Embed Size (px)

Citation preview

Colliers Radar

Asia Pacific Property Research 14 November 2016

Asia Pacific: the dragons rise anew Prospects improving in China and Hong Kong; time to look again at Singapore

Andrew Haskins Executive Director | Research | Asia

The outcome of the US presidential

election raises challenges for Asia.

However, Chinese growth remains high

and a financial crisis is unlikely, while

growth in Hong Kong is improving. The

brighter outlook in these markets should

boost office property, as firm investment

demand suggests, although residential

property faces risks. Singapore's long-

run attractions outweigh near-term

pressure in the office market. Australia's

economy is buoyant, but the positive

story is well-known. Global investors

and occupiers should stay focused on

China and look again at Singapore.

Executive Summary The economic environment in Asia is improving. China's

growth has beaten forecasts recently, and should remain

firm. Given sound national finances and a reasonably

healthy banking system, we think a financial crisis is

unlikely, although a decline in the residential market is

possible. In Hong Kong growth has also surprised on the

upside, office rents are still rising, and Chinese interest is

high. This situation explains the territory's rise to the

second-ranked city investment market in Asia Pacific.

In Singapore growth has been slowing, and rising supply

has weighed on property markets. However, the country

enjoys good governance and high transparency, and we

think it will continue to attract institutional investors

looking for stable long-term returns. Australia's economy

remains buoyant, driving strong rent growth in Sydney

and Melbourne. However, this story is well-known and in

any case there is a growing shortage of property stock.

Donald Trump's US election victory raises challenges for

Asia, including a possible hit to confidence and growth

as well as tariffs on imports. Uncertainty has risen for

China in particular and this must temper our optimism

about improving near-term prospects. Mr Trump's

policies may prove either expansionary or contractionary

for the US economy; there are arguments both ways.

However, if US growth ultimately suffers under Mr

Trump, US interest rates may only rise very gradually

and the dollar may fall. This outcome would support

Hong Kong property assets, since it would mean that

negative real interest rates persist. However, dollar

weakness would hurt Asian exporting nations, notably

Japan where the dull economy and yen strength have

already depressed property investment volumes.

Real though the risks are, the US election outcome

should not blind global property investors and occupiers

to the fact that current economic developments in much

of Asia Pacific are positive. Besides, we expect the

combination of Mr Trump's victory and Brexit in the UK to

serve as a reminder of the potential for shocks in

developed as well as emerging markets, and so mitigate

political and economic concerns about the region.

From an investment perspective, Hong Kong looks good

in the near term. Shanghai and Beijing have appeal if

one looks past low near-term rent growth due to rising

supply. Singapore's 3.5% net yield and long-run

strengths outweigh falling near-term rents. India has high

long-run growth potential and deserves closer attention.

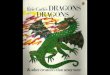

* Average for all Hong Kong; figures in brackets are for Hong Kong Island. ¹ Singapore figures are for CBD. ² Gross and net yields are very similar

in India. ³ Australia: we show gross yields unadjusted for incentives. Source: Colliers International, Bloomberg

Figure 1: Summary of key Asia Pacific urban prime grade office property markets

City Rent growth (2016-2019 avg pa)

City avg. vacancy (end-3Q 2016)

City avg. vacancy (end-2019 est.)

Net oper. income yld

10 year bond yld

Spread

Hong Kong* 4.0% 3.3% 6.2% 3.8% (2.5%) 1.23% 2.6% (1.3%)

Singapore¹ -2.1% 3.7% 8.4% 3.5% 2.11% 1.4%

Shanghai 1.6% 9.8% 10.3% 4.0% 2.83% 1.2%

Beijing -0.2% 7.6% 10.9% 4.5% 2.83% 1.7%

Tokyo -2.4% 3.8% 6.0% 3.6% -0.04% 3.6%

Mumbai (CBD)² 1.3% 7.0% 9.0% 6.4% 6.72% -0.3%

Mumbai (BKC)² 2.2% 14.0% 12.0% 8.3% 6.72% 1.6%

Sydney³ 7.2% 5.6% 3.9% 5.8% 2.56% 3.2%

Melbourne³ 4.3% 7.0% 5.1% 5.5% 2.56% 2.9%

3 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

Contents

Executive Summary ............................ 2

APAC economic situation .................. 5

Asia unpopular, not Asian property ............ 5

Economic prospects strong or improving across much of APAC ................................ 6

Trump's presidency threatens to hold down growth in Asia ............................................. 6

China ..................................................... 8

Real GDP growth remains high and steady 8

Debt is high, but a financial crisis is unlikely ................................................................... 8

Prospects for commercial property favourable ................................................ 10

China now the second-ranked country investment market in APAC ..................... 11

Residential market remains at risk, but recent cooling is encouraging ................... 12

Hong Kong ......................................... 14

Prospects turning brighter ........................ 14

Island office rents and investment market strong, Kowloon weaker ........................... 16

Hong Kong now the second-ranked city investment market in APAC ..................... 16

Risks: retail sector and long-run outlook for residential property ................................... 17

Singapore ........................................... 19

Economic growth has been slowing ......... 19

Office property market under pressure in the near term ............................................ 19

4 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

Long-run prospects brighter ..................... 20

Time to look at Singapore again .............. 21

Australia.............................................. 22

Good times keep rolling for the Lucky Country .................................................... 22

Office markets still very strong in Sydney and Melbourne ......................................... 24

Investment in Australia driven by Asia, especially China....................................... 25

Core markets still attractive, even if investment story is well-known ................ 25

Japan ................................................... 26

Economy only ticking away ...................... 26

Weakening outlook for Tokyo office property market ...................................................... 26

Investment volumes declining .................. 27

Japanese property: dull near-term outlook, brighter in the long term ........................... 27

India ..................................................... 28

Economic outlook remains positive, supported by new policy initiatives........... 28

Office leasing market firm: focus on Bangalore and Hyderabad ....................... 29

Medium-term investment opportunities substantial ............................................... 29

Time for investors to put India on their radar screens .................................................... 30

US election: impact on Asia ............. 31

Trump's victory surprises global markets, but less so than Brexit ............................. 31

Expansionary and contractionary: different views about Trump's economic policies ... 31

Slow US interest rate rises would support Hong Kong property ................................. 32

USD weakness would hurt Japan and other Asian exporting nations ............................ 32

Direct implications for Asian property markets are limited ................................... 32

Trump and Brexit surprises should lower concern about Asia over time ................... 32

5 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

APAC economic

situation

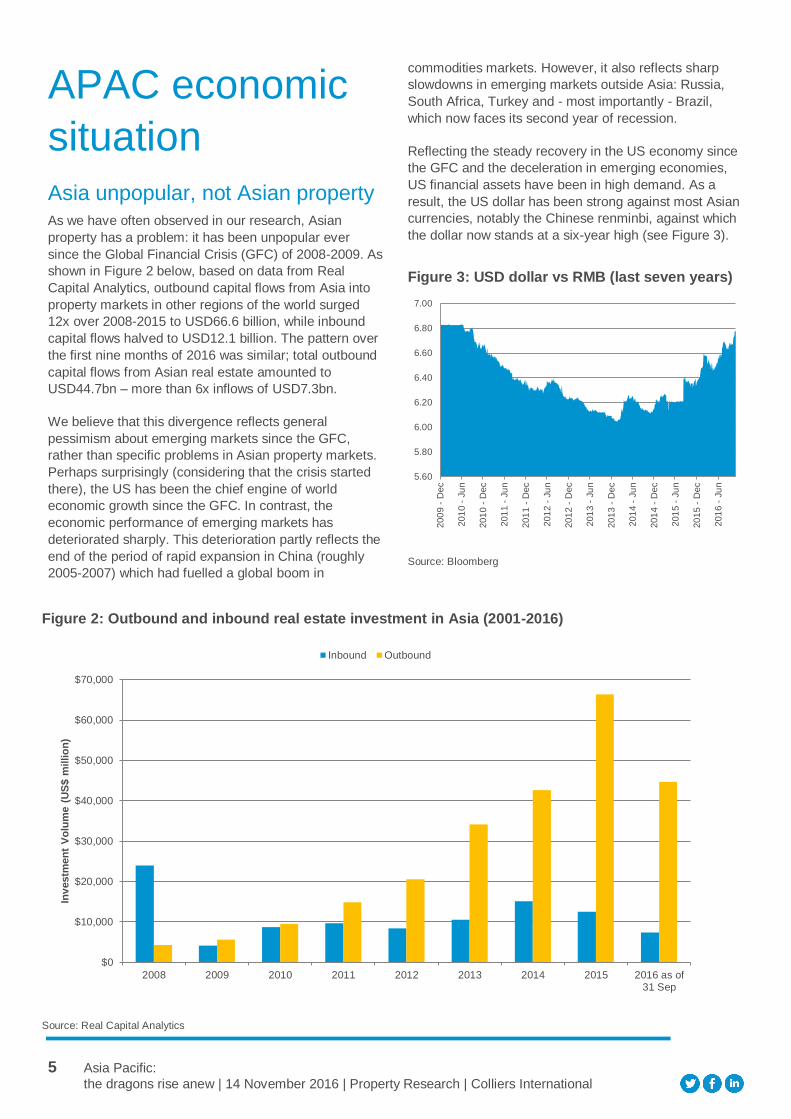

Asia unpopular, not Asian property As we have often observed in our research, Asian

property has a problem: it has been unpopular ever

since the Global Financial Crisis (GFC) of 2008-2009. As

shown in Figure 2 below, based on data from Real

Capital Analytics, outbound capital flows from Asia into

property markets in other regions of the world surged

12x over 2008-2015 to USD66.6 billion, while inbound

capital flows halved to USD12.1 billion. The pattern over

the first nine months of 2016 was similar; total outbound

capital flows from Asian real estate amounted to

USD44.7bn – more than 6x inflows of USD7.3bn.

We believe that this divergence reflects general

pessimism about emerging markets since the GFC,

rather than specific problems in Asian property markets.

Perhaps surprisingly (considering that the crisis started

there), the US has been the chief engine of world

economic growth since the GFC. In contrast, the

economic performance of emerging markets has

deteriorated sharply. This deterioration partly reflects the

end of the period of rapid expansion in China (roughly

2005-2007) which had fuelled a global boom in

commodities markets. However, it also reflects sharp

slowdowns in emerging markets outside Asia: Russia,

South Africa, Turkey and - most importantly - Brazil,

which now faces its second year of recession.

Reflecting the steady recovery in the US economy since

the GFC and the deceleration in emerging economies,

US financial assets have been in high demand. As a

result, the US dollar has been strong against most Asian

currencies, notably the Chinese renminbi, against which

the dollar now stands at a six-year high (see Figure 3).

Figure 3: USD dollar vs RMB (last seven years)

Source: Bloomberg

5.60

5.80

6.00

6.20

6.40

6.60

6.80

7.00

200

9 -

Dec

201

0 -

Ju

n

201

0 -

Dec

201

1 -

Ju

n

201

1 -

Dec

201

2 -

Ju

n

201

2 -

Dec

201

3 -

Ju

n

201

3 -

Dec

201

4 -

Ju

n

201

4 -

Dec

201

5 -

Ju

n

201

5 -

Dec

201

6 -

Ju

n

Figure 2: Outbound and inbound real estate investment in Asia (2001-2016)

Source: Real Capital Analytics

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 as of31 Sep

Inv

estm

en

t V

olu

me (

US

$ m

illio

n)

Inbound Outbound

6 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

Economic prospects strong or improving across much of APAC

Is Asia's general unpopularity still justified? As we shall

argue in detail in this report, we believe that economic

prospects for many countries in the Asia Pacific region

have improved recently. The two large emerging Asian

economies, China and India, continue to grow at 6.5-

7.5% p.a.; and so far this year growth has accelerated

slightly in both markets. Strong secular growth is likely to

continue in both countries for some years.

