Embed Size (px)

Citation preview

12-15 NİSAN2015VARŞOVA-KRAKOV

1 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

Overview of the legal system – forms of business activity available in Poland

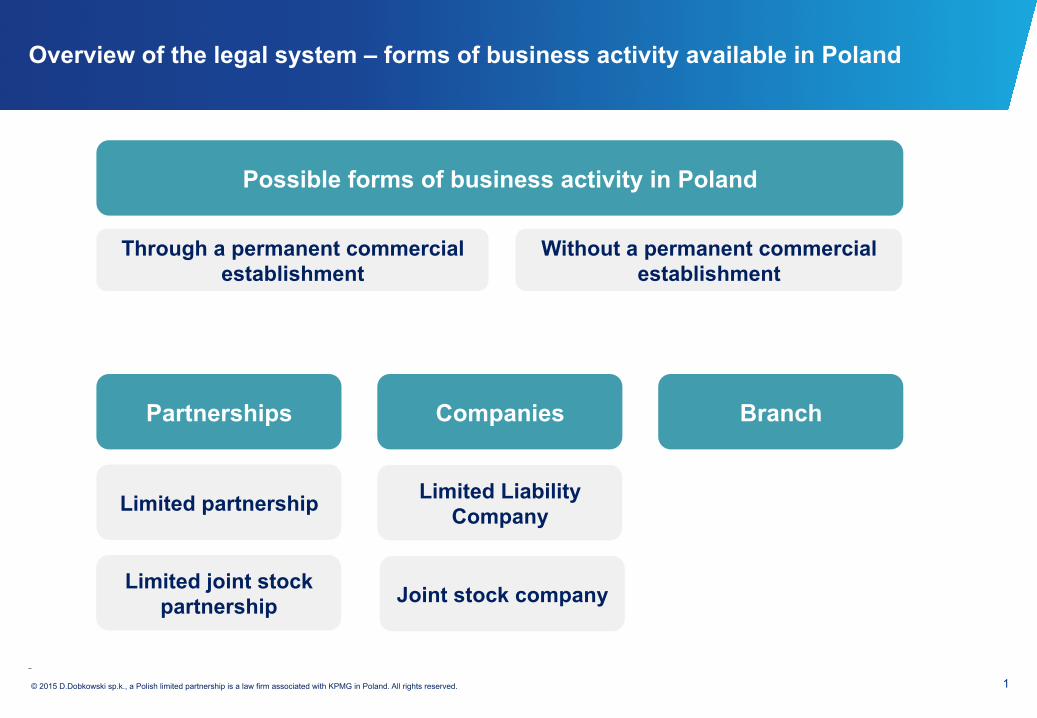

Possible forms of business activity in Poland

Through a permanent commercial establishment

Without a permanent commercial establishment

Partnerships Companies Branch

Limited partnership Limited Liability Company

Limited joint stock partnership Joint stock company

2 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

Overview of the legal system – forms of business activity available in Poland

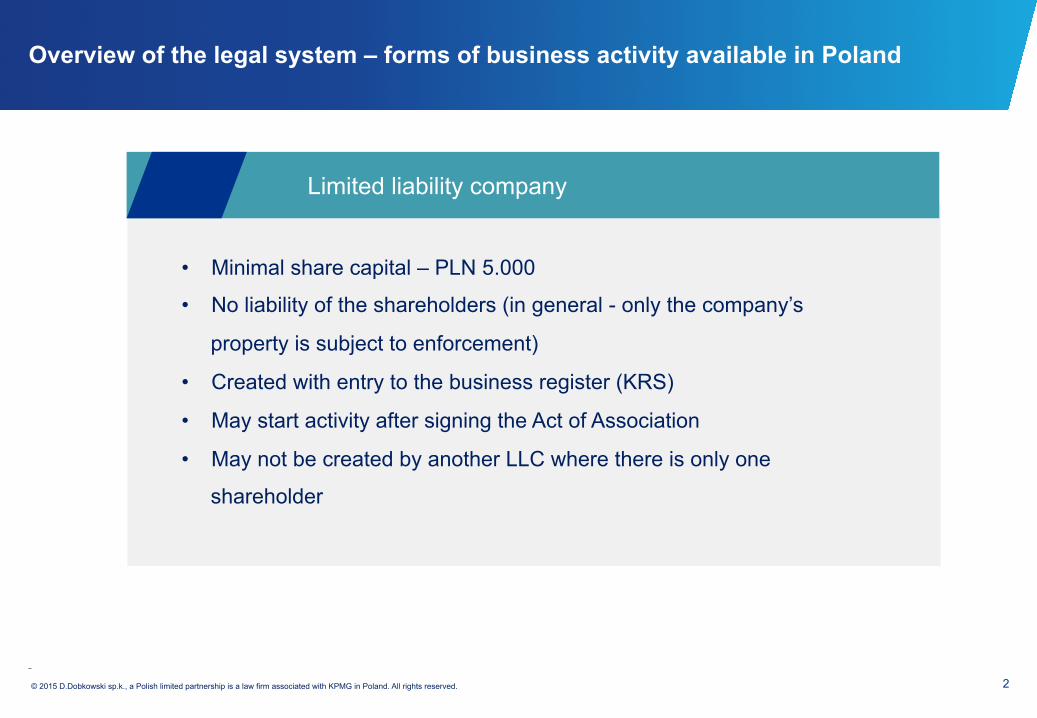

Limited liability company

• Minimal share capital – PLN 5.000

• No liability of the shareholders (in general - only the company’s

property is subject to enforcement)

• Created with entry to the business register (KRS)

