Embed Size (px)

Citation preview

2017

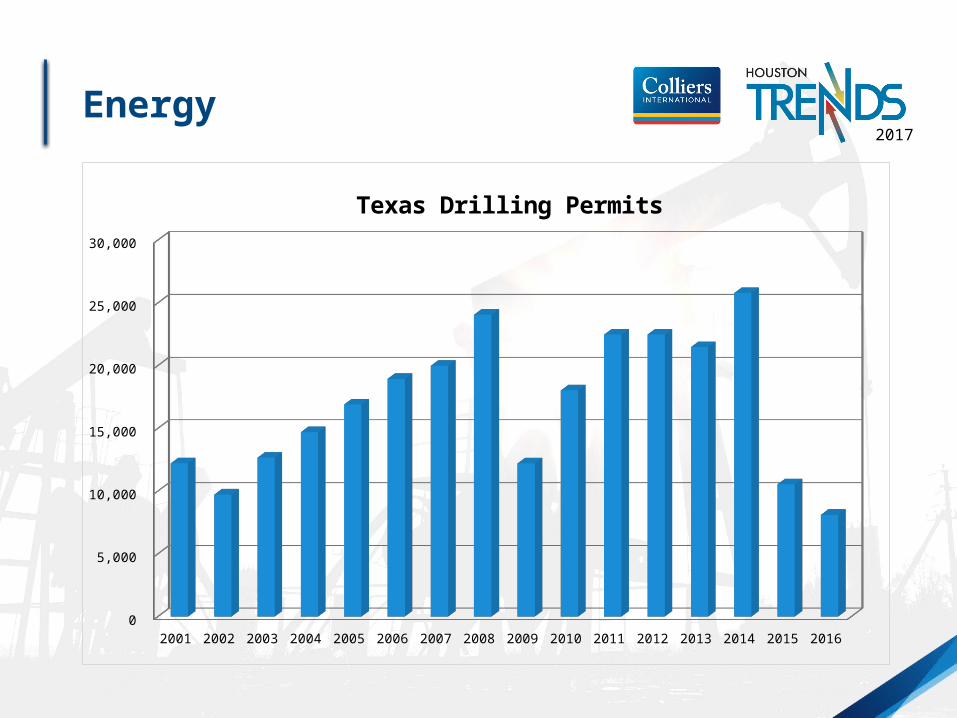

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 20160

5,000

10,000

15,000

20,000

25,000

30,000

Texas Drilling Permits

Energy

2017

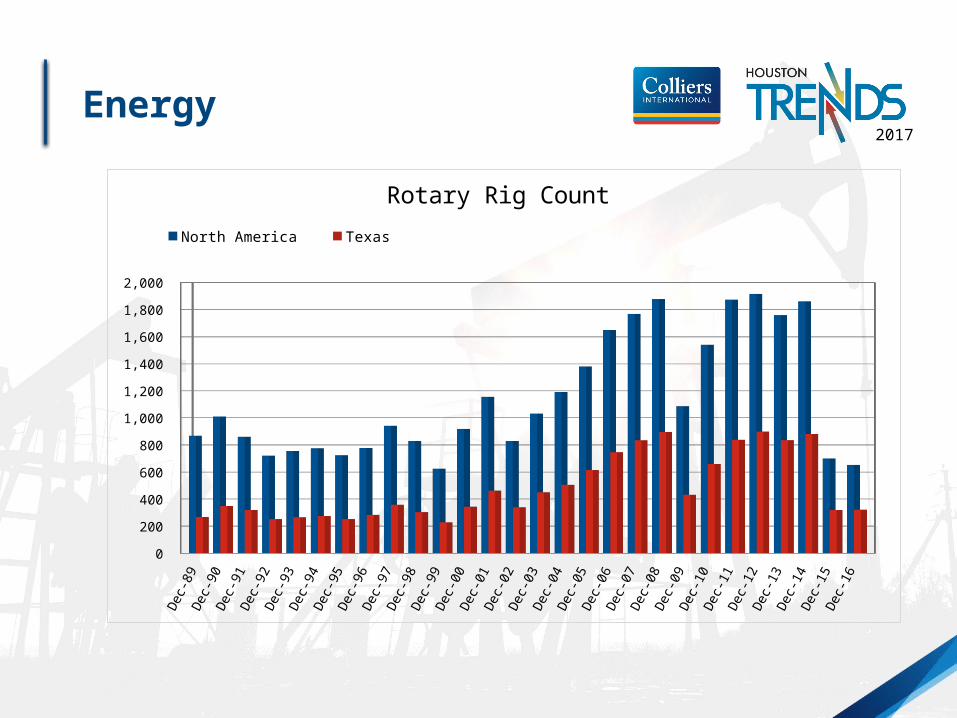

Dec-

89De

c-90

Dec-

91De

c-92

Dec-

93De

c-94

Dec-

95De

c-96

Dec-

97De

c-98

Dec-

99De

c-00

Dec-

01De

c-02

Dec-

03De

c-04

Dec-

05De

c-06

Dec-

07De

c-08

Dec-

09De

c-10

Dec-

11De

c-12

Dec-

13De

c-14

Dec-

15De

c-16

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Rotary Rig Count

North America Texas

Energy

2017

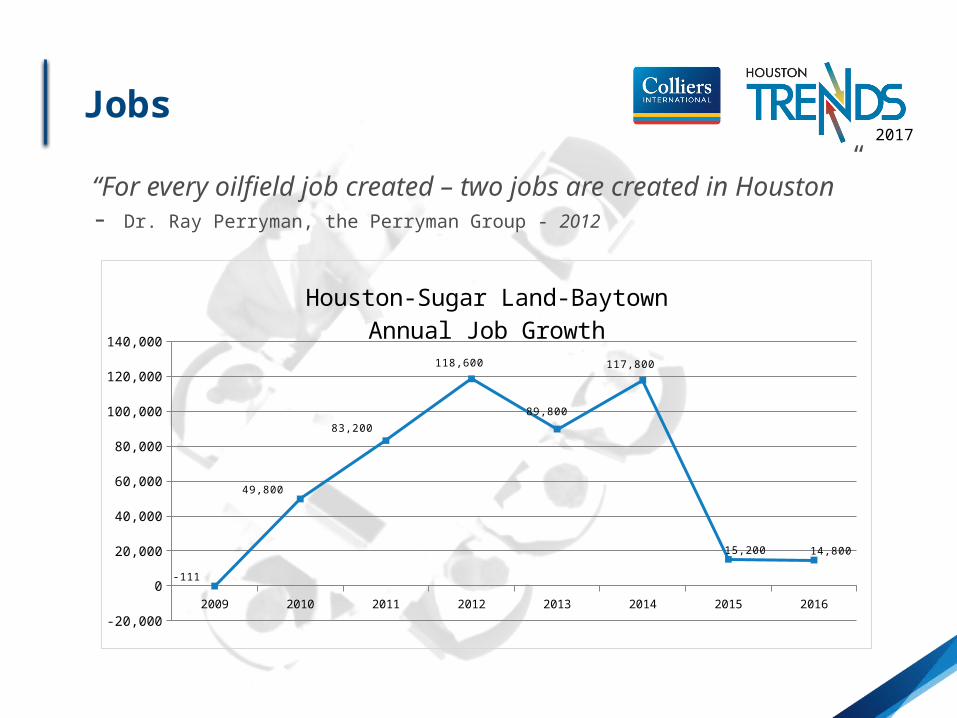

“For every oilfield job created – two jobs are created in Houston” - Dr. Ray Perryman, the Perryman Group - 2012

Jobs

2009 2010 2011 2012 2013 2014 2015 2016-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

