Embed Size (px)

Citation preview

#RSPS15

#RSPS15

LeverageProductIntelligenceToImproveCategoryPerformance

ThisHolidaySeason

SPONSORED BY:

#RSPS15

FollowthiseventonLinkedIn&Twi3er

#RSPS15RetailTouchpoints:@RTouchPoints

Ugam:@UgamSucharitaMulpuru:@smulpuruSudhirHolla:@sudhirhollaDebbieHauss:@dhauss

#RSPS15

Ques=ons,Tweets&Resources

SubmityourquesDons

here

Downloadtoday’sresources

JointheconversaDon#RSPS15

#RSPS15

AboutRetailTouchPoints

ü Launched in 2007

ü Over 30,000 retail subscribers

ü To provide executives with relevant, insightful content across a variety of digital medium

Sign up for our weekly newsletter:

www.retailtouchpoints.com/subscribe

#RSPS15

MODERATOR:DebbieHaussEditor-in-Chief,RetailTouchPointsPanelists

SudhirHollaSeniorVicePresident,[email protected]@sudhirholla

SucharitaMulpuruVP,PrincipalAnalystservingeBusinessandChannelStrategyProfessionalsForrestersmulpuru@forrester.com@smulpuru

Private & Confidential

A look at Product Types of the Future Sucharita Mulpuru, Analyst

September 22, 2015

Private & Confidential

© 2015 Forrester Research, Inc. Reproduction Prohibited 7

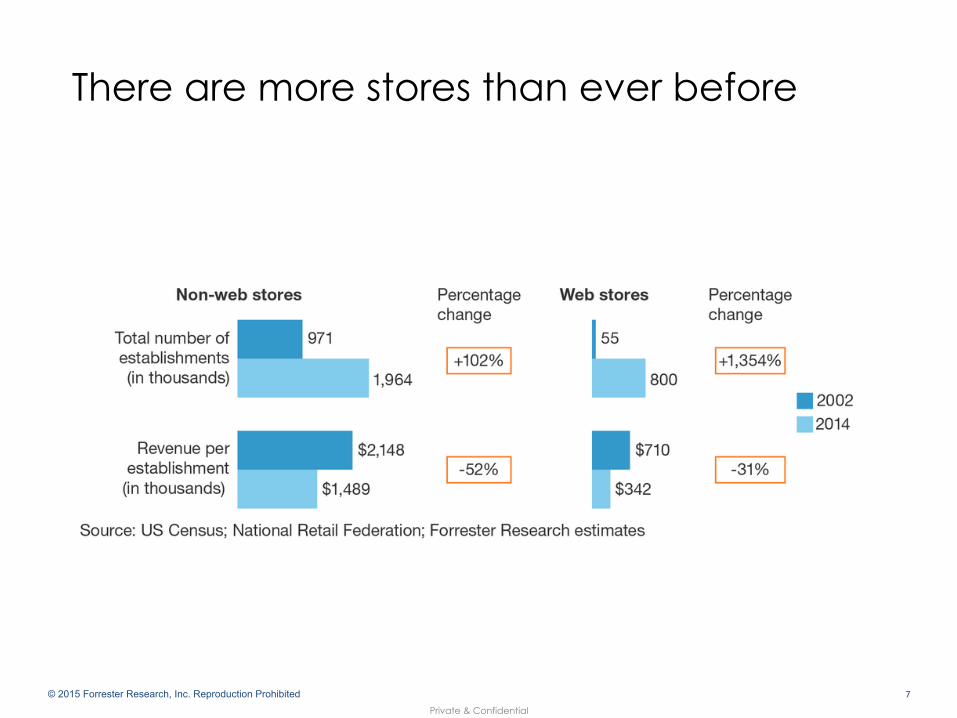

There are more stores than ever before

Private & Confidential

© 2015 Forrester Research, Inc. Reproduction Prohibited 8

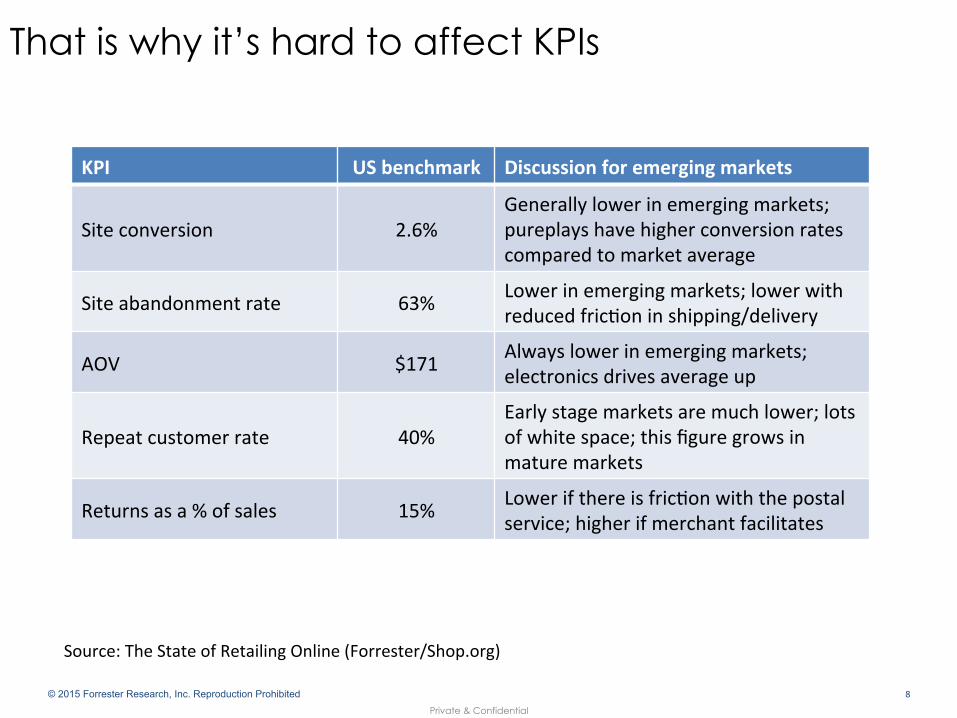

That is why it’s hard to affect KPIs

KPI USbenchmark Discussionforemergingmarkets

Siteconversion 2.6%Generallylowerinemergingmarkets;pureplayshavehigherconversionratescomparedtomarketaverage

Siteabandonmentrate 63% Lowerinemergingmarkets;lowerwithreducedfric=oninshipping/delivery

AOV $171 Alwayslowerinemergingmarkets;electronicsdrivesaverageup

Repeatcustomerrate 40%Earlystagemarketsaremuchlower;lotsofwhitespace;thisfiguregrowsinmaturemarkets

Returnsasa%ofsales 15% Lowerifthereisfric=onwiththepostalservice;higherifmerchantfacilitates

Source:TheStateofRetailingOnline(Forrester/Shop.org)

Private & Confidential

© 2015 Forrester Research, Inc. Reproduction Prohibited 9

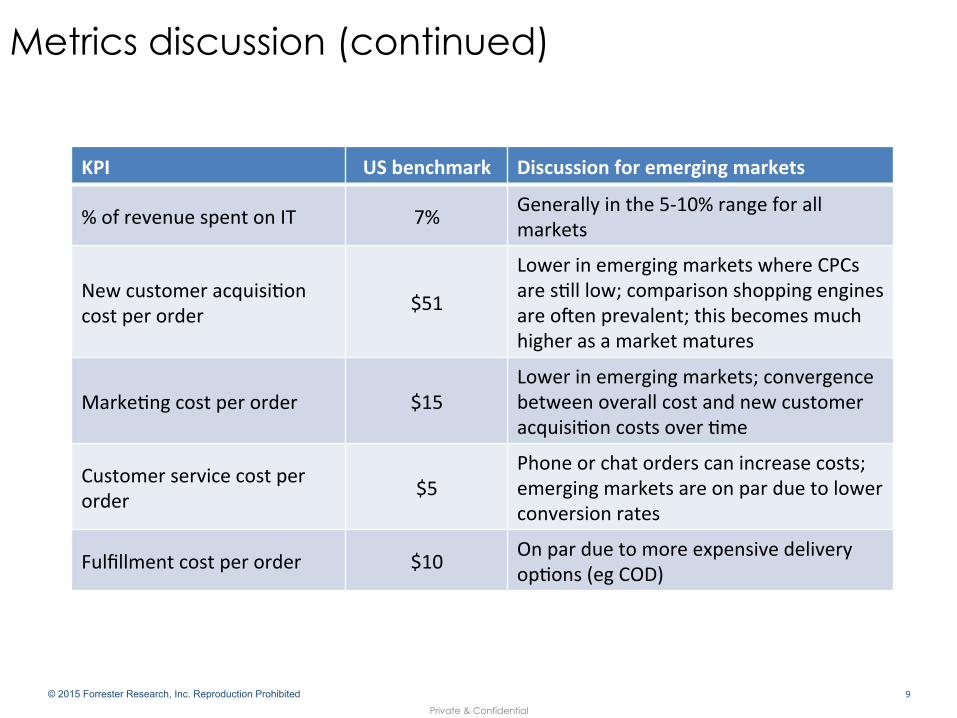

Metrics discussion (continued)

