Embed Size (px)

Citation preview

On the cost of climate change for an

insurance company

Esterina Masiello

ISFA - ICJ – Université Lyon 1 [email protected]

Joint work with Dominik Kortschak and Pierre Ribereau

Our common future under climate change

Paris - July 2015

Climate is changing, so…

1. What is the impact on natural disasters? More particularly on tropical cyclones?

1. ...and the impact on insurance companies in term of losses?

1. and how to integrate climate change in actuarial models?

The impact on tropical cyclones (Source: IPCC AR5 WG1 and SREX Report)

• Frequency and intensity of the strongest tropical cyclones have increased in the North Atlantic basin since the 1970s (very strong evidence)

• As to the future, decreases or no change in the overall global tropical cyclone frequency but substantial increase in the frequency of the most intense storms in some ocean basins by the end of 21st century

• Likely increase in mean maximum wind speed in tropical cyclones as well as in heavy rainfalls associated with tropical cyclones which is expected to intensify cyclone's impacts.

And what about related losses?

• Direct and insured losses from weather-related disasters have substantially increased in recent decades

• With respect to the future, the projected increase in the

frequency of most intensive tropical cyclones will result in higher direct economic losses and loss variability.

This will challenge insurance systems to offer coverage for

premiums which are still affordable while at the same time requiring more risk-based capital (AR5, WG2). If insurance coverage is to be maintained, insurers would need more risk-based capital to indemnify catastrophic losses and remain financially solvent.

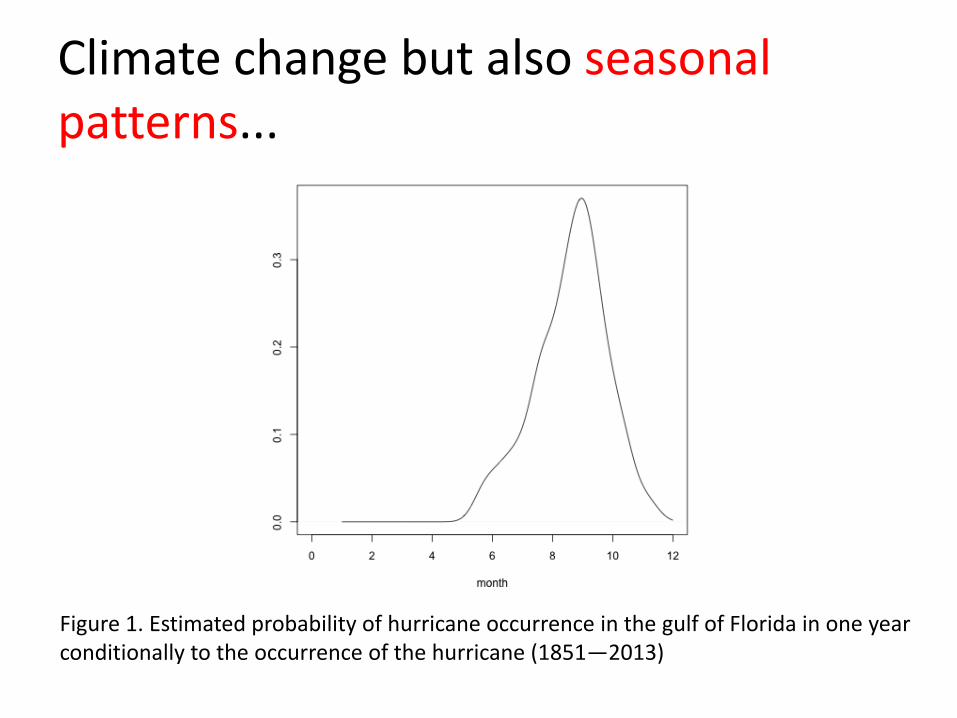

Climate change but also seasonal patterns...

