Embed Size (px)

Citation preview

Smallholder Sugarcane Production in Malawi: An analysis of outgrower participation in the

country’s sugar industry

By

Dr Stephen Atkins

Smallholder Sugarcane Production in Malawi: An analysis of outgrower participation in the country’s sugar industry

This paper:• Details the structure and current dynamics of emerging

sugarcane outgrower sector in Malawi• Provides a focus for Sugarcane Growers Association of Malawi

(SUGAM) to address needs and aspirations of membership • Examines outgrower sugarcane financial production statistics • Estimates contribution of sugarcane to household incomes• Discusses aspects of sugar value chain• Directs SUGAM to an agenda for improving efficiency of

outgrower production systems, and improving transparency and equity in the country’s sugar industry

Agriculture is facing challenges, including:

• very small landholdings devoted to subsistence farming

• low productivity due to land degradation

• declining soil fertility

• lack of irrigation

• lack of diversified farming systems

• poorly developed markets for agricultural inputs and produce

• weak service provision (especially rural financial services, agricultural research and extension)

Agriculture’s Success

• Commercial sugarcane introduced into Malawi in the 1960s with considerable success (Gosnell 2005)

• Sugar production value chain is highly ordered with many different bye-products

• Illovo, multinational miller-cum-planter is currently the only miller in the country.

Oldest mill at Nchalo came into production in August 1964

Second mill commissioned in 1979

Both mills considered very efficient (MG NAS Report 2006)

• Ethanol distillery attached to Dwangwa mill in 1982 by the Ethanol Company Ltd

• 2004 second plant was built by PressCane close to Nhcalo

• GBI building a mini-mill close to Salima

• Another mini-mill built by Mtalimanja Sugar Corporation at Nkhoktakota

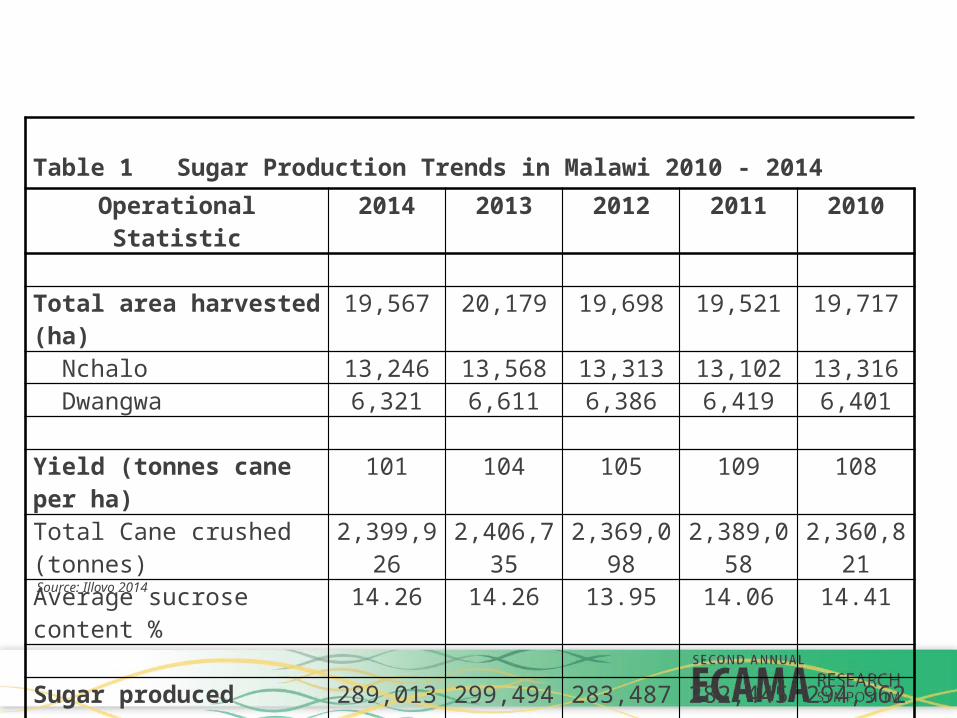

Table 1 Sugar Production Trends in Malawi 2010 - 2014

Operational Statistic 2014 2013 2012 2011 2010

Total area harvested (ha) 19,567 20,179 19,698 19,521 19,717 Nchalo 13,246 13,568 13,313 13,102 13,316 Dwangwa 6,321 6,611 6,386 6,419 6,401 Yield (tonnes cane per ha) 101 104 105 109 108Total Cane crushed (tonnes) 2,399,926 2,406,735 2,369,098 2,389,058 2,360,821Average sucrose content % 14.26 14.26 13.95 14.06 14.41 Sugar produced (tonnes) 289,013 299,494 283,487 282,445 294,962Domestic market % 58% 55% 57% 62% 66%Export market % 42% 45% 43% 38% 34%

