Embed Size (px)

Citation preview

© benefitexpress 2016

Mid-Year Election Changes

• General irrevocability rule - no change required for the plan year.

• 15 events are recognized by the IRS as permitting mid-year election changes.

• Other events are recognized permitting mid-year election changes.

• Administrative requirements that must be met to implement a mid-year election change.

© benefitexpress 2016

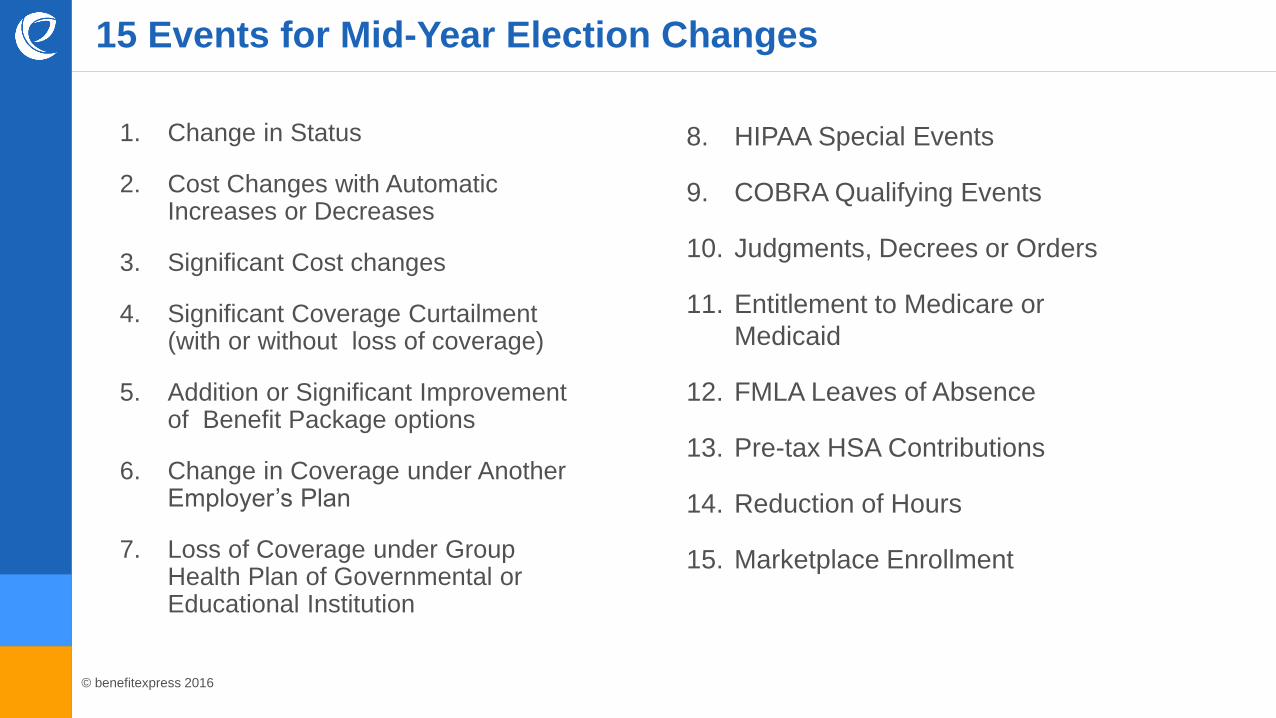

15 Events for Mid-Year Election Changes

1. Change in Status

2. Cost Changes with Automatic Increases or Decreases

3. Significant Cost changes

4. Significant Coverage Curtailment (with or without loss of coverage)

5. Addition or Significant Improvement of Benefit Package options

6. Change in Coverage under Another Employer’s Plan

7. Loss of Coverage under Group Health Plan of Governmental or Educational Institution

8. HIPAA Special Events

9. COBRA Qualifying Events

10. Judgments, Decrees or Orders

11. Entitlement to Medicare or

Medicaid

12. FMLA Leaves of Absence

13. Pre-tax HSA Contributions

14. Reduction of Hours

15. Marketplace Enrollment

© benefitexpress 2016

1 | Change in Status

These changes include:

• Change in employee’s marital status,

• Change in the number of dependents,

• Change in employment status,

• Dependents satisfying or ceasing to satisfy dependent eligibility requirements,

• Change in residence, and

• Commencement or termination of adoption proceedings.

