Embed Size (px)

Citation preview

2015: A Year in Charts

Detroit | 2015

CBD fundamentals firming, suburbs to follow?

Detroit

•Downtown Detroit is in the midst of a renaissance, bolstered by a recent series of high-profile lease

announcements, the latest of which was by Fifth Third Bank. Fifth Third announced that it will lease 62,000 square

feet in the One Woodward building to serve as its regional headquarters. As part of the lease agreement, the One

Woodward building will be renamed Fifth Third Bank at One Woodward. The move will take place over two years

and will involve the relocation of over 150 full-time employees. Fifth Third will keep about 20,000 square feet and up

to 40 employees in Southfield, where it currently leases 105,000 square feet.

Source: JLL Research, Crain’s Detroit

Chart of the week: January 12, 2015

28.9% 24.1%

22.2%

19.3%

17.5%

28.2% 28.7% 29.3% 28.2%

27.0%

15%

20%

25%

30%

35%

2010 2011 2012 2013 2014

CBD Vacancy Suburban Vacancy

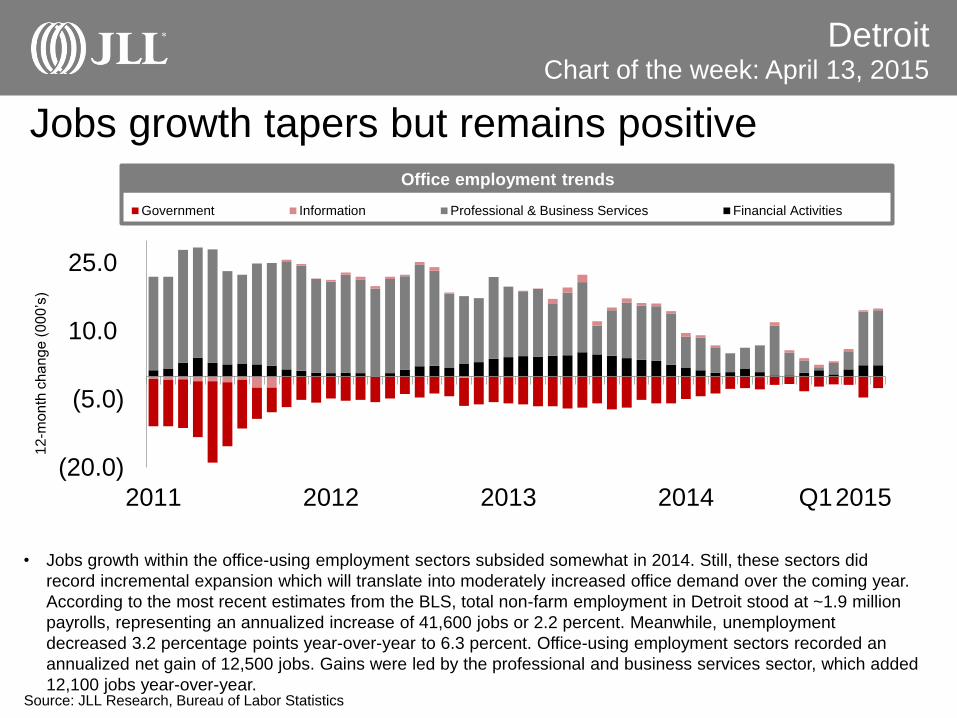

Jobs growth tapers but remains positive

Detroit

• Jobs growth within the office-using employment sectors subsided somewhat in 2014. Still, these sectors did

record incremental expansion which will translate into moderately increased office demand over the coming year.

According to the most recent estimates from the BLS, total non-farm employment in Detroit stood at ~1.9 million

payrolls, representing an annualized increase of 41,600 jobs or 2.2 percent. Meanwhile, unemployment

decreased 3.2 percentage points year-over-year to 6.3 percent. Office-using employment sectors recorded an

annualized net gain of 12,500 jobs. Gains were led by the professional and business services sector, which added

12,100 jobs year-over-year. Source: JLL Research, Bureau of Labor Statistics

Chart of the week: April 13, 2015

(20.0)

(5.0)

10.0

25.0

2011 2012 2013 2014 Q12015

Government Information Professional & Business Services Financial Activities

Office employment trends

12-m

onth

ch

an

ge

(0

00

’s)

Pendulum slowly swings in favor of landlords

Detroit

• Due to significant demand gains in recent years and steadily decreasing vacancy rates, landlords have begun to

push rents. Class A asking rents averaged $22.95 per square foot at the end of Q1, up $0.65 or 2.9 % year-over-

year while Class B asking rents averaged $16.98 per square foot, up $0.24 or 1.5 % year-over-year. Further rent

increases are forecasted over the coming year, particularly downtown and in other key submarkets when demand

is concentrated.

