Embed Size (px)

Citation preview

STARTUP

SURVEY

BY CREATIVESPARK (PTY) LTD. CONFIDENTIAL: NOT FOR PUBLICATION OR CIRCULATIONBY CREATIVESPARK (PTY) LTD (2015) [email protected]

BY CREATIVESPARK (PTY) LTD (2015) [email protected]

The true picture of South Africa’s

startup landscape revealed.

VENTUREBURN’S NATIONWIDE SURVEY INVESTIGATES

THE TECH STARTUP COMMUNITY AND FINDS OUT MORE

ABOUT THIS EVER-EXPANDING LANDSCAPE. GIVEN

VENTUREBURN’S REACH AND AUTHORITY IN THIS

SEGMENT, IT IS THE MOST COMPREHENSIVE SURVEY

TO DATE.

THE VENTUREBURN SOUTH

AFRICAN STARTUP SURVEY:

The true picture of South Africa’s

startup landscape revealed.

• 197 startups were included in the survey analysis (after a data clean-up)

• Of the total number of responses, 334 startups started the survey, 237 completed the survey

• The survey comprised of 42 questions ranging from questions about demographics, funding and

revenue challenges, information about founders and employees, motivations and questions about

markets the startups operate in

• The definition of a startup for the purposes of this survey was: A tech-based startup with revenues

of under R20-million and/or staff numbers from 0-100

• Prizes were offered to startups for completing the survey that included an iPad Mini, Goodie bag,

and 170k worth of marketing value on Ventureburn and associated Burn Media sites

• Survey achieved a 95% confidence level and a 7% margin of error. Sample size assumed a

population of about 5 000 tech startups in South Africa, a more than generous estimate, which

shows that the sample size of 197 is more than sufficient. The sample size is random

• This survey will be referenced and contextualised by an upcoming PWC Emerging Companies

Survey which will pull various startup surveys together in the country

• In order to ensure that the results were representative of the tech startup ecosystem,

we removed inconsistent responses and we removed any responses from employees

(whether holding shares or not)

• Qurio, the official research partner, has done as much as possible to ensure statistical

accuracy with a survey of this nature.

• A decision has been made not to report on Q6 due to the obvious misinterpretation of the

question. Based on the information we had (comparison with Q25), the misinterpretations

were enough to void the question, but it was not necessary to remove the responses from

the data set.

• For some of the checkbox questions (questions where respondents could choose

more than one option), we decided to weigh the questions according to how many

answer options were chosen. These questions are marked with a (W). For example:

– If someone chose 2 options, each answer option would be weighed by 50%

– If someone chose 3 options, each answer option by 33.33%

Paul Kim: Director @ Qurio, BComm Honours Actuarial Science (University of Stellenbosch)

Erin Murdoch: Data Analyst @ Qurio, BSc Applied Maths (University of Stellenbosch), [email protected]

Jacques Coetzee: Head of Ventureburn; Graham van der Made: Contributing writer; Stuart Thomas: Head of Memeburn

Jason Bechervaise; Kyle Hauptfleisch: Commercial lead; Job Mabiala: Sales executive

Matthew Buckland: MD & Founder of Burn Media, Creative Spark

Oliver Kurt Drews, consulting on data (Clifftop Colony)

Special thanks to those who consulted on survey questions: Keet van Zyl (Knife Capital), Brett Commaille (Montegray),

Andrea Bohmert (Knife Capital), Michelle Atagana (Google), Nicholas Haralambous (Entrepreneur consultant).

And a special thanks to our sponsors at FNB, Clifftop Colony and Qurio. Barrett Whiteford, (Head of Marketing : FNB

Business) and Bernice Samuels (Executive Head of Marketing at FNB), Oliver Kurt Drews, Premysl Trojan, and Kevin

Mahoney from Clifftop-Colony Venture Capitalists.

And last, but not least, a special mention to the very clever guys at research company, Qurio.

