Embed Size (px)

Citation preview

winter 2014

development proposal for

GAS WORKS FLATS1900 N Northlake Way

ACKNOWLEDGMENTSMaria Barrientos, Barrientos LLC

Jon Schack, Schack A+D

Dugan Earl, Revolve Development

TJ Lehman, Mack Urban

Matt Orr, Apartment Financial

Joe Ferguson, Lake Union Partners

Heidi Turner, Blanton Turner

Anne Marie Koehler, CBRE

Mark Speidel, I.L. Gross Structural Engineers

Brian Gibson, MRJ Constructors

Gary Beem, Northwest Commercial Mortgage

Bryce Taylor, GLY Construction

Corey Marx, JLL

CJ Bowles, CBRE

Austin Besse, Weber Thompson

Jeff Peterson, CPL

Monica Wallace, Wallace Properties

A special thanks to:

Al Levine

Chris Bitter

EXECUTIVE SUMMARY

adaptive reuse

209 apar tments + 9 live/work

6,100 SF retail

completion: summer 2017

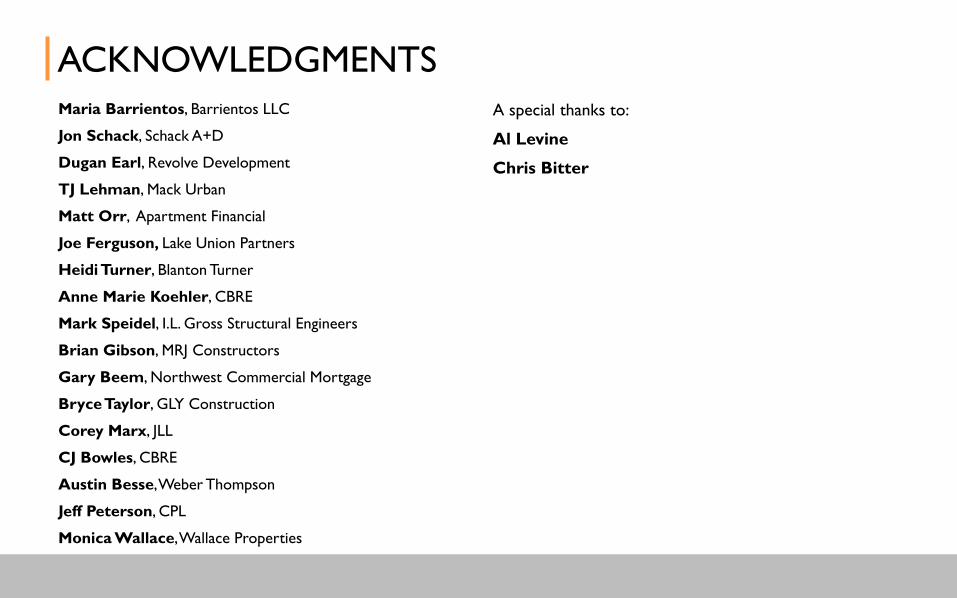

Yield on Cost - 7.1%

Large, well-located mixed-use development

Leveraged IRR – 13.9%

INTRODUCTION

• Leveraged IRR no less than 12%

• 6% yield on cost for multifamily, 6.5% for commercial

• Develop institutional quality real estate

Teutsch’s Objectives:

INTRODUCTION

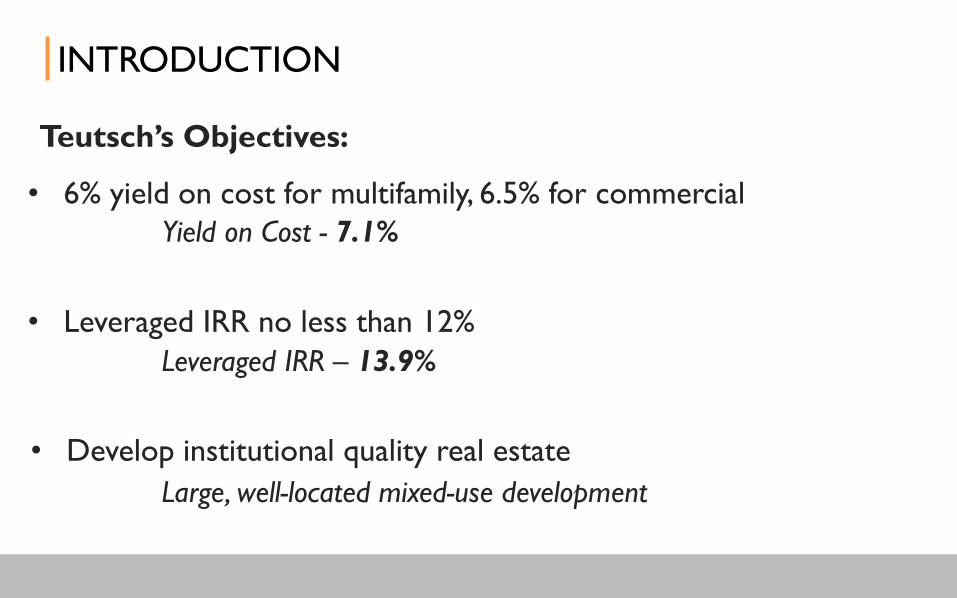

Key Risk Mitigation Strategies:

• No excavation for below grade parking is required

• Development retains neighborhood character, does not maximize

FAR and provides open space

• Work with steep slope to create distinct identities

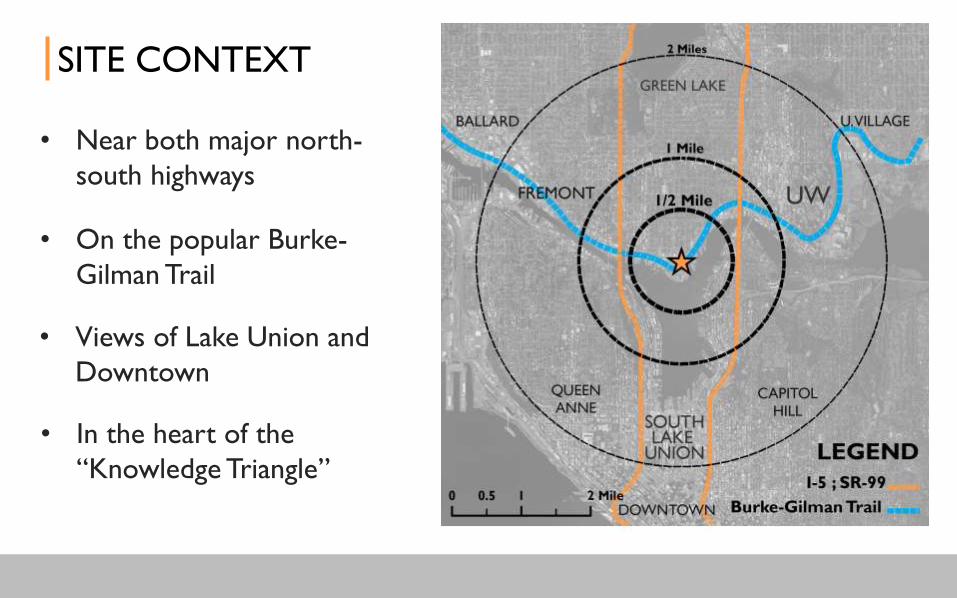

SITE CONTEXT

01

• In the heart of the

“Knowledge Triangle”

• Near both major north-

south highways

• On the popular Burke-

Gilman Trail

• Views of Lake Union and

Downtown

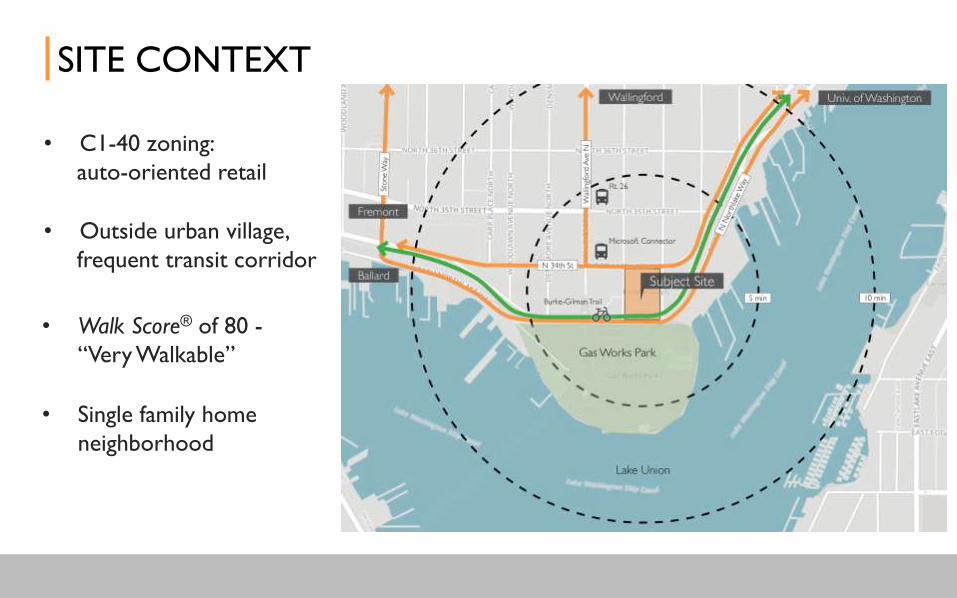

SITE CONTEXT

• C1-40 zoning:

auto-oriented retail

• Walk Score® of 80 -

“Very Walkable”