Source: Illovo 2014

Outgrower Participation

• Smallholder outgrowers encouraged from early-on • 1979 Smallholder Sugar Authority established close to Dwangwa mill

catering for irrigated cane• Privatised in 1999 into two entities – Dwangwa Cane Growers Trust

and Dwangwa Cane Growers Ltd• Other outgrower schemes came under umbrella • Friction between entrants and SCGT/L – breakaways strarted• 1997 Kasinthula Phases I supported by operating company Shire

Valley Cane Growers Ltd and Shire Valley Cane Growers Trust • Kasinthula Phases II to IV between 2000 and 2013• Phata Sugarcane Cooperative established 2013 managed by Agricane• All above irrigated outgrower schemes• Rainfed outgrowers recently joined the industry at Dwangwa especially

in last few years

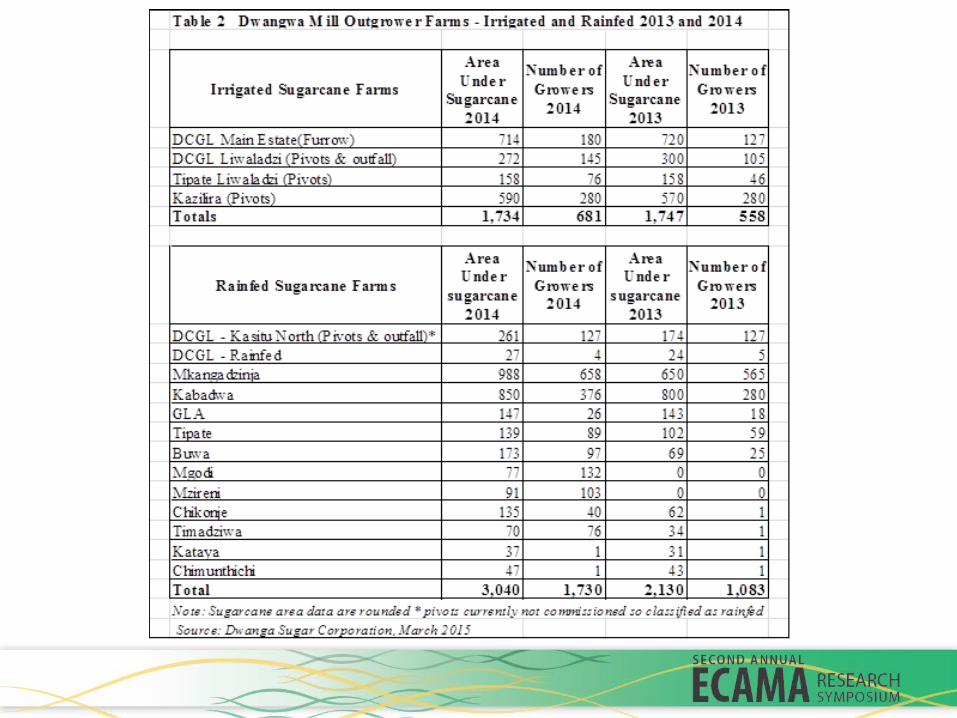

• 2005 outgrowers at Dwangwa mill were 443 • By 2014 grown to 1,730• Dramatic increase of 647 between 2013 and 2014• Expansion from rainfed cane area, but limited by capital and labour• Lack of capital and water for expansion of irrigated area• Majority of rainfed outgrowers cultivate small plots spread over very

large geographical area • Analysis of individual cropped area data provided for 37 members of

one association– combined sugarcane area 24 hectares– average size cane grown 3.35 Ha (SD 4.32) – 30 % cultivated <1 Ha– 76 %cultivated <4 Ha– Minimum 0.4 Ha, maximum 25 Ha

