Embed Size (px)

Citation preview

Barclays Global Consumer Staples Conference

September 6-8, 2016 Boston 1

Forward-Looking Statements

This presentation includes forward-looking statements including, but not limited to, statements regarding Coca-Colaİçecek’s (“CCI”) plans, objectives, expectations and intentions and other statements that are not historical facts.Forward-looking statements can generally be identified by the use of words such as “may,” “will,” “expect,” “intend,”“estimate,” “anticipate,” “plan,” “target,” “believe” or other words of similar meaning. These forward-looking statementsreflect the current views and assumptions of management and are inherently subject to significant business, economicand other risks and uncertainties. Although management believes the expectations reflected in the forward-lookingstatements are reasonable, at this time, you should not place undue reliance on such forward-looking statements.Important factors that could cause actual results to differ materially from CCI’s expectations include, without limitation:changes in CCI’s relationship with The Coca-Cola Company and its exercise of its rights under our bottler's agreements;CCI’s ability to maintain and improve its competitive position in its markets; CCI’s ability to obtain raw materials andpackaging materials at reasonable prices; changes in CCI’s relationship with its significant shareholders; the level ofdemand for its products in its markets; fluctuations in the value of the Turkish Lira or the level of inflation in Turkey;other changes in the political or economic environment in Turkey or CCI’s other markets; adverse weather conditionsduring the summer months; changes in the level of tourism in Turkey; CCI’s ability to successfully implement itsstrategy; and other factors. Should any of these risks and uncertainties materialize, or should any of management’sunderlying assumptions prove to be incorrect, CCI’s actual results from operations or financial conditions could differmaterially from those described herein as anticipated, believed, estimated or expected. Forward-looking statementsspeak only as of this date and CCI has no obligation to update those statements to reflect changes that may occur afterthat date.

2

3

Agenda

A regional powerhouse...

...winning in the marketplace...

...to create shareholder value

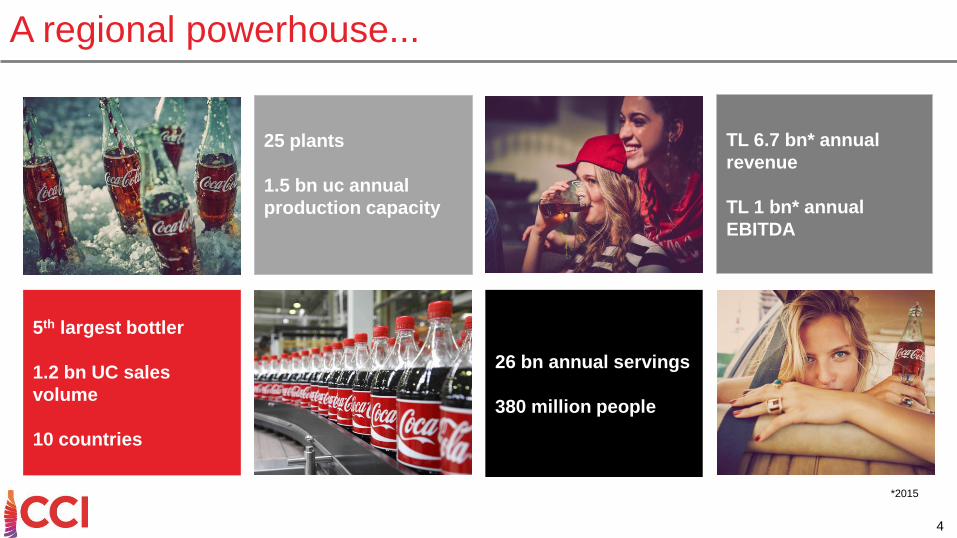

A regional powerhouse...

5th largest bottler

1.2 bn UC sales

volume

10 countries

25 plants

1.5 bn uc annual

production capacity

26 bn annual servings

380 million people

TL 6.7 bn* annual

revenue

TL 1 bn* annual

EBITDA

4

*2015

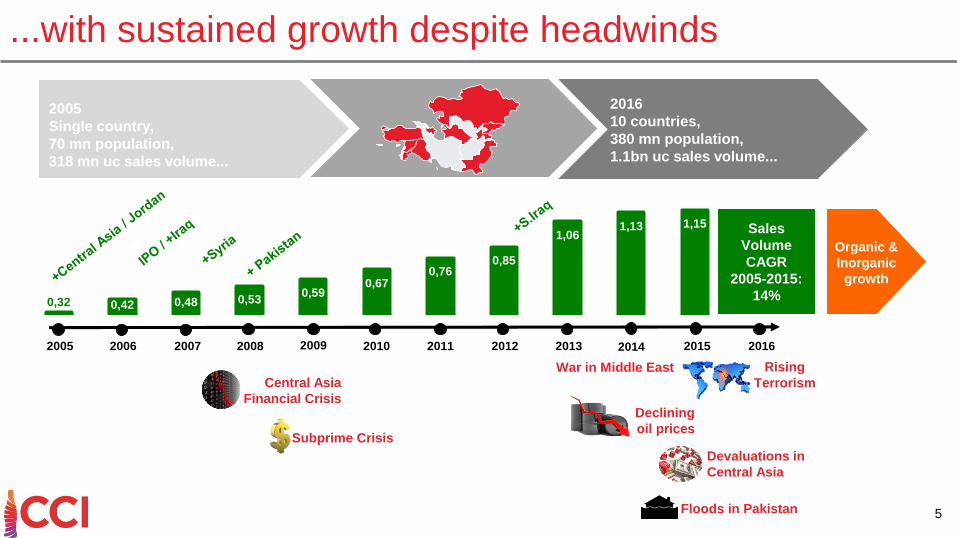

...with sustained growth despite headwinds

2005

Single country,

70 mn population,

318 mn uc sales volume...

2016

10 countries,

380 mn population,

1.1bn uc sales volume...