Source: JLL Research

Chart of the week: April 27, 2015

$15.50

$18.50

$21.50

$24.50

2011 2012 2013 2014 Q1 2015

Class A Class B

Vacancy rates still high but demand is growing

Detroit

• Total vacancy in Detroit was 24.4 percent at the end of the first quarter, down from a high of 32.9 percent in 2010.

Since that time, more than 4.8 million square feet of office space has been absorbed by local companies growing

operations and expanding footprints. Growth has favored downtown, but has not been limited to it. As a result,

vacancy rates are compressing across submarkets and are forecasted to continue to decrease over the coming

year as the region records further demand growth.

Source: JLL Research

Chart of the week: April 27, 2015

15.0%

21.0%

27.0%

33.0%

2011 2012 2013 2014 Q1 2015

Suburban CBD

Foreign Direct Investment In Detroit

Detroit

• FDI in Detroit city and the metro area concentrates heavily in the auto industry. The auto industry alone accounted

for 70.5 percent of all jobs in FOEs in Detroit city, with Chrysler Fiat being the largest employer. Region wide, 41.8

percent of all jobs in FOEs are in the auto industry. Although FDI in both the city and the metro remains heavily

manufacturing focused, services account for a growing share of jobs in FOEs.

Source: Brookings Institution

Chart of the week: May 4, 2015

0 1000 2000 3000 4000 5000 6000 7000

Motor vehicles (38.9%)

Engine & Power Equip (27.9%)

Restaurants ( 5.7%)

Special food services (4.7%)

Motor vehicle parts (3.7%)

Freight Trucking (2.7%)

Investigation & Security (2.6%)

Advertising Services (2.4%)

Pharmaceuticals (1.9%)

Travelers Accommodations (1%)

Rest of the Economy (8.4%)

# of Foreign Owned Establishment Jobs in Detroit

# of FOE Jobs

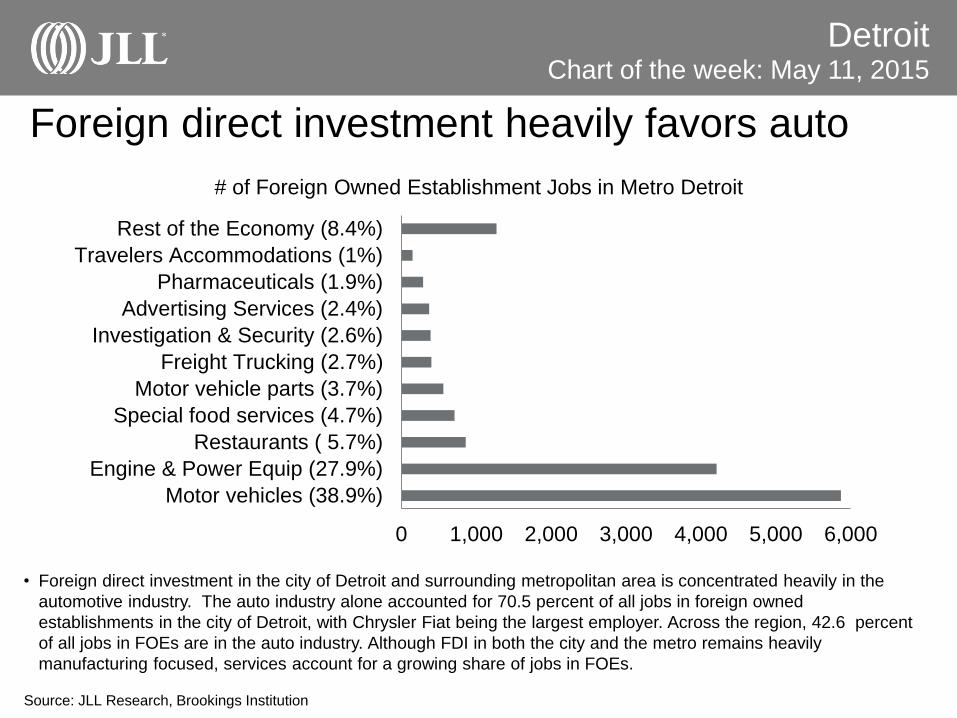

Foreign direct investment heavily favors auto

Detroit

• Foreign direct investment in the city of Detroit and surrounding metropolitan area is concentrated heavily in the

automotive industry. The auto industry alone accounted for 70.5 percent of all jobs in foreign owned

establishments in the city of Detroit, with Chrysler Fiat being the largest employer. Across the region, 42.6 percent

of all jobs in FOEs are in the auto industry. Although FDI in both the city and the metro remains heavily

manufacturing focused, services account for a growing share of jobs in FOEs.