Figure 1. Estimated probability of hurricane occurrence in the gulf of Florida in one year conditionally to the occurrence of the hurricane (1851—2013)

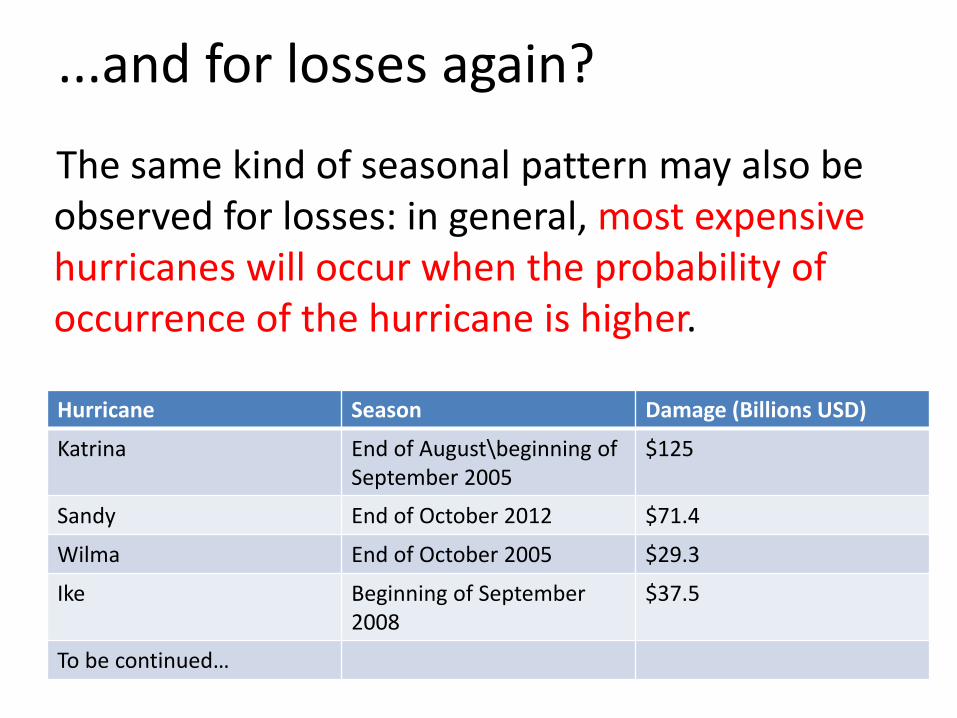

...and for losses again?

The same kind of seasonal pattern may also be observed for losses: in general, most expensive hurricanes will occur when the probability of occurrence of the hurricane is higher.

Hurricane Season Damage (Billions USD)