-111

49,800

83,200

118,600

89,800

117,800

15,200 14,800

Houston-Sugar Land-BaytownAnnual Job Growth

2017

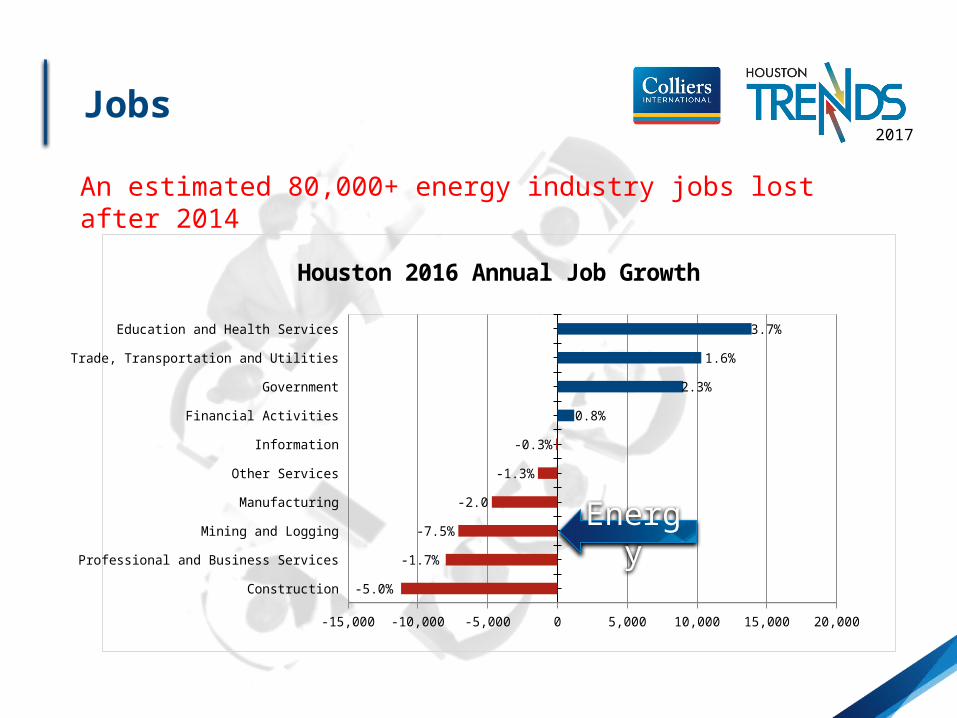

Construction

Professional and Business Services

Mining and Logging

Manufacturing

Other Services

Information

Financial Activities

Government

Trade, Transportation and Utilities

Education and Health Services

-15,000 -10,000 -5,000 0 5,000 10,000 15,000 20,000

-5.0%

-1.7%

-7.5%

-2.0

-1.3%

-0.3%

0.8%

2.3%

1.6%

3.7%

Houston 2016 Annual Job Growth

Energy

An estimated 80,000+ energy industry jobs lost after 2014

Jobs

2017

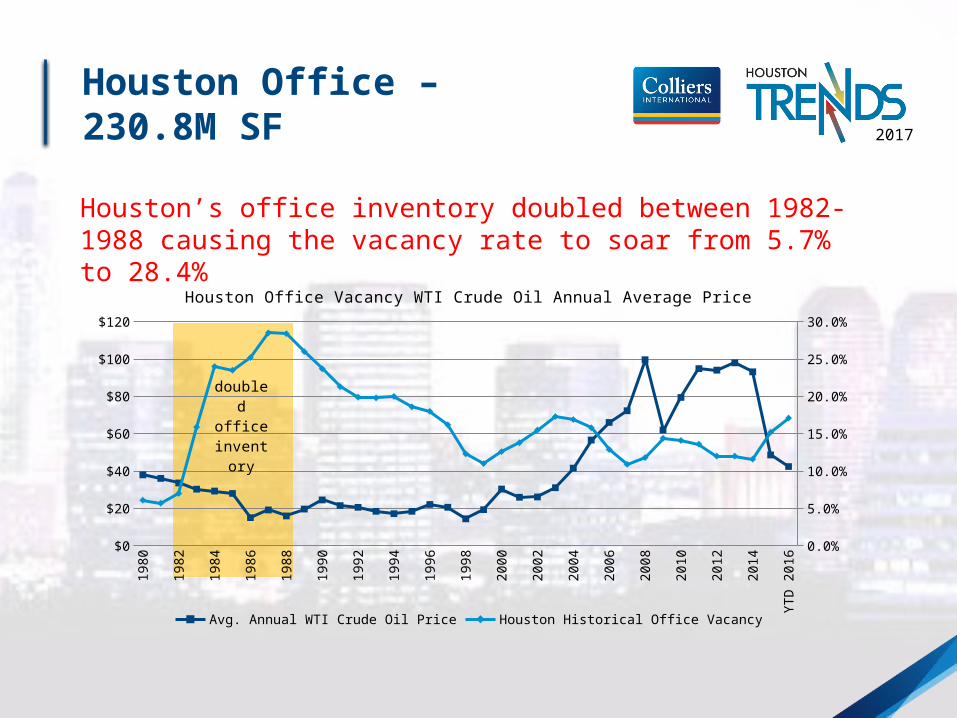

Houston Office – 230.8M SF

Houston’s office inventory doubled between 1982-1988 causing the vacancy rate to soar from 5.7% to 28.4%

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

YTD

2016

$0

$20

$40

$60

$80

$100

$120

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Houston Office Vacancy WTI Crude Oil Annual Average Price

Avg. Annual WTI Crude Oil Price Houston Historical Office Vacancy

doubled office in-ventory

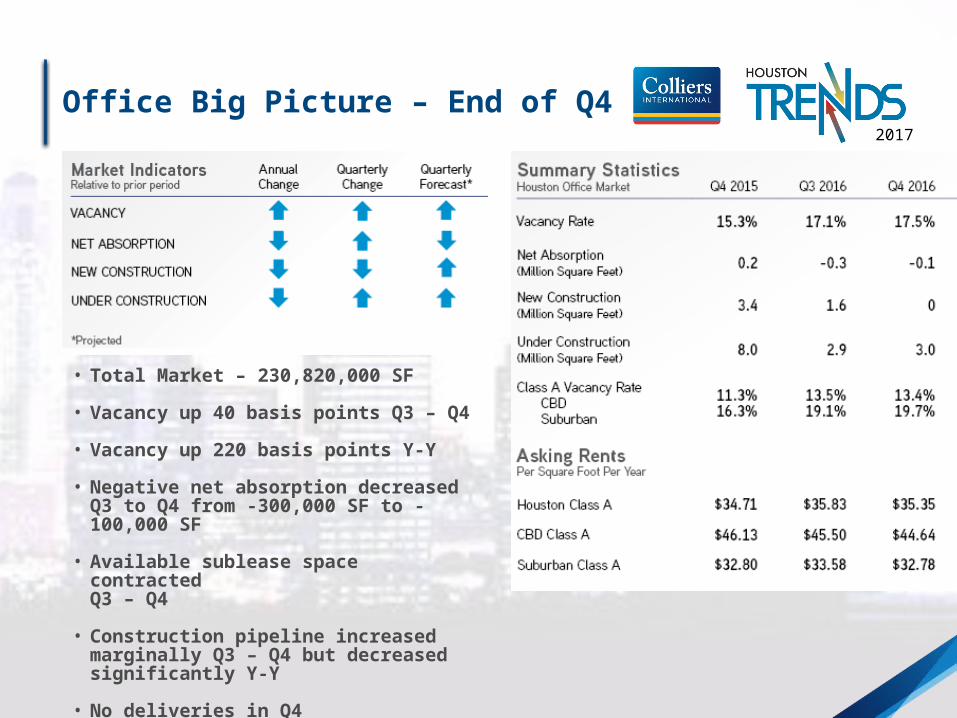

2017Office Big Picture – End of Q4

• Total Market – 230,820,000 SF• Vacancy up 40 basis points Q3 – Q4 • Vacancy up 220 basis points Y-Y• Negative net absorption decreased

