Embed Size (px)

Citation preview

Environmental Performance and the Cost of Capital:

Evidence from REIT Commercial Mortgages and Bonds

Piet Eichholtz

Rogier Holtermans

Nils Kok

Erkan Yönder

A New Source of Capital in the MarketGreen bonds are the new kid in town

Vasakronan (SE) – $197M, 2-yr, 1.315% (November 2013)

Unibail-Rodamco (FR) – $1.03Bn, 10-yr, 2.5% (February 2014)

Regency Centers – $250M, 10-yr, 3.75% (May 2014)

Vornado - $450M, 5-yr, 2.5% (June 2014)

Stockland (AU) - $380M, 7-yr, 1.5% (October 2014)

Energy Efficiency, Sustainability, and Real EstateBuildings directly exposed to regulatory risk

The real estate sector is responsible

for about 80 percent of US electricity consumption

for 40 percent of global carbon emissions

Increasing attention to carbon emissions from buildings

Mandatory disclosure laws

Real Estate Investment Trusts (REITs) are listed property companies.

Have to generate 75% of their income from real estate

Mainly buy, operate, and sell properties

Large exposure to “stranded asset” risk

Green building certifications “guarantee” certain level of sustainability and environmental performance.

Increasing Attention to SustainabilityDirect link to capital markets

How can we measure “sustainability”?

One way is to estimate price of carbon directly

Alternatively, use broader corporate social responsibility (CSR)

or environmental performance measures

Margolis, Elfenbein, and Walsh (2007) survey the literature on the

relationship between CSR and financial performance

Overall, they find a positive relation, but causal direction

unclear

Improved reputation (Turban and Greening, 1997)

Increases in organizational effectiveness (Sharfman and

Fernando, 2008)

Sustainability and Cost of CapitalLiterature mostly focuses on CSR in general

Sharfman and Fernando (2008) Better environmental risk management associated

with lower beta, lower cost of capital (WACC), higher debt capacity …

… but cost of debt is higher

Bauer and Hann (2010) Environmental concerns increase cost of debt and

lower ratings

Proactive environmental management lowers spreads

Goss and Roberts (2011) Worse CSR performance (lower KLD score) leads to

higher spreads on bank loans

But only for low-quality borrowers

Sustainability and Real Estate PerformanceCash flow, value, and risk

Greenness affects the economic performance of office buildings (Eichholtz, Kok, and Quigley, 2010, 2013; Fuerst and McAllister, 2011; Chegut, Eichholtz, and Kok, 2014)

Higher rent and higher value

Higher and more stable occupancy risk

Greenness affects house transactions and prices (Brounenand Kok, 2011; Fuerst, McAllister, and Wyatt, 2015)

Higher prices and shorter time on the market

Greenness also matters at the portfolio level for REITs (Eichholtz, Kok, and Yönder, 2012)

Better operating performance, but alpha no different

Lower beta

Environmental Performance and the Cost of CapitalREITs’ debt capital offers a clean test for the effects of greenness

We test the impact of investments in more sustainable real estate on the spreads and ratings of corporate bonds and on the spreads of commercial mortgages

Among the very few papers testing the relationship

Using a direct measure of environmental sustainability

We evaluate cost of debt at the corporate and at the asset level

The first paper evaluating the impact of environmental performance on the cost of real estate debt

Directly relating cost of capital to “greenness”

DataREIT corporate bonds and commercial mortgages

We collect data for US REITs’ commercial mortgages and corporate bonds from SNL Financial

We calculate spreads at origination using constant maturity treasury rates

Using the closest time to maturity at origination

Final dataset consists of

3044 properties collateralizing REIT commercial mortgages from 2003 until 2012

412 corporate bond issues of 57 REITs, 2003 - 2011

Bond ratings translated to numbers

In our data set, S&P rating ranges from 7 (B-) to 17 (A) while Moody’s ranges from 8 (B2) to 17 (A2)

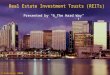

We Use LEED and Energy Star Labels to Assess

Greenness

LEED

The program has been initiated by the US Green Building Council (USGBC).

