Embed Size (px)

Citation preview

HOW TO ADJUST INVENTORY

IN QUICKBOOKS

If your business involves any type of inventory, whether a enormous amount or presently a few items, the inventory

needs to be tracked. You can use QuickBooks for accumulate inventory information and also for regulating inventory counts

and standards based on the current market. You most likely count your inventory on an ordinary basis and any changes should be proof in your financial records. You don't want to pay taxes on inventory that you don't have; therefore, you

should always take an ordinary count and adjust your records as required. It is a very simple process to make these

adjustments with QuickBooks.

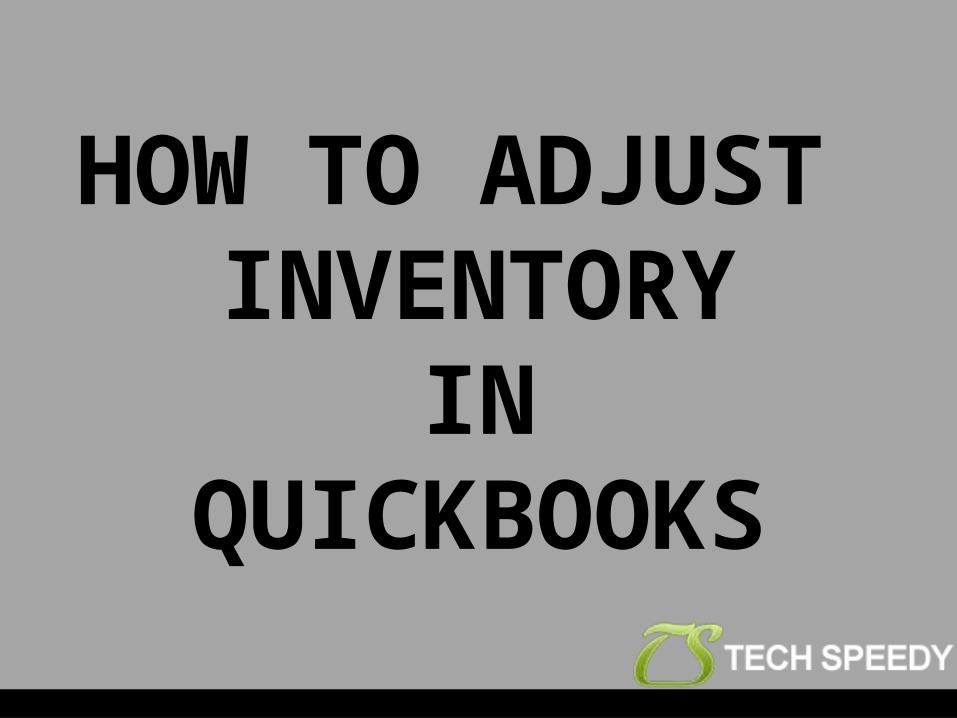

STEP-1 Select "Lists" or "Vendors."

STEP-2 Select "Items" under Lists or "Inventory Activities" under Vendors.

