Embed Size (px)

Citation preview

Wealth Builders Network Team

Profit8.ca

Welcome to

HOME OF COMMON SENSE INVESTING

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved. 11

A Syndicated Mortgage allows several smaller investors to combine their

resources to fund large-scale real estate development projects via a mortgage

instrument.

WHAT IS A SYNDICATED MORTGAGE?

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved. 12

A Syndicated Mortgage is an investment where there is a contractual

agreement between you the LENDER and the BORROWER (DEVELOPER). It

has a DEFINED TERM with a FIXED interest rate and a charge against the

property.

• Your mortgage investment has a

charge against the land and

building.

Every investor has their full face

amount registered in their favour at

the Land Title Office with a direct

charge against the property as

collateral.

• Syndicated Mortgages will be

subordinated to construction

financing which will be provided by a

bank.

WHAT IS A SYNDICATED MORTGAGE?

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved. 13

A Syndicated Mortgage allows you to use your registered funds to invest and

mitigate risk by including an asset backed by real estate.

Stocks Bonds Cash Real Estate

WHAT IS A SYNDICATED MORTGAGE?

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

LTV 70% to 80%

HOW TO INVEST L IKE THE BANK

50%

100%

Construction

Loan(Hard Cost)

Investments(Soft Cost)

25%

25%Equity

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

IS THIS A NEW CONCEPT?

• Syndicated Mortgages have been around for decades, but

have typically been reserved for wealthy investors.

• Syndicated Mortgages have been responsible for financing

large scale developments in all major cities across this great

country.

• It is only within the past few years that Syndicated Mortgages

have become available to the larger public, and as a result,

Canadians are transferring Millions of dollars from

underperforming RRSPs into this superior investment vehicle on

a monthly basis.

• DON’T LET YOUR SELF GET LEFT BEHIND !

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved. 5

TIER1 Advisory’s Syndicated Mortgage product gives you a unique

opportunity to invest in institutional grade, high-profile, large-scale real estate

development projects not usually accessible to individual retail investors.

We ensure the structure of the Syndicated Mortgage

product gives transparency to investors.

We take measures to

alleviate risk by

conducting due diligence

on selected projects, and

develop contingency plans

for exit and favour projects

that have attractive

investment parameters.

OUR ROLE

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

We ensure the transactions between parties are handled

professionally, efficiently and in a timely manner.

Investors Trust Company LawyersMortgage Brokers Developers

OUR ROLE

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved. 4

In their previous roles before TIER1 Advisory, our experienced

team members combined have managed Billions of dollars in

Real Estate assets and development projects. These

individuals have come together to form TIER1 Advisory. Our team

exercises a high degree of due diligence in screening the best

projects to invest in.

Management Team

CEO Raj Singh, B.Sc., MBA

Colman O’Brien B.Eng.

President

Developer

John Davies, B.Arch.

Advisor

Dennis Jewitt, CA

MOTIVATED & EXPERIENCED MANAGEMENT TEAM

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved. 12

Retirement residences

• Strong demand driven by aging population (Empty

nesters deleveraging & de-risking)

• Medium scale projects; 80 – 100 units in high demand

areas minimizing execution risk

Unique opportunities

• Select condominium projects with unique appeal &

characteristics that make them attractive

• Select commercial development opportunities with

high margins of safety

WHAT MAKE US DIFFERENT

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved. 18

TIER1 Advisory’s Syndicated Mortgage offers the following advantages:

• Your Principal - Your investment has a

charge against Canadian real estate. Your

Investment is registered at the Land Title

Office against the property as your

collateral.

• Fixed Returns – Your 8% annual interest

is paid quarterly, additional 4% for each

year of the contract paid upon completion

of project.

• Defined timeline - Investment terms are

typically 24 to 48 months.

• Diversification – You mitigate risk by

investing in multiple asset classes.

• Eligibility - A Syndicated Mortgage is

RRSP, RRIF, LIRA, TFSA, and RESP

eligible.

• Accessibility - allows you to invest in

projects typically reserved for large

financial institutions and the wealthy.

• Transparency - TIER1 Advisory offers

transparency on all Syndicated Mortgages

offered by the developers.

• Simplicity - The underlying investment, a

mortgage contract, is widely held and

understood by almost all investors.

Fundamentally Sound Principles of Investing

PRIMARY INVESTMENT BENEFITS

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

$-

$50,000.00

$100,000.00

$150,000.00

$200,000.00

$250,000.00

$300,000.00

0 Year 3 Year 6 Year 9 Year

INVESTMENTVALUE

$100,0

00

$1

36

,00

0

$1

84

,96

0

$2

51

,54

6* For illustration purposes

only using a 3yr term

mortgage product.

