Embed Size (px)

Citation preview

Excellence by Design

“We Manufacture Materials That Make

the World

GREENER – STRONGER – SMARTER”

Purpose

World Non-Ferrous Conference – Mumbai

Organized by MTLEXS

08th September 2017Mr. J.C. Laddha

CEO (Copper Business)Hindalco Industries Limited

Turnover: $17 bn

EBITDA: $2 bn

Market Cap: $6.5 bn

Asset Base: $ 13.3 bn

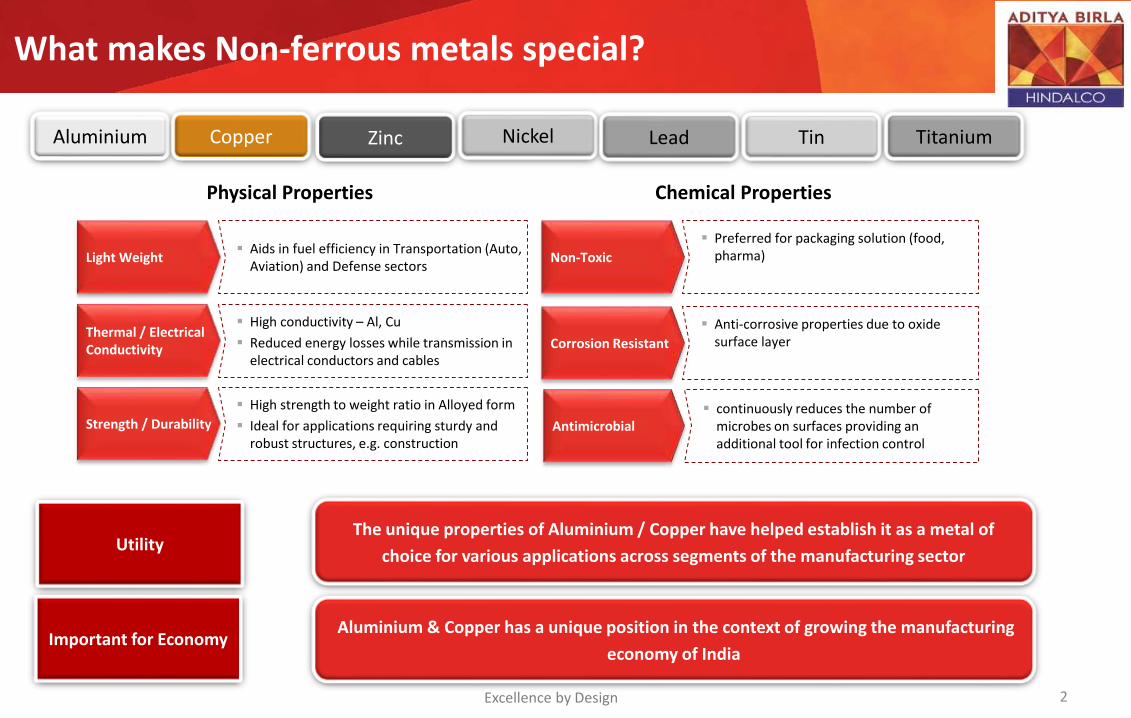

What makes Non-ferrous metals special?

2

Utility

Aluminium & Copper has a unique position in the context of growing the manufacturing

economy of IndiaImportant for Economy

The unique properties of Aluminium / Copper have helped establish it as a metal of

choice for various applications across segments of the manufacturing sector

Light Weight Aids in fuel efficiency in Transportation (Auto,

Aviation) and Defense sectors

Corrosion Resistant

Anti-corrosive properties due to oxide surface layer

Thermal / Electrical Conductivity

High conductivity – Al, Cu

Reduced energy losses while transmission in electrical conductors and cables

Strength / Durability

High strength to weight ratio in Alloyed form

Ideal for applications requiring sturdy and robust structures, e.g. construction

Antimicrobial continuously reduces the number of

microbes on surfaces providing an additional tool for infection control

Non-Toxic

Preferred for packaging solution (food, pharma)