KPI USbenchmark Discussionforemergingmarkets

%ofrevenuespentonIT 7% Generallyinthe5-10%rangeforallmarkets

Newcustomeracquisi=oncostperorder $51

LowerinemergingmarketswhereCPCsares=lllow;comparisonshoppingenginesareocenprevalent;thisbecomesmuchhigherasamarketmatures

Marke=ngcostperorder $15Lowerinemergingmarkets;convergencebetweenoverallcostandnewcustomeracquisi=oncostsover=me

Customerservicecostperorder $5

Phoneorchatorderscanincreasecosts;emergingmarketsareonparduetolowerconversionrates

Fulfillmentcostperorder $10 Onparduetomoreexpensivedeliveryop=ons(egCOD)

Private & Confidential

© 2015 Forrester Research, Inc. Reproduction Prohibited 10

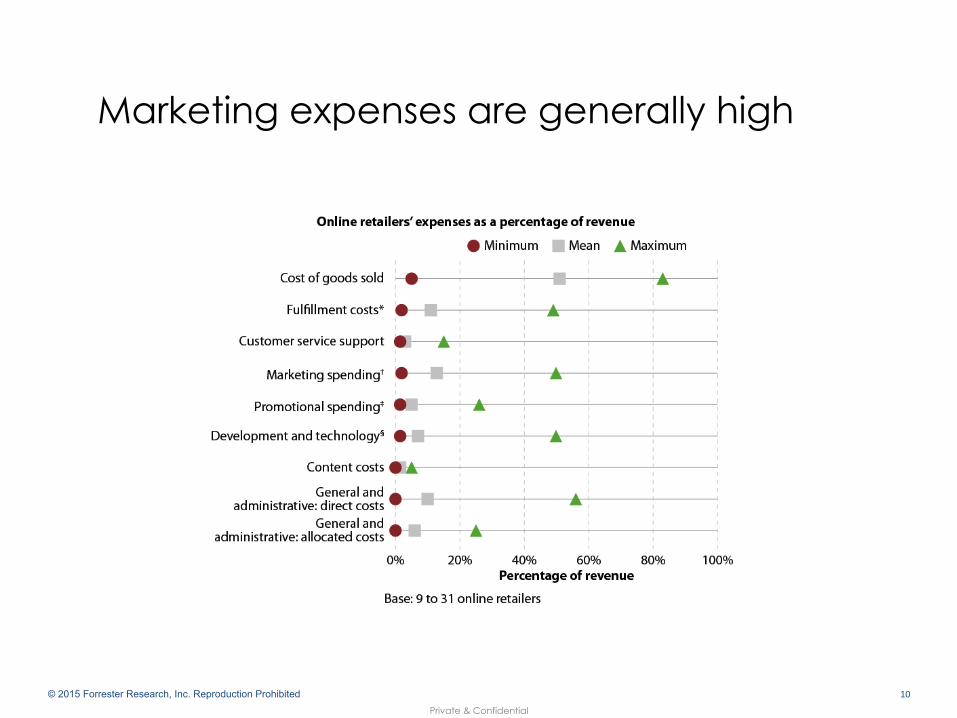

Marketing expenses are generally high

Private & Confidential

© 2015 Forrester Research, Inc. Reproduction Prohibited 11

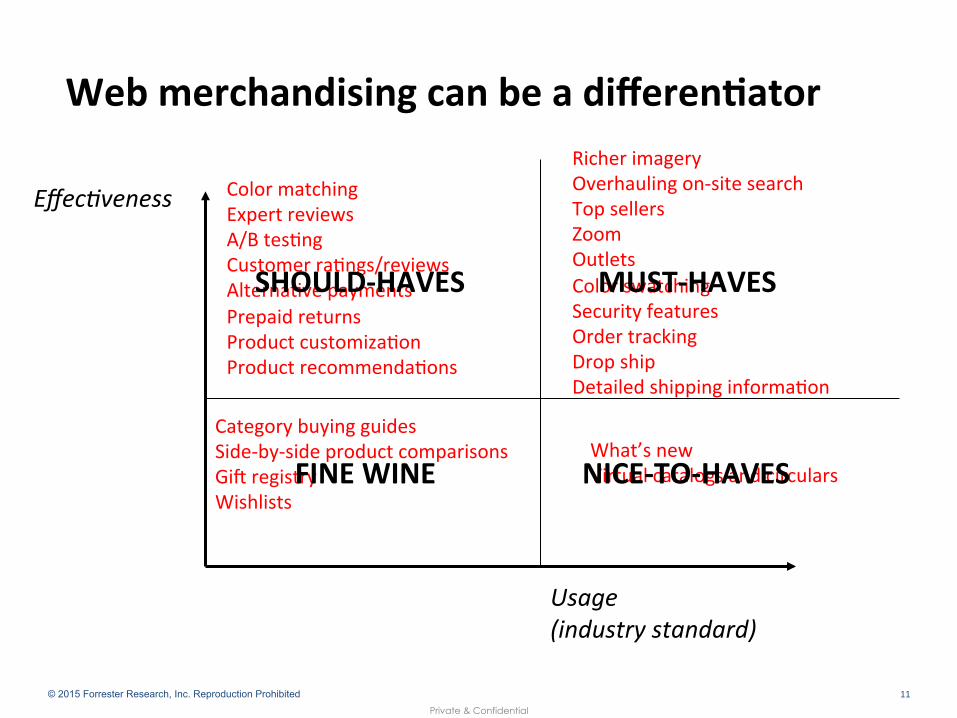

WebmerchandisingcanbeadifferenDator

Usage(industrystandard)

Effec3venessRicherimageryOverhaulingon-sitesearchTopsellersZoomOutletsColorswatchingSecurityfeaturesOrdertrackingDropshipDetailedshippinginforma=on

What’snewVirtualcatalogsandcirculars

CategorybuyingguidesSide-by-sideproductcomparisonsGicregistryWishlists

ColormatchingExpertreviewsA/Btes=ngCustomerra=ngs/reviewsAlterna=vepaymentsPrepaidreturnsProductcustomiza=onProductrecommenda=ons

MUST-HAVESSHOULD-HAVES

NICE-TO-HAVESFINEWINE

Private & Confidential

© 2015 Forrester Research, Inc. Reproduction Prohibited 12

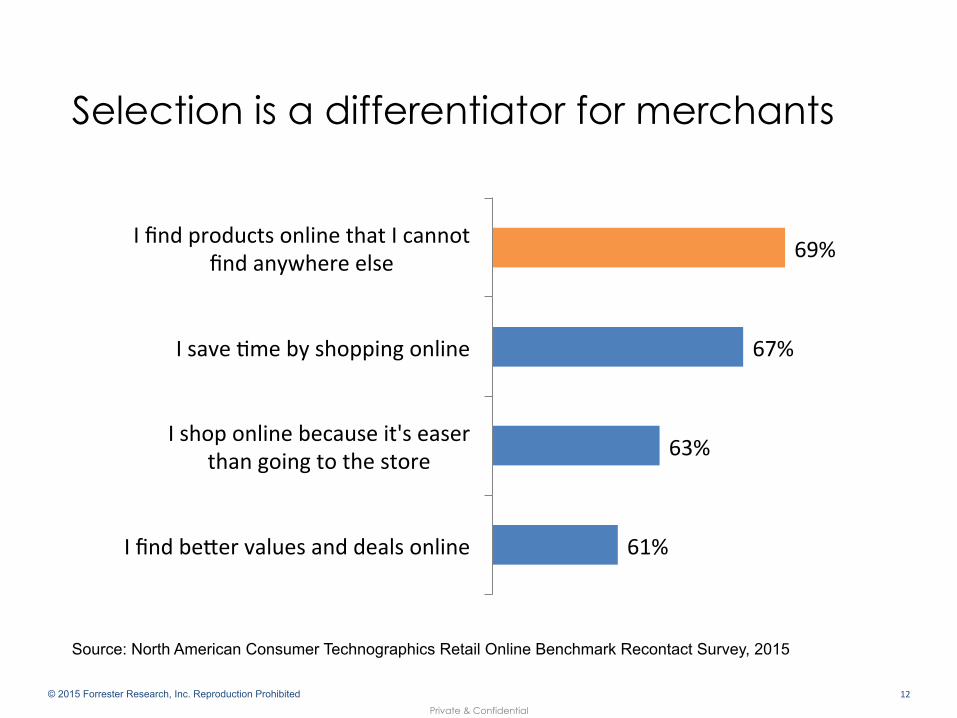

Source: North American Consumer Technographics Retail Online Benchmark Recontact Survey, 2015

