Embed Size (px)

Citation preview

Investing In Melbourne Property

Disclaimer

This presentation is not to be considered legal or

financial advice. The advice provided on this presentation

is general advice only. It has been prepared without

taking into account your objectives, financial situation or

needs. Before acting on this advice you should consider

the appropriateness of the advice, having regard to your

own objectives, financial situation and needs.

Investing In Melbourne Property

• Why Melbourne?

• About Melbourne

• Finance

• Tax

• Legal

• Visas

• Property Management

• The Purchase Process

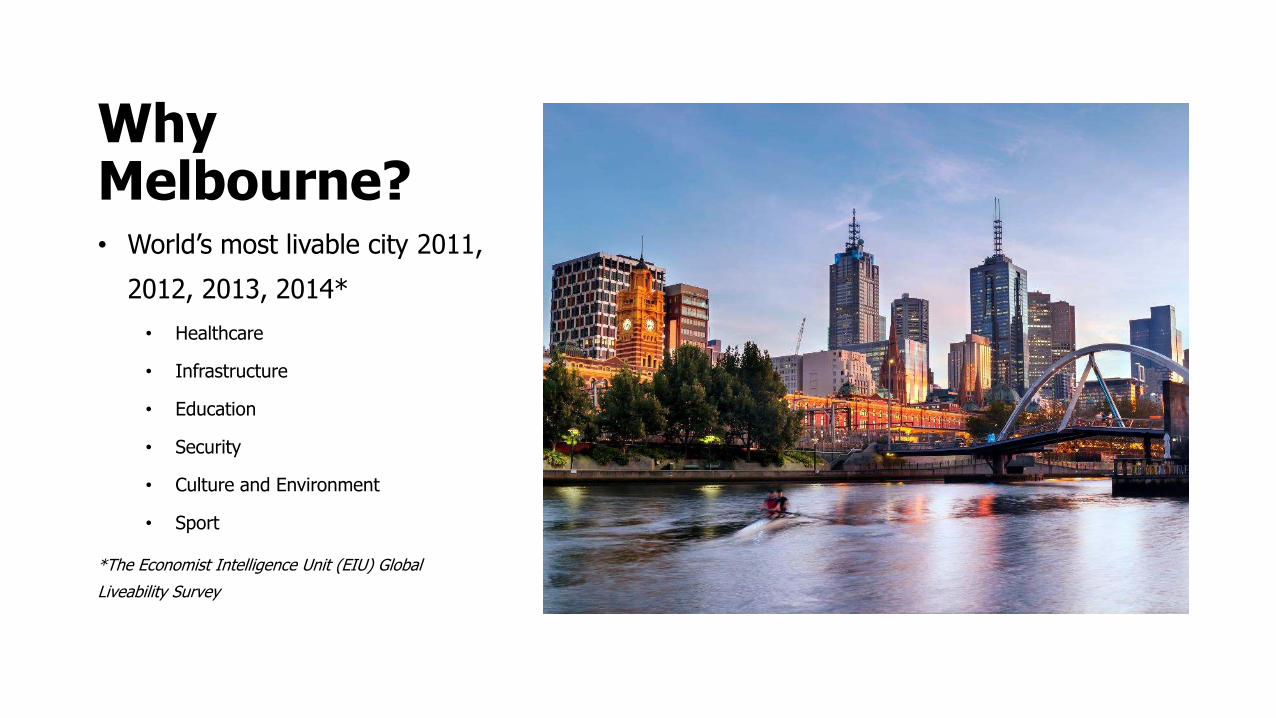

Why Melbourne?• World’s most livable city 2011,

2012, 2013, 2014*

• Healthcare

• Infrastructure

• Education

• Security

• Culture and Environment

• Sport

*The Economist Intelligence Unit (EIU) Global

Liveability Survey

About Melbourne• Located in the state of Victoria

• Most densely populated state in

Australia

• Second largest city in Australia

(4.17 million people)

• Over 75% of the state live in

Melbourne city

• 66% of Melbourne is Australian-

born

About Melbourne• Fastest growing area in Australia

• 10.5% population increase from 2012-

2013

• Districts surrounding Melbourne’s CBD

grew by 15%

• Melbourne growing faster than Sydney

over the past decade

• Over 65,000 new permanent residents

to Victoria a year (2011-2012)