Q3 to Q4 from -300,000 SF to -100,000 SF

• Available sublease space contracted

Q3 – Q4• Construction pipeline increased

marginally Q3 – Q4 but decreased significantly Y-Y

• No deliveries in Q4

2017

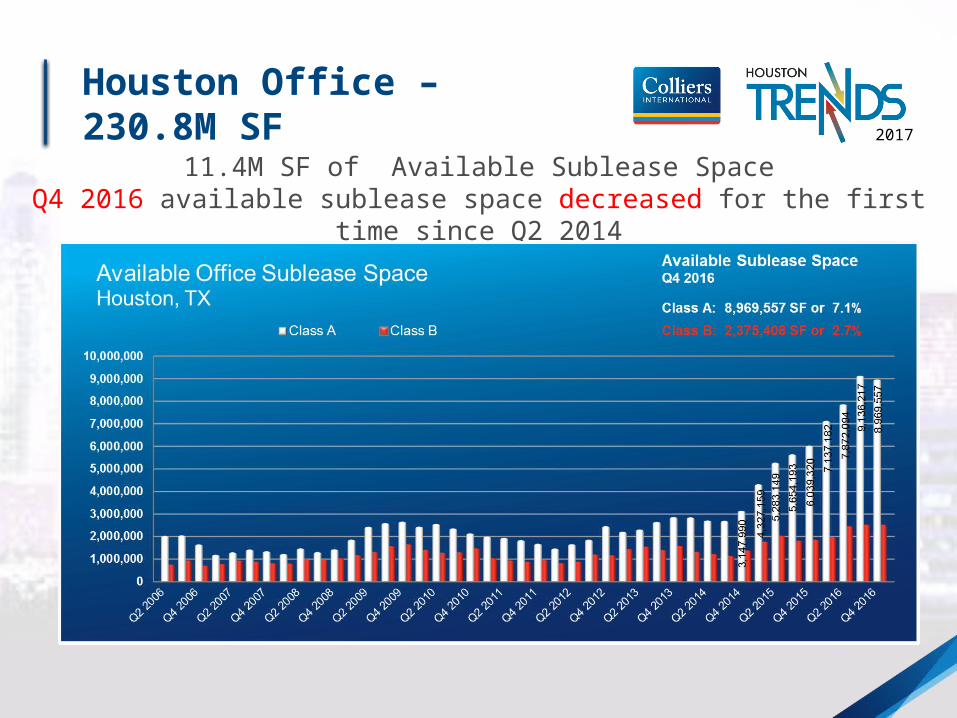

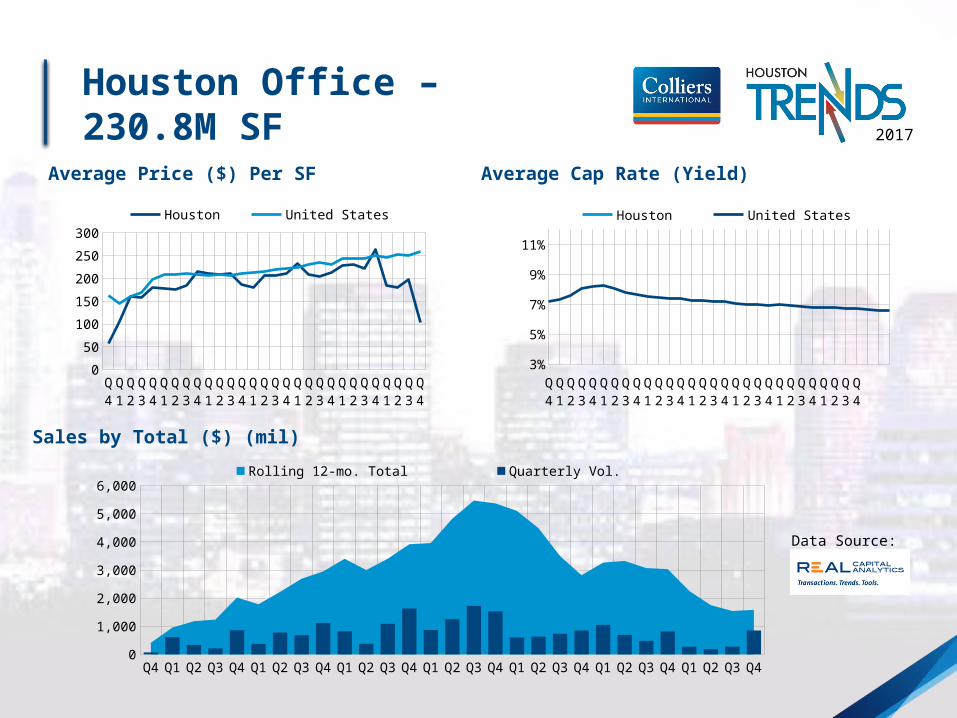

Houston Office – 230.8M SF

11.4M SF of Available Sublease SpaceQ4 2016 available sublease space decreased for the first time since Q2 2014

