Embed Size (px)

Citation preview

Understanding the recent changes to electronic payments

Tuesday 27 July, 11:00am (AEST)Guest Speaker – Dean LongAFTA’s National Manager – Strategy and PolicyEmail: [email protected] or twitter @Dean_Long13

House Keeping;

• Session will be recorded

• Presentation will be available at www.afta.com.au

• Audience will be on mute

• Q & A can be submitted throughout the presentation but will be answered

at the end of the presentation

Introduction

Key terms

Why have changes been made?

Merchant Service Fees

Surcharging

When will I be effected?

What’s next?

Questions?

About DeanAfter starting my travel and tourism journey on Fairstar the fun ship in 1988, tourism and travel became a passion and a profession.

I joined AFTA in May 2014 and lead AFTA’s renewed public policy advocacy program following the removal of travel specific legislation in late 2014. Over this period I have been largely working on the major issue of electronic payments in travel. This includes agents access to merchant facilities and the Government’s review of credit card regulations.

Previously I was the Senior Adviser in the NSW Government on tourism and hospitality policy following working for Tourism NSW. I am is also a member of Western Sydney University’s External Advisory Committee for Bachelor of Tourism Management.

So what is an electronic payment?

Electronic payment

=

89%

Cash

=

11%

41% = direct deposit / debit

38% = MasterCard / Visa

10% = Amex

Acquirer

Card schemes

Interchange fees

Merchant service fees

Forward Delivery Risk

Acquirer – Provide you with your merchant facilities

Card schemes – Provide the systems to facilitate payments

Provide the network to process the payments between the acquirer and the customers bank

Card type refers to either credit or debit / prepaid

Interchange fees – Charged to a travel agent by your acquirer

Paid by you to your customers card issuer

Fees are set by MasterCard and Visa.

Charged to the Merchant typically as part of your merchant rates

Interchange fees in practice

Source: Chargebacks911.com

Merchant Service Fees (MSF) – Charges to a merchant to accept electronic payments

Charged as a percentage of your transaction value

Interchange fees

Card scheme fees – international cards

Account fees – terminal access

Forward Delivery Risk (FDR) – typical retail environment

General chargeback risk to Australian retailers; max 30 days

Australian consumer purchases consumer goods using a credit card

Australian consumer receives and consumes goods. Primary risk to

merchant is fraudulent cards

FDR - For Australian travel agencies

Chargeback risk to Australian travel agents; 70 – 100 days and a minimum of $5.4 billion AUD

Australian consumer purchases travel using a

credit or debit card

Travel agent fulfils obligations and pays suppliers (within an average of 14 days) eg: airline, sightseeing tour and resort. The

travel agent, not the supplier, is at risk of a chargeback if the supplier goes insolvent or otherwise fails to perform.

Why has it changed

Financial System Inquiry recommended changes to the electronic payment system in Australia.

5000 of the 6500 submissions complained about surcharging.

The RBA had developed the new standards following 18 months of consultation.

Changes to Interchange fees - credit

NEWCredit card interchange

Now capped at 0.8%Average every 3 months must be 0.5%

OLDDifferent size merchants had different

ratesAverage every 3 years must be 0.5%

Merchant Service Fee - it will change

Interchange rates will be capped and assessed more regularly.

The cost to you as a merchant should reduce by 1 June 2017.

Customers who use cards for reward points will most likely see a reduction in the number of points they can earn.

What has changed for Surcharging?

You can still apply a surcharge.

You must only surcharge the actual cost.

- It must be demonstrable and not include any internal costs.

You are not allowed to blend to create an average surcharge.

5 permissible costs that can be included in your surcharge

Merchant fees

Terminal rental and servicing

Gateway services

Annual Statement

Fraud prevention services

The cost of insurance for Forward Delivery Risk (no

fault third party charge back)

External provider

Annual Statement – MSF from your acquirer

Terminal rental

Gateway feesMerchant FeesInternational

fees

Companion Amex

Visa credit and debit

MasterCard credit and

debit

Fraud Prevention

Some online businesses have substantial risk of

fraud.

Engage independent companies to minimise

this risk

The cost of insurance for (FDR) - no fault third party chargeback

Consumer pays using a credit card and the travel agent completes four different transactions to suppliers

Australian consumer invokes a chargeback because the

sightseeing tour did not deliver on the contracted service due

to insolvency

Agent becomes a creditor to the insolvent sightseeing tour, even though they have fulfilled their service to the

customer.

How do you work out the new surcharge?

You will need all of the information we have just spoken about:

• Annual Statement

• Receipts from your service providers for electronic fraud prevention and FDR insurance.