Katrina End of August\beginning of September 2005

$125

Sandy End of October 2012 $71.4

Wilma End of October 2005 $29.3

Ike Beginning of September 2008

$37.5

To be continued…

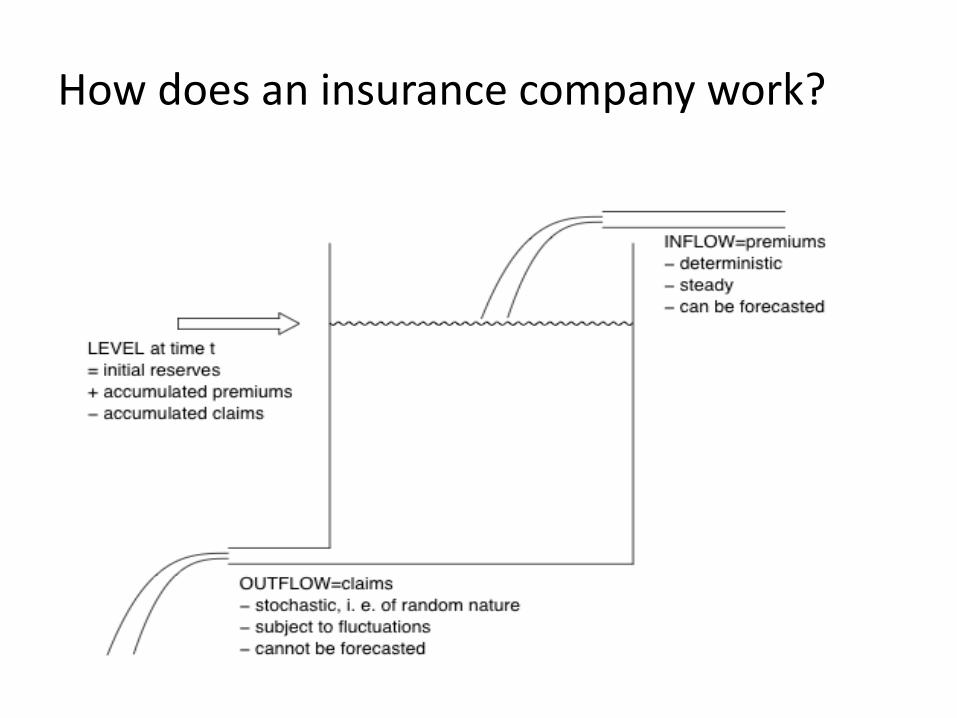

How does an insurance company work?