Press queries and general queries: [email protected]

The true picture of

South Africa’s

startup landscape

revealed…

• Most startups (59%) exist in the Western Cape supporting the idea of “Silicon Cape” being the

home of startups, followed by Gauteng (29%), then KwaZulu-Natal (5%). This supports the notion

that highly mobile tech entrepreneurs choose “lifestyle cities” to start their businesses in, not too

dissimilar to that of San Francisco’s Silicon Valley.

• Startup founders are young. The most popular age category for startup founders is 25-30. Just

under half (44%) of all the startups were created by people in their 20s

• There has been a surge in black entrepreneurs. The startup world is still a white, male world,

however there has been positive demographic shift towards diversity in recent years:

– Startup founders were 66% white and 17% black; this is an improvement on a Silicon Cape

survey (2012), which surveyed the startup landscape as 78% white and 6.1% black

– 68% of founders were male; just 6% were female, and 27% work in combined male and

female founder teams.

• The startup world, which is often romanticised, is a tough environment characterised by long

hours and low pay. The main cause for a startup losing employees was due to “remuneration”

(26%), followed by not liking “startup culture” (14%) and “too much pressure” (11%).

• Benefits like pensions are non-existent (0%) in the startup world and only 2% of those

surveyed offered medical aid

• This begs the question, why do people then create startups? Founders indicated that their

motivations included “spotting a gap in the market” (17%) or a desire to “innovate and be a

pioneer” (15%).

• The next most popular motivations for creating a startup included “Personal development”

(9%), “Be my own boss” (9%), “Lifestyle/flexibility reasons” (9%), “Creative Outlet” (8%) and

“more control over the work I do” (8%)

• Just 17% of startups surveyed said they were profitable

• Only 8% of startup companies remunerate employees via shares, contrary to popular belief

• The biggest challenge facing startups, unsurprisingly, is access to funds (43%), followed by “lack

of technical staff” (12%) and a South African market perceived to be “too small” (9%)

• Funding: Most startups are self funded from the start, the most popular form of funding by far

(56%), with next most popular method of funding as friends and family (15%) and Angel

investment (6%)

• Banks are not places startups traditionally go to for funding (just 2%)

• Crowdfunding, despite the hype, did not feature as a funding source at all (0%)

• 16% of startups were funded to the tune of over R1-million and 4% of startups were funded at R5-

million and up.

• Very few startups make it to Venture Capital (3%) and Private Equity (1%) rounds, a sign of

“increasing success” where startups then traditionally receive cash injections to grow

• Most startups are run from homes and garages (49%), with about 23% from

rented offices, underlying the need to booststrap and cut costs

• The top industries for SA’s tech startups are computer & software services,

media, advertising & marketing, and consumer services

• The smallest industries for SA’s tech startups are: telecommunications, gaming,

real estate, agriculture

• Most founders surveyed tend to be developers or have some kind of technical

background

• The majority startups surveyed (57%) had more than one founder, which from a

risk perspective is always preferable to investors.