LEED covers six different components of sustainability, including energy performance and material selection.

Energy Star

Founded in 1992 by the U.S. Environment Protection Agency (EPA) and the U.S. Department of Energy (DOE).

Energy star evaluates the efficiency of buildings‘ energy use with respect to a base building of similar size and quality.

The Diffusion of Greenness in REIT PortfoliosSlow … but increasing

0.0

1.0

2.0

3.0

4.0

5.0

6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010Year

LEED Energy Star

Sq

uar

e fe

et

REIT Property PortfoliosData matching

Using GIS software, we convert the addresses of buildings into a

unique combination of longitude and latitude

Data Matching

Step 1: Format addresses from USGBC, EPA, SNL Financial

Step 2: Perfect matches

Step 3: Decomposing addresses of a portfolio of properties

Step 4: Searching for similar addresses

Annual greenness of portfolios for each REIT

Considering year of acquisition, sale and certification

Models: Spreads Commercial Mortgages and

Spread / Rating REIT Bonds

Investigate spreads at mortgage level

Different mortgages issued by same firm

Investigate spreads at mortgage level

Different mortgages issued by same firm

Tackling endogeneity issues

Two-staged least squares

Use the weighted share of property greenness in regions as instrument (EKY, 2012)

Follow bonds after issuance to investigate whether changes in REIT greenness affect yield spread (to be done)

Bond_Spread= f(Green_Share;Bond_Characteristics;Firm_Characteristics)

Bond_Rating = f(Green_Share;Bond_Characteristics;Firm_Characteristics)

Mortgage_Spread= fGreen_Label;Mortgage_Characteristics;

Property_Characteristics

æ

èç

ö

ø÷

ControlsAt the level of the mortgage, the property, the firm, the bond

In line with literature for commercial mortgages

Mortgage characteristics

LTV, LTV high (Titman et al 2005), property vintage dummy, book value of the property, time to maturity, a fixed rate dummy, a “cross-collateralization” dummy

Property characteristics

Floor surface area, access to public transportation, amenities, office quality

Bond characteristics

Value of the bond, time to maturity, callable dummy

Firm characteristics

Total assets, interest coverage ratio, firm Q, cash stock

Sample Statistics Commercial Mortgages

Mean Std. Dev. Obs.

Mortgage Characteristics

Mortgage Spread (in %) 283.66 185.51 3044

LTV (in %) 55.00 24.08 3044

Time-to-Maturity (in years) 6.18 4.69 3044

Cross-Coll (in %) 24.08 42.76 3044

Fixed Rate (in %) 82.39 38.10 3044

Property Book Value (in $millions) 48.33 10.55 3044

Property Age Dummy ≤10 years 0.32 0.47 3044

LEED Label (in %) 1.41 11.80 3044

Energy Star Label (in %) 2.69 16.19 3044

Sample Statistics REIT Bonds and REITs

The number of REIT

observations is firm-

years

Bonds are cheaper than

mortgages

Somewhat longer

maturities than the

mortgages

A few more green

buildings

VARIABLES Mean Std. Dev. Obs.

Bond Characteristics

Bond Spread (in bps) 170.02 170.35 412

Debt Value (in $millions) 211.82 203.22 412

Time-to-Maturity (in years) 9.79 5.31 412

Callable (in %) 72.09 44.91 412

REIT Characteristics

LEED Share (in %) 1.35 4.29 232

Energy Star Share (in %) 2.22 7.26 232

Total Assets (in billions) 5.78 5.74 232

Interest Coverage (in %) 323.00 139.56 232

Firm Q 1.43 0.32 232

Cash Stock (in %) 1.53 2.40 232

Findings on Mortgages (mortgage controls only)LEED and Energy Star buildings: lower mortgage spreads

