Embed Size (px)

Citation preview

1

Marie SANCHIS

Fashion Marketing and retailing Year 3

The 28th of March

Retail management With Finance

VS

Financial Analysis

Catriona Foxworthy-Bowers

2

Table of Content

Introduction

I. Thomas Sabo’s Financial Statement 2009/2010

II. Thomas Sabo’s Ratios

III. Thomas Sabo’s Financial Analysis

IV. Comparison Competitor

A) Pandora‟ s Financial statement 2011/2012

B) Pandora‟s Ratios

C) Comparison Competitor Analysis

Conclusion

3

Introduction After the intervention of Catriona Foxworthy-Bowers during two weeks for

the retail management with finance course. We are able to make a financial

analysis of different companies refer to their accounts. In the first part we

will present the financial analysis of Thomas Sabo „the concept of customize

your own jewelry”, one of the most important charms jewels seller in the

world. This is a German concept where the customer has to choose a simple

bracelet or necklace and add his prefer “charms” to the base.

For the comparison to a competitor in the second part we chose Pandora

who have approximately the same concept but in different form, a form of

pearl that you add to the base.

This analysis will be based on the study of ratios of these two companies.

This financial analysis will be useful to compare currant‟s year‟s

performances with the previous years in a company. Also that could help to

find how to improve the company competence in the future.

In a second way the comparison could be interesting to compare

performance of the business with other organization in the same activities

with Thomas Sabo biggest competitor.

4

I. Thomas Sabo’s Financial Statement

5

6

II. Thomas Sabo’s Ratios :

Gross profit percentage

Mark-up ratio

Net Profit Percentage

Current Ratio

Acid Test Ratio

Return on Capital employed

Inventory Turnover

2010 2009

Gross Profit

= 40.3%

= 33.8%

Mark up Ratio

= 67.5%

= 51%

Net Profit Percentage

= 17.4%

= 11.7%

Current Ratio

= 1.95

=1.76

Return on capital

employed

= 79%

= 66%

7

III. Thomas Sabo’s Financial Analysis:

After the reading of the financial statements and the calculating of the ratios,

we are able to make an analysis of the financial position on Thomas Sabo.

However this analysis will be based on the accountants of 2010 and 2009,

then there are not the most recently but the analysis still useful.

First of all the Gross profit is 40.3% of the sales in 2010 and 33.8% in 2009.

The gross Profit ratio represents the gross profit as a proportion of sales.

Higher is this percentage better it is for businesses.

This is a good increase (6.5%) who indicates that the sales grow up or the

cost fall. An increase in the percentage may also indicate a cheaper supplier

found or that Thomas Sabo is improved efficiency in the production process.

Then the Mark up ratio to measure percentage age added to cost of goods

sold to calculate selling price.

The mark up ratio put up between 2009 and 2010, from 51% to 67.5%, it

means that they made a better percentage of profit based on the cost of

goods sold. They marge on the product are better and they win more money

with this increase of 16.5%. Perhaps this increase could be justify like for

the gross profit ratio as an either cut of costs of production or an increase of

the selling price to customers.

The net profit of the company also increase of 5.7%. The net profit measure

profitability after consideration of all expenses (taxes, interest, …) In this

case, Thomas Sabo's‟ net profit is 17.4% in 2010 that is good because this

ratios increase and they win money after had sold their product. This is may

be because of a decrease of expenses compare to the last year.

The current ratio will be expected at 2:1, this ratio is uses to test the

company‟s liquidity and also its working capital position. In other words this

ratio measures the ability of a company to pay its current obligations using

8

current assets. Here the Thomas Sabo‟s ratio is 1.76 in 2009 and 1.96 in

2010 we see an increase of the ratio this is very good because Thomas Sabo

became closer to the ideal ratio. This means that the company has more

current assets than current liabilities. The company has more the ability of

generate cash from its receivables and by selling inventory than in 2009.

The last ratio is the return on capital employed; this is one of the most

important ratios if you want to know if you can invest in a company. It

measures the return on the money the investors have put into the company.

Again for this ratio Thomas Sabo getting better in 2010 with 79% compare to

66% in 2009. An increase of 13% who says how much profit we earn from

the investments the shareholders have made in their company.

To conclude this analysis, Thomas Sabo gets better in 2010 than in 2009,

they have to continue in this way, take care of the production cost, the sell

prices, the marge they take, how long they wait to pay their suppliers and to

have their money back.

9

IV. Comparison Competitor:

A) Pandora’s Financial statements.