Source: JLL Research, Brookings Institution

Chart of the week: May 11, 2015

0 1,000 2,000 3,000 4,000 5,000 6,000

Motor vehicles (38.9%)

Engine & Power Equip (27.9%)

Restaurants ( 5.7%)

Special food services (4.7%)

Motor vehicle parts (3.7%)

Freight Trucking (2.7%)

Investigation & Security (2.6%)

Advertising Services (2.4%)

Pharmaceuticals (1.9%)

Travelers Accommodations (1%)

Rest of the Economy (8.4%)

# of Foreign Owned Establishment Jobs in Metro Detroit

Rate vs Jobs, Moving in a Healthy Direction

Detroit

• According to the most recent estimates from the BLS, total non-farm employment in Detroit stood at ~1.9 million

payrolls, representing an annualized increase of 38,200 jobs or 2.0 percent. Meanwhile, unemployment decreased

3.4 percentage points year-over-year to 6.0 percent.

Source: JLL Research, Bls

Chart of the week: May 18, 2015

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

1,600,000

1,650,000

1,700,000

1,750,000

1,800,000

1,850,000

1,900,000

1,950,000

2,000,000

2008 2010 2012 2014

unemployment rate

total jobs

Professional & Business Services Ramping Up

Detroit

• Office-using employment sectors have experienced substantial employment expansion over the last year, recording

an annualized net gain of 9,500 jobs across the metro. Employment gains were led by the professional and

business services sector, which added 8,900 jobs year-over-year.

Source: JLL Research, Bureau of Labor Statistics

Chart of the week: May 25, 2015

(25.0)

(15.0)

(5.0)

5.0

15.0

25.0

201

1

201

2

201

3

201

4

201

5

Professional & Business Services Information Government Financial Activities

Increased demand compresses Skyline vacancy

Detroit

• The Detroit Skyline has experienced an upsurge in demand over the last five years. Since 2010, net absorption has

topped 1.4 million square feet, reducing vacancy from 26.0 percent to 11.9 percent at the start of 2015. Planned

expansions and additional demand growth will place the Detroit’s Skyline vacancy rate near 8.9 percent by the end

of 2016. With vacancy dipping below 10.0 percent, a common threshold for development, talk of new office

construction in downtown Detroit may become a reality in the near future.

Source: JLL Research

Chart of the week: June 1, 2015

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Detroit Skyline Vacancy

Ann Arbor landlords hold leverage, raise rents

Detroit

• Ann Arbor, as a result of its diverse economic base and prestigious Big Ten university, is showing a positive overall

economic outlook. Fueled by strong market fundamentals and increased office demand, the Ann Arbor office

market continues to tighten. The average asking rent for Class A office space has escalated towards $29.00 per

square foot while Class B rents have recorded a slight uptick towards $21.00 per square foot and Class C rents

have remained level at $15.00 per square foot.

Source: JLL Research

Chart of the week: June 8, 2015

$5.00/fs

$15.00/fs

$25.00/fs

$35.00/fs

Q2 2015201420132012201120102009200820072006

Class A Class B Class C

Ann Arbor office rents

Limited availability a reflection of robust demand

Ann Arbor

• Ann Arbor’s office market is in the midst of transition. Google’s recent relocation and expansion within the Ann

Arbor submarket, from the CBD to the suburbs, has increased downtown’s availability by 85,000 square feet,

representing 5.3 percent of downtown’s total office inventory. However, there is no need to ring the alarm for

downtown, as the owners of the property have already received extensive interest. Home to the University of

Michigan and 45 minutes from Detroit, Ann Arbor appeals to a wide audience.