Note: The plan document must include a provision for each of the above events the employer

wishes to allow.

© benefitexpress 2016

1 | Change in Status

Change in marital status includes:

• Marriage,

• Divorce,

• Death of Spouse,

• Legal Separation, and

• Annulment.

© benefitexpress 2016

1 | Change in Status

Change in the number of dependents:

• Birth,

• Adoption,

• Placement for adoption, and

• Death.

Note: Dependent is defined as a dependent under the Code Section 105(b), except for

children for medical coverage

For Dependent Care Plans, a dependent means an individual eligible for the

dependent care tax credit defined in IRC §21(b)(1)

© benefitexpress 2016

1 | Change in Status

Change in Employment Status:

• Termination or commencement of employment,

• Strike or lockout,

• Commencement or return from unpaid leave of absence.,

• A change in work site, and

• Change in employment status causing a change in eligibility under the plan (example – if the

plan covers only salaried employees and the employee becomes hourly.,

Note: Any of the above events that change the employment status of an employee, the

employee’s spouse or the employee’s dependents would qualify as a change in status.

© benefitexpress 2016

1 | Change in Status

Dependents satisfying or ceasing to satisfying dependent eligibility:

• Status event is one that causes a dependent to satisfy or cease to satisfy the requirements

for coverage due to attainment of a certain age, gain or loss of student status, marriage, or

any similar circumstances.

• Under the applicable consistency rule, if a dependent becomes ineligible for health

coverage due to attaining a certain age, marrying, or losing student status, then the

employee may change his or her election to drop the dependent.

• Or vice versa: An employee may add coverage for a dependent who becomes eligible upon

beginning school.

© benefitexpress 2016

1 | Change in Status

Change In Residence:

• Change in the place of residence of an employee, spouse or dependent.

• Change of residence would have to change the eligibility for health coverage.

• Coverage may be dropped where the change affects eligibility for a managed care option

(even if the employee could elect similar coverage).

© benefitexpress 2016

1 | Change in Status

Commencement or Termination of Adoption Proceedings:

• Commencement or termination of adoption proceedings also allows an election change

under an adoption assistance.

© benefitexpress 2016

1 | Change in Status

Consistency Requirement:

• If a change in status event occurs, a plan can only permit employees to make election

changes that are consistent with the event.

• There is one “general consistency rule” and 4 special consistency rules

Special Consistency Rule for Group Term Life, Disability and Dismemberment Coverage.

Special Consistency Rule for Dependent Care and Adoption Expenses.

Special Consistency Rule for Loss of Spouse’s or Dependent’s Eligibility.

Special Consistency Rule for Gain of Eligibility under another Employer’s Plan.

© benefitexpress 2016

1 | Change in Status

Special Consistency Rule for Group Term Life, Disability and Dismemberment

Coverage

• A participant may increase or decrease group term life, disability and dismemberment

coverage for any change in status event, even through eligibility under the plan is not gained

or lost.

• The occurrence of the event is enough.

• Check the insurance contract to determine wither the event is allowed.