War in Middle East Rising

TerrorismCentral Asia

Financial Crisis

Devaluations in

Central Asia

Declining

oil pricesSubprime Crisis

Floods in Pakistan

0,32 0,42 0,48 0,530,59

0,670,76

0,85

1,061,13 1,15

2005 2007 2008 2009 2010 2011 2012 2013 20142006 2015 2016

Sales

Volume

CAGR

2005-2015:

14%

Organic &

Inorganic

growth

5

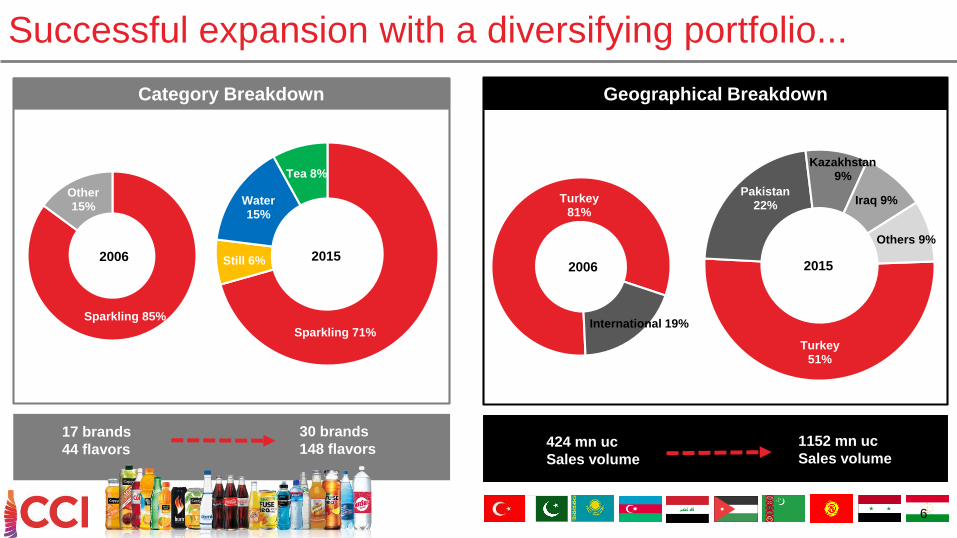

Successful expansion with a diversifying portfolio...

Turkey51%

Pakistan22%

Kazakhstan9%

Iraq 9%

Others 9%

Turkey81%

International 19%

2006 2015

Geographical Breakdown

Sparkling 71%

Still 6%

Water15%

Tea 8%

2015

Sparkling 85%

Other15%

2006

Category Breakdown Geographical Breakdown

1152 mn uc

Sales volume424 mn uc

Sales volume

17 brands

44 flavors

30 brands

148 flavors

6

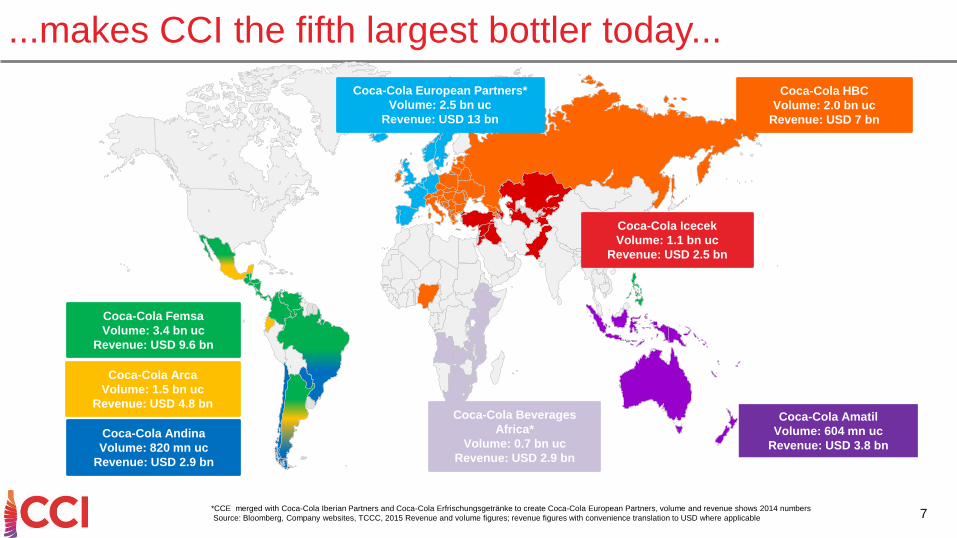

Coca-Cola Femsa

Volume: 3.4 bn uc

Revenue: USD 9.6 bn

Coca-Cola Arca

Volume: 1.5 bn uc

Revenue: USD 4.8 bn

Coca-Cola Andina

Volume: 820 mn uc

Revenue: USD 2.9 bn

Coca-Cola HBC

Volume: 2.0 bn uc

Revenue: USD 7 bn

Coca-Cola Amatil

Volume: 604 mn uc

Revenue: USD 3.8 bn

Coca-Cola Icecek

Volume: 1.1 bn uc

Revenue: USD 2.5 bn

Coca-Cola European Partners*

Volume: 2.5 bn uc

Revenue: USD 13 bn

*CCE merged with Coca-Cola Iberian Partners and Coca-Cola Erfrischungsgetränke to create Coca-Cola European Partners, volume and revenue shows 2014 numbers

Source: Bloomberg, Company websites, TCCC, 2015 Revenue and volume figures; revenue figures with convenience translation to USD where applicable

Coca-Cola Beverages

Africa*

Volume: 0.7 bn uc

Revenue: USD 2.9 bn

...makes CCI the fifth largest bottler today...

7

8

Kyrgyzstan

Afghanistan

Egypt

Pakistan

TurkmenistanIraq

Azerbaijan

Kazakhstan

Russia

TurkeyJordan

Italy

OmanPoland

Greece

South Africa

Saudi ArabiaHungary

UK

Spain

Germany

Bulgaria

Argentina

USA

Mexico

Tajikistan

0

20

40

60

80

100

120

140

160

180

0 10.000 20.000 30.000 40.000 50.000 60.000

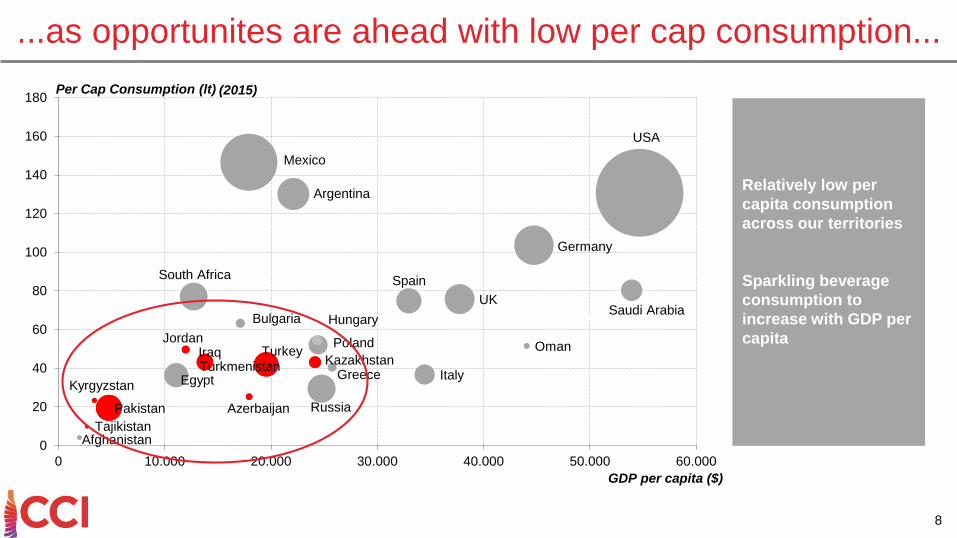

#4

Per Cap Consumption (lt)

GDP per capita ($)

(2015)

...as opportunites are ahead with low per cap consumption...

