Embed Size (px)

Citation preview

Venture Capital 2016Data & Views from VCs and LPs

1VC Survey Data

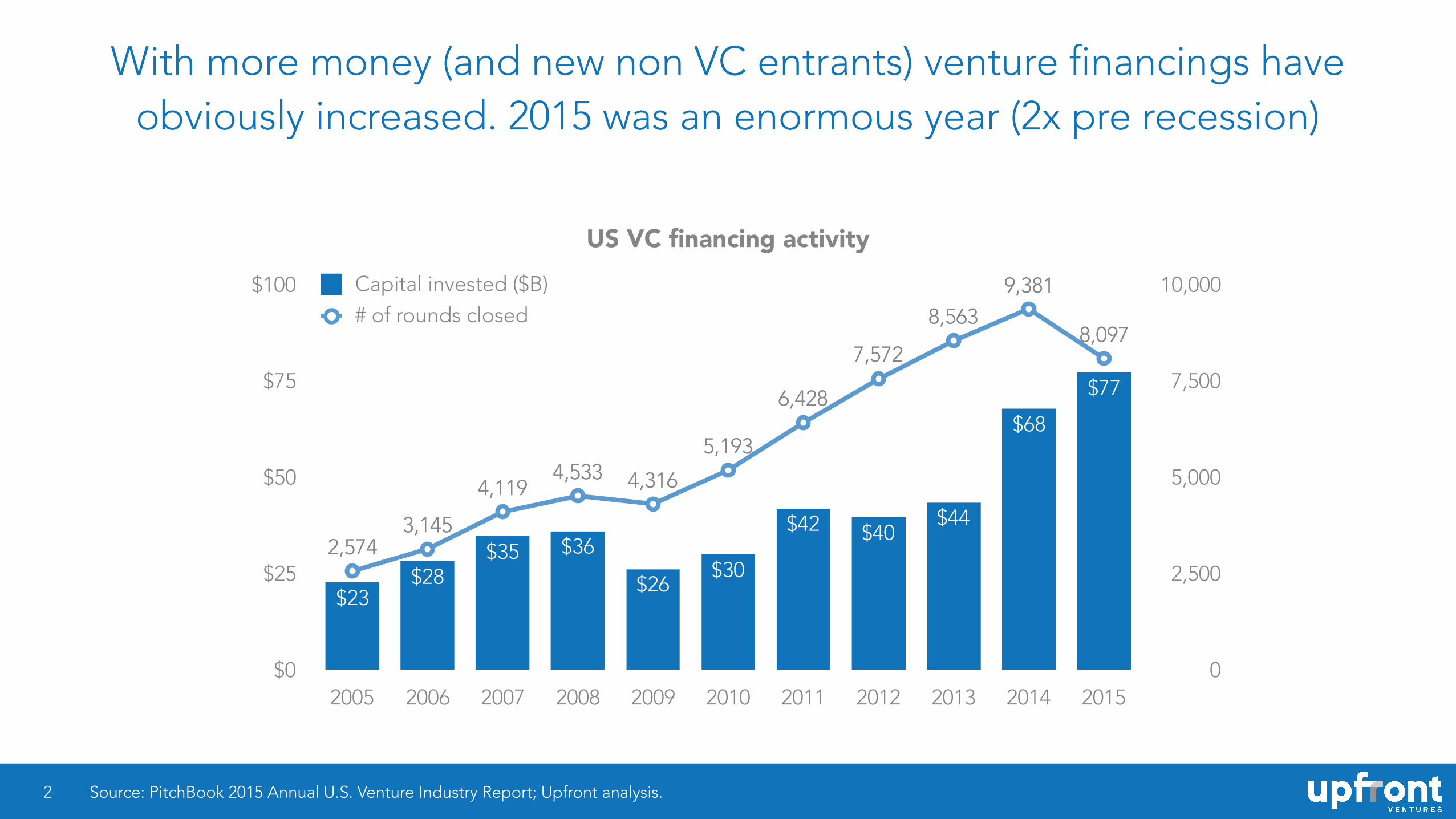

With more money (and new non VC entrants) venture financings have obviously increased. 2015 was an enormous year (2x pre recession)

2

US VC financing activity

0

2,500

5,000

7,500

10,000

$0

$25

$50

$75

$100

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Capital invested ($B)# of rounds closed

8,097

9,3818,563

7,572

6,428

5,193

4,3164,5334,119

3,1452,574

$77

$68

$44$40$42

$30$26

$36$35$28

$23

2,5743,145

4,1194,533 4,316

5,193

6,428

7,572

8,5639,381

8,097

Source: PitchBook 2015 Annual U.S. Venture Industry Report; Upfront analysis.

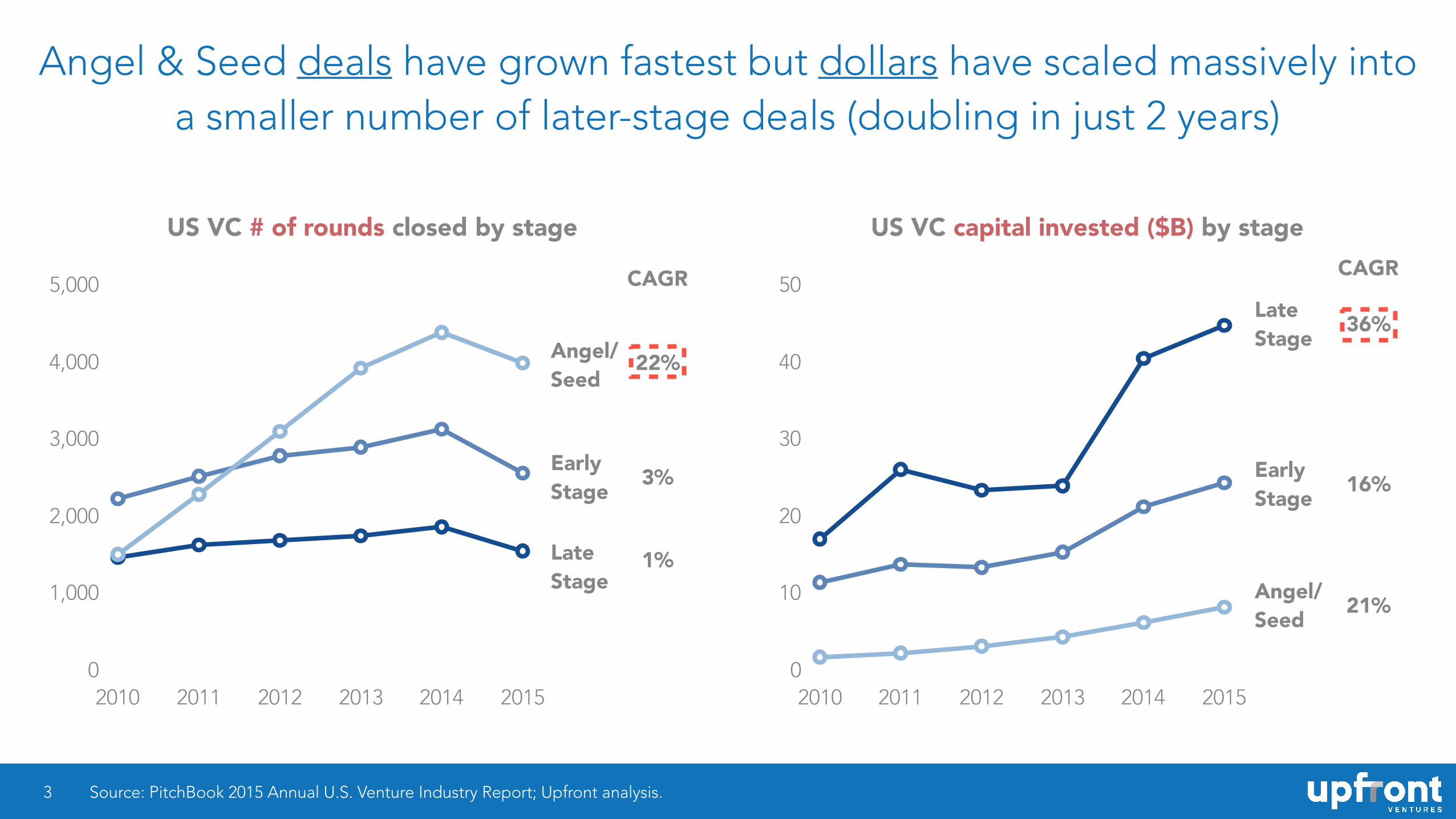

Angel & Seed deals have grown fastest but dollars have scaled massively into a smaller number of later-stage deals (doubling in just 2 years)