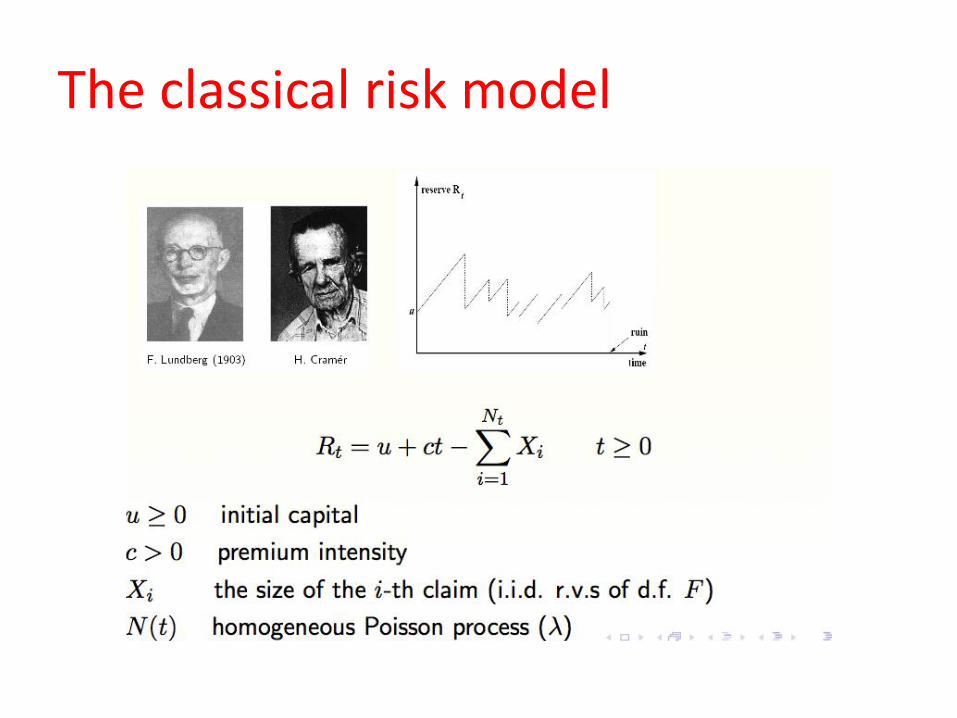

The classical risk model

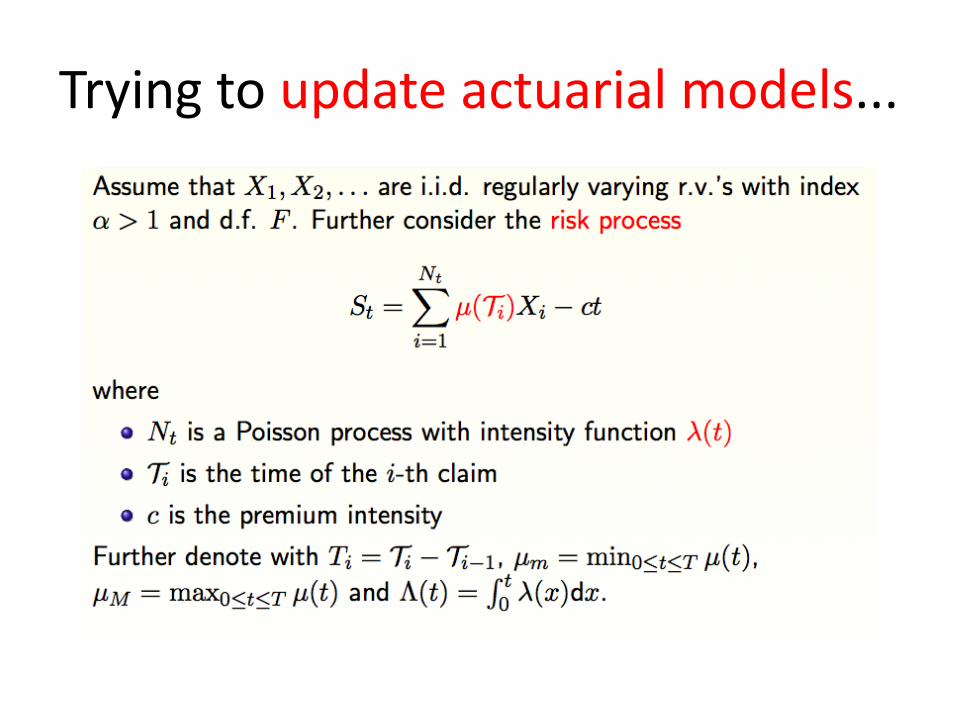

Trying to update actuarial models...

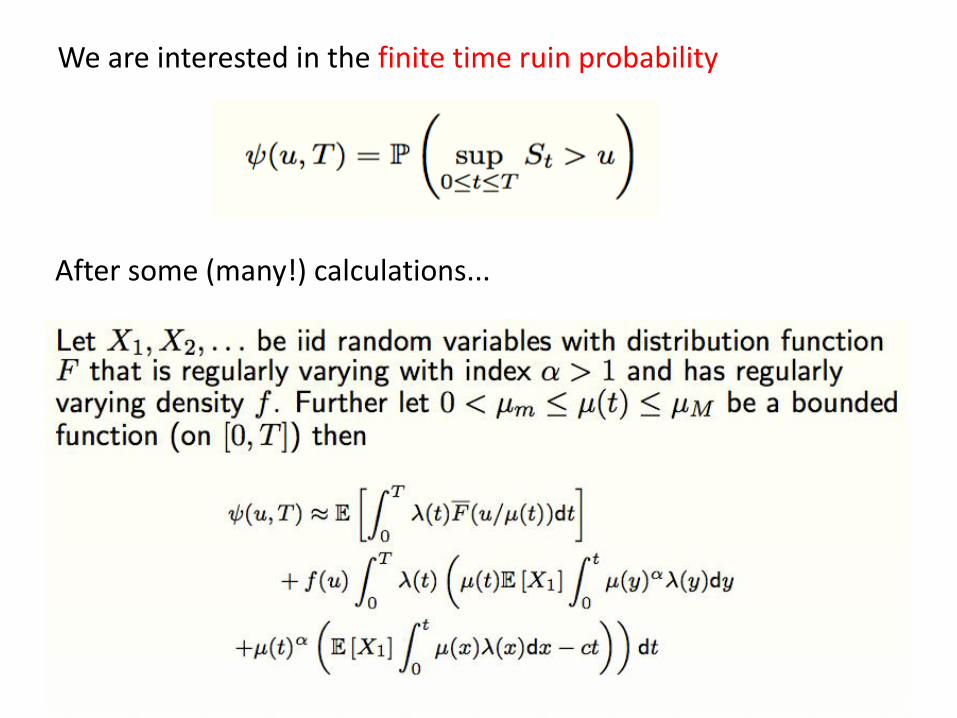

We are interested in the finite time ruin probability

After some (many!) calculations...

How may we apply this theoretical result to try to evaluate the cost of climate change for an insurance company?

