Embed Size (px)

Citation preview

The Future of Payments Insights from Discussions Building on an Ini4al Perspec4ve by: MasterCard on How Payments are Helping to Shape the Future of Commerce

Context The ini4al perspec4ve on the Future of Payments kicked off the Future Agenda 2.0 global discussions taking place through 2015.

This summary builds on the ini4al view and is updated as we progress.

Ini4al Perspec4ves Q4 2014

Global Discussions Q1/2 2015

Insight Synthesis Q3 2015

Sharing Output Q4 2015

Big Data Opportuni9es Most of the opportuni4es big data can offer have yet to be fully exploited. The reality is that there are different chunks of data that are collected, stored and managed in mul4ple ways.

Bricks and Clicks Is omnichannel just a buzz word? How important is the consistent

shopping experience across channels? What is the future of physical stores? Can bricks keep pace with clicks or is it in fact the other way around?

The End of Cash? All the evidence suggests that the use of cash is in decline across the

globe. Cash takes 4me to get at, is riskier to carry, and by most es4mates, cash costs society as much as 1.5% of GDP.

Enabling Financial Inclusion With many organisa4ons now making financial inclusion a priority, it is

likely we will see a significant por4on of the 2.5bn unbanked adults armed with electronic payments products in the future.

Personalised Shopping In ten years you can expect to walk past a shop and your mobile will receive meaningful and personal no4fica4ons on discounts or deals

in store that you are likely to buy based on your shopping preferences.

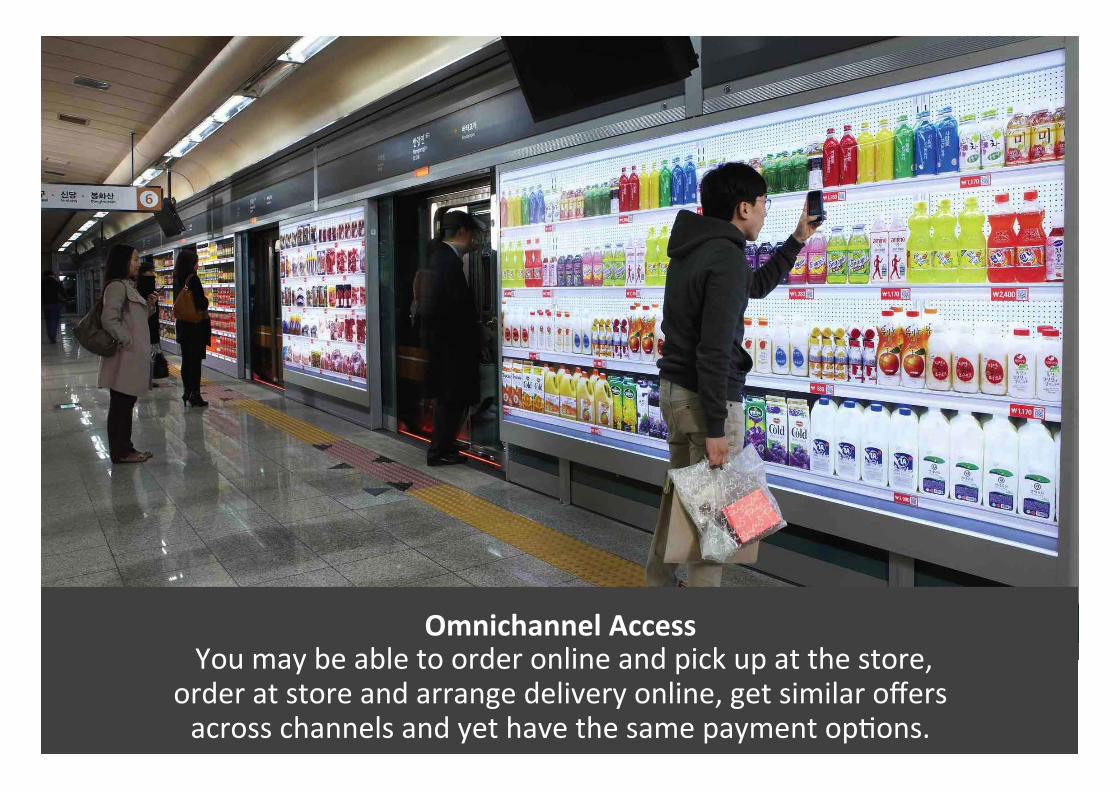

Omnichannel Access You may be able to order online and pick up at the store, order at store and arrange delivery online, get similar offers across channels and yet have the same payment op4ons.

Customers will be able to purchase and receive their items in a variety of ways, across both digital and physical environments.

Growth of Mobile Point of Sale In the next ten years there will be a global acceptance of electronic

payment products. We are nearly there with Square and iZe\le. Such is their success it is expected that by 2019 46% of POS terminals will be mPOS.