3 Source: PitchBook 2015 Annual U.S. Venture Industry Report; Upfront analysis.

US VC # of rounds closed by stage US VC capital invested ($B) by stage

0

10

20

30

40

50

2010 2011 2012 2013 2014 20150

1,000

2,000

3,000

4,000

5,000

2010 2011 2012 2013 2014 2015

Early Stage

CAGR

21%

36%

16%

CAGR

1%

22%

3%

Angel/ Seed

Late Stage

Early Stage

Late Stage

Angel/Seed

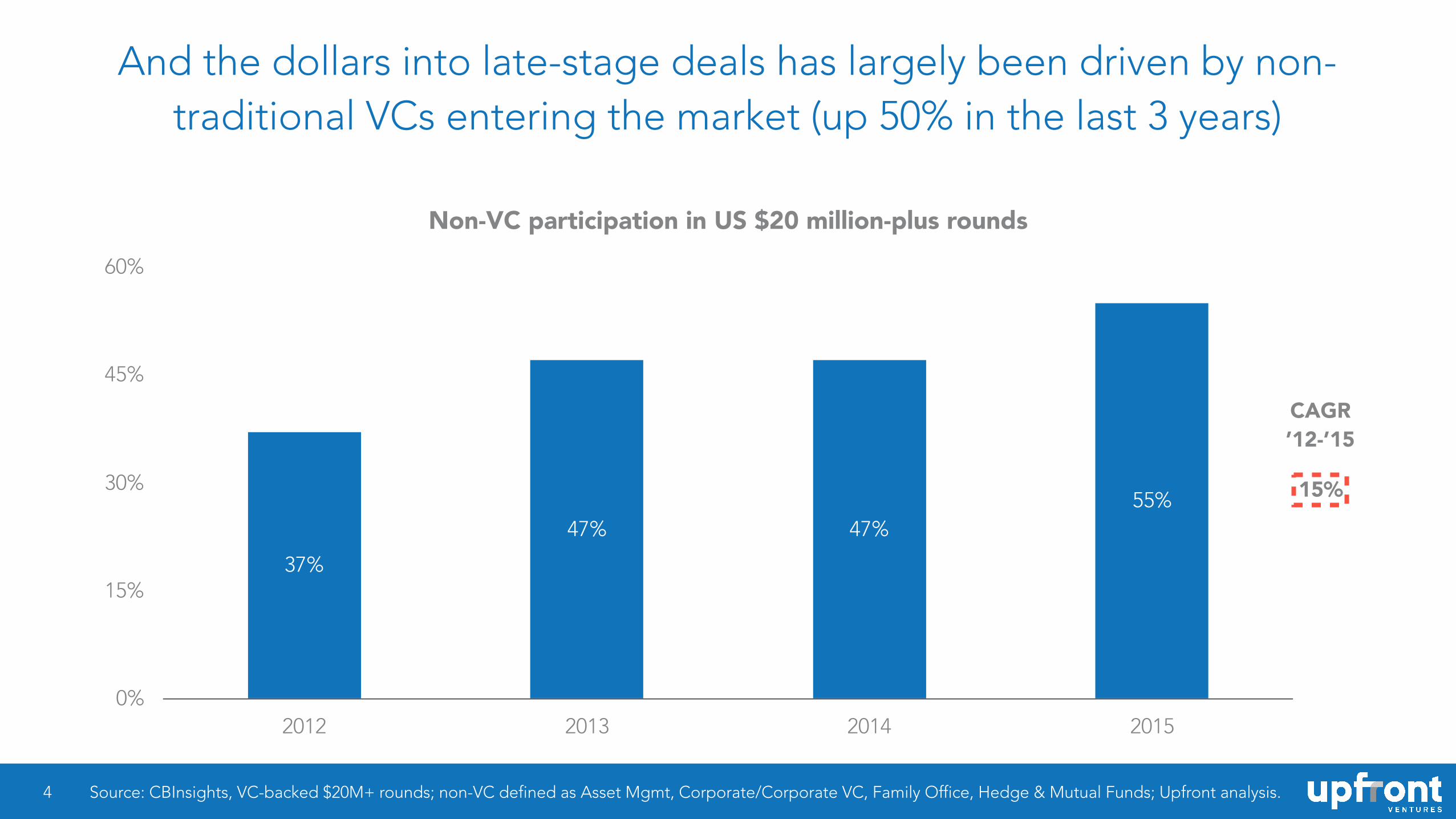

And the dollars into late-stage deals has largely been driven by non-traditional VCs entering the market (up 50% in the last 3 years)

4 Source: CBInsights, VC-backed $20M+ rounds; non-VC defined as Asset Mgmt, Corporate/Corporate VC, Family Office, Hedge & Mutual Funds; Upfront analysis.