Physical Properties Chemical Properties

Excellence by Design

Aluminium Copper Zinc Nickel Lead Tin Titanium

0

5

10

Ch

ina

Ch

ile

Jap

an

USA

Ru

ssia

DR

Co

ngo

Ind

ia

Sou

th K

ore

a

Ger

man

y

Po

lan

d

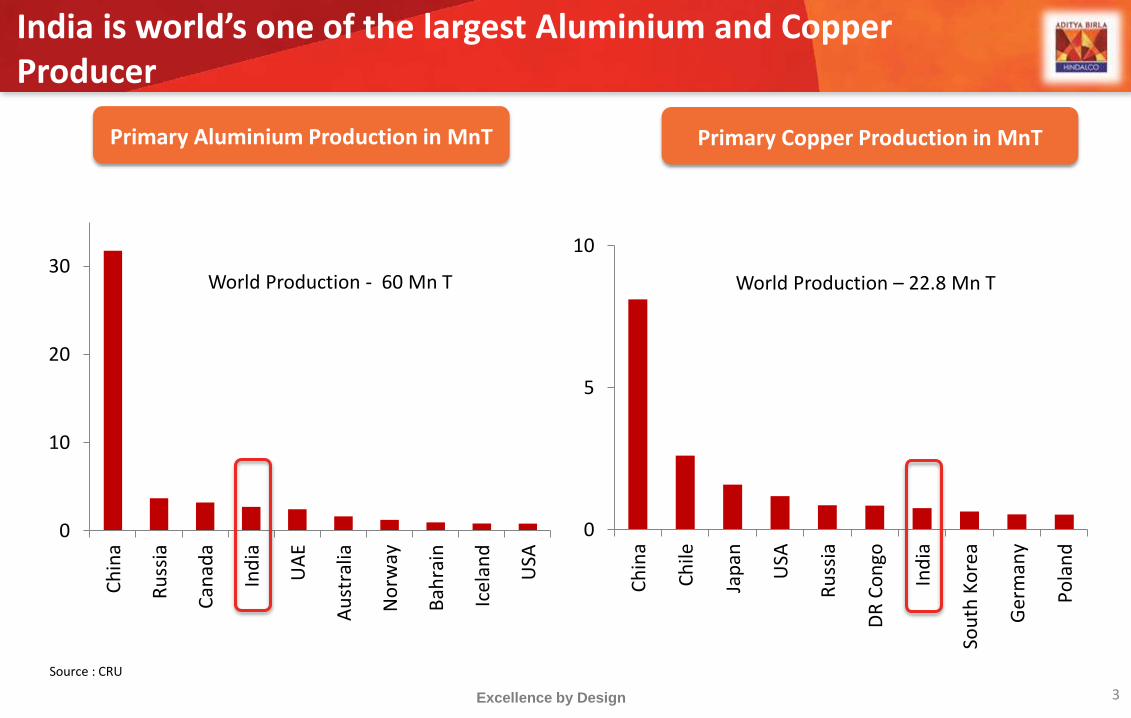

India is world’s one of the largest Aluminium and Copper Producer

3Excellence by Design

Primary Aluminium Production in MnT

0

10

20

30

Ch

ina

Ru

ssia

Can

ada

Ind

ia

UA

E

Au

stra

lia

No

rway

Bah

rain

Icel

and

USA

Primary Copper Production in MnT

World Production - 60 Mn T World Production – 22.8 Mn T

Source : CRU

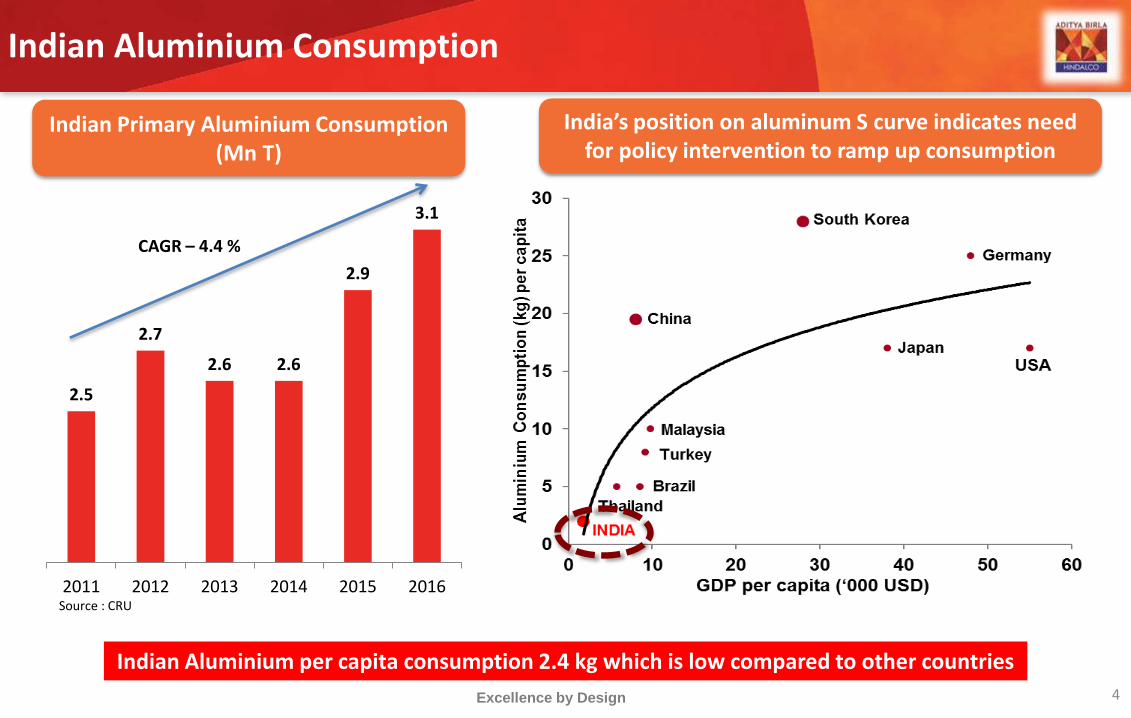

Indian Aluminium Consumption

4

India’s position on aluminum S curve indicates need for policy intervention to ramp up consumption

Excellence by Design

Source : CRU

Indian Primary Aluminium Consumption (Mn T)

2.5

2.7

2.6 2.6

2.9

3.1

2011 2012 2013 2014 2015 2016

CAGR – 4.4 %

Indian Aluminium per capita consumption 2.4 kg which is low compared to other countries

