Embed Size (px)

Citation preview

www.ovum.com

© Copyright Ovum 2014. All rights reserved.

The Evolution of Online Streaming

Inaugural Australian OTT Summit, 17/11/2015

2© Copyright Ovum 2014. All rights reserved.

Agenda

Netflix comes to Australia: content choice highlights distribution complexity

Placing OTT SVOD into context

A changing audience for visual entertainment

TV and OTT: the perfect couple

Next-generation bundling and aggregation

TV and OTT futures: towards a brighter tomorrow

3© Copyright Ovum 2014. All rights reserved.

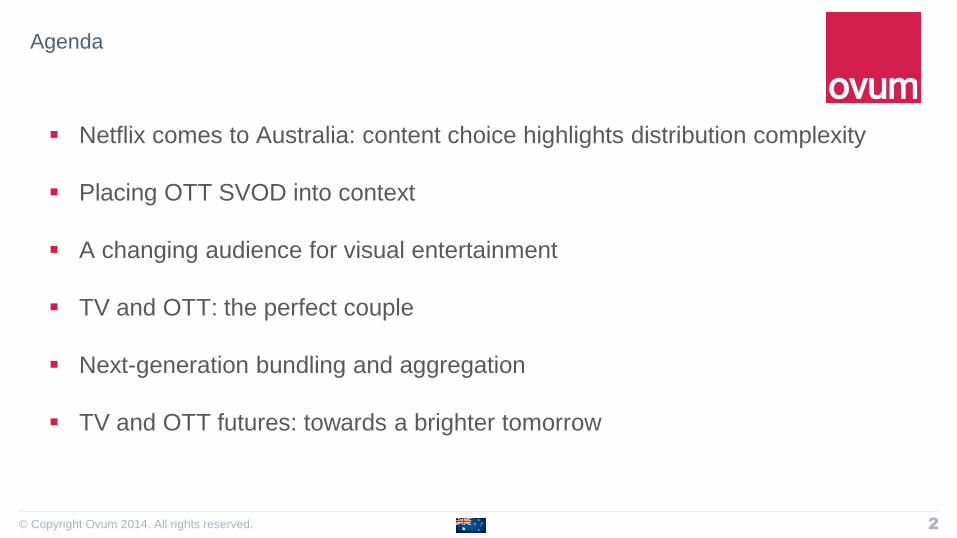

Netflix: driving change and choice for Australian audiences

Ovum was commissioned by nbnTM to examine the Australian TV and video market

Trends, supply chain, OTT service delivery

The OTT video delivery supply chain is diverse, complex and offered by multiple companies who are a effectively a

loose coalition of (usually) shared interests

No single company straddles the entire transport process from glass to glass

Hence it is unrealistic to apply QoS and UX expectations forged from TV - pay TV even - to OTT video

OTT video services and their distribution networks are not vertically integrated…and significantly cheaper

Both a blessing (innovation, no need to ask permission, audience scale, democratised distribution) and a curse (no QoS

guarantee)

2015 is just the beginning

Average monthly data usage on the nbn network rose to 110GB in September, up 51 per cent in six months