Non-VC participation in US $20 million-plus rounds

0%

15%

30%

45%

60%

2012 2013 2014 2015

55%47%47%

37%

CAGR ’12-’15

15%

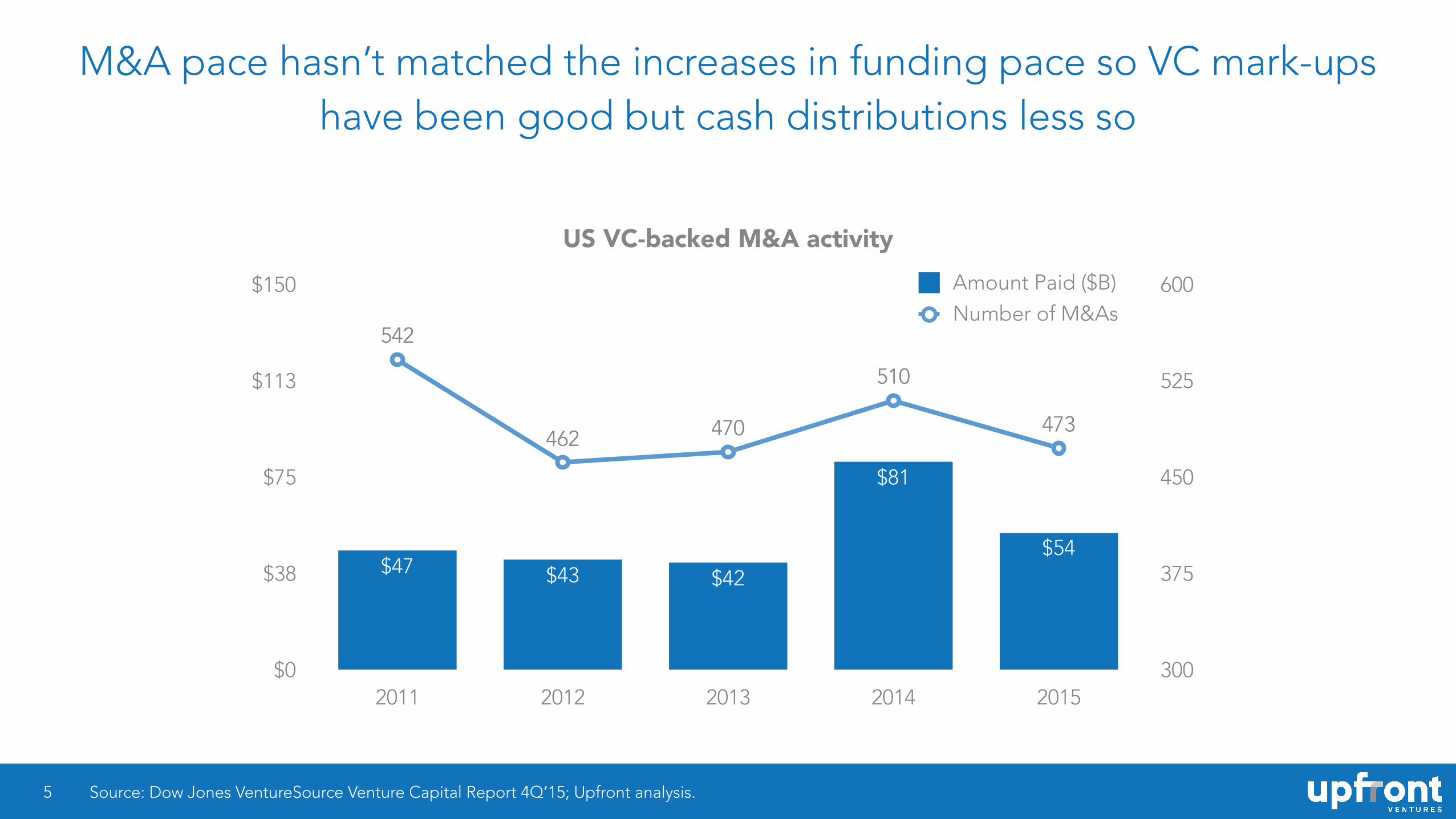

M&A pace hasn’t matched the increases in funding pace so VC mark-ups have been good but cash distributions less so

5

US VC-backed M&A activity

300

375

450

525

600

$0

$38

$75

$113

$150

2011 2012 2013 2014 2015

Amount Paid ($B)Number of M&As

473

510

470462

542

$54

$81

$42$43$47

542

462 470

510

473

Source: Dow Jones VentureSource Venture Capital Report 4Q’15; Upfront analysis.

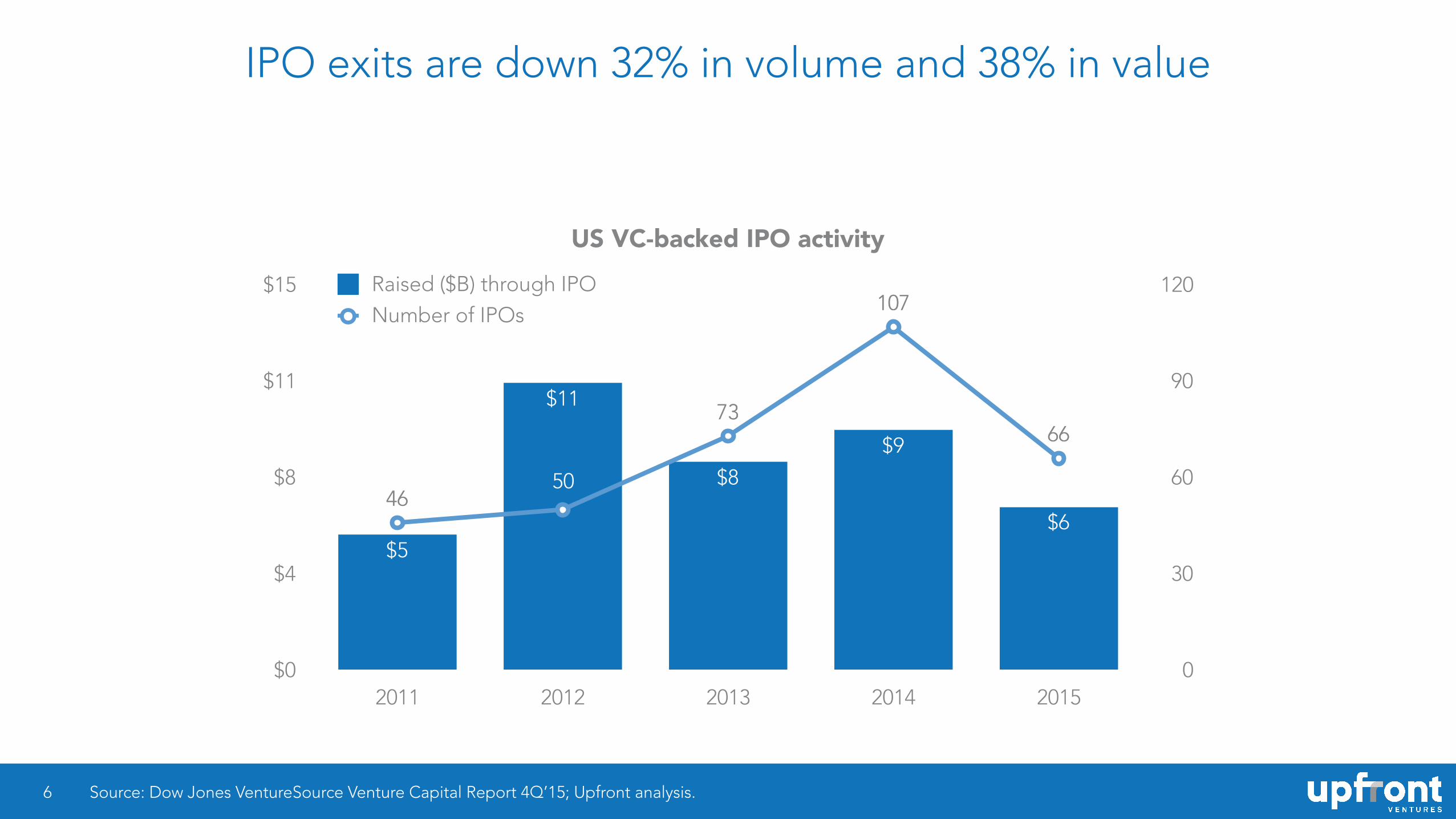

IPO exits are down 32% in volume and 38% in value

6

US VC-backed IPO activity

0

30

60

90

120

$0

$4

$8

$11

$15

2011 2012 2013 2014 2015

Raised ($B) through IPONumber of IPOs

66

107

73

5046

$6

$9

$8

$11

$5

4650

73

107

66

Source: Dow Jones VentureSource Venture Capital Report 4Q’15; Upfront analysis.