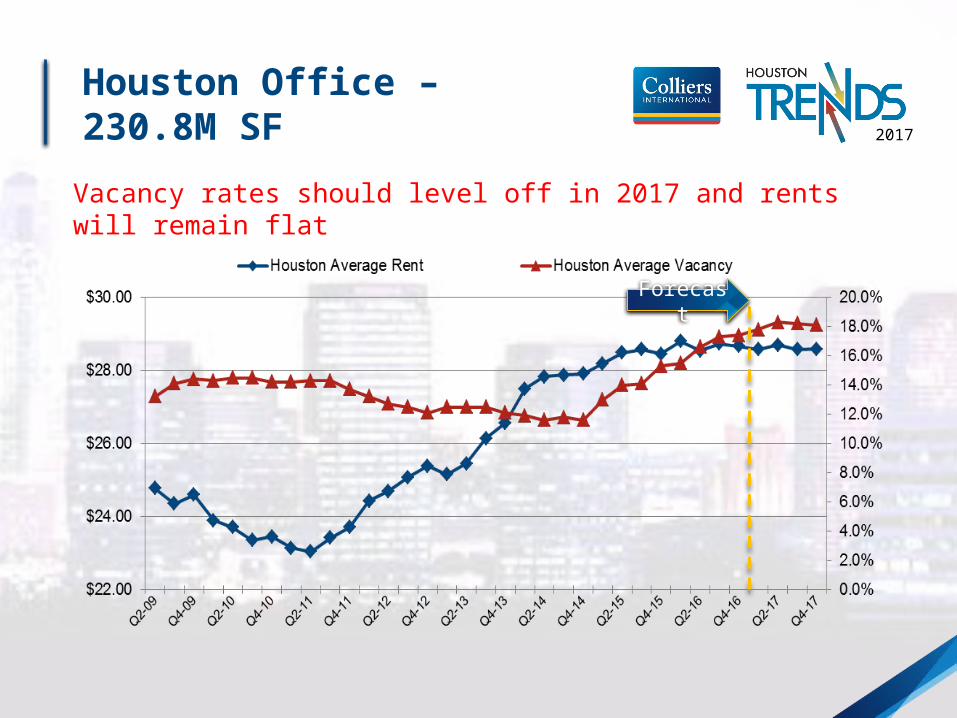

2017Houston Office – 230.8M SF

Forecast

Vacancy rates should level off in 2017 and rents will remain flat

Confidential – Colliers International 2016

2017

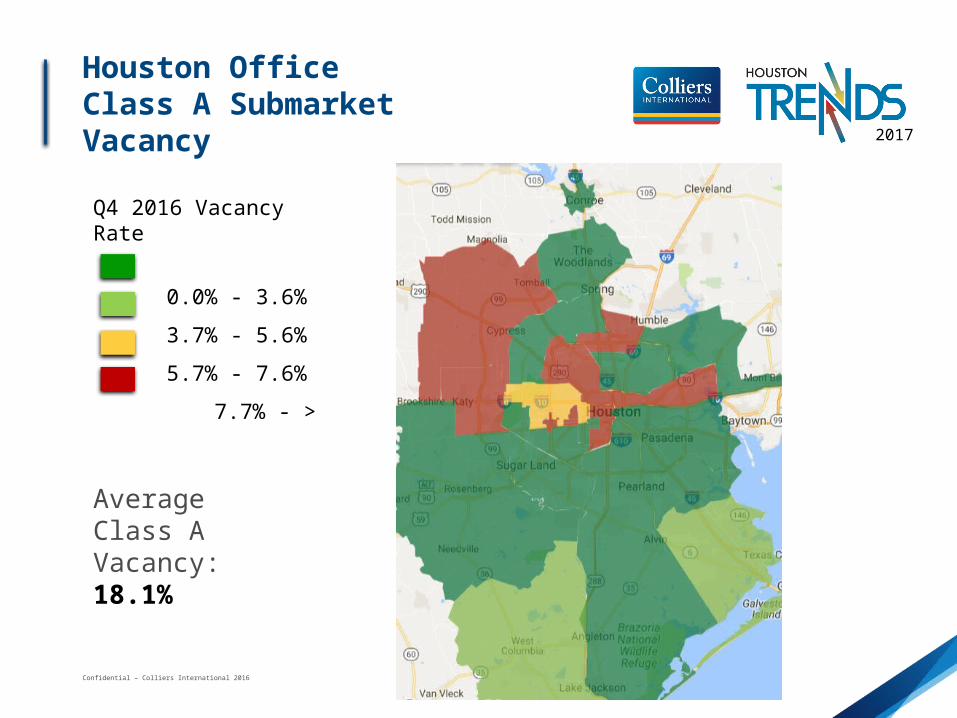

Average Class AVacancy: 18.1%

Houston OfficeClass A Submarket Vacancy

Q4 2016 Vacancy Rate

0.0% - 3.6%

3.7% - 5.6%

5.7% - 7.6%

7.7% - >

Confidential – Colliers International 2016

20172017

Average Cap Rate (Yield)Average Price ($) Per SF

Data Source:

Houston Office – 230.8M SF

Sales by Total ($) (mil)

Q4 '09

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Q2 '13

Q3 '13

Q4 '13

Q1 '14

Q2 '14

Q3 '14

Q4 '14

Q1 '15

Q2 '15

Q3 '15

Q4 '15

Q1 '16

Q2 '16

Q3 '16

Q4 '16

0

1,000

2,000

3,000

4,000

5,000

6,000Rolling 12-mo. Total Quarterly Vol.

Q4 '09

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Q2 '13

Q3 '13

Q4 '13

Q1 '14

Q2 '14

Q3 '14

Q4 '14

Q1 '15

Q2 '15

Q3 '15

Q4 '15

Q1 '16

Q2 '16

Q3 '16

Q4 '16

0

50

100

150

200

250

300Houston United States

Q4 '09

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Q2 '13

Q3 '13

Q4 '13

Q1 '14

Q2 '14

Q3 '14

Q4 '14

Q1 '15

Q2 '15

Q3 '15

Q4 '15

Q1 '16

Q2 '16

Q3 '16

Q4 '16

3%

5%

7%

9%

11%

Houston United States

Confidential – Colliers International 2016

20172017

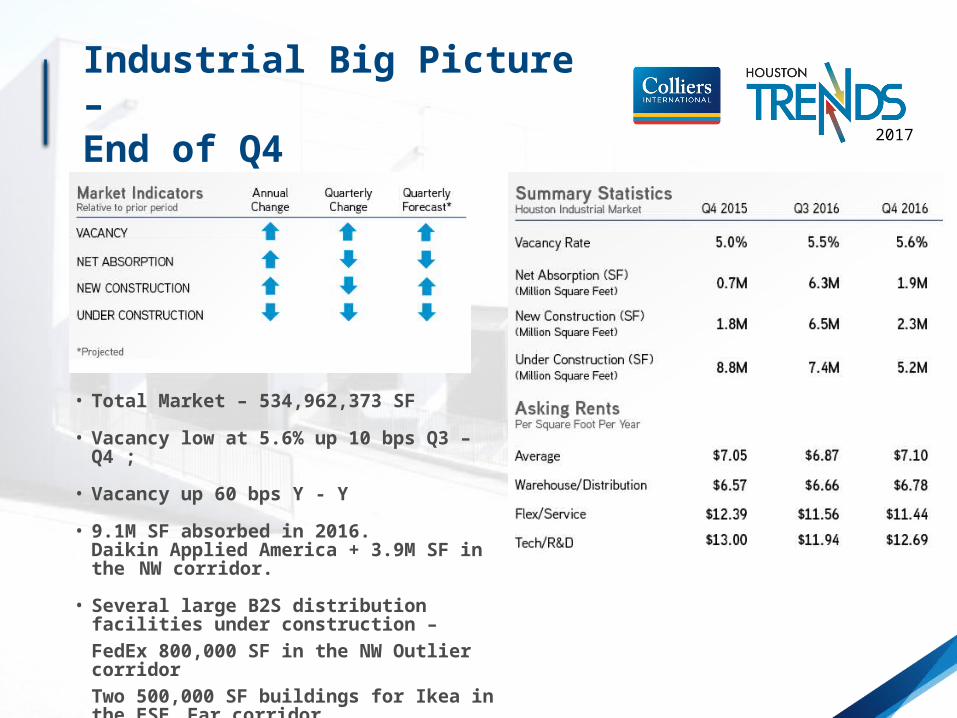

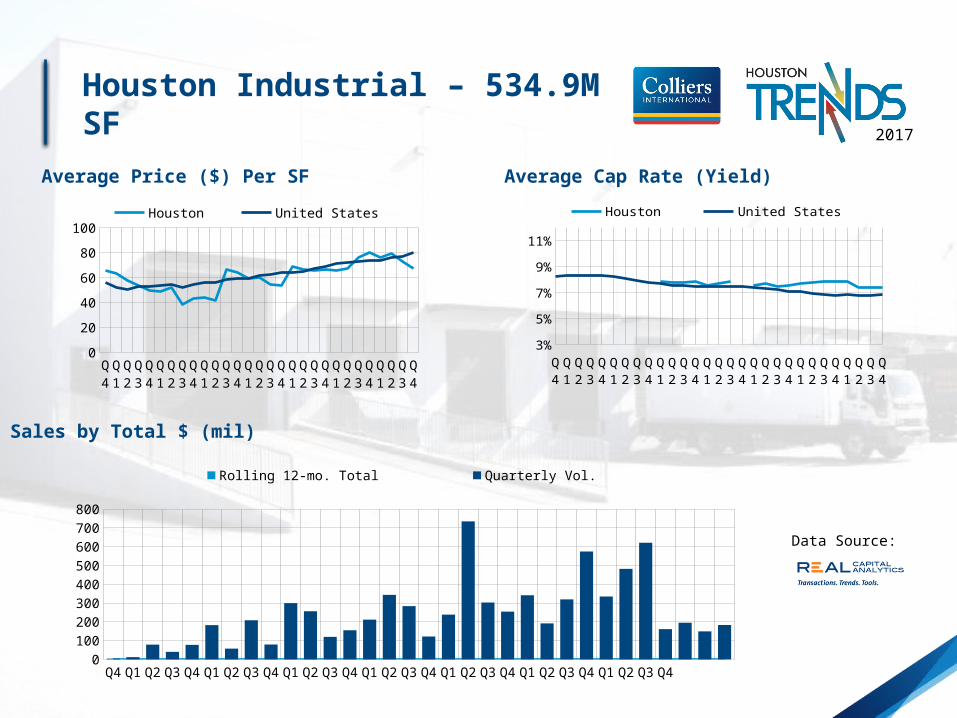

Industrial Big Picture – End of Q4

• Total Market – 534,962,373 SF• Vacancy low at 5.6% up 10 bps Q3 –

Q4 ; • Vacancy up 60 bps Y - Y• 9.1M SF absorbed in 2016.

Daikin Applied America + 3.9M SF in the NW corridor.

• Several large B2S distribution facilities under construction – FedEx 800,000 SF in the NW Outlier corridor

Two 500,000 SF buildings for Ikea in the ESE Far corridor.