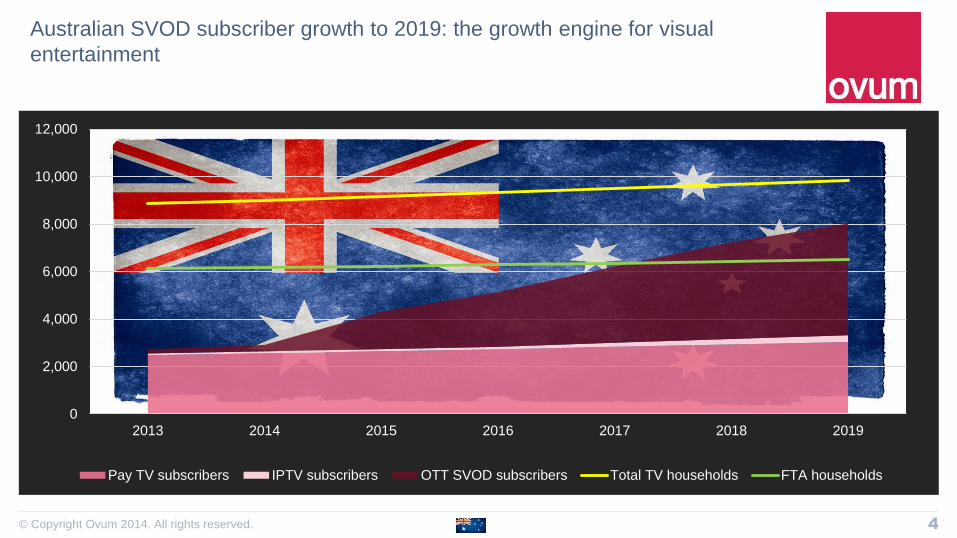

SVOD subscribers will grow by a factor of 17 between 2014 and 2019

There will be 4.7 million OTT SVOD subscriptions in Australia in 2019

Fulfilling audience expectations through network investment is a challenge for the entire online video supply chain

4© Copyright Ovum 2014. All rights reserved.

Australian SVOD subscriber growth to 2019: the growth engine for visual

entertainment

0

2,000

4,000

6,000

8,000

10,000

12,000

2013 2014 2015 2016 2017 2018 2019

Pay TV subscribers IPTV subscribers OTT SVOD subscribers Total TV households FTA households

5© Copyright Ovum 2014. All rights reserved.

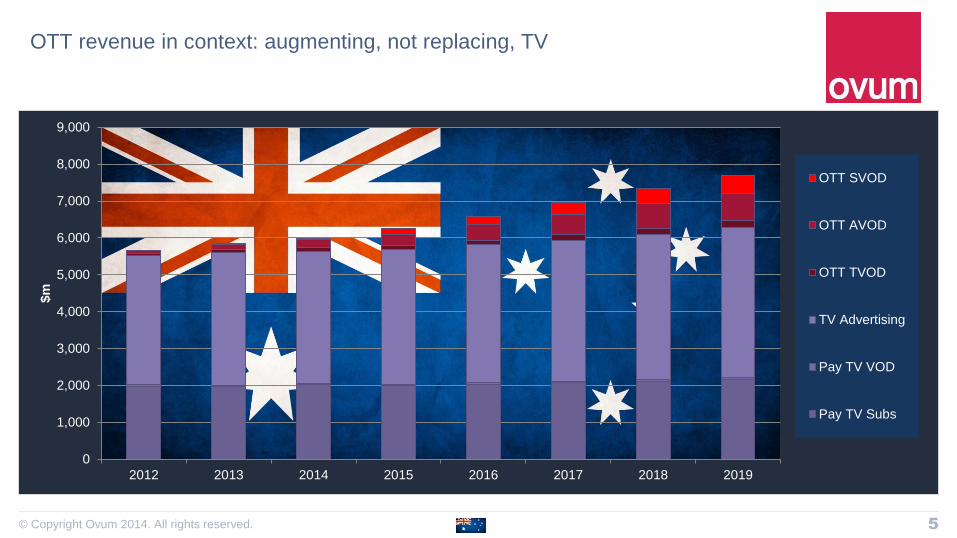

OTT revenue in context: augmenting, not replacing, TV

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2012 2013 2014 2015 2016 2017 2018 2019

$m

OTT SVOD

OTT AVOD

OTT TVOD

TV Advertising

Pay TV VOD

Pay TV Subs

6© Copyright Ovum 2014. All rights reserved.