50

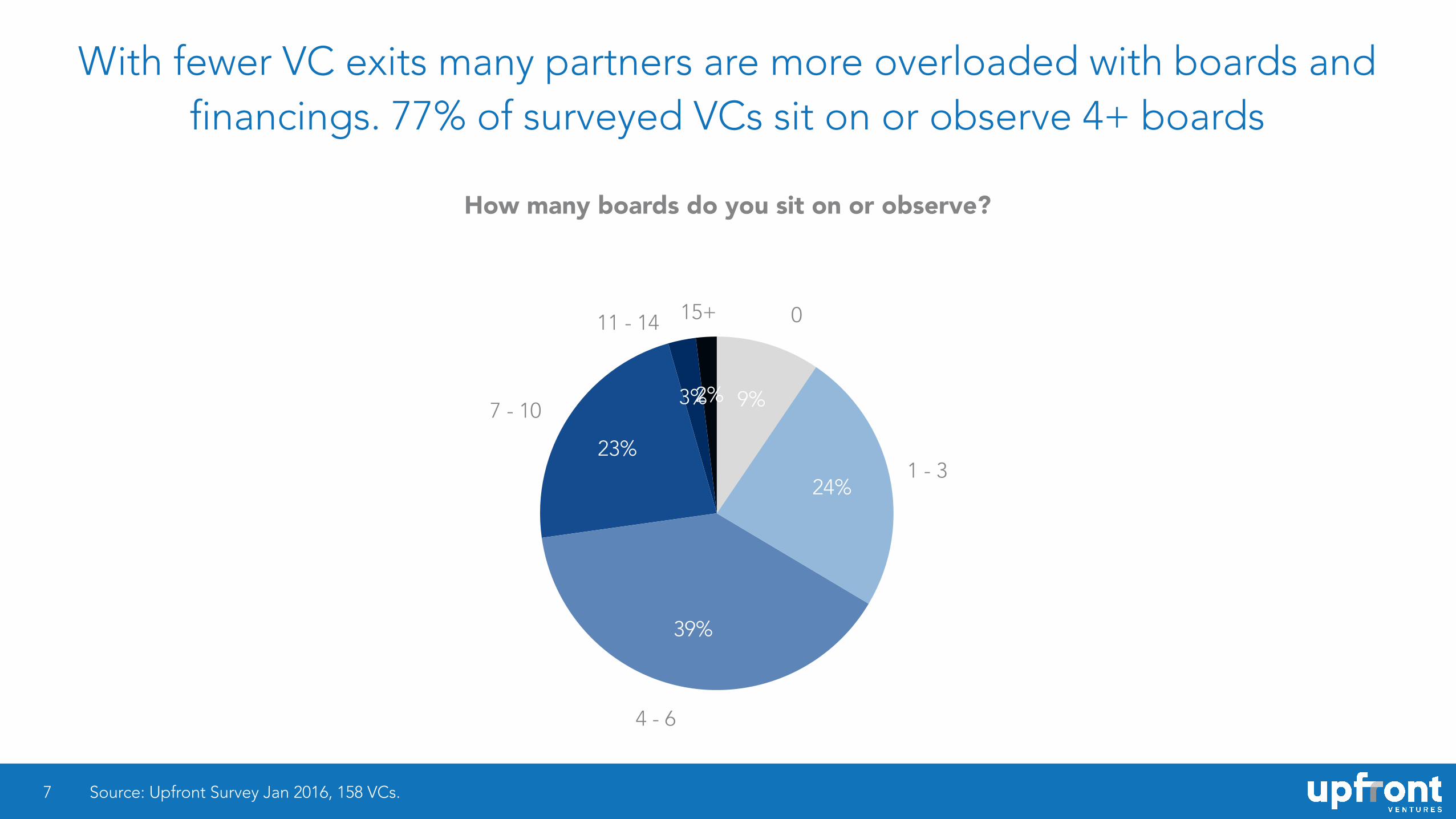

With fewer VC exits many partners are more overloaded with boards and financings. 77% of surveyed VCs sit on or observe 4+ boards

7

2%3%

23%

39%

24%

9%

Source: Upfront Survey Jan 2016, 158 VCs.

How many boards do you sit on or observe?

11 - 14 0

7 - 10

4 - 6

1 - 3

15+

About 2/3rd of respondents and their partners write 1-4 first checks each year

8

How many first check investments do you and a typical partner at your firm make each year?

0%

25%

50%

75%

100%

Respondent Typical partner at respondent's firm

6%6%32%27%

34%28%

24%

25%

5%13%

10+5-103-4

21

Source: Upfront Survey Jan 2016, 159 VCs for Respondent and 158 VCs for Typical partner at respondent’s firm.

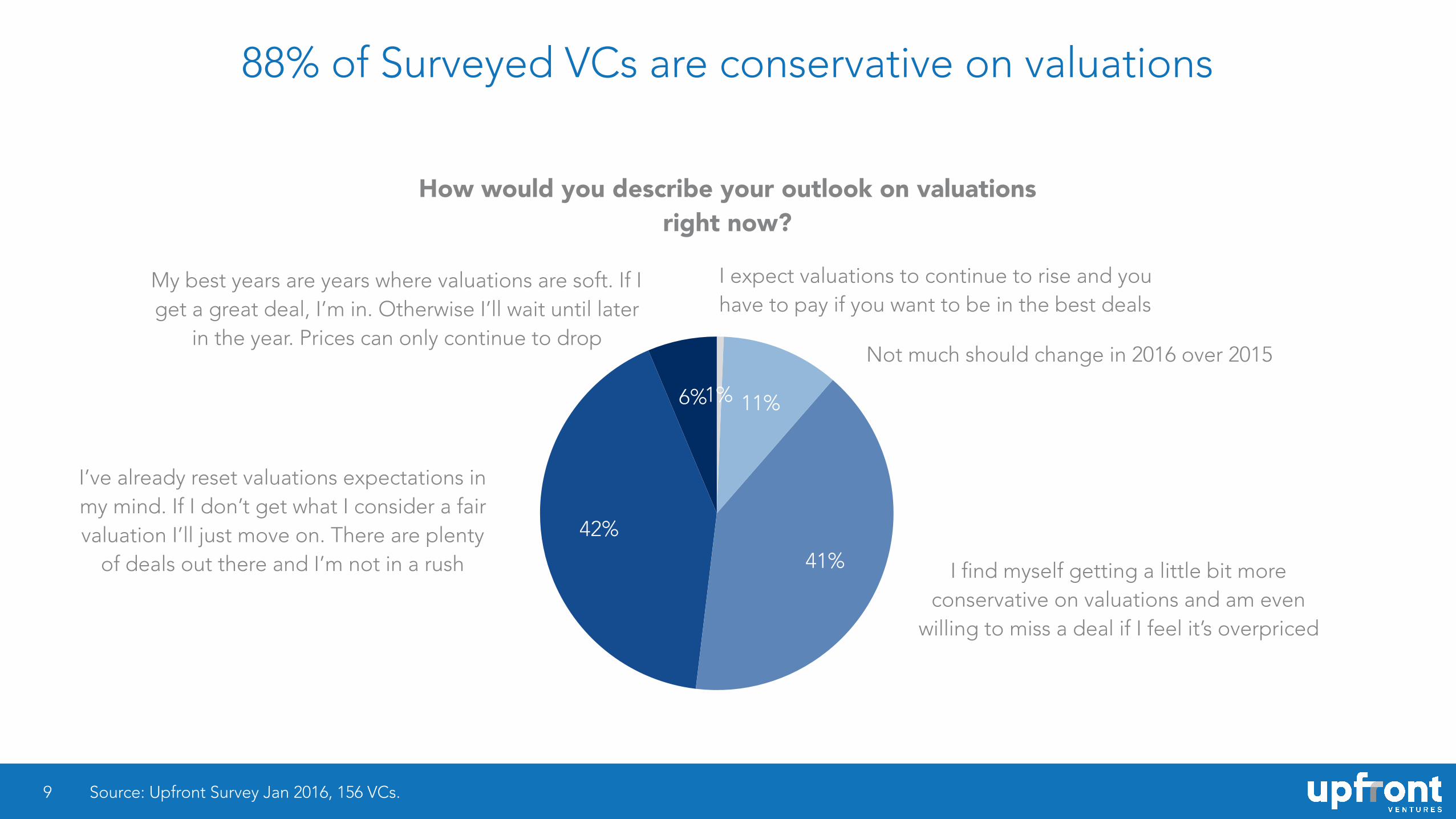

88% of Surveyed VCs are conservative on valuations

9

6%

42%

41%

11%1%

Source: Upfront Survey Jan 2016, 156 VCs.

How would you describe your outlook on valuations right now?