Outgrower Participation

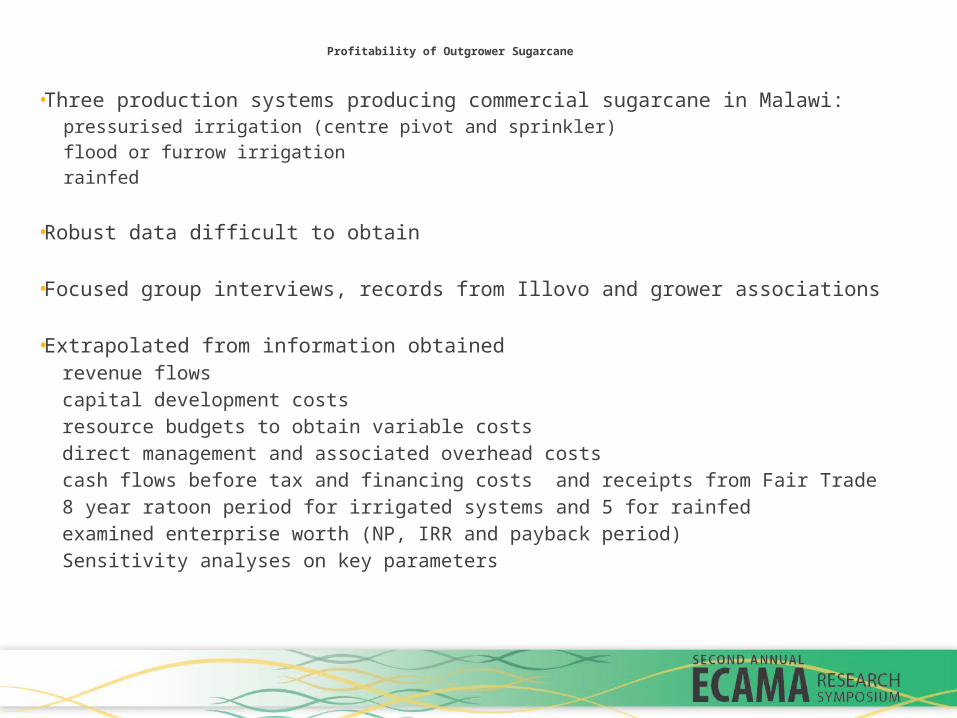

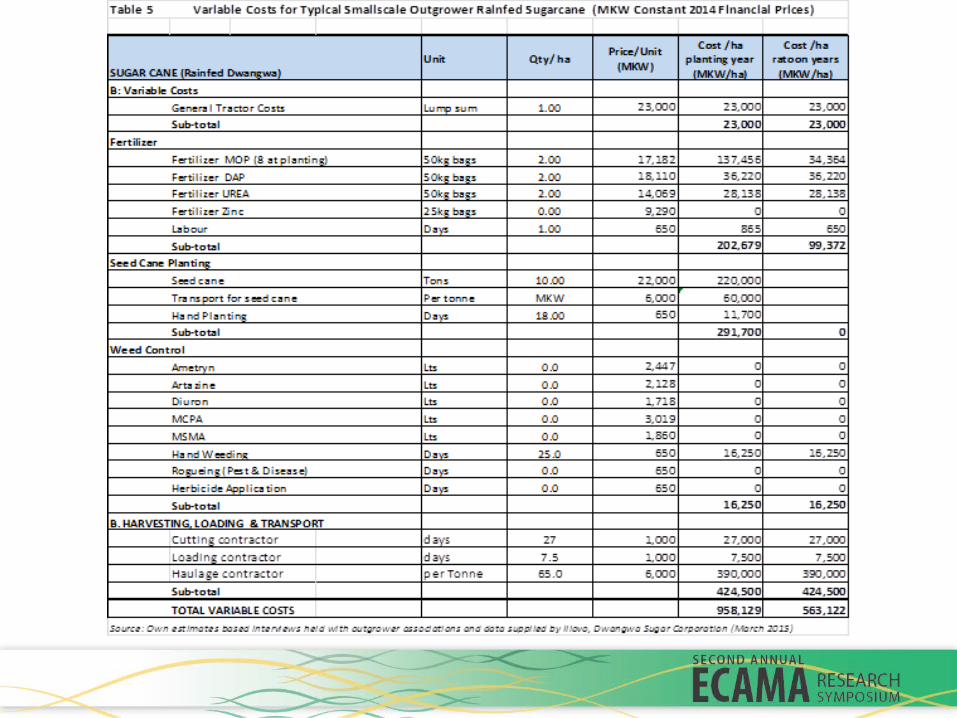

Profitability of Outgrower Sugarcane

• Three production systems producing commercial sugarcane in Malawi:pressurised irrigation (centre pivot and sprinkler)