• Outside urban village,

frequent transit corridor

SITE CONTEXT

• Single family home

neighborhood

Retail Office

Warehouse

SITE IMAGES

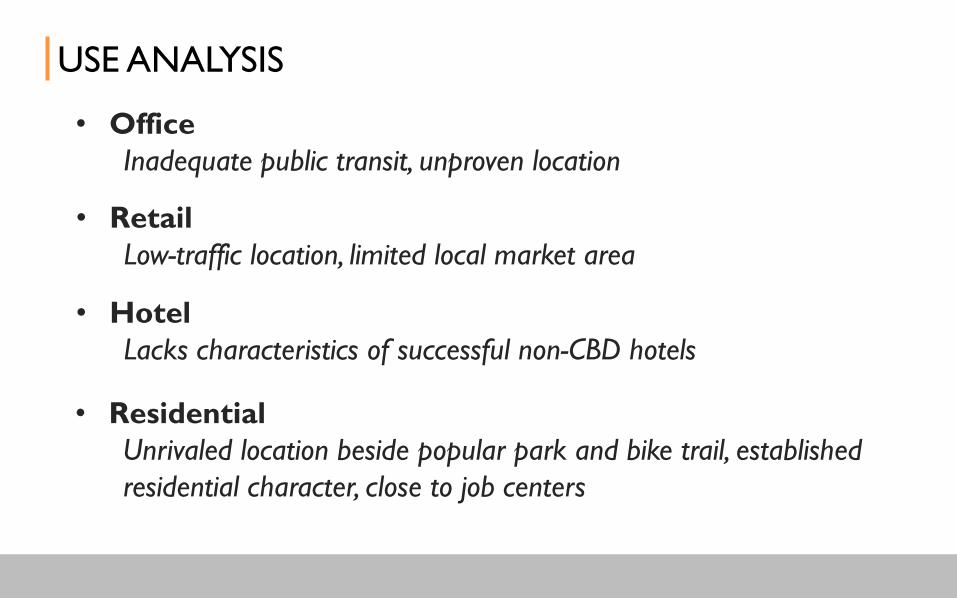

• Office

Inadequate public transit, unproven location

USE ANALYSIS

• Retail

Low-traffic location, limited local market area

• Hotel

Lacks characteristics of successful non-CBD hotels

• Residential

Unrivaled location beside popular park and bike trail, established

residential character, close to job centers

USE ANALYSIS

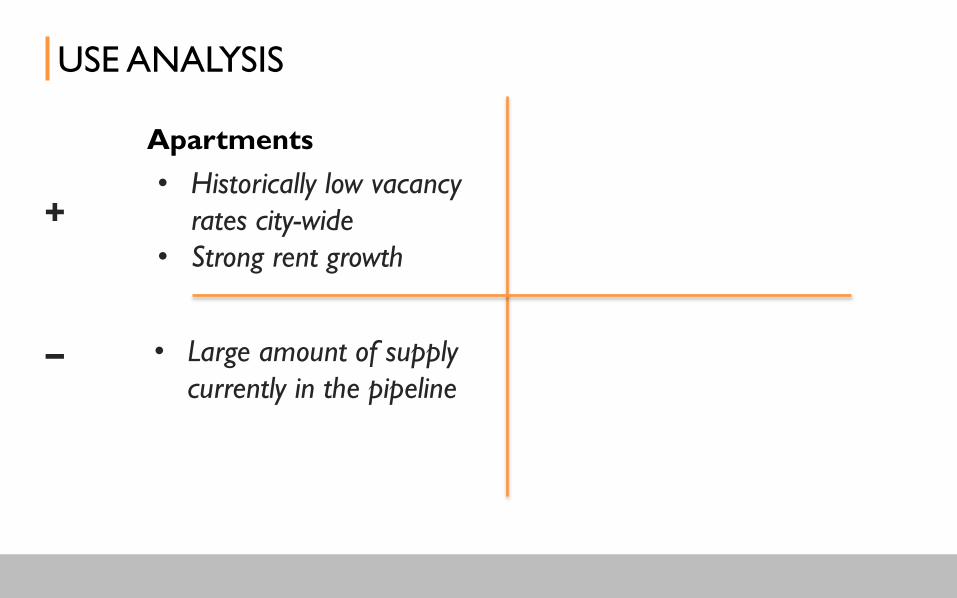

Apartments Condominiums

• Historically low vacancy

rates city-wide

• Strong rent growth

• Little supply

• Low interest rates

• Large amount of supply

currently in the pipeline

+

– • Increased development

complexity

• Interest rates may rise

• Does not mesh with seven-

year hold

MARKET ANALYSIS

02

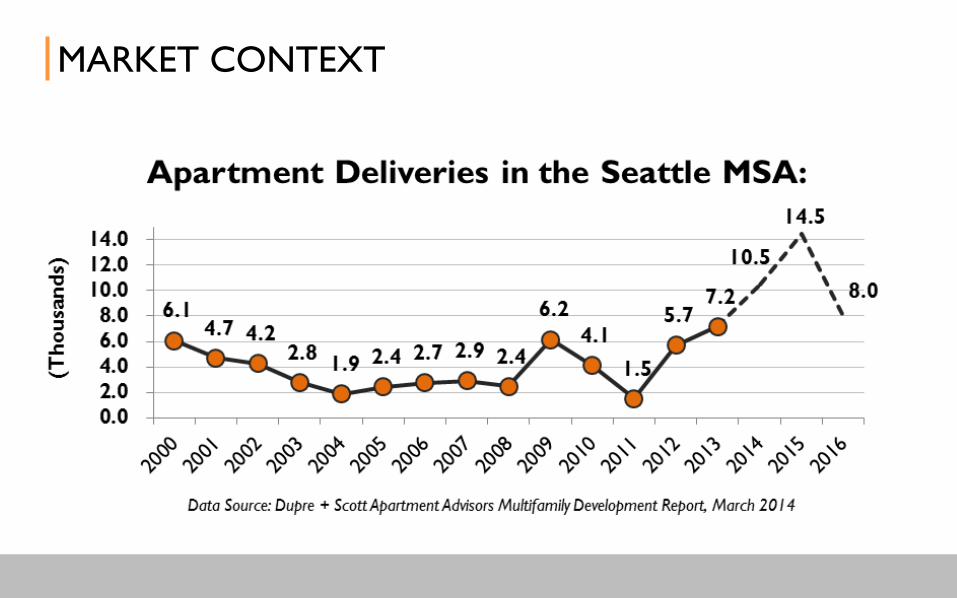

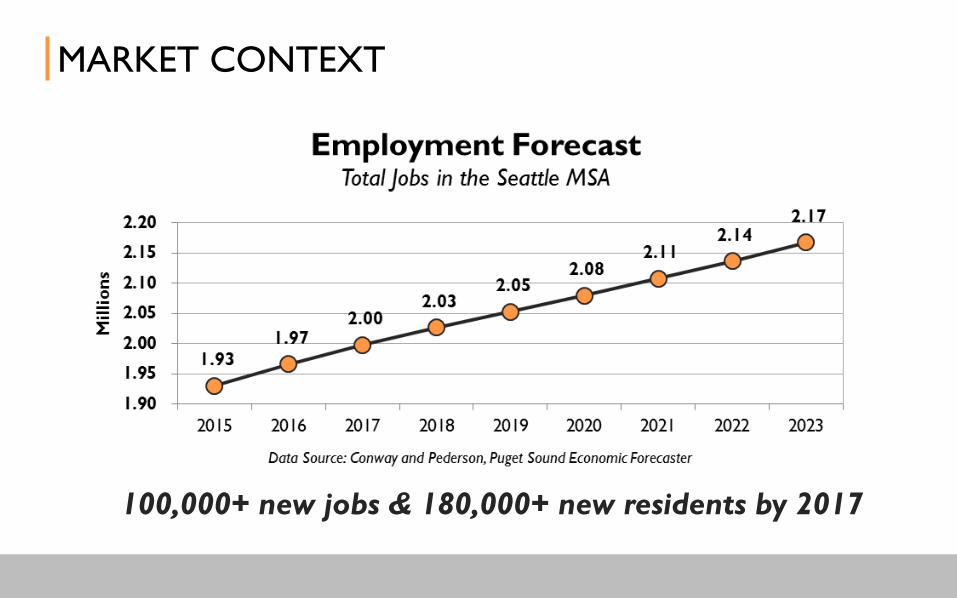

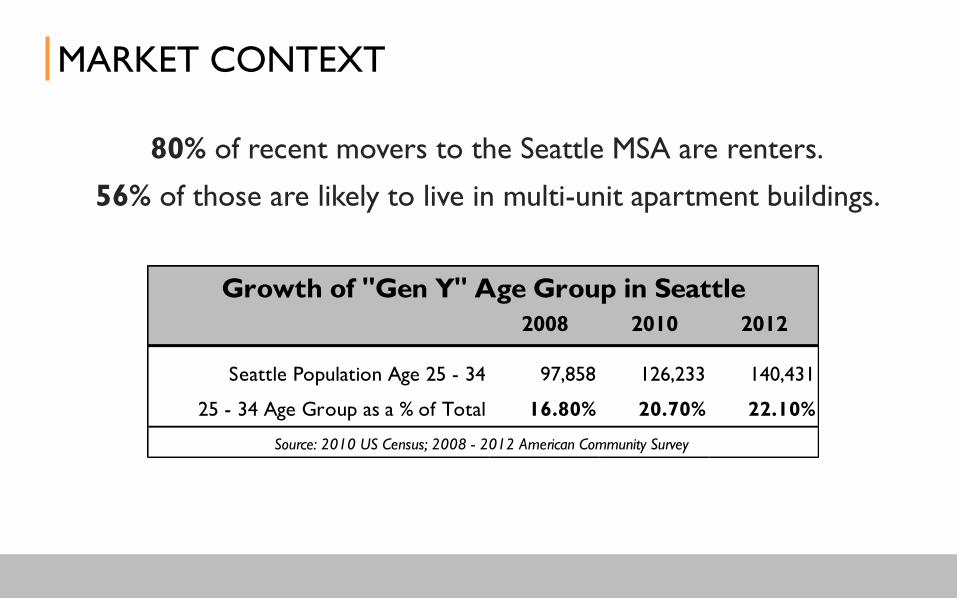

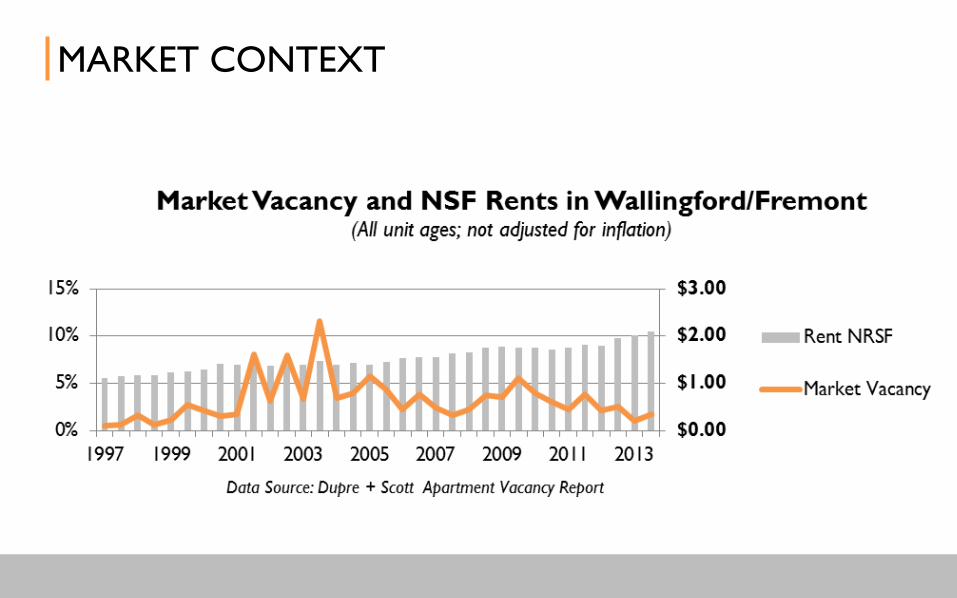

MARKET CONTEXT

MARKET CONTEXT

100,000+ new jobs & 180,000+ new residents by 2017

80% of recent movers to the Seattle MSA are renters.

56% of those are likely to live in multi-unit apartment buildings.