Economy• Victoria has the second largest

economy in Australia

• Accounts for 25% of the country’s

GDP

• Largest income sectors are finance,

insurance and property

• Largest single employer is

manufacturing

• Fastest growing sector is the service

industry

Education• Melbourne University - oldest

university in Australia

• Monash University – largest

enrolment of nearly 56,000

students

• 30% of student population are

International students

• Over 200,000 international students

in Victoria

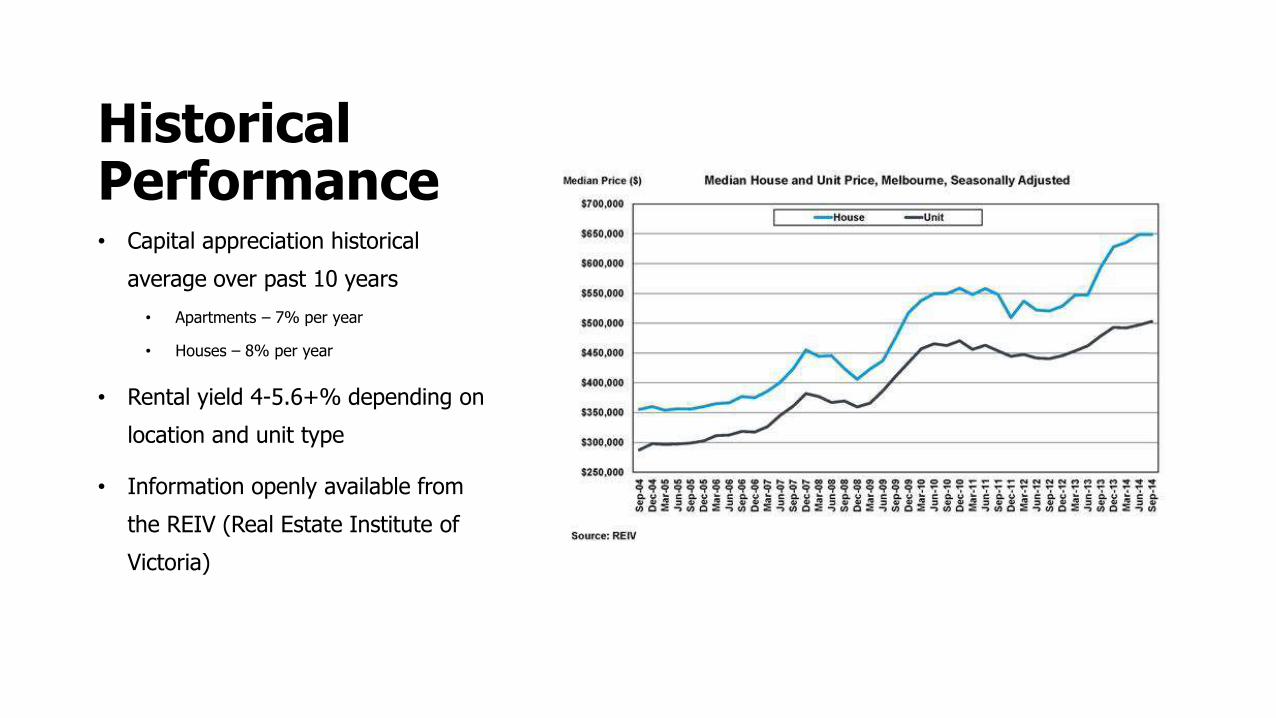

Historical Performance• Capital appreciation historical

average over past 10 years

• Apartments – 7% per year

• Houses – 8% per year

• Rental yield 4-5.6+% depending on

location and unit type

• Information openly available from

the REIV (Real Estate Institute of

Victoria)