Regarding China, concerns about financial stability

persist. These concerns are justifiable, considering that

the country's debt/GDP ratio stands at close to 250%,

and that growth in total social funding (essentially

aggregate credit growth) is running at 12% per year or

higher; it is 16% on some economists' definitions. Over

the long run, China faces a challenge in weaning itself

off a credit-driven growth model driven by high

investment. However, in the near term, given strong

national finances and a banking system which is still

reasonably healthy overall, we see the probability of a

financial crisis as small. The chance of a significant

correction in residential property prices appears higher,

although recent signs of cooling in the market are

encouraging.

Hong Kong has also recorded positive economic

surprises recently. Real GDP growth has picked up,

goods exports have increased, and business sentiment

has improved. Historical evidence suggests that

business confidence in Hong Kong has been closely

correlated with the performance of office rents in the

territory. The recent improvement in confidence should

drive further rent increases in Hong Kong Island,

although the Kowloon market is much weaker.

Singapore’s recent economic performance has been

disappointing. GDP growth slowed sharply in Q2 2016,

and may have been negative, while manufacturing

activity contracted. However, the recent weakness is

insufficient to dent Singapore's long-established

reputation as both a highly resilient economy and a

world-class metropolis which is attractive for business.

In Australia, the economy continues to roll, and the

country has recently recorded its 100th consecutive

quarter of GDP growth. Since the end of the mining

boom, the Australian economy has been driven

increasingly by expansion in professional and services

employment in the traditionally dominant south-eastern

states of New South Wales and Victoria. This expansion

has driven strong rent growth in Sydney and Melbourne,

and looks set to go on for the next couple of years.

In contrast, Japan's economy is ticking away at a very

moderate pace. The economy has been impacted by

weaker household consumption and the strength of the

Japanese yen, which is one of the few Asian currencies

to have risen against the US dollar over most of 2016.

The lingering problems of weak aggregate demand, high

corporate debt and deflation are starting to fade into the

background. However, perhaps the biggest challenge for

Japan remains its poor demographic profile: Oxford

Economics projects an average annual decline in the

working age population of 0.8% over the next decade.

Figure 4: USD dollar vs JPY (last ten years)

Source: Bloomberg

In short, with a few exceptions, economic performance

has been improving across the Asia Pacific region

recently. The UK's vote for Brexit, i.e. departure from the

European Union, on 23 June 2016 caused a certain

shock to confidence, but this was short-lived. We would

have been in a position to express high optimism about

continuing growth prospects in the region had it not been

for the second, perhaps even greater shock to transpire

in the western world so far this year; the election on

8 November of Donald Trump as the 45th President of

the United States of America.

Trump's presidency threatens to hold down growth in Asia

Mr Trump's election victory raises challenges for Asia,

including a possible hit to US and global confidence and

growth and radical trade policies targeting China and

other countries. Uncertainty has increased for China in

particular. This must temper our optimism about

improving economic prospects for China, since it is quite

possible that the carry-over effect into 2017 of stronger

economic growth this year will be offset by the negative

impact of a combination of new tariffs on imports, weaker

US demand for Chinese goods, and a stronger US dollar

which renders Chinese exports less competitive.

60

70

80

90

100

110

120

130

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

Jul-

16

7 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

In office, it is conceivable that Mr Trump will prove rather

less radical than his policy proposals suggest. Nor is it

yet clear whether his policies will serve to boost or

depress US economic growth in the near term; there are

arguments both ways which we shall discuss further in

the final section of this report. However, if US growth

does suffer under Mr Trump, then the Federal Reserve

may only raise US interest rates very gradually over the

next few years. This would be positive for Hong Kong

property assets, since Hong Kong interest rates are

effectively tied to US rates as a result of the territory's

currency peg.

If US interest rates only rise gradually, then the US dollar

may also start to weaken after many years of strength.

This would be negative for Asia exporting nations in

general because it would reduce their trading

competiveness; this would apply not only to China but

also to Japan, South Korea and Taiwan. As it happens,

Japan has already experienced declines in property

investment volumes so far in 2016 as the combined

result of a dull economy and the strength of the

Japanese yen.

Direct medium-term implications of Mr Trump's victory

for the property markets within developing Asian

economies are more limited. As noted, China and India

are experiencing strong secular growth which is unlikely

to slow sharply for some time, despite the risks posed by

Mr Trump's presidency to Chinese trade. Investors and

large multinational occupiers should continue to be

attracted to important commercial property markets like

Shanghai regardless of who is US president. Meanwhile,

demand and supply in the Chinese and Indian residential

markets are driven largely by domestic factors such as

urbanisation, wealth levels, interest rates, lending

policies and real estate regulation which have little to do

with the US.

8 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

China

Real GDP growth remains high and steady We believe that China's real GDP will continue to

expand, albeit at a moderating pace. Real GDP looks set

to grow by at least 6.6% y-o-y over 2016, and according

to the International Monetary Fund growth should

decelerate to the 6.0-6.2% range for 2017. There was a

positive surprise in Q3 2016, in which real GDP rose by

6.7% y-o-y; this was above many economists' forecasts.

Certain economic analysts believe that Chinese

economic growth is modestly lower than the official

figures suggest. Nevertheless, it is important to

understand that GDP growth in the region of 6-7%

means that China is adding more or less the equivalent

of Switzerland to the global economy each year.

Moreover, this robust growth is increasingly being driven

by services and light industry, which now account for

57% of total GDP.

Overall fixed asset investment has been rising in China

recently, growing by 9.0% y-o-y in September 2016 after

a pick-up to 8.2% in August according to figures from the

State Council Information Office. This improvement

partly reflects stronger property investment amid surging

housing sales. However, fixed asset investment in

manufacturing also increased in September, in part

because industrial profits are rising again. Profits in

manufacturing rose by 16% y-o-y in Q3 2016, i.e. at the

fastest growth rate in two years. This growth in profits

reflected not only increasing sales, but also margin

expansion driven by rising output prices. This recovery

was vividly reflected in the first y-o-y increase in the

producer price index (PPI) in 54 months in September

2016. October showed a further 1.2% y-o-y increase in

the PPI. The pick-up in producer prices is good news for

heavy industry in particular.

Other news for industry has not been so good. Exports

from China actually weakened in September 2016. This

was because mainly global demand remained patchy,

outweighing the boost to export performance from a

weaker currency; the Chinese renminbi continues to

hover at around a six-year low versus the US dollar.

Industrial production growth therefore softened

somewhat in September.

Then again, household consumption remained robust in

Q3 2016, rising by 6.6% y-o-y in real terms; sales of

passenger cars were especially firm. The increase in

consumption reflects both strong real wage growth (up

by 6.7% y-on-y over the first three quarters of 2016) and

high government spending in the economy. Rising

consumption is, of course, one of the key explanations

for the continuing growth in the services sector, which

has outpaced growth in industry since 2012.

In the light of the recent positive developments, Oxford

Economics recently nudged up GDP growth forecast for

China to 6.7% for 2016. However, the firm believes that

the positive carry-over effect of this higher number into

next year may now be offset by the impact of the more

challenging global growth environment following the US

election, and so has kept its growth forecast for 2017

unchanged at 6.3%. Moreover, Oxford Economics

foresees a significant slowdown over the next ten years

towards real GDP growth of 5.5% as China gradually

weans itself off a model of credit-fuelled expansion.

Figure 5 below summarises key economic forecasts for

China for the next three years.

Debt is high, but a financial crisis is unlikely While persistent high economic growth has been a

positive surprise in China, this growth is being achieved

at a cost. The cost is rapidly increasing indebtedness.

The most commonly used measure of total outstanding

credit in the Chinese economy is so-called Total Social

Financing (TSF), which is a much broader measure than

simple bank lending. Over 2009-2010, in the aftermath of

Figure 5: China: Recent economic performance and key forecasts

GROWTH RATE (%) 2014 2015 2016 2017 2018 2019

Real GDP 7.3 8.9 6.7 6.3 5.9 5.7

Private consumption 8.2 7.6 7.5 6.9 6.8 6.7

Fixed investment 6.9 7.5 5.6 4.4 4.2 4.0

CPI 2.0 1.4 1.9 2.1 2.5 2.8

USD1.0 = RMB 6.16 6.28 6.62 6.91 6.75 6.54

Source: Oxford Economics

9 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

the Global Financial Crisis (GFC), the authorities allowed

TSF to expand at y-o-y rates of up to 35% in order to

stimulate the Chinese economy. Growth in TSF

decelerated over 2011 before accelerating again in the

wake of global economic stagnation in 2012 and then

slowing again in 2014-2015. However, since the start of

2016 TSF has again been expanding quite rapidly:

according to official government statistics, TSF grew by

12.5% y-o-y in September¹. Certain economic

forecasting groups make adjustments to the data and so

estimate slightly different figures. Oxford Economics

calculates figures for TSF excluding equity, adjusted for

local government loans. On this definition, y-o-y growth

in September was about 16%.

¹ Please see http://www.gov.cn/xinwen/2016-

10/18/content_5120978.htm.

Figure 6: China - bank lending and total social

financing: y-o-y change (to September 2016)

Source: Oxford Economics, CEIC

The People's Bank of China published data for TSF for

October 2016 on 11 November, just before this report

was published. On the Bank's definition, these figures

show that the y-o-y change in TSF for that month was

steady at 12.7%.

As a consequence of the continuing expansion in credit

in the economy, China's total indebtedness has reached

levels which certain observers consider excessive. One

of the commonly used yardsticks of a country's ability to

support outstanding credit in its economy is the

debt/GDP ratio. This ratio is estimated in various

different ways, with the result that there is a range of

figures for China. According to Oxford Economics, the

debt/GDP ratio in China was 250% at the end of 2016.

By the standards of emerging markets, China's debt/

GDP ratio is high. For comparison, most observers quote

a debt/GDP ratio of 66-67% for the other large, high-

growth Asian economy, namely India. In contrast, many

developed countries have higher total debt/GDP ratios.

Although again calculations vary, Japan is usually

considered to top the list with a ratio approaching 400%,

with various smaller European countries such as

Portugal and Greece not far behind.

Despite high and rising indebtedness, we believe that a

financial crisis is unlikely in China, at least for the next

few years. There are various reasons for our view.

> China runs a large current account surplus

China runs a large current account surplus, meaning that

it is not reliant on foreign capital to finance its growth.

> China has a high savings rate

In 2015, China’s economy-wide (“gross national”)

savings ratio was 48.7% of GDP in 2015, compared to

an investment ratio (“gross capital formation”) of 45.7%.

Countries with high savings rates can support rising

levels of debt.

> China's banking system looks reasonably healthy

overall

While individual banks may have problems, in our view

the Chinese banking sector as a whole is reasonably

sound. According to Oxford Economics, the loan/deposit

ratio for the Chinese banking sector at the end of Q3

2016 was 72%, compared to the level of 80-90%

traditionally considered to be prudent by UK and US

banks. Moreover, deposit intake remains strong,

meaning that the loan/deposit ratio should not

deteriorate greatly if lending continues to rise. Since

y-on-y credit growth of 16% (to use Oxford Economics'

adjusted TSF figure) is double nominal GDP growth of

7.8% for Q3 2016, non-performing loans (NPLs) must

surely be rising, and there is widespread scepticism

about the NPL ratios of around 1.5% typically reported

by Chinese banks. However, many economists believe

that the NPL problem in the Chinese banking sector is

less severe than that in India, where many banks have

been extending very low-quality loans in recent years.

Our view that a financial crisis is unlikely in China in the

near term does not mean that the country can be

complacent. As already suggested, in coming years

China needs to reduce its dependence on a credit-

fuelled growth characterised by high levels of

investment. Making the long-awaited shift away from

an investment-led economic model will push down

China's growth rates, but is necessary to prevent severe

5

10

15

20

25

30

35

40

2006 2008 2010 2012 2014 2016

Bank lending

TSF ex equity, adjusted forlocal government loans

% yoy

Bank lending and total social

Source: Oxford Economics, CEIC Data

10 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

long-run imbalances and perhaps outright crisis in the

financial system.

Fortunately, there is scope for optimism that China can

make the shift, for a number of reasons. Firstly, the

government is now aiming to increase the domestic

consumption rate: recent policies include boosting rural

incomes and higher spending on health, including

projects to provide basic medical insurance for at least

90% of the population. Secondly, reform to the "hukou"

(housing registration) system is being pushed forward in

order to allow migrant workers to access social services

in the cities where they work. Thirdly, reforms in the

financial sector are spurring more efficient use of capital,

and providing a greater range of savings instruments for

to both households and companies.