MARKET CONTEXT

2008 2010 2012

Seattle Population Age 25 - 34 97,858 126,233 140,431

25 - 34 Age Group as a % of Total 16.80% 20.70% 22.10%

Growth of "Gen Y" Age Group in Seattle

Source: 2010 US Census; 2008 - 2012 American Community Survey

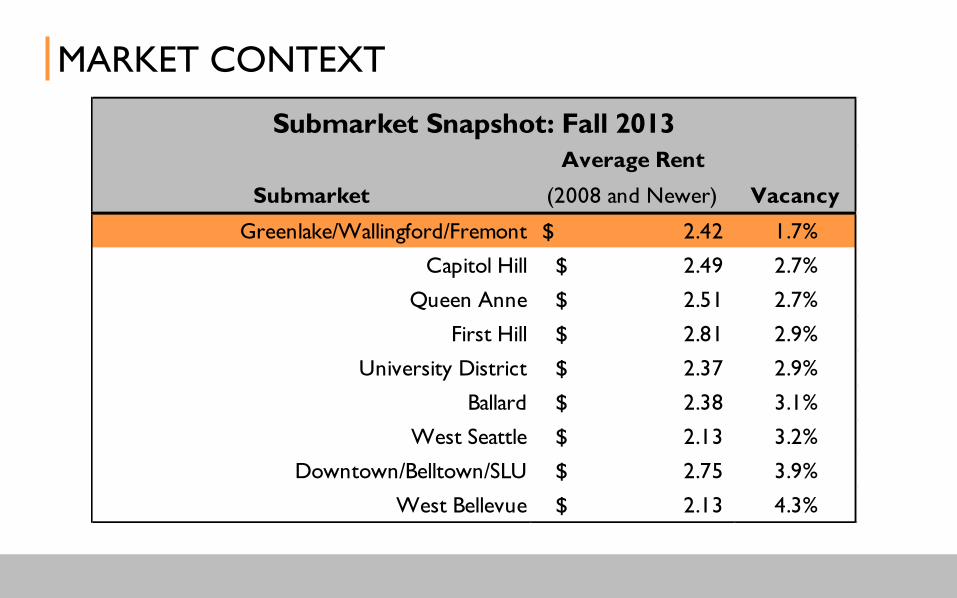

MARKET CONTEXT

Submarket

Average Rent

(2008 and Newer) Vacancy

Greenlake/Wallingford/Fremont 2.42$ 1.7%

Capitol Hill 2.49$ 2.7%

Queen Anne 2.51$ 2.7%

First Hill 2.81$ 2.9%

University District 2.37$ 2.9%

Ballard 2.38$ 3.1%

West Seattle 2.13$ 3.2%

Downtown/Belltown/SLU 2.75$ 3.9%

West Bellevue 2.13$ 4.3%

Submarket Snapshot: Fall 2013

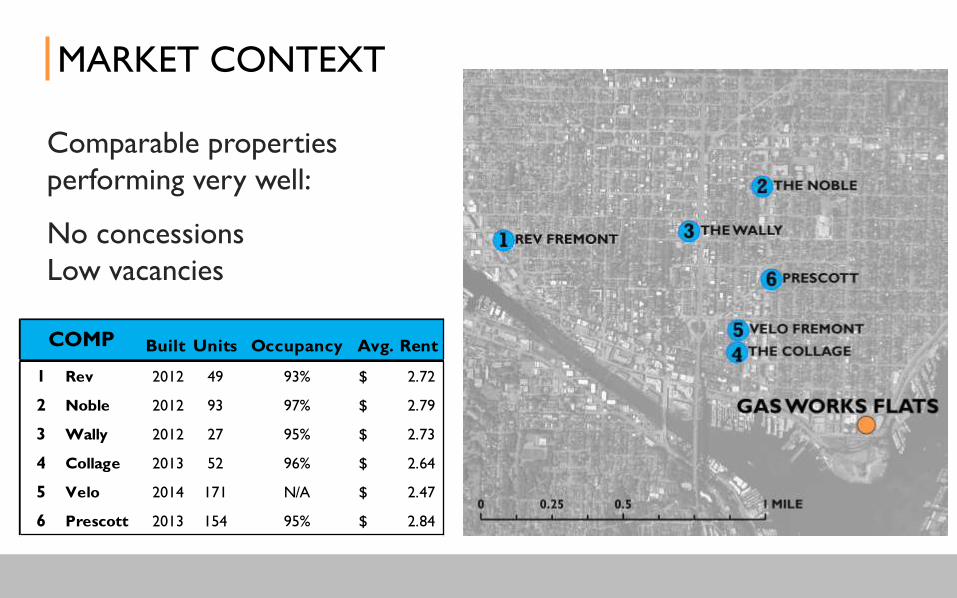

MARKET CONTEXT

MARKET CONTEXT

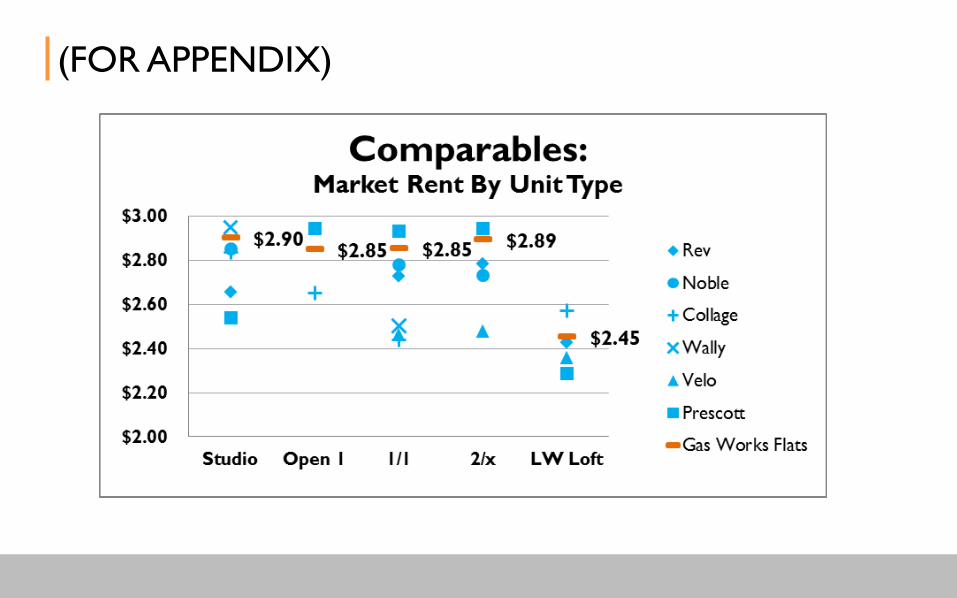

Built Units Occupancy Avg. Rent

1 Rev 2012 49 93% 2.72$

2 Noble 2012 93 97% 2.79$

3 Wally 2012 27 95% 2.73$

4 Collage 2013 52 96% 2.64$

5 Velo 2014 171 N/A 2.47$

6 Prescott 2013 154 95% 2.84$

COMP

Comparable properties

performing very well:

No concessions

Low vacancies

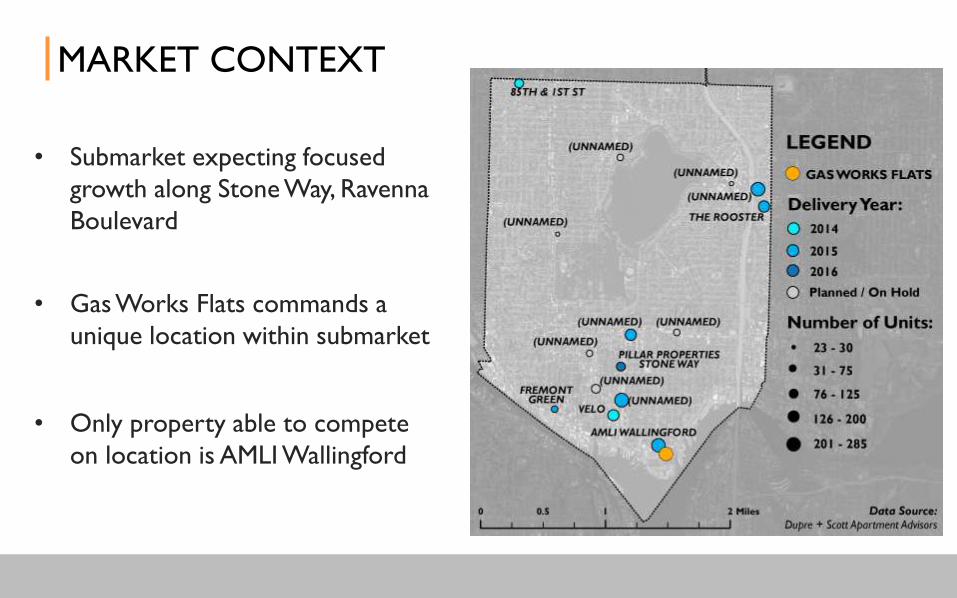

MARKET CONTEXT

• Gas Works Flats commands a

unique location within submarket

• Only property able to compete

on location is AMLI Wallingford

• Submarket expecting focused

growth along Stone Way, Ravenna

Boulevard

WHAT WE’RE PROPOSING

03

DESIGN GOALS

• Embrace the site and its surroundings

• Match product to market demands

• Differentiate by design

• Utilized embodied energy of existing structures

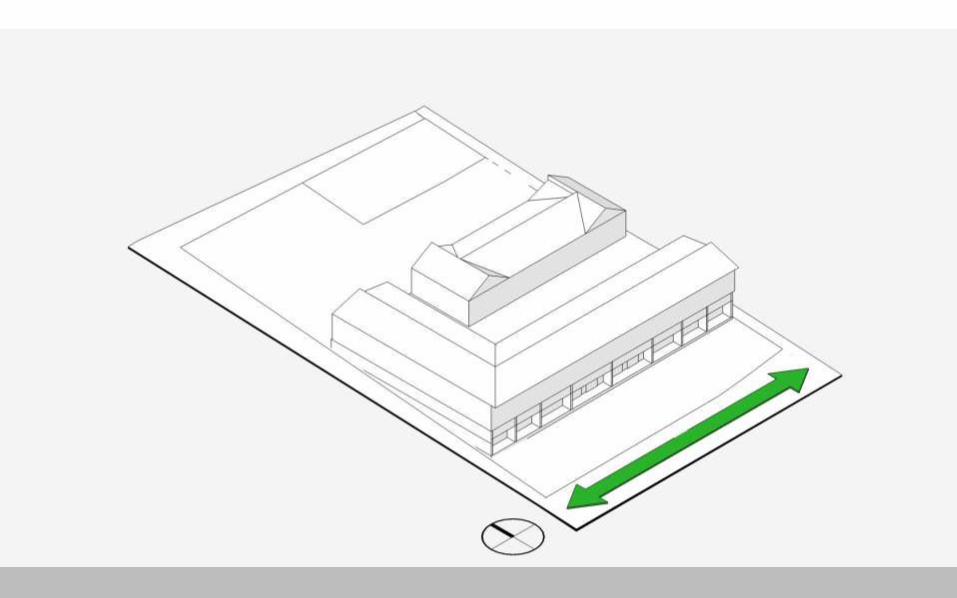

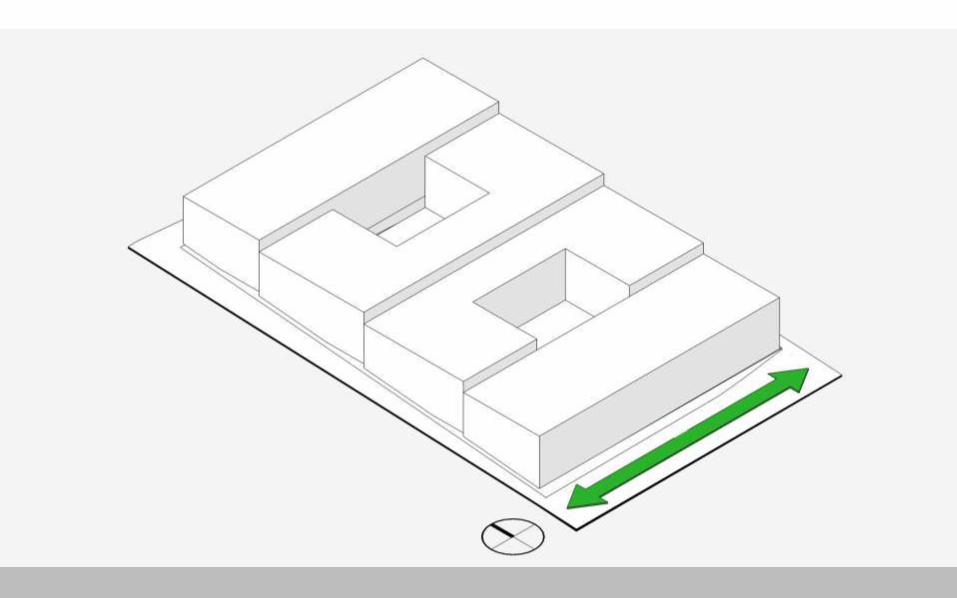

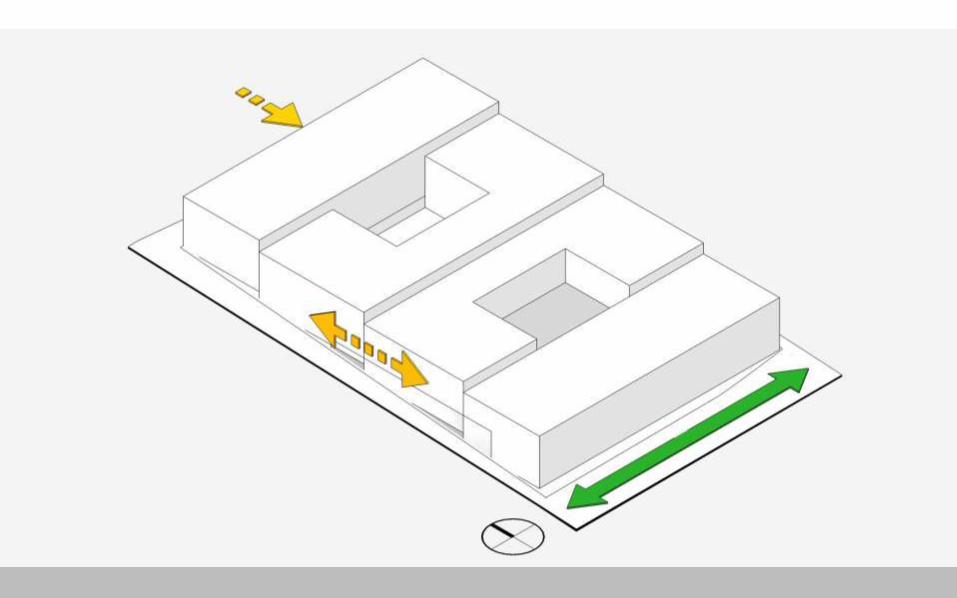

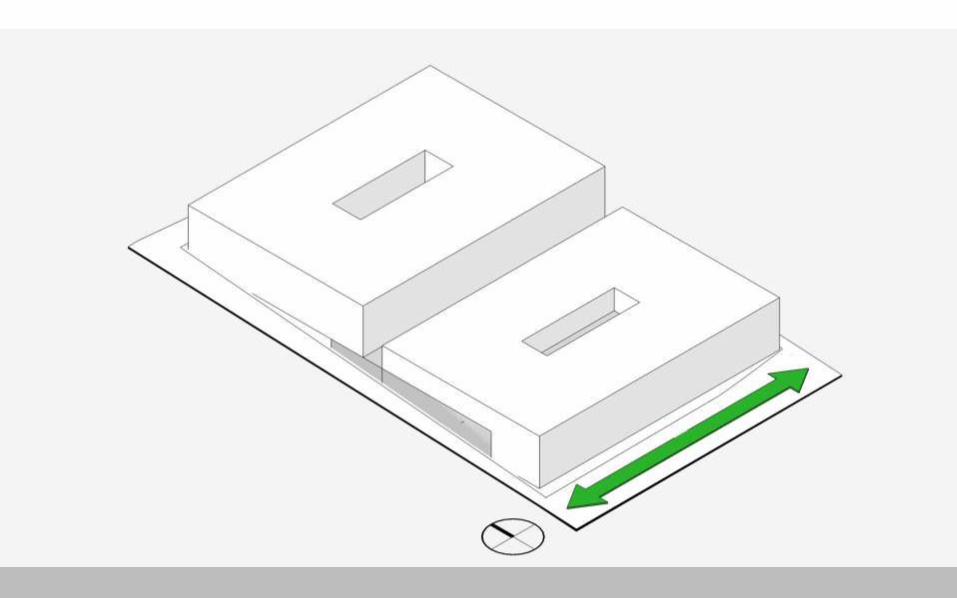

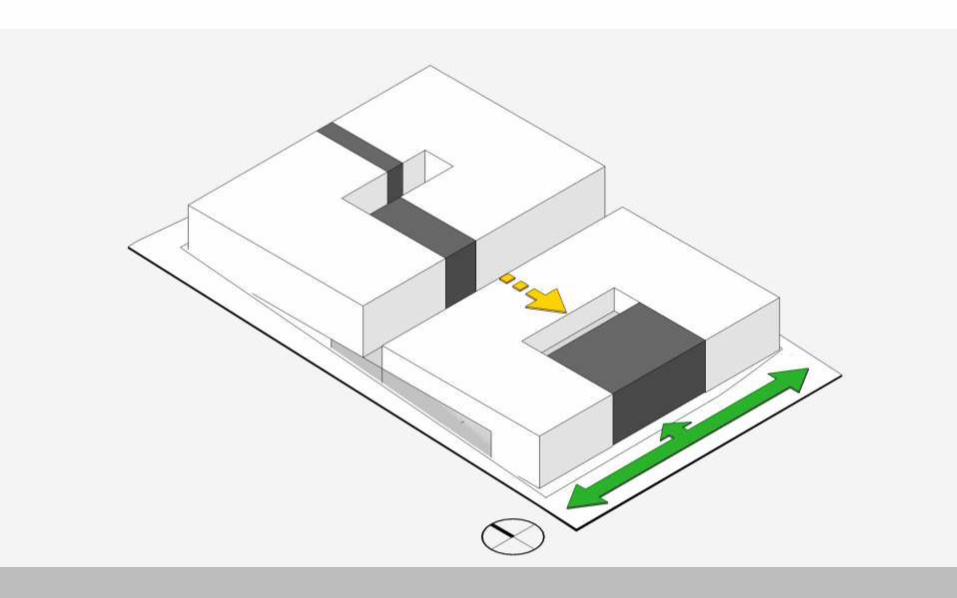

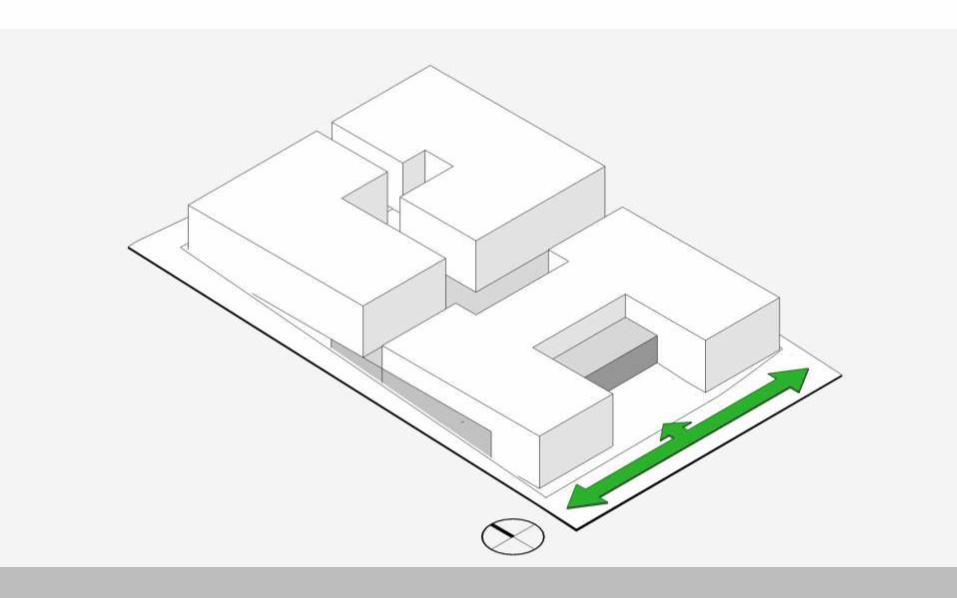

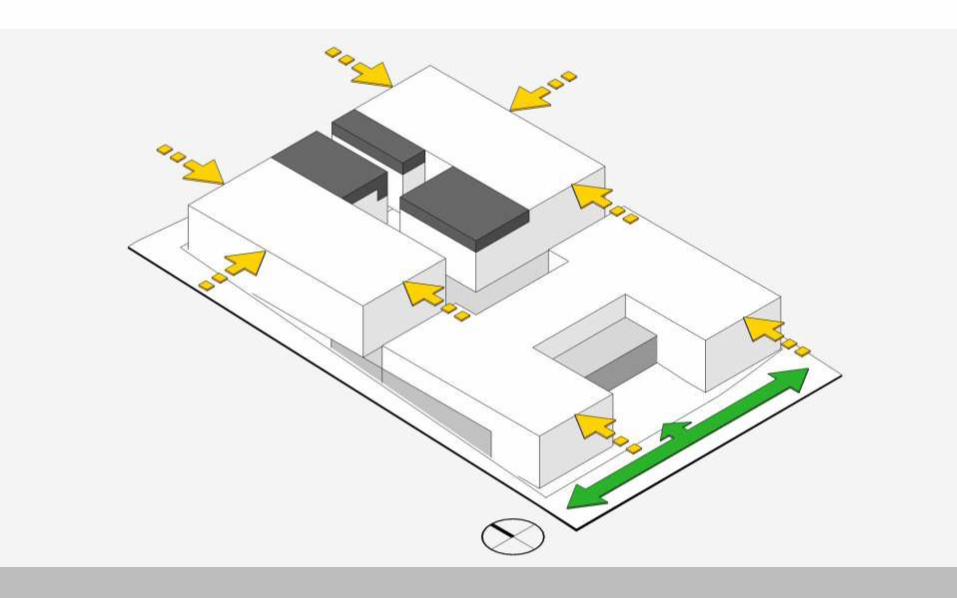

DESIGN PROCESS

DESIGN PROCESS

REUSE – RETAIL AND PARKING

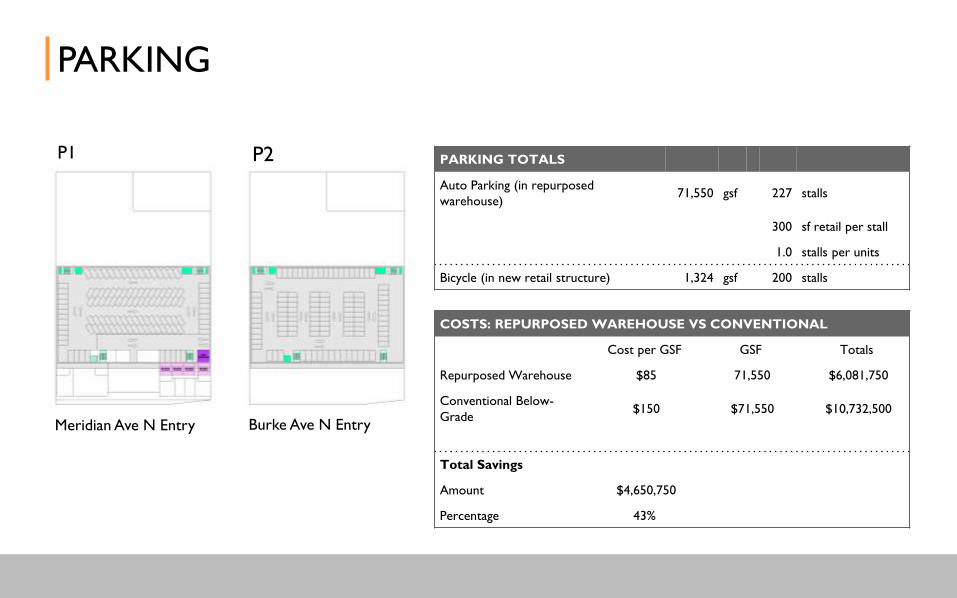

PARKING

PARKING TOTALS

Auto Parking (in repurposed

warehouse)71,550 gsf 227 stalls

300 sf retail per stall