GROWTH OF YOUR INVESTMENT

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

COMPARISON

Mutual Funds / Seg Funds Syndicate Mortgage

Collateral Security

Fixed Interest rate

Quarterly Cash Flow

Fixed Investment Term

Low Volatility

100% Transparency

Easy to Understand

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

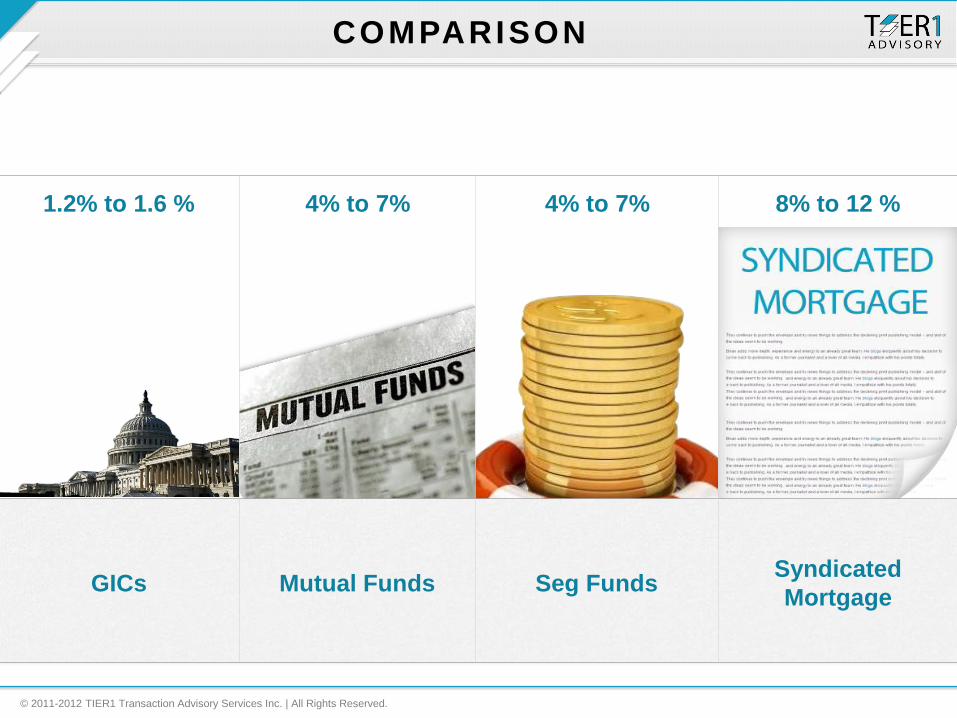

COMPARISON

GICs Mutual Funds Seg FundsSyndicated

Mortgage

1.2% to 1.6 % 4% to 7% 4% to 7% 8% to 12 %

© 2011-2012 Tier 1 Transaction Advisory Services Inc. | All Rights Reserved. 15

Dream Home80%

20%

100%

From Bank

From Family

HOW BANKS INVEST

© 2011-2012 Tier 1 Transaction Advisory Services Inc. | All Rights Reserved. 15

From Investor

YOU BECOME THE BANK

100%

From Bank

From Developer

LTV =70 to 80%

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved. 16

• The Bank places a Charge against the

property for the value of the mortgage.

• If the Mortgagor (borrower) defaults on

the mortgage, the Bank could foreclose

on the property or put it up for sale.

• If the Mortgagor sells the property, the

bank must be paid out at the time of

sale.

• As a TIER1 investor, you have the

same protections under the law.

HOW BANKS SECURE THEIR INVESTMENT

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

Should something go wrong……

Real-estate law dictates that mortgage holders gets

paid before shareholders and debts of the corporation.

Banks get paid first, immediately followed by tier1

investors, then everyone else, including the developer

4% Bonus is paid, before the developer earns a single

penny in profit.

Developer never gets direct access to the funds, funds

sit in lawyers trust account.?