Prospects for commercial property favourable

The improving economic picture provides a favourable

background for continued expansion in commercial

property markets in China. Below we summarise recent

developments in the office property segment in China's

two most important property investment markets,

Shanghai and Beijing. For Shanghai, we predict average

annual growth in Grade A office rents of 1.6% for the

period 2016-2019, despite a significant increase in new

supply and consequent upward move in the vacancy

rate. For Beijing, we expect Grade A rents to decline by

a very modest 0.2% per year over the period 2016-2019.

Shanghai (Q3 2016)

Demand

Shanghai’s economics remained

positive, with tertiary industry growing by

11.6% y-o-y in H1 2016, according to

the city’s statistics bureau. This solid

background continued to drive demand

for Shanghai’s Grade A office space,

with net absorption rebounding to

33,700 sq metres (362,750 sq ft). The

primary contributors to demand were the

finance and professional services

sectors, and retreats by peer-to-peer

lending companies moderated in the

period. Given the background of

continuing strong economic growth and

Shanghai's status as China's

commercial hub and gateway to the

whole Yangtze River Delta region, we

expect Shanghai to remain a very

popular location for multinational

companies.

Rent

Rent increased by 2.5% q-on-q or 6.2%

y-o-y to RMB10.5 per sq metre

(USD0.14 per sq ft) per day in Q3. This

rent includes a VAT tax, which is

deductible in most cases. Consequently,

most tenants actually saw real estate

costs fall in the period. Looking forward,

we predict average annual rent growth

of 1.6% for the period 2016-2019.

Supply

A total of nearly 640,000 sq metres (6.89

million sq ft) of new supply is scheduled

for 2016. More than one-half of this new

supply will be completed in the Pudong

district. We predict a further significant

increase in new supply in 2018 to just

over 900,000 sq metres (9.69 million sq

ft) before new supply falls back in 2018.

Consequently, we predict average

annual new supply of 670,000 sq metres

(7.21 million sq ft) over the period 2016-

2018. This will be almost exactly double

average new supply over the period

2010-2015 of 340,000 sq metres (3.66

million sq ft).

Vacancy rate

The vacancy rate spiked to 9.8% in Q3

as a result of the new supply and

retreats by tenants in the peer-to-peer

lending sector. With new supply likely to

rise further in 2017 but to fall back

thereafter, we predict a vacancy rate of

10.3% for end-2019.

Beijing (Q3 2016)

Demand

Beijing's economy is growing less rapidly

than Shanghai's, but nonetheless

remains high. According to the city's

statistics bureau, real GDP growth in Q3

2016 was unchanged from Q2 at 6.7%

y-on-y. Tertiary industry growth was

7.3% in the period, versus 10.3% in

Shanghai. Multinational companies

reduced space requirements over Q3

due to tighter leasing budgets, while new

business start-ups slowed. In contrast,

demand from domestic companies and

from the IT and media sectors remained

11 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

high. New leases by IT companies alone

included Sina's lease of 9,000 sq m at

Genesis Beijing in the Lufthansa

submarket; Nvidia’s new lease of 1,800

sq m at Fortune Financial Centre in the

CBD submarket; and Symantec’s new

lease of 1,300 sq m at Oriental Plaza in

the East Chang An Avenue submarket.

Rent

Average rent remained stable, falling by

0.1% q-on-q to RMB330.8 per sq metre

per month (USD4.55 per sq ft per

month) due to new supply. We expect

rental growth to be constrained for 2016

due to new supply, and to decline by a

modest 0.2% per year over the period

2016-2019.

Supply

Total grade A office stock in Beijing grew

by 2.2% q-on-q in Q3 2016 to 5.9 million

sq metres (63.5 million sq ft). We know

that 164,000 sq metres (1.77 million sq

ft) of new supply is scheduled for Q4

alone, and that several projects have

been postponed to 2017. Looking

ahead, we predict average annual new

supply of 465,000 sq metres (5.0 million

sq ft) over the period 2016-2019. This

will be slightly more than double the

average annual new supply over the

2010-2015 period of 250,000 sq metres

(2.7 million sq ft).

Vacancy rate

The vacancy rate in Beijing increased by

1.6 percentage points q-on-q to 7.6%.

The large volume of future supply over

the next couple of years will almost

certainly push up the vacancy rate

further. We predict a vacancy rate of at

least 11.0% for end-2019.

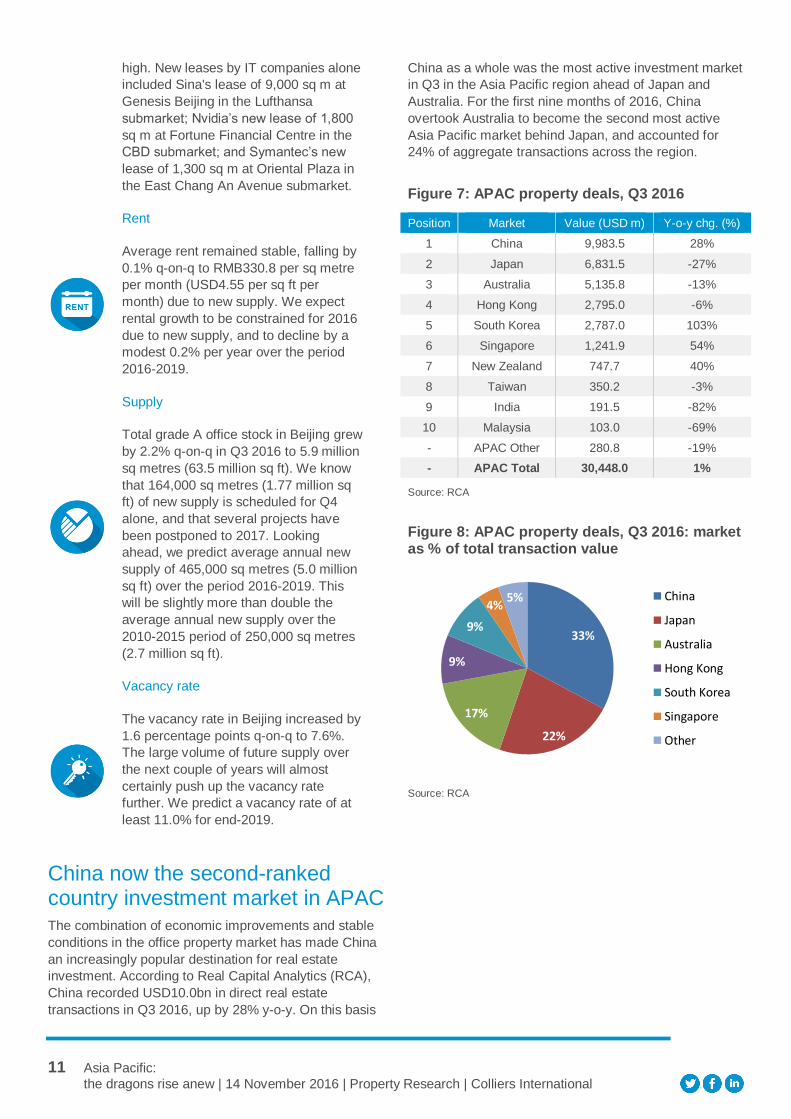

China now the second-ranked country investment market in APAC The combination of economic improvements and stable

conditions in the office property market has made China

an increasingly popular destination for real estate

investment. According to Real Capital Analytics (RCA),

China recorded USD10.0bn in direct real estate

transactions in Q3 2016, up by 28% y-o-y. On this basis

China as a whole was the most active investment market

in Q3 in the Asia Pacific region ahead of Japan and

Australia. For the first nine months of 2016, China

overtook Australia to become the second most active

Asia Pacific market behind Japan, and accounted for

24% of aggregate transactions across the region.

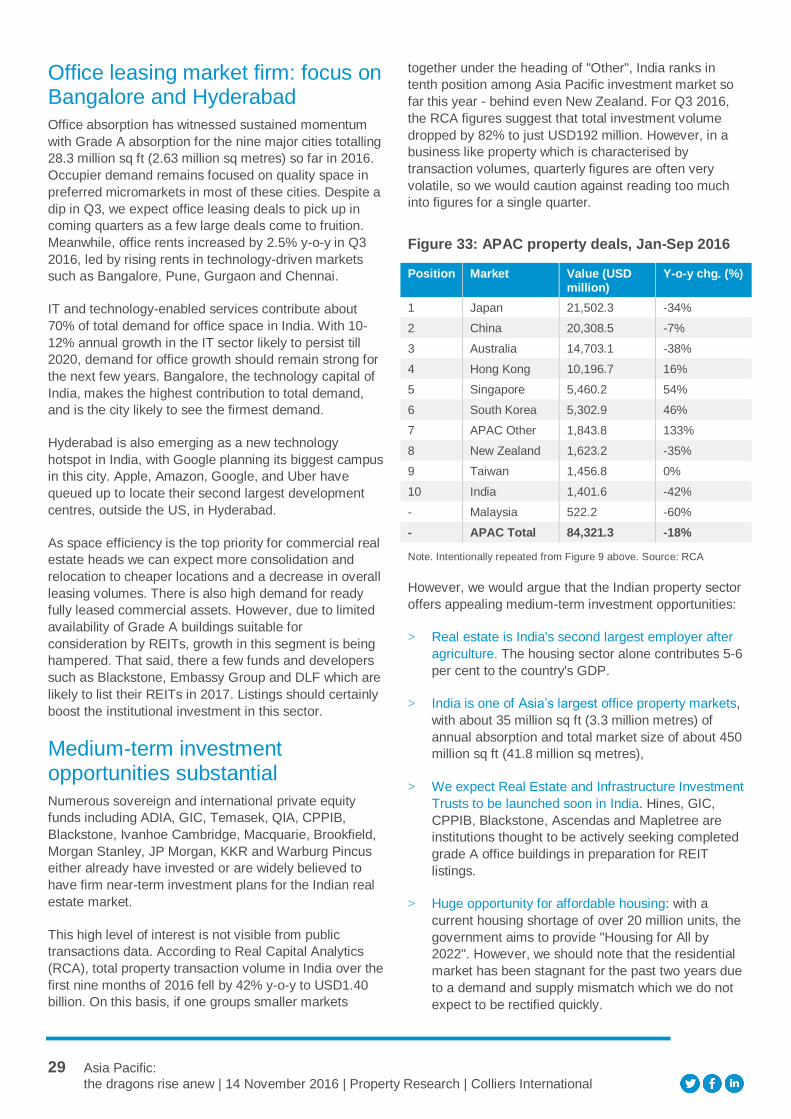

Figure 7: APAC property deals, Q3 2016

Position Market Value (USD m) Y-o-y chg. (%)

