Embed Size (px)

Citation preview

FHA CONDO APPROVAL

BLOWNMORTGAGE.COM

Condo ownership possesses unique circumstances that alterthe way that FHA financing occurs. In order for a borrower tohave an FHA loan on a condo, the condo must have gonethrough FHA condo approval. Typically, the process iscompleted when the development is built, but that is not alwaysthe case. In order for a condo unit to be eligible for FHAfinancing, it must be on the FHA list of approved condos. TheFHA has a standard list of requirements that must be met inorder for a condo to be approved that spans a wide spectrumof topics. The entire process can take between two weeks tothree months to complete, depending on the status of theproject and the number of requirements that the developmentalready meets. If the condo is not already on the FHA list andthe developer is done building the units, the condo associationwill typically handle the approval process.

BLOWNMORTGAGE.COM

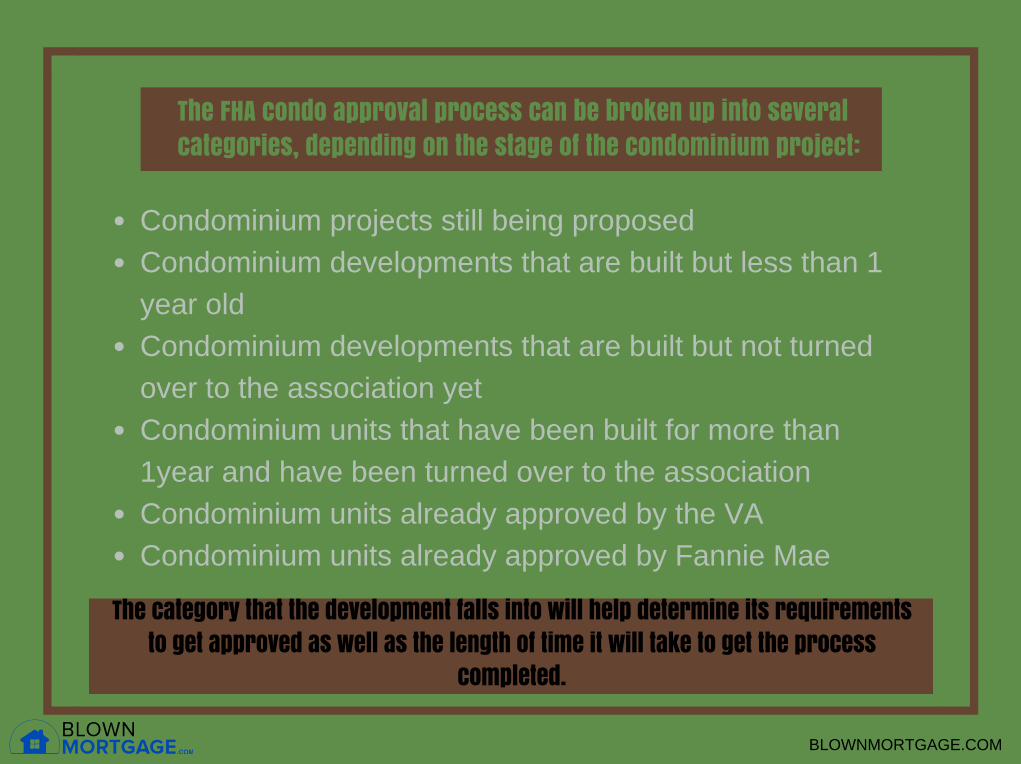

The FHA condo approval process can be broken up into severalcategories, depending on the stage of the condominium project:

Condominium projects still being proposedCondominium developments that are built but less than 1year oldCondominium developments that are built but not turnedover to the association yetCondominium units that have been built for more than1year and have been turned over to the associationCondominium units already approved by the VACondominium units already approved by Fannie Mae

The category that the development falls into will help determine its requirementsto get approved as well as the length of time it will take to get the process

completed.