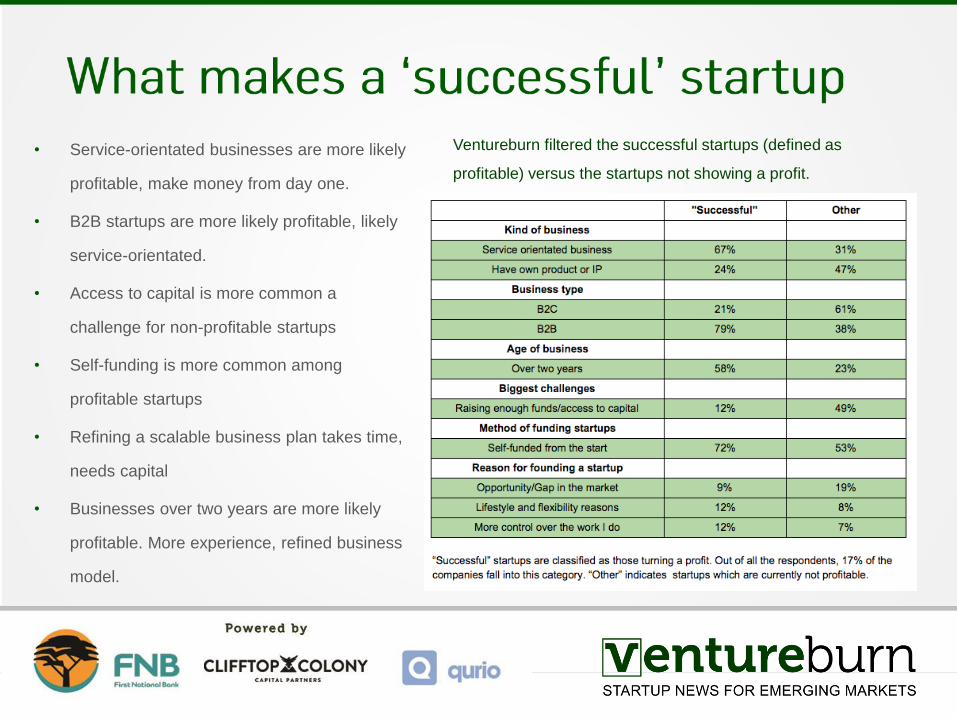

• Service-orientated businesses are more likely

profitable, make money from day one.

• B2B startups are more likely profitable, likely

service-orientated.

• Access to capital is more common a

challenge for non-profitable startups

• Self-funding is more common among

profitable startups

• Refining a scalable business plan takes time,

needs capital

• Businesses over two years are more likely

profitable. More experience, refined business

model.

Ventureburn filtered the successful startups (defined as

profitable) versus the startups not showing a profit.

The detailed

findings…

100%

Q01: Position in startup

Founder

Business Demographics

37%

43%

6%

14%

Service orientatedbusiness (e.g. agency,development house)

Have own product or IP Licence and useanother's product or IP

E-commerce

Q02: Primarily, what kind of business are you?

1%

23%

7%

3%

2%

5%

5%

1%

2%

2%

3%

15%

1%

7%

1%

4%

10%

11%

Agriculture

Computer & Software services

Education

Energy, Electrical & Petro

Entertainment & Leisure

Financial services & Insurance

Food & Beverage

Gaming

Government & Public services

Medical, Healthcare & Biotechnology

Hospitality & Travel

Media, Advertising & marketing

Real estate

Retailing/Distribution

Telecommunications

Transportation

Consumer products & services

Other

Q03: Which industry sector does your startup best fit into?

• Only founders data counted, employees eliminated from survey

• Most (43%) entrepreneurs’ startups are built around their own

product or IP (scalable enterprises), whereas 37% have

service/agency businesses

• Top industries for SA startups are computer & software services,

media, advertising & marketing, and consumer services

• Smallest industries are: telecommunications, gaming, real

estate, agriculture

45%

54%

1%

Q04: Is your business B2B, B2C or B2G?

B2B

B2C

B2G

39%

32%

13%

8%

3% 3% 2%

Less than 1year

1 to 2 years 2 to 3 years 3 to 4 years 4 to 5 years 5 to10 yearsMore than 10years

Q05: How long has the startup been in business?

59%

2% 3%

29%

1% 1%5%

1% 0%

Western Cape Northern Cape Eastern Cape Gauteng Free State North West Kwazulu-Natal Mpumalanga Limpopo

Q07: In which province is the startup based?

• Most startups (59%) are recorded in the Western Cape supporting

the idea of “Silicon Cape” being the home of startups, followed by

Gauteng (29%)

• Startups closely split between appealing to B2B and B2C, with very

little business with government

• Most startup businesses (39%) have been around for less than a

year, with 71% of startups are under 2 years old giving credence to

the view that most business fail within first 18 months*

• Less than 8% of startups surveyed are more than 4 years old

*According to Business Insider between 50 to 70 percent fail within the first 18 months

http://www.businessinsider.com/small-business-owners-are-optimistic-2013-6

37%

6%

3%

7%

19%

2%

0%

1%

1%

27%

I don't know my startup's BEE status

BEE Level 1 (Highest compliance)

BEE Level 2

BEE Level 3

BEE Level 4

BEE Level 5

BEE Level 6

BEE Level 7

BEE Level 8 (Lowest compliance)