1 China 9,983.5 28%

2 Japan 6,831.5 -27%

3 Australia 5,135.8 -13%

4 Hong Kong 2,795.0 -6%

5 South Korea 2,787.0 103%

6 Singapore 1,241.9 54%

7 New Zealand 747.7 40%

8 Taiwan 350.2 -3%

9 India 191.5 -82%

10 Malaysia 103.0 -69%

- APAC Other 280.8 -19%

- APAC Total 30,448.0 1%

Source: RCA

Figure 8: APAC property deals, Q3 2016: market as % of total transaction value

Source: RCA

33%

22%

17%

9%

9%

4% 5% China

Japan

Australia

Hong Kong

South Korea

Singapore

Other

12 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

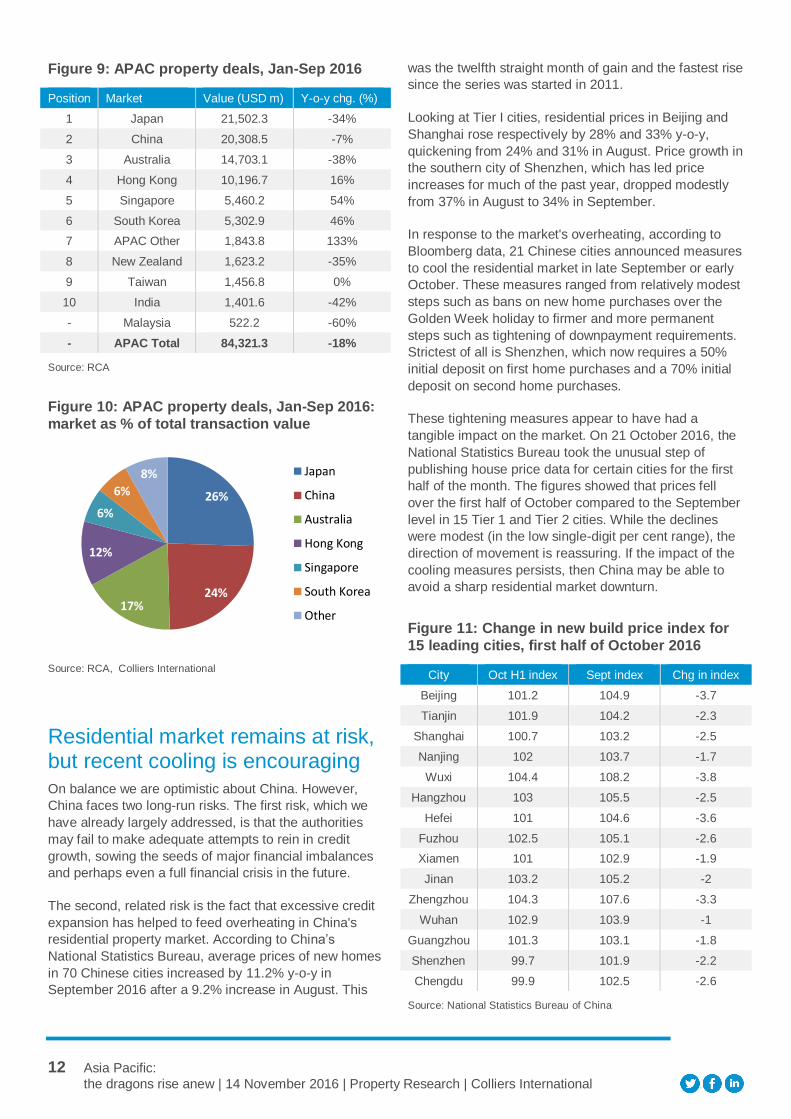

Figure 9: APAC property deals, Jan-Sep 2016

Position Market Value (USD m) Y-o-y chg. (%)

1 Japan 21,502.3 -34%

2 China 20,308.5 -7%

3 Australia 14,703.1 -38%

4 Hong Kong 10,196.7 16%

5 Singapore 5,460.2 54%

6 South Korea 5,302.9 46%

7 APAC Other 1,843.8 133%

8 New Zealand 1,623.2 -35%

9 Taiwan 1,456.8 0%

10 India 1,401.6 -42%

- Malaysia 522.2 -60%

- APAC Total 84,321.3 -18%

Source: RCA

Figure 10: APAC property deals, Jan-Sep 2016:

market as % of total transaction value

Source: RCA, Colliers International

Residential market remains at risk, but recent cooling is encouraging

On balance we are optimistic about China. However,

China faces two long-run risks. The first risk, which we

have already largely addressed, is that the authorities

may fail to make adequate attempts to rein in credit

growth, sowing the seeds of major financial imbalances

and perhaps even a full financial crisis in the future.

The second, related risk is the fact that excessive credit

expansion has helped to feed overheating in China's

residential property market. According to China’s

National Statistics Bureau, average prices of new homes

in 70 Chinese cities increased by 11.2% y-o-y in

September 2016 after a 9.2% increase in August. This

was the twelfth straight month of gain and the fastest rise

since the series was started in 2011.

Looking at Tier I cities, residential prices in Beijing and

Shanghai rose respectively by 28% and 33% y-o-y,

quickening from 24% and 31% in August. Price growth in

the southern city of Shenzhen, which has led price

increases for much of the past year, dropped modestly

from 37% in August to 34% in September.

In response to the market's overheating, according to

Bloomberg data, 21 Chinese cities announced measures

to cool the residential market in late September or early

October. These measures ranged from relatively modest

steps such as bans on new home purchases over the

Golden Week holiday to firmer and more permanent

steps such as tightening of downpayment requirements.

Strictest of all is Shenzhen, which now requires a 50%

initial deposit on first home purchases and a 70% initial

deposit on second home purchases.

These tightening measures appear to have had a

tangible impact on the market. On 21 October 2016, the

National Statistics Bureau took the unusual step of

publishing house price data for certain cities for the first

half of the month. The figures showed that prices fell

over the first half of October compared to the September

level in 15 Tier 1 and Tier 2 cities. While the declines

were modest (in the low single-digit per cent range), the

direction of movement is reassuring. If the impact of the

cooling measures persists, then China may be able to

avoid a sharp residential market downturn.

Figure 11: Change in new build price index for

15 leading cities, first half of October 2016

City Oct H1 index Sept index Chg in index

Beijing 101.2 104.9 -3.7

Tianjin 101.9 104.2 -2.3

Shanghai 100.7 103.2 -2.5

Nanjing 102 103.7 -1.7

Wuxi 104.4 108.2 -3.8

Hangzhou 103 105.5 -2.5

Hefei 101 104.6 -3.6

Fuzhou 102.5 105.1 -2.6

Xiamen 101 102.9 -1.9

Jinan 103.2 105.2 -2

Zhengzhou 104.3 107.6 -3.3

Wuhan 102.9 103.9 -1

Guangzhou 101.3 103.1 -1.8

Shenzhen 99.7 101.9 -2.2

Chengdu 99.9 102.5 -2.6

Source: National Statistics Bureau of China

26%

24% 17%

12%

6%

6%

8% Japan

China

Australia

Hong Kong

Singapore

South Korea

Other

13 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

Another reason why it would be wrong to suggest that a

residential property crash in China is either certain or

imminent is that the recent strong recovery in the

housing market has been unevenly spread. Indeed,

many Tier 3 or Tier 4 cities are still struggling to digest

large inventories of unsold housing. Housing unit sales

are now recovering in smaller as well as large cities, and

this recovery is helping to reduce housing stock, even if

it remains high by historical levels. While developments

in Tier 1 cities receive the greatest attention, the

situation in smaller cities is more representative of the

residential property sector overall and, therefore, more

important for national policy-making.

Nevertheless, the Chinese authorities need to continue

to pay close attention to residential prices in Tier 1 and

Tier 2 cities. It is interesting to note that the national

government appears to have market cooling measures

largely to the discretion of individual city authorities. This

approach is understandable, because individual Chinese

cities vary widely by population and wealth levels.

However, it may be that a more nationally coordinated

approach to cooling the residential market is required to

preclude (or, at least, greatly reduce) the risk of a

housing price crash.

14 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

Hong Kong

Prospects turning brighter

Hong Kong’s economy is steadily improving. Whereas

real GDP growth for Q1 2016 was 0.8% y-o-y, GDP

growth for Q2 reached 1.7%. Other recent data have

also generally been positive. Notably, goods exports

grew for the first time in 16 months in August, rising by

0.8% y-o-y; this growth accelerated to 3.6% y-o-y in

September. The recovery in exports has been driven by

increasing shipments to mainland China, Hong Kong's

biggest export destination; exports to China grew by

5.1% y-o-y in September. Moreover, goods imports have

been outpacing exports, with growth of 2.8% y-o-y in

August followed by 4.1% in September. The strength of

imports points to a recovery in domestic demand.

The Hong Kong government released GDP data for Q3

on 11 November, just before publication of this report: y-

o-y growth in the period increased further to 1.9%. This

further improvement in growth was driven by continued

strength in domestic demand, with consumer spending,

investment and imports all picking up. Exports also

increased, although imports grew faster. Oxford

Economics has commented that the reassuring Q3 data

may lead the firm to revise up its current 2016 forecast of

real GDP growth of 1.4%.

The encouraging growth figures have contributed to an

improvement in business sentiment, as measured by the

PMI survey. The PMI survey for September 2016 came

Figure 13: Recent economic performance and key forecasts for Hong Kong

GROWTH RATE (%) 2014 2015 2016 2017 2018 2019

Real GDP 2.7 2.4 1.4 2.0 2.5 2.5

Private consumption 3.3 4.7 1.0 2.0 2.5 2.5

Fixed investment -0.1 -2.0 -2.7 2.5 4.1 4.0

CPI 4.5 3.0 2.5 2.4 2.3 2.1

USD1.0 = HKD 7.75 7.75 7.76 7.76 7.76 7.76

Source: Oxford Economics

Figure 12: Business sentiment in Hong Kong continues to improve

Source: Hong Kong Census and Statistics Department

15 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

in at 49.3, the highest level since March 2015 and

edging closer to the 50 mark that indicates expansion

rather than contraction.

In addition to the PMI survey, we find the Quarterly

Business Tendency Survey Report produced by the

Hong Kong government's Census and Statistics

Department to be very useful. This survey collects the

views of business owners and senior managers about

their prospects for coming quarters, and so becomes a

de facto business sentiment index. The Business

Tendency Survey for Q4 2016 showed that the

proportion of respondents expecting business conditions

to deteriorate on a q-on-q basis had decreased to 10%,

from 17% in Q3 2016.

Historical evidence suggests that the results from certain

subsectors of the Business Tendency Survey, namely

financing and insurance, real estate, professional and

business services, and information and communications,

are closely correlated with the performance of office

rents in Hong Kong. This close historical correlation is

illustrated in Figure 14 below, which also shows our

assumptions about how the relationship will develop over

the period 2017-2020.

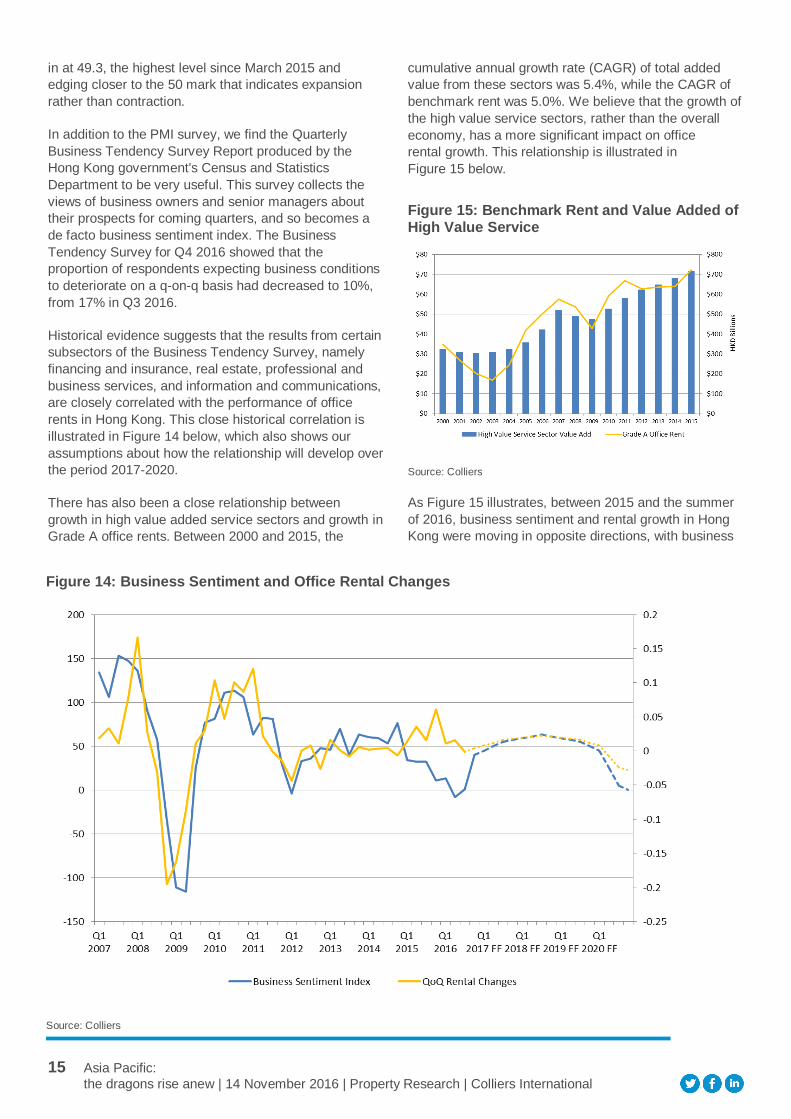

There has also been a close relationship between

growth in high value added service sectors and growth in

Grade A office rents. Between 2000 and 2015, the

cumulative annual growth rate (CAGR) of total added

value from these sectors was 5.4%, while the CAGR of

benchmark rent was 5.0%. We believe that the growth of

the high value service sectors, rather than the overall

economy, has a more significant impact on office

rental growth. This relationship is illustrated in

Figure 15 below.