BLOWNMORTGAGE.COM

Proposed Condo BuildingsThe category that requires the most work is the condos being built category. Because there is no history of the development, the builder or developer is starting from scratch. The process is best started as early as possible in order to ensure its completion by the time the condos are able to be purchased and closed upon. The documentation/information required includes:

BLOWNMORTGAGE.COM

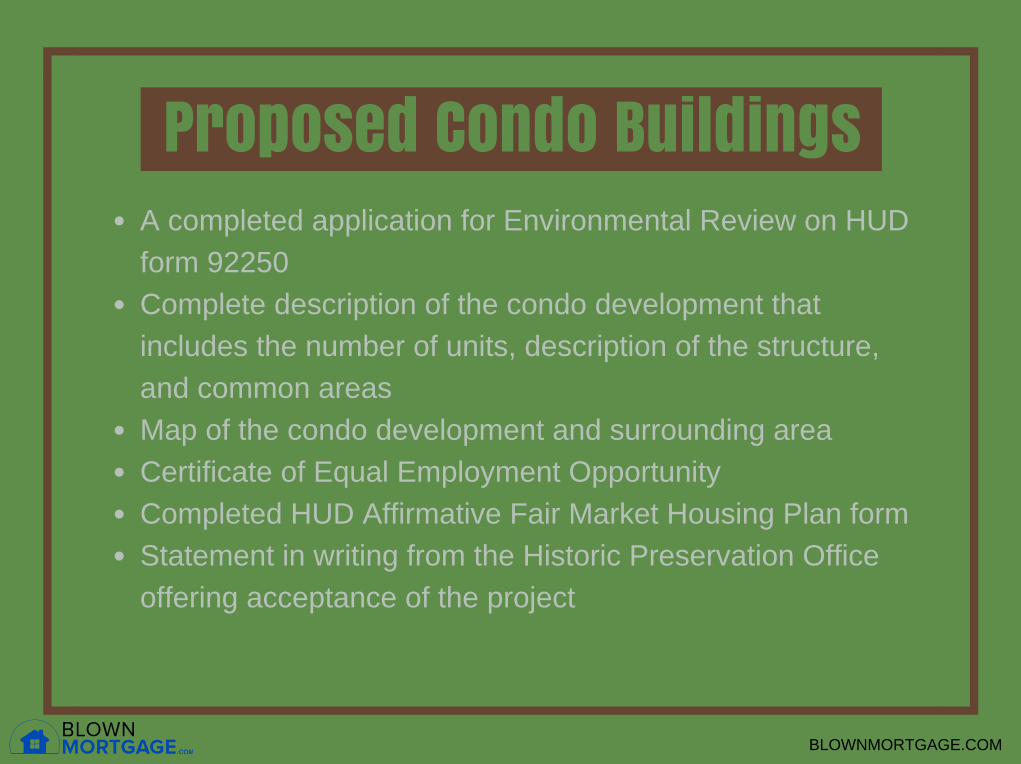

Proposed Condo BuildingsA completed application for Environmental Review on HUDform 92250Complete description of the condo development thatincludes the number of units, description of the structure,and common areasMap of the condo development and surrounding areaCertificate of Equal Employment OpportunityCompleted HUD Affirmative Fair Market Housing Plan formStatement in writing from the Historic Preservation Officeoffering acceptance of the project

BLOWNMORTGAGE.COM

Proposed Condo BuildingsOnce the environmental review is completed, FHA will require further documentation in regards to the construction of the units, as well as the operating budget, any legal documents, and the intended management plan. HUD will review the budget and management propositions to ensure that they are adequate and reasonable. Once all of the above aspects have met with proper approval, the process of conditional approval for sale of the condos with FHA financing can begin. There will be conditions that need to be met during the presale including requirements for owner occupancy as well as the need to provide the site survey and proof of a minimum one-year warranty against any builder defects or defaults.