Relatively low per

capita consumption

across our territories

Sparkling beverage

consumption to

increase with GDP per

capita

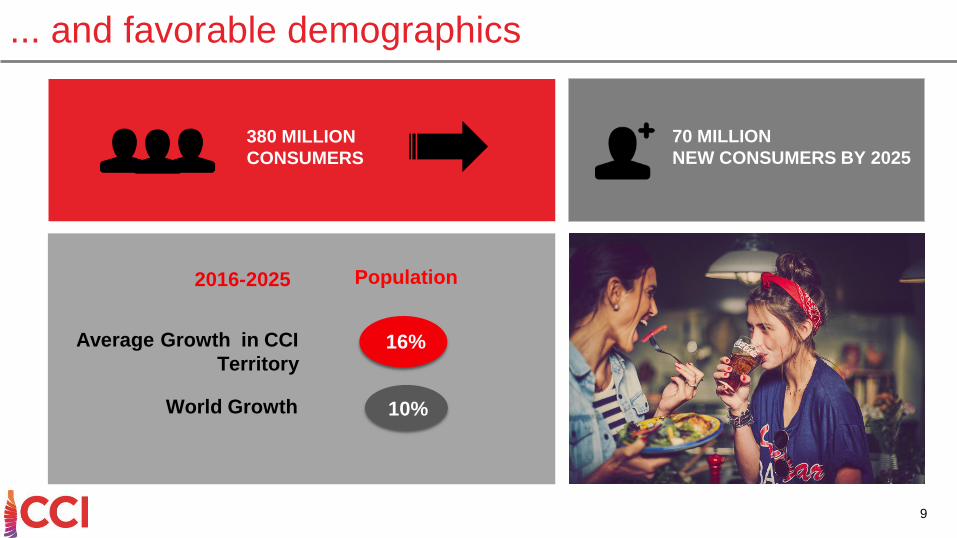

... and favorable demographics

380 MILLION

CONSUMERS

70 MILLION

NEW CONSUMERS BY 2025

World Growth

Average Growth in CCI

Territory

2016-2025 Population

16%

10%

9

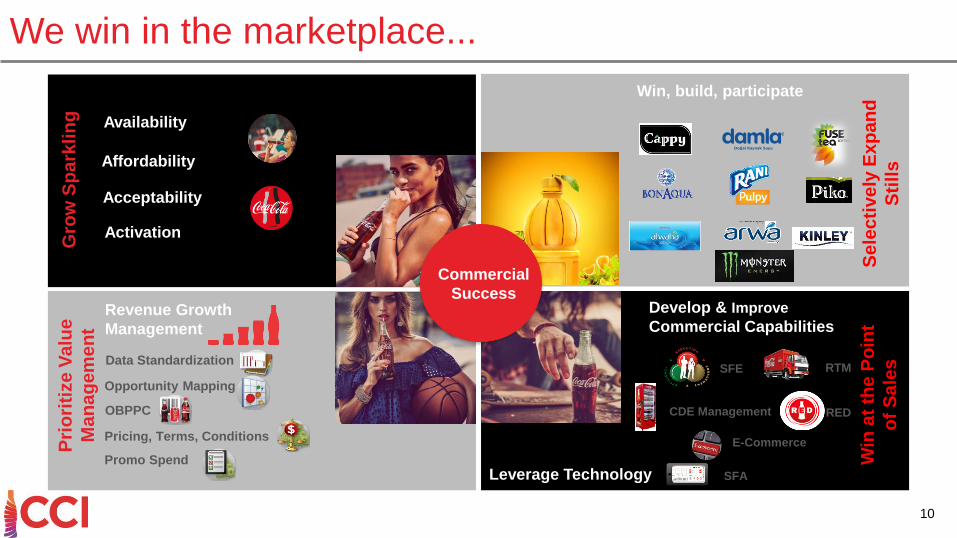

We win in the marketplace...

Availability

Acceptability

Activation

Gro

w S

pa

rkli

ng

Se

lec

tive

ly E

xp

an

d

Sti

lls

Win, build, participate

Revenue Growth

Management

Pri

ori

tize

Va

lue

Ma

na

gem

en

t

Opportunity Mapping

OBPPC

Pricing, Terms, Conditions

Promo Spend

Data Standardization

Win

at

the

Po

int

of

Sa

les

Develop & Improve

Commercial Capabilities

SFE RTM

RED

E-Commerce

CDE Management

Leverage Technology SFA

Commercial

Success

10

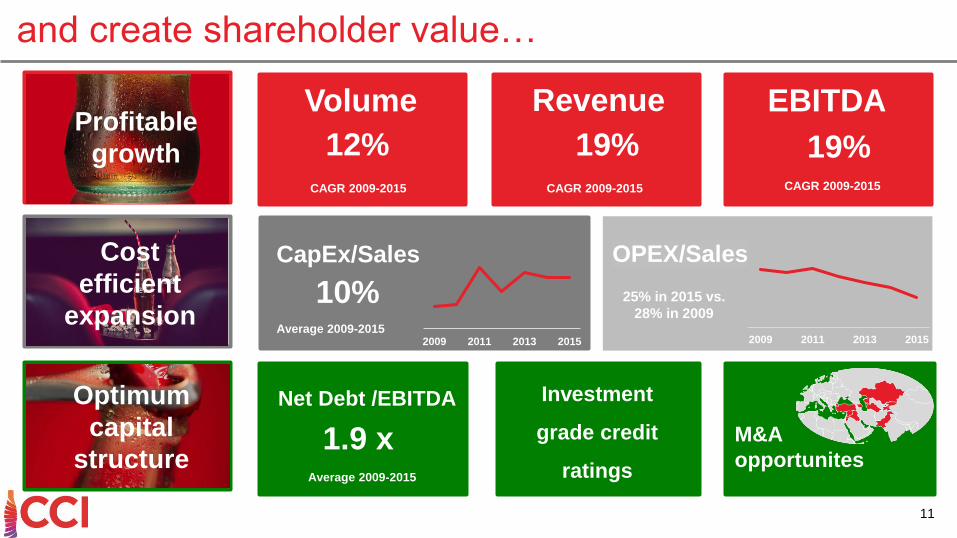

Affordability

19%

Revenue

CAGR 2009-2015

and create shareholder value…

12%

Volume

CAGR 2009-2015

19%

EBITDA

CAGR 2009-2015

Profitable

growth

10%

CapEx/Sales

Average 2009-2015

1.9 x

Net Debt /EBITDA

Average 2009-2015

M&A

opportunites

11

OPEX/Sales

2009 2011 2013 2015

Optimum

capital

structure

Cost

efficient

expansion

Investment

grade credit

ratings

25% in 2015 vs.