Figure 15: Benchmark Rent and Value Added of High Value Service

Source: Colliers

As Figure 15 illustrates, between 2015 and the summer

of 2016, business sentiment and rental growth in Hong

Kong were moving in opposite directions, with business

Figure 14: Business Sentiment and Office Rental Changes

Source: Colliers

16 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

sentiment deteriorating but benchmark rent rising. In

other words, a decoupling took place. We believe that

this decoupling chiefly reflected an extremely low

vacancy rate and strong demand from the Chinese

companies in the core CBD area. We believe the

decoupling will not develop into a long-term

phenomenon and assume that the vacancy rate will

eventually move back towards the historical average.

Island office rents and investment market strong, Kowloon weaker

Past records have revealed that business sentiment

tends to move in three to four year cycles and it is very

rare for the survey result to stay in negative territory for a

long period. As noted, business sentiment in Hong Kong

was moving downwards until Q2 2016, which looks as

though it was probably the bottom of the most recent

cycle. Looking forward, we expect the present rebound

in business sentiment to continue over the rest of this

year and into 2017, driven by stabilisation in the Chinese

economy and modest US economic expansion. This in

turn should support positive rent growth. This is the crux

of our prediction that the benchmark rent in Hong Kong

will rise by 12% between end-2015 and end-2020.

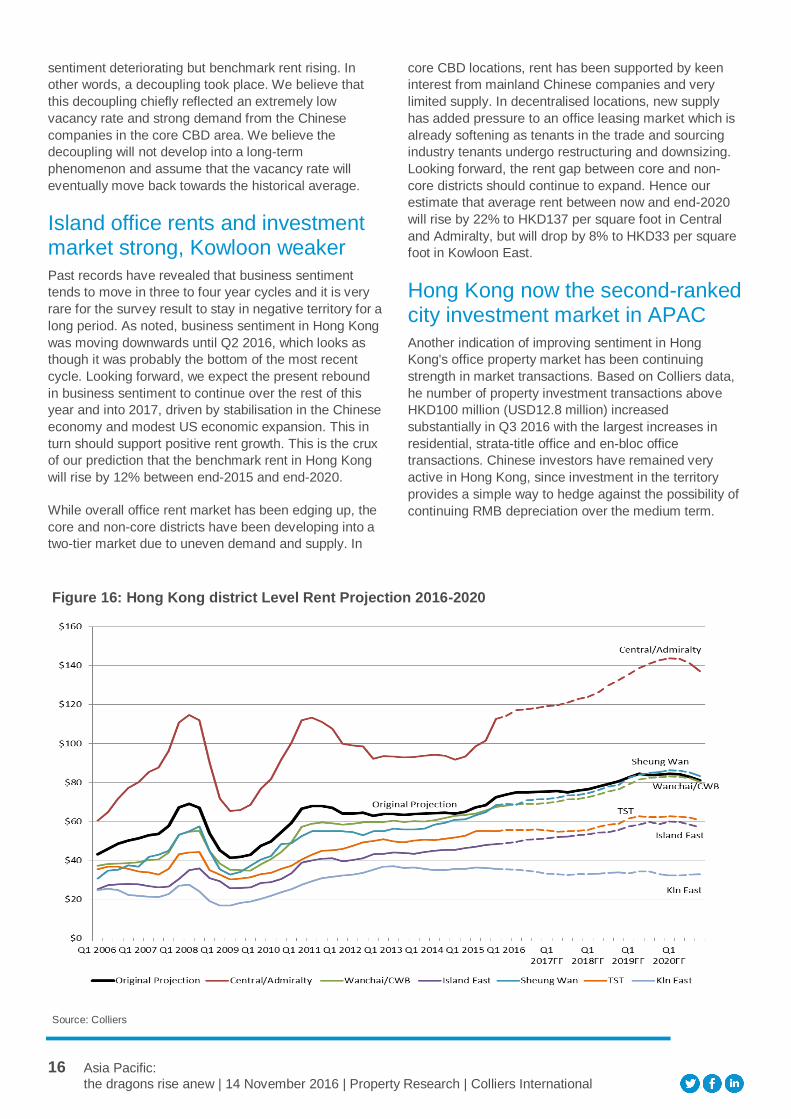

While overall office rent market has been edging up, the

core and non-core districts have been developing into a

two-tier market due to uneven demand and supply. In

core CBD locations, rent has been supported by keen

interest from mainland Chinese companies and very

limited supply. In decentralised locations, new supply

has added pressure to an office leasing market which is

already softening as tenants in the trade and sourcing

industry tenants undergo restructuring and downsizing.

Looking forward, the rent gap between core and non-

core districts should continue to expand. Hence our

estimate that average rent between now and end-2020

will rise by 22% to HKD137 per square foot in Central

and Admiralty, but will drop by 8% to HKD33 per square

foot in Kowloon East.

Hong Kong now the second-ranked city investment market in APAC

Another indication of improving sentiment in Hong

Kong's office property market has been continuing

strength in market transactions. Based on Colliers data,

he number of property investment transactions above

HKD100 million (USD12.8 million) increased

substantially in Q3 2016 with the largest increases in

residential, strata-title office and en-bloc office

transactions. Chinese investors have remained very

active in Hong Kong, since investment in the territory

provides a simple way to hedge against the possibility of

continuing RMB depreciation over the medium term.

Figure 16: Hong Kong district Level Rent Projection 2016-2020

Source: Colliers

17 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

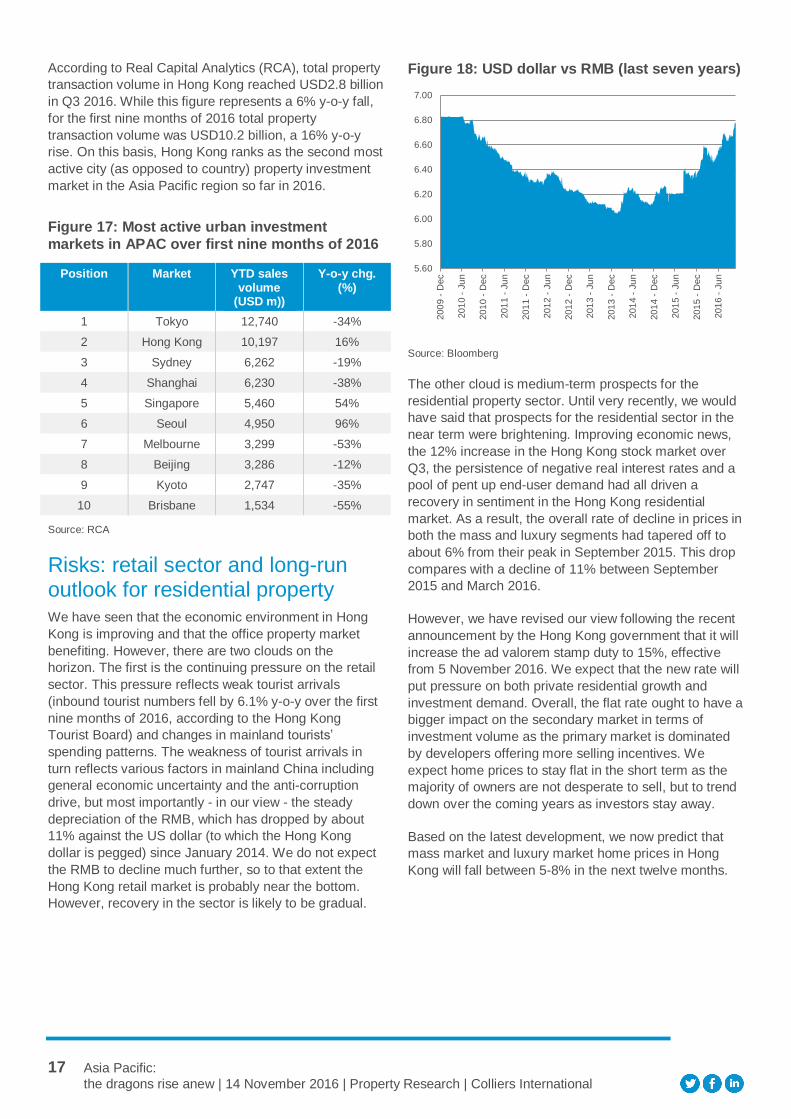

According to Real Capital Analytics (RCA), total property

transaction volume in Hong Kong reached USD2.8 billion

in Q3 2016. While this figure represents a 6% y-o-y fall,

for the first nine months of 2016 total property

transaction volume was USD10.2 billion, a 16% y-o-y

rise. On this basis, Hong Kong ranks as the second most

active city (as opposed to country) property investment

market in the Asia Pacific region so far in 2016.

Figure 17: Most active urban investment

markets in APAC over first nine months of 2016

Position Market YTD sales volume

(USD m))

Y-o-y chg. (%)

1 Tokyo 12,740 -34%

2 Hong Kong 10,197 16%

3 Sydney 6,262 -19%

4 Shanghai 6,230 -38%

5 Singapore 5,460 54%

6 Seoul 4,950 96%

7 Melbourne 3,299 -53%

8 Beijing 3,286 -12%

9 Kyoto 2,747 -35%

10 Brisbane 1,534 -55%

Source: RCA

Risks: retail sector and long-run outlook for residential property We have seen that the economic environment in Hong

Kong is improving and that the office property market

benefiting. However, there are two clouds on the

horizon. The first is the continuing pressure on the retail

sector. This pressure reflects weak tourist arrivals

(inbound tourist numbers fell by 6.1% y-o-y over the first

nine months of 2016, according to the Hong Kong

Tourist Board) and changes in mainland tourists’

spending patterns. The weakness of tourist arrivals in

turn reflects various factors in mainland China including

general economic uncertainty and the anti-corruption

drive, but most importantly - in our view - the steady

depreciation of the RMB, which has dropped by about

11% against the US dollar (to which the Hong Kong

dollar is pegged) since January 2014. We do not expect

the RMB to decline much further, so to that extent the

Hong Kong retail market is probably near the bottom.

However, recovery in the sector is likely to be gradual.

Figure 18: USD dollar vs RMB (last seven years)

Source: Bloomberg

The other cloud is medium-term prospects for the

residential property sector. Until very recently, we would

have said that prospects for the residential sector in the

near term were brightening. Improving economic news,

the 12% increase in the Hong Kong stock market over

Q3, the persistence of negative real interest rates and a

pool of pent up end-user demand had all driven a

recovery in sentiment in the Hong Kong residential

market. As a result, the overall rate of decline in prices in

both the mass and luxury segments had tapered off to

about 6% from their peak in September 2015. This drop

compares with a decline of 11% between September

2015 and March 2016.

However, we have revised our view following the recent

announcement by the Hong Kong government that it will

increase the ad valorem stamp duty to 15%, effective

from 5 November 2016. We expect that the new rate will

put pressure on both private residential growth and

investment demand. Overall, the flat rate ought to have a

bigger impact on the secondary market in terms of

investment volume as the primary market is dominated

by developers offering more selling incentives. We

expect home prices to stay flat in the short term as the

majority of owners are not desperate to sell, but to trend

down over the coming years as investors stay away.

Based on the latest development, we now predict that

mass market and luxury market home prices in Hong

Kong will fall between 5-8% in the next twelve months.