flood or furrow irrigation

rainfed

• Robust data difficult to obtain

• Focused group interviews, records from Illovo and grower associations

• Extrapolated from information obtainedrevenue flows

capital development costs

resource budgets to obtain variable costs

direct management and associated overhead costs

cash flows before tax and financing costs and receipts from Fair Trade

8 year ratoon period for irrigated systems and 5 for rainfed

examined enterprise worth (NP, IRR and payback period)

Sensitivity analyses on key parameters

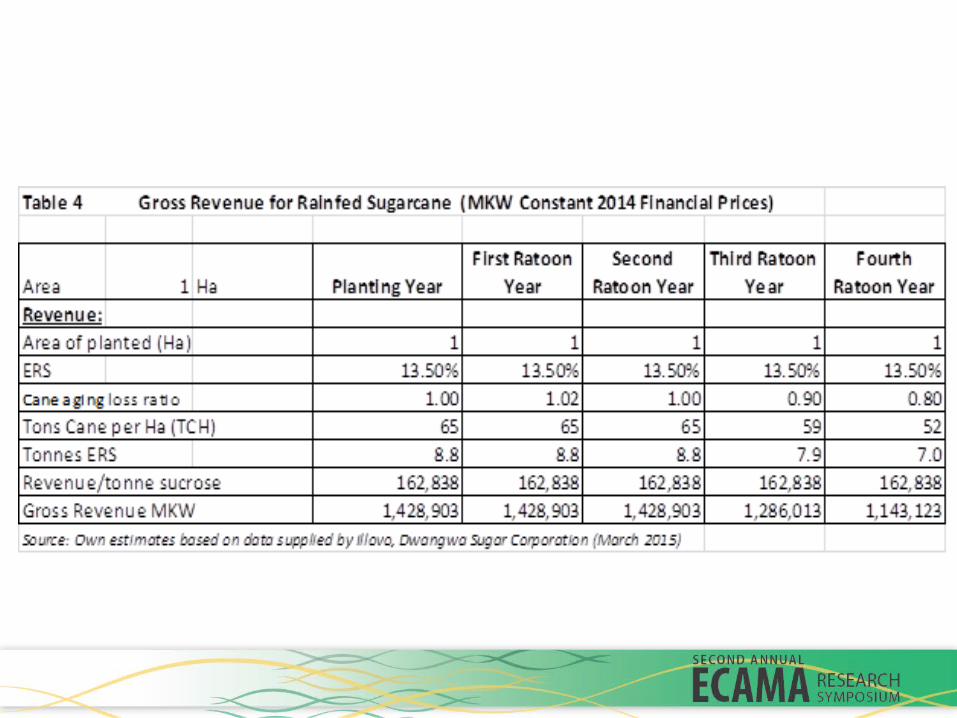

Table 6 Indicative Cash Flows for Outgrower Sugarcane Production in Malawi (US$/Ha Constant 2014 Financial Prices)

Parameter

Lower Shire centre pivot irrigation

Dwangwa centre pivot irrigation

Dwangwa furrow

irrigation

Dwangwa rainfed

Net cash flow before financing and tax during 1st harvest year

-9,331

-9,157

-7,100

831

Average net annual cash flow for ratoon years before financing and tax

3,297

2,921

3,230

1,831

Plough-out year 8 8 8 5

NPV (US$/Ha) 4,442 3,490 6,269 4,435

IRR % 28% 25% 28% 928%

Break-even year 3 4 3 1

Table 8 Sensitivity analysis for four sugarcane production systems in Malawi (US$/Ha)

Lower Shire Centre Pivot

Dwangwa Centre Pivot

Dwangwa Flood

IrrigationDwangwa Rainfed

Base Case NPV (US$) 4,442 3,490 6,269 4,435

Tax deducted from Gross Revenue (30%) NPV (US$) (4,410) (1,820) (2,937) 1,461Revenue Increased by 20% NPV (US$) 10,344 688 12,404 4,417 Switching Value (%) -15% -11% -20% -45%