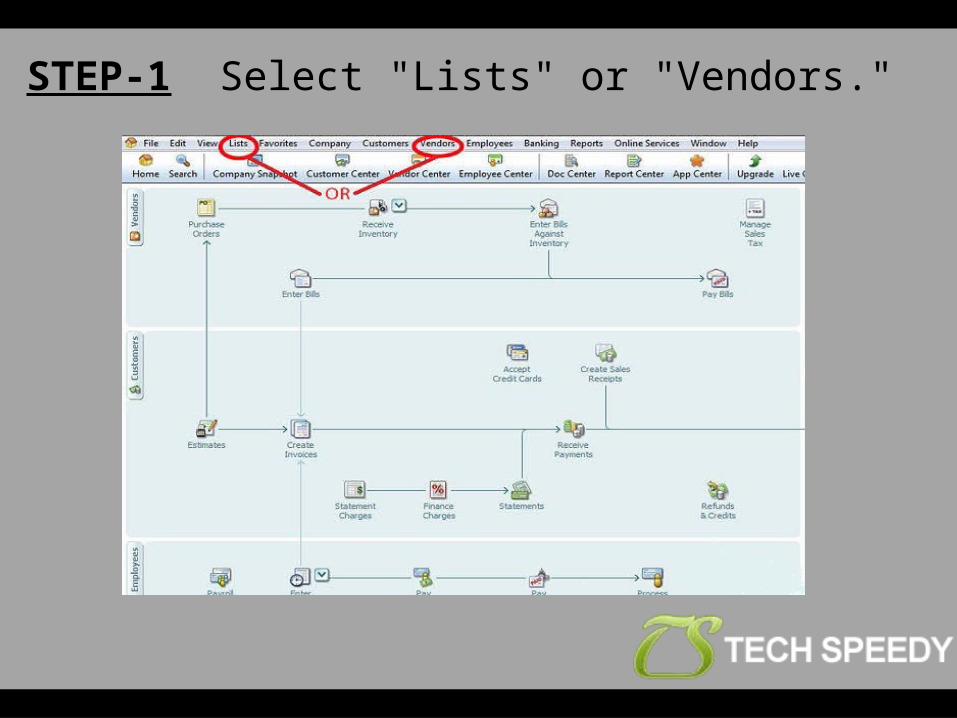

STEP-3 Select "Adjust Quantity/Value on Hand" in the drop-down list under either Lists or Vendors.

STEP-4 Enter the date that you made your physical count of your inventory.

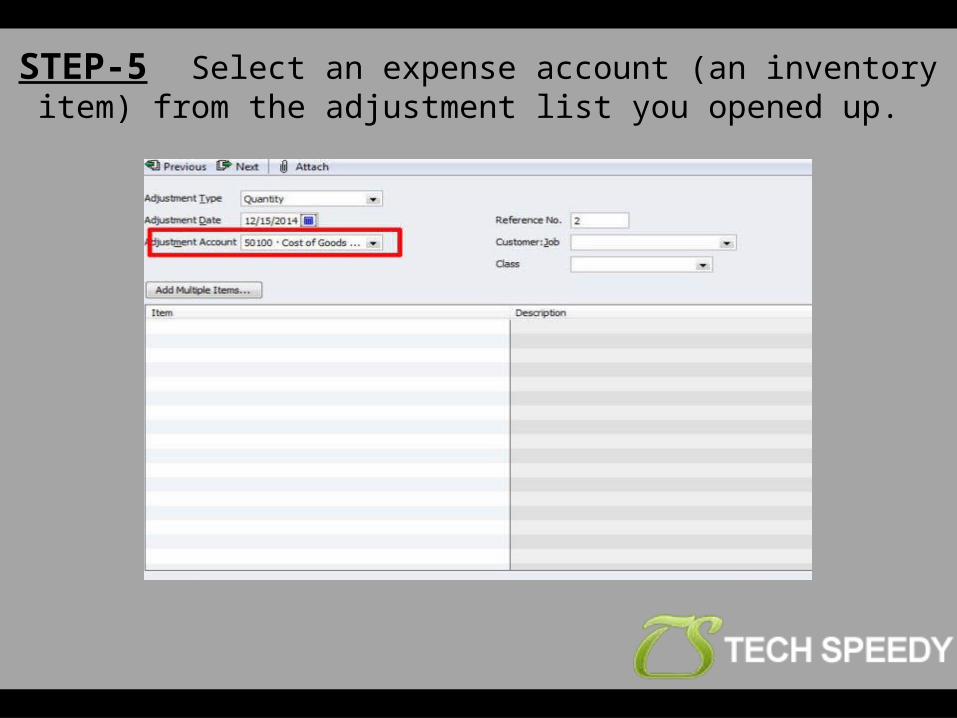

STEP-5 Select an expense account (an inventory item) from the adjustment list you opened up.