• May start activity after signing the Act of Association

• May not be created by another LLC where there is only one

shareholder

3 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

Overview of the legal system – forms of business activity available in Poland

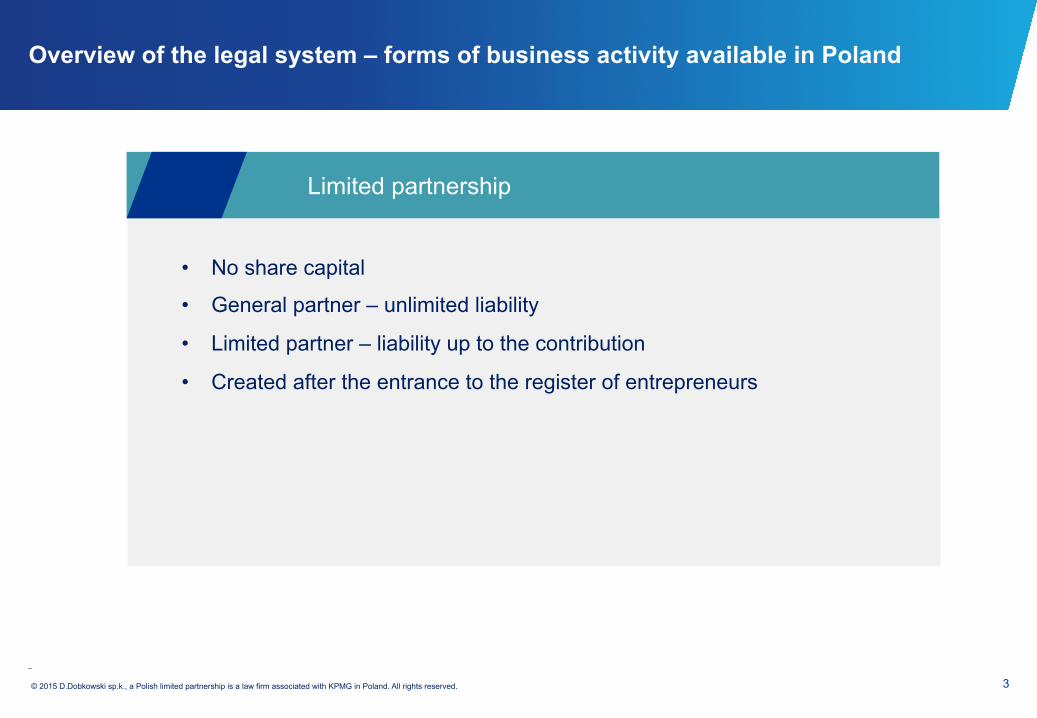

Limited partnership

• No share capital

• General partner – unlimited liability

• Limited partner – liability up to the contribution

• Created after the entrance to the register of entrepreneurs

4 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

Overview of the legal system – forms of business activity available in Poland

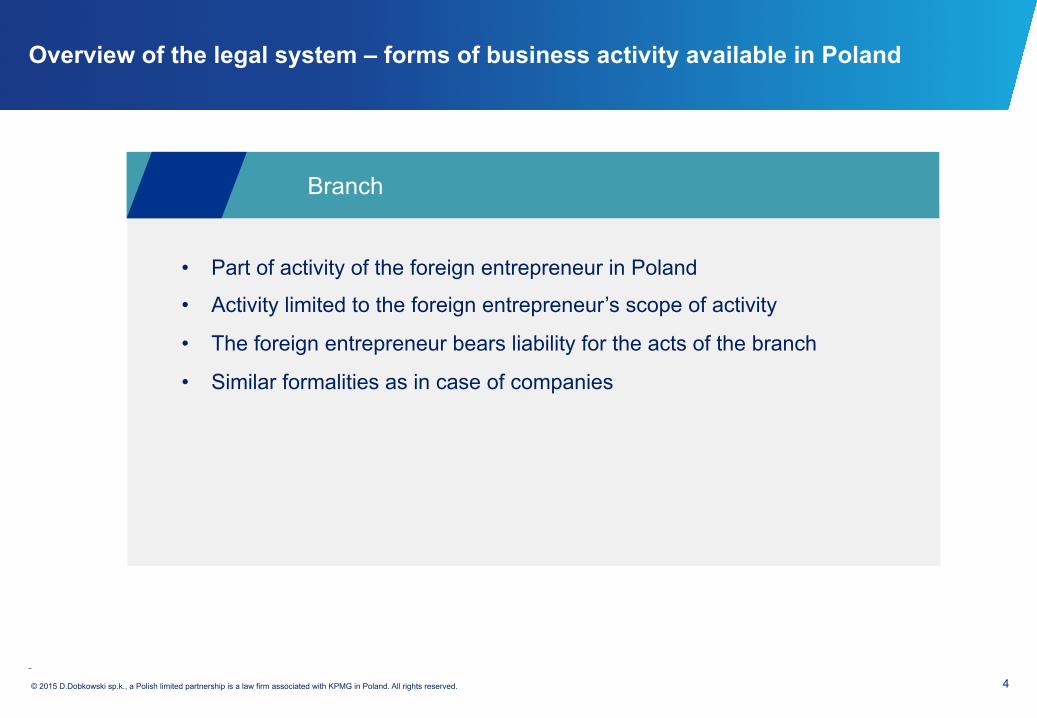

Branch

• Part of activity of the foreign entrepreneur in Poland

• Activity limited to the foreign entrepreneur’s scope of activity

• The foreign entrepreneur bears liability for the acts of the branch

• Similar formalities as in case of companies

5 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

Lease agreements for premises in Shopping Centres - I

• The Landlord authorizes the Tenant to use the premises for business purposes

• May be concluded for an indefinite period or definite period (up to 30 years)

• Generally required payments:

Ø Fixed Rent

Ø Turnover Rent

Ø Service Charges

Ø Marketing Charges

• The agreements are extensive (50-60 pages)

• As the agreements contain many provisions

unfavorable for tenants, before signing they

require consultation with a lawyer and

negotiations with the Landlord

6 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

Lease agreements for premises in Shopping Centres - II

Most significant risks related to the lease agreements:

• Concluded for a definite (long) period of time (min. 5 years)

• No possibility for the Tenant to terminate it prematurely for economic reasons