Variable Costs increased by 20% NPV (US$) 2,762 1,230 4,315 3,357Variable costs decreased by 20% NPV (US$) 6,212 5,751 8,333 5,513 Switching Value (%) 50% 30% 64% 82%

Admin Overheads increased by 20% NPV (US$) 3,205 2,253 5,032 4,202Admin overheads decreased by 20% NPV (US$) 5,679 4,728 7,506 4,668 Switching Value (%) 30% 56% 200% 380%

Profitability of sugarcane production systems• Cash flows highly sensitive to sucrose yields and prices• Sucrose yields depend on good crop management by outgrowers • Outgrower sugarcane management teams

mixed ability

differing pricing systems

lack of business plans

cash flow problems

poor record keeping

lack of financial management skills (not accounting skills)

• Poor dissemination and transparency of information • Haulage costs are a high proportion of variable costs• Rainfed cane haulage systems very inefficient• Rural roads poor• Rainfed haulage contractors are small, poorly run enterprises• Loan interest rates onerous – +/- 46% per annum• Sugarcane can assist rural households move out of poverty

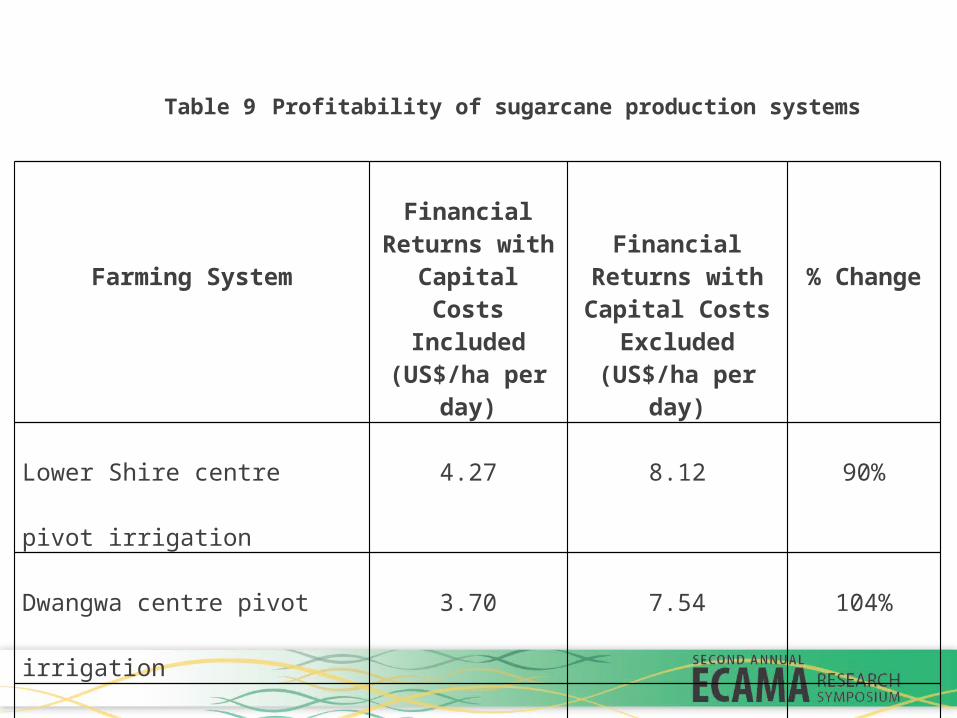

Table 9 Profitability of sugarcane production systems

Farming System

Financial Returns with Capital Costs

Included(US$/ha per day)

Financial Returns with Capital Costs

Excluded(US$/ha per day)

% Change

Lower Shire centre pivot irrigation 4.27 8.12 90%

Dwangwa centre pivot irrigation 3.70 7.54 104%

Dwangwa furrow irrigation 4.92 8.17 66%

Dwangwa rainfed 3.97 3.97 0%

Profitability of sugarcane production systems

• To sustain good yields and good revenue streams the industry needs to:

develop professional standards

have ability to regulate

invest in emerging farmers associations

• These are key roles for SUGAM

• Pertinent to understand how sucrose prices are determined, and how industry profits are usually distributed through the value chain, and how production standards could be regulated