1.0 stalls per units

Bicycle (in new retail structure) 1,324 gsf 200 stalls

COSTS: REPURPOSED WAREHOUSE VS CONVENTIONAL

Cost per GSF GSF Totals

Repurposed Warehouse $85 71,550 $6,081,750

Conventional Below-

Grade$150 $71,550 $10,732,500

Total Savings

Amount $4,650,750

Percentage 43%

P1 P2

Meridian Ave N Entry Burke Ave N Entry

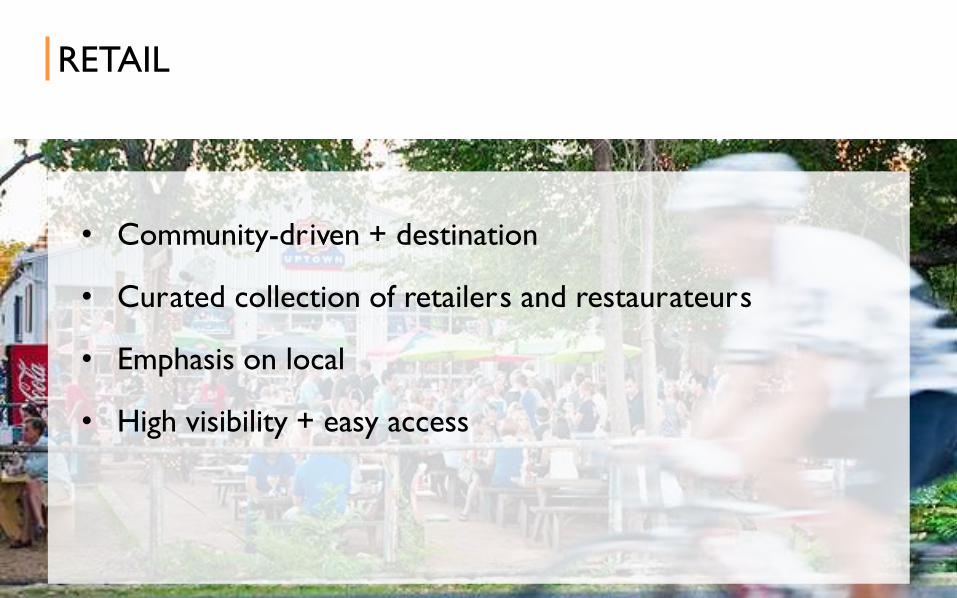

RETAIL

• Community-driven + destination

• Curated collection of retailers and restaurateurs

• Emphasis on local

• High visibility + easy access

GAS WORKS FLATS - SOUTH

69 apartments

industrial, loft-style

10’ floor-to-ceiling height

rooftop courtyard

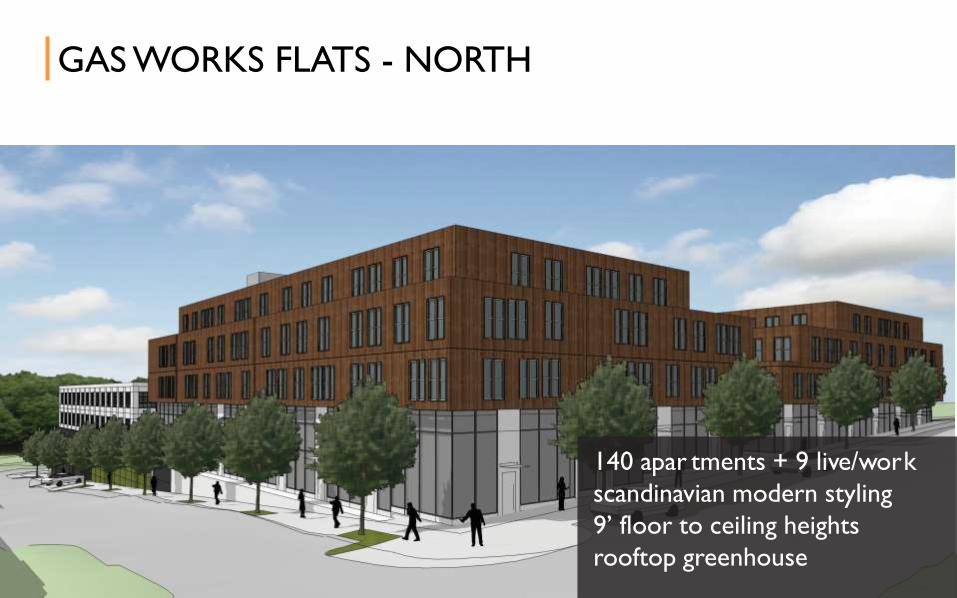

GAS WORKS FLATS - NORTH

140 apar tments + 9 live/work

scandinavian modern styling

9’ floor to ceiling heights

rooftop greenhouse

APARTMENT MIX

25%38%12%25% 9 units

HOW WE’RE GOING TO BUILD IT

04

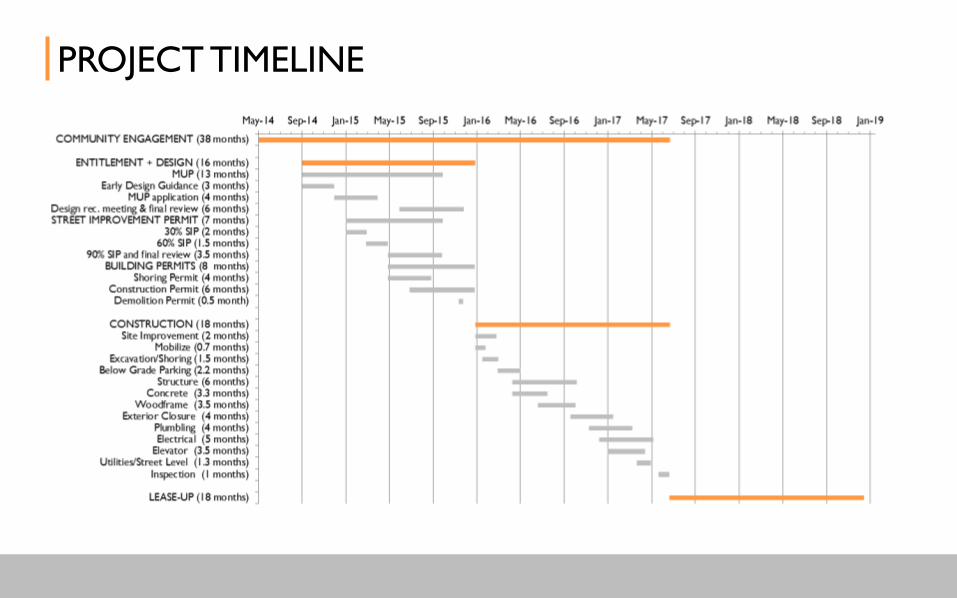

PROJECT TIMELINE

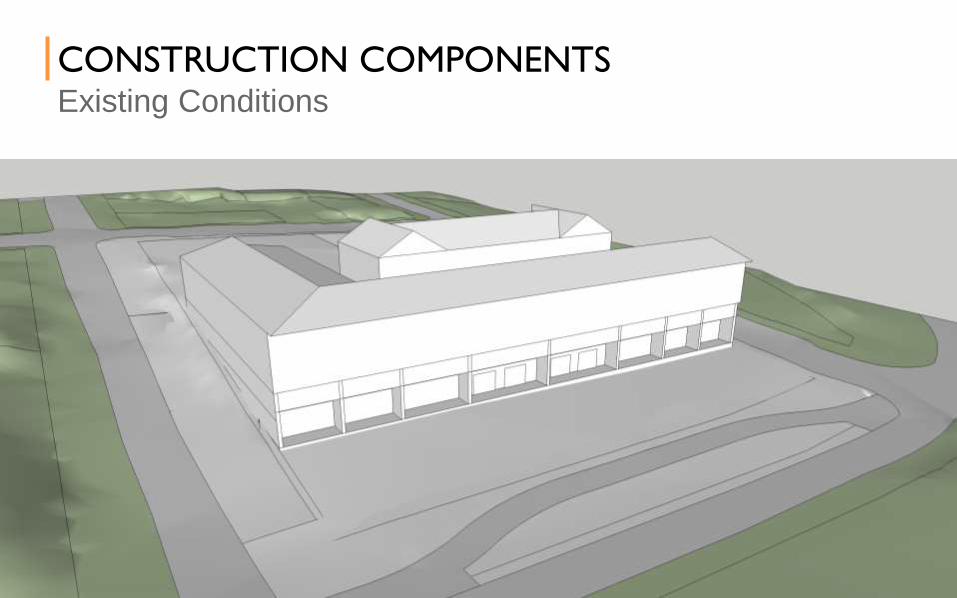