Ø Tenant has to use the Premises for the agreed period and pay the Rent

• Possibility for the Landlord to terminate the agreement for various reasons

e.g. in case anyone files for the Tenant’s bankruptcy

Ø Such reasons may in fact be used as an excuse to terminate the agreement

(i.e. if a better tenant wants to lease the premises)

7 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

Activity in Poland without a permanent establishment – part I

Franchising agreements

• The Franchisor authorizes the Franchisee to use its business concept including trademarks

• May include the Franchisee’s obligation to purchase the Franchisor’s products

• Franchisee is an independent entity • All risks related to the activity subject to the agreement are

borne by the Franchisee • Apart from the payments for products:

ü Entrance payment ü Periodic (most often: monthly) payments dependent on

the turnover ü Marketing charges

8 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

Activity in Poland without a permanent establishment – part II

Commission/agency agreements

• the agent (retailer) sells the goods of the principal

• the goods are sold in the name of the agent or in the name

of the principal

• the agent is entitled to a commission based on the sales of

the goods

• the agent has to transfer to the principal the amounts for

the goods minus commission

• generally the principal remains the owner of the goods -˃

the agent is entitled to return if unsold

9 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

The following taxes are most frequently encountered: ● value added tax (VAT)

● excise tax

● income tax, which is levied on legal persons (Corporate Income Tax) and individuals (Personal Income Tax)

● real estate tax

● stamp duty

● tax on civil law transactions/capital tax (PCC)

● tax on the extraction of certain minerals (copper and silver).