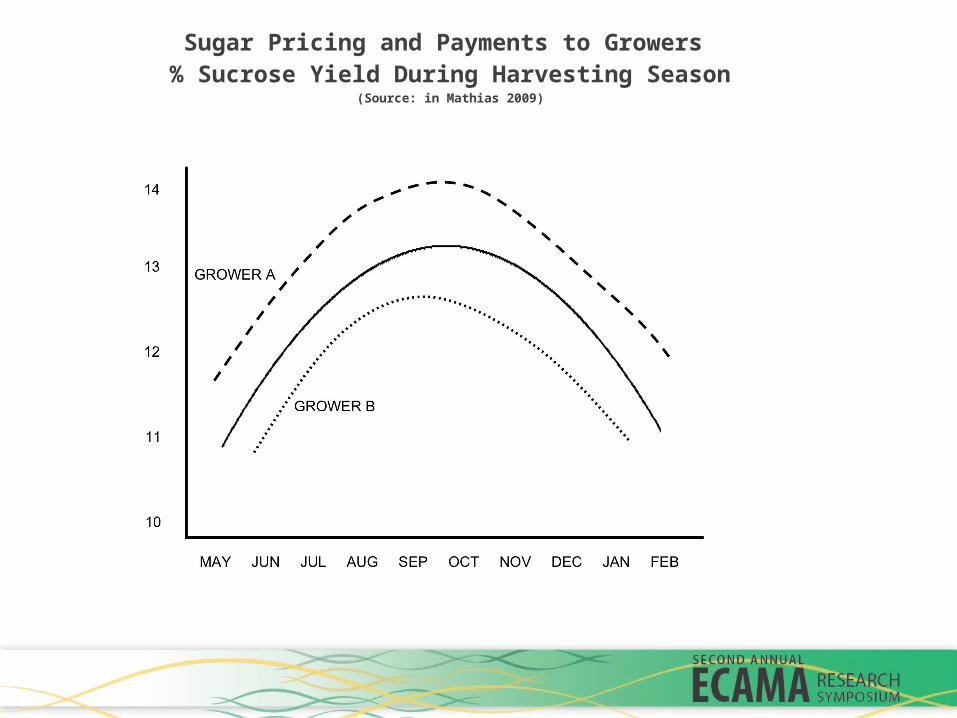

Sugar Pricing and Payments to Growers % Sucrose Yield During Harvesting Season

(Source: in Mathias 2009)

Sugar Pricing and Payments to Growers

• Industry standards should be used to provide for fair and equitable development amongst stakeholders

• Standards usually enshrined in Cane Supply Agreements (CSA) between millers and growers

• Harvest and deliver cane to miller on a strictly rateable schedule • Rateable delivery schedule dictates the cut and haul procedures,

establishes optimum harvest delivery schedule to ensure mill capacity is maximised, that sucrose content of outgrower cane does not drop through unnecessary delays on the road and at mill gate

• Provides growers and millers more efficient harvest and mill operations and better returns on the substantial capital invested mill complexes

