Embed Size (px)

Citation preview

Financial Best Practices

We divvy up financial management into nine best practice areas, and

apply our proven methods to all of our entrepreneurial client partners.

Their success is our success which we experience every day as we coach them to increase revenue, reduce costs, optimize profit, and get out from under the piles of bills and invoices to do what

they love to do.

Financial Team

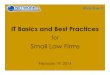

Bookkeeper: Accomplishes financial tasks. Processes all incoming mail, pays bills, generates

invoices, makes bank deposits, implements collection efforts, processes payroll, generates

1099s, and closes the book.

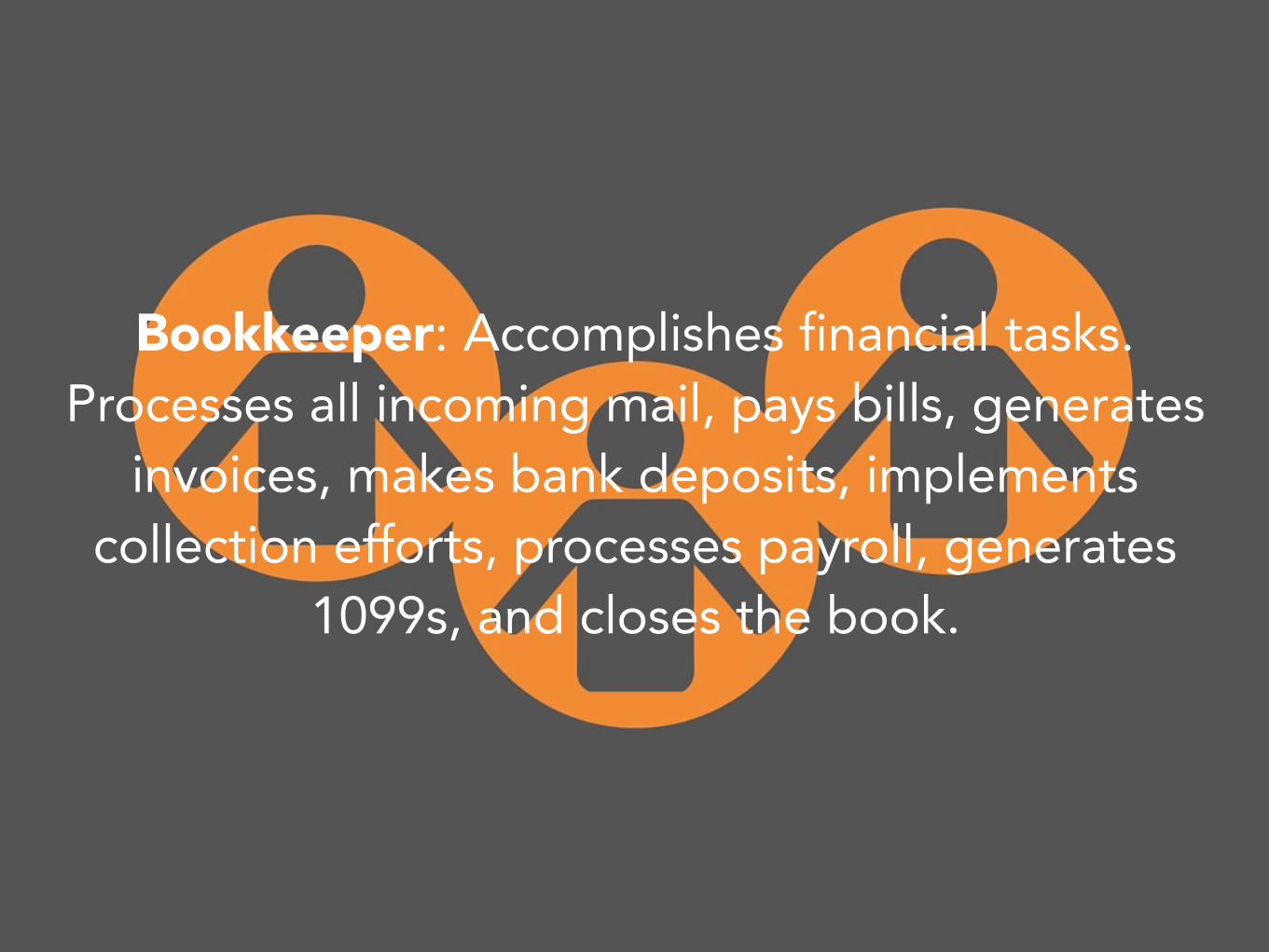

Accountant: Ensures accuracy of reports. Classifies all transactions, makes adjusting journal entries, reconciles accounts, generates reports,

and creates the annual budget.