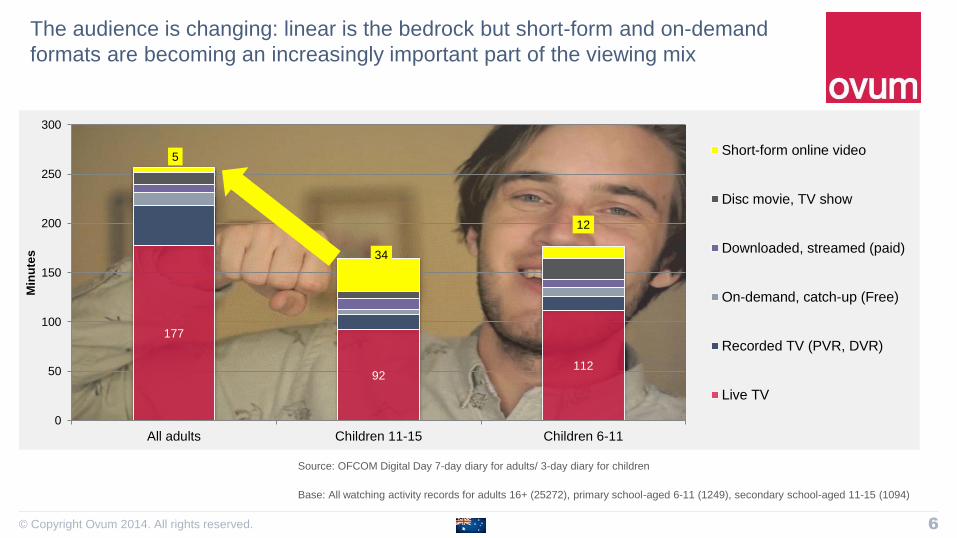

The audience is changing: linear is the bedrock but short-form and on-demand

formats are becoming an increasingly important part of the viewing mix

177

92112

5

34

12

0

50

100

150

200

250

300

All adults Children 11-15 Children 6-11

Min

ute

s

Short-form online video

Disc movie, TV show

Downloaded, streamed (paid)

On-demand, catch-up (Free)

Recorded TV (PVR, DVR)

Live TV

Source: OFCOM Digital Day 7-day diary for adults/ 3-day diary for children

Base: All watching activity records for adults 16+ (25272), primary school-aged 6-11 (1249), secondary school-aged 11-15 (1094)

7© Copyright Ovum 2014. All rights reserved.

OTT has provided (overdue) competition for traditional TV…and has had a

hugely, positive impact on the quality of the TV experience

OTT services like Netflix and Youtube have satisfied audience needs the traditional TV industry has

been slow to address

Transactional OTT established (iTunes): supplanting the disc market

Digital media, short-form tube sites (Youtube), social video (Snapchat, Facebook), games streaming (Twitch):

content formats which didn’t exist previously

Standalone SVOD (Amazon, Netflix) gaining traction: on-demand, binge and off main screen viewing

Traditional TV players are also leveraging OTT distribution

Broadcaster, rights owner direct to consumer OTT services proliferating

Improving the core TV product to justify high ARPUs: stacking rights, nDVR

Launching EST to compete in home entertainment release window

Launching standalone linear OTT streaming services: skinny bundling for OTT

Competing through bundling: content, connectivity and telephony…and more

Aggregating third party OTT and mobile video services

8© Copyright Ovum 2014. All rights reserved.

TheatricalHome Ent,

ESTTVOD, PPV

FSPTW SSPTW FTA

“We are evaluating retaining our rights for longer, and forgo or delay content licensing. This

would push the SVOD window to a multiyear period, consistent with traditional syndication”

‘Traditional’

Sky

Sky evolved

Competition

Jeff Bewkes, Warner Bros

9© Copyright Ovum 2014. All rights reserved.

Selling SVOD on a standalone basis is challenging: content services need a route

to the audience

10© Copyright Ovum 2014. All rights reserved.