Annual Statement – Acquirer (financial institution)

Card Scheme Card Type Number of transactions MSF as a percentage

MasterCard Credit 369 1.1

MasterCard Debit 200 0.1

Visa Credit 342 1.2

Visa Debit 200 0.1

Amex Companion Credit 90 1.6

Total credit n/a 801 n/a

Total debit n/a 400 n/a

Annual Statement - Amex

Card Type Number of transactions MSF as a percentage

Green 45 2.1

Black 20 3.2

Total 65 n/a

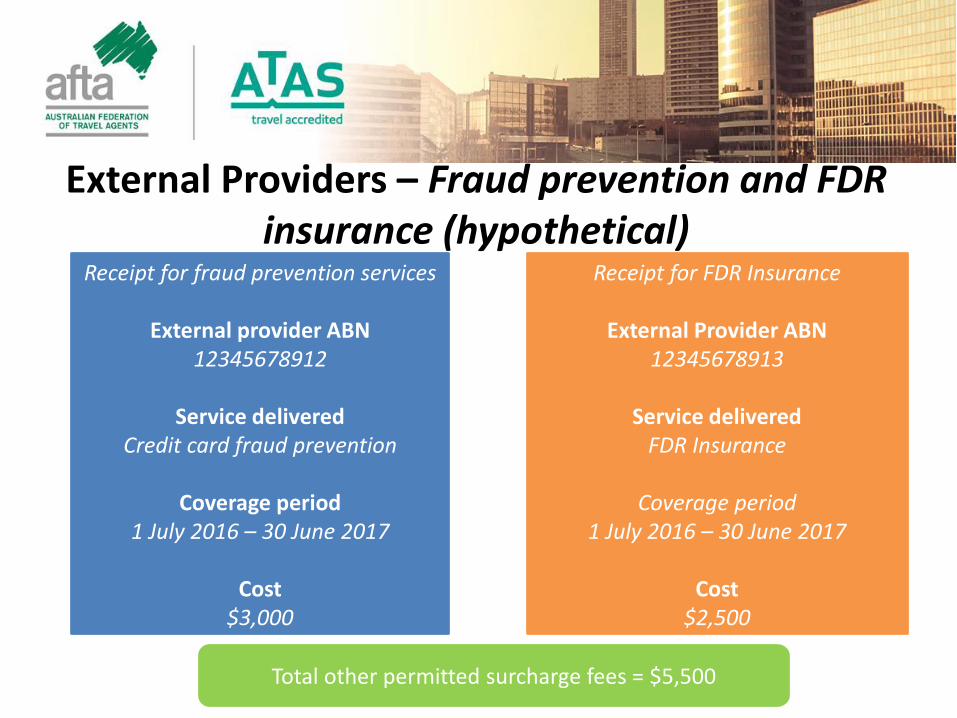

External Providers – Fraud prevention and FDR insurance (hypothetical)

Receipt for fraud prevention services

External provider ABN12345678912

Service deliveredCredit card fraud prevention

Coverage period1 July 2016 – 30 June 2017

Cost$3,000

Receipt for FDR Insurance

External Provider ABN12345678913

Service deliveredFDR Insurance

Coverage period1 July 2016 – 30 June 2017

Cost$2,500

Total other permitted surcharge fees = $5,500

Attributing fraud prevention and FDR Costs

Total value of all card schemestransactions

Total Fraudpermitted

costs

Additional costs as a

percentage

Total FDRpermitted

costs

100

Total value of all card scheme transactions

100

Additional costs as a

percentage

Attributing fraud prevention and FDR Costs

$1,000,000$3,000 0.3%

$2,500

100

$1,000,000 100 0.25%

Your permitted surcharge rate

MSFFraud

prevention

FDR insurance

Surcharge rate

1.1 0.3 0.25 1.65%

MasterCard Credit Example

Simple Formula

Applying your surcharge rates

Debit surcharge

Credit surcharge

Debit surcharge

Credit surcharge

Companion credit

surcharge

Amex Credit

surcharge

Always express your surcharge rate as a percentage.

Penalties

ASX listed company – $108,000 per contravention

Non listed company – $10,800 per contravention

Other business type - $720 per contravention

1 September 2016

1 June 2017 1 July 20181 July 20171 September

2017

Large business must comply with the new regulations

Acquirer will provide an Annual Statement

Allowable items to be calculated and surcharge rates set.

New interchange rates will come into affect

All businesses must comply with new regulations on permitted surcharge

Ensure rate of surcharge complies with the new standards.

Yearly review of your surcharge rate

When will these changes be implemented?

Your business will be classified as a small businessif it meets two or more of the following criteria

• Your businesses’ revenue for the financial year is less than $25 million.

– Revenue is defined as any money that your business derived for the provision of its services i.e commissions and service fees.

• Your businesses’ gross assets at the end of the financial year is less than $12.5 million.

• Your businesses’ has fewer than 50 employees at the end of the financial year.

Where can I find further information?

AFTA electronic payment support material

RBA website Q&A

ACCC website Q&A

Your bank and acquirer

Questions