CONSTRUCTION COMPONENTSExisting Conditions

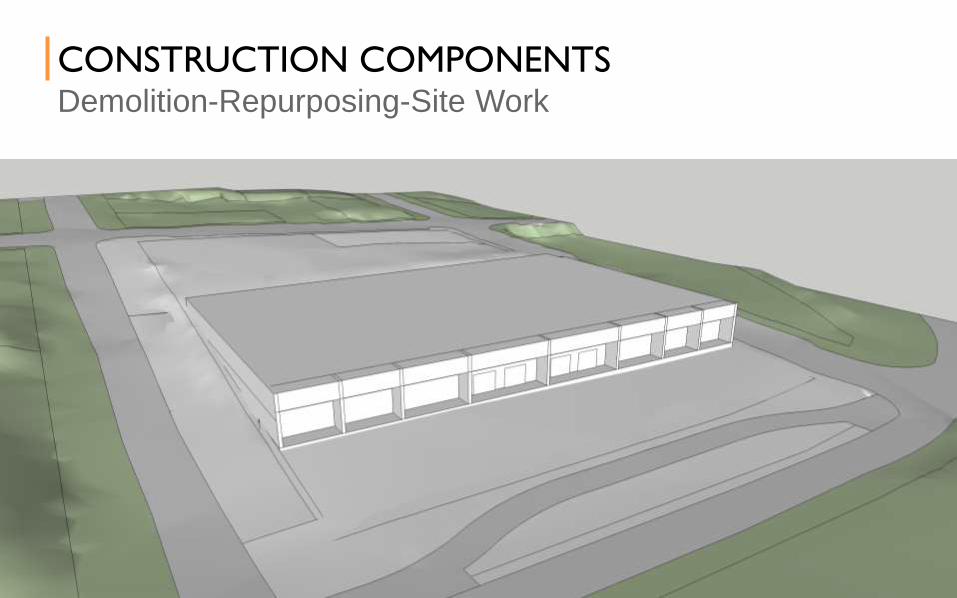

CONSTRUCTION COMPONENTSDemolition-Repurposing-Site Work

CONSTRUCTION COMPONENTSType I-A Construction

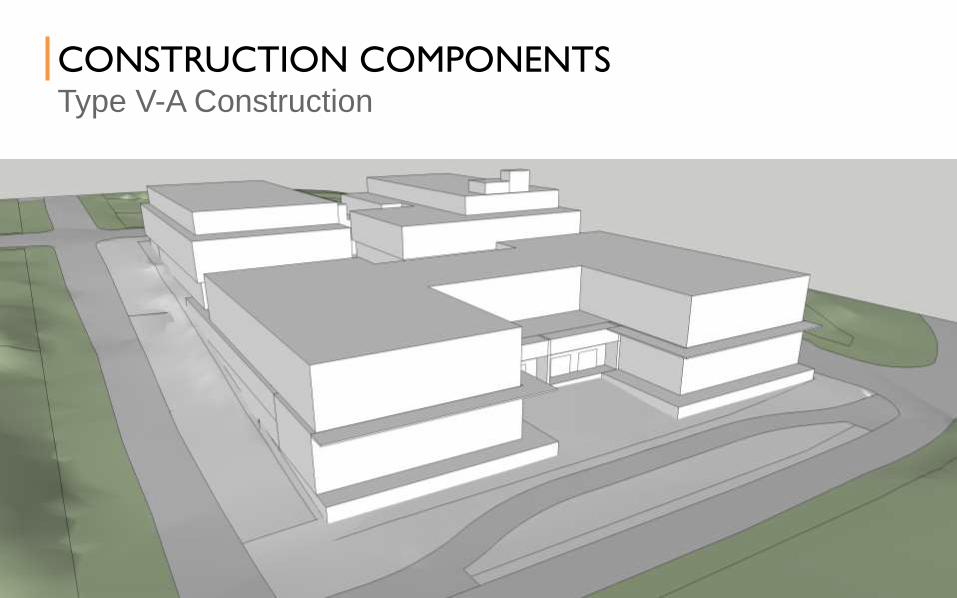

CONSTRUCTION COMPONENTSType V-A Construction

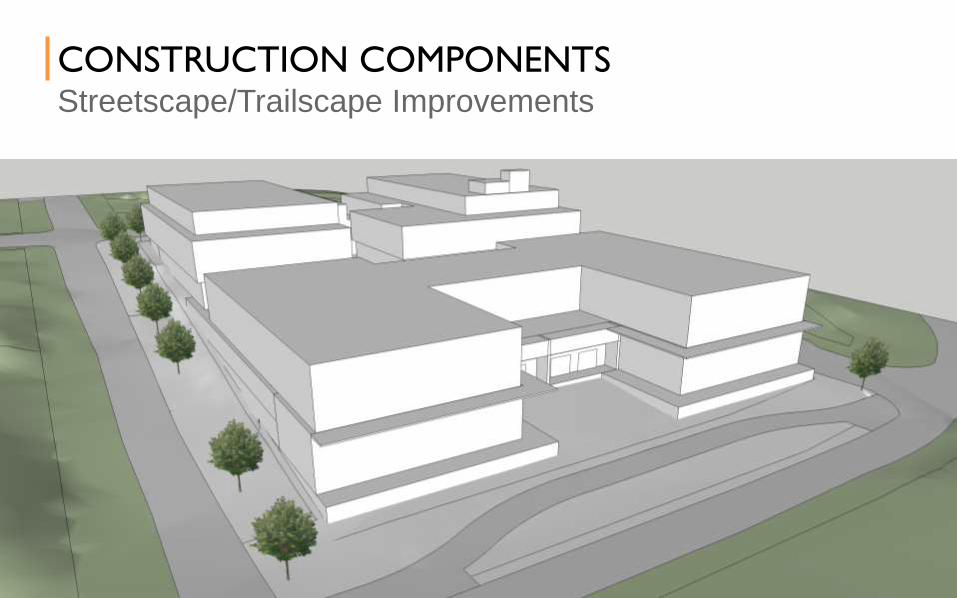

CONSTRUCTION COMPONENTSStreetscape/Trailscape Improvements

HOW IT PERFORMS

05

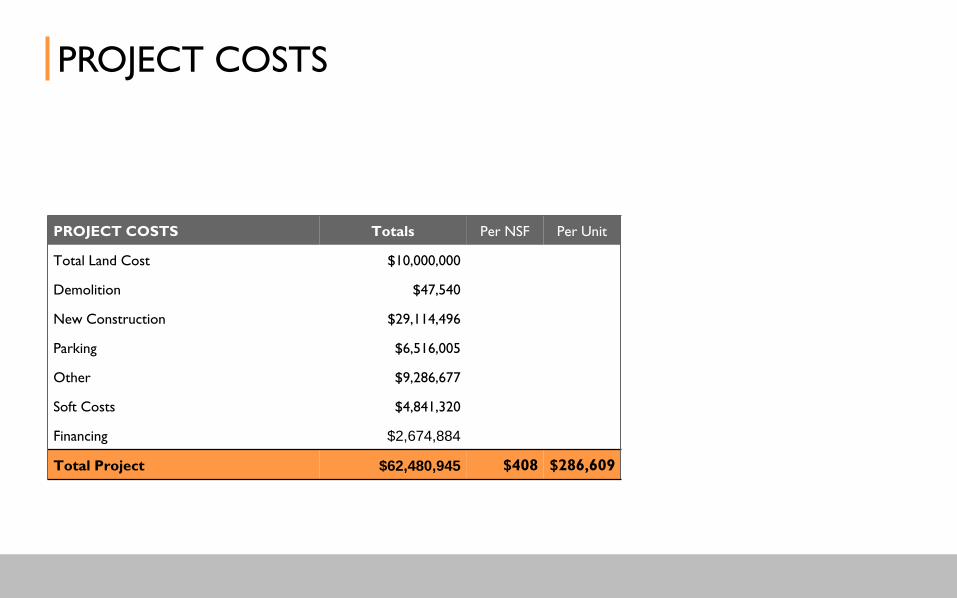

PROJECT COSTS

PROJECT COSTS Totals Per NSF Per Unit

Total Land Cost $10,000,000

Demolition $47,540

New Construction $29,114,496

Parking $6,516,005

Other $9,286,677

Soft Costs $4,841,320

Financing $2,674,884

Total Project $62,480,945 $408 $286,609

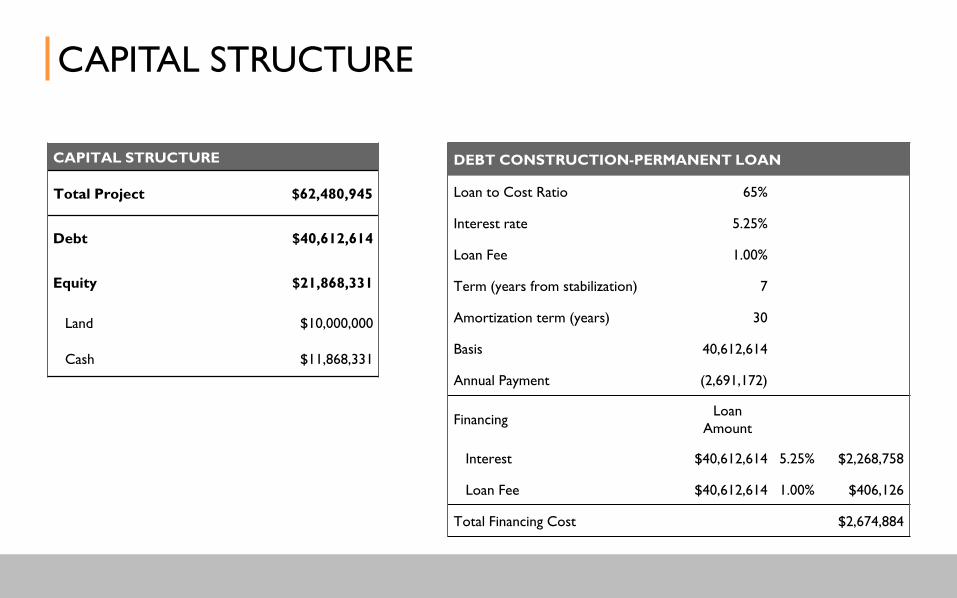

CAPITAL STRUCTURE

DEBT CONSTRUCTION-PERMANENT LOAN

Loan to Cost Ratio 65%

Interest rate 5.25%

Loan Fee 1.00%

Term (years from stabilization) 7

Amortization term (years) 30

Basis 40,612,614

Annual Payment (2,691,172)