Apart from taxes there might be also other payment obligations like customs

General Rules of Taxation As a general rule, all new businesses are expected to register for tax purposes in Poland and obtain a NIP number (taxpayer identification number).

Additionally, entities conducting business activities are generally required to maintain appropriate records to serve as the basis for tax calculation, compute and settle taxes due during the financial year, make tax prepayments when necessary and follow other tax obligations stipulated in tax acts.

Overview of the tax regime – taxes in Poland

10 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

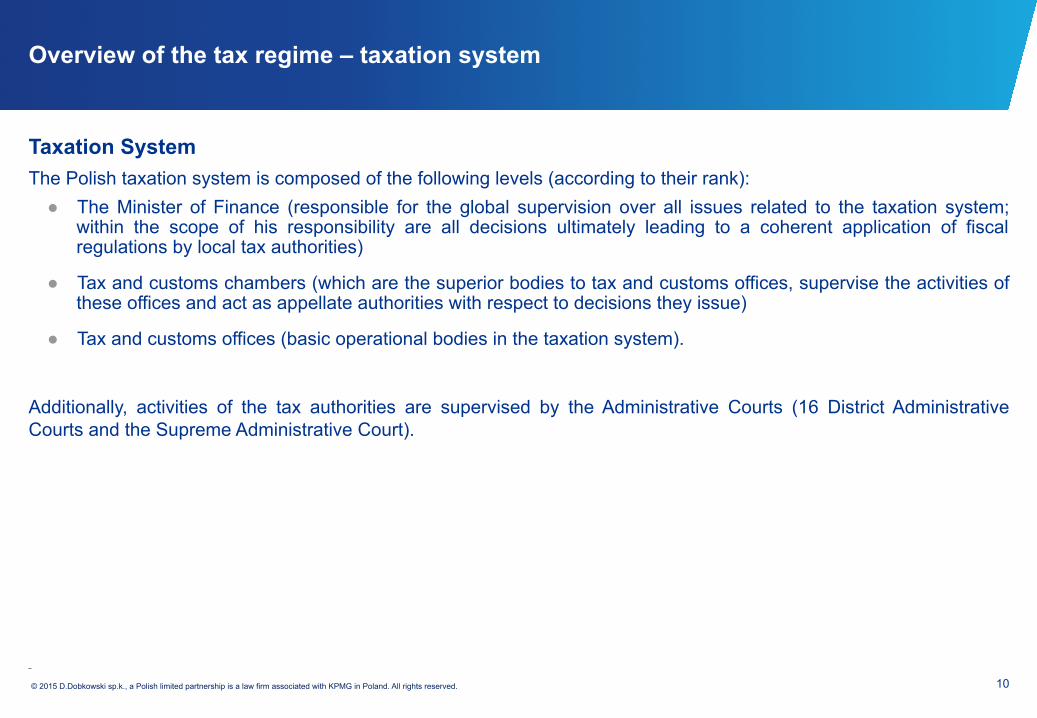

Taxation System The Polish taxation system is composed of the following levels (according to their rank): ● The Minister of Finance (responsible for the global supervision over all issues related to the taxation system;

within the scope of his responsibility are all decisions ultimately leading to a coherent application of fiscal regulations by local tax authorities)

● Tax and customs chambers (which are the superior bodies to tax and customs offices, supervise the activities of these offices and act as appellate authorities with respect to decisions they issue)

● Tax and customs offices (basic operational bodies in the taxation system).

Additionally, activities of the tax authorities are supervised by the Administrative Courts (16 District Administrative Courts and the Supreme Administrative Court).