Source: JLL Research

Chart of the week: June 15, 2015

0.0%

15.0%

30.0%

45.0%

Q2 2015201420132012201120102009200820072006

Class A Class B Class C

Ann Arbor submarket availability

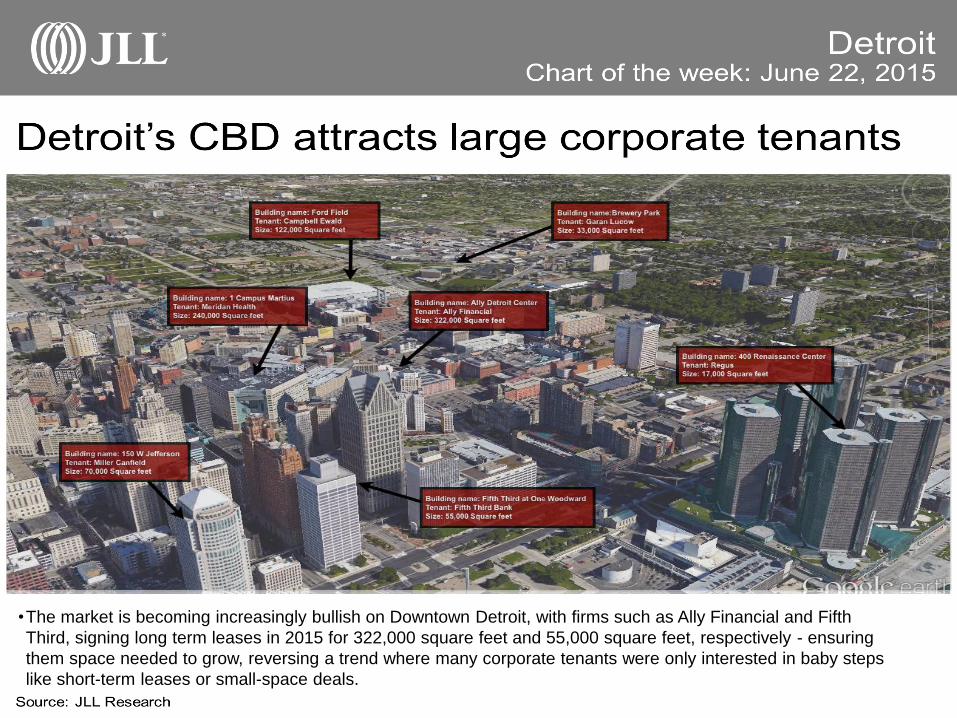

•The market is becoming increasingly bullish on Downtown Detroit, with firms such as Ally Financial and Fifth

Third, signing long term leases in 2015 for 322,000 square feet and 55,000 square feet, respectively - ensuring

them space needed to grow, reversing a trend where many corporate tenants were only interested in baby steps

like short-term leases or small-space deals.

Detroit

• With an improving economy and increasing space needs by office tenants, total vacancy is expected to continue its

downward trend through 2015. Albeit Detroit’s improving economic condition, fundamentals are unlikely to justify

any speculative construction for the short term. Consequently, demand growth will continue to translate almost

entirely into vacancy improvements.

Source: JLL Research, U.S. Bureau of Labor Statistics

Chart of the week: June 29, 2015

600

630

660

690

15.0%

20.0%

25.0%

30.0%

2010 2011 2012 2013 2014 2015 YTD

Total Office Employment (000s) Vacancy %

Job growth spurs office demand in Detroit

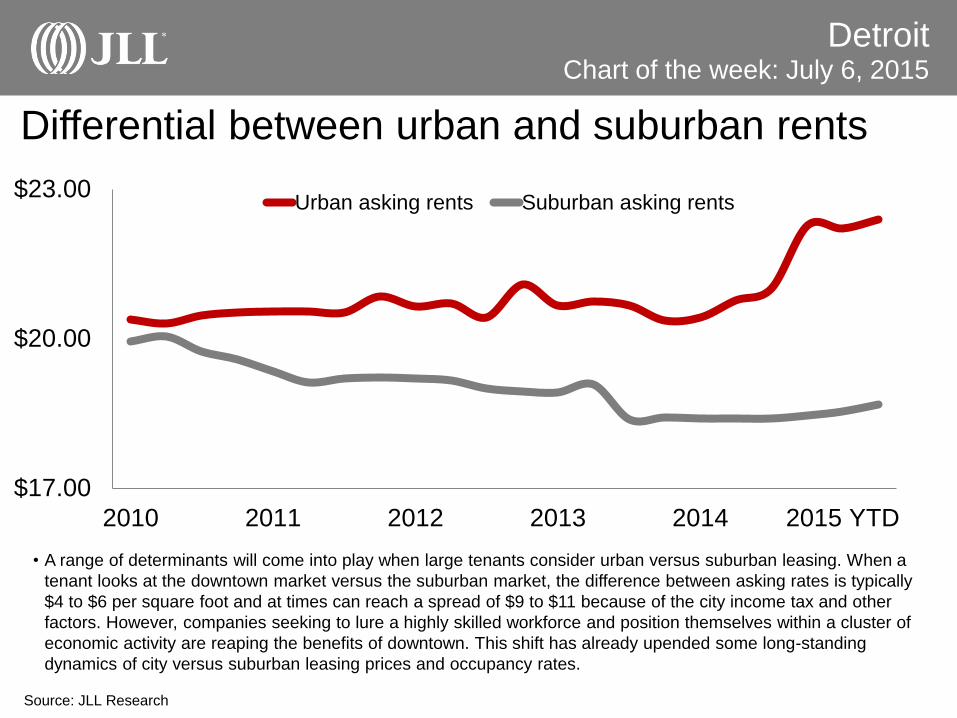

Differential between urban and suburban rents

Detroit

• A range of determinants will come into play when large tenants consider urban versus suburban leasing. When a

tenant looks at the downtown market versus the suburban market, the difference between asking rates is typically

$4 to $6 per square foot and at times can reach a spread of $9 to $11 because of the city income tax and other

factors. However, companies seeking to lure a highly skilled workforce and position themselves within a cluster of

economic activity are reaping the benefits of downtown. This shift has already upended some long-standing

dynamics of city versus suburban leasing prices and occupancy rates.