FinancingLoan

Amount

Interest $40,612,614 5.25% $2,268,758

Loan Fee $40,612,614 1.00% $406,126

Total Financing Cost $2,674,884

CAPITAL STRUCTURE

Total Project $62,480,945

Debt $40,612,614

Equity $21,868,331

Land $10,000,000

Cash $11,868,331

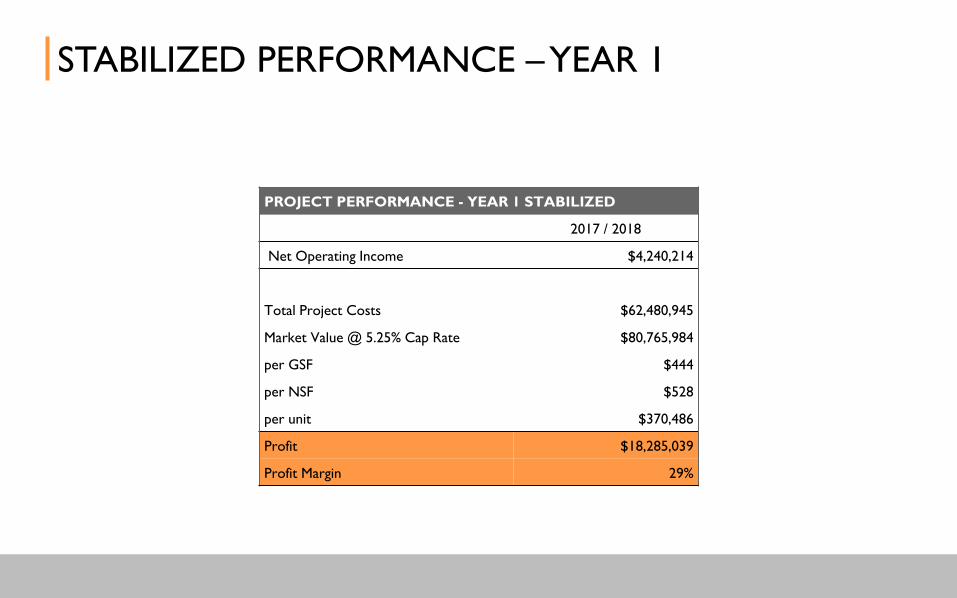

STABILIZED PERFORMANCE –YEAR 1

PROJECT PERFORMANCE - YEAR 1 STABILIZED

2017 / 2018

Net Operating Income $4,240,214

Total Project Costs $62,480,945

Market Value @ 5.25% Cap Rate $80,765,984

per GSF $444

per NSF $528

per unit $370,486

Profit $18,285,039

Profit Margin 29%

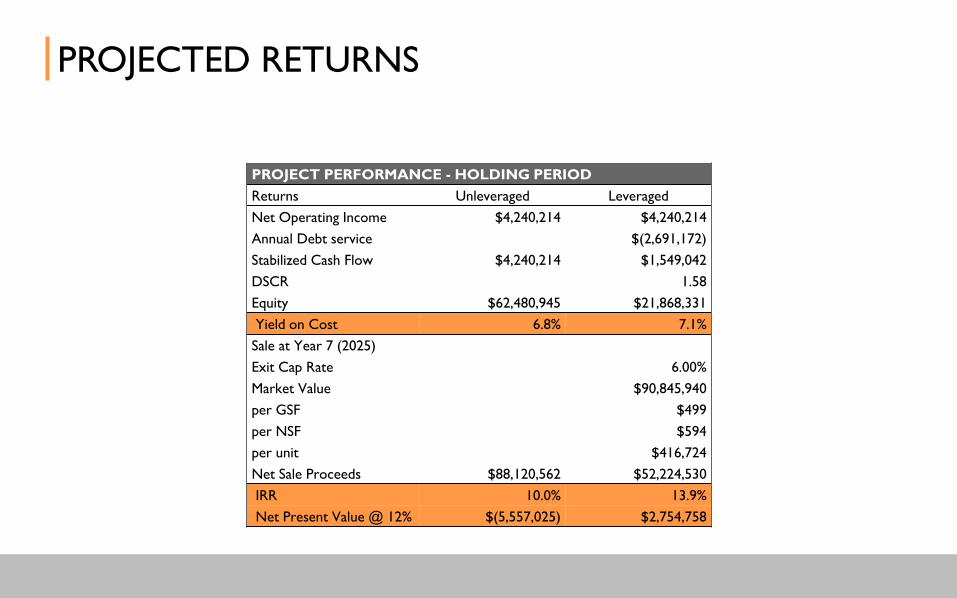

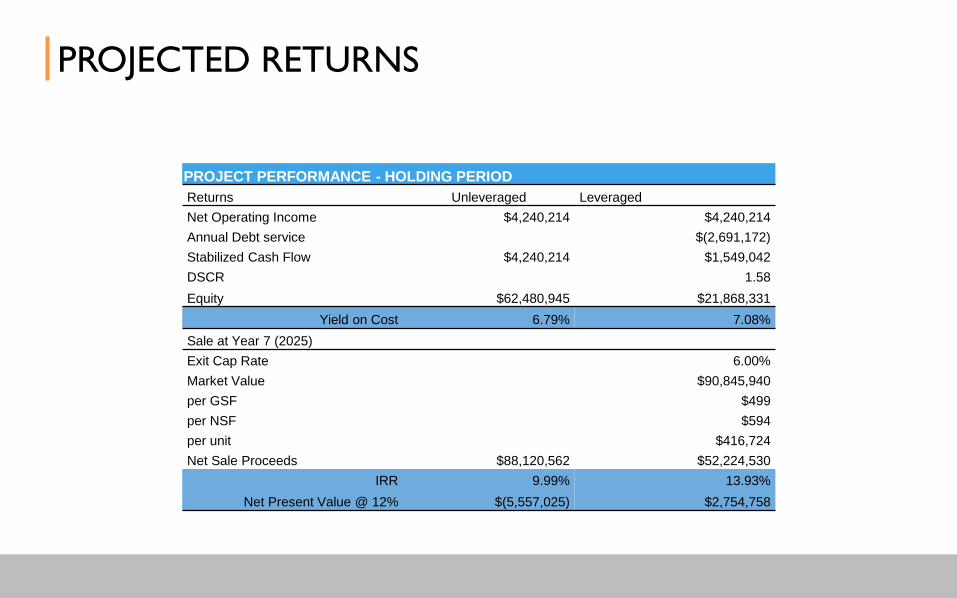

PROJECTED RETURNS

PROJECT PERFORMANCE - HOLDING PERIOD

Returns Unleveraged Leveraged

Net Operating Income $4,240,214 $4,240,214

Annual Debt service $(2,691,172)

Stabilized Cash Flow $4,240,214 $1,549,042

DSCR 1.58

Equity $62,480,945 $21,868,331

Yield on Cost 6.8% 7.1%

Sale at Year 7 (2025)

Exit Cap Rate 6.00%

Market Value $90,845,940

per GSF $499

per NSF $594

per unit $416,724

Net Sale Proceeds $88,120,562 $52,224,530

IRR 10.0% 13.9%

Net Present Value @ 12% $(5,557,025) $2,754,758

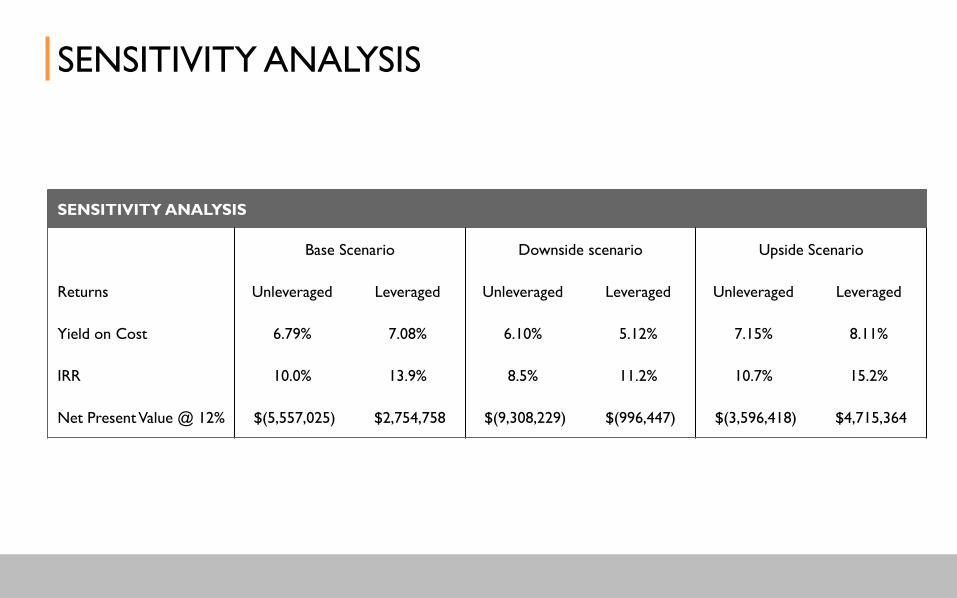

SENSITIVITY ANALYSIS

SENSITIVITY ANALYSIS

Base Scenario Downside scenario Upside Scenario

Returns Unleveraged Leveraged Unleveraged Leveraged Unleveraged Leveraged

Yield on Cost 6.79% 7.08% 6.10% 5.12% 7.15% 8.11%

IRR 10.0% 13.9% 8.5% 11.2% 10.7% 15.2%

Net Present Value @ 12% $(5,557,025) $2,754,758 $(9,308,229) $(996,447) $(3,596,418) $4,715,364

CONCLUSION

APPENDIX

PARKING

PARKING COSTSCost per GSF GSF Totals

Re-Use Parking Costs

Ground Level $50 35,775 $1,788,750

Deck Level $120 35,775 $4,293,000

Total Cost 71,550 $6,081,750

Blended Parking Cost $85

Conventional Below-Grade Parking Costs

1st level $100 $35,775 $3,577,500

2nd level $200 $35,775 $7,155,000

Total Cost $71,550 $10,732,500

Reuse Saving over Conventional Below-

Grade

Total $4,650,750

Percentage 43%

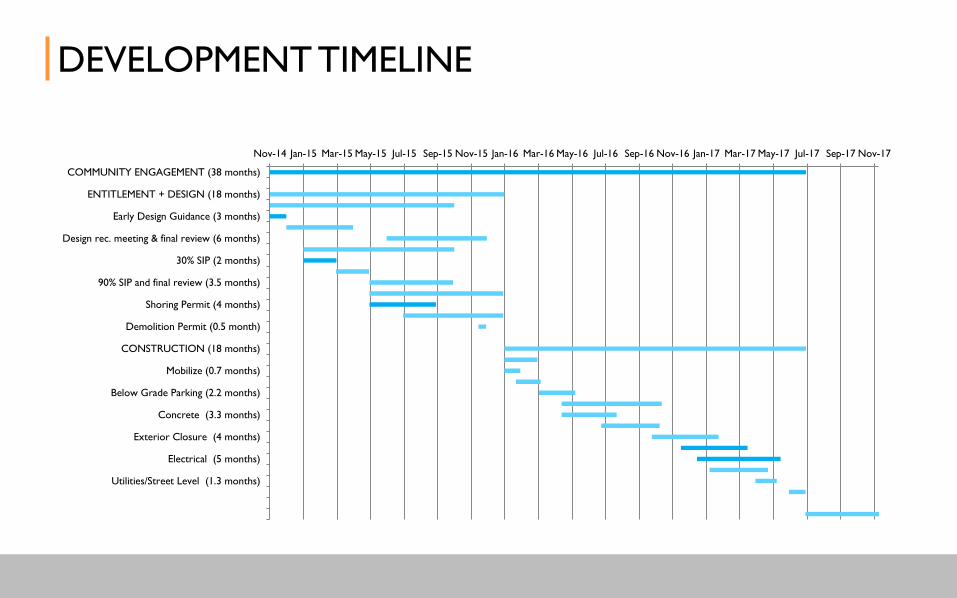

DEVELOPMENT TIMELINE

Nov-14 Jan-15 Mar-15 May-15 Jul-15 Sep-15 Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16 Jan-17 Mar-17 May-17 Jul-17 Sep-17 Nov-17

COMMUNITY ENGAGEMENT (38 months)

ENTITLEMENT + DESIGN (18 months)

Early Design Guidance (3 months)

Design rec. meeting & final review (6 months)

30% SIP (2 months)

90% SIP and final review (3.5 months)

Shoring Permit (4 months)

Demolition Permit (0.5 month)

CONSTRUCTION (18 months)

Mobilize (0.7 months)

Below Grade Parking (2.2 months)

Concrete (3.3 months)

Exterior Closure (4 months)

Electrical (5 months)

Utilities/Street Level (1.3 months)

(FOR APPENDIX)

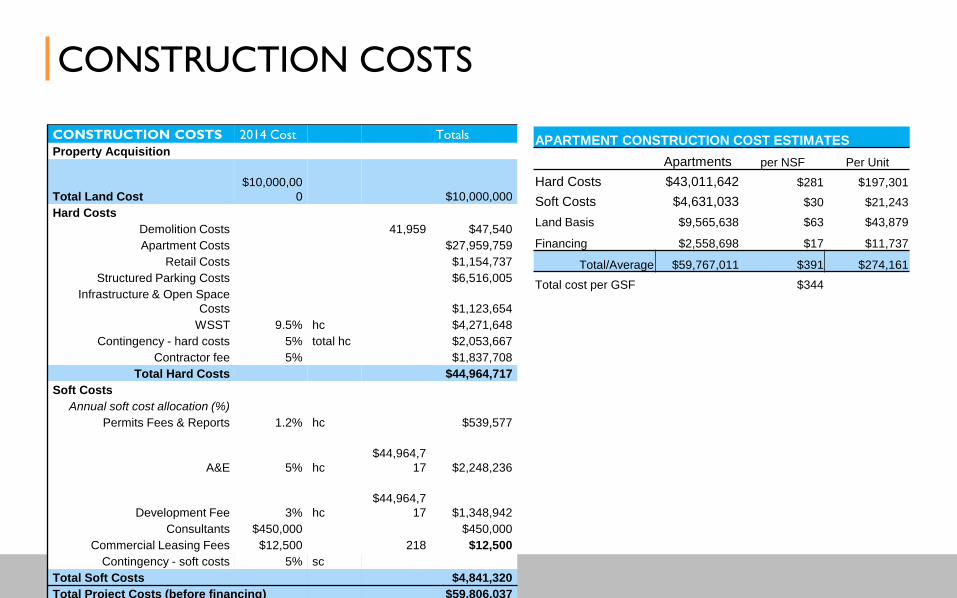

CONSTRUCTION COSTS

CONSTRUCTION COSTS 2014 Cost Totals

Property Acquisition

Total Land Cost

$10,000,00

0 $10,000,000

Hard Costs

Demolition Costs 41,959 $47,540

Apartment Costs $27,959,759

Retail Costs $1,154,737

Structured Parking Costs $6,516,005

Infrastructure & Open Space

Costs $1,123,654

WSST 9.5% hc $4,271,648

Contingency - hard costs 5% total hc $2,053,667

Contractor fee 5% $1,837,708

Total Hard Costs $44,964,717

Soft Costs

Annual soft cost allocation (%)