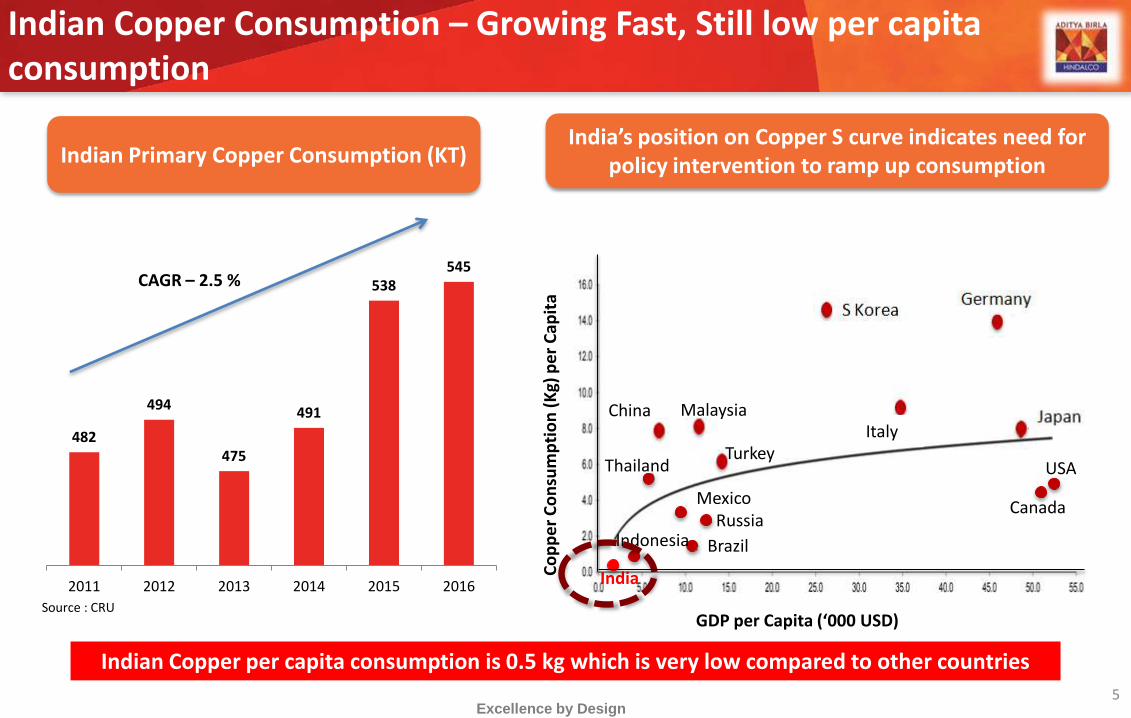

Indian Copper Consumption – Growing Fast, Still low per capita consumption

5

Indian Primary Copper Consumption (KT) India’s position on Copper S curve indicates need for

policy intervention to ramp up consumption

Co

pp

er

Co

nsu

mp

tio

n (

Kg)

pe

r C

apit

a

Italy

Canada

USA

Russia

Brazil

Mexico

Indonesia

India

Thailand

China Malaysia

Turkey

GDP per Capita (‘000 USD)

482

494

475

491

538545

2011 2012 2013 2014 2015 2016

Excellence by Design

Source : CRU

CAGR – 2.5 %

Indian Copper per capita consumption is 0.5 kg which is very low compared to other countries

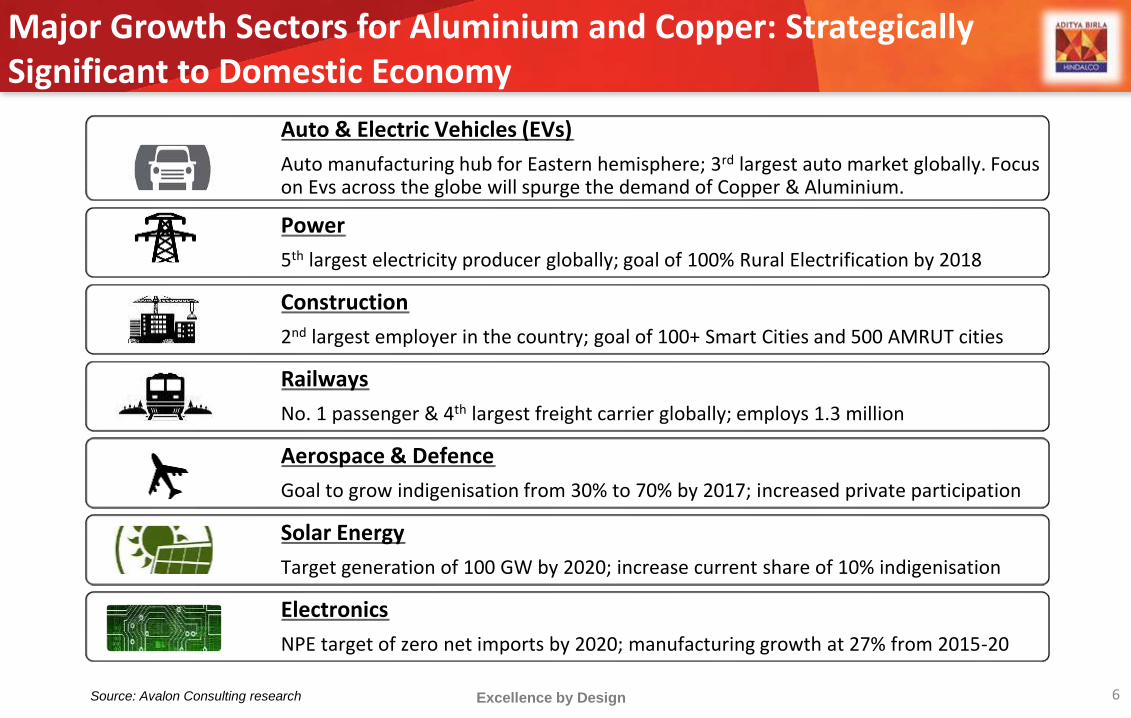

Major Growth Sectors for Aluminium and Copper: Strategically Significant to Domestic Economy

6Source: Avalon Consulting research

Auto & Electric Vehicles (EVs)

Auto manufacturing hub for Eastern hemisphere; 3rd largest auto market globally. Focus on Evs across the globe will spurge the demand of Copper & Aluminium.

Power

5th largest electricity producer globally; goal of 100% Rural Electrification by 2018

Construction

2nd largest employer in the country; goal of 100+ Smart Cities and 500 AMRUT cities

Railways

No. 1 passenger & 4th largest freight carrier globally; employs 1.3 million

Aerospace & Defence

Goal to grow indigenisation from 30% to 70% by 2017; increased private participation

Solar Energy

Target generation of 100 GW by 2020; increase current share of 10% indigenisation

Electronics

NPE target of zero net imports by 2020; manufacturing growth at 27% from 2015-20

Excellence by Design

Excellence by Design7

Development of Aluminium Industry in

China- A Unique Case Study

Primary Aluminium Production in China

8Excellence by Design

1012

14

1719

2223

26

29

34

38

9 9

1314 14

1720

22

25

2831

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Capacity Production

Growth in Smelting Capacity in China (MnT)