Source: JLL Research

Chart of the week: July 6, 2015

$17.00

$20.00

$23.00

2010 2011 2012 2013 2014 2015 YTD

Urban asking rents Suburban asking rents

Detroit’s CBD vacancy steadily declines

Detroit

• The market is becoming increasingly bullish on downtown Detroit, with firms such as Ally Financial and Fifth Third

signing long term leases for 320,000 square feet and 62,000 square feet, respectively. Class A vacancy in the CBD

continues to decline from a recent high of 24.9 percent in 2010 to 9.6 percent at the end of Q2 2015. The CBD will

continue to creep near capacity in the near-term as demand growth outpaces supply additions.

Source: JLL Research

Chart of the week: July 13, 2015

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2010 2011 2012 2013 2014 2015

Detroit CBD Class A Vacancy

Detroit

• Industrial employment sectors have experienced substantial employment expansion over the last year, recording

an annualized net gain of 32,200 jobs across the metro. Employment gains were led by the manufacturing sector,

which added 14,200 jobs year-over-year, suggesting continued growth in demand for warehouse space.

Source: JLL Research

Chart of the week: July 27, 2015

-10.0

5.0

20.0

35.0

20

11

20

12

20

13

20

14

20

15

Mining, Logging & Construction Trade,Transportation & UtilitiesManufacturing Other Services

Manufacturing is driving Detroit’s job market

Michigan manufacturing leads nation in

job growth

Detroit

• Out of more than 2,700 counties across the U.S., four counties in the top 10 with the best manufacturing

economies in terms of creating jobs were in Michigan: Wayne and Macomb counties in Detroit and Kent and

Ottawa counties in Grand Rapids. Stimulated by a confluence of factors-including public and private initiatives,

high-tech incubators, philanthropic funding and an influx of venture capital, Metro Detroit has the fourth largest

advance industries sector in the country. This confirms Metro Detroit is still a vibrant manufacturing hub, only its

more technology advanced and agile than it was.

Source: JLL Research

Chart of the week: August 3, 2015

0

20,000

40,000

60,000

80,000

100,000

WayneCounty, MI

MacombCounty, MI

Kent County,MI

OaklandCounty, MI

OttawaCounty, MI

2013 Jobs 2014 Jobs

Modern space requirements spur new warehouse

construction

Detroit

• Warehouse construction has been developers focus of late, representing about two thirds of construction activity.

Of the product currently under construction, 511,000 square feet is being built speculative while 340,000 square

feet is set for owner-occupancy and the remaining 81,000 square feet is build to suit. Looking forward, a focus on

quality space and convenient location, rather than price, will drive location decisions for Metro Detroit’s industrial

tenants.

Source: JLL Research

Chart of the week: August 17, 2015

0.0

0.4

0.8

1.2

Completions YTD Under Construction Pipeline

m.s.f

Advance industries accelerate, leading jobs revival

Detroit

• Metro Detroit’s economic recovery is relying largely on the marrying of its industrial past to a digital future. Detroit

has the fourth largest advanced industries sector among the largest 100 metropolitan areas in the U.S., contributing

279,350 jobs to the regional economy and representing 14.8 percent of total employment. Due to a paradigm shift

in the market, landlords and tenants are finding creative ways to house the growing and adapting advance

industries in everything from trendy loft style offices to high tech manufacturing facilities.

Source: JLL Research

Chart of the week: August 24, 2015

010,00020,00030,00040,00050,00060,00070,000

Motor VehicleParts

Manufacturing

Architectural,Engineering, andRelated Services

Motor VehicleManufacturing

ComputuerSystems Design

and RelatedServices

Managements,Scientific and

TechinicalConsultingServices

Total jobs by

New Center: Detroit’s next hot neighborhood

Detroit

• The New Center area has the “bones” that many developers look for. Its main thoroughfare is West Grand

Boulevard - home to the former General Motors long-time headquarters. Meanwhile, the Fisher building is 82

percent full, with tenants including the Fisher Theater - a 2,000 seat site for pre-Broadway production and

Broadway touring companies. HFZ and Redico paid $12.2 million for the Fisher Building with plans to convert the

office building into a multifamily project. Peter Allen & Associates is expected to begin on their $14 million project in

the fall, with completion by the time the M-1 Rail project is completed in 2017.

Source: JLL Research

Chart of the week: August 31, 2015

Fisher Kahn building sold for

$12.2 million at auction to HFZ

Capital of New York and Redico

of Detroit

Central Detroit Christian Community

Development Corporation will invest $10.2

million to redevelop the donated Casamira

Apartments building in Detroit.

Former General Motor

headquarters. The building, now

called Cadillac Place, houses state

offices.

The St. Regis. is currently under

contract to be sold to a local

investor for $10 million.

