Embed Size (px)

DESCRIPTION

BOURBON factsheet, april 2014

Citation preview

BOURBON in 2013: A leader in offshore oil and gas marine servicesIn a very dynamic oil and gas market, BOURBON offers a wide range of exploration support, development, and production services, both in deepwater offshore and continental offshore. In addition to the expertise and professionalism of its crews, BOURBON’s strategic choices in recent years have led the group to a leadership position, operating a fleet of 485* recent, innovative, and efficient vessels.* including the cement carrier Endeavor

Marine Services Activity

466 vessels (+27 vessels compared to 2012), 81% of turnover

The oil and gas offshore support fleet provides :

3 transport of equipment and special products (PSV – Platform Supply Vessels);

3 tug services, anchor handling and positioning of drilling platforms and machinery (AHTS – Anchor Handling Tug Supply vessels);

3 assistance to resupply vessels / FPSO (Terminal Tugs);

3 transport of personnel to sites and between platforms in a single field (Surfers), emergency supplies and response teams (FSIV – Fast Supply Intervention Vessels).

The coastline protection fleet is composed of assistance and salvage tugs (preventing wrecks, assisting and salvaging vessels in distress, fighting pollution risks).

Subsea Services Activity

18 vessels, 12 underwater robots (ROVs), 17% of revenues

BOURBON offers a wide range of services, from engineering, supervision, and management of undersea operations at oil and gas fields and wind farms, for developing installations, to Inspection, Maintenance, and Repair (IMR).

2014 PROSPECTSThe demand for offshore vessels is supported by the high level of spending in the offshore oil & gas sector.In deepwater offshore, average spend-ing over the next three years is ex-pected to grow by approximately 10% per year. In the shallow water market, vessel demand growth is driven by the steady spending in the oil & gas sector, notably by activities aimed at main-taining production of existing fields. The Subsea services market is buoyed by the growing number of subsea well-heads and the development of new deepwater oil fields.The majority of deliveries for vessels currently on order are expected in 2014. From now on, new orders for vessels will be executed as opportunities arise and will not impact revenues before 2016.In 2014, BOURBON is targeting revenue growth of 8-10% and a slight improve-ment of the EBITDAR/Revenues ratio.

3 GROSS OPERATING INCOME (EBITDA)**

575,7 M€*+ 41,7 %*

3 OPERATING INCOME (EBIT)**

302,6 M€*+ 87,3 %*

+73,1 MILLION EUROS

3 NET EARNINGS, GROUP SHARE

115,0 M€

3 REVENUES

+ 10,5%*1311,9 MILLION EUROS

2013 RESULTS

InvESTOR FACT SHEET1

InvESTOR Fact SheetMARCH 2014

* Variation 2013 / 2012** Includes the capital gains made on the sale of vessels

3 OPERATIONAL PERFORMANCEp TRIR (Total recordable incidents

per one million hours worked, based on 24 hours/day): 0.48

p Technical availability rate for the fleet: 94.5%

p Vessel fuel consumption reduced by up to 30%

p Underwater operations at depths of up to 3,000 m

p Coastline protection: over 1,600 operations conducted since 1976

p 11,150 employees

p 84 different nationalities

p 84% seafarers and crew

p 16% onshore staff

3 WOMEN AND MEN

3 THE FLEETp 485 offshore** vessels, with

an average age of 6 years

p 52 vessels ordered

3 INTERNATIONAL ACTIVITYp Operating in 50 countries

p 28 operational subsidiaries

p Revenue breakdown by geographic area:

- Africa 57,2%- Europe & Mediterranean /

Middle East 17,4%- North and South America

14,3%- Asia 11,1%

* figures as of 12/31/2014** Including the cement career Endeavor

BOURBOn In nUMBERS *

InvESTOR FACT SHEET 2

Capitalizing on BOURBON’s dNa to prepare for beyond 2015Now more than ever, BOURBON is continuing its determined growth strategy, in order to ensure its position as leader in offshore oil and gas marine services.

For over 10 years, BOURBON has put customer satisfaction at the heart of its strategy and is committed to operational excellence at every stage, based on four pillars: safety of personnel and facilities, competency, technical availabili-ty of vessels, and optimizing costs.

The Group is now looking beyond 2015 by transforming itself in order to implement a new phase of growth and value creation through the “Transforming for beyond” plan and its four components:

3 MyBourbon, a customer relations platform

3 Under the flag of excellence, the employer brand of BOURBON employees,

3 BOURBON Way, which involves developing tools for achieving operational excellence and cost control

3 Asset Smart, the financial part of this action plan.

ASSET SMART: ACTIvE FLEET MAnAGEMEnT

In 2013, BOURBON announced its transforma-tion plan, based on the sale of 30% of its fleet of supply vessels by 2015, for a total of $2.5 bil-lion US, with the vessels operated for 10 years under a bareboat charter contract.

The implementation of this program is now well underway; the Group has signed an initial $1.5 billion US contract with ICBC Financial Leas-ing ($860 million US of which was received as of March 5, 2014), followed by a second con-tract with SCB (Standard Chartered Bank), for $150 million US ($65 million US of which was received as of March 5, 2014). These contracts involve the sale of 57 vessels.

Along with these transfers, the Group con-tinues to manage its fleet of vessels that are partially compliant or non-compliant with its technical standards (7 vessels sold, for a total of $183 million US).