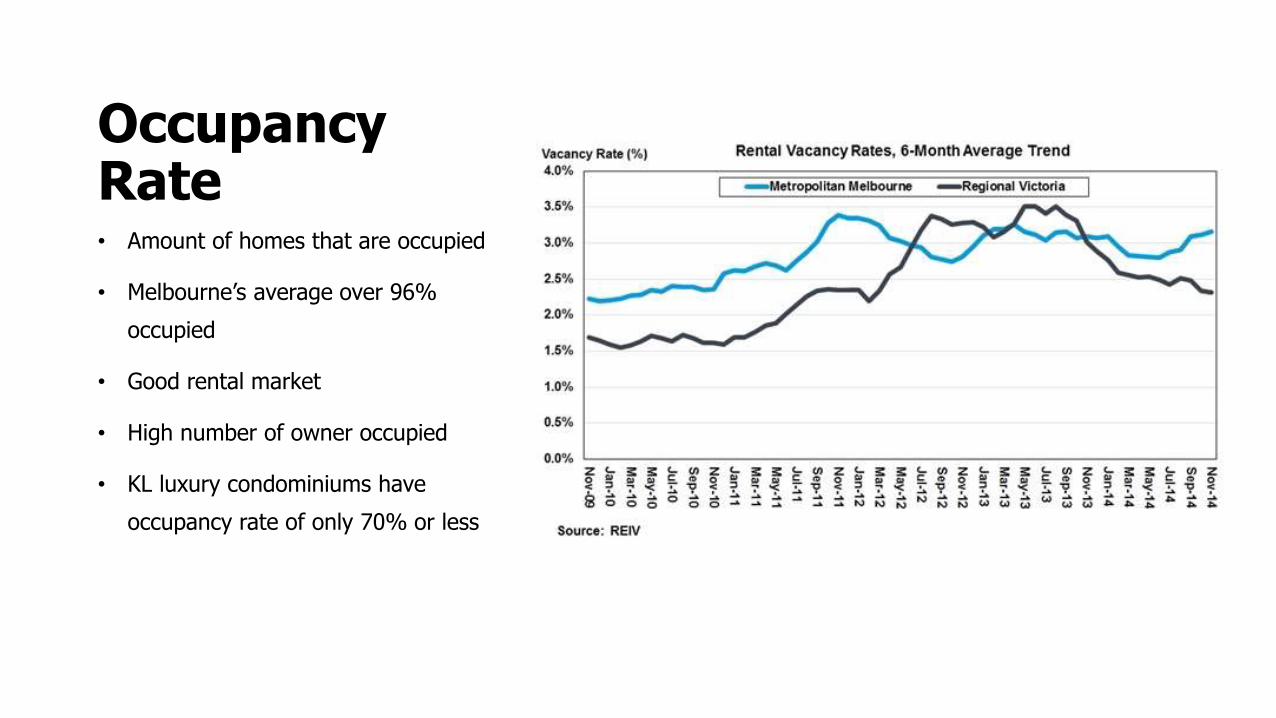

Occupancy Rate• Amount of homes that are occupied

• Melbourne’s average over 96%

occupied

• Good rental market

• High number of owner occupied

• KL luxury condominiums have

occupancy rate of only 70% or less

Regulation• 10% down payment held in a trust

• By Australian regulation, this money

can’t be touched by the developer

• Upon settlement, this 10% is

transferred to the bank with interest

gained*

• 70% of units must be sold before

developer’s bank loan kicks in

Financing• Local loans allow maximum of 70%

financing

• Australian dollar loans allow 80% financing

• Australian banks can’t discriminate on age

• Current interest rate is the lowest for over

50 years

• Australian dollar weakened with the Ringgit

against the US Dollar

• Interest only loans for up to 15 years

Tax Benefits For Foreigners• Depreciation of fixtures and fittings

over 5 years, i.e. light fittings, blinds,

cupboards, etc.

• Claim property inspection as tax

deductibles (air ticket,

accommodation, food, transport etc.)