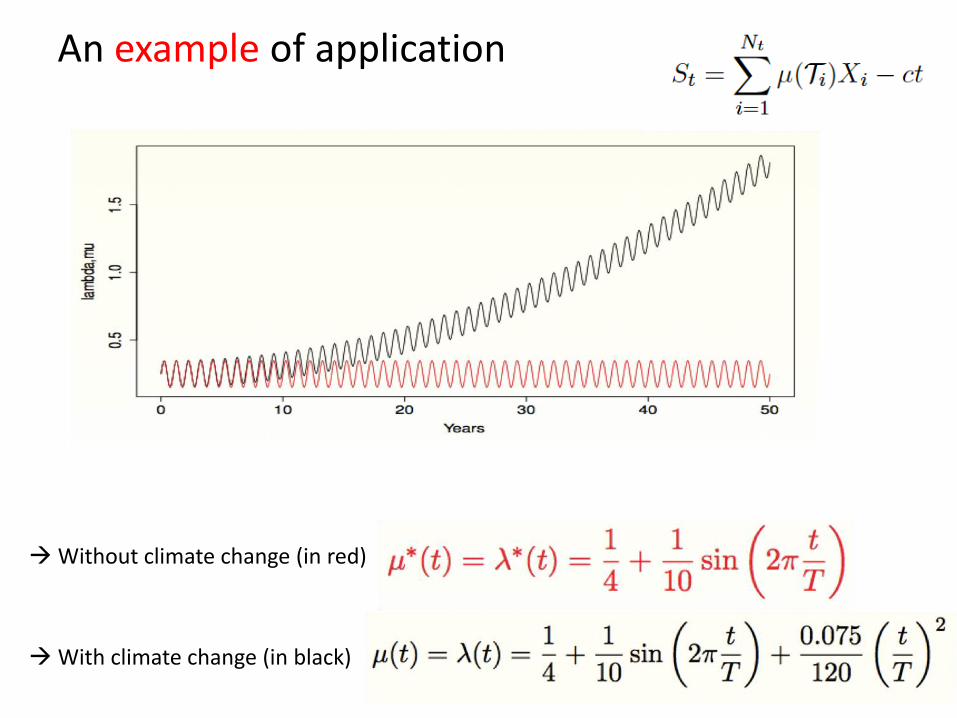

An example of application

Without climate change (in red)

With climate change (in black)