BLOWNMORTGAGE.COM

Condos Built for Less than One YearCondos that are under construction or have been in existencefor less than one year will undergo a similar process with a fewless requirements. The main difference with FHA financing forcondos in existence for less than one year is the maximumLTV that is allowed. If there is not a minimum ten-yearwarranty in place, the maximum LTV is 90% for FHA financing.This differs from standard FHA financing which typically onlyrequires 3.5% down as opposed to 10% down, so it isimportant to understand this when shopping for a condo. Thestipulations that must be met in order to obtain a condo that isbuilt for less than one year includes:

BLOWNMORTGAGE.COM

Condos Built for Less than One YearWritten request for approval that contains the description ofthe condo development along with the number of units it willcontain and the types of common areasMap of the areaSurveySchedule of condo developmentLegal documents for the condo drawn up by an attorneyThe proposed budget for the associationThe proposed management plan for the developmentCurrent status of the development’s finances and reservesProof of previous association meetings if they occurred

BLOWNMORTGAGE.COM

Condos Built for Less than One Year

Upon receipt of the appropriate documents, theField Office will conduct inspections to determinethe eligibility of the condo development. If theunits pass inspection, appraisals will benecessary to complete the process.

BLOWNMORTGAGE.COM

Condos Built but not Turned Over to the Association

Condo developments that are done building yetstill have units that were not sold might not havebeen turned over to the association yet. Thesedevelopments can receive FHA condo approvalas long as they meet a few additionrequirements, in addition to the standardrequirements from above.

BLOWNMORTGAGE.COM

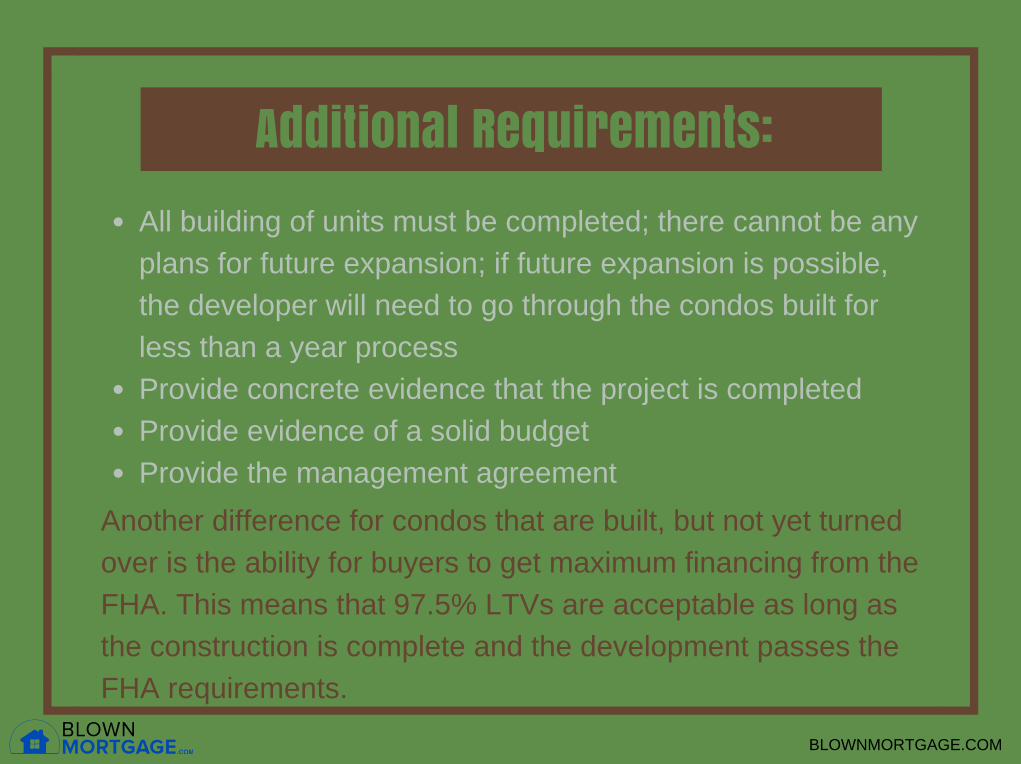

Additional Requirements:All building of units must be completed; there cannot be anyplans for future expansion; if future expansion is possible,the developer will need to go through the condos built forless than a year processProvide concrete evidence that the project is completedProvide evidence of a solid budgetProvide the management agreement

Another difference for condos that are built, but not yet turnedover is the ability for buyers to get maximum financing from theFHA. This means that 97.5% LTVs are acceptable as long asthe construction is complete and the development passes theFHA requirements.