Consistency Requirement | Special Consistency Rules

© benefitexpress 2016

1 | Change in Status

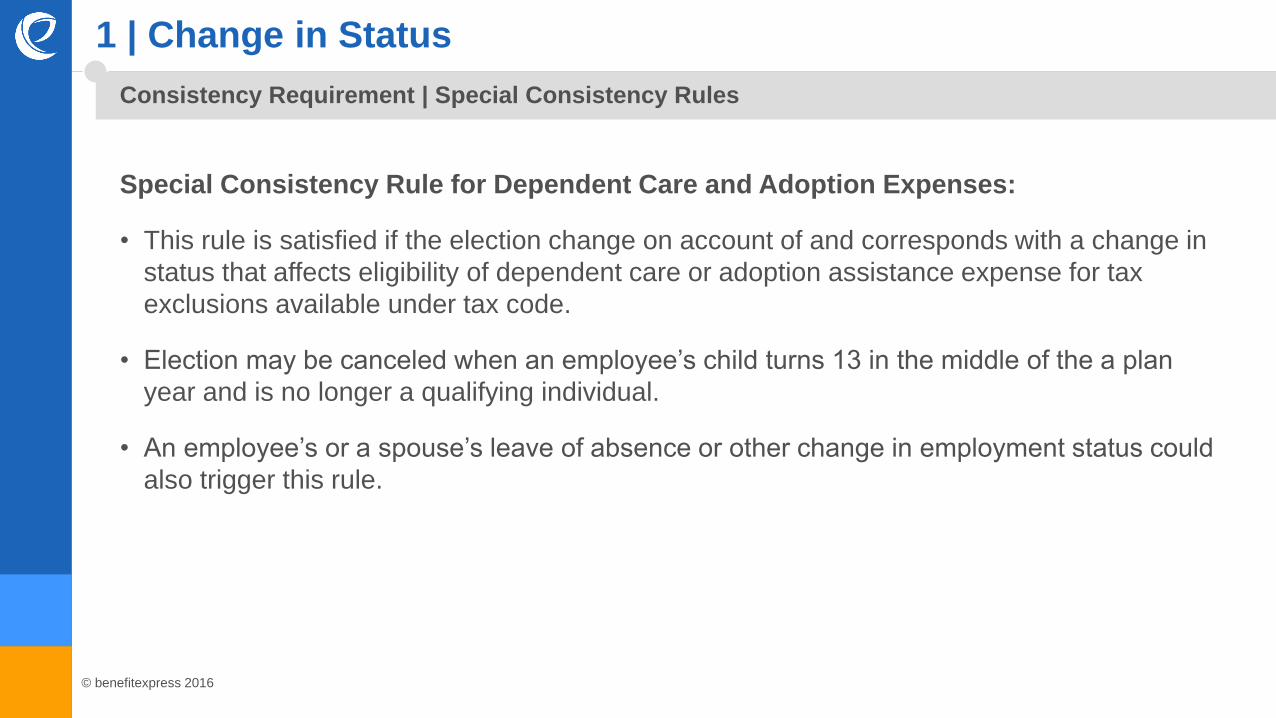

Special Consistency Rule for Dependent Care and Adoption Expenses:

• This rule is satisfied if the election change on account of and corresponds with a change in

status that affects eligibility of dependent care or adoption assistance expense for tax

exclusions available under tax code.

• Election may be canceled when an employee’s child turns 13 in the middle of the a plan

year and is no longer a qualifying individual.

• An employee’s or a spouse’s leave of absence or other change in employment status could

also trigger this rule.

Consistency Requirement | Special Consistency Rules

© benefitexpress 2016

1 | Change in Status

Special Consistency Rule for Loss of Spouse’s or Dependent’s Eligibility:

• An employee can cancel accident or health coverage for only the spouse or dependent.

• An election to cancel coverage for anyone else fails to correspond with that change in

status.

• May create a hardship under plans that offer limited coverage categories.

Consistency Requirement | Special Consistency Rules

© benefitexpress 2016

1 | Change in Status

Special Consistency Rule for Gain of Eligibility under another Employer’s Plan:

• If coverage is gained as a result of a change in martial or employment status, then an

employees election to cease or decrease coverage for that individual corresponds with the

change in status if coverage for that individual becomes effect or is increased under the

other employer’s plan.

Consistency Requirement | Special Consistency Rules

© benefitexpress 2016

1 | Change in Status

General Consistency Rule

• If one of the 4 special rules do not apply then the general consistency rule applies.