Grand Boulevard is the last

stop on phase 1 of the

$170 million M1 Rail.

Amtrak; Detroit to

Chicago in 6 hours

or less

Peter Allen &

Associates

are planning a

$14 million

mixed use

development

Detroit

• Last week was proof Detroit’s CBD continues to sizzle. Bedrock announced it paid $40 million for the Book Tower

skyscraper on Washington Boulevard, which is intended for mixed-use; Lear Corporation purchased a 50,000

square foot building in Harmonie Park for its satellite headquarters; and AT&T is currently shopping a sale-lease

back for its 461,000 square foot Michigan headquarters. With downtown’s Class A vacancy at 9.6 percent, rents

north of $22.00 per square foot and ever-increasing demand, one must ask how much longer before the shovels hit

the dirt?

Source: JLL Research

Chart of the week: September 7, 2015

Lear Corps

Satellite

Headquarters

AT&T is seeking a

sale-leaseback for

its 461,000

square foot

headquarters

The Book Tower is

being converted into

$140 million mixed-

used development

New Red Wing

Arena

A $70 million planned

development in Brush Park

would include 337 residential

units and retail space.

District Detroit, The $650

million development is to be

funded with a mix of $365.5

million in private investment and

an estimated public investment of

$284.5 million.

Smart money is investing in Downtown Detroit

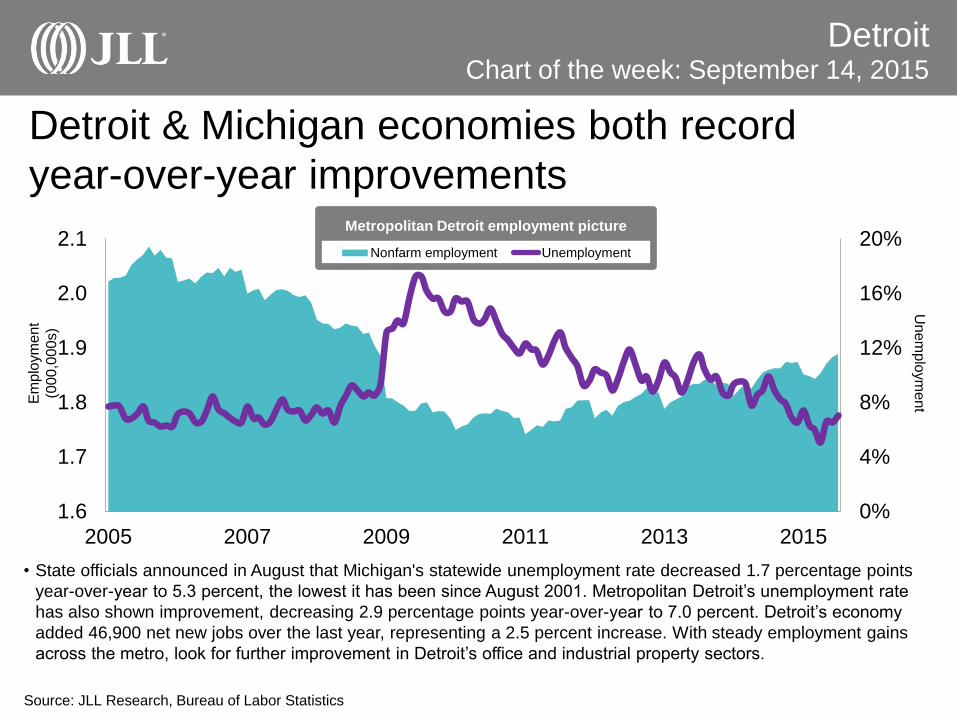

Detroit & Michigan economies both record

year-over-year improvements

Detroit

• State officials announced in August that Michigan's statewide unemployment rate decreased 1.7 percentage points

year-over-year to 5.3 percent, the lowest it has been since August 2001. Metropolitan Detroit’s unemployment rate

has also shown improvement, decreasing 2.9 percentage points year-over-year to 7.0 percent. Detroit’s economy

added 46,900 net new jobs over the last year, representing a 2.5 percent increase. With steady employment gains

across the metro, look for further improvement in Detroit’s office and industrial property sectors.

Source: JLL Research, Bureau of Labor Statistics

Chart of the week: September 14, 2015

0%

4%

8%

12%

16%

20%

1.6

1.7

1.8

1.9

2.0

2.1

2005 2007 2009 2011 2013 2015

Nonfarm employment Unemployment

Metropolitan Detroit employment picture

Em

plo

ym

ent

(000

,00

0s)

Un

em

plo

ym

ent

Office construction is on the upswing in Metro

Detroit

Detroit

• Detroit’s office development is beginning to move beyond the rehabbing of old buildings. Increasing rents, positive

absorption and limited availability are determining factors needed to give developers the confidence to start new

construction. In the third quarter of 2015, 897,825 square feet was under construction, up from 669,522 square feet

in the previous quarter. As of now, new construction is primarily owner-occupied and build to suit, however, we

project speculative construction will increase as inventory continues to tighten across the submarkets.