Checks and Balances in place to protect your clients

principal

SAFETY OF YOUR INVESTMENT

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

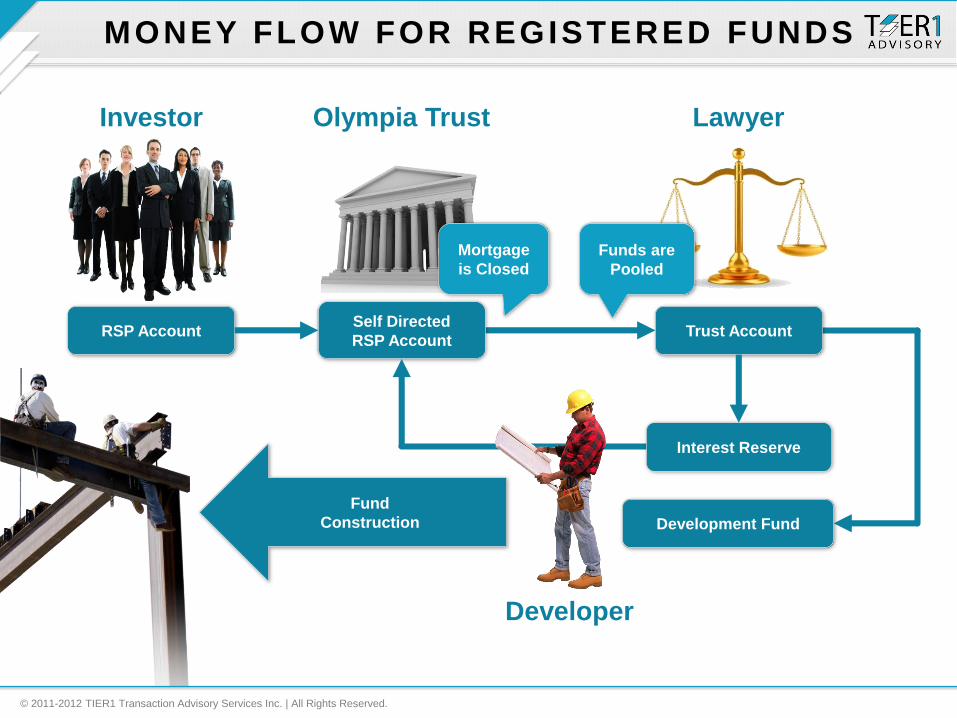

Fund

Construction

Investor Olympia Trust Lawyer

Developer

Self Directed

RSP AccountRSP Account

Development Fund

Interest Reserve

Trust Account

MONEY FLOW FOR REGISTERED FUNDS

Funds are

Pooled

Mortgage

is Closed

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

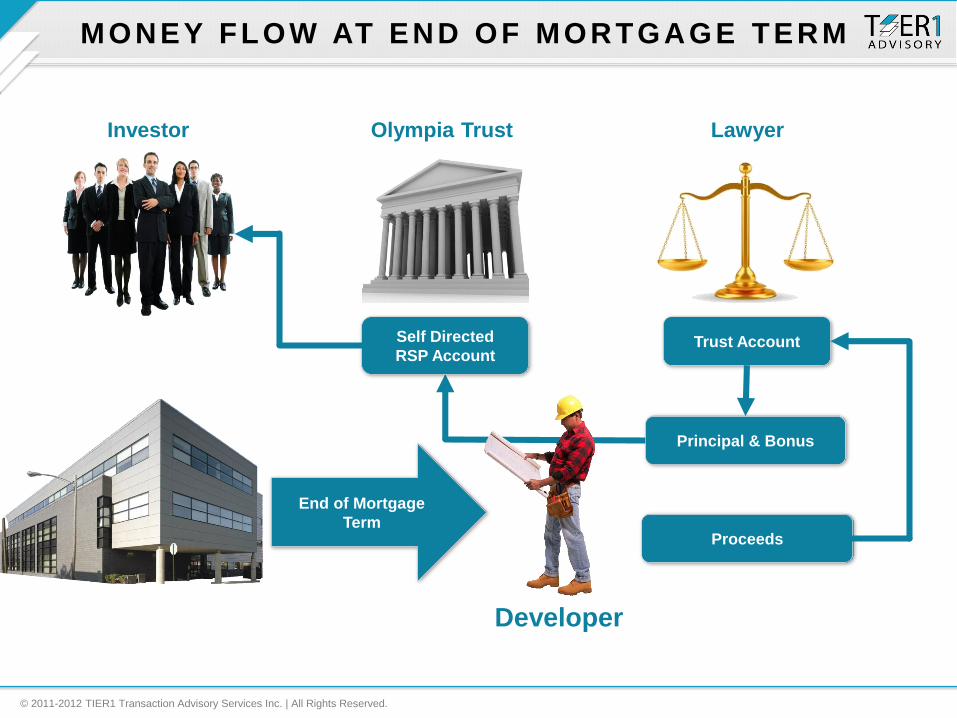

Trust Account

Proceeds

Principal & Bonus

Self Directed

RSP Account

MONEY FLOW AT END OF MORTGAGE TERM

Investor Olympia Trust Lawyer

Developer

End of Mortgage

Term

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

Land in the path of growth

Condos

Sub Divisions

Commercial Real-estate

Retirement Facilities

Long Term/Alzheimer Care Facilities

BANK

Land in the path of growth

Condos

Sub Divisions

Commercial Real-estate

Retirement Facilities

Long Term/Alzheimer Care Facilities

SYNDICATED MORTGAGES

WHERE CAN THE SYNDICATE INVEST

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved. 12

Q1) What is the minimum amount that can be invested?A1) $25,000 for cash or registered products, $20,000 for TFSA.