Selection is a differentiator for merchants

61%

63%

67%

69%

Ifindbe3ervaluesanddealsonline

Ishoponlinebecauseit'seaserthangoingtothestore

Isave=mebyshoppingonline

IfindproductsonlinethatIcannotfindanywhereelse

Private & Confidential

© 2015 Forrester Research, Inc. Reproduction Prohibited 13

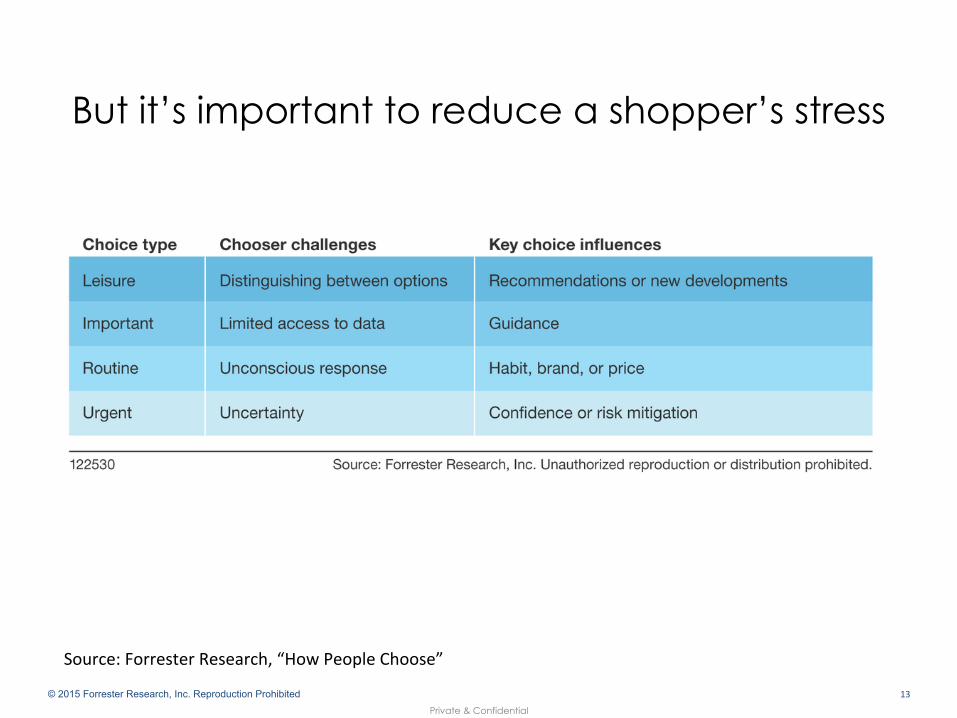

But it’s important to reduce a shopper’s stress

Source:ForresterResearch,“HowPeopleChoose”

Private & Confidential

© 2015 Forrester Research, Inc. Reproduction Prohibited 14

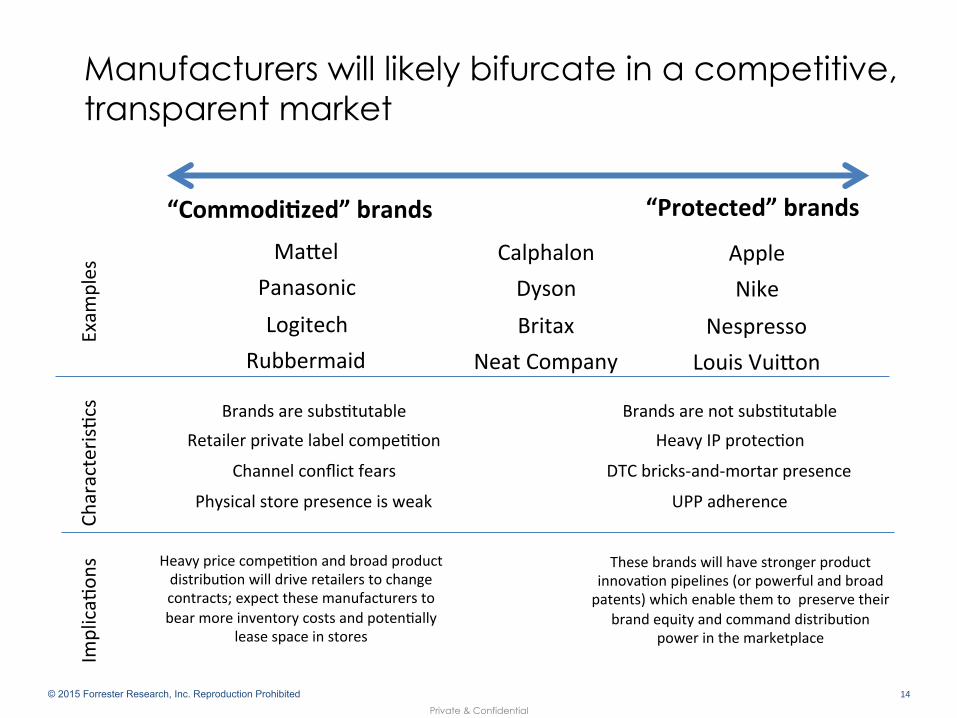

Manufacturers will likely bifurcate in a competitive, transparent market

“CommodiDzed”brands “Protected”brands

Exam

ples

Characteris=cs

Ma3elPanasonicLogitech

Rubbermaid

Brandsaresubs=tutableRetailerprivatelabelcompe==on

Channelconflictfears

Physicalstorepresenceisweak

AppleNike

NespressoLouisVui3on

Brandsarenotsubs=tutableHeavyIPprotec=on

DTCbricks-and-mortarpresence

UPPadherence

Implica=

ons Heavypricecompe==onandbroadproduct

distribu=onwilldriveretailerstochangecontracts;expectthesemanufacturerstobearmoreinventorycostsandpoten=ally

leasespaceinstores

Thesebrandswillhavestrongerproductinnova=onpipelines(orpowerfulandbroadpatents)whichenablethemtopreservetheir

brandequityandcommanddistribu=onpowerinthemarketplace

CalphalonDysonBritax

NeatCompany

Private & Confidential

© 2015 Forrester Research, Inc. Reproduction Prohibited 15

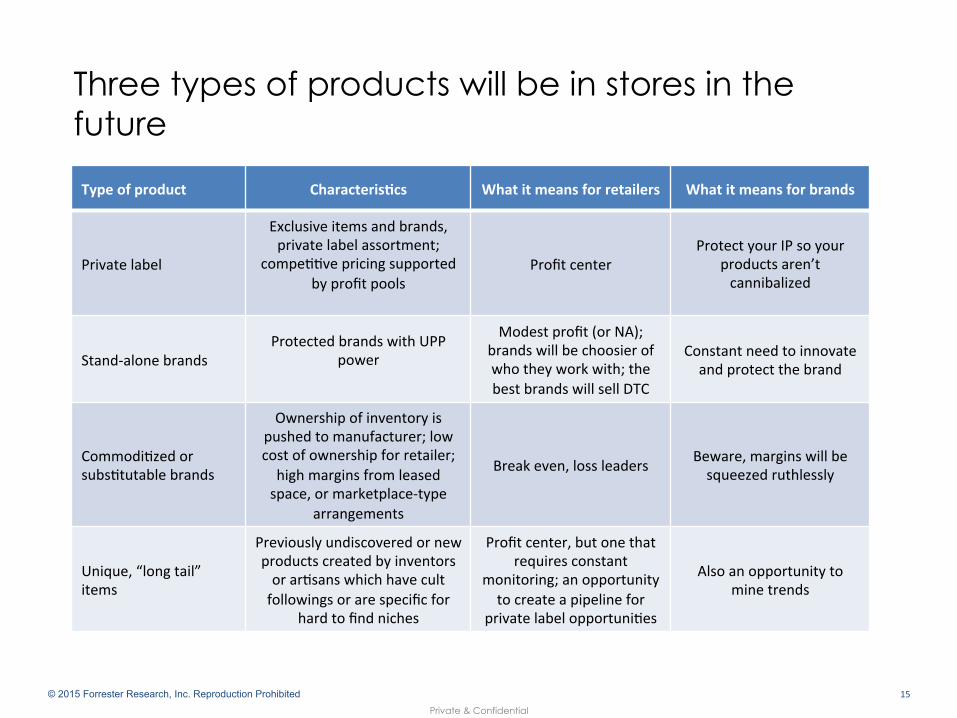

Three types of products will be in stores in the future

Typeofproduct CharacterisDcs Whatitmeansforretailers Whatitmeansforbrands

Privatelabel

Exclusiveitemsandbrands,privatelabelassortment;