Share in Global Production

54%52%49%46%43%36%34%33%28%26% 41%

CAGR: 14.3% CAGR: 13.2%

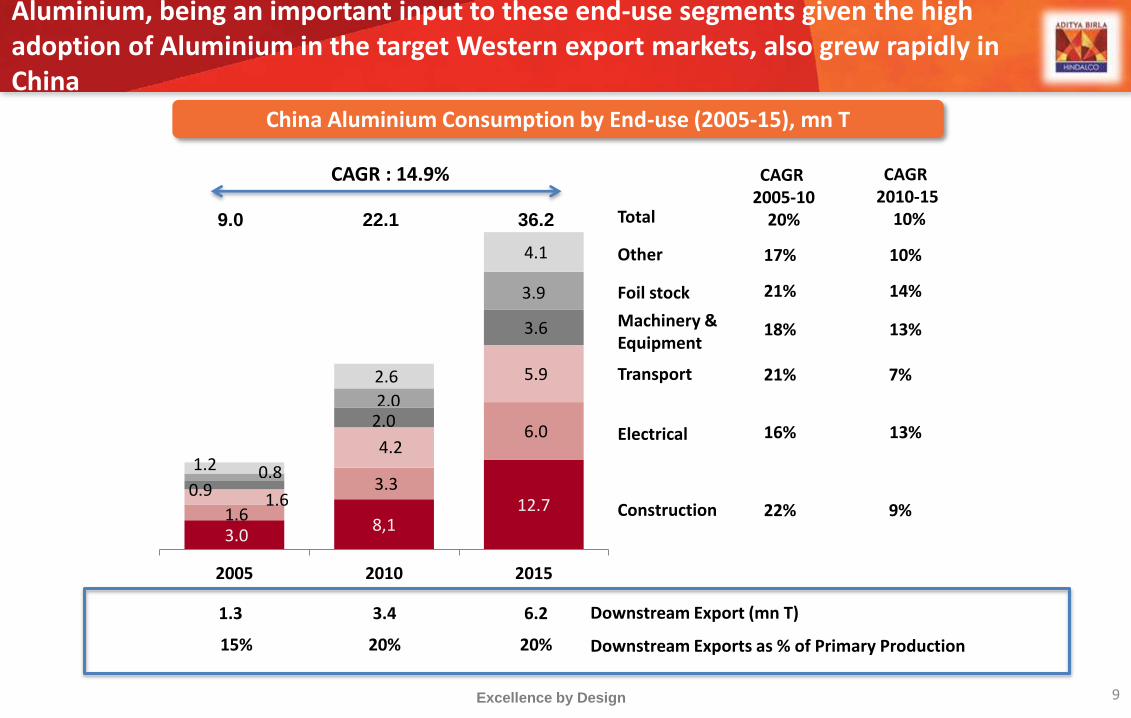

Aluminium, being an important input to these end-use segments given the high adoption of Aluminium in the target Western export markets, also grew rapidly in China

9Excellence by Design

China Aluminium Consumption by End-use (2005-15), mn T

3.0 8,1

12.71.6

3.3

6.0

1.6

4.2

5.9

0.9

2.0

3.6

0.8

2.0

3.9

1.2

2.6

4.1

2005 2010 2015

Construction

Electrical

Transport

Foil stock

Other

CAGR2005-10

20%

CAGR 2010-15

10%9.0 22.1 36.2

Machinery & Equipment

Total

17%

21%

18%

21%

16%

22%

10%

14%

13%

7%

13%

9%

15% 20% 20% Downstream Exports as % of Primary Production

Downstream Export (mn T)1.3 3.4 6.2

CAGR : 14.9%

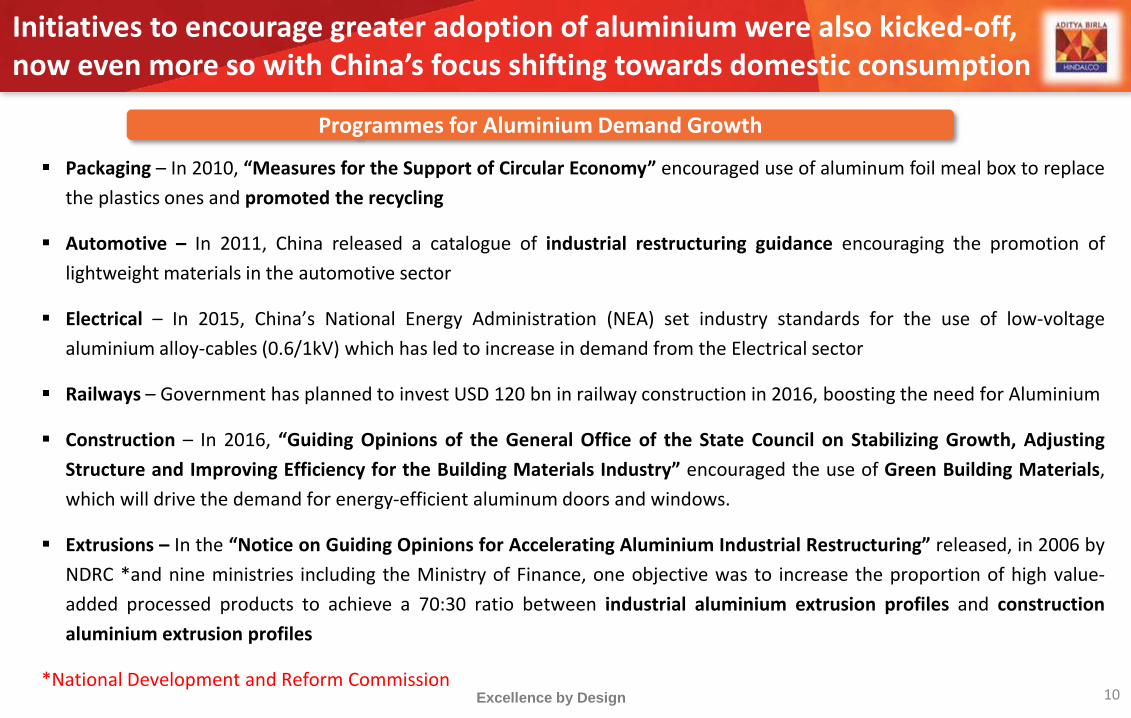

Initiatives to encourage greater adoption of aluminium were also kicked-off, now even more so with China’s focus shifting towards domestic consumption

10Excellence by Design

Packaging – In 2010, “Measures for the Support of Circular Economy” encouraged use of aluminum foil meal box to replace

the plastics ones and promoted the recycling

Automotive – In 2011, China released a catalogue of industrial restructuring guidance encouraging the promotion of

lightweight materials in the automotive sector

Electrical – In 2015, China’s National Energy Administration (NEA) set industry standards for the use of low-voltage

aluminium alloy-cables (0.6/1kV) which has led to increase in demand from the Electrical sector

Railways – Government has planned to invest USD 120 bn in railway construction in 2016, boosting the need for Aluminium

Construction – In 2016, “Guiding Opinions of the General Office of the State Council on Stabilizing Growth, Adjusting

Structure and Improving Efficiency for the Building Materials Industry” encouraged the use of Green Building Materials,

which will drive the demand for energy-efficient aluminum doors and windows.