Not compliant

Q34: BEE Status

6%

4%

45%

12%

11%

23%

Incubator or VC offices

Garage

My home

Remotely

Shared working space

Rent/own offices

Q14: Where is the startup run from? (W)

• Most startups don’t know their BEE status (37%) or are not

compliant (27%)

• For those that are compliant, the most popular category was

BEE level 4 (19%), a level which micro-enterprises

automatically qualify for if their revenues are under R5-million

• Most startups are run from home (45%), with about 23% from

rented offices and 11% from shared work spaces

• This means most startups are cost conscious, and therefore

bootstrapped

43%

37%

15%

3%

2%

1

2

3

4

5 or more

Q08: How many founders does the startup have?

Founders

1%

18%

26%

21%

15%

11%

8%

Less than 20 years old 20 to 25 years old 25 to 30 years old 30 to 35 years old 35 to 40 years old 40 to 50 years old 50+ years old

Q09: Which age group do the founders fall into?

8%

66%

4%

6%

17%

1%

Prefer not to say

White

Indian

Coloured

Black

Asian

Q12: Race of the Founders

68%

5%

27%

Q10: Gender of the founders

Male

Female

Both

52%

30%

18%

Q13: Are the founders technical?

Yes, founder/s main developer

Yes, founder/s assist in development strategy

No

• Most startups have between 1-2 founders (80%)

• 57% of startups have more than one founder

• Only 2% of startups have 5 or more founders

• The majority of startups (43%) had a single founder

• The most popular age category for startups founders is

25-30, followed by 30-35

• Just under half (44%) of all startups were created by

people in their 20s

• The startup world is still a white-male dominated world, however there

has been a positive demographic shift towards diversity

• Startup founders were 66% white and 17% black; this is an

improvement on a Silicon Cape survey (2012), which surveyed the

startup landscape as 78% white and 6.1% black

• 68% of founders were male; 6% female, and 27% worked in combined

male and female teams.

• Most founders tend to be developers or have some kind of technical

background. Only 18% aren’t technical.

70%

30%

Q37: Were you previously employed by a corporate?

Yes No

34%

66%

Q38: Would you ever work for a corporate again?

Yes No

25%

33%

42%

Q39: Net Promoter Score

Detractor

Passive

Promoter

NPS=16%

4%

9%

7%

17%

9%

8%

4%

8%

2%

7%

15%

9%

1%

Make the big bucks

Personal development

To find more meaning in my life

Opportunity/Gap in the market

Be my own boss

More control over the work I do

Don’t like rigidity/rules of corporate

Creative outlet

Altruism

Startup culture

Want to innovate/be a pioneer

Lifestyle and flexibility reasons

Other

Q35: Reason for founding a startup (W)

Reason for Founding a Startup

• Top reasons for leaving corporate life to create a startup, include:

• “Opportunity/Gap in the market”

• “Want to innovate/be a pioneer”

• “Lifestyle/flexibility”

• “Personal development”

• “Be my own boss”

• Least popular reasons include:

• “Make the big bucks”

• “Altruism”

• “Don’t like rules of corporate”

• Most founders (70%) were previously employed by a corporate.

This means that South Africans value building their networks and

skills in corporate settings before heading out to create their own

ventures.

• Most founders indicated they would not like to return to corporate

life (66%), clearly indicating that the startup bug has bitten!

• 42% of startup founders indicated that they would recommend the

“startup way” to others, while 25% say they would not recommend

the entrepreneurial startup journey

38%

50%

9%

2%

0%

1%

0

1 to 5

6 to 10

11 to 25

26 to 40

41 to 100

Q15: Nr of employees the startup has (Excluding founders)

Employees

20%19%

26%

6%

12%

6%

3%

8%

Volunteer Below Market salaries Market salaries Over market salaries Other incentives Profit share Bonuses Shares

Q16: How are employees remunerated? (W)

• 88% of startups have 5 employees or fewer

• 38% have no employees (just a founder)

• Only 1% have 41-100 employees

• Most employees on startups are remunerated with

“market related” salaries; 39% of employees work on

volunteer basis or for a “below market related” salary

• Only 8% of startup companies remunerate via shares,

contrary to popular belief

2% 0%

15%

7% 7%

18%

5%

46%

Medical Aid Pension Skills development(training, education

etc)