28% in 2009

2009 2011 2013 2015

Net Debt / EBITDA

2.09x 1H16 vs.

2.71x in 1H15

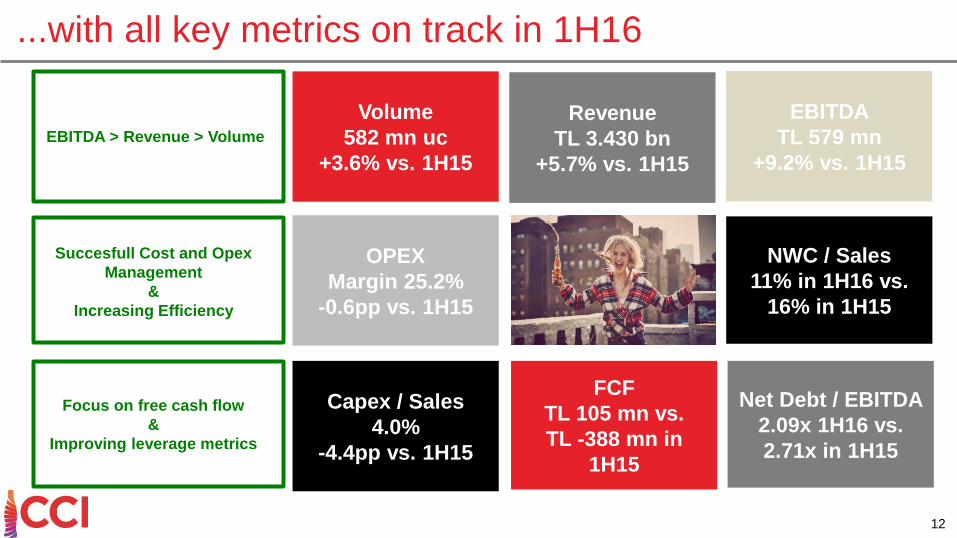

...with all key metrics on track in 1H16

Volume

582 mn uc

+3.6% vs. 1H15

EBITDA

TL 579 mn

+9.2% vs. 1H15

OPEX

Margin 25.2%

-0.6pp vs. 1H15

FCF

TL 105 mn vs.

TL -388 mn in

1H15

Revenue

TL 3.430 bn

+5.7% vs. 1H15

Capex / Sales

4.0%

-4.4pp vs. 1H15

12

NWC / Sales

11% in 1H16 vs.

16% in 1H15

EBITDA > Revenue > Volume

Succesfull Cost and Opex

Management

&

Increasing Efficiency

Focus on free cash flow

&

Improving leverage metrics

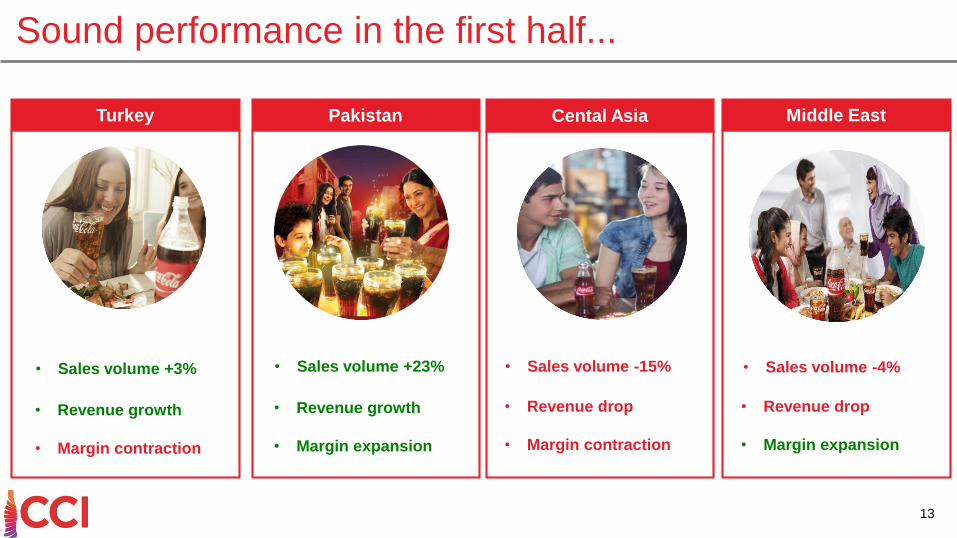

Sound performance in the first half...

Turkey Middle EastCental AsiaPakistan

• Sales volume +3% • Sales volume +23% • Sales volume -15% • Sales volume -4%

• Revenue growth

• Margin contraction

• Revenue growth

• Margin expansion

• Revenue drop

• Margin contraction

• Revenue drop

• Margin expansion

13

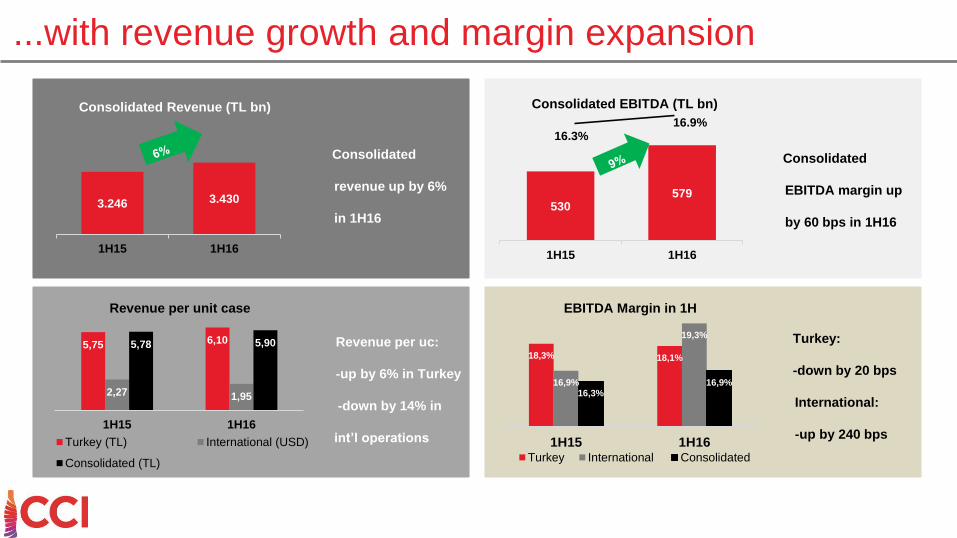

...with revenue growth and margin expansion

3.246 3.430

1H15 1H16

Consolidated Revenue (TL bn)