BLOWNMORTGAGE.COM

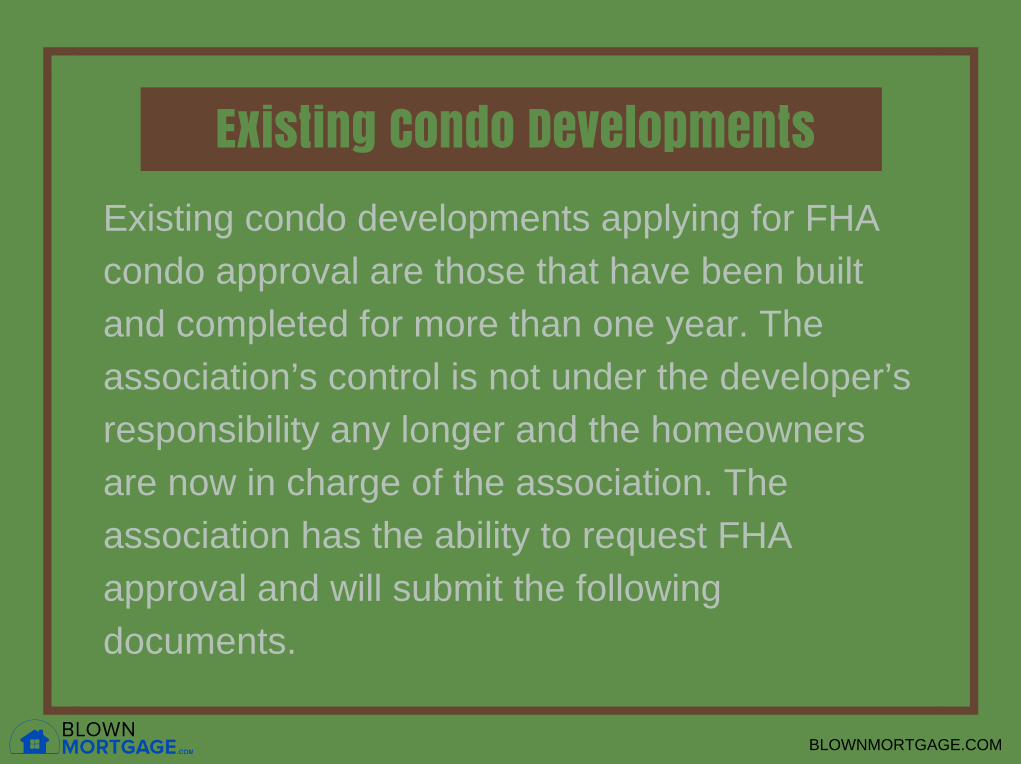

Existing Condo DevelopmentsExisting condo developments applying for FHA condo approval are those that have been built and completed for more than one year. The association’s control is not under the developer’s responsibility any longer and the homeowners are now in charge of the association. The association has the ability to request FHA approval and will submit the following documents.