Confidential – Colliers International 2016

20172017

Q2-09

Q4-09

Q2-10

Q4-10

Q2-11

Q4-11

Q2-12

Q4-12

Q2-13

Q4-13

Q2-14

Q4-14

Q2-15

Q4-15

Q2-16

Q4-16

Q2-17

Q4-17

$5.00

$5.50

$6.00

$6.50

$7.00

$7.50

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Houston Average Rent Houston Average Vacancy

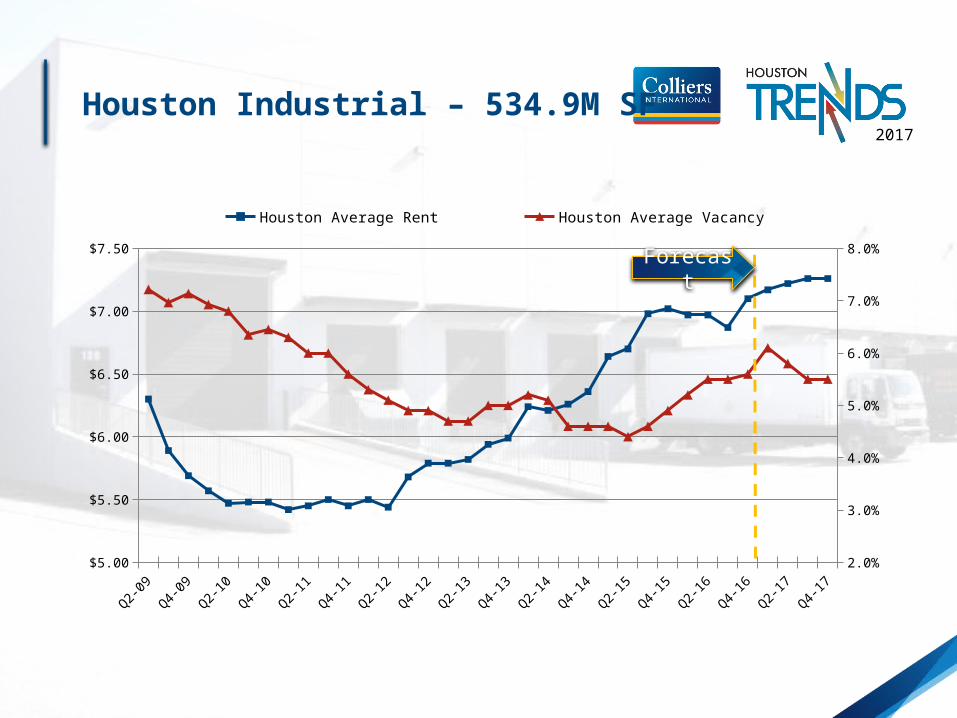

Houston Industrial – 534.9M SF

Forecast

Confidential – Colliers International 2016

2017

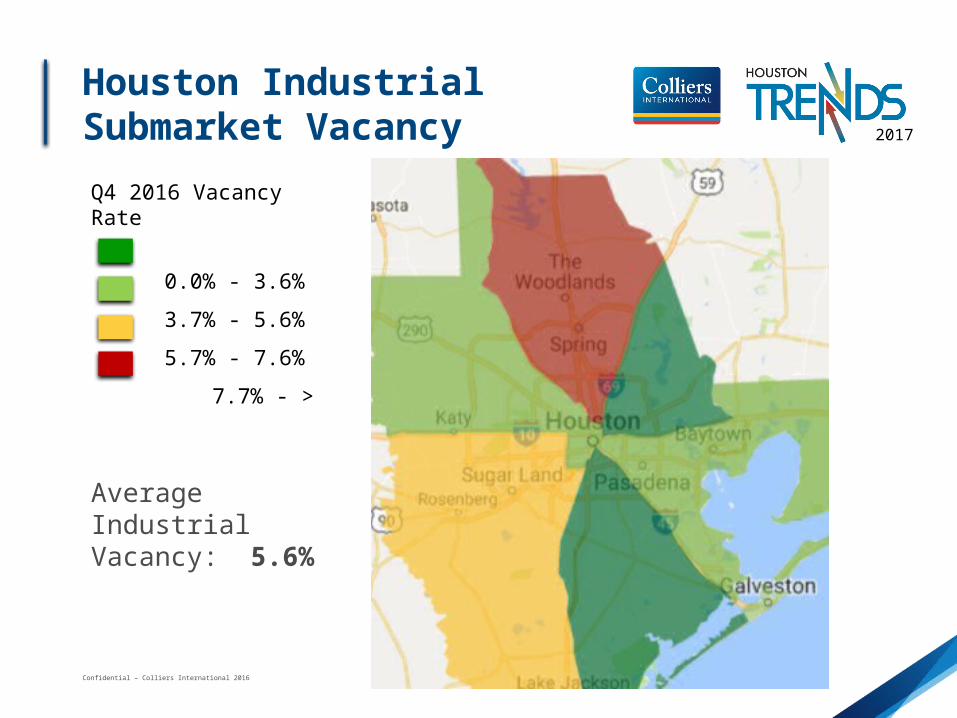

Average Industrial Vacancy: 5.6%

Houston IndustrialSubmarket VacancyQ4 2016 Vacancy Rate

0.0% - 3.6%

3.7% - 5.6%

5.7% - 7.6%

7.7% - >

Confidential – Colliers International 2016

20172017

Sales by Total $ (mil)

Data Source:

Average Cap Rate (Yield)Average Price ($) Per SF

Houston Industrial – 534.9M SF

Q4 '09

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Q2 '13

Q3 '13

Q4 '13

Q1 '14

Q2 '14

Q3 '14

Q4 '14

Q1 '15

Q2 '15

Q3 '15

Q4 '15

Q1 '16

Q2 '16

Q3 '16

Q4 '16

0100200300400500600700800

Rolling 12-mo. Total Quarterly Vol.