10

11

12

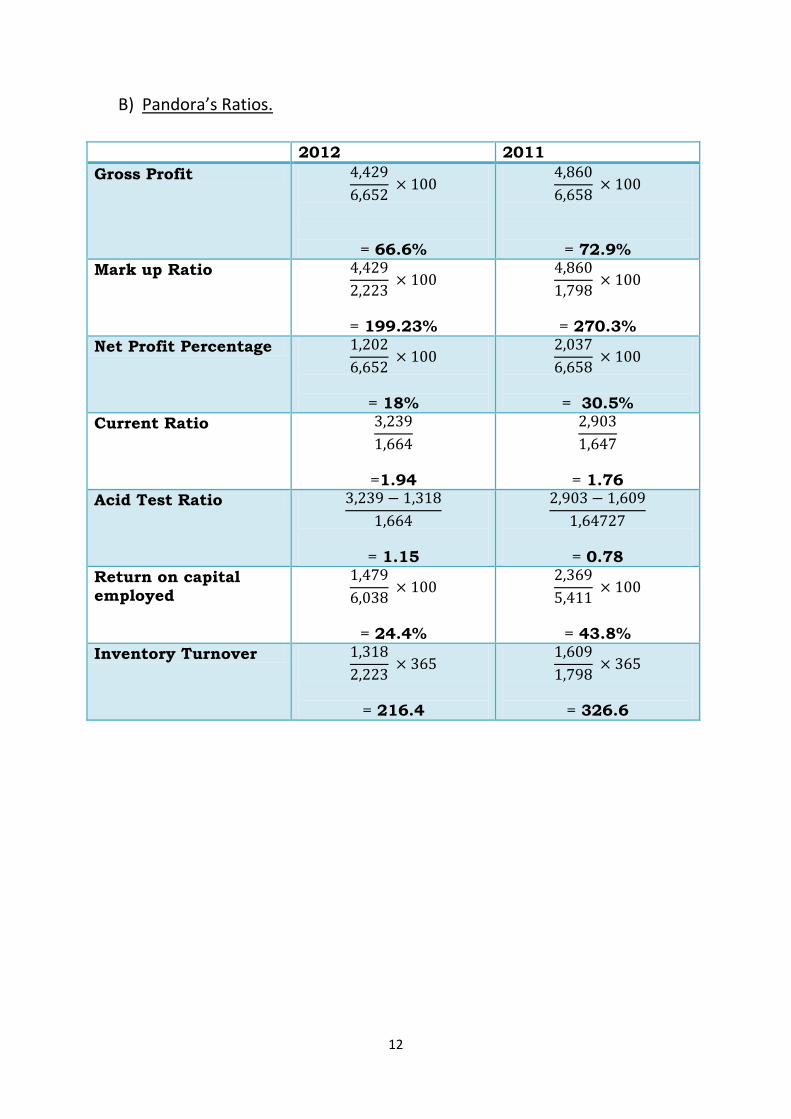

B) Pandora’s Ratios.

2012 2011

Gross Profit

= 66.6%

= 72.9%

Mark up Ratio

= 199.23%

= 270.3%

Net Profit Percentage

= 18%

= 30.5%

Current Ratio

=1.94

= 1.76

Acid Test Ratio

= 1.15

= 0.78

Return on capital employed

= 24.4%

= 43.8%

Inventory Turnover

= 216.4

= 326.6

13

C) Comparison Competitor analysis. After have made the Thomas Sabo accountants‟ analysis we are going to

compare Thomas Sabo to one of its most important competitor “Pandora”.

This company sells the same type of product, jewelers.

However we are going to compare the company but without the same year of

account 2009-2010 for Thomas Sabo and 2011-2012 for Pandora, we will

then don‟t forget the economy situation of the world these last few years and

say that perhaps Thomas Sabo and Pandora are not in prefect equality.

Nevertheless the comparison is still interesting to learn more about the

company‟s financial situations.

The first ratio considered is the Gross profit percentage, for Thomas Sabo

this percentage increase with the time but for Pandora it‟s a decrease of

13%. By the way Pandora has the best percentage with 66.6% in 2012 and

only 40.3% for Thomas Sabo in 2010. Pandora has a better management of

the production‟s cost or the best sell prices.

After the ratio noticed is the Mark up ratio with again a decrease in Pandora

and an increase in Thomas Sabo. That could say that there is a problem in

the selling price, Thomas Sabo has a better management of the prices than

Pandora.

The third ratio is the percentage of net profit. Pandora has always the same

problem with a big decrease and Thomas Sabo an increase however for this

ratio Pandora make more profit than Thomas Sabo. This shows how much

of each sales pound shows up as net income after all expenses are paid. In

the comparison here this means that Thomas Sabo has to take care of

manage their expenses. And Pandora is higher than Thomas Sabo in this

sector.

Then the current ratio, proof of company‟s liquidity, they both have

approximately the same with a general growth. They are both close to the

14

ideal ratio 2:1 because they have 1.95 and 1.94 for the most recent year.

This means that both have working capital it‟s really good but it could be a

disadvantage because they are very illiquid and would not be able to operate

under the conditions described. Its bills are coming due faster than its

generation of cash. They also can pay there bill in current assets.

To finish with the last ratio, the return on capital employed for Pandora fell

in 2012 with a decrease of 20% (43.8% in 2011 and 24.4% in 2012).

This ratio is now a little bit low (24.4%) the investment are not appropriate or

badly appropriate. For this sector Thomas Sabo is better with 79% in 2010

either an increase of 13%. With the condition of Pandora is doesn‟t give

confidence to the investors.

To conclude this analysis, Pandora has got the biggest decrease on the

margin ratios compare to Thomas Sabo, but they have better returns ratios

that perhaps mean that they want to take care of pay their bill or pay in

quickly to the detriment of their profit. In another hand, the data for

Pandora are more recent and with the economic crisis the Thomas Sabo ratio

don‟t fit well with the nowadays situation.

Conclusion

In conclusion we can see the importance of calculate the ratios based on the

company accounts and not only read the accounts. A financial analysis

would be really useful to reorganize a company, find different ways of

production or organization. Modify the company after analysis would be

optimizing the capacity of the company.