Extrusions – In the “Notice on Guiding Opinions for Accelerating Aluminium Industrial Restructuring” released, in 2006 by

NDRC *and nine ministries including the Ministry of Finance, one objective was to increase the proportion of high value-

added processed products to achieve a 70:30 ratio between industrial aluminium extrusion profiles and construction

aluminium extrusion profiles

*National Development and Reform Commission

Programmes for Aluminium Demand Growth

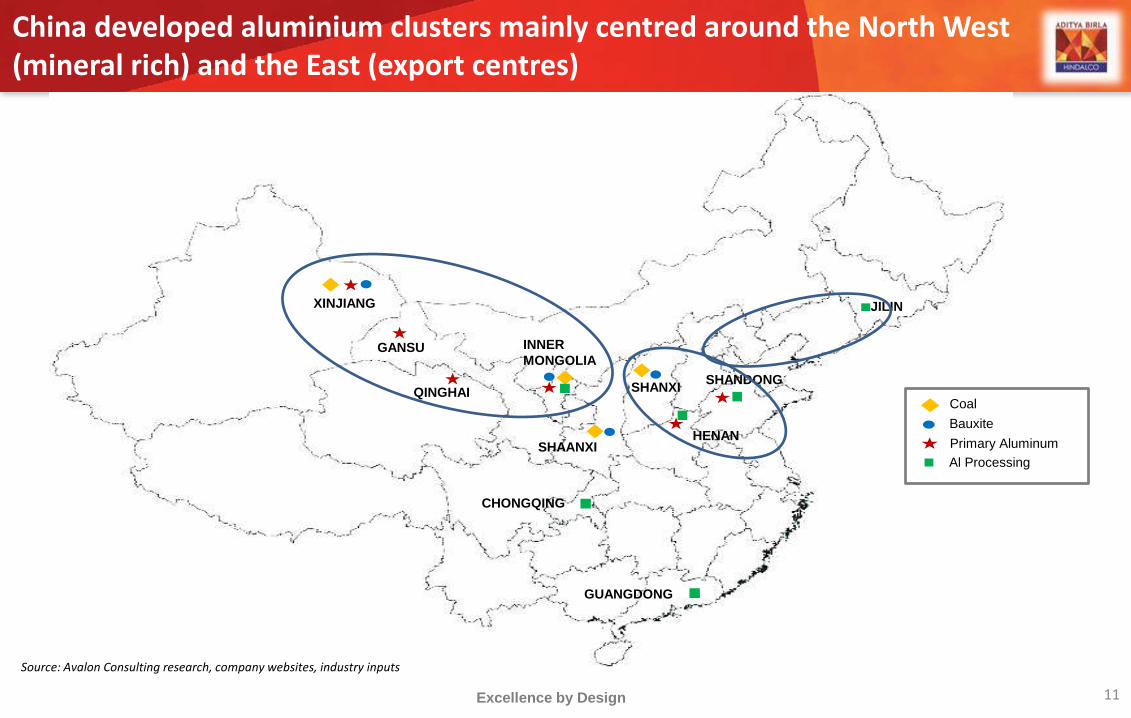

China developed aluminium clusters mainly centred around the North West (mineral rich) and the East (export centres)

11Excellence by Design

XINJIANG

INNER

MONGOLIA

SHANXI

SHAANXI

SHANDONG

HENAN

GANSU

QINGHAI

CHONGQING

GUANGDONG

JILIN

Coal

Primary Aluminum

Bauxite

Al Processing

Source: Avalon Consulting research, company websites, industry inputs

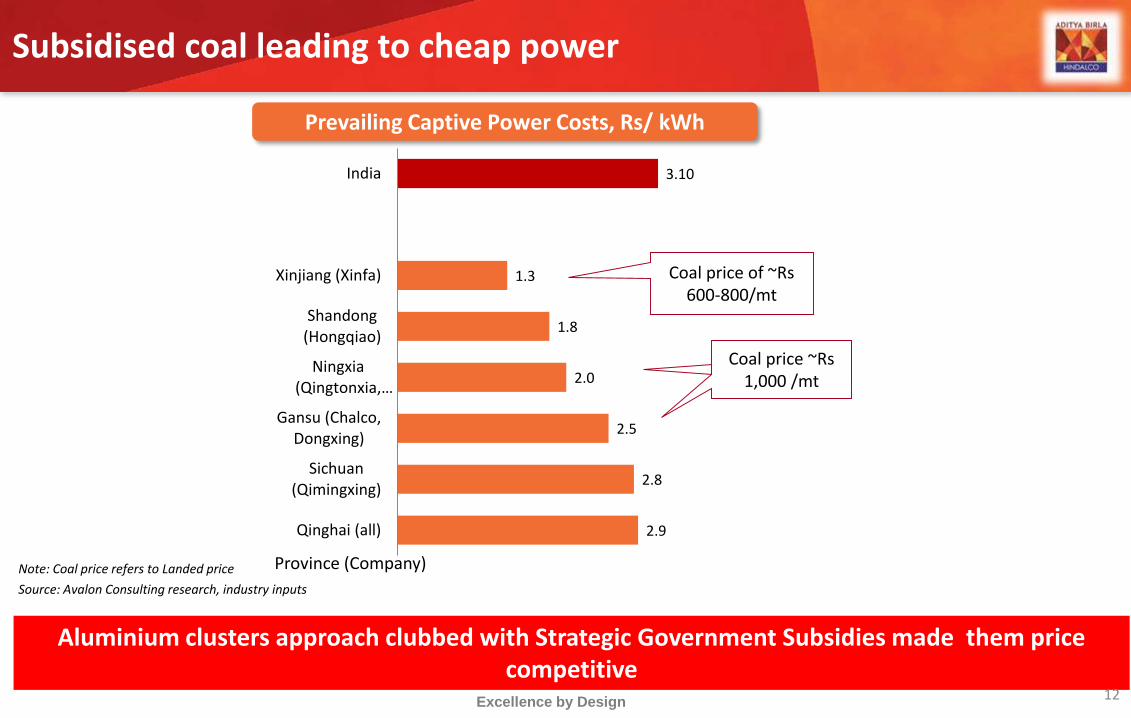

Aluminium clusters approach clubbed with Strategic Government Subsidies made them price competitive