Travel benefits(petrol, travel

allowance etc)

Productivityallowance (laptop,

cellphone, dataetc)

Office benefits(coffee, lunch etc)

Other None of the above

Q17: Additional benefits offered to employees (W)

26%

6%

5%

8%

4%

6%

9%

14%

5%

11%

6%

Remuneration

Benefits

Employee performance

Poached by corporate

Poached by competitor

Personal reasons

Battles with multiple roles and disciplines

Startup culture does not agree with them

Working hours

Too much pressure

Other

Q18: Main causes for losing employees in startups (W)

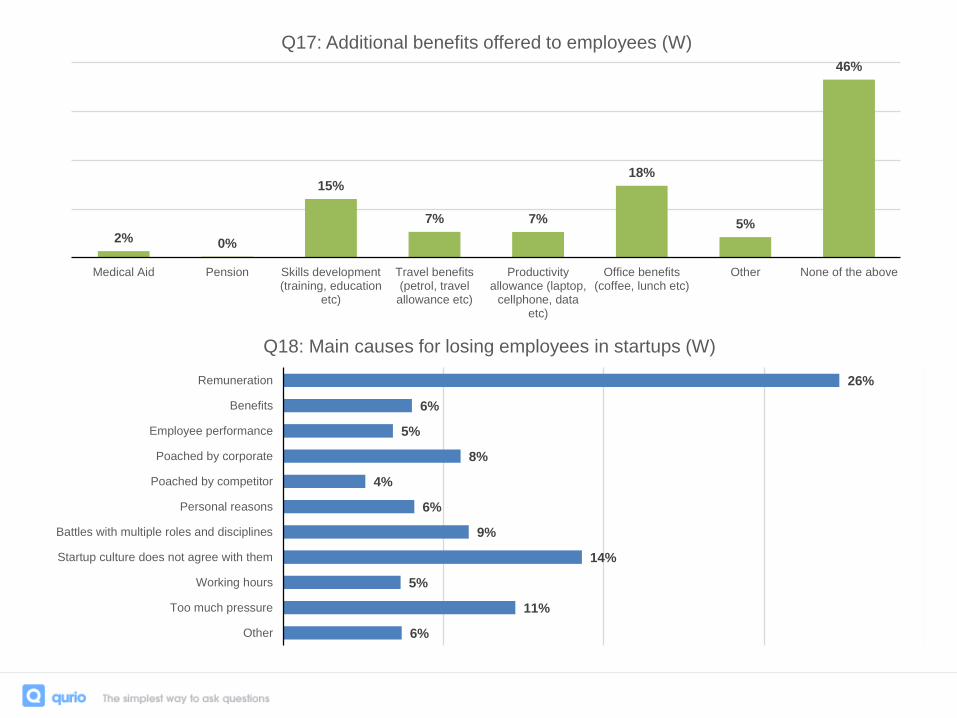

• Startup life tends to be glamorised, but the survey reveals that it can be

tough

• Almost half of all startups (46%) offer no benefits to their employees

• No startup in the survey offers any pension benefits (0%) and only 2% do

medical aid

• The main cause for a startup losing employees was due to “remuneration”

(26%), followed by not liking “startup culture” (14%) and “too much

pressure” (11%)

• A sum of 39% lose employees due to having a culture clash with the

industry itself (culture, pressure, battles with multiples roles, long working

hours)

43%

3%

9%

7%

12%

6%

7%

14%

Raising enough funds/access to capital

Lack of government support

Market too small

Lack of support in ecosystem

Not enough skilled technical staff/development

Not enough skilled staff

Too much red tape

Other

Q19: What is the biggest challenge startups face?