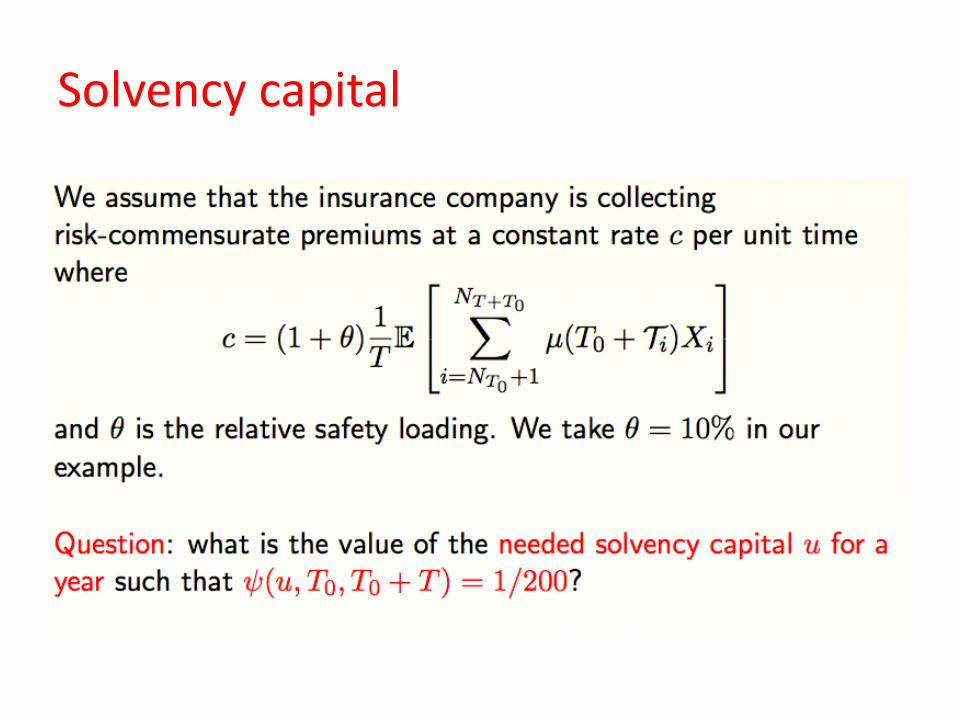

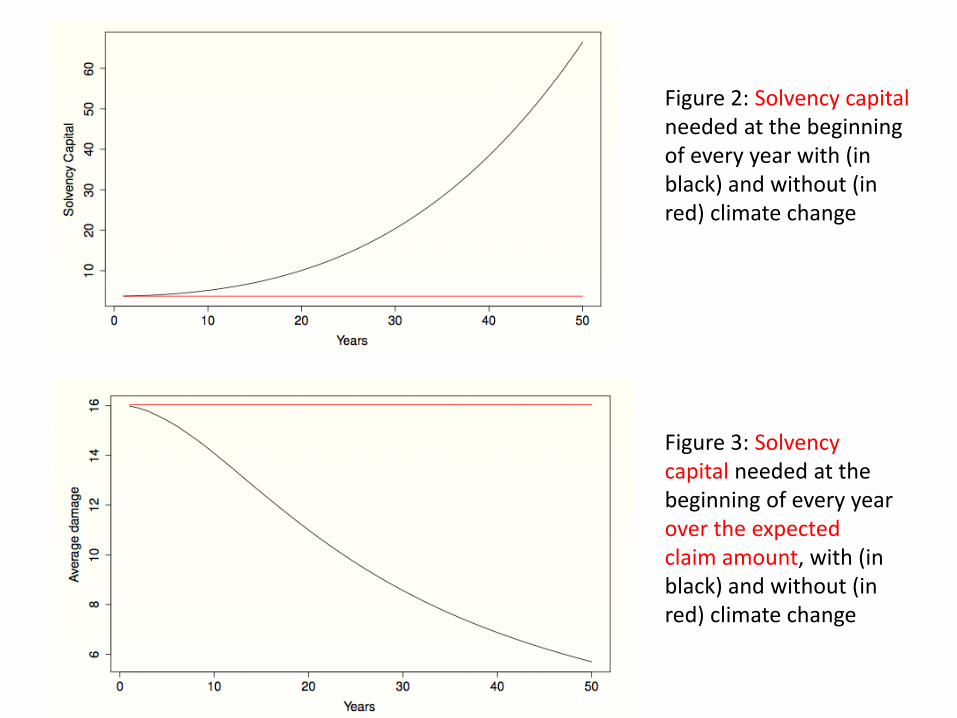

Solvency capital

Figure 2: Solvency capital needed at the beginning of every year with (in black) and without (in red) climate change

Figure 3: Solvency capital needed at the beginning of every year over the expected claim amount, with (in black) and without (in red) climate change

Trying to define the cost of climate change…

What is the extra amount of money (cost of trend) that an insurance company has to provide in a model with climate change?

The accumulate cost of trend is the difference between the solvency capital with trend, and the solvency capital without trend and the collected premiums times the safety loading.

Cost of climate change for the year t = accumulated cost of climate change for the year t - accumulated cost of climate change for the year t-1.