compe==vepricingsupportedbyprofitpools

ProfitcenterProtectyourIPsoyour

productsaren’tcannibalized

Stand-alonebrandsProtectedbrandswithUPP

power

Modestprofit(orNA);brandswillbechoosierofwhotheyworkwith;thebestbrandswillsellDTC

Constantneedtoinnovateandprotectthebrand

Commodi=zedorsubs=tutablebrands

Ownershipofinventoryispushedtomanufacturer;lowcostofownershipforretailer;highmarginsfromleasedspace,ormarketplace-type

arrangements

Breakeven,lossleaders Beware,marginswillbesqueezedruthlessly

Unique,“longtail”items

Previouslyundiscoveredornewproductscreatedbyinventorsorar=sanswhichhavecultfollowingsorarespecificfor

hardtofindniches

Profitcenter,butonethatrequiresconstant

monitoring;anopportunitytocreateapipelinefor

privatelabelopportuni=es

Alsoanopportunitytominetrends

Private & Confidential

© 2015 Forrester Research, Inc. Reproduction Prohibited 16

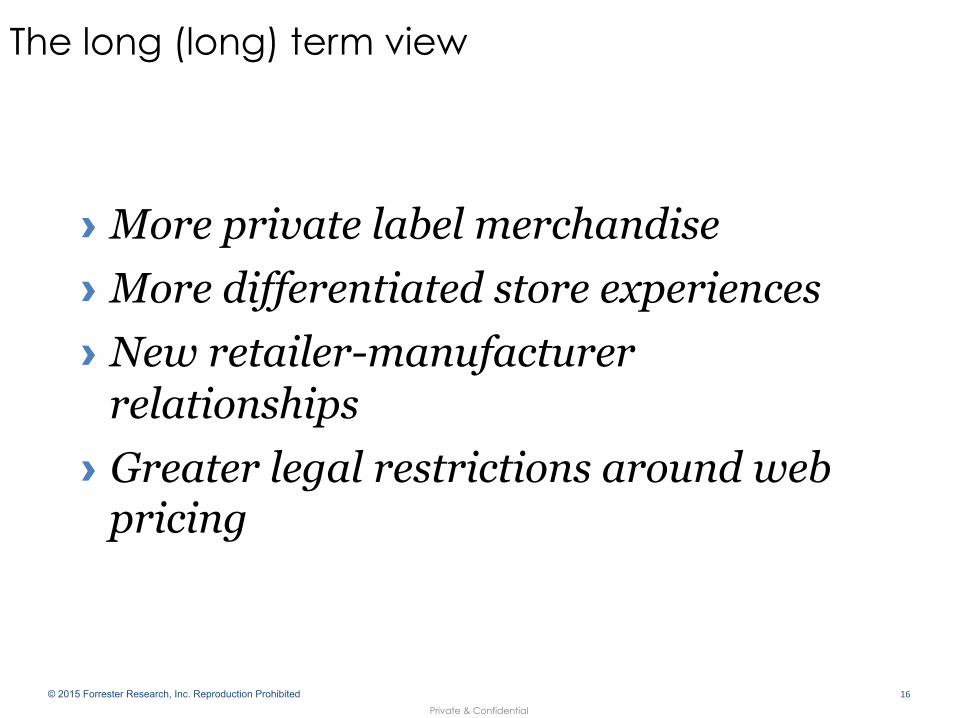

The long (long) term view

› More private label merchandise › More differentiated store experiences › New retailer-manufacturer

relationships › Greater legal restrictions around web

pricing

Private & Confidential 17 Private & Confidential

• More private label merchandise

• More differentiated store experiences

• New retailer-manufacturer relationships

• Greater legal restrictions around web pricing

Product Intelligence

Category Performance

Private & Confidential 18 Private & Confidential

What do these 3 products have in common?

Private & Confidential 19 Private & Confidential

First, let’s talk about “Poo-Pourri”

Private & Confidential 20 Private & Confidential

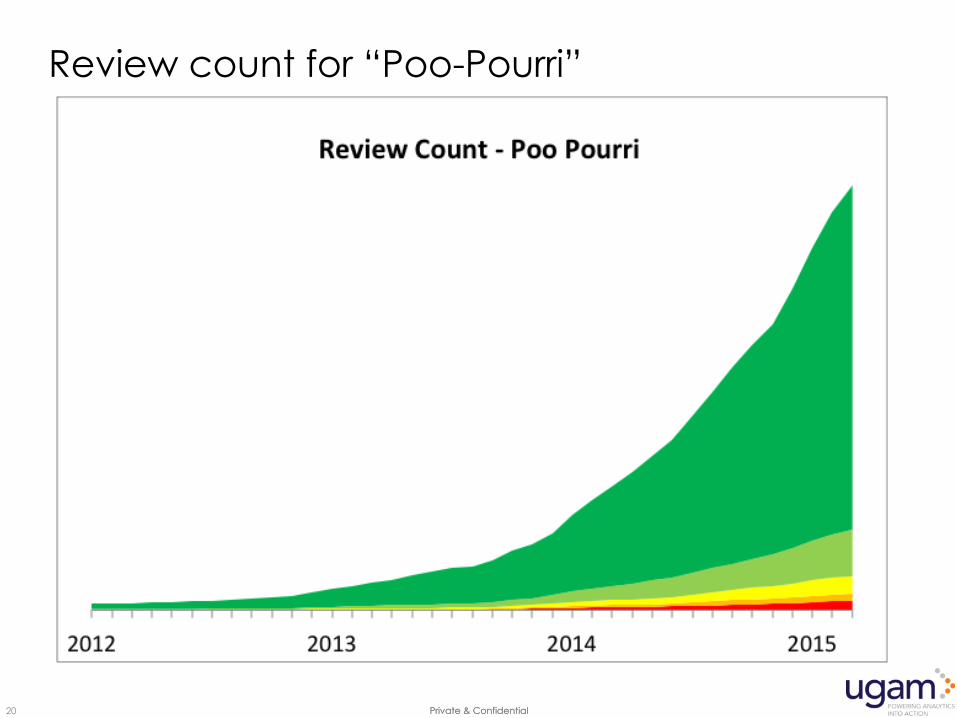

Review count for “Poo-Pourri”

Private & Confidential 21 Private & Confidential

VS.