Overview of the tax regime – taxation system

11 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

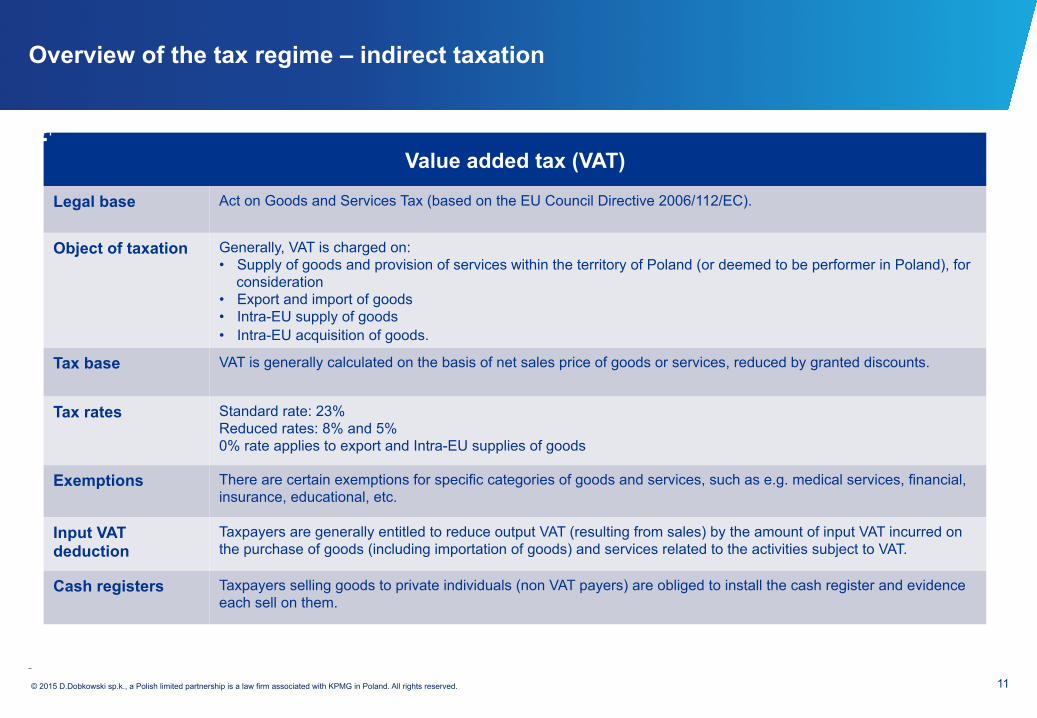

Value added tax (VAT)

Legal base Act on Goods and Services Tax (based on the EU Council Directive 2006/112/EC).

Object of taxation Generally, VAT is charged on: • Supply of goods and provision of services within the territory of Poland (or deemed to be performer in Poland), for

consideration • Export and import of goods • Intra-EU supply of goods • Intra-EU acquisition of goods.

Tax base VAT is generally calculated on the basis of net sales price of goods or services, reduced by granted discounts.

Tax rates Standard rate: 23% Reduced rates: 8% and 5% 0% rate applies to export and Intra-EU supplies of goods

Exemptions There are certain exemptions for specific categories of goods and services, such as e.g. medical services, financial, insurance, educational, etc.

Input VAT deduction

Taxpayers are generally entitled to reduce output VAT (resulting from sales) by the amount of input VAT incurred on the purchase of goods (including importation of goods) and services related to the activities subject to VAT.

Cash registers Taxpayers selling goods to private individuals (non VAT payers) are obliged to install the cash register and evidence each sell on them.