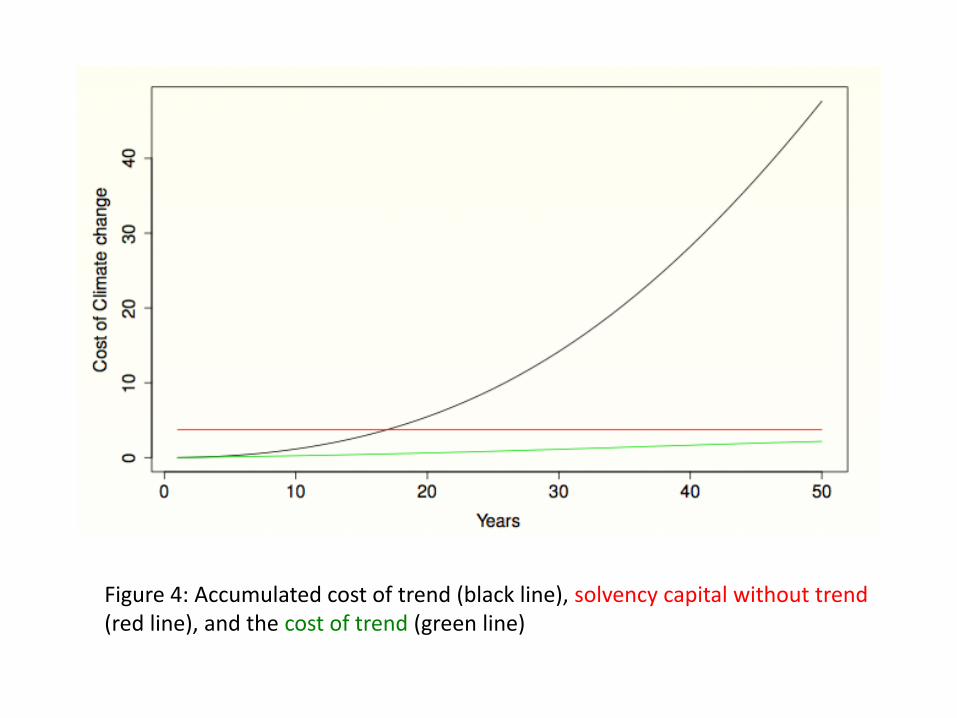

Figure 4: Accumulated cost of trend (black line), solvency capital without trend (red line), and the cost of trend (green line)

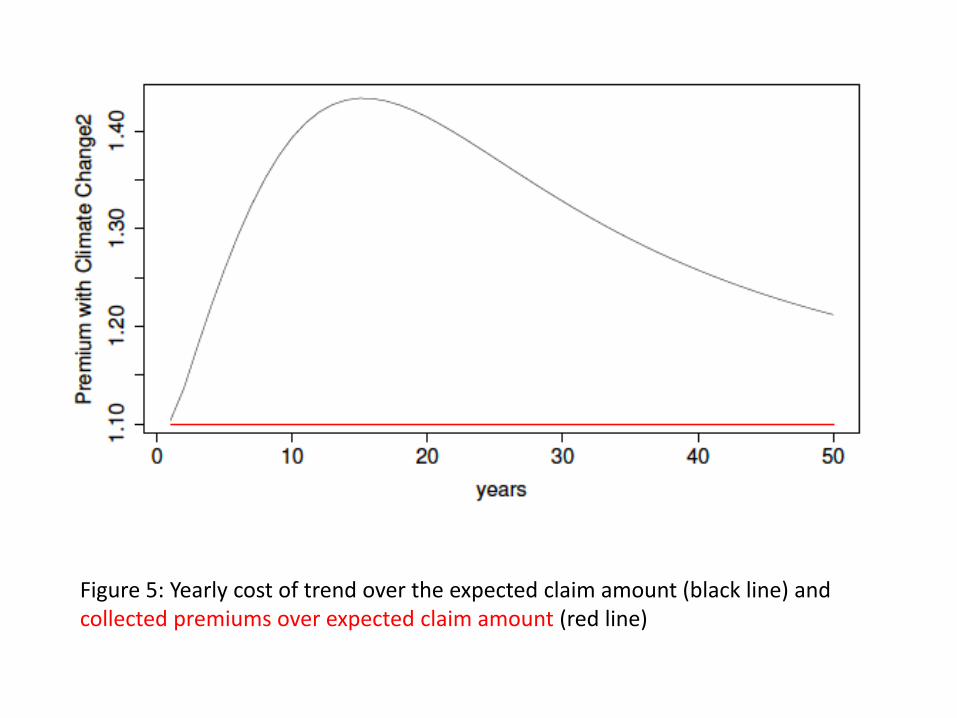

Figure 5: Yearly cost of trend over the expected claim amount (black line) and collected premiums over expected claim amount (red line)

In conclusion…

• Insurance company are particularly concerned by natural disasters and the impact of those disasters has been increasing because the climate has been changing!

• This may affect the solvency of an insurance company!

• Climate change also has the potential to threaten the widespread availability and affordability of insurance for people and their property in many regions.