• Under this rule, an election change satisfies the consistency requirement “if the election

change is on account of and corresponds with a change in status that affects eligibility for

coverage under the employer’s plan.”

• The rule includes 2 elements:

The change in status event must affect eligibility for coverage under the employer’s plan, and

The election change must be on account of and correspond with the event.

Consistency Requirement

© benefitexpress 2016

1 | Change in Status

General Consistency Rule

• The change in status event must affect eligibility for coverage under the employer’s plan.

Gain or loss of coverage eligibility under the component benefit plan or the cafeteria plan will satisfy the consistency requirement.

A change in status that affects eligibility includes the increase or decrease of the number of an employee’s family member or dependents who benefit from coverage under the plan.

• The election change must be on account of and correspond with the event.

If one type of coverage is lost or gained, then the employee is limited to changing an election with respect to that coverage.

Other eligible individuals can also be added when a spouse or dependent gains eligibility as a change in status event

If an employee was no previous enrolled and a change in status occurs this rule will also allow the employee to enroll in order to enroll the dependents.

Consistency Requirement

© benefitexpress 2016

2 | Automatic Increases/Decreases in Elective Contributions as a Result of Cost Changes

• Prospective changes in employee payments corresponding to a change in the cost of a

qualified benefit may be automatically.

• Applies to all qualified benefits except Health Care FSAs.

• The plan document must contain provisions allowing such changes.

• If the cost difference is not significant, the payment election change is automatic otherwise,

the participants may be able to make an election change.

© benefitexpress 2016

3 | Significant Cost Changes

• If the cost of a benefits option under a cafeteria plan significantly increases or decreases, a

plan may permit a mid-year election changes.

• If costs significantly increase, participants may change to less costly option providing similar

coverage or drop coverage, but can drop coverage only if no similar plan exists.

• If costs significantly decrease, participants may commence participation in that plan option

even if they had not previously enrolled in any coverage.

• These rules apply to all qualified benefits except Health Care FSAs.

© benefitexpress 2016

4 | Significant Curtailment of Coverage

• The election can be revoked if no other benefit option providing similar coverage is offered.

• If similar coverage is available, it can be elected but coverage can not be dropped.

• Applies to all qualified benefits except Health Care FSAs.

• The plan document must contain provisions allowing an election change as a result of

“significant curtailment of coverage.”

© benefitexpress 2016

4 | Significant Curtailment of Coverage

Definition of “Significant Curtailment of Coverage”

• There must be a overall reduction in coverage provided under the plan as to constitute

reduced coverage generally.

• Events that constitute significant curtailment include a significant:

increase in deductibles,

increase in co-payments, and

increase in the out-of-pocket cost- sharing amounts under the plan.

© benefitexpress 2016

4 | Significant Curtailment of Coverage

Definition of “Loss of Coverage”

• The complete loss of coverage under a benefit option.

• A managed care plan ceasing to be available in the area where the participant resides.

• An individual losing all coverage as a result of an annual or lifetime maximum.

• A substantial decrease in the medical providers available under an option.

• A reduction in benefits for a specific type of medical condition for which treatment is being

received.

• Any other similar fundamental loss of coverage.

© benefitexpress 2016

4 | Significant Curtailment of Coverage

Definition of “Similar Coverage”

• Coverage for the same category of benefits (e.g., major medical to major medical).

• Coverage must be available to cover the same individuals (e.g., family to family or single to

single).

• A cafeteria plan may treat a spouse’s or dependent’s plan as similar coverage.

• Cost is not a factor in determining similar coverage.

© benefitexpress 2016

5 | Addition or Significant Improvement of Benefit Plan Option

• Participants can elect new or newly improved benefits on a prospective basis whether or not

they previously made an election under the cafeteria plan.

• Applies to all qualified benefits except Health Care FSAs.

• The plan document must contain provisions allowing such changes.