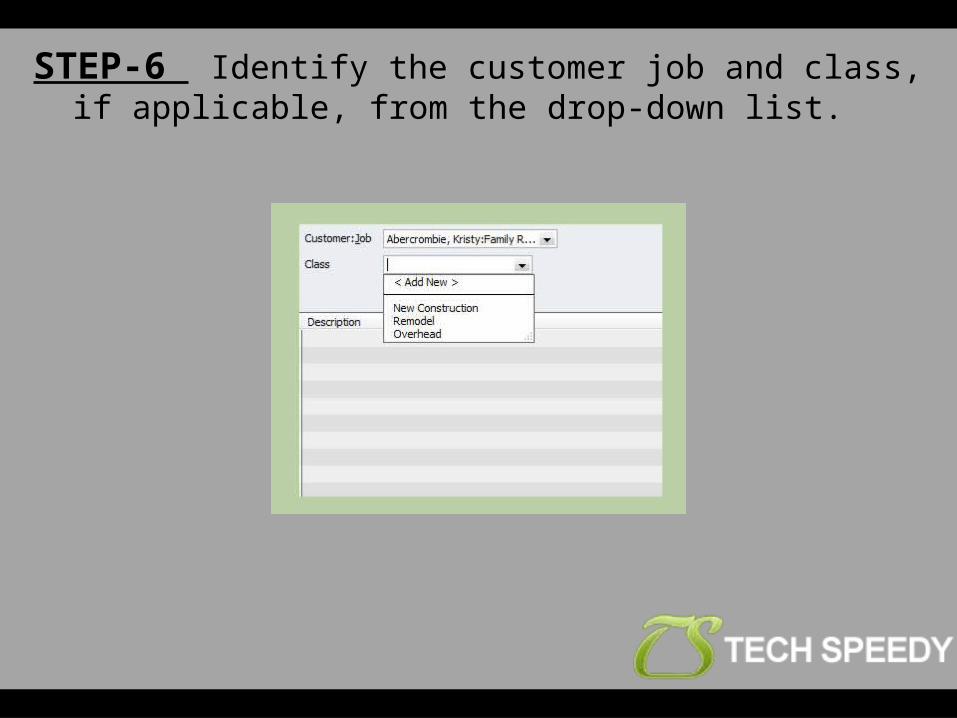

STEP-6 Identify the customer job and class, if applicable, from the drop-down list.

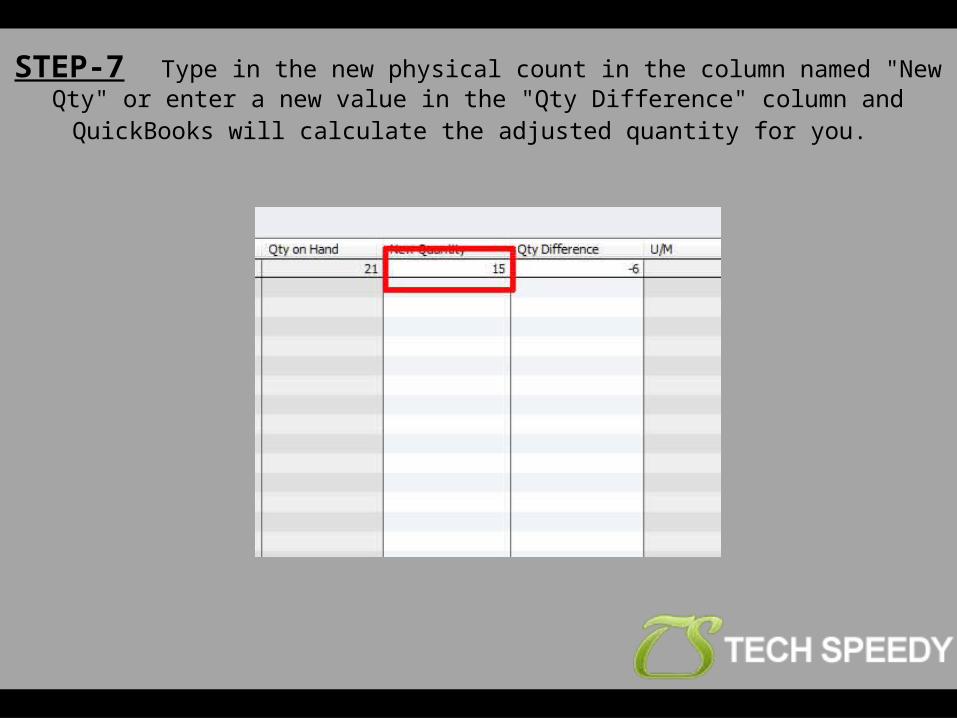

STEP-7 Type in the new physical count in the column named "New Qty" or enter a new value in the "Qty Difference" column and QuickBooks will calculate

the adjusted quantity for you.