Sugar Pricing and Payments to Growers

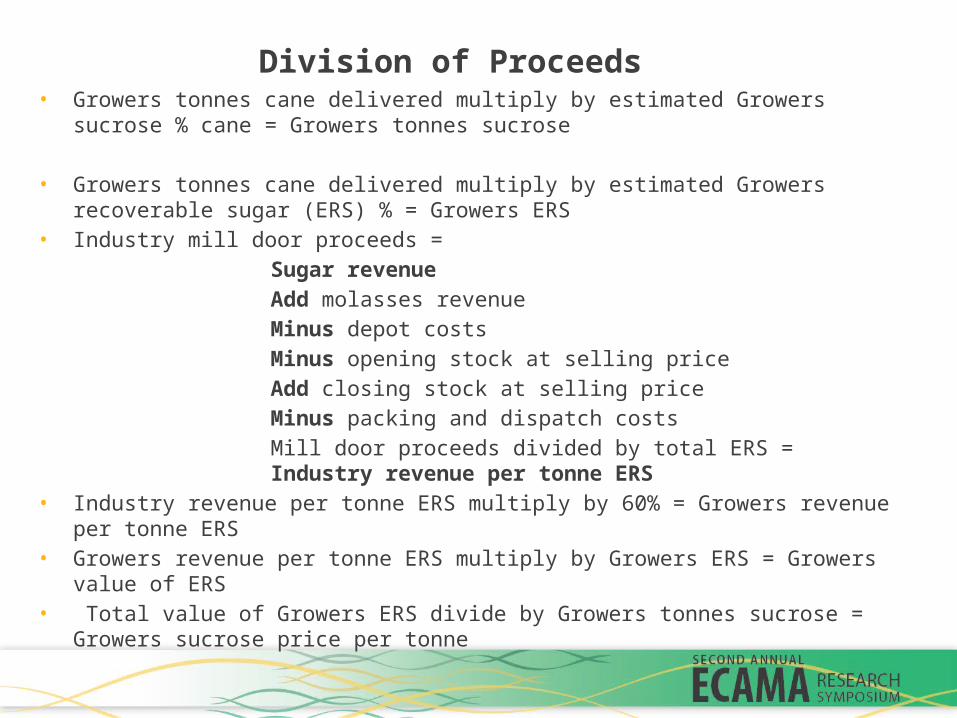

• Cane payment system is largely based around the ‘estimated recoverable sucrose’ (ERS)

• Involves complex process for assessment through laboratory testing incorporating recovery system, percentage brix and fibre, moisture content and purity of juice

• Value of molasses factored into the sucrose payment• Can have other bye-products included but not usual• Division of proceeds (DOP) sugarcane pricing is usually

transparent and fair system• Well-crafted CSAs and DOPs can provide powerful platform for

developing openness, equity and trust

Division of Proceeds• Growers tonnes cane delivered multiply by estimated Growers sucrose % cane = Growers tonnes

sucrose

• Growers tonnes cane delivered multiply by estimated Growers recoverable sugar (ERS) % = Growers ERS

• Industry mill door proceeds =

Sugar revenue

Add molasses revenue

Minus depot costs

Minus opening stock at selling price

Add closing stock at selling price

Minus packing and dispatch costs

Mill door proceeds divided by total ERS = Industry revenue per tonne ERS

• Industry revenue per tonne ERS multiply by 60% = Growers revenue per tonne ERS• Growers revenue per tonne ERS multiply by Growers ERS = Growers value of ERS• Total value of Growers ERS divide by Growers tonnes sucrose = Growers sucrose price per

tonne

An Agenda for SUGAM

• SUGAM should become the voice of outgrowers’ advocating and lobbying government and other stakeholders

• Promote the development of all outgrowers including organisation structures

• Maintain annual register of growers and catalogue production data as presented in this paper

• Campaign for cheaper development and seasonal loans from commercial and development banks

• Support general improvement in outgrower technical and financial management skills, advise on contracts

• Develop one-stop-shop for technical and managerial extension support including the much needed financial and taxation advisory services

An Agenda for SUGAM

• Promote block farming, following best practices • Operationalise soil sampling facilities at Chitedze and

Bvumbwe for outgrowers• Promote formation and operationalise mill cane committees• Broker codes of best practice for cane cutting and haulage