Q4 '09

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Q2 '13

Q3 '13

Q4 '13

Q1 '14

Q2 '14

Q3 '14

Q4 '14

Q1 '15

Q2 '15

Q3 '15

Q4 '15

Q1 '16

Q2 '16

Q3 '16

Q4 '16

0

20

40

60

80

100Houston United States

Q4 '09

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Q2 '13

Q3 '13

Q4 '13

Q1 '14

Q2 '14

Q3 '14

Q4 '14

Q1 '15

Q2 '15

Q3 '15

Q4 '15

Q1 '16

Q2 '16

Q3 '16

Q4 '16

3%

5%

7%

9%

11%

Houston United States

Confidential – Colliers International 2016

20172017

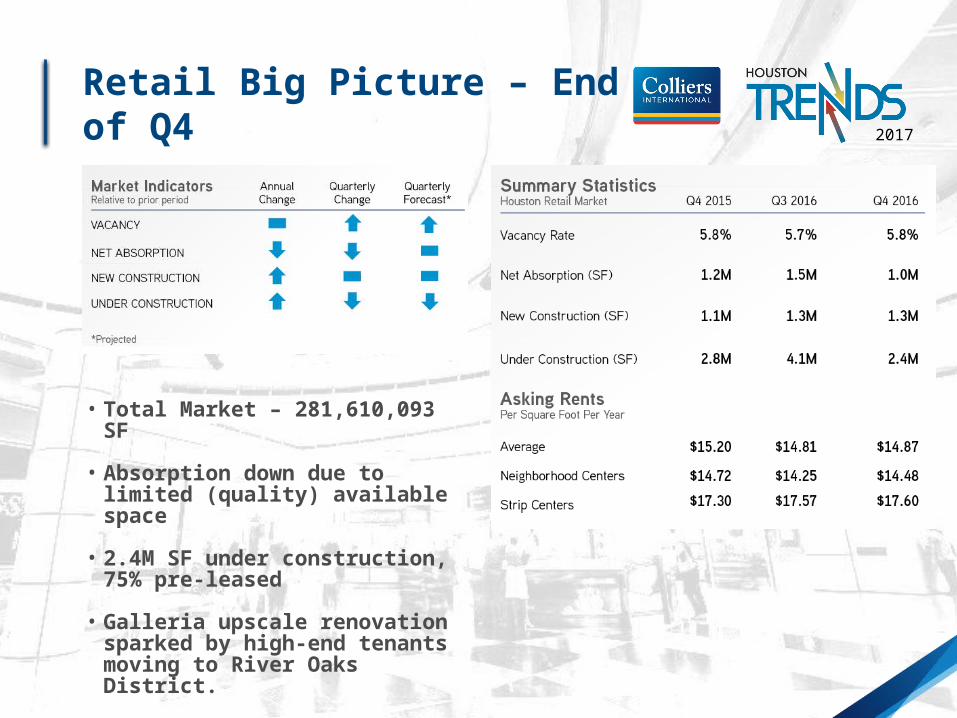

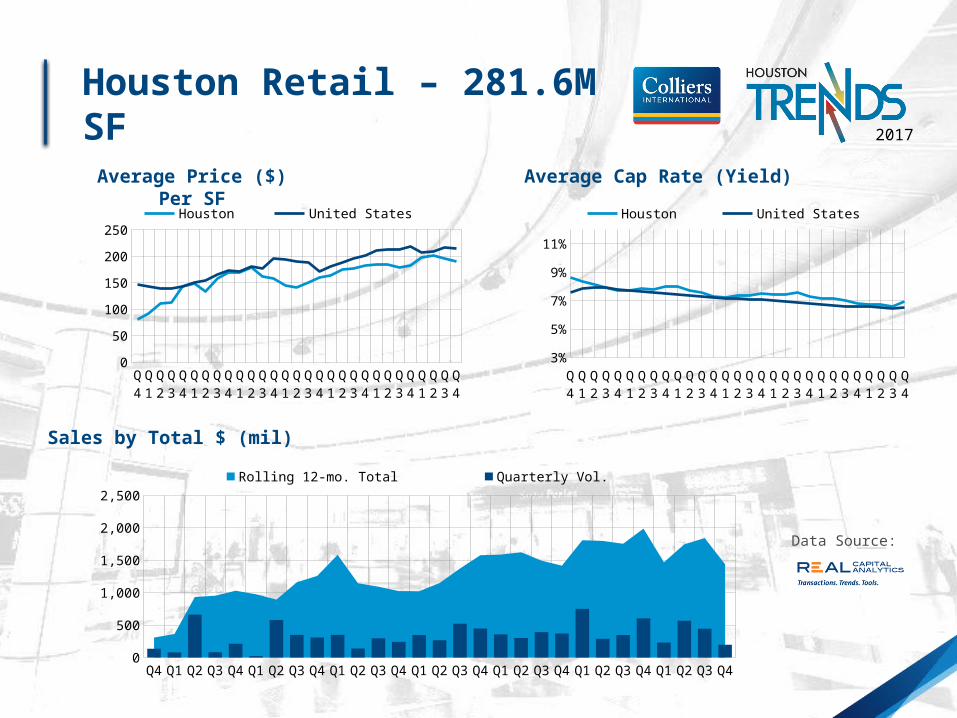

Retail Big Picture – End of Q4

• Total Market – 281,610,093 SF• Absorption down due to

limited (quality) available space

• 2.4M SF under construction, 75% pre-leased

• Galleria upscale renovation sparked by high-end tenants moving to River Oaks District.

Confidential – Colliers International 2016

20172017

Q1-09

Q3-09

Q1-10

Q3-10

Q1-11

Q3-11

Q1-12

Q3-12

Q1-13

Q3-13

Q1-14

Q3-14

Q1-15

Q3-15

Q1-16

Q3-16

Q1-17

Q3-17

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Houston Average Vacancy

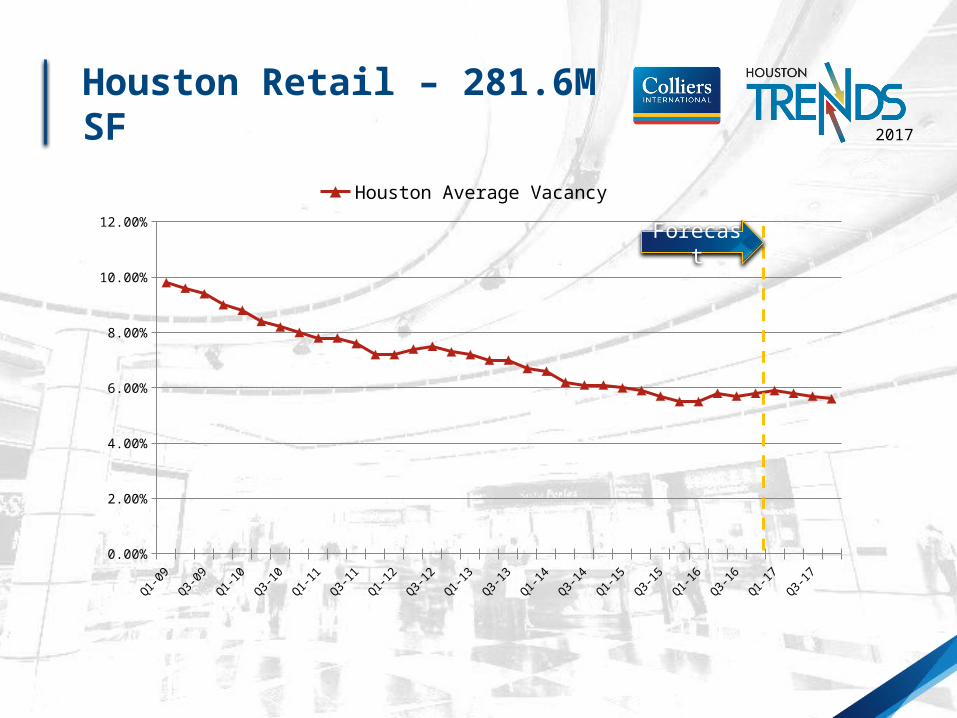

Houston Retail – 281.6M SF

Forecast

Confidential – Colliers International 2016

20172017

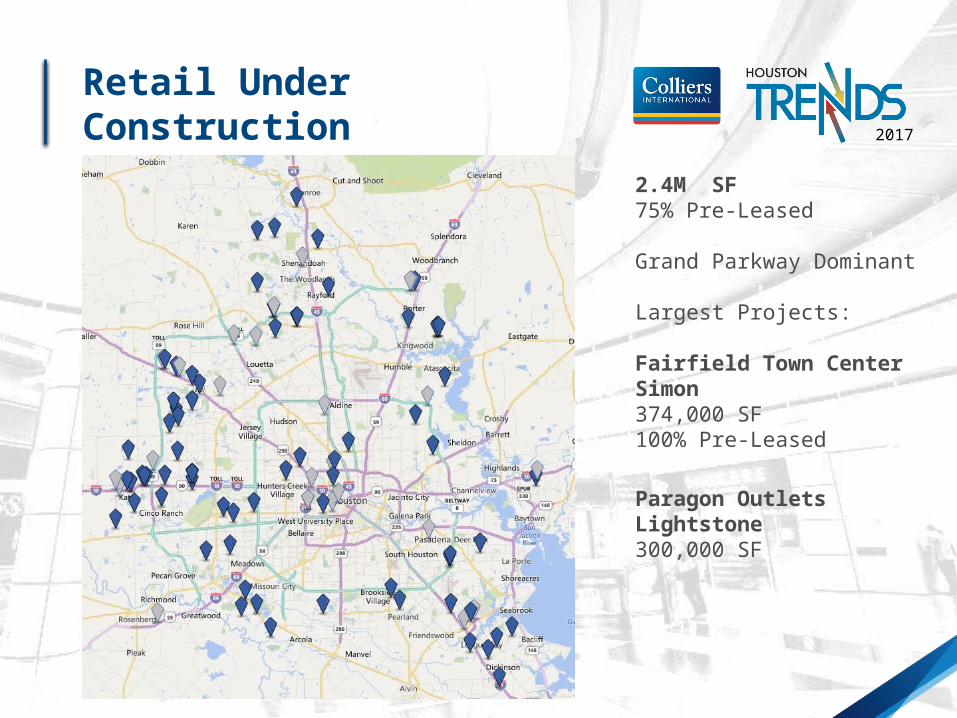

Retail Under Construction

2.4M SF 75% Pre-Leased

Grand Parkway Dominant

Largest Projects:

Fairfield Town CenterSimon374,000 SF100% Pre-Leased

Paragon OutletsLightstone300,000 SF

Confidential – Colliers International 2016

2017

Active Larger (Anchor) Tenants

Confidential – Colliers International 2016

20172017

Sales by Total $ (mil)

Average Cap Rate (Yield)Average Price ($) Per SF

Data Source:

Houston Retail – 281.6M SF

Q4 '09

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Q2 '13

Q3 '13

Q4 '13

Q1 '14

Q2 '14

Q3 '14

Q4 '14

Q1 '15

Q2 '15

Q3 '15

Q4 '15

Q1 '16

Q2 '16

Q3 '16

Q4 '16

0

500

1,000

1,500

2,000

2,500Rolling 12-mo. Total Quarterly Vol.