Subsidised coal leading to cheap power

12Excellence by Design

2.9

2.8

2.5

2.0

1.8

1.3

3.10

Qinghai (all)

Sichuan(Qimingxing)

Gansu (Chalco,Dongxing)

Ningxia(Qingtonxia,…

Shandong(Hongqiao)

Xinjiang (Xinfa)

India

Prevailing Captive Power Costs, Rs/ kWh

Province (Company)

Source: Avalon Consulting research, industry inputs

Coal price of ~Rs 600-800/mt

Coal price ~RMB 100/mtCoal price ~Rs

1,000 /mt

Note: Coal price refers to Landed price

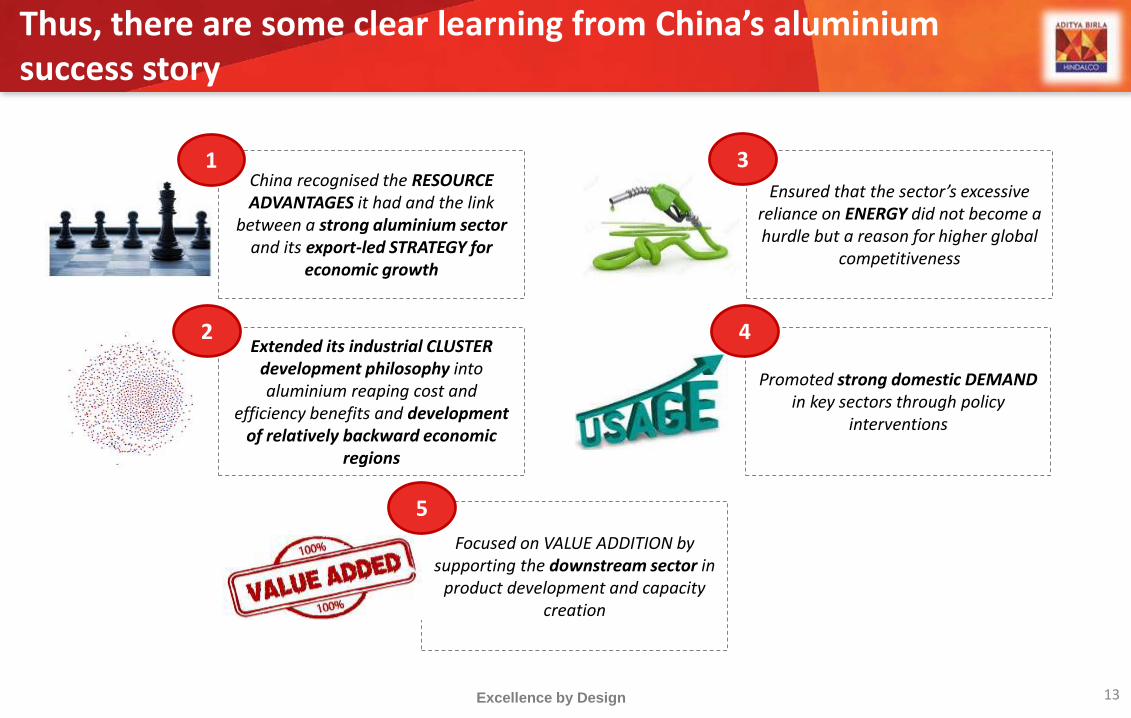

Thus, there are some clear learning from China’s aluminium success story

13Excellence by Design

Ensured that the sector’s excessive reliance on ENERGY did not become a hurdle but a reason for higher global

competitiveness

China recognised the RESOURCE ADVANTAGES it had and the link

between a strong aluminium sector and its export-led STRATEGY for

economic growth

Extended its industrial CLUSTER development philosophy into aluminium reaping cost and