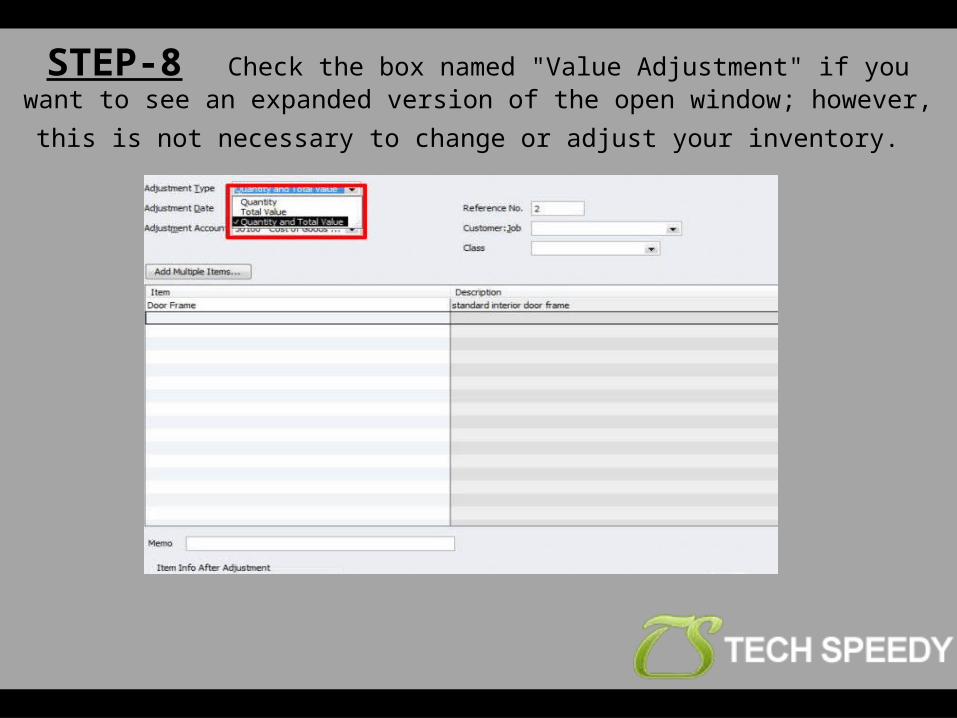

STEP-8 Check the box named "Value Adjustment" if you want to see an expanded version of the open window; however, this is not necessary to change or adjust your

inventory.