© benefitexpress 2016

6 | Change in Coverage of Spouse or Dependent Under Another Employer Plan

• Recognized when the other employer’s plan allows an election change consistent with the

regulations or when the other employer’s plan has a different period of coverage.

• A participant may make changes that correspond to changes under any other employer’s

plan – including coverage received through a domestic partner’s plan.

• The new election must be on account of and correspond with the change under the plan of

the spouse or dependent.

© benefitexpress 2016

6 | Change in Coverage of Spouse or Dependent Under Another Employer Plan

Four Types of Coverage Changes are Possible Under a Spouse or Dependent’s

Qualified Benefits Plan.

• Mandatory changes in coverage initiated by the insurer of the spouse’s plan.

• Mandatory changes in coverage initiated by the spouse’s employer.

• Optional coverage changes initiated by the spouse’s employer.

• Changes in coverage initiated by the participant’s spouse during an open enrollment.

Note: Corresponding changes to employee’s plan must be allowed by the plan document and

does not apply to Health Care FSAs.

© benefitexpress 2016

7 | Loss of Health Coverage Under Government or Educational Institution

If the plan so provides, mid-year election changes are permitted on account of coverage

losses under group health plans of certain governmental or educational institutions, including:

• A State’s children health insurance program under Title XXI of the Social Security Act

• A medical care program of an Indian Tribal government

• A State health benefits risk pool or

• A foreign government group health plan

Note: Applies to all qualified benefits except Health Care FSAs.

© benefitexpress 2016

8 | HIPAA Special Enrollments

• Plan may permit mid-year election changes that correspond to special enrollment rights

under HIPAA.

• Group health plans must allow special enrollment periods for certain individuals:

Individuals who did not enroll because they had coverage under another group health plan and

subsequently lose that coverage.

Employee acquires a new dependent (birth, adoption or placement for adoption), and

Individuals who lose or gain eligibility for Medicaid or CHIP,

• Plans do not have to allow pre-tax election changes, but must at least allow the changes on

an after-tax basis.

© benefitexpress 2016

9 | COBRA Qualifying Event

A cafeteria plan may permit an employee to make a mid-year election change if a COBRA

event occurs to the employee, spouse or dependent.

Employee may increase pre-tax salary reductions to cover the COBRA premiums.

Example:

• Employee has reduction of hours triggering a COBRA event.

• He can increase pre-tax salary reductions to cover cost of COBRA premiums.

© benefitexpress 2016

10 | Judgments, Decrees, Orders

A cafeteria plan may allow mid-year changes on account of judgment decrees and orders

resulting from divorce, legal separation, annulment, or change in legal custody .

Example:

• An employer receives a qualified medical child support order (QMCSO) requiring the

employee to cover a dependent child.

• The employee is allowed to change his election in order to cover the child.

© benefitexpress 2016

11 | Entitlement to Medicare or Medicaid

• A cafeteria plan may allow mid-year election changes on account of eligibility of the

employee, spouse or dependent for Medicare or Medicaid.

• Gaining Medicare or Medicaid allows participant to cancel or reduce health coverage.

• Losing Medicare or Medicaid allows participant to elect or increase coverage.

