Embed Size (px)

Citation preview

Health Insurance Business –

India perspective

Healthcare Trends

Products

Penetration

Claims Analysis

Distribution Channels

Profitability

Sharad Mathur

Senior Vice President & Head – Agency, Digital & Alternate Channel

SBI General Insurance Company Limited

(A JV between State Bank of India & Insurance Australia Group)

11th Asia Conference on Healthcare & Health Insurance, Singapore

Healthcare expenditure expected to grow backed by macro drivers &

growing awareness

• India’s healthcare spending as a %

of GDP is lower than some of the

key economies

• Currently India’s healthcare is

predominantly through out of pocket

expenses

• The healthcare spends in India is

expected to grow at ~14% over the

next 5 year as per EIU projections

Trends in healthcare spending

• Large growing population with

changing lifestyle

• Advent of lifestyle related

diseases

• Increase in healthcare delivery

prices and introduction of

complex medical interventions

Macro drivers for healthcare

spends

• Increasingly insurance is being

adopted by the Indian retail segment

• There has been growing penetration of

rural mass market and BPL population

through Government sponsored

schemes

Coverage and awareness

3.10%4.0% 4.60% 4.00%

5.60%6.2%

8.90% 9.70%

0.0%

4.0%

8.0%

12.0%

Total expenditure on health as % of GDP India’s comparison with key countries

Source: World Bank database, WHO database

Growing contribution of health insurance to GI market is supported by

increasing volumes & prices of health insurance

Expected Growth in total premium of Health

Insurance in billion USD

Source: IRDAI, Industry Discussions

Contribution of Health in overall GI industry

Premium

Volume

Pricing

Health insurance

penetration backed by

shift in disease pattern,

higher awareness

Growth in “Addressable

population”

1

Healthcare inflation will

lead to cost of insurance

Detariffication impact –

elimination of cross

subsidies and continued

upward revision of health

premiums

Low priced policies will

attract large volumes of

low income consumers

2

5

6

7

Government push for

greater coverage

3

Access to multiple

channels including digital

4 18% 21% 24% 25% 28% 25% 25% 22% 25%

82% 79% 76% 75% 72% 75% 75% 78% 75%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Health Other GI

2.50 2.83

3.33

4.00

4.67

5.50

6.33

7.50

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

Expected CAGR = 17%

Cu

sto

me

r M

ix

• Retail : ~37%, Group: ~51%, Govt: ~12%

• Mass market focus Focusing on increasing retail business

• Retail : ~35%, Group: ~48%, Govt: ~17%

• Focus on younger customers with better income profile

Focus on Retail and government business

• Retail : ~73%, Group: ~22%, Govt: ~ 5% • Strong technical capabilities while starting

operations Huge focus on retail and profitable group business

Pro

du

ct • Low priced products especially in the

group segment Significant focus on right pricing (Group + retail)

• Profitable products • Offers a basket of products with high

risk products being priced better Profitability focus through innovative products

• Innovative products with focus on wellness and wider coverage

Develop integrated care model as scale of medical partner improves

Ch

ann

el • Large branch presence

• Well developed agent base

• High focus on the bancassurance channel

• Aggressively developing alternate channels (online/telemarketing)

Focus on Bancassurance channel as a key channel

• Limited branch presence • Focus on agency channel • Shifting focus towards alternate channels

(online, telemarketing) Focus on Agency and direct channel

Op

era

tio

ns

• Claims management outsourced to TPAs

• Plan to enhance control over claims management by setting up a new TPA, promoted by the four PSUs

Insourcing health claims management

• In-house claims management (e.g. ICICI Lombard, Bajaj Allianz), stake in a TPA (e.g. Reliance)

Captive claims administration for superior service

• In-house / captive claims management

In the current market, three broad segments of insurers exist which have

varying strategies

PSU insurers Multi Line private players Pure Play health insurers

Source: IRDAI, Industry discussions

Health Products Composition - Existing

17% 12%

5% 14%

48%

51%

22%

47%

12% 9%

48%

13%

23% 28% 25% 26%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pvt Insurers Public Insurers Stand Alone Health

Grand Total

Individual Ins excluding Family/Floater Product

Family/Floater Ins excluding Individual Product

Group Ins excluding Govt. sponsored Schemes

Govt sponsored Health Schemes

Health Products linked to Customer Buying Behavior/ Segments

Retail Corporate

and SME

Central and

State Governments

Customer

Segments

• Indemnity products - Individual or

family floater

• Benefits : predominantly

hospitalization expenses

• Fixed benefit products - hospital

daily allowance or critical illness

• Exclusions: OPD, GPs,

pharmacies, etc.