5.60

5.80

6.00

6.20

6.40

6.60

6.80

7.00

200

9 -

Dec

201

0 -

Ju

n

201

0 -

Dec

201

1 -

Ju

n

201

1 -

Dec

201

2 -

Ju

n

201

2 -

Dec

201

3 -

Ju

n

201

3 -

Dec

201

4 -

Ju

n

201

4 -

Dec

201

5 -

Ju

n

201

5 -

Dec

201

6 -

Ju

n

18 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

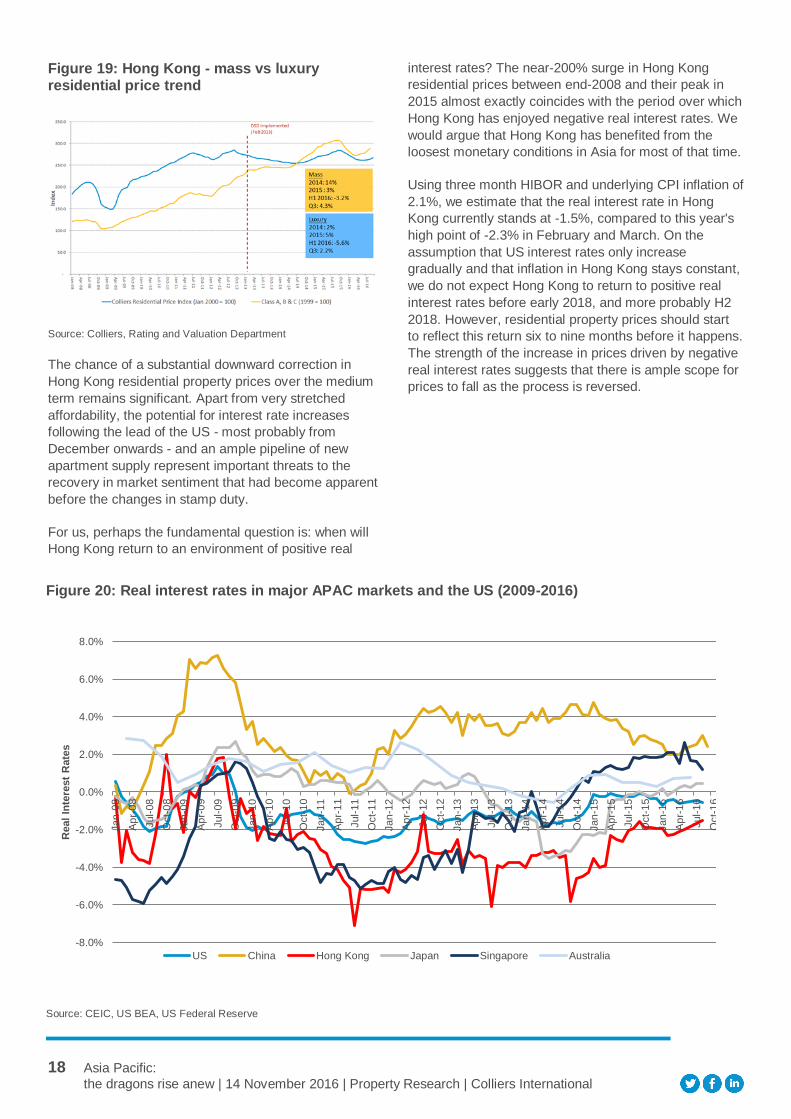

Figure 19: Hong Kong - mass vs luxury residential price trend

Source: Colliers, Rating and Valuation Department

The chance of a substantial downward correction in

Hong Kong residential property prices over the medium

term remains significant. Apart from very stretched

affordability, the potential for interest rate increases

following the lead of the US - most probably from

December onwards - and an ample pipeline of new

apartment supply represent important threats to the

recovery in market sentiment that had become apparent

before the changes in stamp duty.

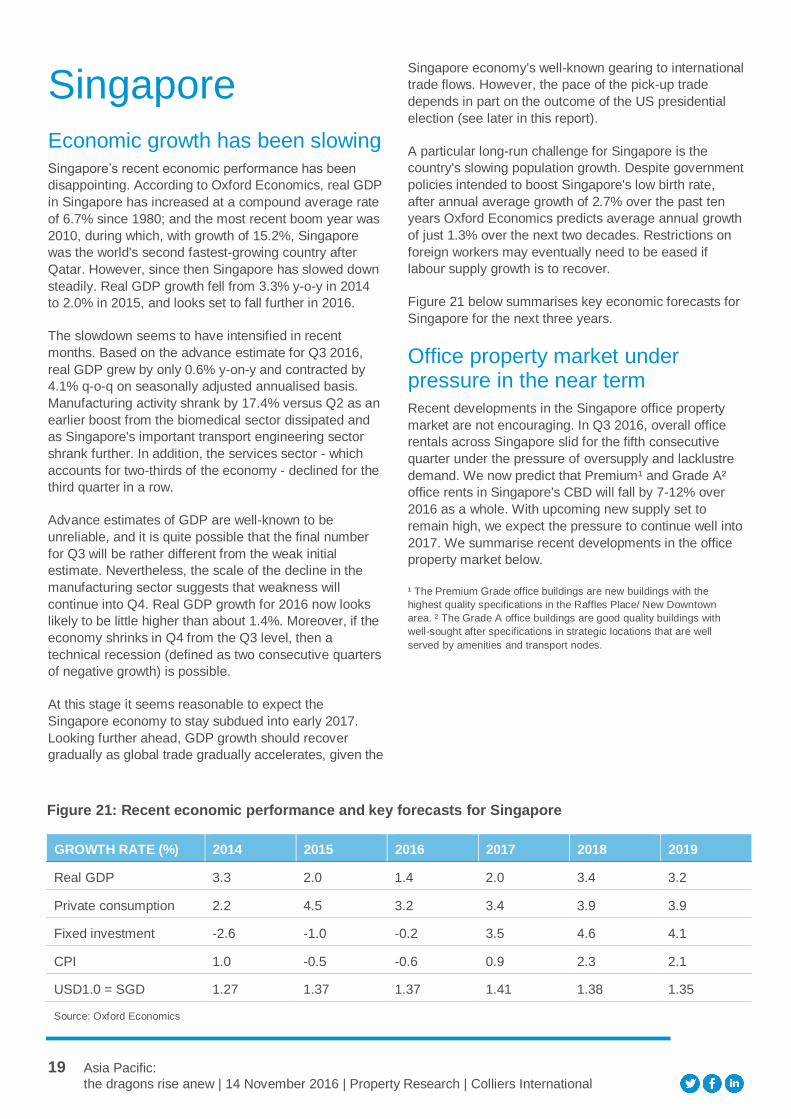

For us, perhaps the fundamental question is: when will

Hong Kong return to an environment of positive real

interest rates? The near-200% surge in Hong Kong

residential prices between end-2008 and their peak in

2015 almost exactly coincides with the period over which

Hong Kong has enjoyed negative real interest rates. We

would argue that Hong Kong has benefited from the

loosest monetary conditions in Asia for most of that time.

Using three month HIBOR and underlying CPI inflation of

2.1%, we estimate that the real interest rate in Hong

Kong currently stands at -1.5%, compared to this year's

high point of -2.3% in February and March. On the

assumption that US interest rates only increase

gradually and that inflation in Hong Kong stays constant,

we do not expect Hong Kong to return to positive real

interest rates before early 2018, and more probably H2

2018. However, residential property prices should start

to reflect this return six to nine months before it happens.

The strength of the increase in prices driven by negative

real interest rates suggests that there is ample scope for

prices to fall as the process is reversed.

Figure 20: Real interest rates in major APAC markets and the US (2009-2016)

Source: CEIC, US BEA, US Federal Reserve

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Jan

-08

Ap

r-0

8

Jul-

08

Oct-

08

Jan

-09

Ap

r-0

9

Jul-

09

Oct-

09

Jan

-10

Ap

r-1

0

Jul-

10

Oct-

10

Jan

-11

Ap

r-1

1

Jul-

11

Oct-

11

Jan

-12

Ap

r-1

2

Jul-

12

Oct-

12

Jan

-13

Ap

r-1

3

Jul-

13

Oct-

13

Jan

-14

Ap

r-1

4

Jul-

14

Oct-

14

Jan

-15

Ap

r-1

5

Jul-

15

Oct-

15

Jan

-16

Ap

r-1

6

Jul-

16

Oct-

16

Real

Inte

rest

Rate

s

US China Hong Kong Japan Singapore Australia

19 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

Singapore

Economic growth has been slowing

Singapore’s recent economic performance has been

disappointing. According to Oxford Economics, real GDP

in Singapore has increased at a compound average rate

of 6.7% since 1980; and the most recent boom year was

2010, during which, with growth of 15.2%, Singapore

was the world's second fastest-growing country after

Qatar. However, since then Singapore has slowed down

steadily. Real GDP growth fell from 3.3% y-o-y in 2014

to 2.0% in 2015, and looks set to fall further in 2016.

The slowdown seems to have intensified in recent

months. Based on the advance estimate for Q3 2016,

real GDP grew by only 0.6% y-on-y and contracted by

4.1% q-o-q on seasonally adjusted annualised basis.

Manufacturing activity shrank by 17.4% versus Q2 as an

earlier boost from the biomedical sector dissipated and

as Singapore's important transport engineering sector

shrank further. In addition, the services sector - which

accounts for two-thirds of the economy - declined for the

third quarter in a row.

Advance estimates of GDP are well-known to be

unreliable, and it is quite possible that the final number

for Q3 will be rather different from the weak initial

estimate. Nevertheless, the scale of the decline in the

manufacturing sector suggests that weakness will

continue into Q4. Real GDP growth for 2016 now looks

likely to be little higher than about 1.4%. Moreover, if the

economy shrinks in Q4 from the Q3 level, then a

technical recession (defined as two consecutive quarters

of negative growth) is possible.

At this stage it seems reasonable to expect the

Singapore economy to stay subdued into early 2017.

Looking further ahead, GDP growth should recover

gradually as global trade gradually accelerates, given the

Singapore economy's well-known gearing to international

trade flows. However, the pace of the pick-up trade

depends in part on the outcome of the US presidential

election (see later in this report).

A particular long-run challenge for Singapore is the

country's slowing population growth. Despite government

policies intended to boost Singapore's low birth rate,

after annual average growth of 2.7% over the past ten

years Oxford Economics predicts average annual growth

of just 1.3% over the next two decades. Restrictions on

foreign workers may eventually need to be eased if

labour supply growth is to recover.

Figure 21 below summarises key economic forecasts for

Singapore for the next three years.

Office property market under pressure in the near term

Recent developments in the Singapore office property

market are not encouraging. In Q3 2016, overall office

rentals across Singapore slid for the fifth consecutive

quarter under the pressure of oversupply and lacklustre

demand. We now predict that Premium¹ and Grade A²

office rents in Singapore's CBD will fall by 7-12% over

2016 as a whole. With upcoming new supply set to

remain high, we expect the pressure to continue well into

2017. We summarise recent developments in the office

property market below.

¹ The Premium Grade office buildings are new buildings with the

highest quality specifications in the Raffles Place/ New Downtown

area. ² The Grade A office buildings are good quality buildings with

well-sought after specifications in strategic locations that are well

served by amenities and transport nodes.