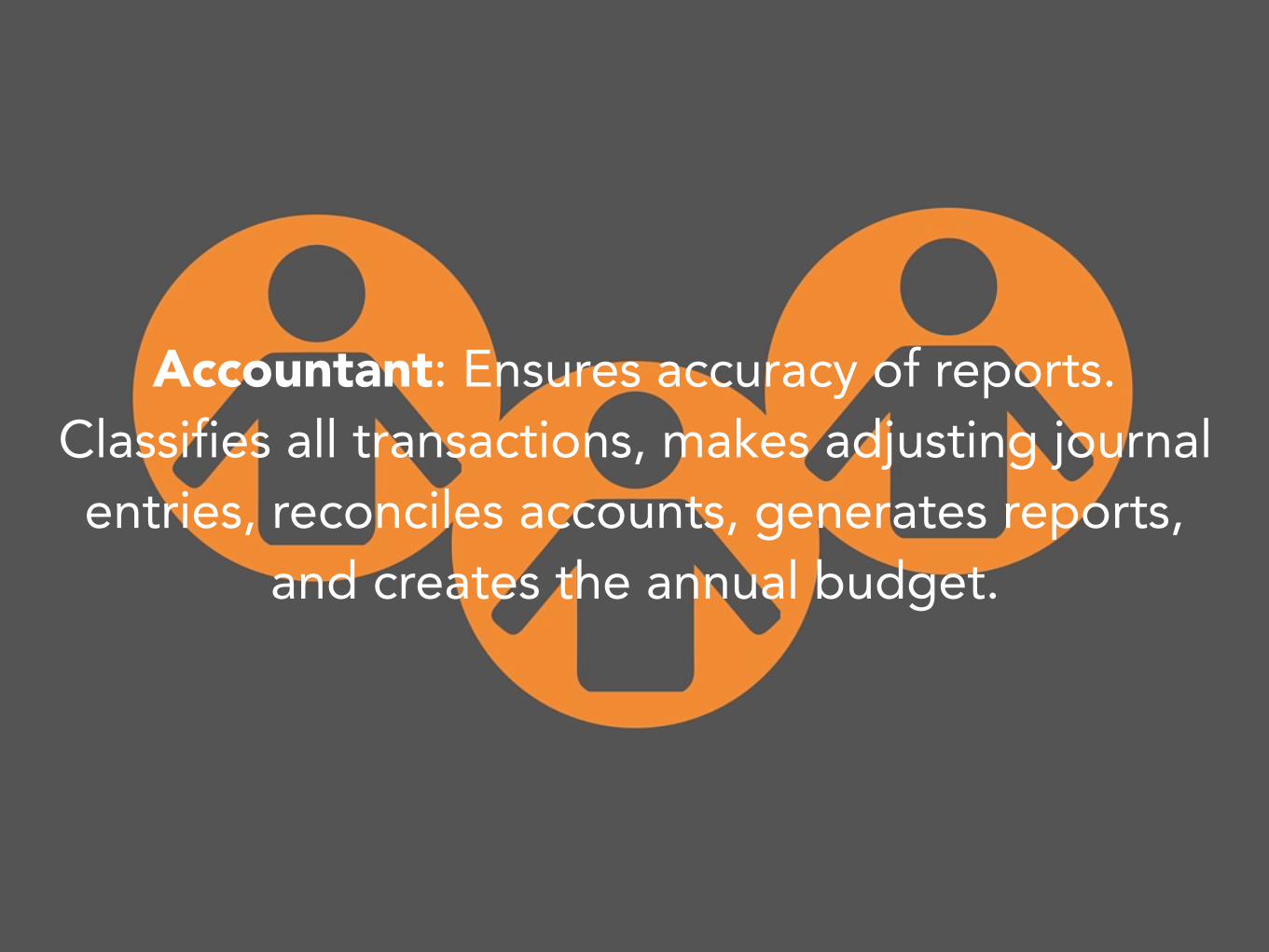

CFO or Analyst: Interprets the reports, manages cash flow, and maintains the financial

health of the organization. Monitors bank balances, analyzes weekly AR and AP reports,

analyzes monthly and quarterly reports, recommends actions to adjust operating

expenses, reduce debt, and generate quarterly distributions.