efficiency benefits and development of relatively backward economic

regions

Promoted strong domestic DEMAND in key sectors through policy

interventions

Focused on VALUE ADDITION by supporting the downstream sector in

product development and capacity creation

1

2

3

4

5

Excellence by Design 14

How can we grow the

Indian Aluminium / Copper Industry

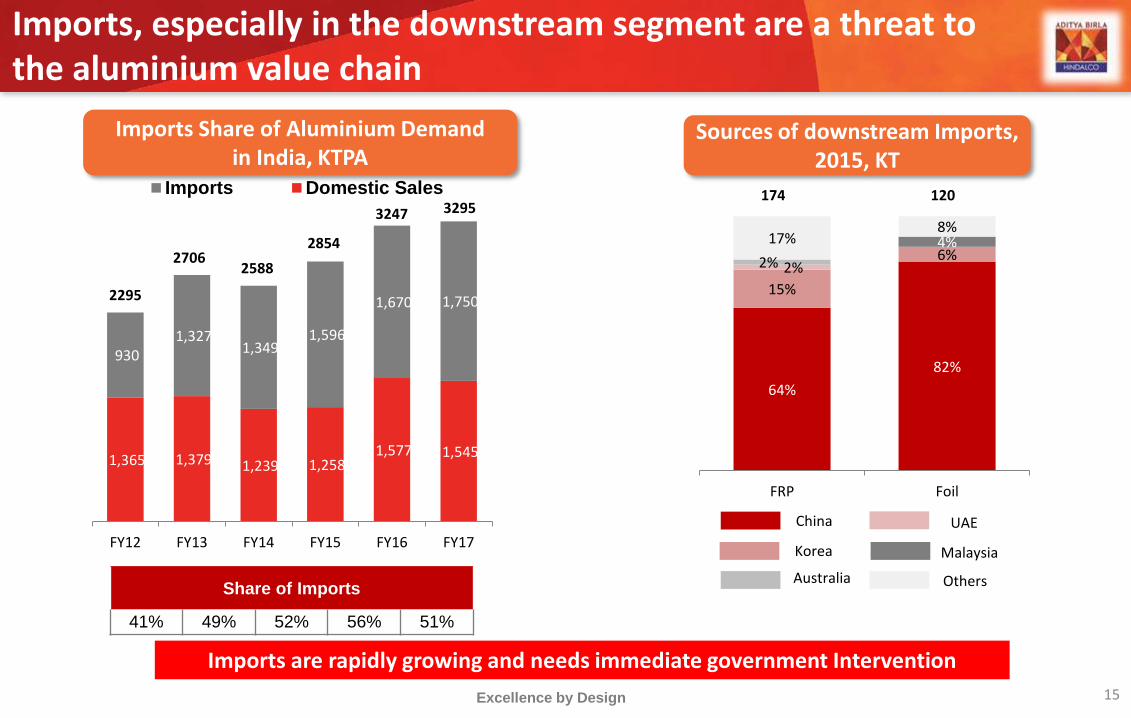

Imports, especially in the downstream segment are a threat to the aluminium value chain