contractors• Assist develop CSA documents and DOP formulation, and

communicate to members, in simple terms, the ramifications and logic behind them

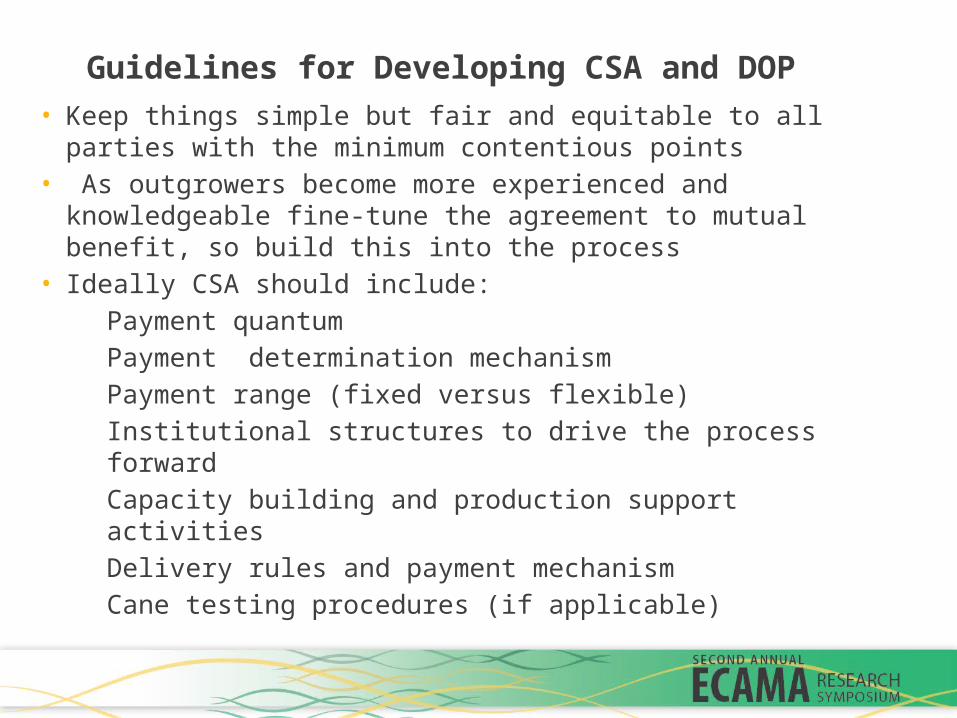

Guidelines for Developing CSA and DOP

• Keep things simple but fair and equitable to all parties with the minimum contentious points

• As outgrowers become more experienced and knowledgeable fine-tune the agreement to mutual benefit, so build this into the process

• Ideally CSA should include:

Payment quantum

Payment determination mechanism

Payment range (fixed versus flexible)

Institutional structures to drive the process forward

Capacity building and production support activities

Delivery rules and payment mechanism

Cane testing procedures (if applicable)

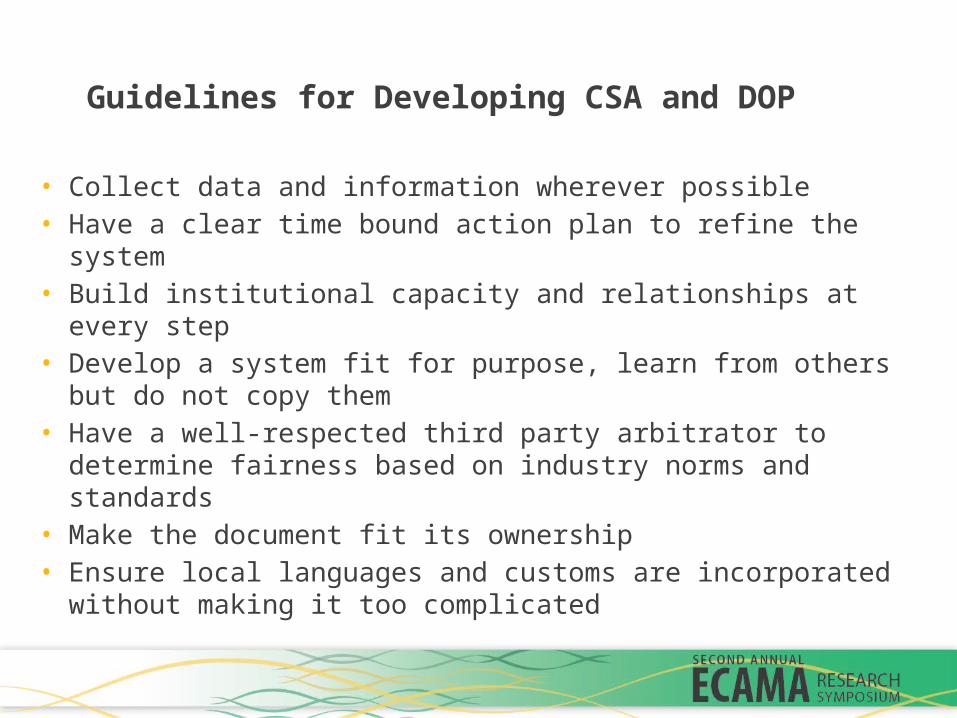

Guidelines for Developing CSA and DOP

• Collect data and information wherever possible• Have a clear time bound action plan to refine the system• Build institutional capacity and relationships at every step• Develop a system fit for purpose, learn from others but do not

copy them• Have a well-respected third party arbitrator to determine

fairness based on industry norms and standards • Make the document fit its ownership • Ensure local languages and customs are incorporated without

making it too complicated

There are many other action points not discussed today, but I hope this presentation has given some weight for industry support to the development of SUGAM as an apex sugarcane outgrower body and voice, which I think is vital to the transparent and sustainable growth of the outgrower sugarcane subsector.

Thank You