Source: JLL Research

Chart of the week: September 21, 2015

0

200,000

400,000

600,000

800,000

1,000,000

2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3

Square feet of office product under construction

Landlords are beginning to refinance downtown

properties

Detroit

• Downtown Detroit is beginning to show its credit worthiness to the capital markets. Just this past week, a deal

closed for the First National Building, owned by a Dan Gilbert affiliated entity, to get a $70 million loan, which was

brokered by Bernard Financial. It was purchased in August 2011 for $8.1 million by 660 Woodward Associates. It is

the largest commercial mortgage-backed securities loan on a Detroit building since Bedrock and Meridian Health

purchased the former Compuware Corporation headquarters building last year for $142 million. The pie chart

represents the aggregate value of refinancing activity in the CBD. Source: JLL Research, Real Analytics

Chart of the week: September 28, 2015

First National Building

One Woodward Building

1001 Woodward

fmr United Way Bldg

719 Griswold

$51.5 million

$37 Million $41 Million

$10.1

Million

$70 Million

Aggregate Value of refinancing in CBD 2013-2015

Urban submarkets continue to outperform

suburban submarkets

Detroit

• Detroit’s submarkets are in the midst of a tug of war. In the urban submarkets, the average asking rent currently

stands at $20.08 per square foot, up 5.1 percent from this time last year. Meanwhile, vacancy has steadily

decreased year-over-year from 17.9 percent to 14.4 percent today. In the suburban submarkets, although rents are

improving, they are appreciating at a slower pace than they are downtown. Suburban rents have increased 3.8

percent year-over-year to $17.91 per square foot.

Source: JLL Research

Chart of the week: October 5, 2015

$15

$18

$21

0%

15%

30%

Q3 2012 Q3 2013 Q3 2014 Q3 2015

Urban Rents Suburban Rents Urban Vacancy Suburban Vacancy

Philanthropy’s impact on Grand Rapids real estate

Detroit

• Grand Action, a non-profit organization made of the city’s wealthiest benefactors, led the way on three major

projects that transformed downtown Grand Rapids. The three projects were the Van Andel Arena, DeVos Place

Convention Center and, most recently, the Grand Rapids Downtown Market. Now investors are taking notice; with

the perfect scenario of high rents, high occupancy and low interest rates, waves of new investments are occurring

across the region. Look for new construction to begin answering the demand for heavy industrial and downtown

Class A office. Source: JLL Research

Chart of the week: October 12, 2015

100,000

300,000

500,000

Q3 2015Q2 2015Q1 2015Q4 2014Q3 2014

Office product under construction (s.f.)

Landlords push rents as quality blocks dwindle

Detroit

• Asking warehouse/distribution rates remained flat in the third quarter of 2015, averaging $4.30 per square foot. The

I-96 corridor submarket had the highest average rental rate at $5.74 per square foot while the Detroit submarket

came in lower at $2.97 per square foot. R&D and flex rates are double that of warehouse/distribution in almost all

submarkets, and continue to fluctuate significantly among the geographic market sectors. Rates range as high as

$12.03 per square foot in the Washtenaw County submarket to as low as $6.06 per square foot in the City of

Detroit submarket.

Source: JLL Research

Chart of the week: October 19, 2015

7%

9%

11%

13%

15%

17%

19%

21%

$3.80

$4.00

$4.20

$4.40

2010 2011 2012 2013 2014 2015

Asking rents Total availability

Detroit is becoming a premier logistics hub

Detroit

• Detroit is on the verge of becoming an advanced high-tech logistics district. The state is currently researching a

$1.6-billion plan to transform Detroit into the logistics capital of the Midwest. With the Gordie Howe International

Bridge opening up a new supply route across the U.S-Canadian border, local developers of industrial space are

hoping shipping companies or other delivery businesses will choose Detroit as its gateway to and from the Midwest

and parts of Canada. The completion of three projects is considered necessary for a new Detroit logistics district to

operate efficiently: the Gordie Howe bridge, the Detroit Intermodal Freight Terminal and the Continental Rail

Gateway. Source: JLL Research, Bureau of Labor Statistics

Chart of the week: October 26, 2015

-40

-20

0

20

40

2010 2011 2012 2013 2014 2015

Trade,Transportation & Utilities ManufacturingOther Services Mining, Logging & Construction

Industrial Employment trends (12-month change, 000s)

Community development incentives encourage

growth

Detroit

• Smart developers are taking advantage of incentives designed to decrease risk and increase returns. Many new

projects are being financed using creative capital stacks that include traditional sources and nontraditional sources

such as forgivable loans, tax credits, non-profit program-related investments and crowdfunding. The State of