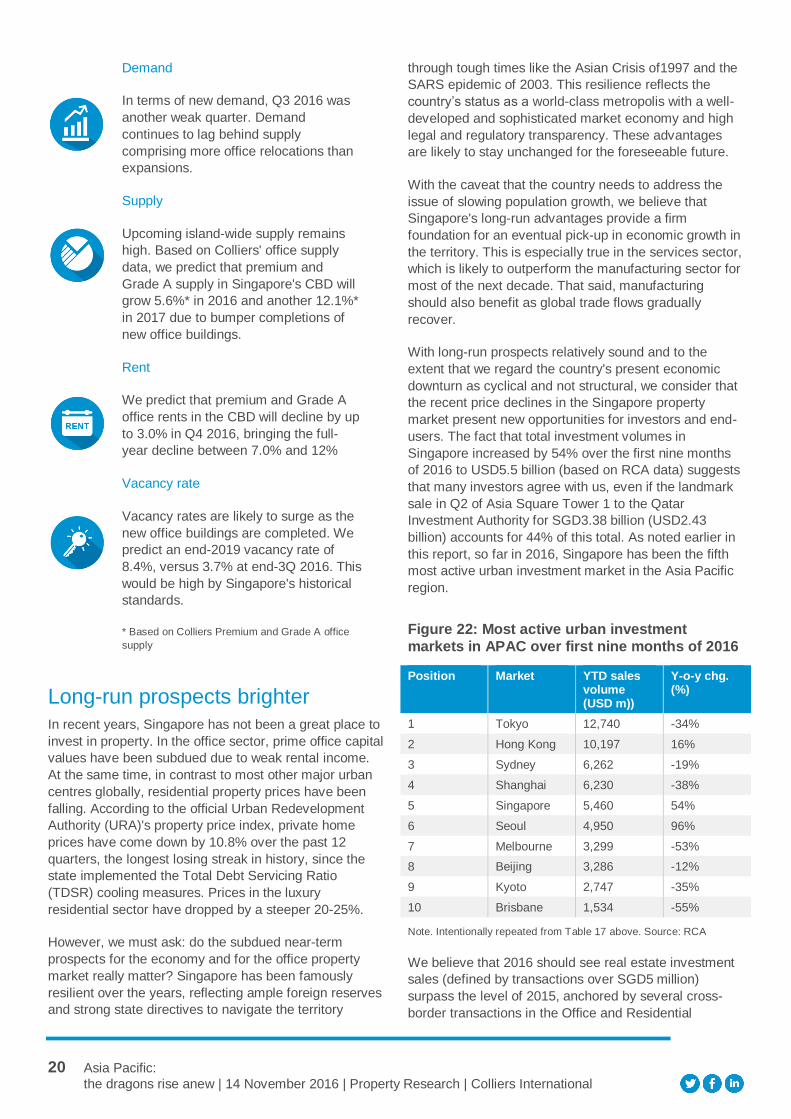

Figure 21: Recent economic performance and key forecasts for Singapore

GROWTH RATE (%) 2014 2015 2016 2017 2018 2019

Real GDP 3.3 2.0 1.4 2.0 3.4 3.2

Private consumption 2.2 4.5 3.2 3.4 3.9 3.9

Fixed investment -2.6 -1.0 -0.2 3.5 4.6 4.1

CPI 1.0 -0.5 -0.6 0.9 2.3 2.1

USD1.0 = SGD 1.27 1.37 1.37 1.41 1.38 1.35

Source: Oxford Economics

20 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

Demand

In terms of new demand, Q3 2016 was

another weak quarter. Demand

continues to lag behind supply

comprising more office relocations than

expansions.

Supply

Upcoming island-wide supply remains

high. Based on Colliers' office supply

data, we predict that premium and

Grade A supply in Singapore's CBD will

grow 5.6%* in 2016 and another 12.1%*

in 2017 due to bumper completions of

new office buildings.

Rent

We predict that premium and Grade A

office rents in the CBD will decline by up

to 3.0% in Q4 2016, bringing the full-

year decline between 7.0% and 12%

Vacancy rate

Vacancy rates are likely to surge as the

new office buildings are completed. We

predict an end-2019 vacancy rate of

8.4%, versus 3.7% at end-3Q 2016. This

would be high by Singapore's historical

standards.

* Based on Colliers Premium and Grade A office

supply

Long-run prospects brighter

In recent years, Singapore has not been a great place to

invest in property. In the office sector, prime office capital

values have been subdued due to weak rental income.

At the same time, in contrast to most other major urban

centres globally, residential property prices have been

falling. According to the official Urban Redevelopment

Authority (URA)'s property price index, private home

prices have come down by 10.8% over the past 12

quarters, the longest losing streak in history, since the

state implemented the Total Debt Servicing Ratio

(TDSR) cooling measures. Prices in the luxury

residential sector have dropped by a steeper 20-25%.

However, we must ask: do the subdued near-term

prospects for the economy and for the office property

market really matter? Singapore has been famously

resilient over the years, reflecting ample foreign reserves

and strong state directives to navigate the territory

through tough times like the Asian Crisis of1997 and the

SARS epidemic of 2003. This resilience reflects the

country’s status as a world-class metropolis with a well-

developed and sophisticated market economy and high

legal and regulatory transparency. These advantages

are likely to stay unchanged for the foreseeable future.

With the caveat that the country needs to address the

issue of slowing population growth, we believe that

Singapore's long-run advantages provide a firm

foundation for an eventual pick-up in economic growth in

the territory. This is especially true in the services sector,

which is likely to outperform the manufacturing sector for

most of the next decade. That said, manufacturing

should also benefit as global trade flows gradually

recover.

With long-run prospects relatively sound and to the

extent that we regard the country's present economic

downturn as cyclical and not structural, we consider that

the recent price declines in the Singapore property

market present new opportunities for investors and end-

users. The fact that total investment volumes in

Singapore increased by 54% over the first nine months

of 2016 to USD5.5 billion (based on RCA data) suggests

that many investors agree with us, even if the landmark

sale in Q2 of Asia Square Tower 1 to the Qatar

Investment Authority for SGD3.38 billion (USD2.43

billion) accounts for 44% of this total. As noted earlier in

this report, so far in 2016, Singapore has been the fifth

most active urban investment market in the Asia Pacific

region.

Figure 22: Most active urban investment

markets in APAC over first nine months of 2016

Position Market YTD sales volume (USD m))

Y-o-y chg. (%)

1 Tokyo 12,740 -34%

2 Hong Kong 10,197 16%

3 Sydney 6,262 -19%

4 Shanghai 6,230 -38%

5 Singapore 5,460 54%

6 Seoul 4,950 96%

7 Melbourne 3,299 -53%

8 Beijing 3,286 -12%

9 Kyoto 2,747 -35%

10 Brisbane 1,534 -55%

Note. Intentionally repeated from Table 17 above. Source: RCA

We believe that 2016 should see real estate investment

sales (defined by transactions over SGD5 million)

surpass the level of 2015, anchored by several cross-

border transactions in the Office and Residential

21 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

segments, where sovereign wealth funds, institutional

investors and high net worth individuals continue to

acquire trophy assets on a long-term view.

Looking forward, any easing of the cooling measures

could provide some impetus for participation in the luxury

residential sector. Foreigners may find it attractive to re-

enter the market when the additional buyer's stamp duty

of 15% imposed on foreigners is eventually relaxed or

removed.

Time to look at Singapore again

We believe that Singapore's prime real estate in general

should continue to be sought after by global institutional

investors looking for stable long-term returns in a

diversified portfolio. The near-term outlook for growth in

office rents is clouded by our assumption of a significant

increase in supply: hence our estimate of negative

average annual prime grade office rent growth (-2.1%)

between 2016 and 2019. However, the prime grade

office net operating yield for the Singapore CBD of 3.5%

is reasonably attractive - and more so than the

corresponding figure of 2.5% for prime grade office

property on Hong Kong Island.

The long-run attractions of Singapore explain, in our

view, why the investment market has been so firm in

Singapore recently: investors are looking beyond a

modest near-term decline in office rents to the prospect

of rental growth and capital appreciation further into the

future. As suggested, the office segment is not the only

part of the property market that is attractive for long-run

investment: the residential segment, including luxury

property, is well worth considering too.

22 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

Australia

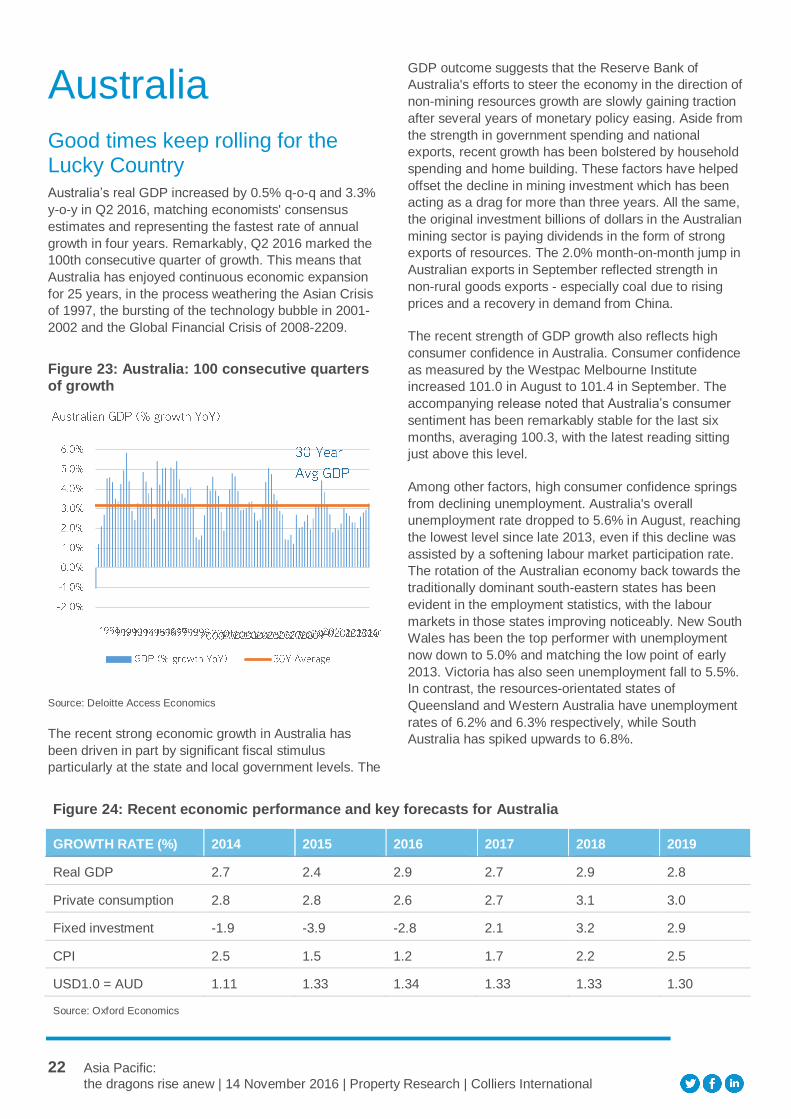

Good times keep rolling for the Lucky Country Australia’s real GDP increased by 0.5% q-o-q and 3.3%

y-o-y in Q2 2016, matching economists' consensus

estimates and representing the fastest rate of annual

growth in four years. Remarkably, Q2 2016 marked the

100th consecutive quarter of growth. This means that

Australia has enjoyed continuous economic expansion

for 25 years, in the process weathering the Asian Crisis

of 1997, the bursting of the technology bubble in 2001-

2002 and the Global Financial Crisis of 2008-2209.

Figure 23: Australia: 100 consecutive quarters of growth

Source: Deloitte Access Economics

The recent strong economic growth in Australia has

been driven in part by significant fiscal stimulus

particularly at the state and local government levels. The

GDP outcome suggests that the Reserve Bank of

Australia's efforts to steer the economy in the direction of

non-mining resources growth are slowly gaining traction

after several years of monetary policy easing. Aside from

the strength in government spending and national

exports, recent growth has been bolstered by household

spending and home building. These factors have helped

offset the decline in mining investment which has been

acting as a drag for more than three years. All the same,

the original investment billions of dollars in the Australian

mining sector is paying dividends in the form of strong

exports of resources. The 2.0% month-on-month jump in

Australian exports in September reflected strength in

non-rural goods exports - especially coal due to rising

prices and a recovery in demand from China.

The recent strength of GDP growth also reflects high

consumer confidence in Australia. Consumer confidence

as measured by the Westpac Melbourne Institute

increased 101.0 in August to 101.4 in September. The

accompanying release noted that Australia’s consumer

sentiment has been remarkably stable for the last six

months, averaging 100.3, with the latest reading sitting

just above this level.