Challenges Facing Startups

3%

4%

1%

1%

56%

3%

0%

3%

2%

2%

4%

1%

3%

6%

11%

Other

Service work to supplement revenues

Funds by way of grant or donors

Government or quasi government funding

Self-funded from the start

Credit cards

Crowd funding

Revenue from another business

Revenue from a startup competition

Bank finance (loan)

Loans from friends and family

Private equity investment

Venture capital investment

Angel investment

Investment by friends and family

Q22: How did the startup first access funds? (W)

Funding of Startups

44%

12% 12%

8% 8%6% 6%

4%

Less than R50k R50k to R100k R100k to R250k R250 to R500k R500k to R1m R1m to R2m R2m to R5m R5m+

Q23: How much funding did your startup receive in total?

90%

2%8%

Q24: Where were the funds sourced from?

South Africa

Africa

Outside of Africa

34%

24%

17%

9%

17%

0 to 3 months 3 to 6 months 6 to 12 months 12+ months We're profitable

Q25: How many months before funding runs out?

2%

4%

10%

10%

25%

23%

27%

R100m and above

R25m to R100m

R10m to R25m

R5m to R10m

R1m to R5m

0 to R1m

Not looking to raise

Q26: How much funding does your business need to raise in the next 3 years?

• Biggest challenge facing startups, unsurprisingly, is access to funds (43% of

startups), followed by “lack of technical staff” (12%) and a South African market that

is perceived to be too small (9%)

• More than half of all startups are self-funded from the start (56%)

• The next most popular method of funding is friends and family (11%), Angel

investment (6%)

• Typically conservative banks are not places startups go for funding (2%). Alarmingly

3% of founders indicated they used their credit cards to start their companies

• Crowd-funding, despite the hype, is non-existent as a form of funding (0%)

• Very few startups make it to Venture Capital rounds, typically where they will get cash

injections to scale further (3%)

• Most startups surveyed received funding of R50 000 or under (44%)

• 16% of startups were funded to the tune of over R1-million

• 4% of startups were funded in the R5-million-plus bracket

• Most funding emanates from South Africa

• Only 17% of startups surveyed were profitable

• 75% of startups indicated they will be running out of funding within the next year

• 27% indicated they were not looking for funding, where as 50% were looking for R1-million-

plus funding

• The majority of startups indicated they were to source funds from venture capitalists (14%),

private equity (10%) and angel investment (9%). This is in contrast to those that actually

achieve Venture Caoital funding (3%).

• Just 7% said that they would continue to self-fund their startup

• Only 4% indicated that they would source funds from friends and family

58%

7%12% 11%

7%4%

2% 1% 1%

R0k to R100k ayear

R100k to R250kper year

R250k to R500kper year

R500k to R1mper year

R1m to R2m peryear

R2m to R5m peryear

R5m to R10mper year

R10m to 20m peryear

R20m+ per year

Q32: Revenue generated by the startup

13%

6%

20%

35%

18%

8%

Anywhere from 100% annual revenue growth and upwards

Anywhere from 75% annual revenue growth and upwards

Anywhere from 50% annual revenue growth and upwards

Anywhere from 25% annual revenue growth and upwards

Anywhere from 10% annual revenue growth and upwards

Anywhere from 0% annual revenue growth and upwards

Q33: Floor annual revenue growth rate, to be deemed successful

65%

13%

2% 0% 1%3%

15%

1%

South Africa Africa North America South America Australasia Europe Whole world Other

Q28: Which market does your startup operate in? (W)

Market Related

43%

23%

14%

20%

R0 to R100m a year R100m to R500m a year R500m to R1b a year R1b plus a year

Q29: What is the size of the market you are addressing in terms of revenue per year?

41%

14%

23%

22%

Dominate market

Top 3 position in market

Highest possible market share

Sustainable business

Q30: Startup objective, when positioning company in desired market

• Most startups (58%) indicated they were generating revenues of R0-R100 000 per

year with the majority looking for high growth of between 25%-50% pa

• Most startups believed their market size was between R0-R100-million, with at least

20% indicating they were operating in a R1-billion market

• Most startups have high hopes, looking to dominate their defined market (41%)

• Most startups are marketed via “word of mouth” (24%), personal networks (19%), and

social media (21%)

• Traditional marketing was the least preferred form of promotion (3%), which supports

the notion that most startups, most of whom are bootstrapping, cannot afford

traditional forms of marketing