Overview of the tax regime – indirect taxation

12 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

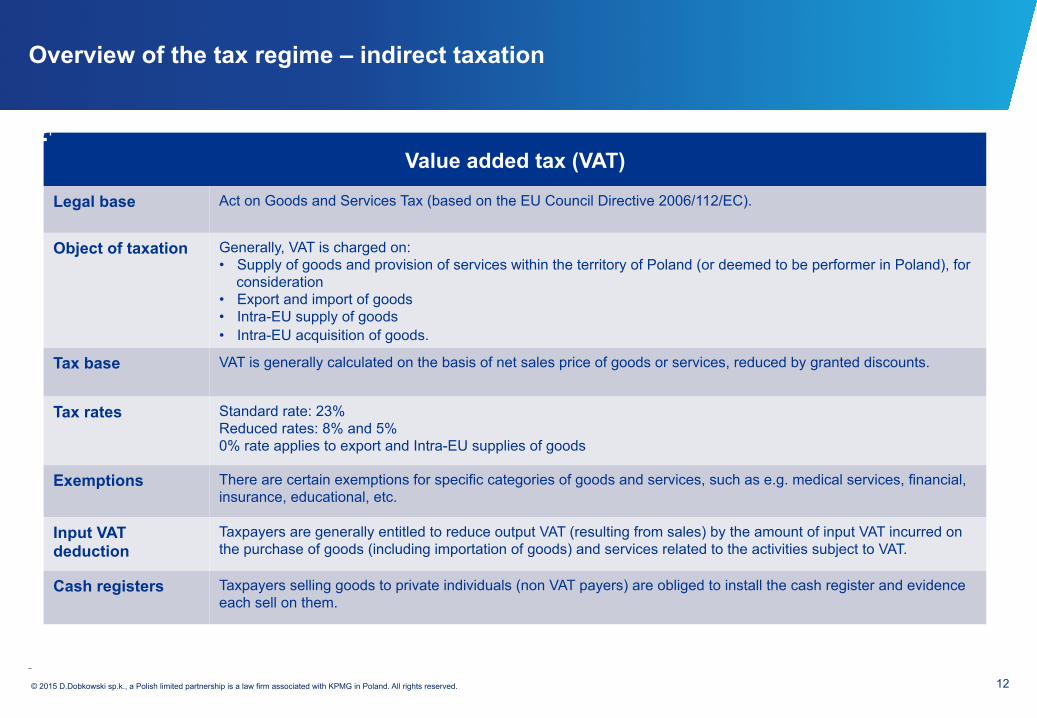

Value added tax (VAT)

Legal base Act on Goods and Services Tax (based on the EU Council Directive 2006/112/EC).

Object of taxation Generally, VAT is charged on: • Supply of goods and provision of services within the territory of Poland (or deemed to be performer in Poland), for

consideration • Export and import of goods • Intra-EU supply of goods • Intra-EU acquisition of goods.

Tax base VAT is generally calculated on the basis of net sales price of goods or services, reduced by granted discounts.

Tax rates Standard rate: 23% Reduced rates: 8% and 5% 0% rate applies to export and Intra-EU supplies of goods

Exemptions There are certain exemptions for specific categories of goods and services, such as e.g. medical services, financial, insurance, educational, etc.

Input VAT deduction

Taxpayers are generally entitled to reduce output VAT (resulting from sales) by the amount of input VAT incurred on the purchase of goods (including importation of goods) and services related to the activities subject to VAT.

Cash registers Taxpayers selling goods to private individuals (non VAT payers) are obliged to install the cash register and evidence each sell on them.

Overview of the tax regime – indirect taxation

13 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

Customs

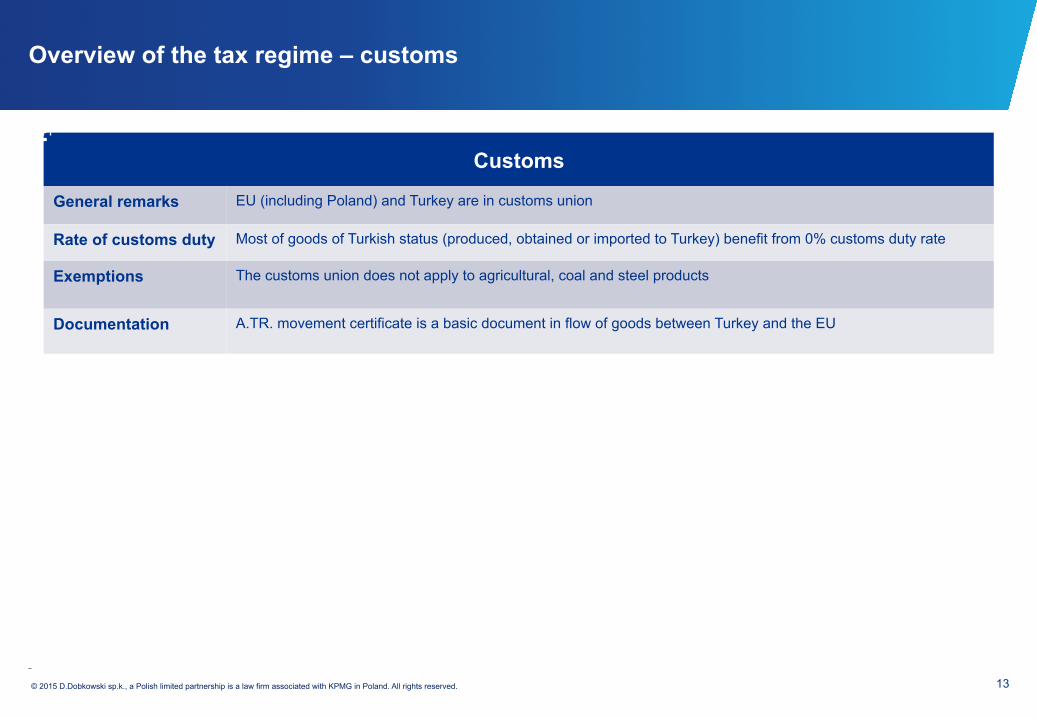

General remarks EU (including Poland) and Turkey are in customs union

Rate of customs duty Most of goods of Turkish status (produced, obtained or imported to Turkey) benefit from 0% customs duty rate