Permits Fees & Reports 1.2% hc $539,577

A&E 5% hc

$44,964,7

17 $2,248,236

Development Fee 3% hc

$44,964,7

17 $1,348,942

Consultants $450,000 $450,000

Commercial Leasing Fees $12,500 218 $12,500

Contingency - soft costs 5% sc

Total Soft Costs $4,841,320

Total Project Costs (before financing) $59,806,037

APARTMENT CONSTRUCTION COST ESTIMATES

Apartments per NSF Per Unit

Hard Costs $43,011,642 $281 $197,301

Soft Costs $4,631,033 $30 $21,243

Land Basis $9,565,638 $63 $43,879

Financing $2,558,698 $17 $11,737

Total/Average $59,767,011 $391 $274,161

Total cost per GSF $344

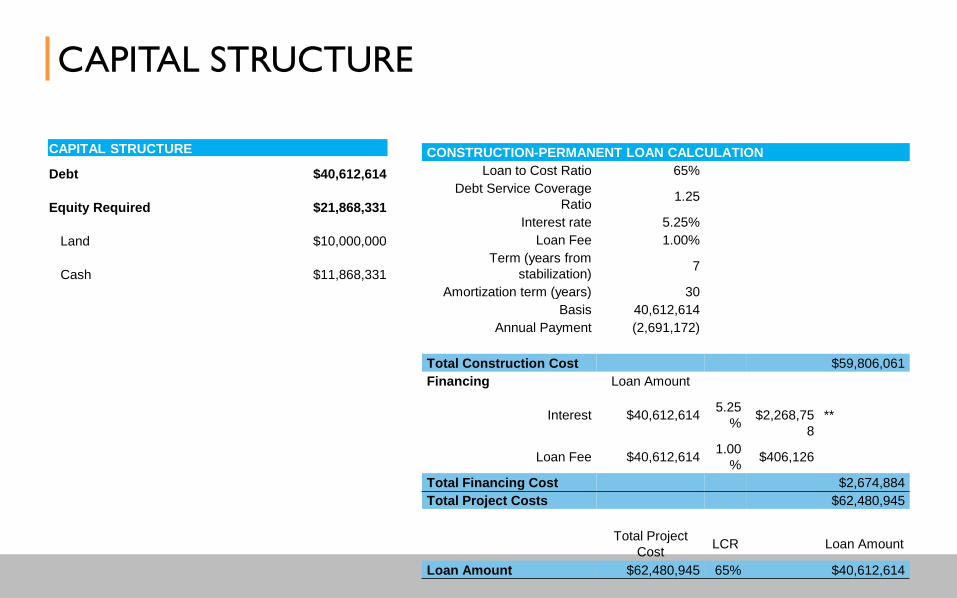

CAPITAL STRUCTURE

CONSTRUCTION-PERMANENT LOAN CALCULATION

Loan to Cost Ratio 65%

Debt Service Coverage

Ratio1.25

Interest rate 5.25%

Loan Fee 1.00%

Term (years from

stabilization)7

Amortization term (years) 30

Basis 40,612,614

Annual Payment (2,691,172)

Total Construction Cost $59,806,061

Financing Loan Amount

Interest $40,612,614 5.25

%$2,268,75

8

**

Loan Fee $40,612,614 1.00

%$406,126

Total Financing Cost $2,674,884

Total Project Costs $62,480,945

Total Project

CostLCR Loan Amount

Loan Amount $62,480,945 65% $40,612,614

CAPITAL STRUCTURE

Debt $40,612,614

Equity Required $21,868,331

Land $10,000,000

Cash $11,868,331

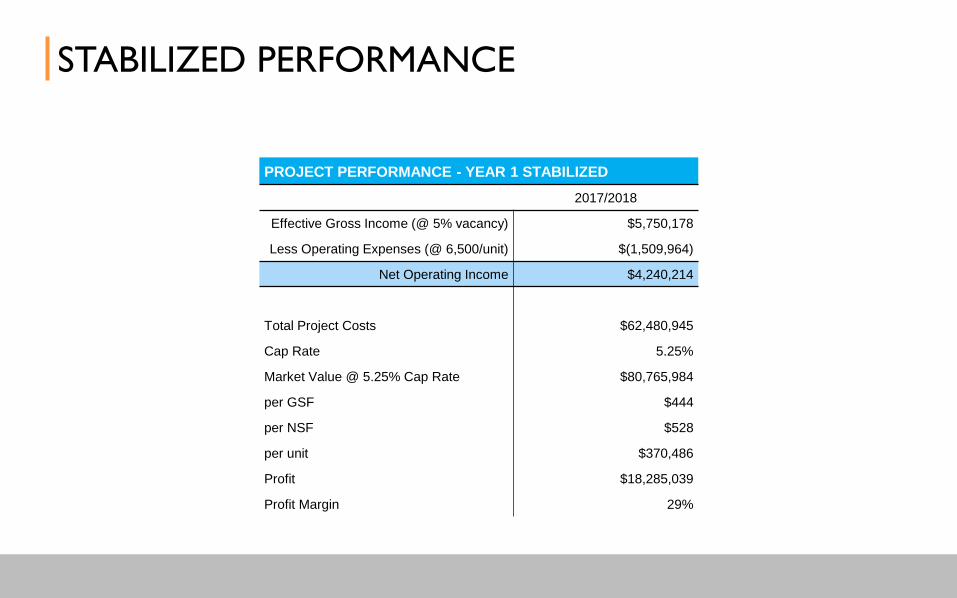

STABILIZED PERFORMANCE

PROJECT PERFORMANCE - YEAR 1 STABILIZED

2017/2018

Effective Gross Income (@ 5% vacancy) $5,750,178

Less Operating Expenses (@ 6,500/unit) $(1,509,964)

Net Operating Income $4,240,214

Total Project Costs $62,480,945

Cap Rate 5.25%

Market Value @ 5.25% Cap Rate $80,765,984

per GSF $444

per NSF $528

per unit $370,486

Profit $18,285,039

Profit Margin 29%

PROJECTED RETURNS

PROJECT PERFORMANCE - HOLDING PERIOD

Returns Unleveraged Leveraged

Net Operating Income $4,240,214 $4,240,214

Annual Debt service $(2,691,172)

Stabilized Cash Flow $4,240,214 $1,549,042

DSCR 1.58

Equity $62,480,945 $21,868,331

Yield on Cost 6.79% 7.08%

Sale at Year 7 (2025)

Exit Cap Rate 6.00%

Market Value $90,845,940

per GSF $499

per NSF $594

per unit $416,724

Net Sale Proceeds $88,120,562 $52,224,530

IRR 9.99% 13.93%

Net Present Value @ 12% $(5,557,025) $2,754,758

SENSITIVITY ANALYSIS

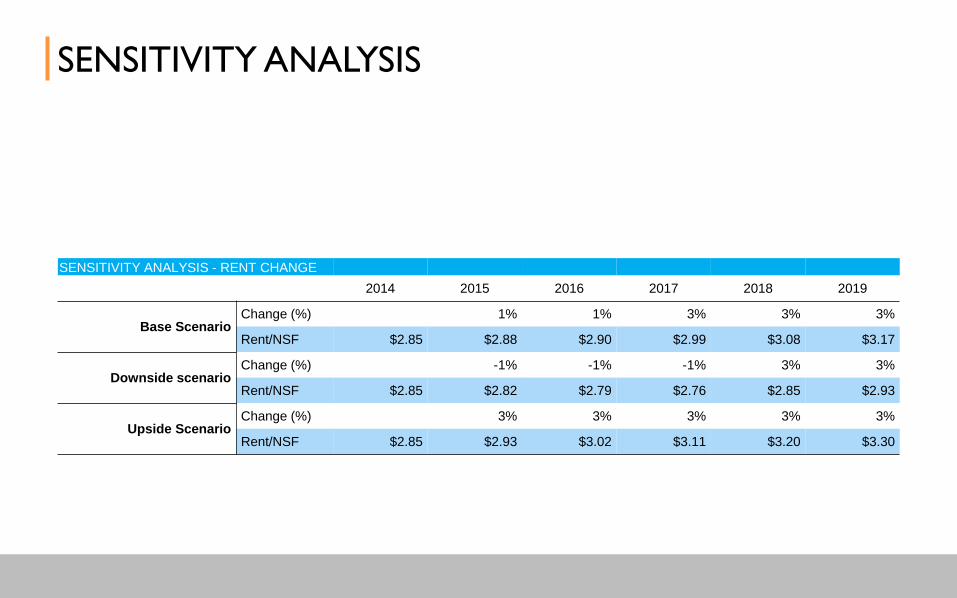

SENSITIVITY ANALYSIS - RENT CHANGE

2014 2015 2016 2017 2018 2019

Base ScenarioChange (%) 1% 1% 3% 3% 3%

Rent/NSF $2.85 $2.88 $2.90 $2.99 $3.08 $3.17

Downside scenarioChange (%) -1% -1% -1% 3% 3%

Rent/NSF $2.85 $2.82 $2.79 $2.76 $2.85 $2.93

Upside ScenarioChange (%) 3% 3% 3% 3% 3%

Rent/NSF $2.85 $2.93 $3.02 $3.11 $3.20 $3.30

SENSITIVITY ANALYSIS

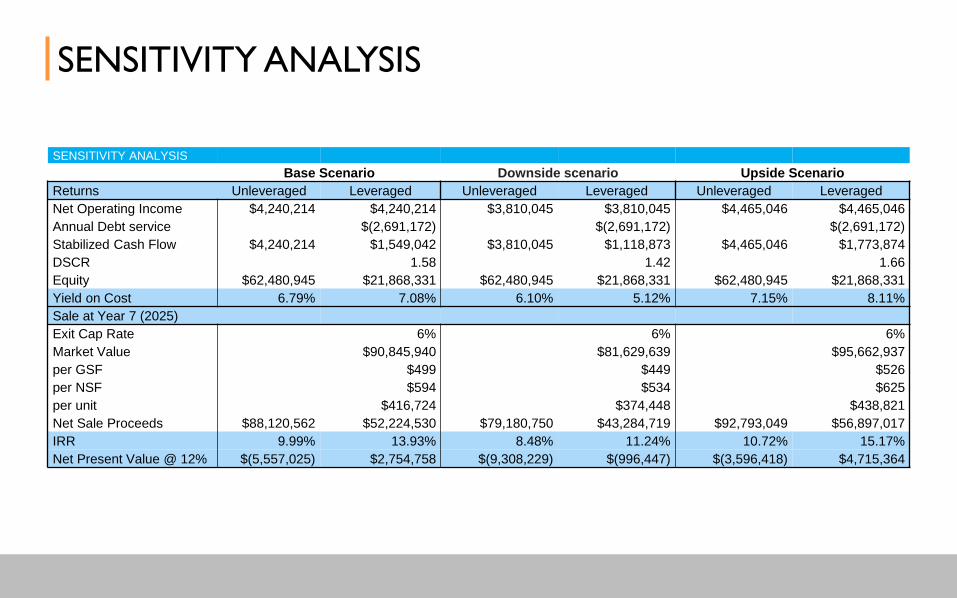

SENSITIVITY ANALYSIS

Base Scenario Downside scenario Upside Scenario

Returns Unleveraged Leveraged Unleveraged Leveraged Unleveraged Leveraged

Net Operating Income $4,240,214 $4,240,214 $3,810,045 $3,810,045 $4,465,046 $4,465,046

Annual Debt service $(2,691,172) $(2,691,172) $(2,691,172)

Stabilized Cash Flow $4,240,214 $1,549,042 $3,810,045 $1,118,873 $4,465,046 $1,773,874

DSCR 1.58 1.42 1.66

Equity $62,480,945 $21,868,331 $62,480,945 $21,868,331 $62,480,945 $21,868,331

Yield on Cost 6.79% 7.08% 6.10% 5.12% 7.15% 8.11%

Sale at Year 7 (2025)

Exit Cap Rate 6% 6% 6%

Market Value $90,845,940 $81,629,639 $95,662,937

per GSF $499 $449 $526

per NSF $594 $534 $625

per unit $416,724 $374,448 $438,821

Net Sale Proceeds $88,120,562 $52,224,530 $79,180,750 $43,284,719 $92,793,049 $56,897,017

IRR 9.99% 13.93% 8.48% 11.24% 10.72% 15.17%

Net Present Value @ 12% $(5,557,025) $2,754,758 $(9,308,229) $(996,447) $(3,596,418) $4,715,364