5,75 6,10

2,27 1,95

5,78 5,90

1H15 1H16

Revenue per unit case

Turkey (TL) International (USD)

Consolidated (TL)

Consolidated

revenue up by 6%

in 1H16

Turkey:

-down by 20 bps

International:

-up by 240 bps

530579

1H15 1H16

Consolidated EBITDA (TL bn)

16.3%16.9%

18,3% 18,1%

16,9%

19,3%

16,3%16,9%

1H15 1H16

EBITDA Margin in 1H

Turkey International Consolidated

Consolidated

EBITDA margin up

by 60 bps in 1H16

Revenue per uc:

-up by 6% in Turkey

-down by 14% in

int’l operations

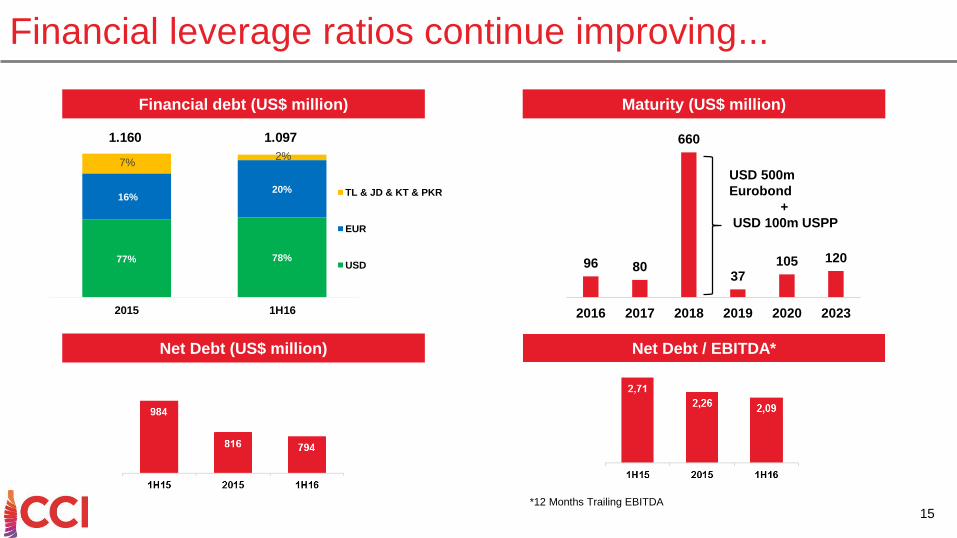

Financial leverage ratios continue improving...

77% 78%

16%20%

7%2%

2015 1H16

TL & JD & KT & PKR

EUR

USD

1.0971.160

Financial debt (US$ million)

Net Debt (US$ million) Net Debt / EBITDA*

Maturity (US$ million)

*12 Months Trailing EBITDA

15

96 80

660

37105 120

2016 2017 2018 2019 2020 2023

USD 500m

Eurobond

+

USD 100m USPP

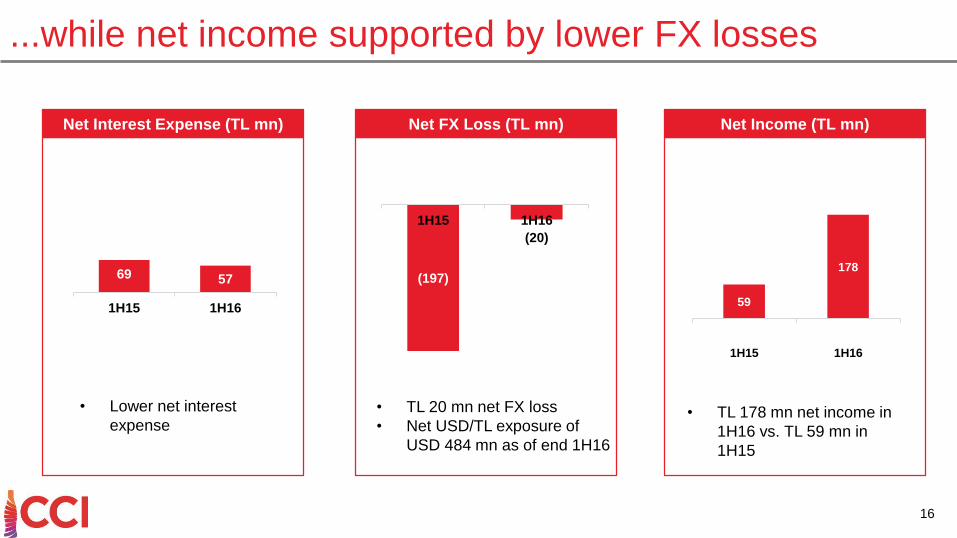

...while net income supported by lower FX losses

• TL 178 mn net income in

1H16 vs. TL 59 mn in

1H15

• Lower net interest

expense• TL 20 mn net FX loss

• Net USD/TL exposure of

USD 484 mn as of end 1H16

Net Interest Expense (TL mn) Net FX Loss (TL mn) Net Income (TL mn)

69 57

1H15 1H16

(197)

(20)