(1) (2) (3) (4)

VARIABLES Spread Spread Spread Spread

LEED -0.526** -0.596**

[0.245] [0.265]

Energy Star -0.298* -0.286*

[0.173] [0.170]

REIT dummies N N Y Y

Observations 3,044 3,044 3,044 3,044

Adj. R-squared 0.50 0.50 0.56 0.56

If a mortgage is collateralized by a certified property, the borrower pays a

lower spread

53-60 bps for LEED, corresponding to a $268k-$304k decline in average

interest expense

29-30 bps for Energy Star, translating into a $152k decline in the interest

expense

Findings on Mortgages (mortgage controls only)Continued – mortgage controls

(1) (2) (3) (4)

VARIABLES Spread Spread Spread Spread

LTV 0.502* 0.502* 0.139 0.14

[0.293] [0.291] [0.273] [0.271]

LTV Dummy -0.450*** -0.450*** -0.286** -0.284**

(LTV≥0.7) [0.139] [0.139] [0.137] [0.136]

Property Age Dummy -0.182** -0.184** -0.108 -0.111

(≤10 years) [0.082] [0.082] [0.074] [0.074]

log(Property Book Value) -0.128*** -0.130*** -0.074* -0.078**

[0.037] [0.037] [0.038] [0.038]

Time-to-Maturity -0.118*** -0.118*** -0.116*** -0.116***

[0.011] [0.011] [0.011] [0.011]

Cross-Coll -0.078 -0.076 -0.365** -0.361**

[0.187] [0.187] [0.162] [0.163]

Fixed Rate 1.722*** 1.720*** 1.752*** 1.753***

[0.191] [0.192] [0.179] [0.179]

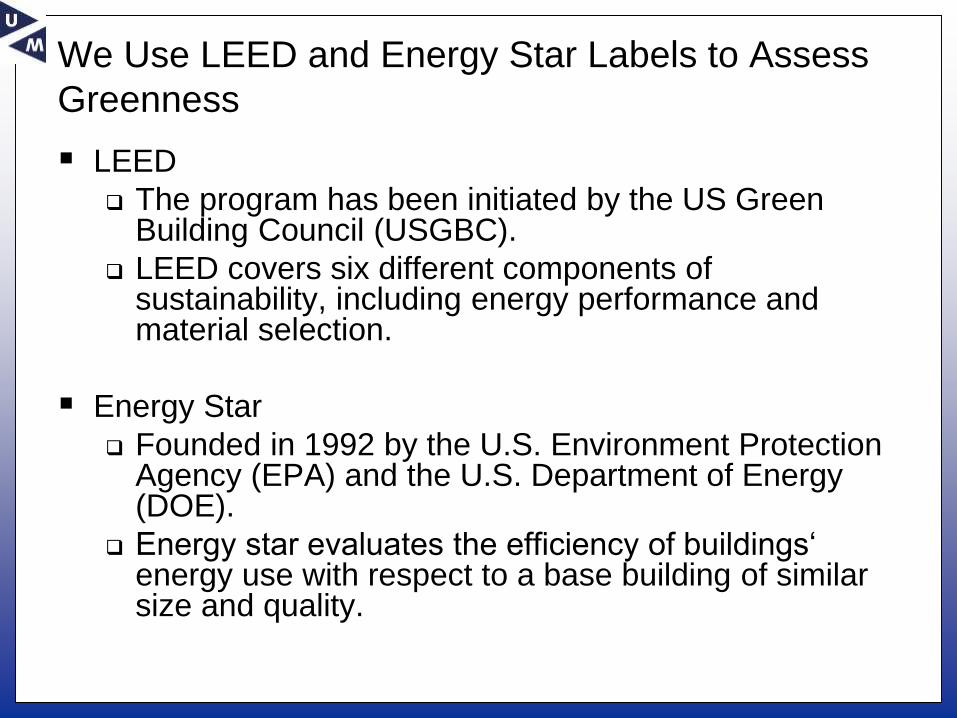

Findings on Mortgages (with property controls)Green spread reduction same magnitude, but a bit bigger

We match SNL data with CoStar to obtain building hedonics.