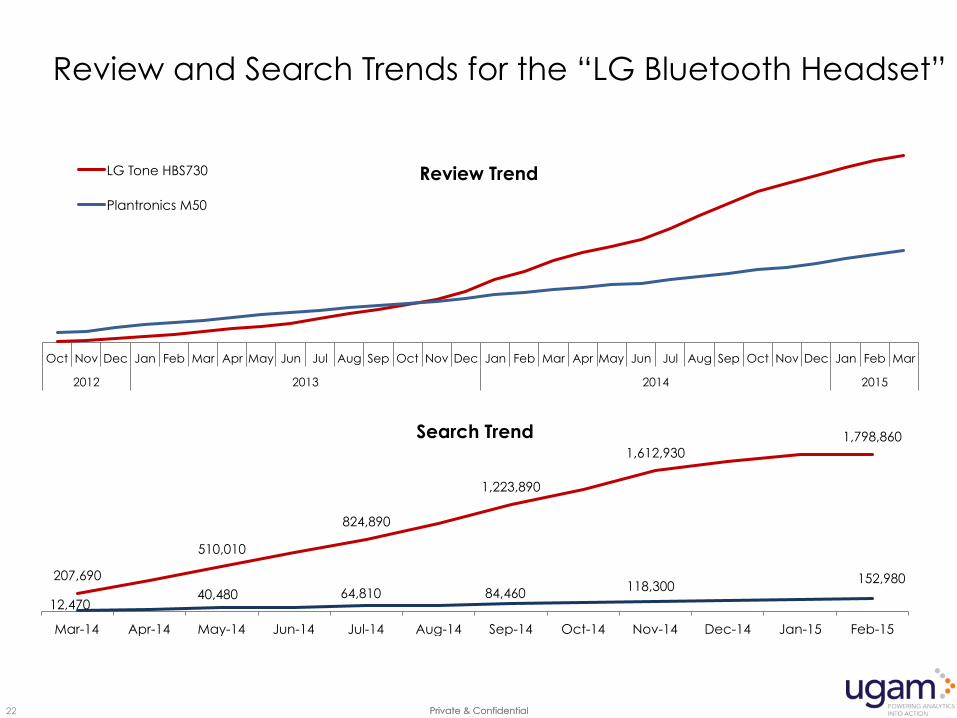

Next, let’s take a look at the “LG Bluetooth Headset”

Private & Confidential 22 Private & Confidential

207,690

510,010

824,890

1,223,890

1,612,930 1,798,860

12,470 40,480 64,810 84,460 118,300 152,980

Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15

Search Trend

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2012 2013 2014 2015

Review Trend LG Tone HBS730

Plantronics M50

Review and Search Trends for the “LG Bluetooth Headset”

Private & Confidential 23 Private & Confidential

I hear voices…..

Private & Confidential 24 Private & Confidential

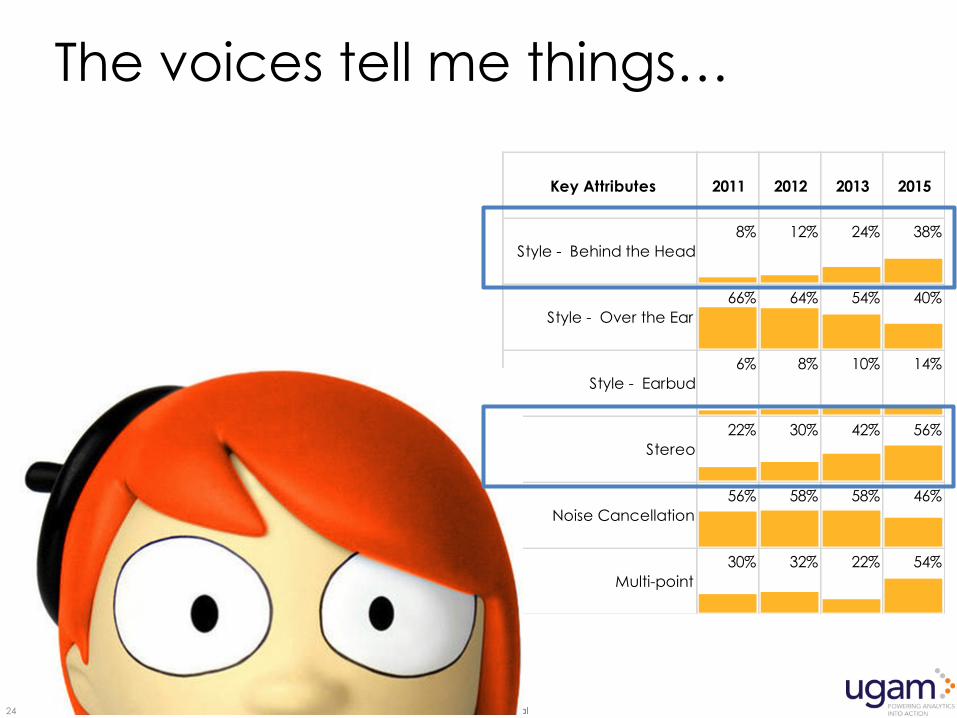

Multi-point

Noise Cancellation

Stereo

Style - Earbud

Style - Over the Ear

Style - Behind the Head

Key Attributes

30%

56%

22%

6%

66%

8%

2011

32%

58%

30%

8%

64%

12%

2012

22%

58%

42%

10%

54%

24%

2013

54%

46%

56%

14%

40%

38%

2015

The voices tell me things…

Private & Confidential 25 Private & Confidential

We all hear voices…

Consumers are freely and constantly telling us what they like, what they don’t like, and what they want. They are also telling us why they want it, and how much they are willing to pay for it.

…not everyone is listening though.

Private & Confidential 26 Private & Confidential

• It is about hearing voices.

• It is about translating these voices a.k.a. digital footprints that consumers leave behind to understand the characteristics of a product in relation to a consumer need

What is Product Intelligence?