1H15 1H16

59

178

1H15 1H16

16

Key takeaways

17

Challenging

operating

environment

Improving

leverage ratios

Positive FCF

Maintaining

growth

momentum

Succesfull

cost & opex

management

Healhty

balance sheet

Focus on RGM

Increasing

efficiency

Appendix18

19

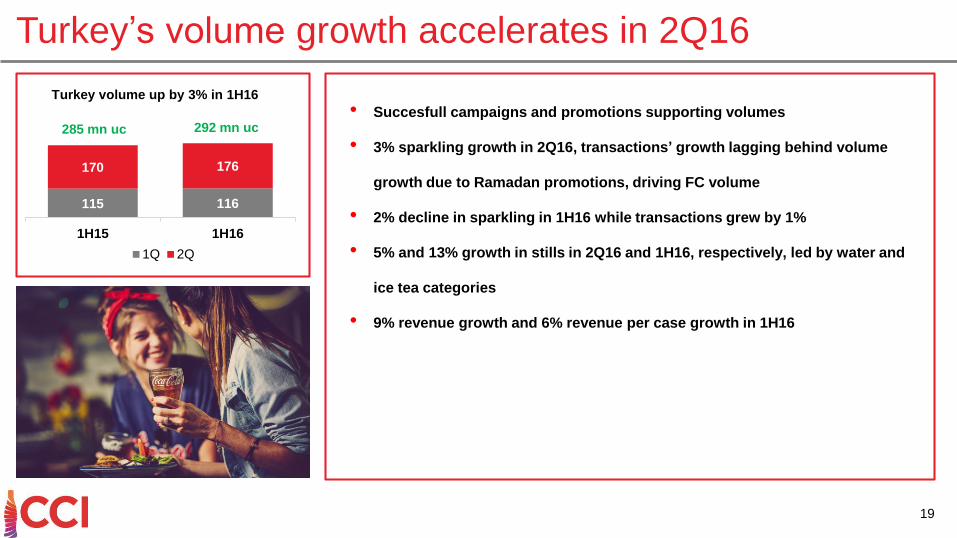

Turkey’s volume growth accelerates in 2Q16

• Succesfull campaigns and promotions supporting volumes

• 3% sparkling growth in 2Q16, transactions’ growth lagging behind volume

growth due to Ramadan promotions, driving FC volume

• 2% decline in sparkling in 1H16 while transactions grew by 1%

• 5% and 13% growth in stills in 2Q16 and 1H16, respectively, led by water and

ice tea categories

• 9% revenue growth and 6% revenue per case growth in 1H16

115 116

170 176

1H15 1H16

Turkey volume up by 3% in 1H16

1Q 2Q

285 mn uc 292 mn uc

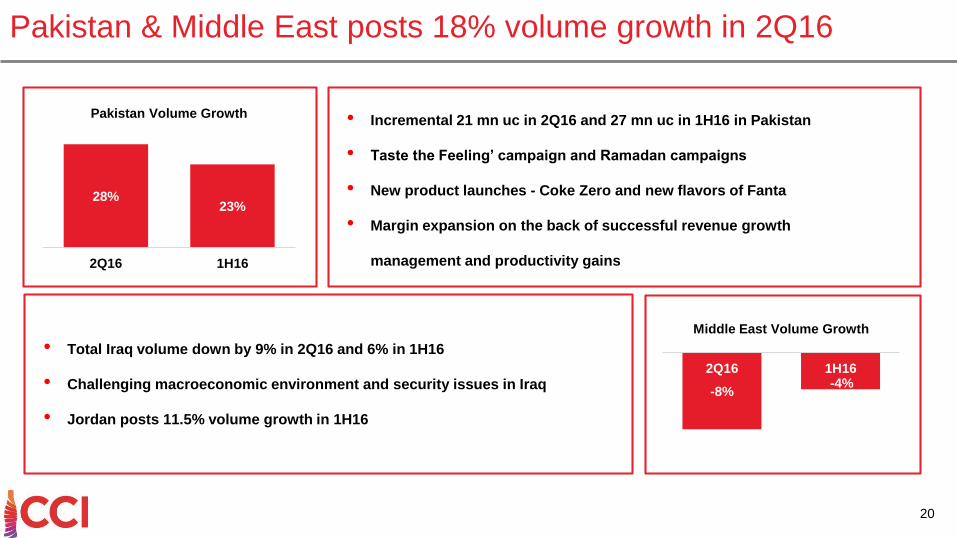

• Incremental 21 mn uc in 2Q16 and 27 mn uc in 1H16 in Pakistan

• Taste the Feeling’ campaign and Ramadan campaigns

• New product launches - Coke Zero and new flavors of Fanta

• Margin expansion on the back of successful revenue growth

management and productivity gains

• Total Iraq volume down by 9% in 2Q16 and 6% in 1H16

• Challenging macroeconomic environment and security issues in Iraq

• Jordan posts 11.5% volume growth in 1H16

Pakistan & Middle East posts 18% volume growth in 2Q16

20

28%23%

2Q16 1H16

Pakistan Volume Growth

-8%-4%

2Q16 1H16

Middle East Volume Growth

21

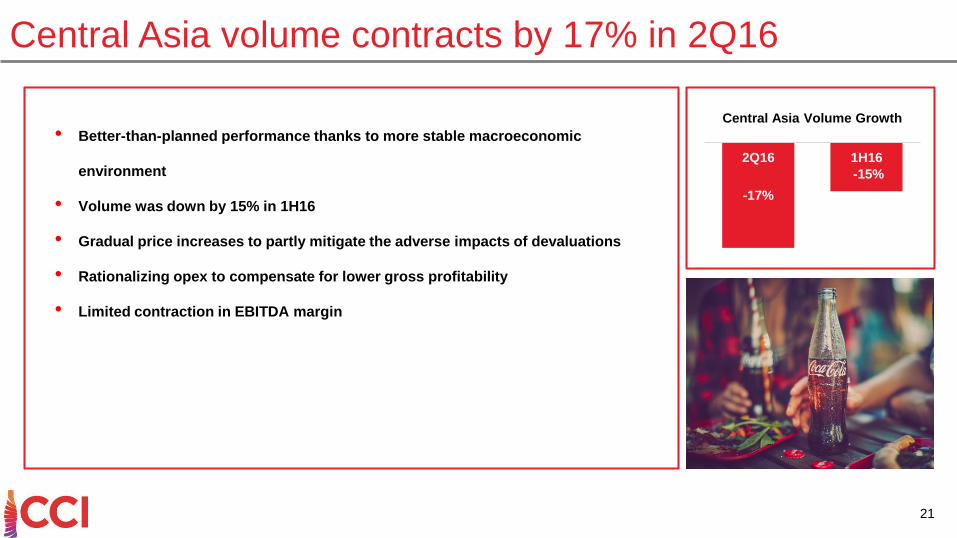

Central Asia volume contracts by 17% in 2Q16

• Better-than-planned performance thanks to more stable macroeconomic

environment

• Volume was down by 15% in 1H16

• Gradual price increases to partly mitigate the adverse impacts of devaluations

• Rationalizing opex to compensate for lower gross profitability