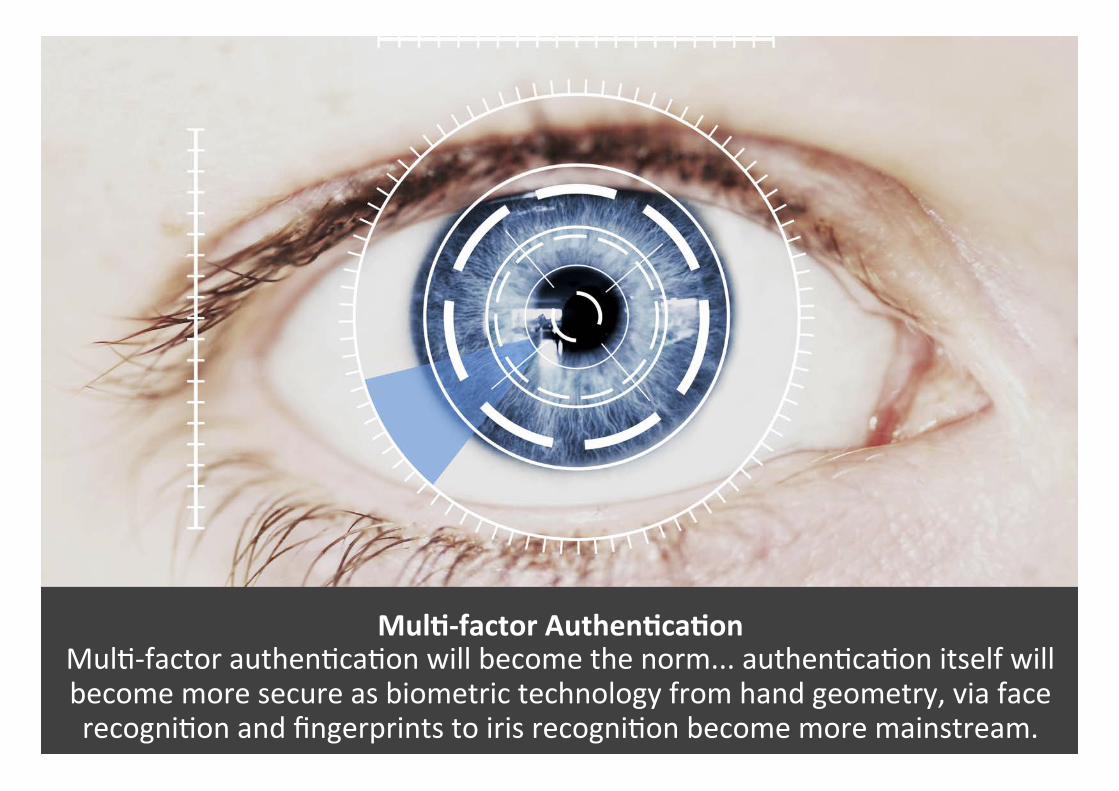

Mul9-‐factor Authen9ca9on Mul4-‐factor authen4ca4on will become the norm... authen4ca4on itself will become more secure as biometric technology from hand geometry, via face recogni4on and fingerprints to iris recogni4on become more mainstream.

There will be a range of appropriate ways of authen4ca4ng payments, generally changing from passive and complex (passwords) to ac4ve and simple (biometrics)

Cross-‐Border Commerce Cross-‐border commerce is growing faster than domes4c commerce and so will become increasingly important and influen4al. Cross-‐border flow of goods,

services and finance could increase threefold to $85 trillion by 2025.