Not much should change in 2016 over 2015

I expect valuations to continue to rise and you have to pay if you want to be in the best deals

My best years are years where valuations are soft. If I get a great deal, I’m in. Otherwise I’ll wait until later

in the year. Prices can only continue to drop

I’ve already reset valuations expectations in my mind. If I don’t get what I consider a fair valuation I’ll just move on. There are plenty

of deals out there and I’m not in a rush I find myself getting a little bit more conservative on valuations and am even

willing to miss a deal if I feel it’s overpriced

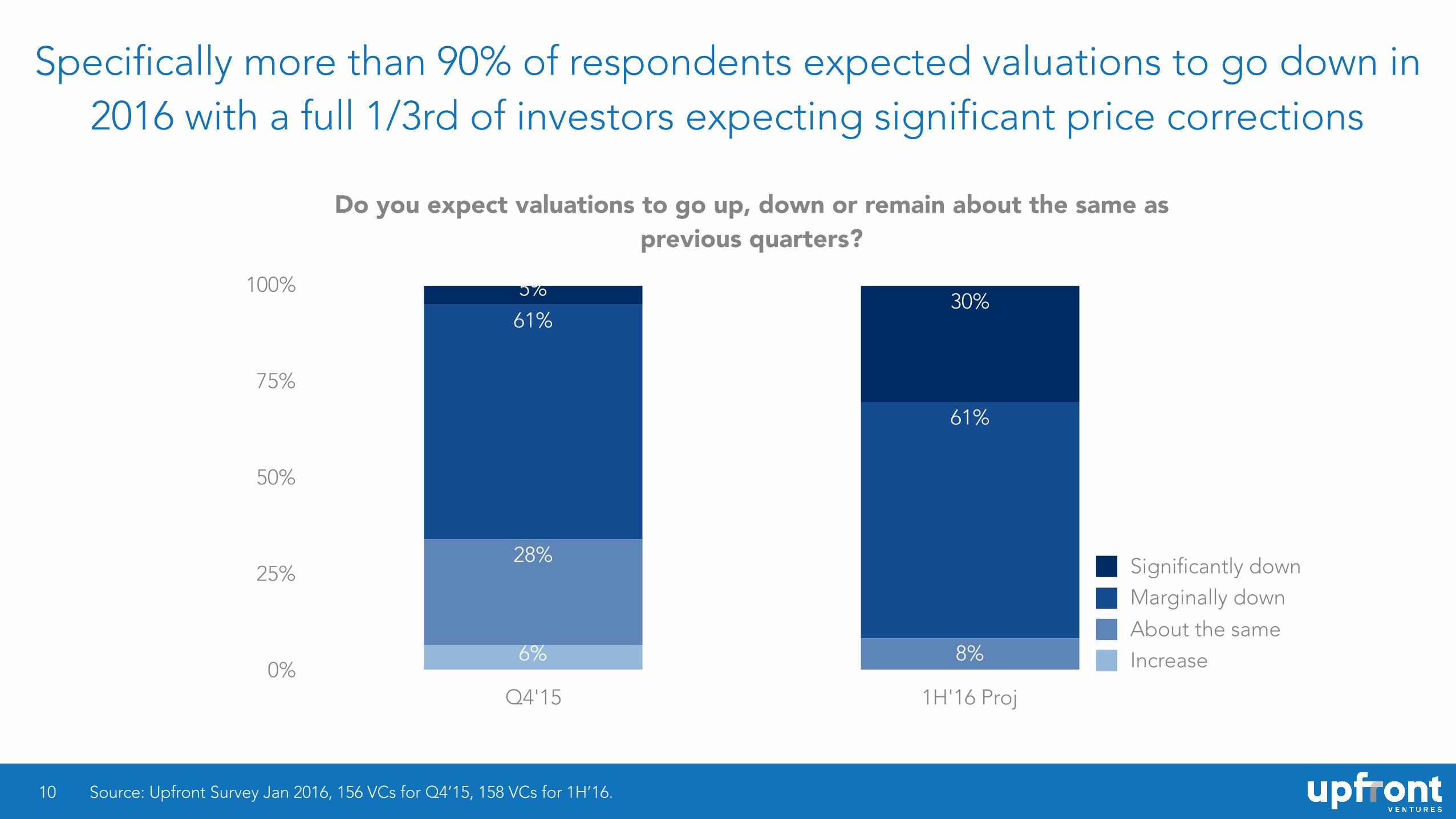

Specifically more than 90% of respondents expected valuations to go down in 2016 with a full 1/3rd of investors expecting significant price corrections

10

Do you expect valuations to go up, down or remain about the same as previous quarters?

0%

25%

50%

75%

100%

Q4'15 1H'16 Proj

30%5%

61%

61%

8%

28%

6% IncreaseAbout the same

Marginally downSignificantly down

Source: Upfront Survey Jan 2016, 156 VCs for Q4’15, 158 VCs for 1H’16.

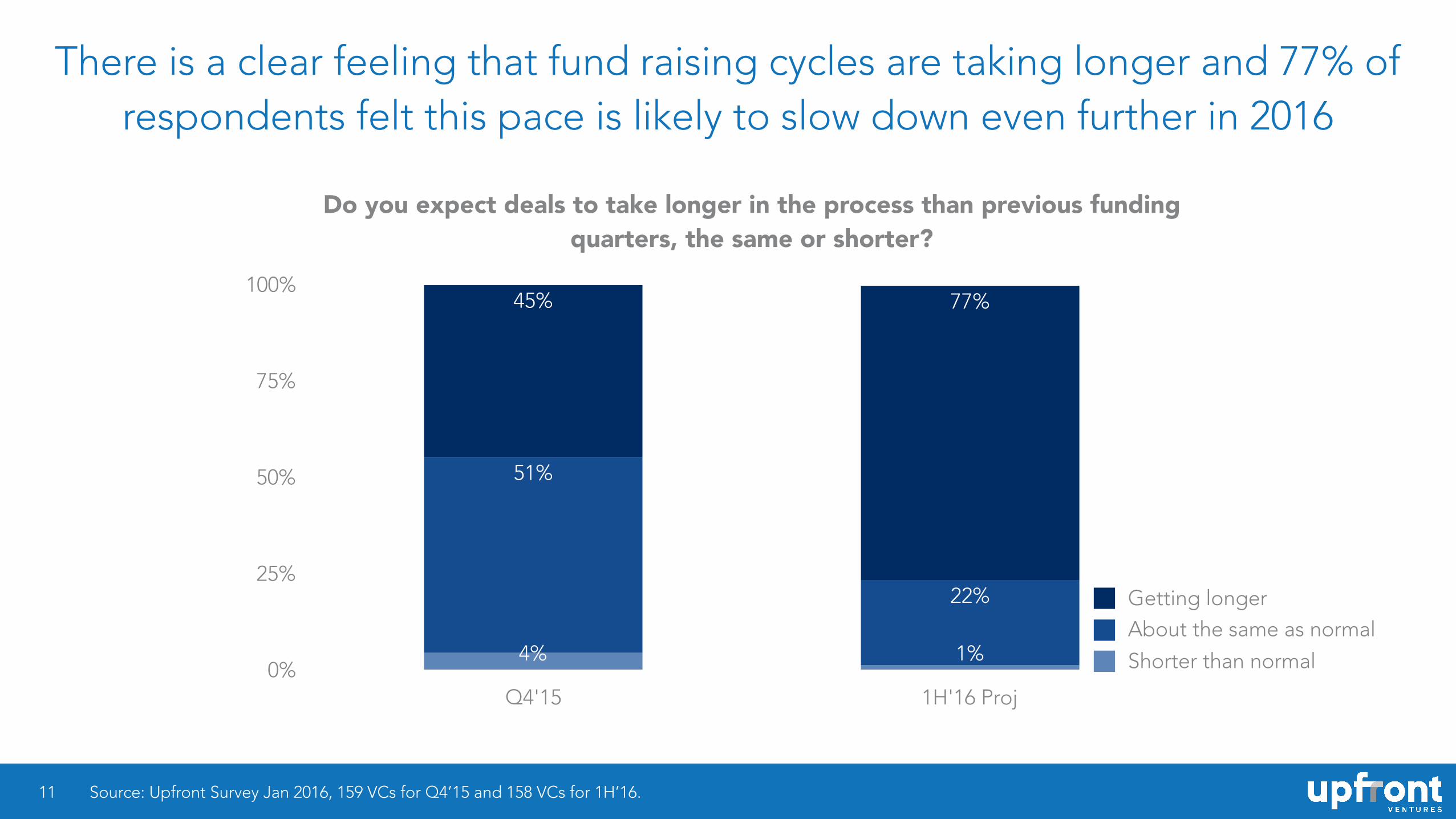

There is a clear feeling that fund raising cycles are taking longer and 77% of respondents felt this pace is likely to slow down even further in 2016

11

Do you expect deals to take longer in the process than previous funding quarters, the same or shorter?