• Borrowing expenses can be claimed

as a tax deductible

• Used to offset your rental income

• Accrue tax credits if you eventually

move to Australia

Stamp Duty Savings• State of Victoria has stamp duty

incentives for buying new

properties

• Encourage new developments in

the state

• Stamp duty is proportional to

construction completion

• Off-the-plan projects, stamp duty is

on land value only

Fees• Body corporate

• Similar to management fee in Malaysia

• Used to maintain the building or area

that you live in

• Paid by the home owner

• Council fees

• Fees to offset public services

• Waste collection and disposal services

for your neighborhood

• Maintain parks and gardens

• Roads and planning

Conveyancing

• Conveyancing is the process of transferring ownership of a

legal title of land (property) from one person or entity to

another

• E.g. from developer to purchaser

• Conveyancers don’t necessarily have to be lawyers but

usually are

• Prepare, clarify and lodge legal documents – e.g. contract

of sale, memorandum of transfer

• Research the property and its certificate of title – check for

easements, type of title and any other information that

needs addressing

• Put the deposit money in a trust account

• Calculate the adjustment of rates and taxes

• Settle the property – act on your behalf, advise you when

the property is settled, contact your bank or financial

institution on when final payments are being made

• Represent your interest with a vendor or their agent

Australian Visas• You don’t need a visa to buy

Australian property

• FIRB application is required

• Buying one property does not

qualify you for a residency

• Buying multiple properties to

form a business may qualify

for a business visa

Australian Visas• Foreigners must sell their property

back to a resident

• Choose locations where locals want to stay

• Foreigners can only buy new

property, not sub sale

• Permeant residents qualify for first

home buyers grant

• Permanent residents can sell and

buy property to anyone

Property Management• Advertise your property for rent

• Show your unit to potential tenants

• Shortlist and filter tenants

• Inspect your unit for defects upon

receiving from the developer

• Collect rental

• Pay any fees from rental

• Organize for fixes on your unit

• Typically 7% of rental is charged as

their fees

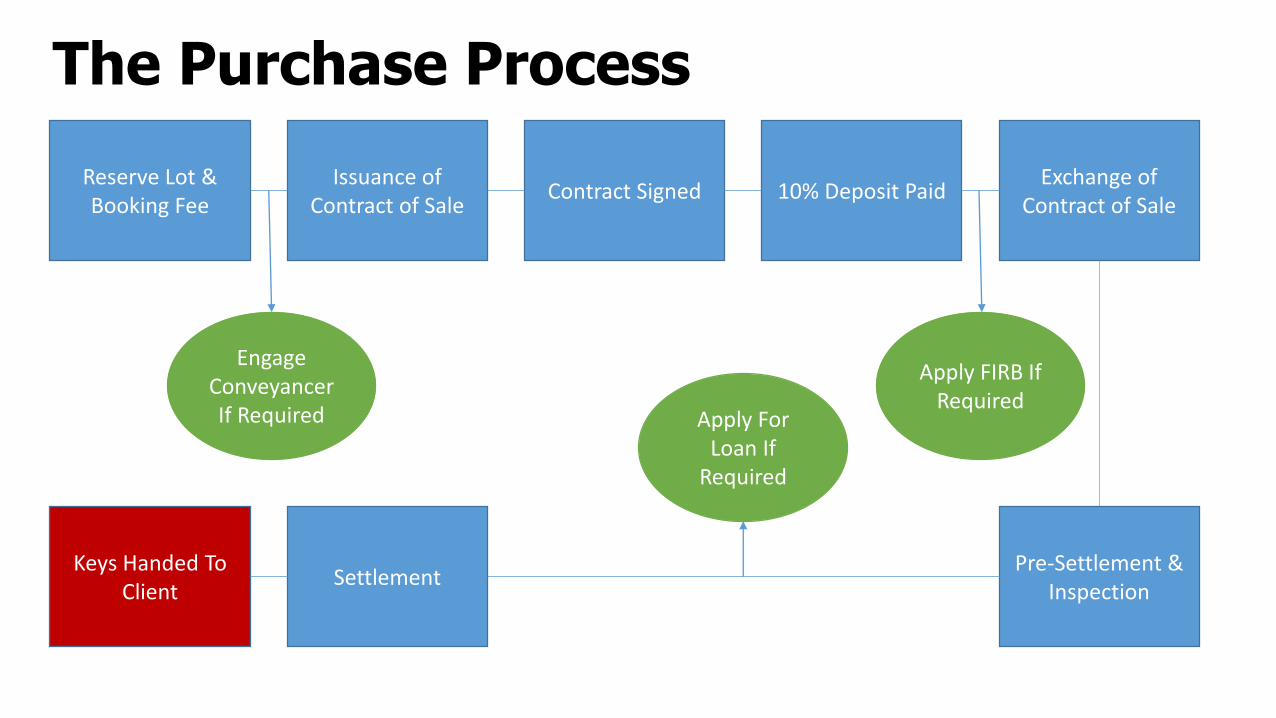

Reserve Lot & Booking Fee

Issuance of Contract of Sale

Contract Signed 10% Deposit PaidExchange of

Contract of Sale

Pre-Settlement & Inspection

SettlementKeys Handed To

Client

Engage Conveyancer If Required

Apply FIRB If Required

Apply For Loan If

Required

The Purchase Process

The Purchase Process

• Purchaser pays booking fee

• Within 7 days of paying booking fee:

• The Sales and Purchase Agreement (SPA) is signed and

the 10% down payment is transferred to a trust account

• Legal fees (if any) are paid

• Apply FIRB if required

• 3-6 months before the project is completed loan

application process begins

• Pre-settlement and inspection of the property

• Upon settlement date the remainder down payment is

collected (10-30% depending on loan margin financing)

plus stamp duty and transferred over to the same trust

account as mentioned above

• Stamp duty is paid on top of the down payment amount

and varies depending on size and location of the property

• The loan can be settled externally by the client or with

a mortgage house or partner banks both locally or

overseas

• Keys are collected by purchaser or property manager

Thank YouFor more information on investing in Australian property, please contact

William Lee at:

+6 018 2388 972