Exemptions

The customs union does not apply to agricultural, coal and steel products

Documentation A.TR. movement certificate is a basic document in flow of goods between Turkey and the EU

Overview of the tax regime – customs

14 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

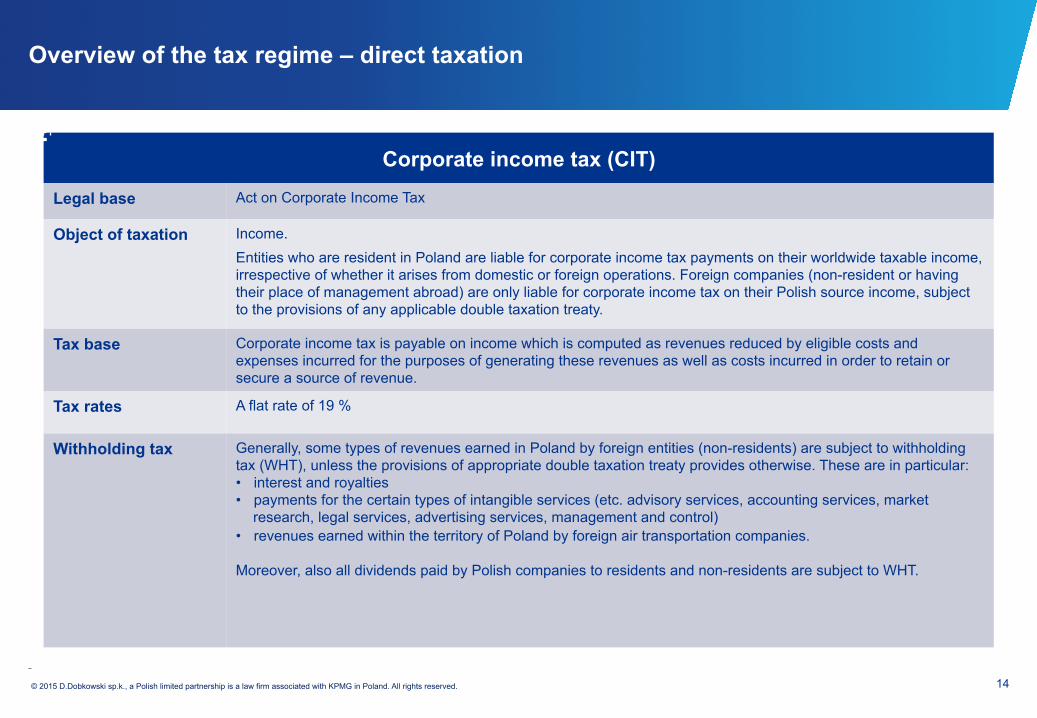

Corporate income tax (CIT)

Legal base Act on Corporate Income Tax

Object of taxation Income.

Entities who are resident in Poland are liable for corporate income tax payments on their worldwide taxable income, irrespective of whether it arises from domestic or foreign operations. Foreign companies (non-resident or having their place of management abroad) are only liable for corporate income tax on their Polish source income, subject to the provisions of any applicable double taxation treaty.

Tax base

Corporate income tax is payable on income which is computed as revenues reduced by eligible costs and expenses incurred for the purposes of generating these revenues as well as costs incurred in order to retain or secure a source of revenue.

Tax rates A flat rate of 19 %

Withholding tax Generally, some types of revenues earned in Poland by foreign entities (non-residents) are subject to withholding tax (WHT), unless the provisions of appropriate double taxation treaty provides otherwise. These are in particular: • interest and royalties • payments for the certain types of intangible services (etc. advisory services, accounting services, market

research, legal services, advertising services, management and control) • revenues earned within the territory of Poland by foreign air transportation companies. Moreover, also all dividends paid by Polish companies to residents and non-residents are subject to WHT.