Q4 '09

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Q2 '13

Q3 '13

Q4 '13

Q1 '14

Q2 '14

Q3 '14

Q4 '14

Q1 '15

Q2 '15

Q3 '15

Q4 '15

Q1 '16

Q2 '16

Q3 '16

Q4 '16

0

50

100

150

200

250Houston United States

Q4 '09

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Q2 '13

Q3 '13

Q4 '13

Q1 '14

Q2 '14

Q3 '14

Q4 '14

Q1 '15

Q2 '15

Q3 '15

Q4 '15

Q1 '16

Q2 '16

Q3 '16

Q4 '16

3%

5%

7%

9%

11%

Houston United States

Confidential – Colliers International 2016

20172017

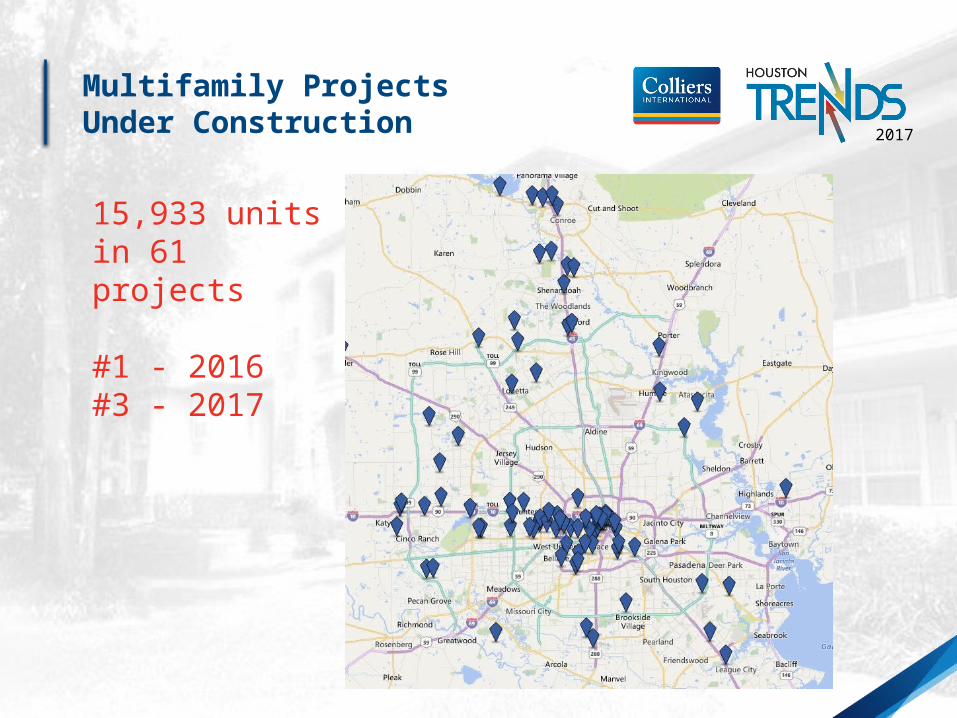

Multifamily Projects Under Construction

15,933 units in 61 projects

#1 - 2016#3 - 2017

Confidential – Colliers International 2016

20172017

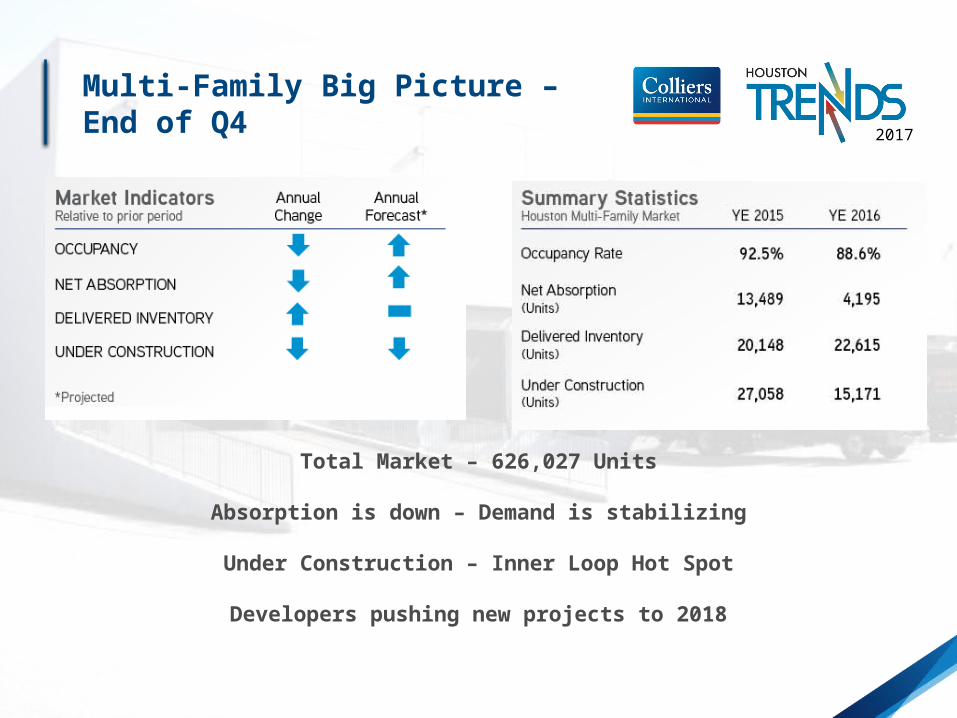

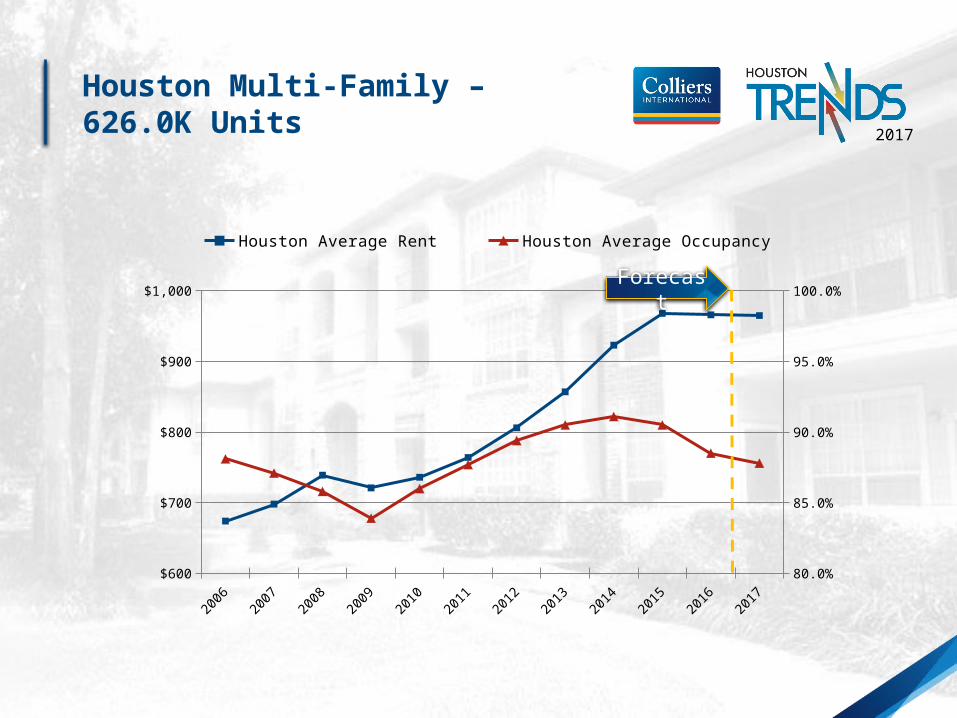

Multi-Family Big Picture – End of Q4

Total Market – 626,027 Units

Absorption is down – Demand is stabilizing

Under Construction – Inner Loop Hot Spot

Developers pushing new projects to 2018

Confidential – Colliers International 2016

20172017

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

$600

$700

$800

$900

$1,000

80.0%

85.0%

90.0%

95.0%

100.0%

Houston Average Rent Houston Average Occupancy

Houston Multi-Family – 626.0K Units

Forecast

Confidential – Colliers International 2016

20172017

Data Source:

Average Cap Rate (Yield)Average Price ($) Per Unit

Sales by Total $ (mil)

Houston Multi-Family 537.8K Units

Q4 '09

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Q2 '13

Q3 '13

Q4 '13

Q1 '14

Q2 '14

Q3 '14

Q4 '14

Q1 '15

Q2 '15

Q3 '15

Q4 '15

Q1 '16

Q2 '16

Q3 '16

Q4 '16

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000Rolling 12-mo. Total Quarterly Vol.

Q4 '09

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Q2 '13

Q3 '13

Q4 '13

Q1 '14

Q2 '14

Q3 '14

Q4 '14

Q1 '15

Q2 '15

Q3 '15

Q4 '15

Q1 '16

Q2 '16

Q3 '16

Q4 '16

020,00040,00060,00080,000

100,000120,000140,000160,000

Houston United States

Q4 '09

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Q2 '13

Q3 '13

Q4 '13

Q1 '14

Q2 '14

Q3 '14

Q4 '14

Q1 '15

Q2 '15

Q3 '15

Q4 '15

Q1 '16

Q2 '16

Q3 '16

Q4 '16

3%

5%

7%

9%

11%

Houston United States

Confidential – Colliers International 2016

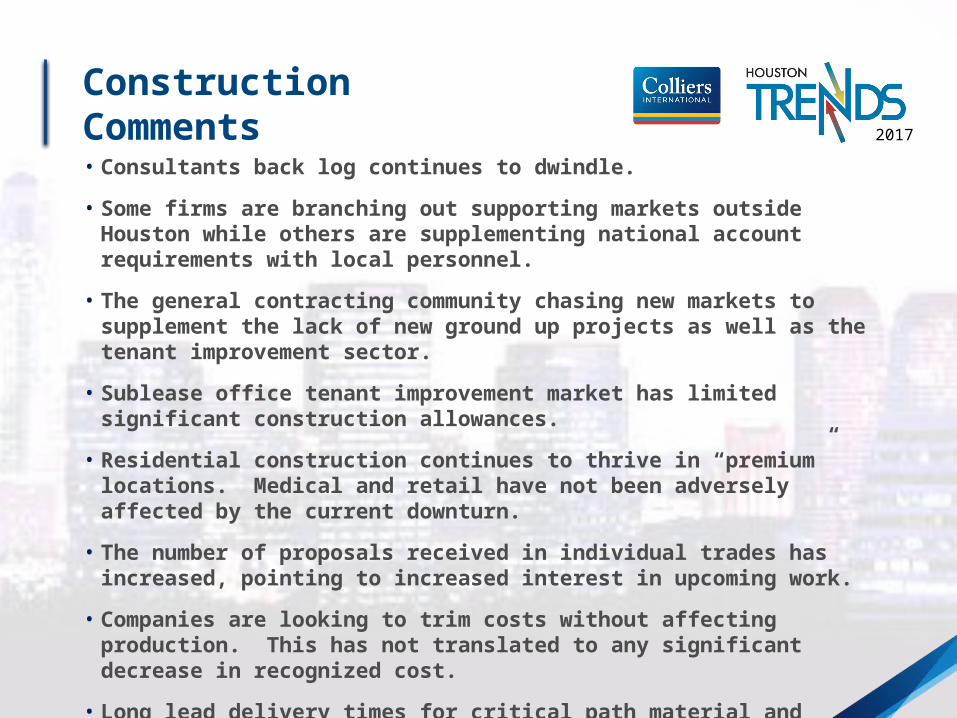

20172017• Consultants back log continues to dwindle.

• Some firms are branching out supporting markets outside Houston while others are supplementing national account requirements with local personnel.

• The general contracting community chasing new markets to supplement the lack of new ground up projects as well as the tenant improvement sector.

• Sublease office tenant improvement market has limited significant construction allowances.

• Residential construction continues to thrive in “premium” locations. Medical and retail have not been adversely affected by the current downturn.

• The number of proposals received in individual trades has increased, pointing to increased interest in upcoming work.

• Companies are looking to trim costs without affecting production. This has not translated to any significant decrease in recognized cost.

• Long lead delivery times for critical path material and equipment continues to drive completion dates.

Construction Comments

Confidential – Colliers International 2016

2017

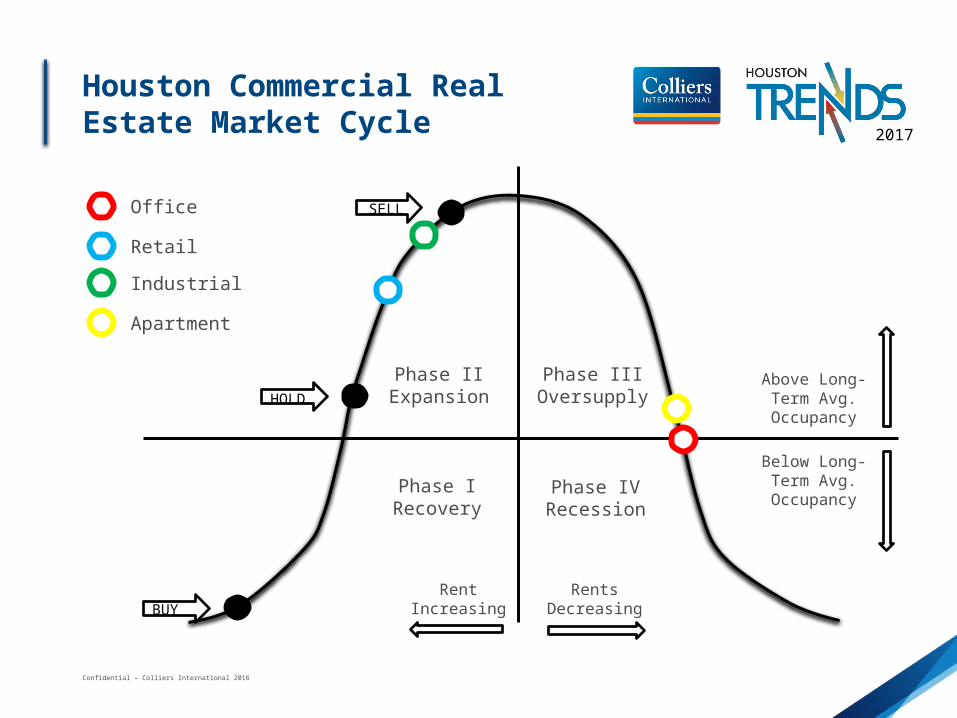

Office

Retail

Industrial

Apartment

Phase IRecovery

Phase IIExpansion

Phase IVRecession

Phase IIIOversupply

Rent Increasing

Rents Decreasing

Above Long-Term Avg.

Occupancy

Below Long-Term Avg. Occupancy

SELL

HOLD

BUY

Houston Commercial Real Estate Market Cycle

Thank you, have a great 2017.