0%

25%

50%

75%

100%

Q4'15 1H'16 Proj

77%45%

22%

51%

1%4% Shorter than normal

About the same as normalGetting longer

Source: Upfront Survey Jan 2016, 159 VCs for Q4’15 and 158 VCs for 1H’16.

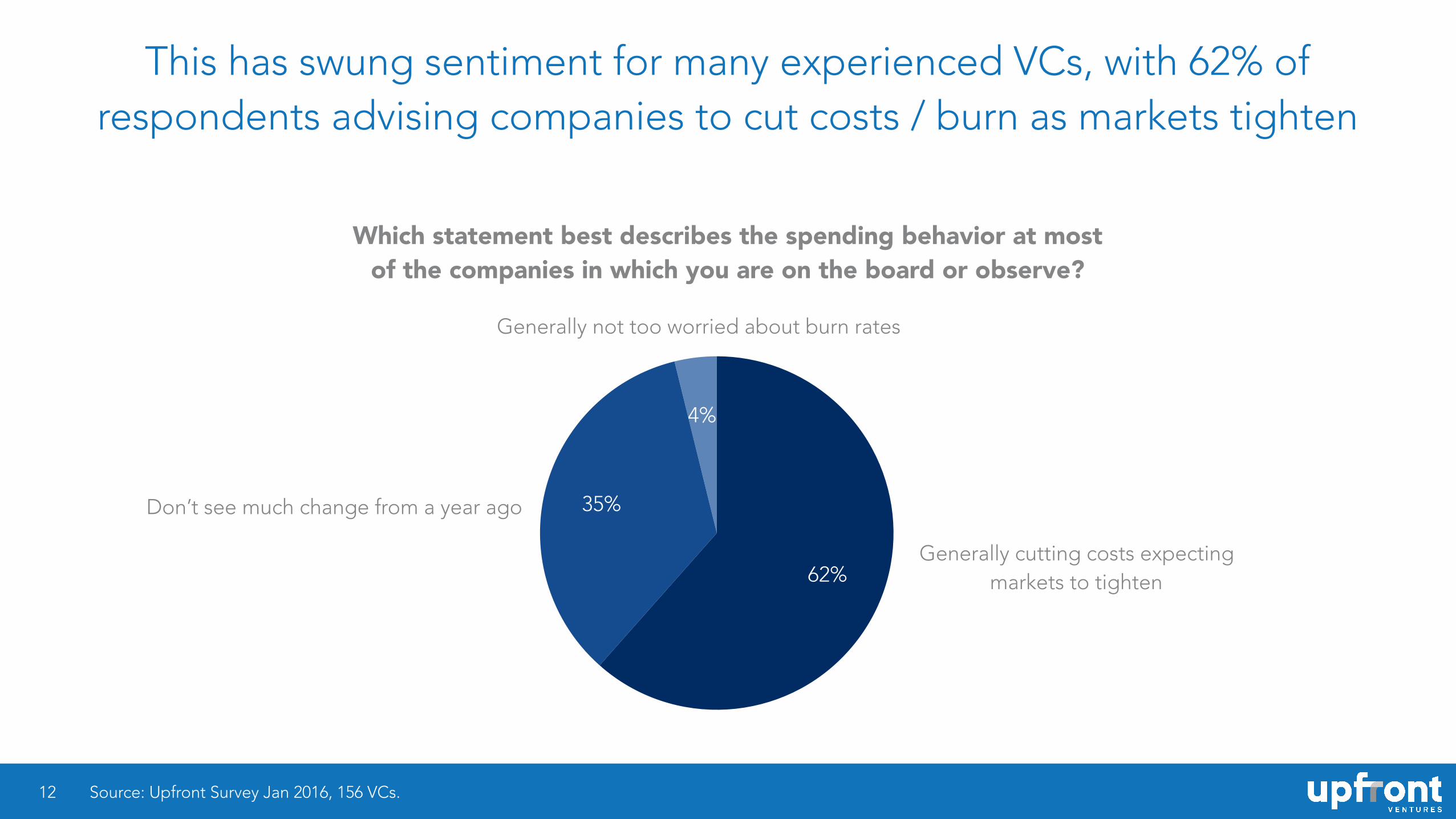

This has swung sentiment for many experienced VCs, with 62% of respondents advising companies to cut costs / burn as markets tighten

12

4%

35%

62%

Source: Upfront Survey Jan 2016, 156 VCs.

Which statement best describes the spending behavior at most of the companies in which you are on the board or observe?