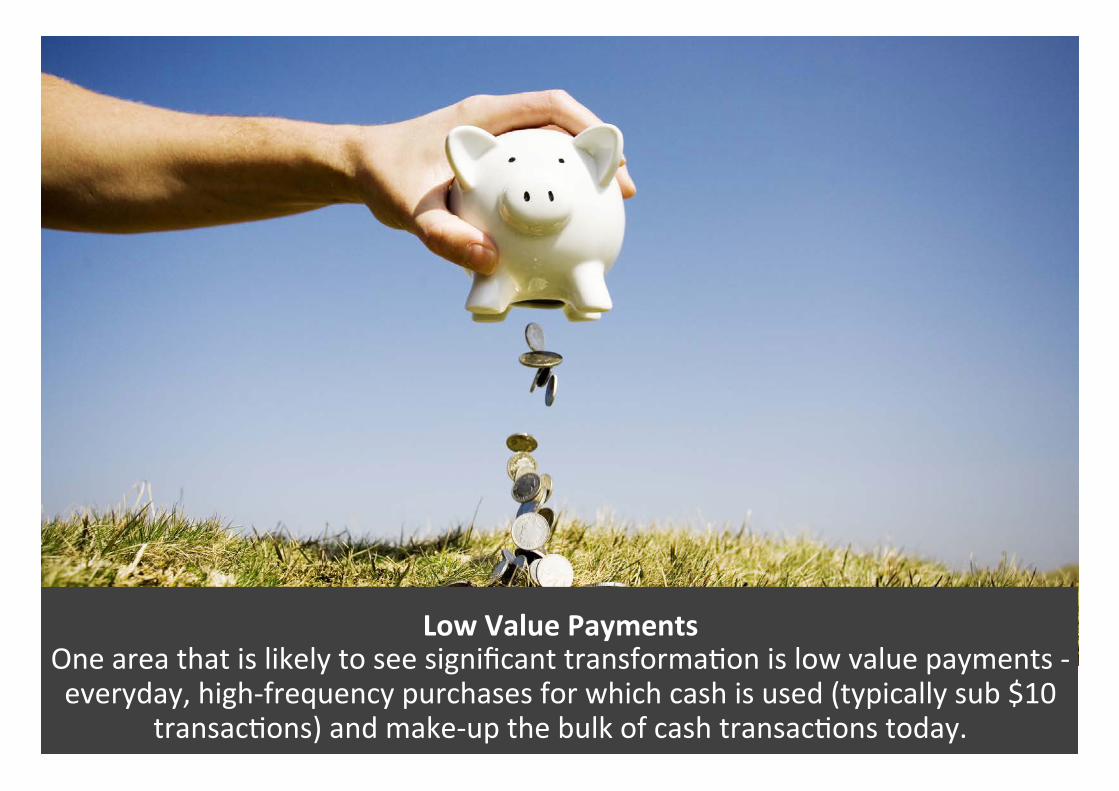

Low Value Payments One area that is likely to see significant transforma4on is low value payments -‐ everyday, high-‐frequency purchases for which cash is used (typically sub $10

transac4ons) and make-‐up the bulk of cash transac4ons today.

Sub $10 transac4ons will become increasingly fric4onless, 4ed into pay-‐as-‐you-‐go business models i.e. on-‐demand content.

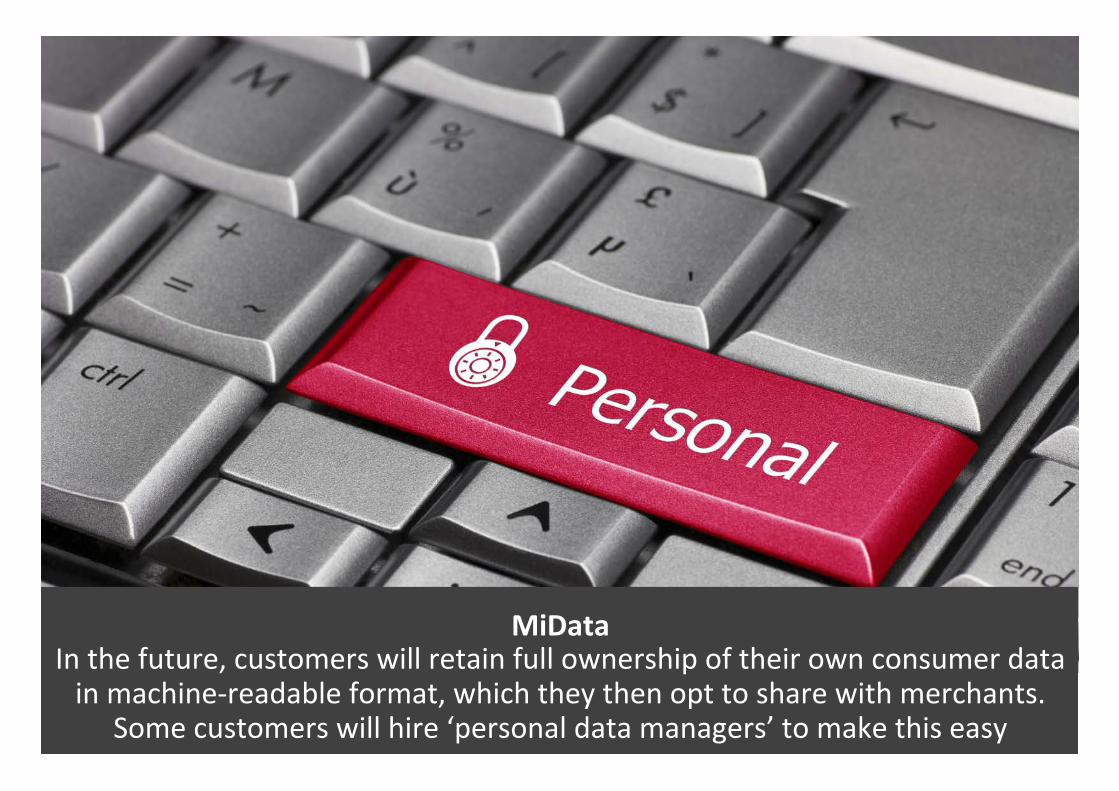

MiData In the future, customers will retain full ownership of their own consumer data in machine-‐readable format, which they then opt to share with merchants.