Among other factors, high consumer confidence springs

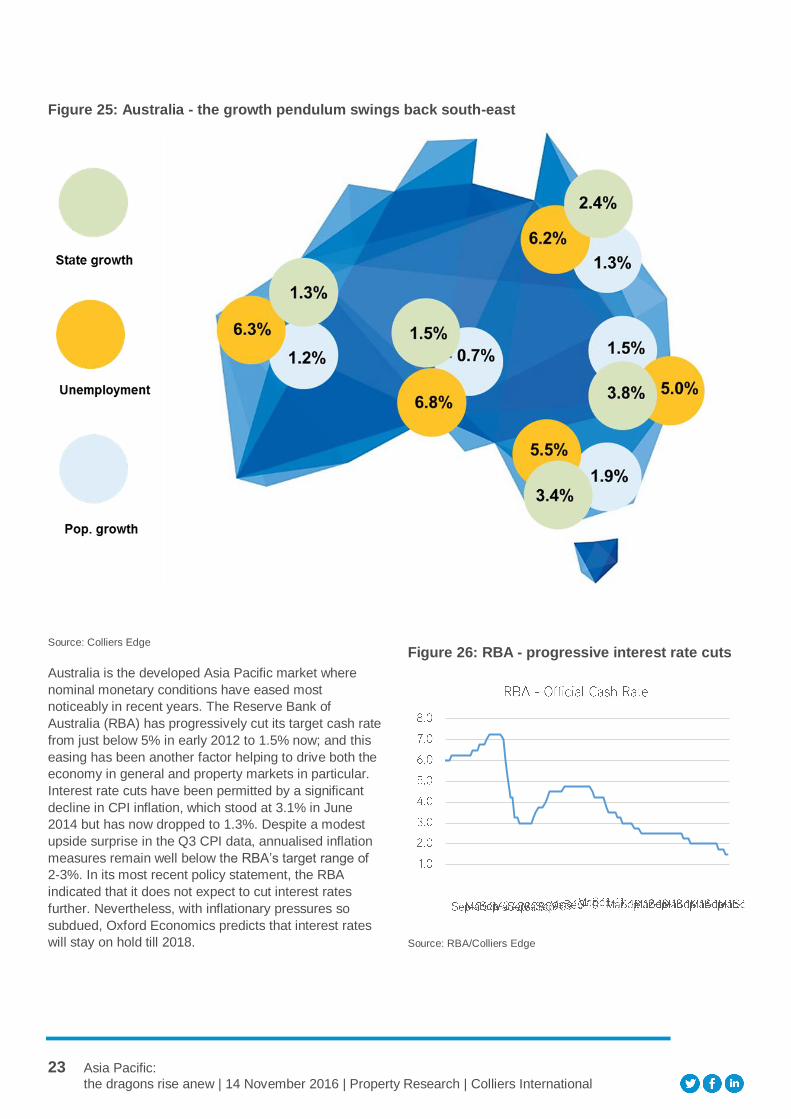

from declining unemployment. Australia's overall

unemployment rate dropped to 5.6% in August, reaching

the lowest level since late 2013, even if this decline was

assisted by a softening labour market participation rate.

The rotation of the Australian economy back towards the

traditionally dominant south-eastern states has been

evident in the employment statistics, with the labour

markets in those states improving noticeably. New South

Wales has been the top performer with unemployment

now down to 5.0% and matching the low point of early

2013. Victoria has also seen unemployment fall to 5.5%.

In contrast, the resources-orientated states of

Queensland and Western Australia have unemployment

rates of 6.2% and 6.3% respectively, while South

Australia has spiked upwards to 6.8%.

Figure 24: Recent economic performance and key forecasts for Australia

GROWTH RATE (%) 2014 2015 2016 2017 2018 2019

Real GDP 2.7 2.4 2.9 2.7 2.9 2.8

Private consumption 2.8 2.8 2.6 2.7 3.1 3.0

Fixed investment -1.9 -3.9 -2.8 2.1 3.2 2.9

CPI 2.5 1.5 1.2 1.7 2.2 2.5

USD1.0 = AUD 1.11 1.33 1.34 1.33 1.33 1.30

Source: Oxford Economics

23 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

Source: Colliers Edge

Australia is the developed Asia Pacific market where

nominal monetary conditions have eased most

noticeably in recent years. The Reserve Bank of

Australia (RBA) has progressively cut its target cash rate

from just below 5% in early 2012 to 1.5% now; and this

easing has been another factor helping to drive both the

economy in general and property markets in particular.

Interest rate cuts have been permitted by a significant

decline in CPI inflation, which stood at 3.1% in June

2014 but has now dropped to 1.3%. Despite a modest

upside surprise in the Q3 CPI data, annualised inflation

measures remain well below the RBA’s target range of

2-3%. In its most recent policy statement, the RBA

indicated that it does not expect to cut interest rates

further. Nevertheless, with inflationary pressures so

subdued, Oxford Economics predicts that interest rates

will stay on hold till 2018.

Figure 26: RBA - progressive interest rate cuts

Source: RBA/Colliers Edge

Figure 25: Australia - the growth pendulum swings back south-east

24 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

Office markets still very strong in Sydney and Melbourne

The Sydney and Melbourne office property markets

continue to benefit from the buoyant economic

conditions. Demand is strong due to expansion in

professional and services employment, while supply is

limited or diminishing. Nor has falling inflation impacted

rental growth, because strong employment numbers are

driving down vacancy and giving Australian landlords

more room to lower their traditionally high incentive

payments. As shown in Figure 27 below, over mid-2016,

Sydney and Melbourne were experiencing effective

rental growth of 10-20% y-o-y.

Incentives still have some way to fall. Currently,

incentives are equivalent to 25% of rental income for

Grade A office buildings in Sydney. However, high levels

of withdrawal and rising tenant demand should put

strong downward pressure on incentives in the medium

term. Melbourne incentives are also falling, but at a

slower rate than in Sydney, which benefits from a higher

level of demand from financial services and larger

technology companies. Melbourne demand is more

diversified, with education, professional services firms

and government being the primary movers.

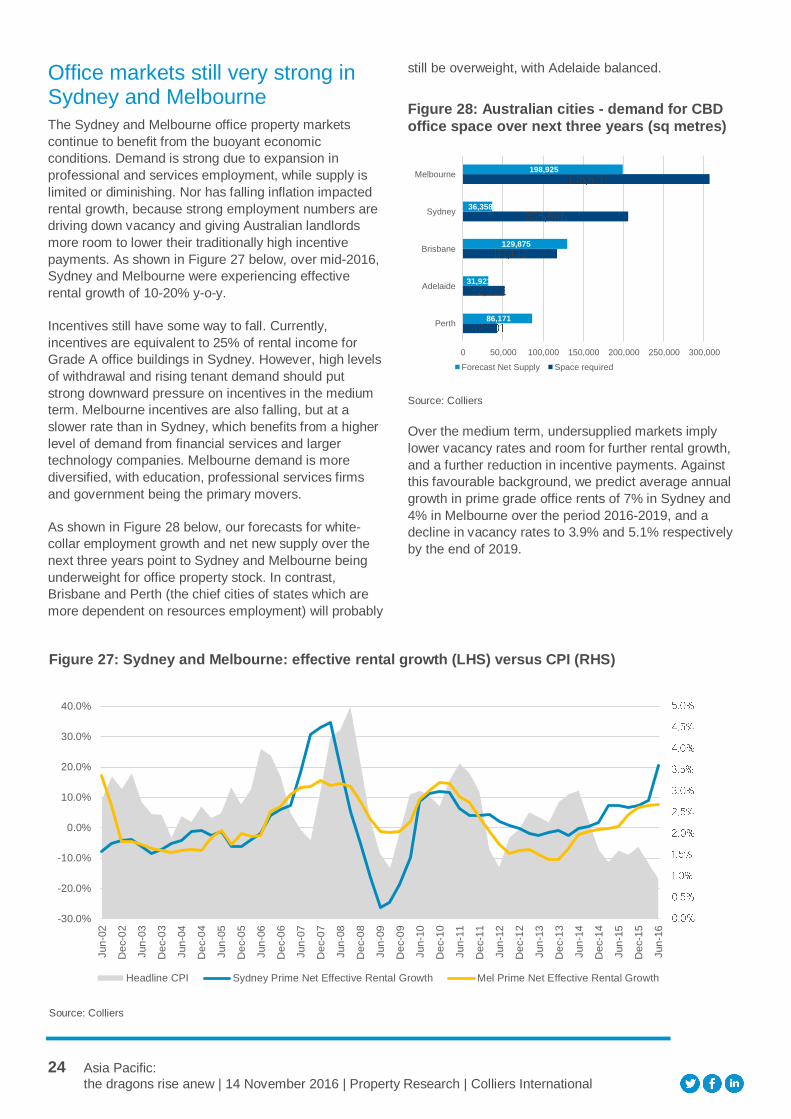

As shown in Figure 28 below, our forecasts for white-

collar employment growth and net new supply over the

next three years point to Sydney and Melbourne being

underweight for office property stock. In contrast,

Brisbane and Perth (the chief cities of states which are

more dependent on resources employment) will probably

still be overweight, with Adelaide balanced.

Figure 28: Australian cities - demand for CBD

office space over next three years (sq metres)

Source: Colliers

Over the medium term, undersupplied markets imply

lower vacancy rates and room for further rental growth,

and a further reduction in incentive payments. Against

this favourable background, we predict average annual

growth in prime grade office rents of 7% in Sydney and

4% in Melbourne over the period 2016-2019, and a

decline in vacancy rates to 3.9% and 5.1% respectively

by the end of 2019.

86,171

31,921

129,875

36,358

198,925

0 50,000 100,000 150,000 200,000 250,000 300,000

Perth

Adelaide

Brisbane

Sydney

Melbourne

Forecast Net Supply Space required

Figure 27: Sydney and Melbourne: effective rental growth (LHS) versus CPI (RHS)

Source: Colliers

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

Jun

-02

De

c-0

2

Jun

-03

De

c-0

3

Jun

-04

De

c-0

4

Jun

-05

De

c-0

5

Jun

-06

De

c-0

6

Jun

-07

De

c-0

7

Jun

-08

De

c-0

8

Jun

-09

De

c-0

9

Jun

-10

De

c-1

0

Jun

-11

De

c-1

1

Jun

-12

De

c-1

2

Jun

-13

De

c-1

3

Jun

-14

De

c-1

4

Jun

-15

De

c-1

5

Jun

-16

Headline CPI Sydney Prime Net Effective Rental Growth Mel Prime Net Effective Rental Growth

25 Asia Pacific:

the dragons rise anew | 14 November 2016 | Property Research | Colliers International

Investment in Australia driven by Asia, especially China

As shown in Figure 29 below, in recent years investment

in Australian office markets has been heavily driven by

Asian investors, and especially by Chinese investors.

China has been the fastest-growing investor in

Australian commercial real estate since 2009. From

2001-2008 only AUD50 million (USD38 million) of

Chinese investment was recorded; however from 2009

to the present there been over AUD17.0 billion (USD12.8

billion) of direct investment. Despite the surge in Chinese

interest, however, Singapore is still the largest source of

foreign investment in Australia. Colliers Australia

anticipates further investment from Asian countries in

2017, particularly from Singapore and perhaps also

Japan, which may look to re-enter the market. US

investors may also look at Australia again.

Core markets still attractive, even if investment story is well-known

On a gross basis unadjusted for incentives, prime grade

office property in Sydney and Melbourne yields 5.5%-

5.8%, or between 3.2% and 3.5% above Australian ten-

year bonds. One could argue that the prevalence of

incentive payments in the Australian commercial

property means that true office property yields are 1.0-

1.5 percentage points lower than the headline figures,

but this is a blunt and questionable calculation and in

any case incentive payments are falling.

Given our expectation of a significant additional wave of

investment in Australia from Asia in 2017, there is good

reason to believe that demand for office property in

Australia will remain very strong. This demand should

push up capital values, and so suggests that further

yield compression in Sydney and Melbourne at least

is probable. Risks to this scenario include weakening

wages growth, cuts in government spending and

economic slowdown in China, but for the moment

we see only limited scope for concern on any of

these fronts.

Like Singapore, Australia benefits from high legal and

regulatory transparency and low sovereign risk. It is little