BLOWNMORTGAGE.COM

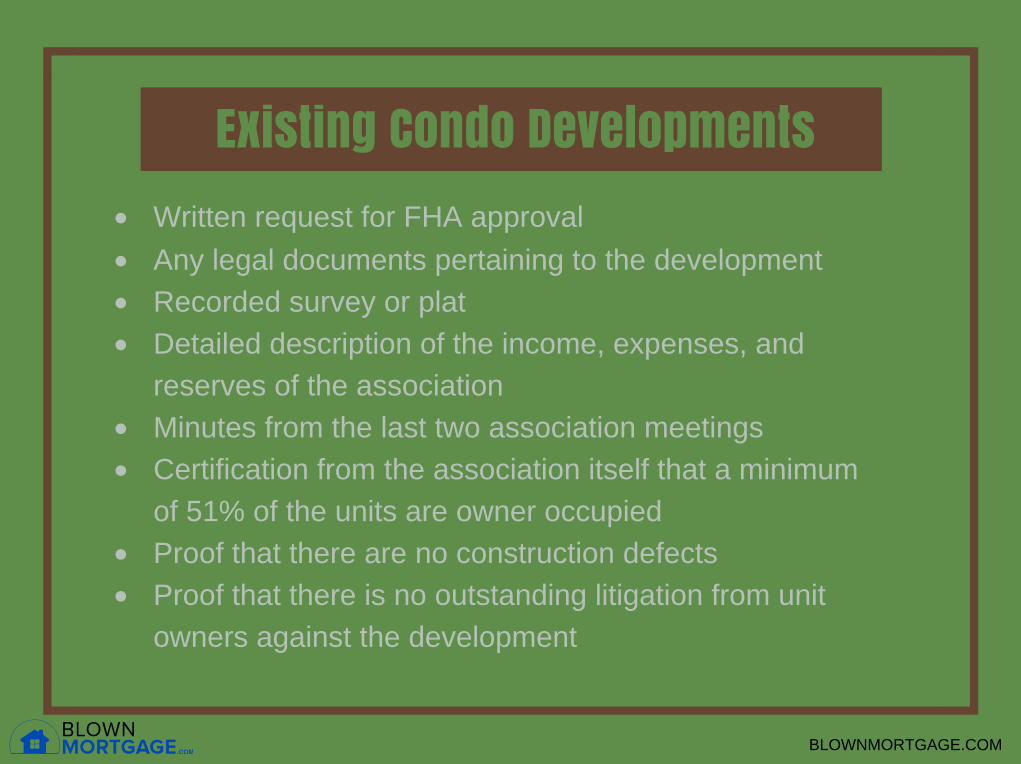

Existing Condo Developments• Written request for FHA approval• Any legal documents pertaining to the development• Recorded survey or plat• Detailed description of the income, expenses, and

reserves of the association• Minutes from the last two association meetings• Certification from the association itself that a minimum

of 51% of the units are owner occupied• Proof that there are no construction defects• Proof that there is no outstanding litigation from unit

owners against the development

BLOWNMORTGAGE.COM

Condo Developments Approved by the VA

If the condo development has been previously approved for VAfunding, obtaining FHA condo approval is rather simple andmuch less complicated than any of the above situations. Thefollowing items must be provided to ensure approval by theFHA:

Approval letter from the VACopies of any legal documents that have been recordedRecorded plat and surveyProposed or existing budgetMinutes from any association meetingsUndergo an onsite visit in order to ensure the sustainability ofthe projectProof of owner occupancy in at least 51% of the units

BLOWNMORTGAGE.COM

Condo Developments Approved by Fannie Mae

FHA condo approval of condos already approved byFannie Mae is very simple. The only documents requiredare the FNMA Form 1026 Application or FNMA Form1027 Conditional Project Acceptance along with anysupporting documentation that rendered your approval.Typically, an on-site review will also be performed toensure satisfaction of HUD’s requirements for FHA condoapproval.

BLOWNMORTGAGE.COM

CLICK HERETO LEARN MORE:

BLOWNMORTGAGE.COMLENDER HOTLINE: 888-581-5008

BLOWNMORTGAGE.COM

INFORMATION PROVIDED BY:

Justin McHood

Mortgage Commentator

Information Originally Published: 12/12/15

Justin McHood is Americas Mortgage Commentator and hasbeen providing Mortgage commentary for over 10 years.

BLOWNMORTGAGE.COM

MORTGAGECOMMENTATOR.COM

@MORTGAGECOM_

FACEBOOK.COM/MORTGAGECOMMENTATOR

LEARN MORE ABOUT MORTGAGE COMMENTATOR:

LENDER HOTLINE:888-581-5008

BLOWNMORTGAGE.COM