• Limited contraction in EBITDA margin

-17%

-15%

2Q16 1H16

Central Asia Volume Growth

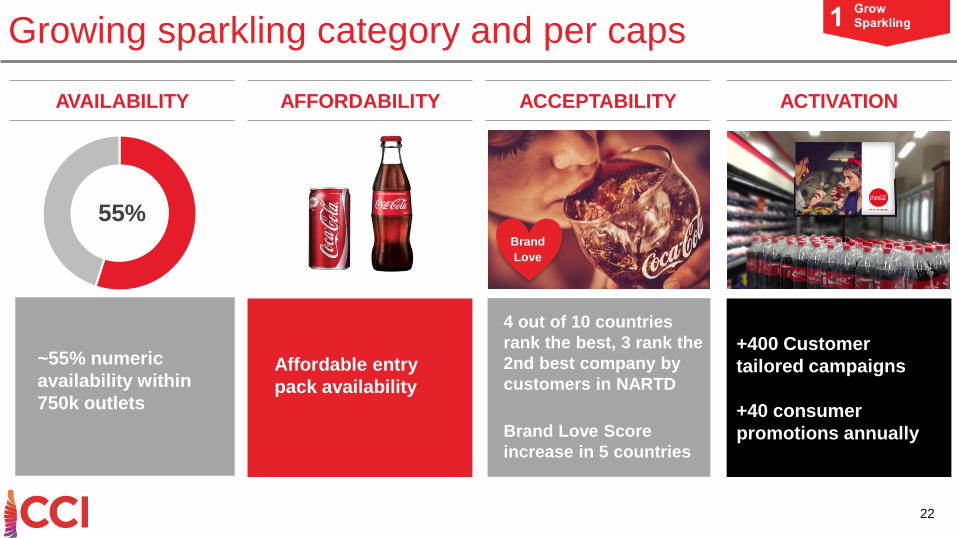

AVAILABILITY AFFORDABILITY ACCEPTABILITY

55%

ACTIVATION

Affordable entry

pack availability

Brand

Love

Growing sparkling category and per caps

~55% numeric

availability within

750k outlets

4 out of 10 countries

rank the best, 3 rank the

2nd best company by

customers in NARTD

Brand Love Score

increase in 5 countries

+400 Customer

tailored campaigns

+40 consumer

promotions annually

22

Selectively expanding stills

Win Today Build for Tomorrow Participate ProfitablyWin in Attractive Categories Create Winning Positions Capture Fair Share of Profit

Prioritize countries & portfolio

23

Occasion

Brand

Package

Price

Channel

IC mix in

portfolio

27%

+6pp in

2010-2015

Revenue Growth Management

24

Accelerating revenue and margin growth

Effective Customer

Investment

&

Management

Focus on IC

transactions

+155%

in 2010-2015

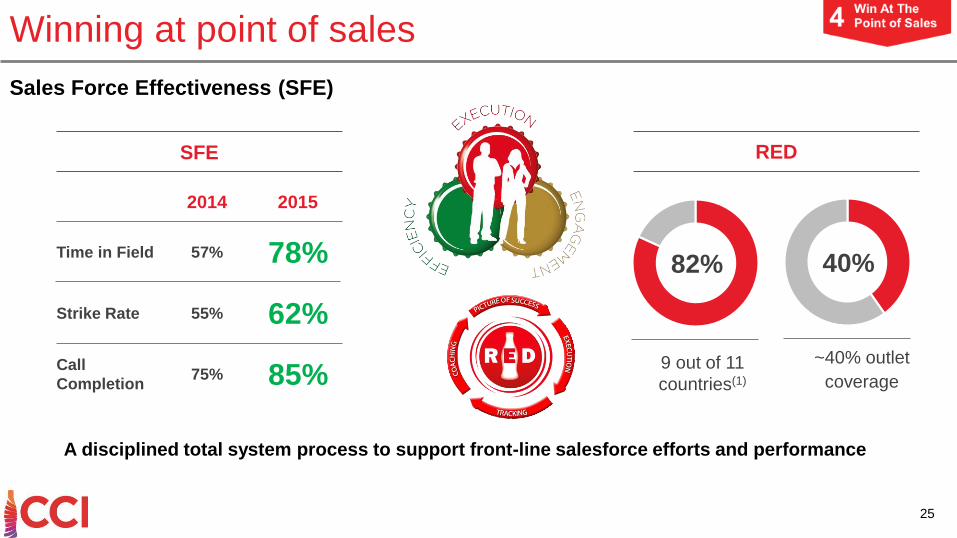

Winning at point of sales

SFE

2015

Time in Field 57% 78%

2014

Strike Rate 55% 62%

Call

Completion75% 85%

RED

9 out of 11

countries(1)

82% 40%

~40% outlet

coverage

A disciplined total system process to support front-line salesforce efforts and performance

Sales Force Effectiveness (SFE)

25

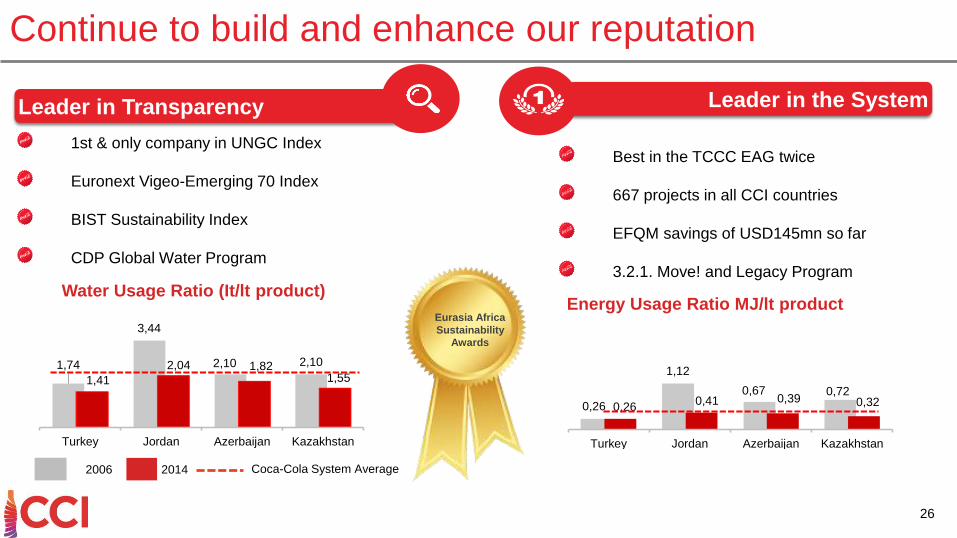

Continue to build and enhance our reputation

1st & only company in UNGC Index

Euronext Vigeo-Emerging 70 Index

BIST Sustainability Index

CDP Global Water Program

Leader in Transparency

Best in the TCCC EAG twice

667 projects in all CCI countries

EFQM savings of USD145mn so far

3.2.1. Move! and Legacy Program

Leader in the System

1,74

3,44

2,10 2,10

1,41

2,04 1,821,55

Turkey Jordan Azerbaijan Kazakhstan

Water Usage Ratio (It/lt product)