© benefitexpress 2016

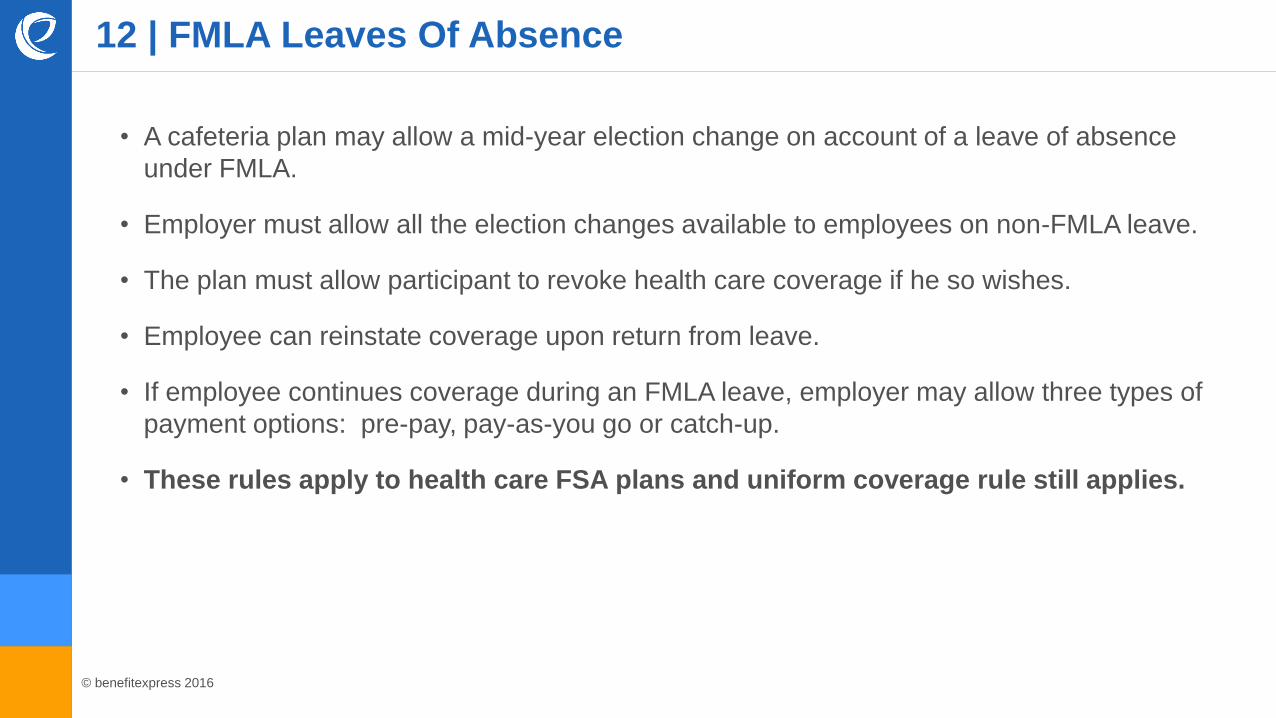

12 | FMLA Leaves Of Absence

• A cafeteria plan may allow a mid-year election change on account of a leave of absence

under FMLA.

• Employer must allow all the election changes available to employees on non-FMLA leave.

• The plan must allow participant to revoke health care coverage if he so wishes.

• Employee can reinstate coverage upon return from leave.

• If employee continues coverage during an FMLA leave, employer may allow three types of

payment options: pre-pay, pay-as-you go or catch-up.

• These rules apply to health care FSA plans and uniform coverage rule still applies.

© benefitexpress 2016

13 | Pre-tax HSA Contributions

• If pre-tax HSA contributions are offered, then prospective HSA election changes must be

allowed at least monthly—a time period that correlates with the HSA monthly eligibility

rules—and upon a loss of HSA eligibility.

• The employee may not change any of his or her other elections as a result of the HSA

election change unless otherwise permitted due to one of the other permitted election

change events previously described.

© benefitexpress 2016

14 | Reduction of Hours

• An employee hours are reduced to less than 30.

• Such reduction does not make employee ineligible for medical coverage employee.

• Employee can be allowed to drop coverage if employee intends to enroll in other minimum

essential coverage.

• Such election does not apply to Health Care FSA.

© benefitexpress 2016

15 | Marketplace Enrollment

• An employee who is eligible to enroll in Marketplace coverage (during an Marketplace

special or open enrollment period) may drop coverage midyear.

• Such election does not apply to Health care FSAs.

© benefitexpress 2016

Allowed Events for Mid-Year Election Changes for Health FSAs

1 | Change in status

9 | COBRA qualifying events

10 | Judgments, decrees or orders

11 | Entitlement to Medicare or Medicaid

12 | FMLA leaves of absence

© benefitexpress 2016

Other Events That Might Permit Mid-Year Elections

• Military leave under USERRA.