These actions, resulting in a significant reduction in net debt, confirm BOURBON’s strategy and contribute to establishing of a new phase of growth, beyond the BOURBON 2015 Leadership Strategy plan.

SHaRE InFORMATIOn

DIvIDEnDS

€1/share: this is the dividend amount for 2013 earnings that will be proposed at the Shareholders’ Meeting on May 20, 2014. If approved, it will begin to be distributed starting June 3, 2014. To receive this dividend, you must be in possession of your shares by the market closure on May 28, 2014, the day before the ex-coupon date.

2013 FInAnCIAL CALEnDAR

April 30, 2014 1st quarter 2014 revenue release

May 20, 2014 Annual Shareholder’s Meeting

August 27, 2014 Release and presentation of 1st quarter 2014 revenues

3 CONTACT

Investor relations, analysts, shareholders:

All information on the Group, including an area dedicated to shareholders, is available to you at www.bourbon-online.com/en/finance

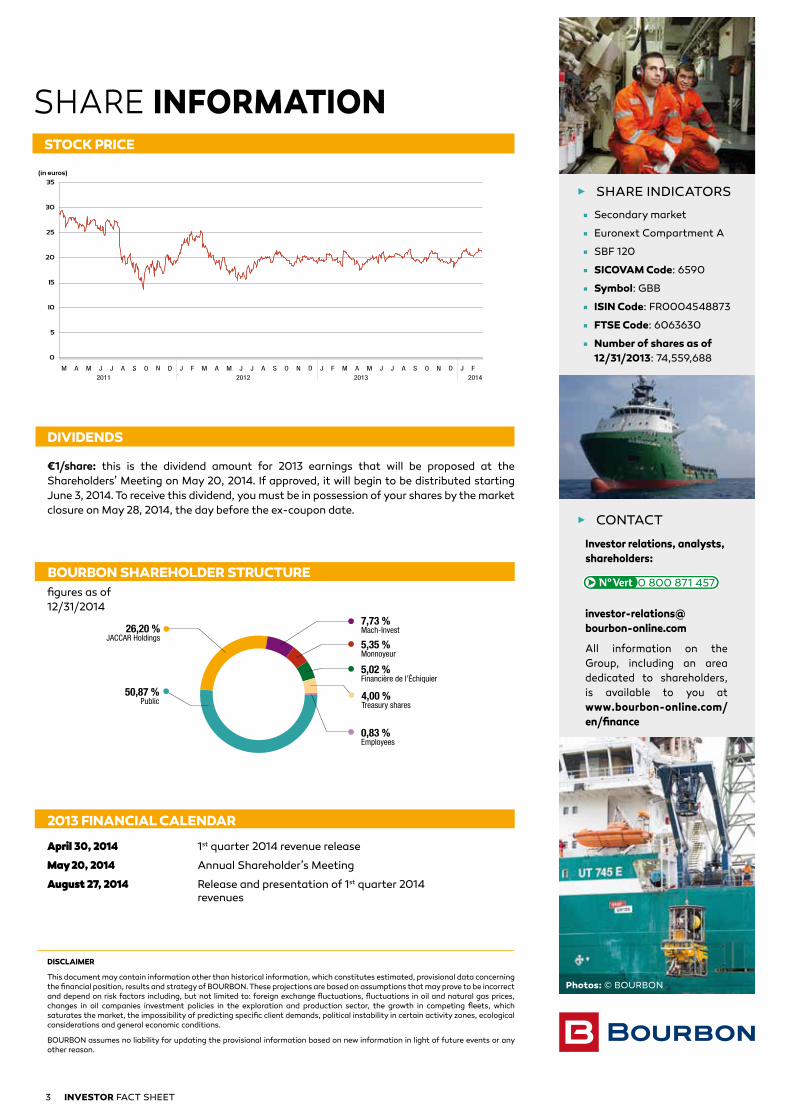

2011 2012 2013 2014

N D JJM A M J A S O A DF AM M J J S O N J A DF AM M J J S O N J F

0

5

10

15

20

25

30

35

(in euros)

STOCK PRICE

3 SHARE INDICATORS

p Secondary market

p Euronext Compartment A

p SBF 120

p SICOvAM Code: 6590

p Symbol: GBB

p ISIn Code: FR0004548873

p FTSE Code: 6063630

p number of shares as of 12/31/2013: 74,559,688

InvESTOR FACT SHEET3

0 800 871 457figures as of 12/31/2014

BOURBOn SHAREHOLDER STRUCTURE

26,20 %JACCAR Holdings

50,87 %Public

0,83 %Employees

4,00 %Treasury shares

5,02 %Financière de l’Échiquier

5,35 %Monnoyeur

7,73 %Mach-Invest

DISCLAIMER

This document may contain information other than historical information, which constitutes estimated, provisional data concerning the financial position, results and strategy of BOURBON. These projections are based on assumptions that may prove to be incorrect and depend on risk factors including, but not limited to: foreign exchange fluctuations, fluctuations in oil and natural gas prices, changes in oil companies investment policies in the exploration and production sector, the growth in competing fleets, which saturates the market, the impossibility of predicting specific client demands, political instability in certain activity zones, ecological considerations and general economic conditions.

BOURBON assumes no liability for updating the provisional information based on new information in light of future events or any other reason.

Photos: © BOURBON