Private & Confidential 27 Private & Confidential

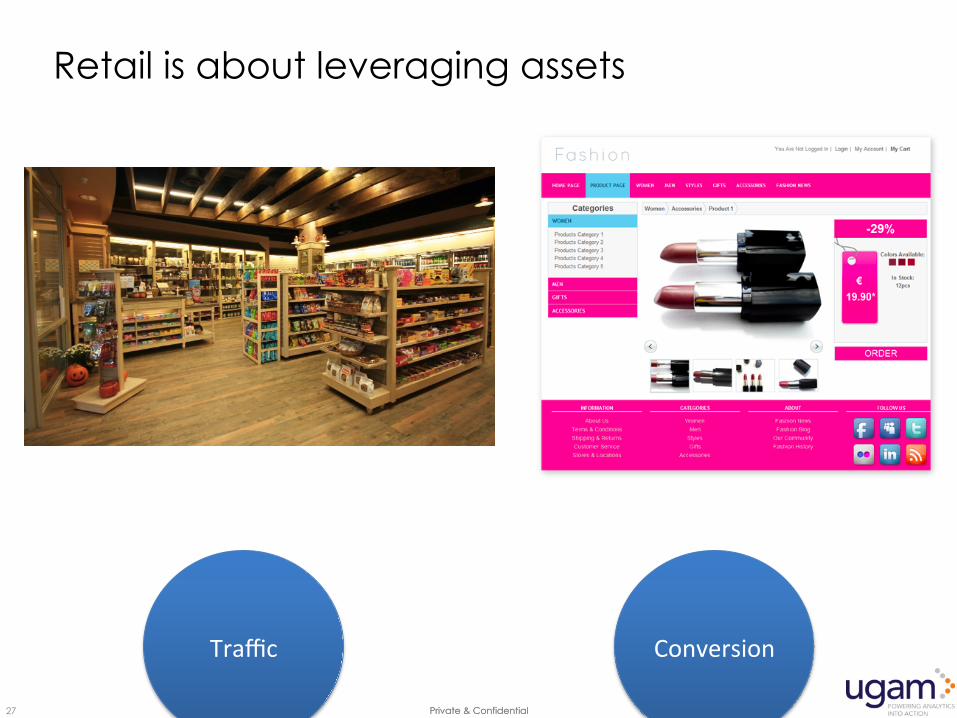

Traffic Conversion

Retail is about leveraging assets

Private & Confidential 28 Private & Confidential

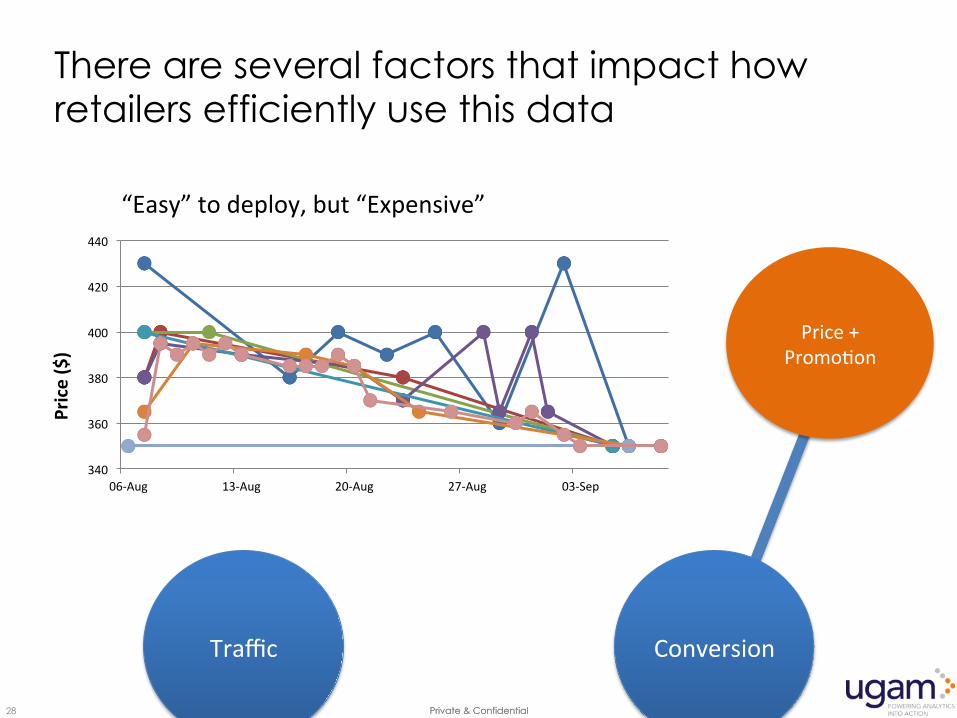

Traffic Conversion

Price+Promo=on

340

360

380

400

420

440

06-Aug 13-Aug 20-Aug 27-Aug 03-Sep

Price($)

“Easy”todeploy,but“Expensive”

There are several factors that impact how retailers efficiently use this data

Private & Confidential 29 Private & Confidential

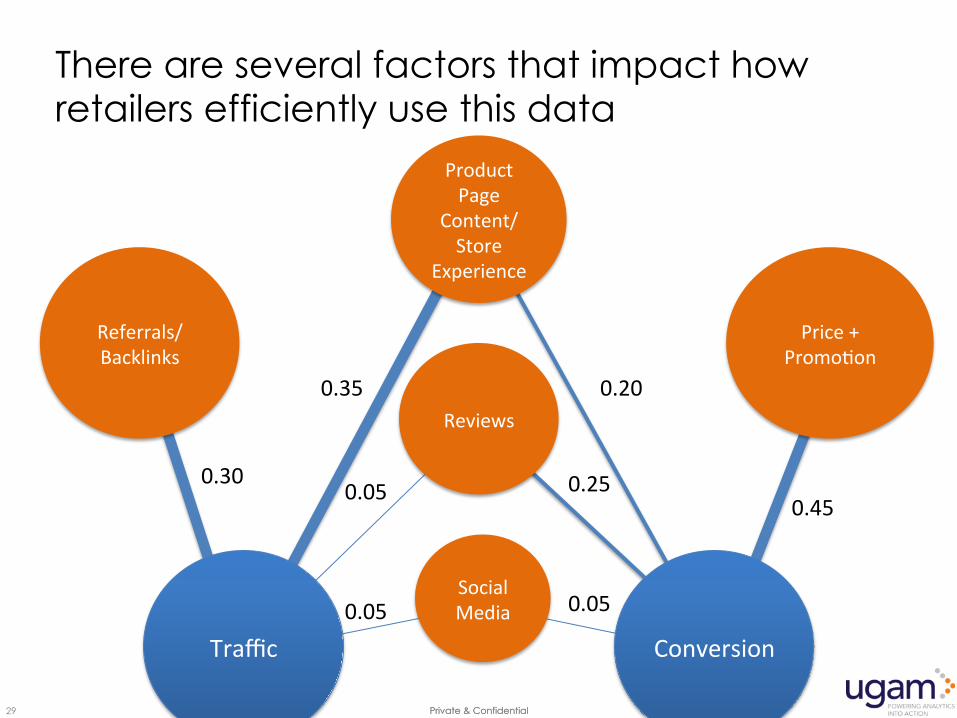

Referrals/Backlinks

ProductPage

Content/Store

Experience

Reviews

SocialMedia

Price+Promo=on

Traffic Conversion

0.30

0.35

0.05

0.05

0.20

0.450.25

0.05

There are several factors that impact how retailers efficiently use this data

Private & Confidential 30 Private & Confidential

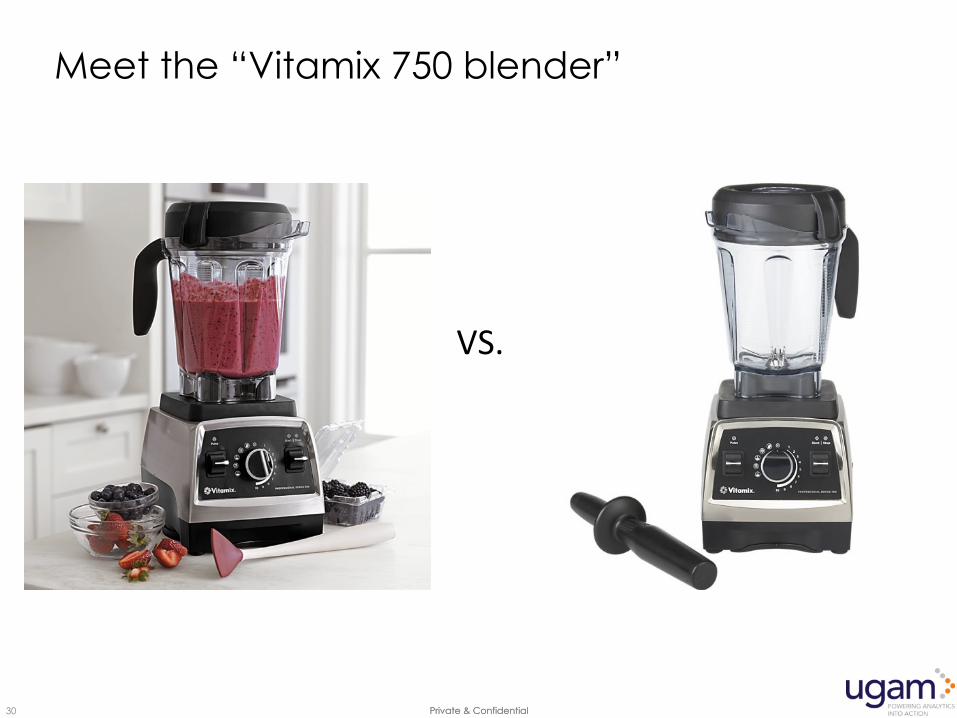

VS.

Meet the “Vitamix 750 blender”

Private & Confidential 31 Private & Confidential

Meet the “Vitamix 750 blender”

VS.