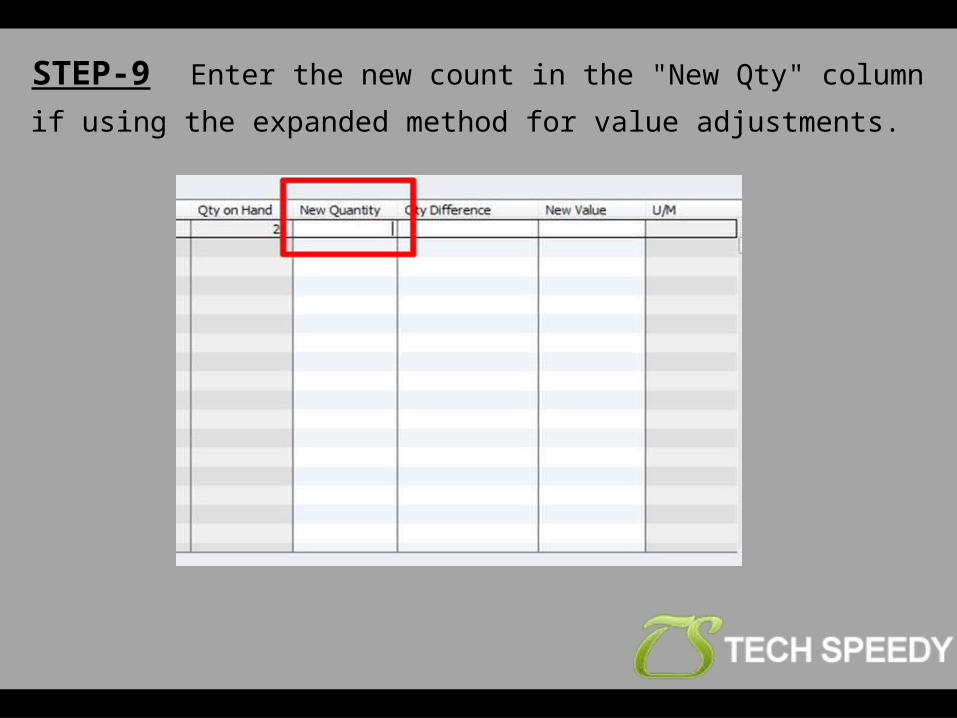

STEP-9 Enter the new count in the "New Qty" column if

using the expanded method for value adjustments.

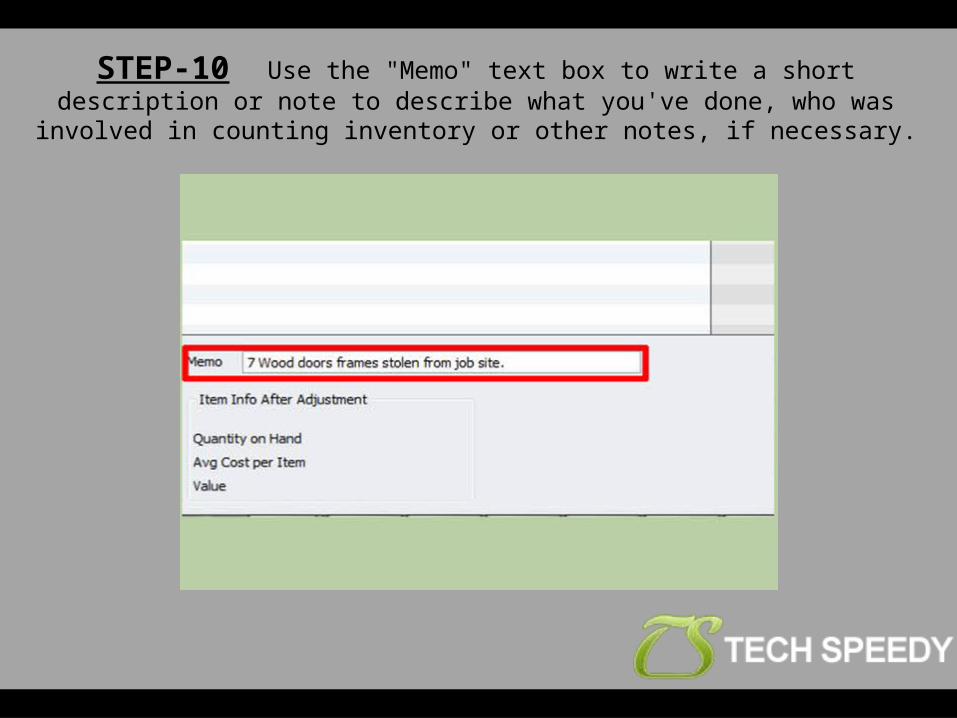

STEP-10 Use the "Memo" text box to write a short description or note to describe what you've done, who was involved in counting inventory or

other notes, if necessary.

STEP-11 Click the button marked "Save & Close" or "Save & New" to record your revisions.

CONTACT US

Website = www.techspeedy.usToll Free No. = +1-844-879-3982

Follow Us On

FACEBOOK TWITTER GOOGLE+