Generally cutting costs expecting markets to tighten

Don’t see much change from a year ago

Generally not too worried about burn rates

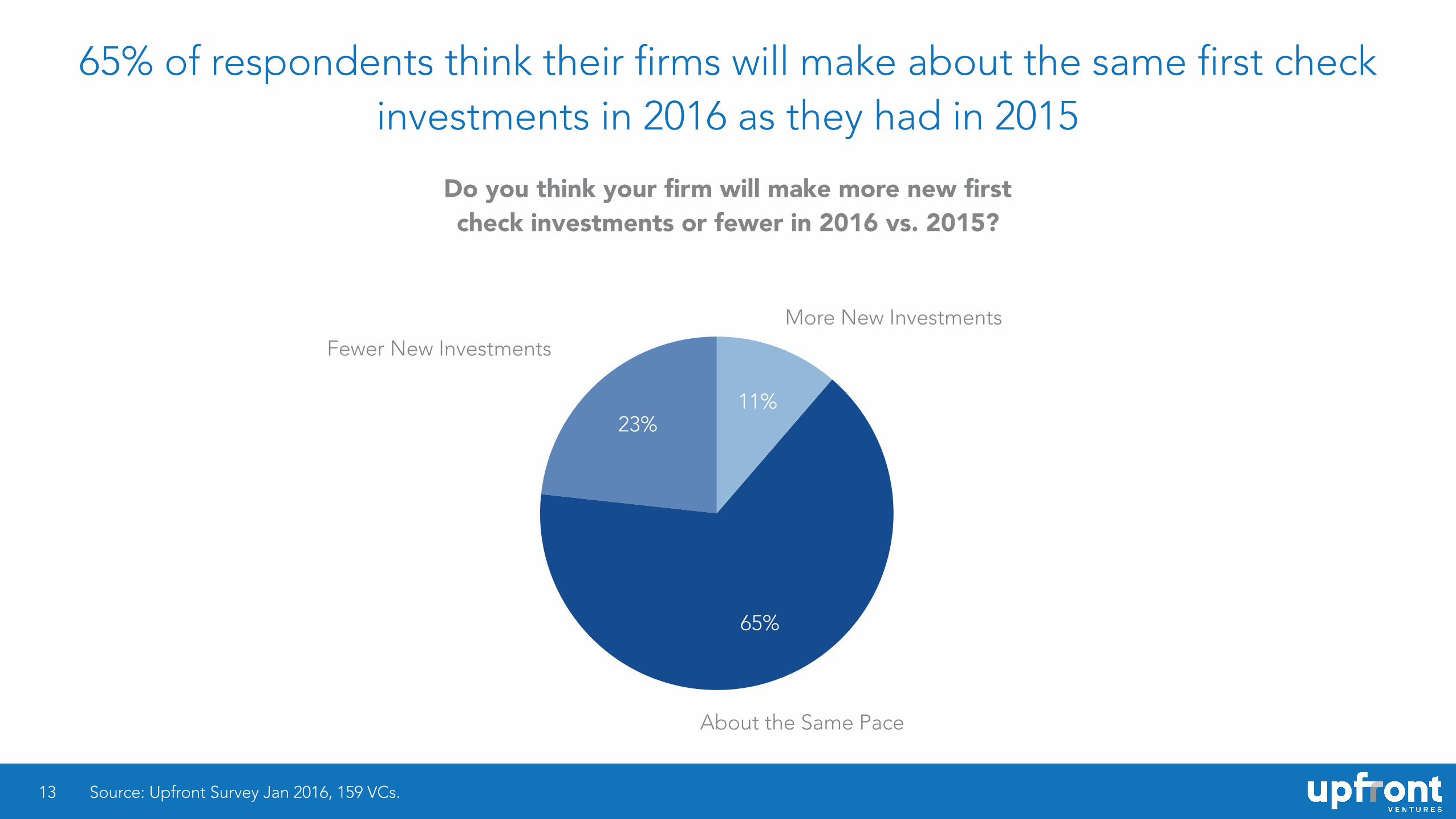

65% of respondents think their firms will make about the same first check investments in 2016 as they had in 2015

13

23%

65%

11%

Source: Upfront Survey Jan 2016, 159 VCs.

Do you think your firm will make more new first check investments or fewer in 2016 vs. 2015?

More New InvestmentsFewer New Investments

About the Same Pace

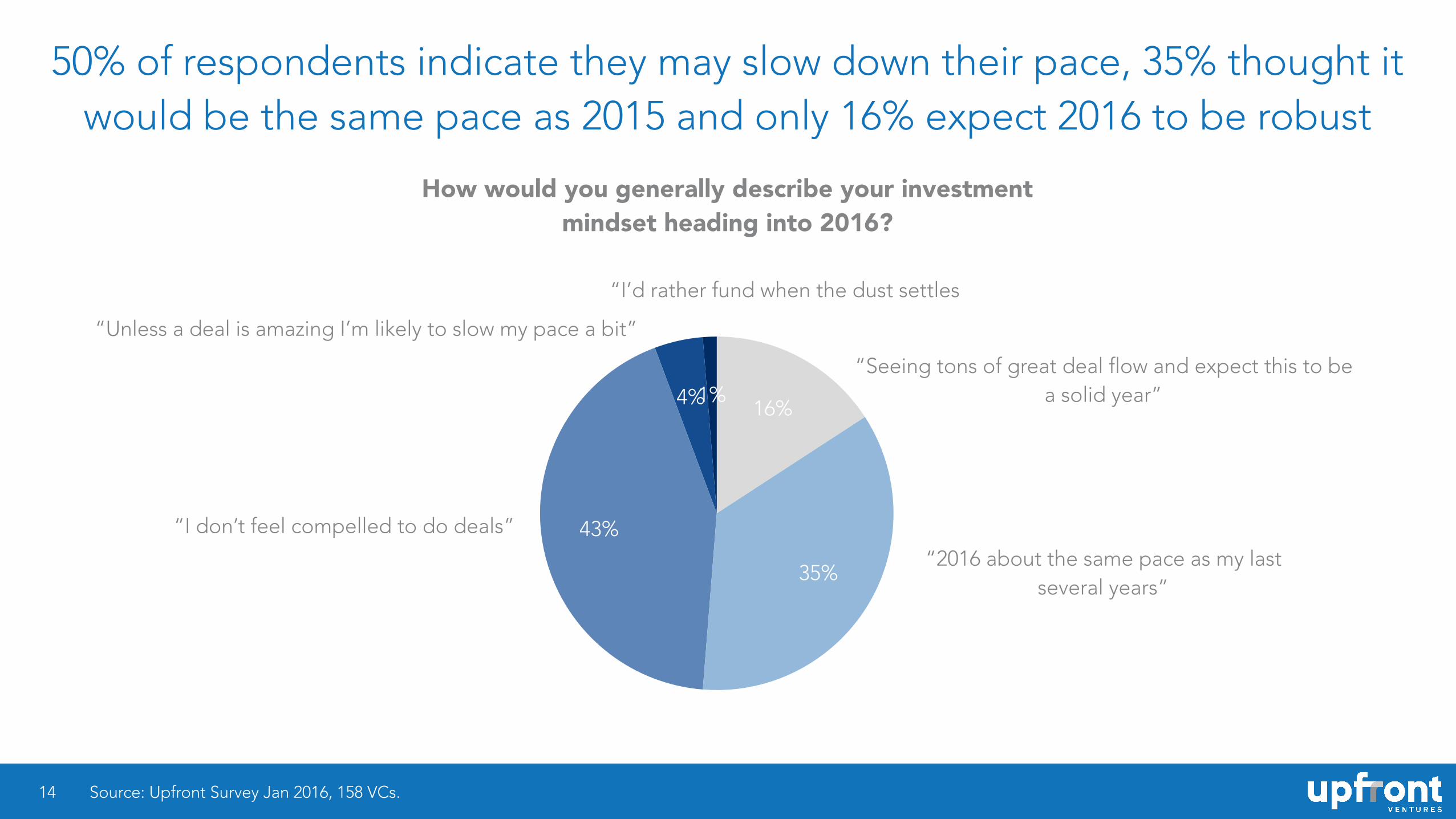

50% of respondents indicate they may slow down their pace, 35% thought it would be the same pace as 2015 and only 16% expect 2016 to be robust

14

1%4%

43%

35%

16%

Source: Upfront Survey Jan 2016, 158 VCs.

How would you generally describe your investment mindset heading into 2016?

“Seeing tons of great deal flow and expect this to be a solid year”

“Unless a deal is amazing I’m likely to slow my pace a bit”

“I don’t feel compelled to do deals”

“2016 about the same pace as my last several years”