Private & Confidential 32 Private & Confidential

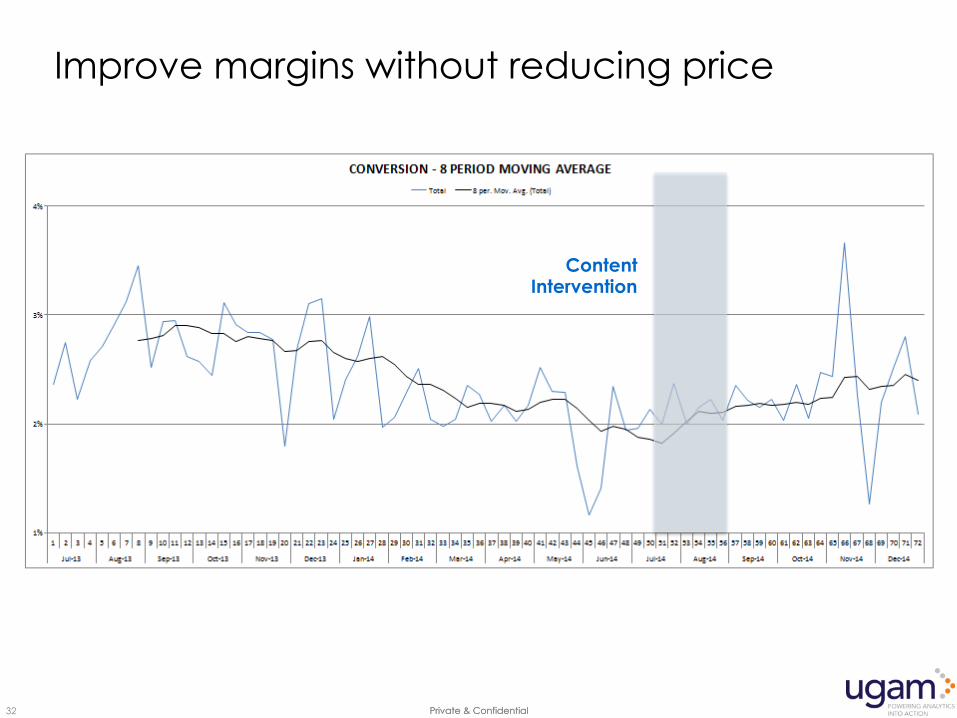

Content Intervention

Improve margins without reducing price

Private & Confidential 33 Private & Confidential

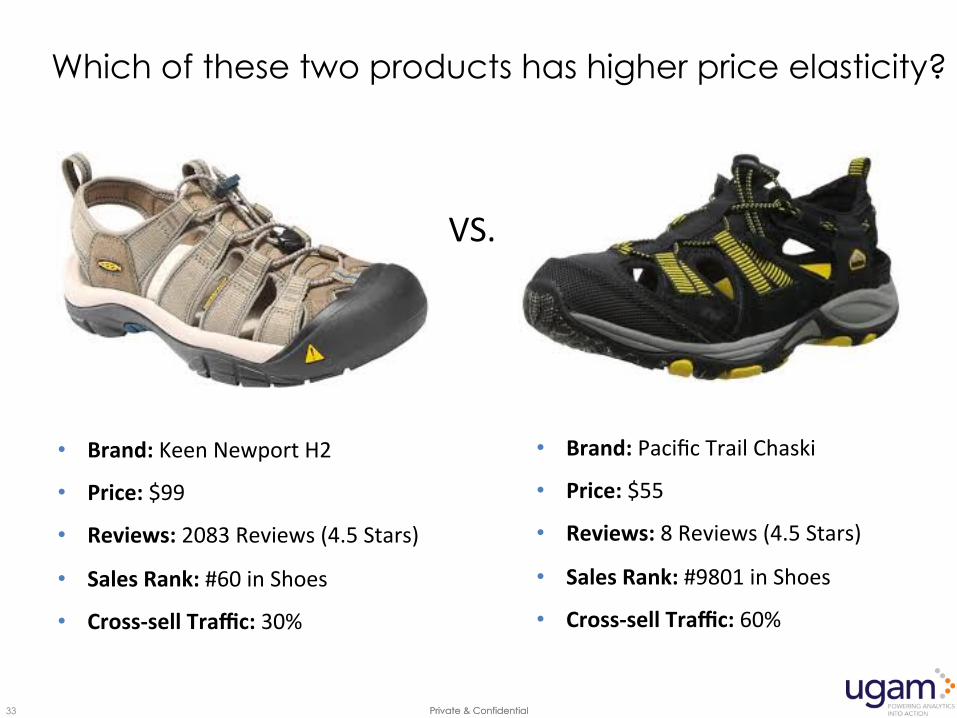

• Brand:PacificTrailChaski

• Price:$55

• Reviews:8Reviews(4.5Stars)

• SalesRank:#9801inShoes

• Cross-sellTraffic:60%

• Brand:KeenNewportH2

• Price:$99

• Reviews:2083Reviews(4.5Stars)

• SalesRank:#60inShoes

• Cross-sellTraffic:30%

VS.

Which of these two products has higher price elasticity?

Private & Confidential 34 Private & Confidential

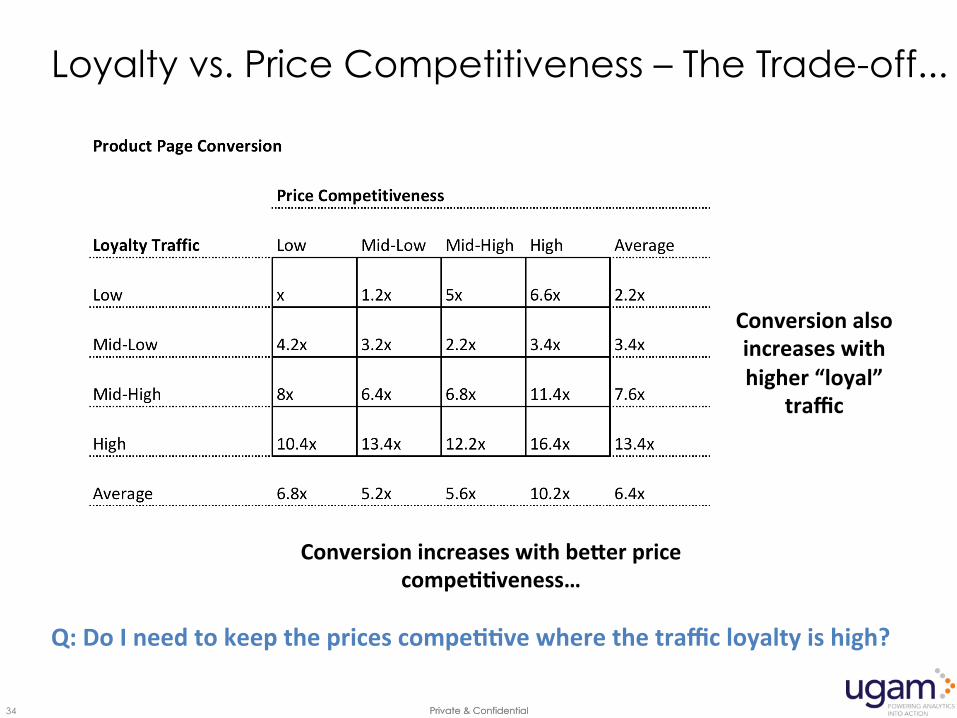

Conversionincreaseswithbe_erpricecompeDDveness…

Conversionalsoincreaseswithhigher“loyal”

traffic

Q:DoIneedtokeepthepricescompeDDvewherethetrafficloyaltyishigh?

Loyalty vs. Price Competitiveness – The Trade-off...

Private & Confidential 35 Private & Confidential

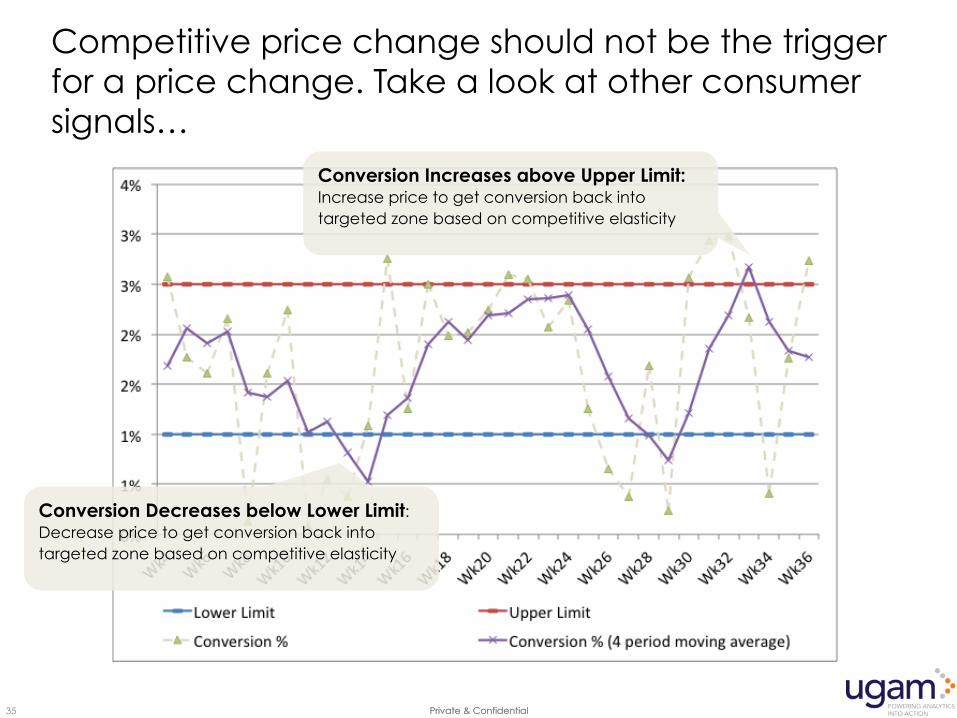

Conversion Increases above Upper Limit: Increase price to get conversion back into targeted zone based on competitive elasticity

Conversion Decreases below Lower Limit: Decrease price to get conversion back into targeted zone based on competitive elasticity

Competitive price change should not be the trigger for a price change. Take a look at other consumer signals…