CEO or Strategist: Uses the words of wisdom from the CFO to set strategy and vision,

allocate capital, build culture, lead the senior team, and cultivate the growth of the

organization.

CPA or Tax Agent: Manages and reports tax liabilities, recommends semiannual

adjustments to mitigate unexpected tax payments, prepares and files tax returns.

Corporate Entity

Incorporating a business turns a sole proprietorship or general partnership into a company formally recognized by your state

of incorporation.

When you incorporate, the company becomes its own legal business structure — set apart from the individuals who founded

the business.

Partner with your CPA to determine the most efficient legal structure according to the type of business, number of owners, and financial situation to avoid risk and to take advantage of the appropriate investment vehicles and

tax planning options.

There are 4 types of businesses: sole proprietorships

partnerships corporations cooperatives

Applications & Tools

Use a robust accounting software package to keep books and manage finances.

Configure the software to meet the specific needs of your company to produce reports

that answer the question you are asking about the financial health of your organization.

Bank with financial institutions that offer full-featured, secure online reporting

and bill pay services.

Sync your financial data between banks and your accounting software for efficient

and accurate management.

Ensure your financial data is backed up, secure, and available 24/7.

Documentation & Data

Develop a ‘Policies & Procedures’ manual that focuses on the management of digital and

hard copy documents and adhere to it 100%.

Remain compliant to IRS regulations to be prepared for unexpected IRS reviews

and/or audits.

Ensure your digital financial data is accessible 24/7 to all users and is hosted in a secure environment.

Money In

Track time and expenses for internal staff and external contractors and accurately transfer

the data onto invoices that are prepared and distributed on a regular schedule.

Manage collections on a 30-45-60 day schedule to regulate cash flow.

Implement processes to manage expenses paid with cash to reduce risk of theft.

Deposit cash and checks into your bank account within 24 hours of receiving payment, and document payments

thoroughly to allow for detailed auditing.

Review your merchant bank vendors regularly to ensure accuracy and to monitor fees.

Money Out

Develop and adhere to standard procedures to receive and input bills into the accounting software that ensures the accurate and timely tracking of payables

and the management of cash flow.

Use digital methods to pay bills through your bank and other automatic systems to efficiently

process payables on time by eliminating the need for check signing and snail mail.

When sales tax is collected, report on and pay according to state-mandated deadlines.

Payroll, Distribution & Deferred Income

Contract with a reputable payroll vendor to process payroll for W2 employees.

Track contractor payments in real time to be prepared for annual 1099-MISC tax reporting.

Process payroll tax returns and payments according to IRS and state guidelines.

Distribute profits quarterly.

Implement a qualified deferred compensation plan that is structured and compiled with

to maximize contributions for key employees.

Review the qualified plan regularly and communicate to all employees annually

to encourage participation.

Reporting, Analysis & Cash Flow

Escrow your profit weekly — prior to incurring operational expenses — and allocate funds

against debt, savings, taxes, capital improvements, and the distribution of profit.

Reconcile all accounts monthly to ensure the accuracy of deposits and withdrawals.

Design standard and custom financial reports around your specific business needs,

and analyze them on a regular basis.

Manage against key metrics monthly, and review their effectiveness quarterly.

Analyze cash flow quarterly to be prepared for kinks in the budget.

Strive to maintain a three month operational reserve in an interest-bearing savings/money

market account and operate debt free.

Financial Events

Process W2 and 1099 forms during the month of January, and distribute by the annual IRS deadline.

Submit financial reports and supporting documentation to your CPA at least 30 days prior to the IRS and state tax filing deadlines

for use in preparing and submitting tax returns without an extension.

Partner with your CPA two times per year for tax planning purposes to

mitigate tax liability surprises.

Set and measure strategic and financial goals each quarter.

Finalize an annual budget by December 31st based on the prior year’s financial data.

We love the pure spirit of the American entrepreneur.

To find out more, download our eBook now.