15Excellence by Design

Imports Share of Aluminium Demand in India, KTPA

1,365 1,379 1,239 1,258 1,577 1,545

930 1,327

1,349 1,596

1,670 1,750

FY12 FY13 FY14 FY15 FY16 FY17

Imports Domestic Sales

Share of Imports

41% 49% 52% 56% 51%

Sources of downstream Imports, 2015, KT

64%

82%

15%

6%2%

4%

2%

17%8%

FRP Foil

120174

UAE

Korea

Australia

Malaysia

China

Others

Imports are rapidly growing and needs immediate government Intervention

2295

27062588

2854

3247 3295

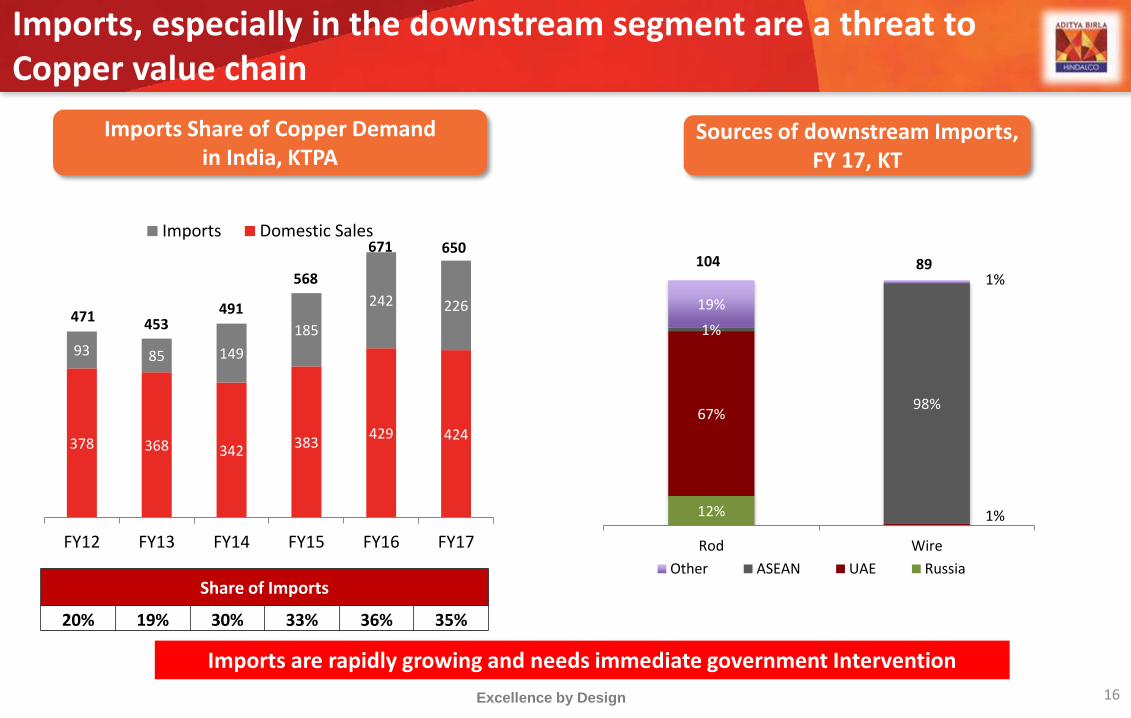

16Excellence by Design

378 368 342383

429 424

93 85 149

185

242 226

FY12 FY13 FY14 FY15 FY16 FY17

Imports Domestic Sales

Share of Imports

20% 19% 30% 33% 36% 35%

Imports Share of Copper Demand in India, KTPA

Sources of downstream Imports, FY 17, KT

Imports, especially in the downstream segment are a threat to Copper value chain

Imports are rapidly growing and needs immediate government Intervention

471 453491

568

671 650

12%

67%

1%

1%

98%

19%

1%

Rod Wire

Other ASEAN UAE Russia

104 89

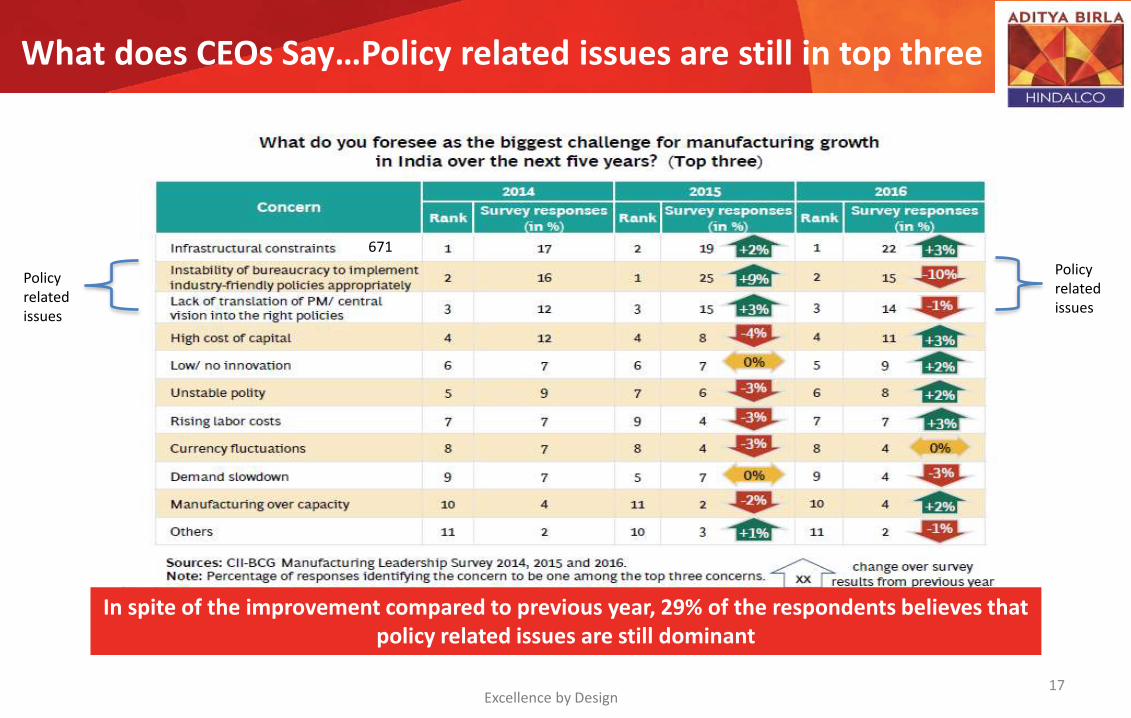

What does CEOs Say…Policy related issues are still in top three

17

In spite of the improvement compared to previous year, 29% of the respondents believes that policy related issues are still dominant

Policy related issues

Policy related issues

Excellence by Design

671

Create a structure within the government that facilitates policy and decision making related to Aluminium/Copper

18Excellence by Design

Special Interest Group to be

created within the government

to deal with issues related to the aluminium / copper industry

Track global developments in the aluminum/copper sector and craft

policy in collaboration with industry

Review indirect taxes and duties with regard to aluminium / copper

production and imports so as to promote industry development

Devise and implement regulations and mechanisms to ensure

economical and environmentally viable handling of scrap

Liaise with key stakeholders in major end-use industries to ensure

adoption of aluminium/copper through awareness and policy setting

Coordinate with programme managers of campaigns like Make in India,

National Solar Mission, etc. to promote aluminium/copper

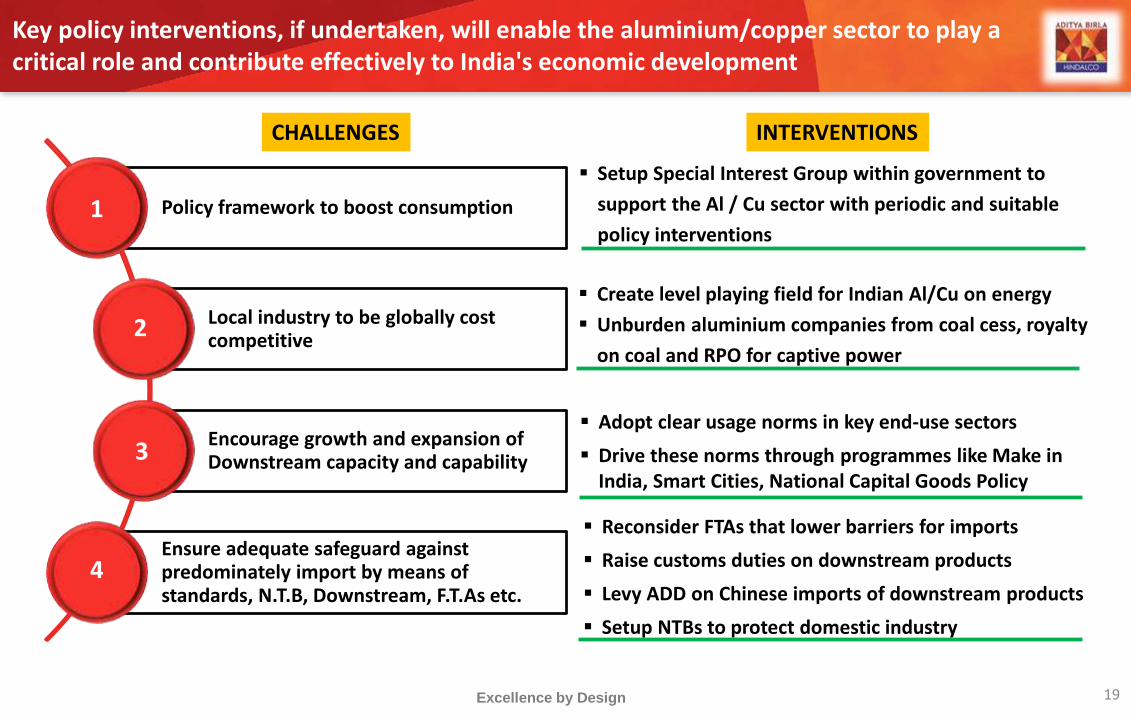

Key policy interventions, if undertaken, will enable the aluminium/copper sector to play a critical role and contribute effectively to India's economic development

19Excellence by Design

Policy framework to boost consumption

Local industry to be globally cost competitive

Encourage growth and expansion of Downstream capacity and capability

Ensure adequate safeguard against predominately import by means of standards, N.T.B, Downstream, F.T.As etc.

1

2

3

4

Setup Special Interest Group within government to

support the Al / Cu sector with periodic and suitable

policy interventions

Create level playing field for Indian Al/Cu on energy

Unburden aluminium companies from coal cess, royalty

on coal and RPO for captive power

CHALLENGES INTERVENTIONS

Adopt clear usage norms in key end-use sectors

Drive these norms through programmes like Make in India, Smart Cities, National Capital Goods Policy

Reconsider FTAs that lower barriers for imports

Raise customs duties on downstream products

Levy ADD on Chinese imports of downstream products

Setup NTBs to protect domestic industry

Excellence by Design20

Thank You