Private & Confidential 36 Private & Confidential

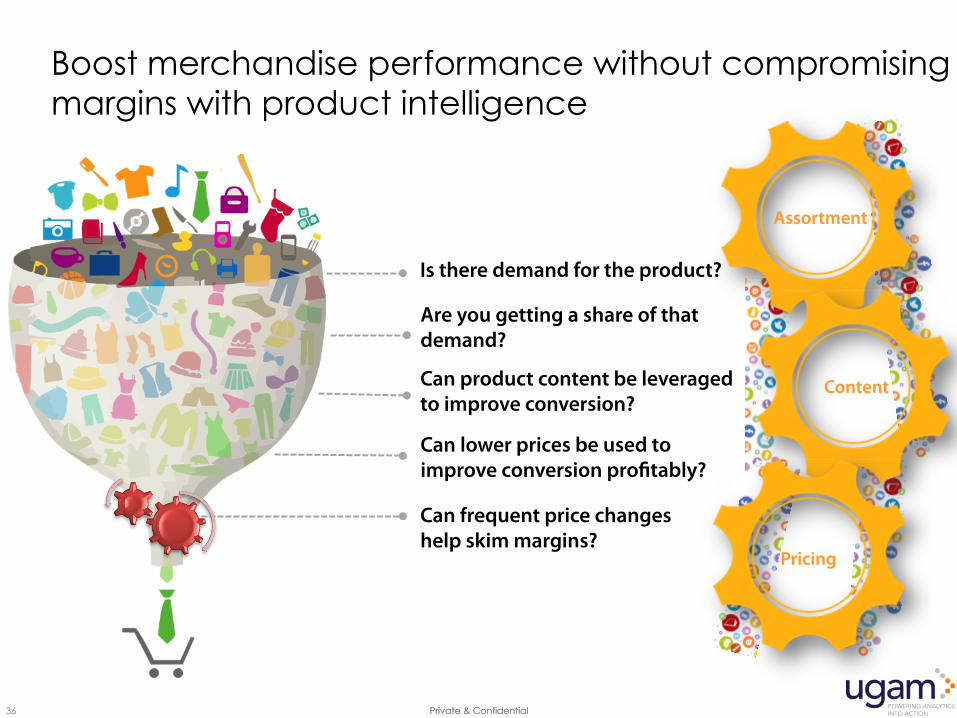

Are you getting a share of that demand?

Can product content be leveraged to improve conversion?

Can lower prices be used to improve conversion profitably?

Can frequent price changes help skim margins?

Is there demand for the product?

Assortment

Content

Pricing

Boost merchandise performance without compromising margins with product intelligence

Private & Confidential 37 Private & Confidential

0

10

20

30

40

50

60

70

80

90

100

020406080100

Pred

ictedProd

uctR

ank

ActualProductRank

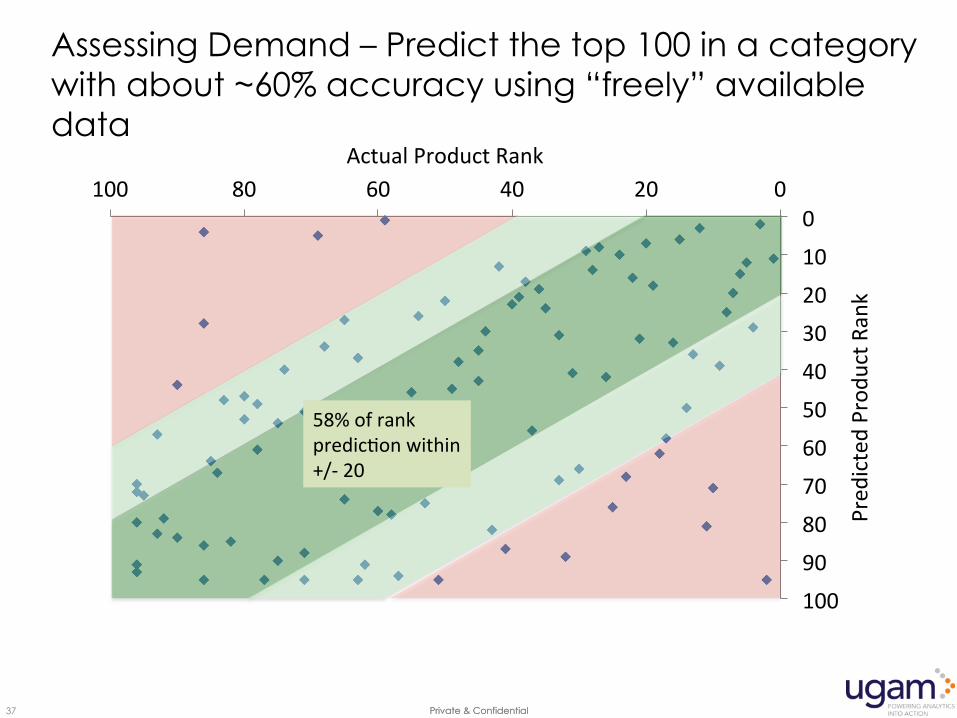

58%ofrankpredic=onwithin+/-20

Assessing Demand – Predict the top 100 in a category with about ~60% accuracy using “freely” available data

Private & Confidential 38 Private & Confidential

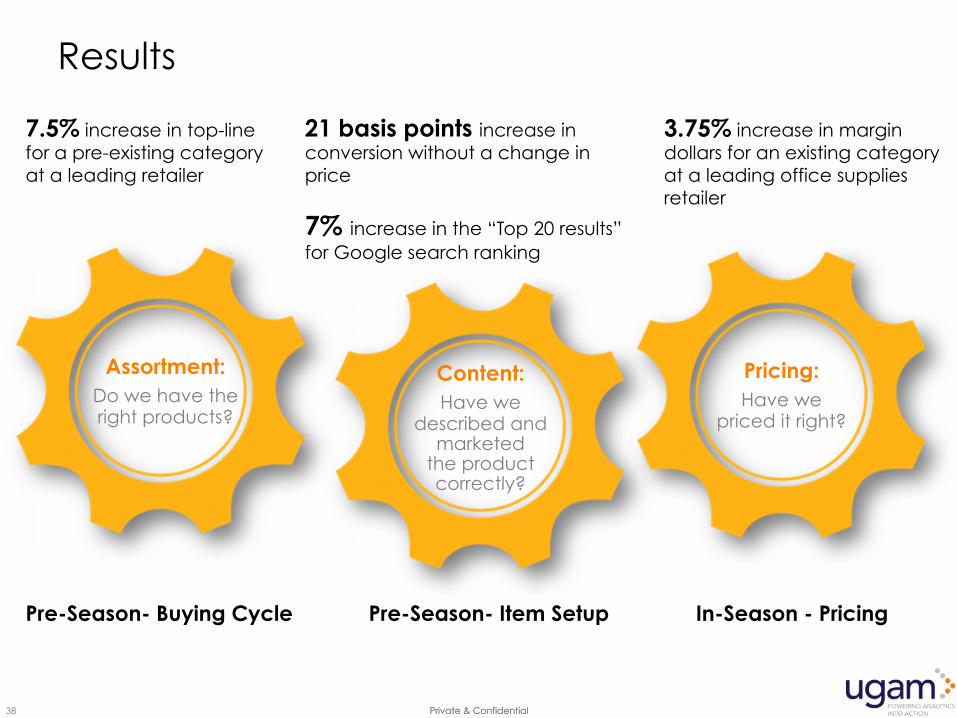

Assortment: Do we have the right products?

Content: Have we

described and marketed

the product correctly?

Pricing: Have we

priced it right?

Pre-Season- Buying Cycle Pre-Season- Item Setup In-Season - Pricing

7.5% increase in top-line for a pre-existing category at a leading retailer

21 basis points increase in conversion without a change in price

7% increase in the “Top 20 results” for Google search ranking

3.75% increase in margin dollars for an existing category at a leading office supplies retailer

Results

#RSPS15

Q&A//Panelists

SudhirHollaSeniorVicePresident,[email protected]@sudhirholla

SucharitaMulpuruVP,PrincipalAnalystservingeBusinessandChannelStrategyProfessionalsForrestersmulpuru@forrester.com@smulpuru

MODERATOR:DebbieHaussEditor-in-Chief,RetailTouchPoints

#RSPS15

PLEASEJOINUSFOROURNEXTSESSION:Tomorrowat12PMET/9AMPT

Thanksfora3endingthiswebinar!

h_p://www3.retailtouchpoints.com/rsp15/