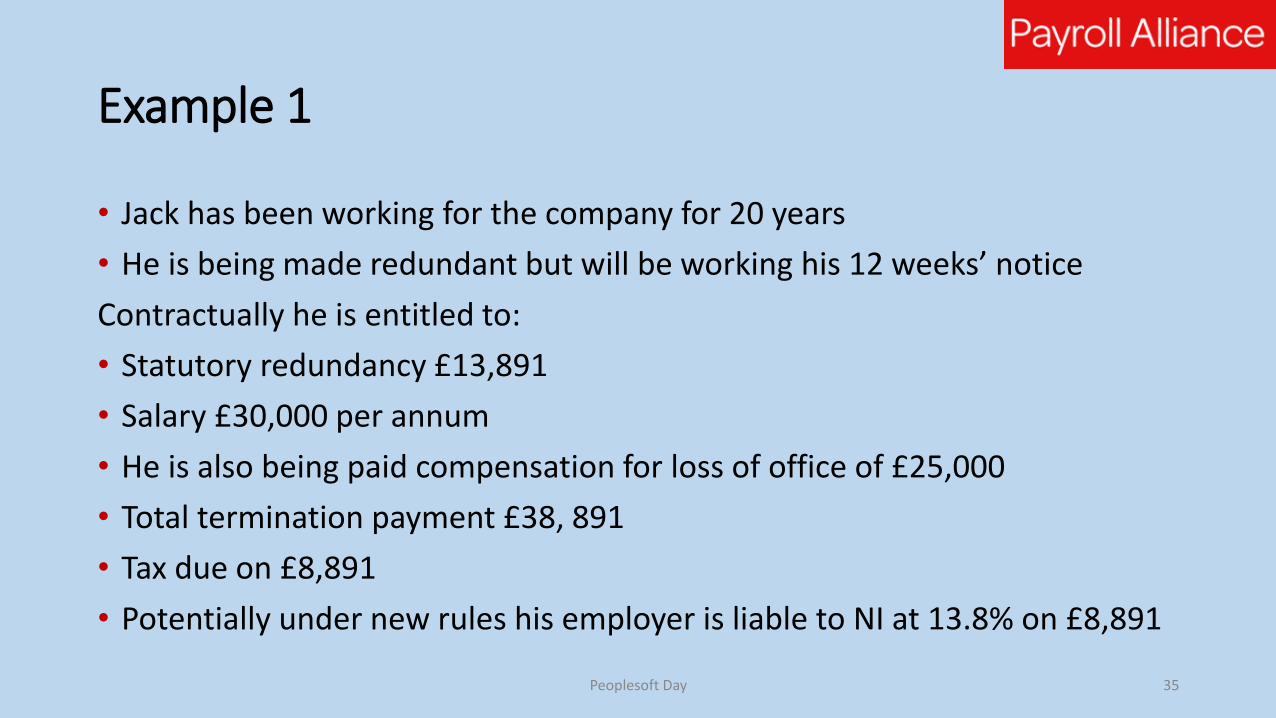

Example 1

• Jack has been working for the company for 20 years

• He is being made redundant but will be working his 12 weeks’ notice

Contractually he is entitled to:

• Statutory redundancy £13,891

• Salary £30,000 per annum

• He is also being paid compensation for loss of office of £25,000

• Total termination payment £38, 891

• Tax due on £8,891

• Potentially under new rules his employer is liable to NI at 13.8% on £8,891

Peoplesoft Day 35

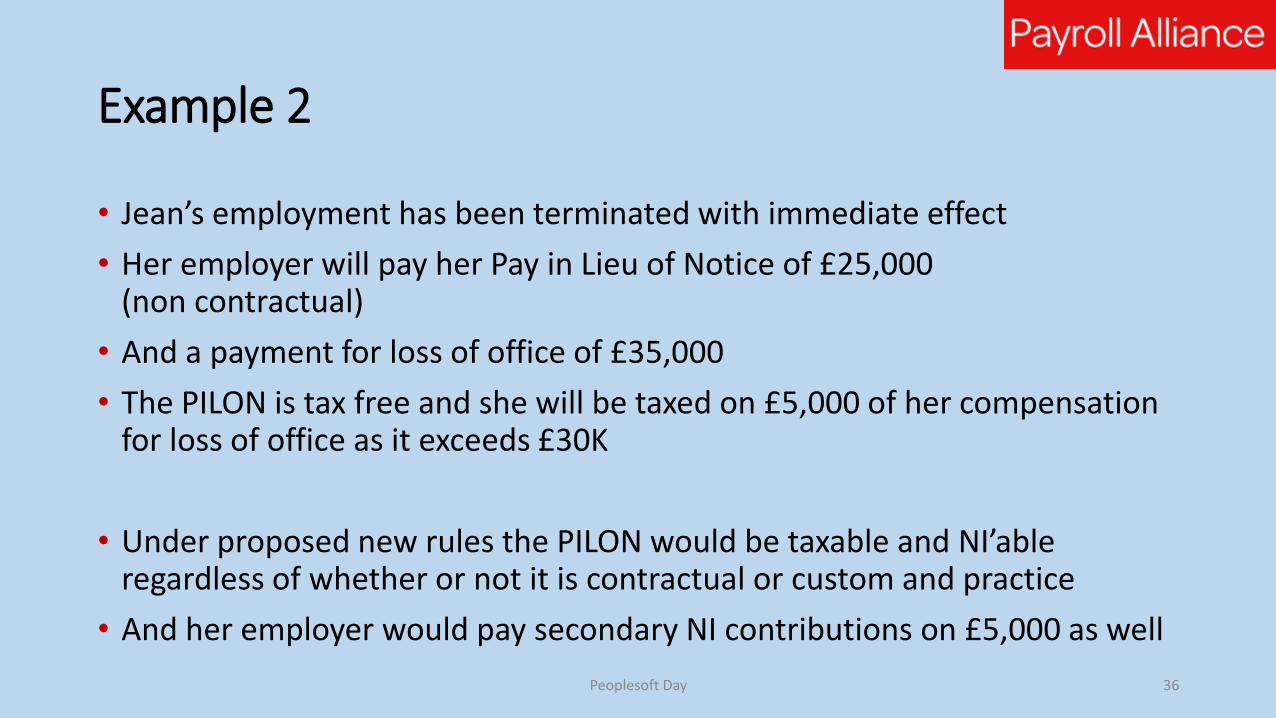

Example 2

• Jean’s employment has been terminated with immediate effect

• Her employer will pay her Pay in Lieu of Notice of £25,000 (non contractual)

• And a payment for loss of office of £35,000

• The PILON is tax free and she will be taxed on £5,000 of her compensation for loss of office as it exceeds £30K

• Under proposed new rules the PILON would be taxable and NI’ableregardless of whether or not it is contractual or custom and practice

• And her employer would pay secondary NI contributions on £5,000 as well

Peoplesoft Day 36

Thank you for listeningAny questions?www.payrollalliance.co.uk

Peoplesoft Day 37