Michigan is playing its part in these capital stacks by awarding over $13.5 million this year to development projects

creating over 300 permanent full-time equivalent jobs. The result is economic growth and a win-win for the people

of Detroit and its real estate market. Source: JLL Research, State of Michigan

Chart of the week: November 2, 2015

$0

$30

$60

CasamiraDetroit

1215Griswold

KWAResidential

HMVentures

1145Griswold

Street

TrailHeadRO LLC

Woodwardand Erskine

LLC

Total project investment Projected state award amount($M)

Michigan Strategic Fund’s largest investments in metro Detroit

Strong jobs growth may encourage rate hike

Detroit

• Total nonfarm employment in metro Detroit stood at 1,950,500 in September 2015, up 46,400 or 2.4 percent over

the year. During the same period, the national job count increased 1.9 percent. All of this has implications for the

direction of monetary policy. Indeed, traders are now pricing in a 70% likelihood that the Federal Reserve will lift

rates in December, which would be the first such hike since June 2006. An initial rate hike from the Fed would

signal the end of extremely loose, zero-interest rate policy, which it introduced in December 2008 in its effort to

stimulate the economy out of the financial crisis. Source: JLL Research, Bureau of Labor Statistics

Chart of the week: November 9, 2015

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

2010 2011 2012 2013 2014 2015

Detroit United States

Job growth (12-month change): United States vs. Detroit

Detroit’s strategic advantage is its location

Detroit

• With the introduction of the new Gordie Howe International Bridge, the realm of business and opportunities to be

created or offered have exponentially increased. Michigan officials are researching a $1.6-billion plan that could

make Detroit the new logistics capital of the Midwest. In addition to the major economic growth this would offer, a

potential of 22,000 long-term jobs in Michigan with up to 8,000 right here in Detroit could be created. The map

above highlights Detroit’s location advantage and company’s ability to reach 50 million plus people in a drive time

of six hours. Source: JLL Research

Chart of the week: November 16, 2015

Rings represent miles and drive times

360 Miles

240 Miles

120 Miles

Recent job numbers point to fed rate hike

Detroit

• According to the most recent estimates from the Bureau of Labor Statistics, total nonfarm employment in Detroit

stood at ~2.0 million payrolls, representing an annualized increase of 38,700 jobs or 2.0 percent. Meanwhile,

unemployment decreased 1.6 percentage points year-over-year to 6.3 percent. Nationally, total nonfarm payroll

employment increased by 211,000 in November, and the unemployment rate was essentially unchanged at 5.0

percent. The latest jobs data, easily meets the targets laid out by the central bank as prerequisites for a rate hike,

economists said.

Source: JLL Research, Bureau of Labor Statistics

Chart of the week: December 07, 2015

0%

4%

8%

12%

16%

20%

1,550,000

1,650,000

1,750,000

1,850,000

1,950,000

2,050,000

2,150,000

2005 2007 2009 2011 2013 2015

Nonfarm employment

Unemployment

Ann Arbor, six square miles surrounded by reality

Detroit

• Whether researching the Ann Arbor market using the latest quarterly office report or just sitting in a café on Friday

afternoon, one will quickly come to the conclusion that Ann Arbor is six square miles surrounded by reality. The

University of Michigan attracts a worldly and diverse student body that is converting educational training into

disruptive start-ups. Class A rents towards $35.00 per square foot while pushing Class A vacancy to zero.

Suburban Class A rents for the quarter were $25.75 per square foot, nearly 14 percent more than Detroit CBD

Class A asking rates.

Source: JLL Research

Chart of the week: December 14, 2015

$15

$25

$35

YTD 201520142013201220112010

Downtown Suburban

This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without

the prior written consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from sources generally regarded to be reliable. However, no

representation is made, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang

LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016

For More Information, Please Contact

35

Aaron Moore

Analyst, Great Lakes Research

+1 248 581 3308

Larry Emmons

Managing Director

+ 1 248 581 3388

Andrew Batson

Manager, Great Lakes Research

+1 216 937 4374

About JLL

JLL (NYSE: JLL) is a professional services and investment management firm offering specialized real estate services to clients seeking increased value by owning, occupying and

investing in real estate. A Fortune 500 company with annual fee revenue of $4.7 billion and gross revenue of $5.4 billion, JLL has more than 230 corporate offices, operates in 80

countries and has a global workforce of approximately 58,000. On behalf of its clients, the firm provides management and real estate outsourcing services for a property portfolio of

3.4 billion square feet, or 316 million square meters, and completed $118 billion in sales, acquisitions and finance transactions in 2014. Its investment management business, LaSalle

Investment Management, has $57.2 billion of real estate assets under management. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For

further information, visit www.jll.com.