Mortgages collateralized by certified properties have lower spreads

67-81 bps for LEED, corresponding to a $339k-$410k decline in interest

expense

44 bps for Energy Star, corresponding to a $226k decline in interest expense

Findings on Mortgages (with property controls) Continued – property quality controls

No surprises in results controls variables: collateral quality matters for

the mortgage spread• More amenities and better (accessibility of) locations associated with

lower spreads

• Building size and renovation not material

(1) (2) (3) (4)

VARIABLES Spread Spread Spread Spread

ln(Sqft) -0.003 0.005 0.011 0.028

[0.095] [0.095] [0.106] [0.105]

Renovated Dummy -0.052 -0.064 -0.162 -0.175

[0.131] [0.129] [0.134] [0.131]

Amenities Dummy -0.330** -0.324** -0.360*** -0.362***

(≤5 different amenities) [0.143] [0.143] [0.127] [0.129]

Transit Stop Dummy -0.349*** -0.353*** -0.149 -0.152

[0.123] [0.122] [0.103] [0.105]

Findings on Office Mortgages (with property controls)Spread reduction effect is robust

The regression now includes a Class A quality dummy

Mortgages collateralized by certified offices have lower spreads

59-78 bps for LEED, corresponding to a $298k-$395k decline in the interest

expense

38 bps for Energy Star, corresponding to a $196k decline in interest expense

Findings on Office Mortgages (with property controls) Continued – property quality controls

Results controls variables similar as in broader sample: collateral

quality matters for mortgage spread• More amenities, higher office quality, better (accessibility of) locations all

associated with lower spreads

• Building size and renovation status not important

Findings on REIT Corporate BondsA “greener” portfolio has lower spreads and higher ratings

As the LEED share increases by one standard deviation, the spread declines by

19 bps, corresponding to a $424k decline in interest expense

For a one-level increase in S&P (Moody’s) rating, a REIT needs to increase its

LEED share by 2.1 (1.5) standard deviations

The models pass the identification tests

(1) (2) (3) (4) (5) (6)

VARIABLES Spread Spread S&P S&P Moody’s Moody’s

LEED Share -4.529** 6.536** 9.144***

[1.766] [2.823] [3.538]

Energy Star Share -0.646 0.925 0.040

[0.443] [0.622] [0.623]

Hansen J (Prob.) 0.26 0.17 0.13 0.24 0.02 0.15

Kleibergen-Paap

(Prob.)

0.00 0.00 0.00 0.00 0.00 0.00

Findings on REIT Corporate BondsContinued – firm and bond controls

(1) (2) (3) (4) (5) (6)

VARIABLES Spread Spread S&P S&P Moody’s Moody’s

log(Debt Value) -0.032 -0.008 0.113** 0.064* 0.094** 0.081**

[0.071] [0.065] [0.046] [0.034] [0.048] [0.041]

Time-to-Maturity -0.130*** -0.136*** -0.001 0.002 -0.002 -0.006

[0.034] [0.036] [0.009] [0.008] [0.011] [0.010]

Callable 0.586** 0.567** 0.087 -0.137 0.328 0.081

[0.243] [0.239] [0.219] [0.179] [0.245] [0.189]

log(Firm Size) -0.174* -0.264*** 0.832*** 0.848*** 0.706*** 0.757***

(lagged) [0.097] [0.072] [0.161] [0.150] [0.147] [0.158]

Interest Coverage -0.358*** -0.306*** -0.272*** -0.207*** -0.219*** -0.166

(lagged) [0.057] [0.054] [0.059] [0.070] [0.066] [0.122]