0,26

1,12

0,67 0,72

0,260,41 0,39 0,32

Turkey Jordan Azerbaijan Kazakhstan

20142006 Coca-Cola System Average

Energy Usage Ratio MJ/lt productEurasia Africa

Sustainability

Awards

26

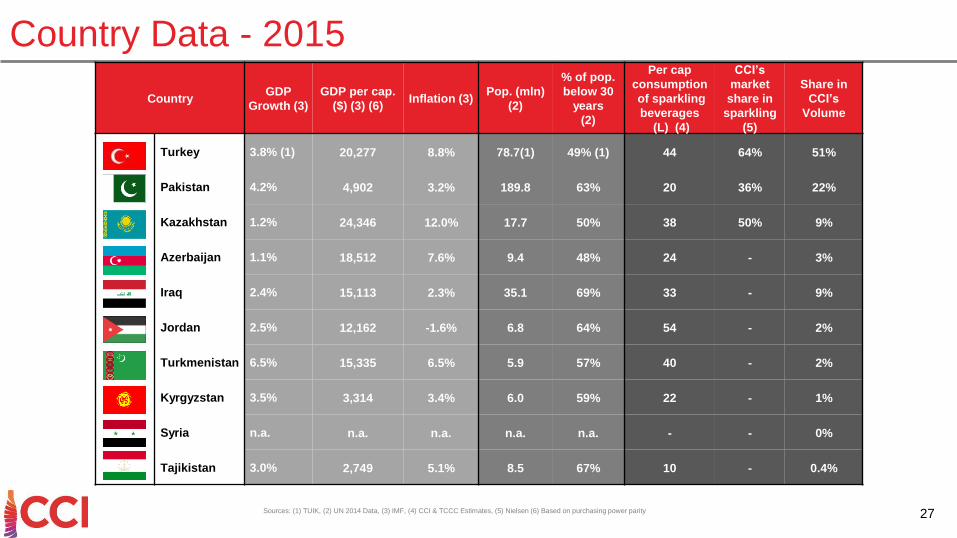

CountryGDP

Growth (3)

GDP per cap.

($) (3) (6)Inflation (3)

Pop. (mln)

(2)

% of pop.

below 30

years

(2)

Per cap

consumption

of sparkling

beverages

(L) (4)

CCI’s

market

share in

sparkling

(5)

Share in

CCI’s

Volume

Turkey 3.8% (1) 20,277 8.8% 78.7(1) 49% (1) 44 64% 51%

Pakistan 4.2% 4,902 3.2% 189.8 63% 20 36% 22%

Kazakhstan 1.2% 24,346 12.0% 17.7 50% 38 50% 9%

Azerbaijan 1.1% 18,512 7.6% 9.4 48% 24 - 3%

Iraq 2.4% 15,113 2.3% 35.1 69% 33 - 9%

Jordan 2.5% 12,162 -1.6% 6.8 64% 54 - 2%

Turkmenistan 6.5% 15,335 6.5% 5.9 57% 40 - 2%

Kyrgyzstan 3.5% 3,314 3.4% 6.0 59% 22 - 1%

Syria n.a. n.a. n.a. n.a. n.a. - - 0%

Tajikistan 3.0% 2,749 5.1% 8.5 67% 10 - 0.4%

Sources: (1) TUIK, (2) UN 2014 Data, (3) IMF, (4) CCI & TCCC Estimates, (5) Nielsen (6) Based on purchasing power parity

Country Data - 2015

27

28

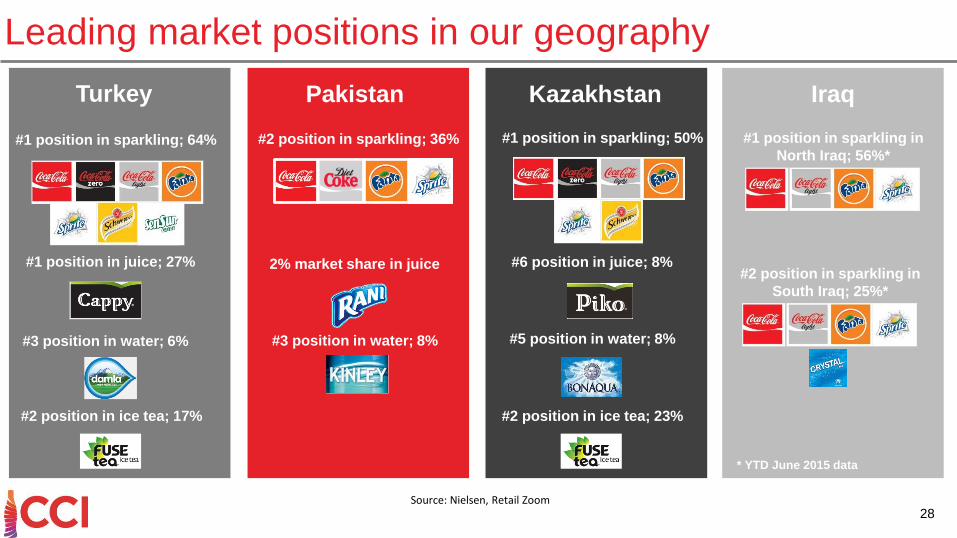

Leading market positions in our geography

Turkey

#1 position in sparkling; 64%

#1 position in juice; 27%

#3 position in water; 6%

#2 position in ice tea; 17%

Pakistan

#2 position in sparkling; 36%

#3 position in water; 8%

Kazakhstan

#1 position in sparkling; 50%

#6 position in juice; 8%

#5 position in water; 8%

#2 position in ice tea; 23%

Iraq

#1 position in sparkling in

North Iraq; 56%*

2% market share in juice

* YTD June 2015 data

#2 position in sparkling in

South Iraq; 25%*

Source: Nielsen, Retail Zoom

Ratings

29

Credit Ratings

Long Term Issuer Rating, ‘Baa3’, Under Review

(Moody’s rating, July 21, 2016)

Local Currency Senior Unsecured and IDR, ‘BBB’, Negative Outlook

(Fitch Rating, August 26, 2016)

Corporate Governance Rating

9.45 out of 10

(Saha Rating, July 1, 2016)

Coca-Cola İçecek Investor Relations

Tel: +90 216 528 4000 Fax: +90 216 365 8457

------------------------------------Deniz Can Yücel

Investor Relations ManagerTel: +90 216 528 3386

Borsa Istanbul: CCOLA.IS - Bloomberg: CCOLA TI - Reuters: CCOLA.IS ADR-OTC: COLAY - Eurobond - Irish Stock Exchange: CCOLAT 30