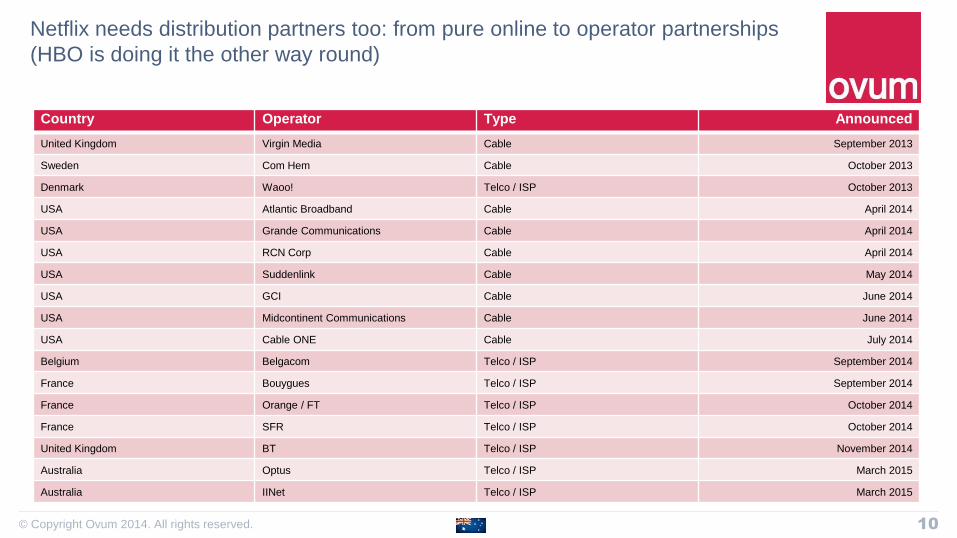

Netflix needs distribution partners too: from pure online to operator partnerships

(HBO is doing it the other way round)

Country Operator Type Announced

United Kingdom Virgin Media Cable September 2013

Sweden Com Hem Cable October 2013

Denmark Waoo! Telco / ISP October 2013

USA Atlantic Broadband Cable April 2014

USA Grande Communications Cable April 2014

USA RCN Corp Cable April 2014

USA Suddenlink Cable May 2014

USA GCI Cable June 2014

USA Midcontinent Communications Cable June 2014

USA Cable ONE Cable July 2014

Belgium Belgacom Telco / ISP September 2014

France Bouygues Telco / ISP September 2014

France Orange / FT Telco / ISP October 2014

France SFR Telco / ISP October 2014

United Kingdom BT Telco / ISP November 2014

Australia Optus Telco / ISP March 2015

Australia IINet Telco / ISP March 2015

11© Copyright Ovum 2014. All rights reserved.

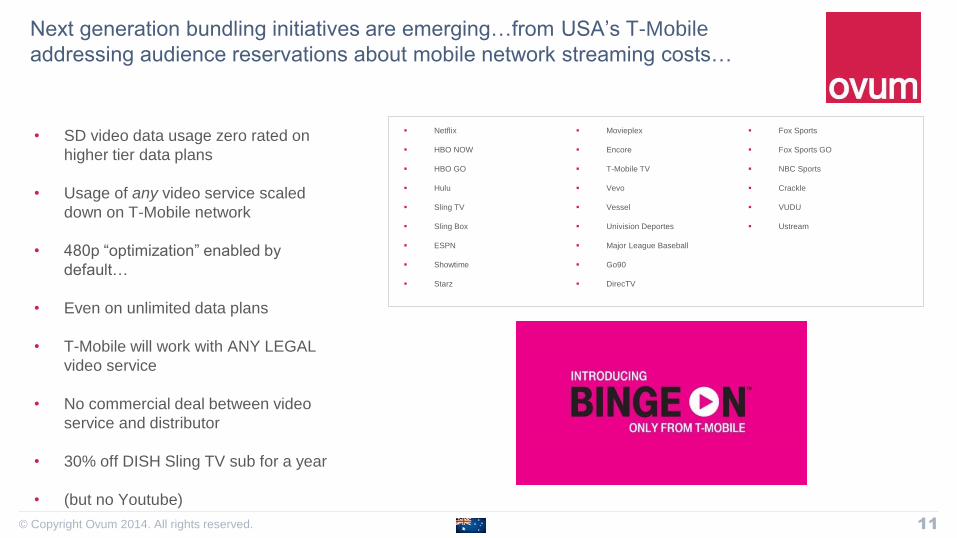

Next generation bundling initiatives are emerging…from USA’s T-Mobile

addressing audience reservations about mobile network streaming costs…

• SD video data usage zero rated on

higher tier data plans

• Usage of any video service scaled

down on T-Mobile network

• 480p “optimization” enabled by

default…

• Even on unlimited data plans

• T-Mobile will work with ANY LEGAL

video service

• No commercial deal between video

service and distributor

• 30% off DISH Sling TV sub for a year

• (but no Youtube)