• Mistakes made by employee or employer.

• Participant Fails Medical Underwriting.

• Mid –year election changes may be required to pass non-discrimination testing.

• Automatic loss of coverage.

© benefitexpress 2016

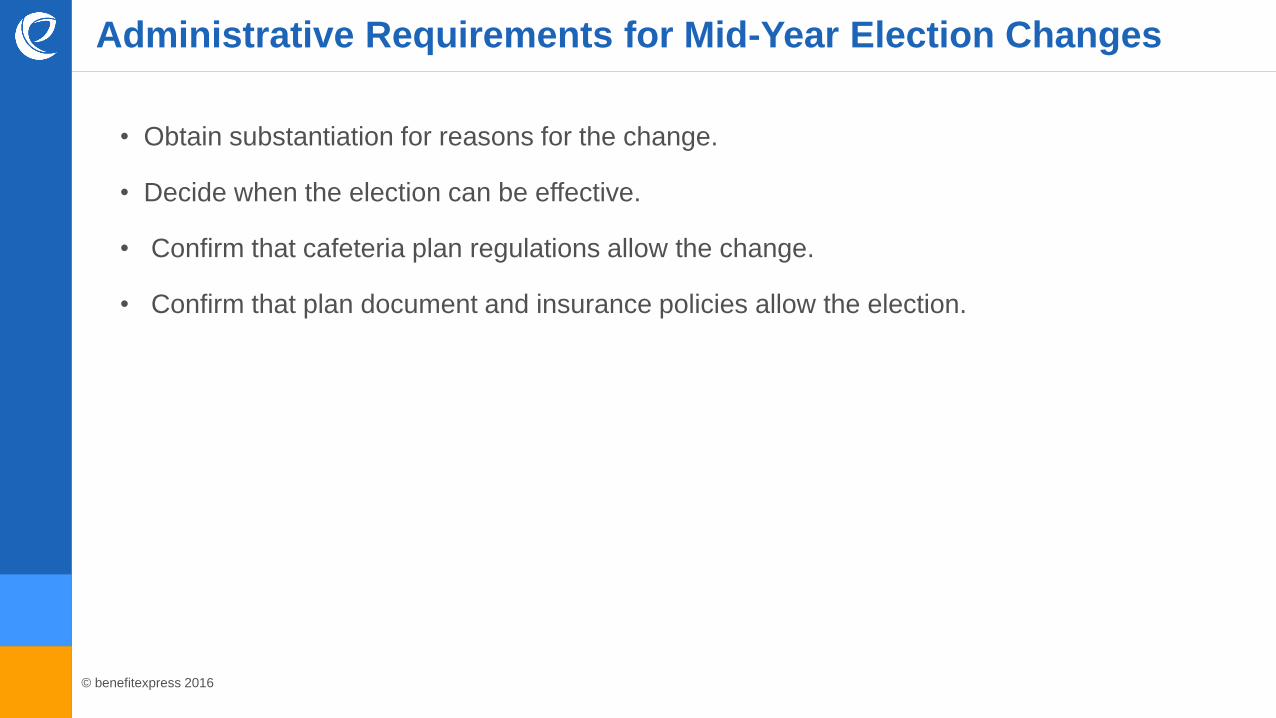

Administrative Requirements for Mid-Year Election Changes

• Obtain substantiation for reasons for the change.

• Decide when the election can be effective.

• Confirm that cafeteria plan regulations allow the change.

• Confirm that plan document and insurance policies allow the election.

© benefitexpress 2016

Terms of the Insurance Contract

• Remember that just because the cafeteria plan rules may allow midyear election changes, it

does not necessarily follow that a change is permitted under the insurance policy or other

documents governing the underlying benefit.

• For example, an insurance policy might not allow the change at all or might allow it only if

certain conditions are met.

Questions?

© benefitexpress 2016

Contact

Larry Grudzien

Attorney at Law

708-717-9638

larrygrudzien.com