Interest Coverage 0.016*** 0.010*** 0.031** 0.024* 0.011 0.010

(squared/lagged) [0.003] [0.003] [0.014] [0.014] [0.017] [0.024]

Firm Q -0.316 -0.467* 1.980*** 2.030*** 1.426*** 1.469***

(lagged) [0.271] [0.278] [0.464] [0.458] [0.308] [0.320]

Cash Stock 0.577 3.198 4.599 2.130 -1.145 -1.827

(lagged) [3.072] [3.003] [3.149] [2.803] [3.030] [3.145]

Concluding Remarks

We assess the impact of environmental performance on the cost of capital by evaluating commercial mortgage spreads, REIT bond spreads, and bond ratings

LEED label is consistently associated with bigger (and more significant) spread difference than Energy Star

A mortgage collateralized by a green labeled (office) building has a lower spread 59-81 bps for LEED, implying a $298-$410k decline in the average annual

interest expense

38-44 bps for Energy Star, translating into a $196k-$226k decline in average annual interest expense

For bonds, the spread declines by 8-19 bps as the LEED share increases by one standard deviation, corresponding to a $169k-$424k decline in interest expense Also, higher LEED share leads to better bond ratings

Next steps

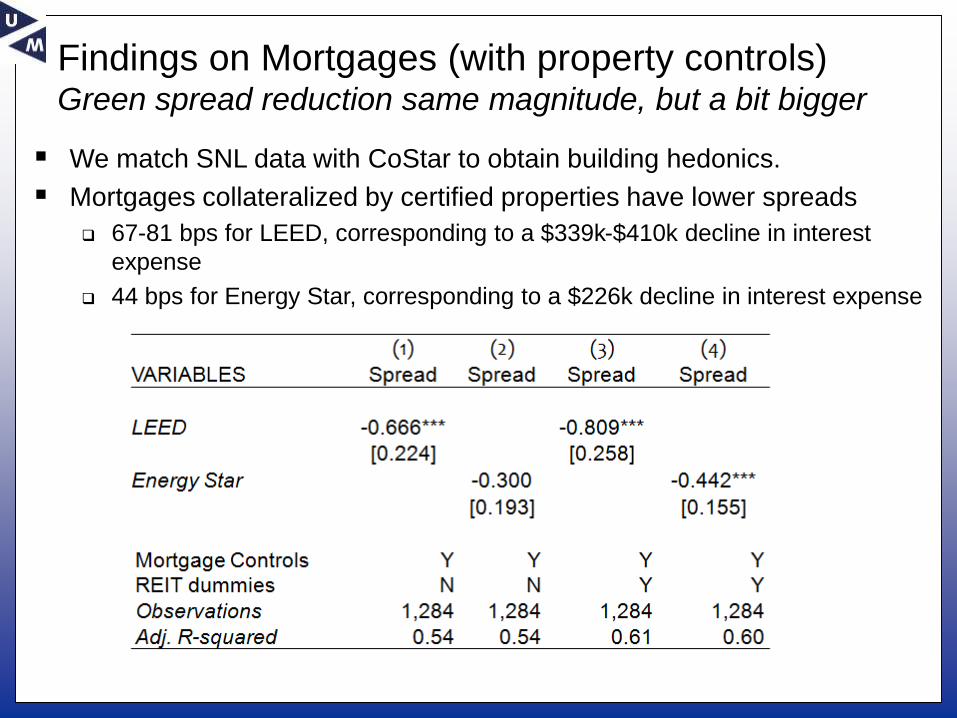

What is the mechanism behind the results?

Lower default risk on LEED/Energy Star buildings? (a la Quercia et al. 2013)

Higher quality borrower?

Serving specific lender preferences

Causality between “Greenness” and cost of debt could be different

Look for bond data during life of the bonds, and yield effect of changes in firm greenness after issuance

The dynamics in the current low-interest environment might be different from 2008-2010

Heterogeneity in estimated effects

Expand dataset to include more recent years