Netflix

HBO NOW

HBO GO

Hulu

Sling TV

Sling Box

ESPN

Showtime

Starz

Movieplex

Encore

T-Mobile TV

Vevo

Vessel

Univision Deportes

Major League Baseball

Go90

DirecTV

Fox Sports

Fox Sports GO

NBC Sports

Crackle

VUDU

Ustream

12© Copyright Ovum 2014. All rights reserved.

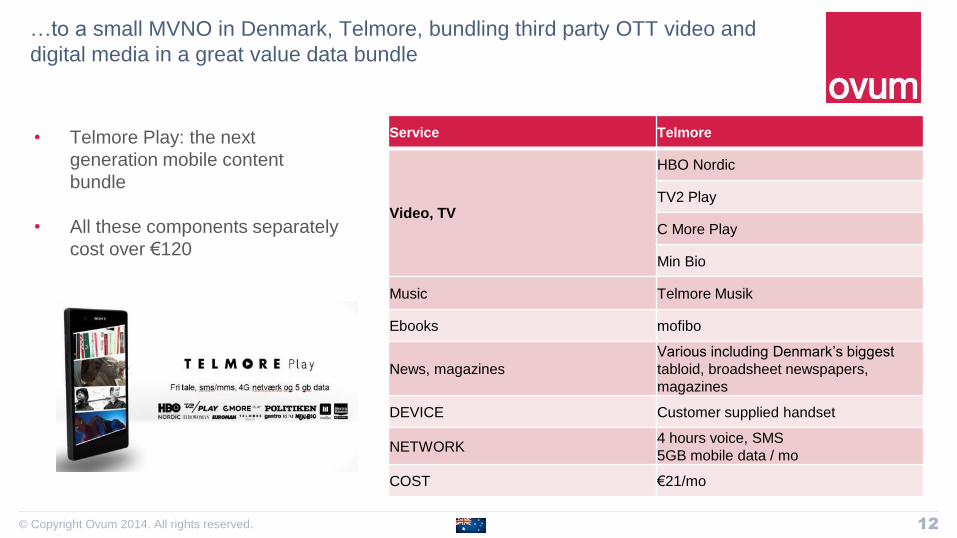

…to a small MVNO in Denmark, Telmore, bundling third party OTT video and

digital media in a great value data bundle

• Telmore Play: the next

generation mobile content

bundle

• All these components separately

cost over €120

Service Telmore

Video, TV

HBO Nordic

TV2 Play

C More Play

Min Bio

Music Telmore Musik

Ebooks mofibo

News, magazines

Various including Denmark’s biggest

tabloid, broadsheet newspapers,

magazines

DEVICE Customer supplied handset

NETWORK4 hours voice, SMS

5GB mobile data / mo

COST €21/mo

13© Copyright Ovum 2014. All rights reserved.