Overview of the tax regime – direct taxation

15 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

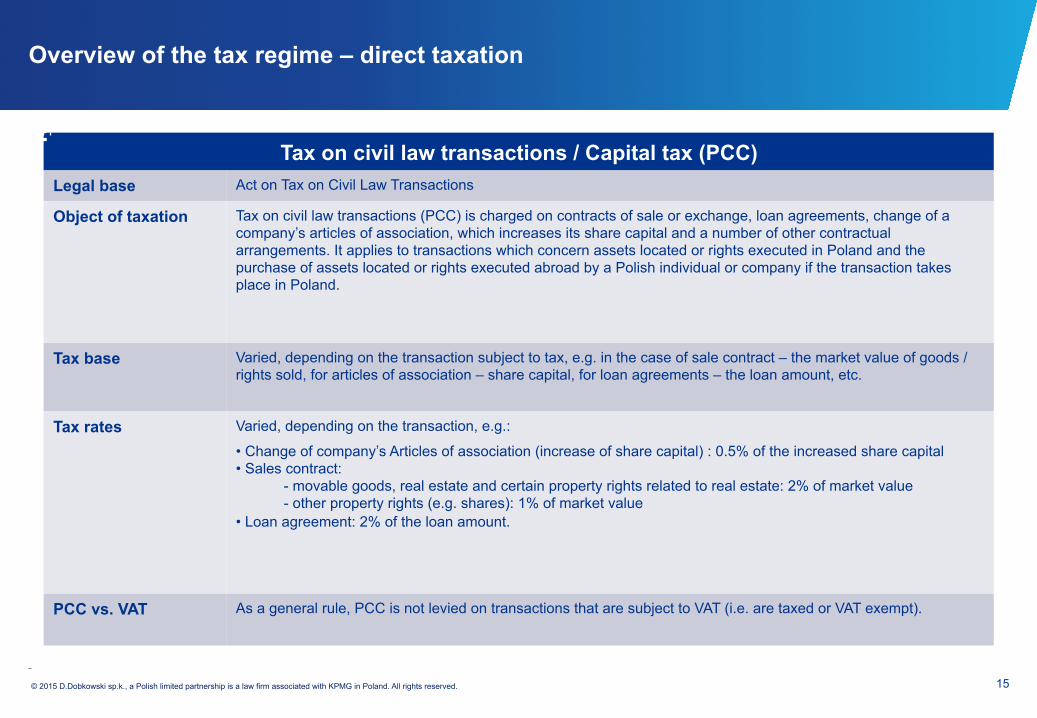

Tax on civil law transactions / Capital tax (PCC) Legal base Act on Tax on Civil Law Transactions

Object of taxation Tax on civil law transactions (PCC) is charged on contracts of sale or exchange, loan agreements, change of a company’s articles of association, which increases its share capital and a number of other contractual arrangements. It applies to transactions which concern assets located or rights executed in Poland and the purchase of assets located or rights executed abroad by a Polish individual or company if the transaction takes place in Poland.

Tax base

Varied, depending on the transaction subject to tax, e.g. in the case of sale contract – the market value of goods / rights sold, for articles of association – share capital, for loan agreements – the loan amount, etc.

Tax rates Varied, depending on the transaction, e.g.:

• Change of company’s Articles of association (increase of share capital) : 0.5% of the increased share capital • Sales contract:

- movable goods, real estate and certain property rights related to real estate: 2% of market value - other property rights (e.g. shares): 1% of market value

• Loan agreement: 2% of the loan amount.

PCC vs. VAT As a general rule, PCC is not levied on transactions that are subject to VAT (i.e. are taxed or VAT exempt).

Overview of the tax regime – direct taxation

16 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

D. Dobkowski LP

ul. Chłodna 51

00-867 Warsaw

Przemysław Kamil Rosiak Partner Associate, Legal Advisory e-mail: [email protected]

Contact

Magdalena Bęza Senior Associate, Legal Advisory e-mail: [email protected]

Agnieszka Jóźwiak Associate, Legal Advisory e-mail: [email protected]

17 © 2015 D.Dobkowski sp.k., a Polish limited partnership is a law firm associated with KPMG in Poland. All rights reserved.

KPMG Tax M.Michna ul. Chłodna 51

00-867 Warsaw

Jacek Bajger Tax Partner, Tax e-mail: [email protected]

Contact

Dominika Łabędzka Tax Manager, Tax ICT e-mail: [email protected]

Łukasz Daniek Tax Supervisor, Tax VAT e-mail: [email protected]