Some customers will hire ‘personal data managers’ to make this easy

Unbundling of Payments Value Chain Greater compe44on, new innova4ons and changing regula4ons will mean that the current value chain will spread out, removing steps and

so reducing costs for both consumers and suppliers.

Changing Customer Expecta9ons Customers will expect different things from their payments experience: instead of just ‘security’, there will also be a need for greater individual control, flexibility, choice, efficiency, convenience and “good fric4on”.

Prolifera9on of Currencies People will increasingly use mul4ple forms of currency in different contexts: alongside na4onal legal tender, we will see more local and crypto-‐currencies – many decoupled from exis4ng systems.

Regula9on of Services A new regula4on model will emerge in the payments world. Whereas

to date regulators have focused on “defini4ons of en44es” their role will shik to being more about “regula4on of services” and wider alignment.

Transac9onal vs. Emo9onal Seamless payments will distance consumers from understanding

monetary value. Brands will have to reconsider the way they connect to customers providing more holis4c and emo4onal value.

Seamless Ubiquitous Payments The ability to ‘transact anywhere’ with integrated, sophis4cated

authen4ca4on such as biometrics increases: More contactless technology and a convergence of standards, enable global informa4on exchanges.

Integrated Global Governance Regula4on to support global, regional and local transac4ons will increase.

A set of global integrated standards and governance for payments will emerge to which key regulators and merchants all sign up to.

Evolu9on of Security The need for physical security reduces with demise of the use of cash. In its place, more secure digital solu4on plamorms pervade with a consolida4on of iden4ty and payments into an ecosystem that includes crypto-‐currencies.

Reduced Human Control We see a world where most connected devices can be used

for payments, more people will be financially included and there are more automated payment choices and channels.

Device is King, Consumer is Queen Whether on devices or in the cloud, our digital repositories will know who we are, where we are and what we redeem. Businesses need to understand these new intermediaries and how they define our rela4onships with their brands.

Tension with Regula9on Some regional regulatory interven4ons protect consumers whilst others prevent innova4on by limi4ng use of new technologies. A power struggle

between brands and government emerges around wider data sharing and use.

The Composite Consumer Flexible digital iden44es allow consumers to connect with each other even as they connect with brands. Loyal rela4onships will be made not just with individual customers but also with families, couples, and groups of friends.

A Systema9c View Policy makers from around the world will have to look at the problems

of wealth crea4on and wealth inequality in a more systemic way, with the use, for example, of a complexity framework.

Data Darwinism Data is a new form of power: Corporate consolida4on places data in the hands of a few who are able to dictate terms above others. Governments correspondingly have less power as they have less access to key data.

Seamless Data Representa9on Improvements in the way in which data is visualized and presented leads to rising consump4on and wider use. In turn, we see greater efficiencies and benefits for individuals, companies, governments and society as a whole.

Trust and Integrity of the System As more individual control and simplicity is sought, how will the privacy

con4nuum evolve, will tokenisa4on diminish security concerns and do we know what trust will mean in the future?

Free Banking from Non-‐tradi9onal Players Innova4ve business models -‐ underpinned by changing technology, consumer demand and Governments pushing for cheaper or free banking -‐ open the doors to new entrants from outside the sector that break old monopolies.

Compe9tor Collabora9on Wider collabora4ons change the payments landscape with credit card companies partnering with merchants, MNOs, and new entrants. These partnerships share infrastructure, increasing consumer u4lity and choice.

Digital Regulatory Regions With learnings from successes in East Africa, autonomous/sovereign regulatory authori4es come together to create con4guous digital regulatory regions that span geographic borders and boundaries and lead to payments convergence.

Mobile Currency Convergence Ambi4ons for convergence of payment types is accelerated by the crea4on

of seamless mobile consumer experiences that unite mul4ple cash-‐less stores of value including a range of tradi4onal and alterna4ve currencies.

Financial Inclusion Driven by Payments Companies Improvements in financial educa4on for the mass are driven by the payments

industry, not governments. Predica4ve algorithms protect consumers by reducing their ability to over-‐extend themselves with cheap credit.

Future Agenda 84 Brook Street London W1K 5EH +44 203 0088 141 futureagenda.org

The world’s leading open foresight program

What do you think? Join In | Add your views into the mix

www.futureagenda.org