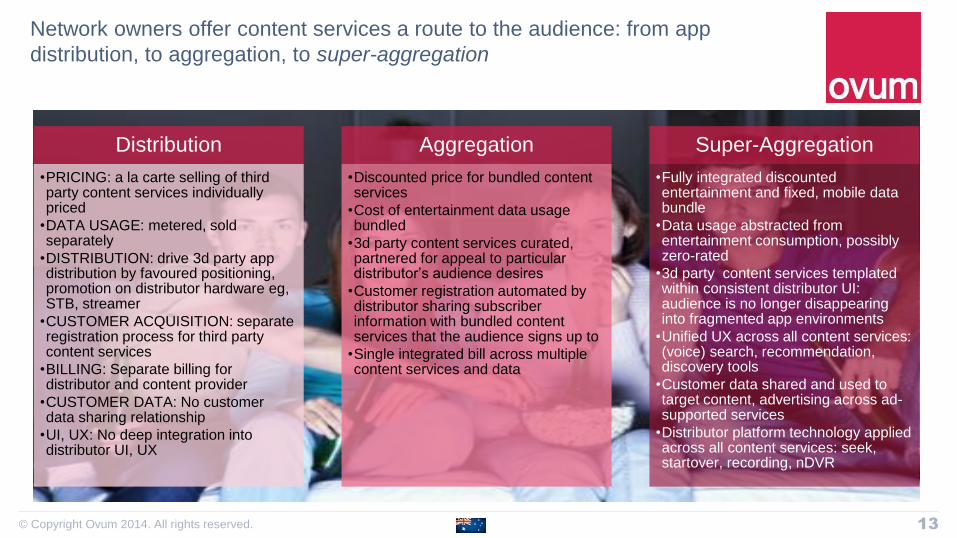

Network owners offer content services a route to the audience: from app

distribution, to aggregation, to super-aggregation

Distribution

•PRICING: a la carte selling of third party content services individually priced

•DATA USAGE: metered, sold separately

•DISTRIBUTION: drive 3d party app distribution by favoured positioning, promotion on distributor hardware eg, STB, streamer

•CUSTOMER ACQUISITION: separate registration process for third party content services

•BILLING: Separate billing for distributor and content provider

•CUSTOMER DATA: No customer data sharing relationship

•UI, UX: No deep integration into distributor UI, UX

Aggregation

•Discounted price for bundled content services

•Cost of entertainment data usage bundled

•3d party content services curated, partnered for appeal to particular distributor’s audience desires

•Customer registration automated by distributor sharing subscriber information with bundled content services that the audience signs up to

•Single integrated bill across multiple content services and data

Super-Aggregation

•Fully integrated discounted entertainment and fixed, mobile data bundle

•Data usage abstracted from entertainment consumption, possibly zero-rated

•3d party content services templatedwithin consistent distributor UI: audience is no longer disappearing into fragmented app environments

•Unified UX across all content services: (voice) search, recommendation, discovery tools

•Customer data shared and used to target content, advertising across ad-supported services

•Distributor platform technology applied across all content services: seek, startover, recording, nDVR

14© Copyright Ovum 2014. All rights reserved.

A brighter future for the audience, content and networks

Paid OTT and mobile video services of all stripes benefit from a route to the audience, aggregation,

integrated billing…

…and the audience benefits from simplification and UX consistency

Current fragmentation is beneficial neither for content services looking to grow or audiences who don’t want to

manage multiple subscriptions across different services with varying levels of UX

Potential bill shock for mobile video usage stymies market growth

The audience appreciates the value proposition of visual entertainment more than data and is moved

to spend accordingly

Cost of data is falling and will become increasingly commoditised

Leaving aside the possibility of an Elon Musk or Google driven “moonshot” working

“OTT will eat TV” is an oversimplification of a nuanced reality

Not a zero-sum game: OTT services tend to augment and complement traditional TV

Besides we won’t be saying OTT anything in a few years time…

15© Copyright Ovum 2014. All rights reserved.

The future: personalised, dynamic, accountable…data-driven

Audience segmented

to individual level

Content delivered via

dynamically constructed

personalised streams

Advertising is targeted,

accountable, dynamically

inserted into linear, VOD, OTT

Great content doesn’t

change

Streams…000s of them

Ad targeting Content selection

Brands buy audiences not

time slotsRelease windows persist

OTT/TV distinction meaningless

Data used to value advertising and content.

To determine which ads and content to

show to each viewer.

Linear TV

DVR

OTT catch up

OTT linear

OTT FVOD &

$VOD

Legacy

consumption modes

are still available

16© Copyright Ovum 2014. All rights reserved.

Thank you

Ed Barton

TV Practice Leader, Principal Analyst