Q2) Are the returns guaranteed?A2) The returns are fixed based upon the Mortgage contract, in the same our mortgage

rate for our home is fixed.

FREQUENTLY ASKED QUESTIONS

Interest Schedule

3yr Term = 12 quarterly pay periods12 payments @ 2% = 24%; plus

End of term bonus payment @ 3 yrs x 4% / yr = 12%

Total = 36% = (12 x 2%) + (12%)

4yr Term = 16 quarterly pay periods16 payments @ 2% = 32%; plus

End of term bonus payment @ 4 yrs x 4% / yr = 16%

Total = 48% = (16 x 2%) + (16%)

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

FREQUENTLY ASKED QUESTIONS

Q3) Do Banks get involved in financing

these Real Estate projects?

A5) There are two levels of financing when

developing real estate - Soft costs and Hard

costs. Soft costs include items such as

architectural & engineering services, various

approvals & consents, inspection, equipment,

project management, insurance, and taxes.

Hard costs are all costs associated the

construction of the physical building.

TIER1 Advisory finances Soft Costs and some

hard costs, while Banks finance Hard Costs.

Q4) What will happen if the Developer goes

Bankrupt/Disappears?

A6) The property may be foreclosed under the

mortgage contract. Proceeds from the

foreclosure will be used to repay investors on a

pro rata basis. The experienced Developers that

TIER1 Advisory works with mitigate such risks.

However, if this situation occurs, the Developer

will likely lose his equity upon foreclosure

making him motivated to succeed.

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

FREQUENTLY ASKED QUESTIONS

Q5) Where is the 8% interest paid from?

A8) The Developer is required to set aside an

interest reserve at the start of the project. This

reserve allocates sufficient funds to pay the

interest due to all participants of the Syndicated

Mortgage.

Q6) What happens if the project is not

completed within the term of the mortgage

contract?

A9) The terms of the mortgage contract must be

adhered to otherwise the Developer will be in

breach of the contract. The Developer will be

open to any actions taken by the Bare Trustee

on behalf of investors within the Syndicated

Mortgage, including, but not restricted to

foreclosure. For example, Investors may vote to

extend the terms of the mortgage.

Q7) Can I get back my money before the end

of the mortgage term?

A3) No, your funds are being loaned as a

mortgage and will be used in the development

of the property. Therefore, the moneys are not

available to be redeemed until the contractual

end of the mortgage term.

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

FREQUENTLY ASKED QUESTIONS

Q8) Is the 4% Bonus guaranteed?

A10) The 4% is a contractual obligation that is

paid out to investors at the end of the mortgage

term. While this is not a guarantee, the

investors get their payment first, to the extent

that there is a profit, before the developers gets

any profit from the project.

Q9) In what position is the Syndicated

Mortgage?

A11) The Syndicated Mortgage is initially in first

position while the Developer is servicing the

land and marketing the project. Only when the

Developer reaches the construction phase of

the project will the Bank financing take first

position. The Syndicated Mortgage will then

move to, and remain in second position for the

remainder of the project.

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

RRSP PROCESS

• Complete Syndicate Mortgage

Application

• Sign off on all three Olympia Trust

forms:

a) Plan Application – required to open Self

Directed account

b) Transfer Authorization form

c) Web Access form

d) Provide copy of current account statements

from where funds are being transferred.

• Sign Mortgage Documents with

lawyer and mortgage broker.

• Interest will be paid directly into

your Olympia Trust Self Directed

account every quarterly, 90 days

from the date of closing.

• Closings take place approximately

every three weeks.

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

CASH PROCESS

• Complete Syndicate Mortgage

Application and provide a draft or

money order payable to law firm in

trust.

• Sign Mortgage Documents with

lawyer and mortgage broker.

• Upon closing, you will receive 4

cheques for the first years

interest. The first cheque

• will be dated 90 days from closing.

• Closings take place approximately

every two to three weeks.

© 2011-2012 TIER1 Transaction Advisory Services Inc. | All Rights Reserved.

Principal 100% Secured By Prime Real Estate

Define Term - 24 to 48 months

8% Fixed Rate Of Return, paid quarterly ( CASH FLOW)

4% end of term bonus

CASH, RRSP, RESP, LIRA, RIF, LIF, TFSA Eligible Investment

Become a private lender with your registered funds

Invest in projects typically reserved only for large financial institutions and the wealthy.

Face amount of your investment Is fully registered via a direct charge against the

property .

100% Transparency

Easy to understand

TIER1’S SYNDICATE MORTGAGE INVESTMENT OFFERS

THANK YOU