“I’d rather fund when the dust settles

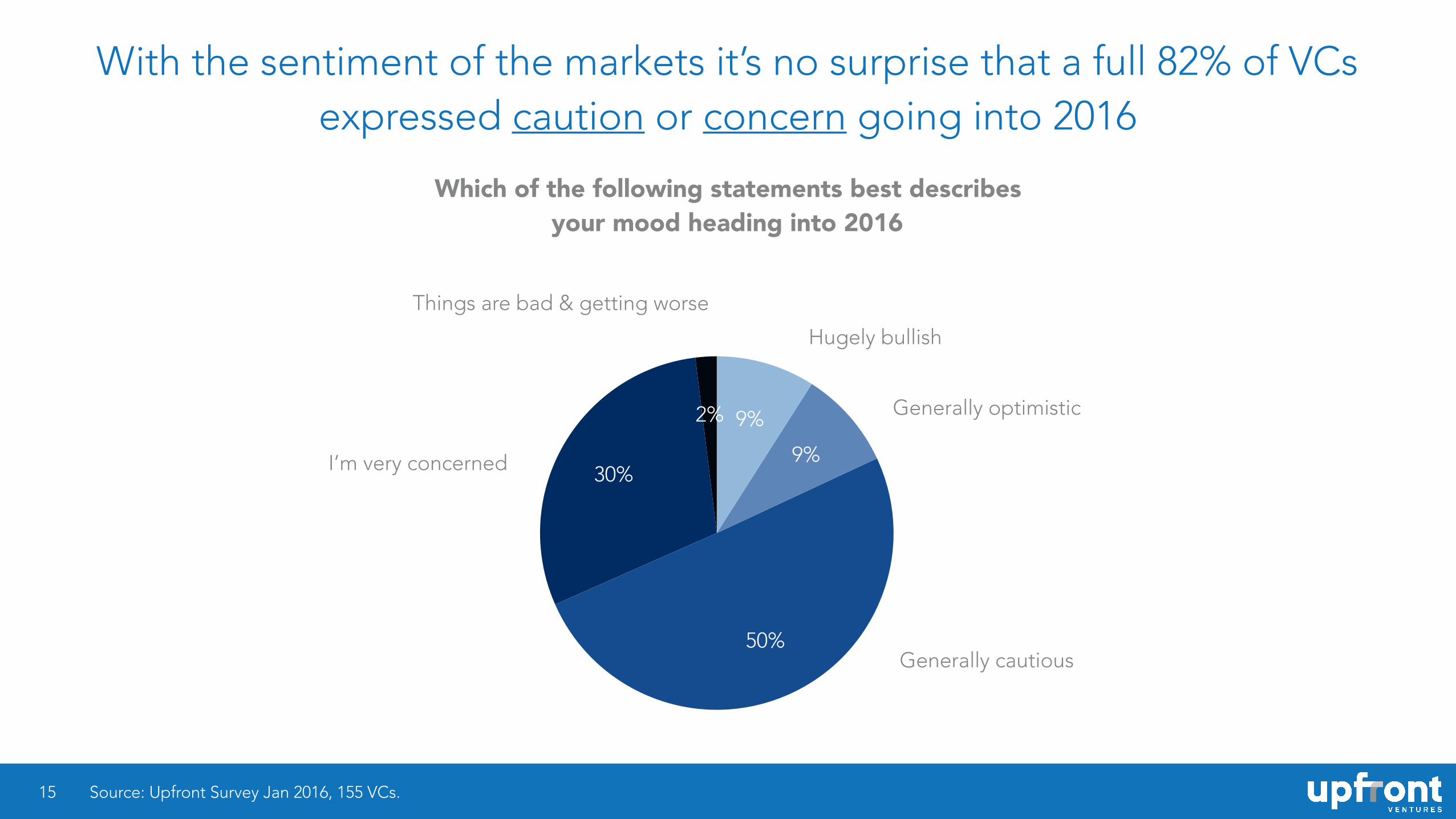

With the sentiment of the markets it’s no surprise that a full 82% of VCs expressed caution or concern going into 2016

15

2%

30%

50%

9%

9%

Source: Upfront Survey Jan 2016, 155 VCs.

Hugely bullish

I’m very concerned

Things are bad & getting worse

Generally cautious

Generally optimistic

Which of the following statements best describes your mood heading into 2016

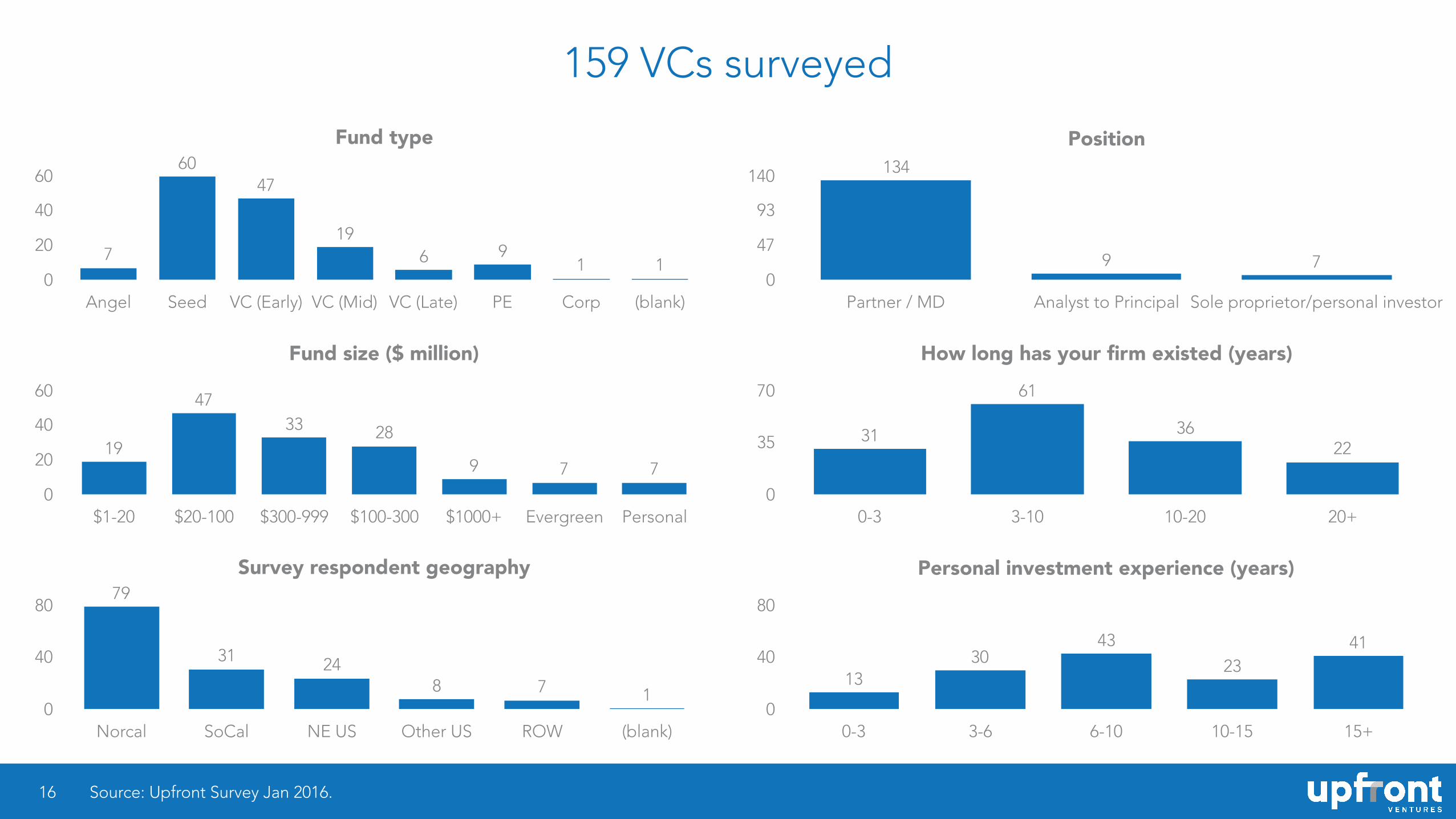

159 VCs surveyed

16

Fund type

0

20

40

60

Angel Seed VC (Early) VC (Mid) VC (Late) PE Corp (blank)

1196

19

4760

7

Source: Upfront Survey Jan 2016.

Fund size ($ million)

0

20

40

60

$1-20 $20-100 $300-999 $100-300 $1000+ Evergreen Personal

779

283347

19

Survey respondent geography

0

40

80

Norcal SoCal NE US Other US ROW (blank)

1782431

79

Position

0

47

93

140

Partner / MD Analyst to Principal Sole proprietor/personal investor

79

134

How long has your firm existed (years)

0

35

70

0-3 3-10 10-20 20+

2236

61

31

Personal investment experience (years)

0

40

80

0-3 3-6 6-10 10-15 15+

4123

4330

13

![[vc 1037 - listing.archiviolocation.com · [vc 1037] ARCHIVIOLOCATION.COM [vc 1037] ARCHIVIOLOCATION.COM [vc 1037] ARCHIVIOLOCATION.COM [vc 1037] ARCHIVIOLOCATION.COM. archivio location](https://img.pdfslide.us/doc/110x75/5fcd99d1df347e1ae154645c/vc-1037-vc-1037-archiviolocationcom-vc-1037-archiviolocationcom-vc-1037.jpg)