• Typical loss ratios of 60% - 68%

• Single policy covering all

members

• Higher restrictions compared to

retail individual policies

• Sold across corporates; however

limited purchase by small

enterprises

• Typical loss ratios of 75% - 135%

• Low sum insured products

• Simple hospitalization cashless

covers with per member price

between US$ 5 – US$ 15

• Typical family floater sum

assured limited to US$ 1550 –

US$ 4500

• Typical loss ratios of 80% - 120%

Product Features

• Needs to be actively sold the

product

• High loyalty to agent /

intermediary

• Recent grievances data shows

increasing ‘mis-trust’ of health

insurers

• Highly price –sensitive market

• High bargaining power of client

• Uses either broker or direct route

• Increasing migration to self-

insurance

• Large state wise or district wise

contracts

• Not intermediated

• Bids based on combination of

technical and commercial scores

Customer Buying Behavior

Product Innovation - Approach

Customer centric innovation:

• Short-Term Medical Plans

• Accident, cancer & critical illness coverage

• Prescription insurance and discount

• Dental insurance and discount

• Vision insurance

• Health & wellness programs

• Lifestyle discounts

Ideation:

• Identify unique & unmet customer needs

• Define customer segment-specific plans

• Develop the operational capabilities to

effectively deliver these plans (services)

• Monitor and learn from them

How do we innovate on services?

• Ease of sale – right products for the right channel

• Simpler & effective underwriting

• Policy wordings adapted for local market with illustrations

• Ease of claims submission with fast assessment

• Identification of trusted hospitals

• Sharing of information on fraud

• Better communication with customers

Innovation has to be collaborative &

effective:

Two types of innovation — sustainable & disruptive:

• Sustainable innovation takes something that exists today & makes it better. Insurance

product features may be added or fine-tuned, processes streamlined or distribution

channels expanded upon. There is tremendous value in consistent, targeted change that

occurs over time.

• Disruptive innovation is a game changer, something that completely alters the way an

industry operates. Four examples of insurance industry disruptors that have occurred in

recent years include:

– predictive analytics

– usage-based insurance (UBI)

– insurance-linked securitization

– micro-insurance

Product Innovation – Approach Continued..

Health Protection Gap/ Penetration – Indian Scenario

Only 288 mn (22.2%) are covered by health insurance, of which 214 mn are insured by government schemes, 48 mn are covered by group insurance, while 25 mn use individual or family floater plans

Health protection gap is big in India. Gap is projected to rise by 12.3 % annually to $214 bn by 2020

Government & society ‘ll ‘ve to spend more in the future to make up for the growing demand for healthcare services due to higher income growth & a large population

out-of-pock-et expenses account for 60% of the total healthcare expenditure, with a very minor contribution from private insurance plans

With emerging middle class estimated to grow 10-fold from 50 mn at present to 475 mn by 2030, the demand for quality health-care & speed to access services will be greater

Increased consumer awareness along with easier access to healthcare are essential to drive penetration & double health insurance coverage in India by 2020

Health protection gap is the difference between the level of health-care costs, versus the amount that is

available to cover those costs. If total healthcare expenditure remained a constant % of GDP, the country

is likely to face a shortfall in health-care financing of around $43 bn in 2020. This will require additional

spending or higher out-of-pocket funding by individuals

Health Claims Analysis – Male & Female Demography

Male Age Band Highest Claim

Frequency Age Band

2nd Highest Claim

Frequency Age Band

3rd Highest Claim

Frequency

Infectious 1-5 years 0.915% 6-15 years 0.704% 25-36 years 0.52%

Clinical Findings Above 70 years 0.762% 1-5 years 0.758% 61-65 years 0.51%

Digestive 66 - 70 years 0.574% Above 70 years 0.544% 61-65 years 0.48%

Injury Above 70 years 0.335% 66 - 70 years 0.330% 26-35 years 0.31%

Urology 66 - 70 years 0.993% Above 70 years 0.827% 61-65 years 0.77%

Circulatory 66 - 70 years 1.910% Above 70 years 1.219% 61-65 years 0.93%

Female Age Band Highest Claim

Frequency Age Band

2nd Highest Claim

Frequency Age Band

3rd Highest Claim

Frequency

Pregnancy 26-35 years 0.95% 16-25 years 0.36% 36-45 years 0.17%

Infectious Above 1-5 years 0.94% 26-35 years 0.79% 16-25 years 0.72%

Clinical Findings 1-5 years 0.81% Above 70 years 0.64% 61-65 years 0.55%

Urology 66-70 years 0.80% 61-65 years 0.78% 56-60 years 0.59%

Digestive 66-70 years 0.48% 61-65 years 0.46% 26-35 years 0.42%

Eye 66-70 years 1.73% 61-65 years 1.42% Above 70

years 1.32%

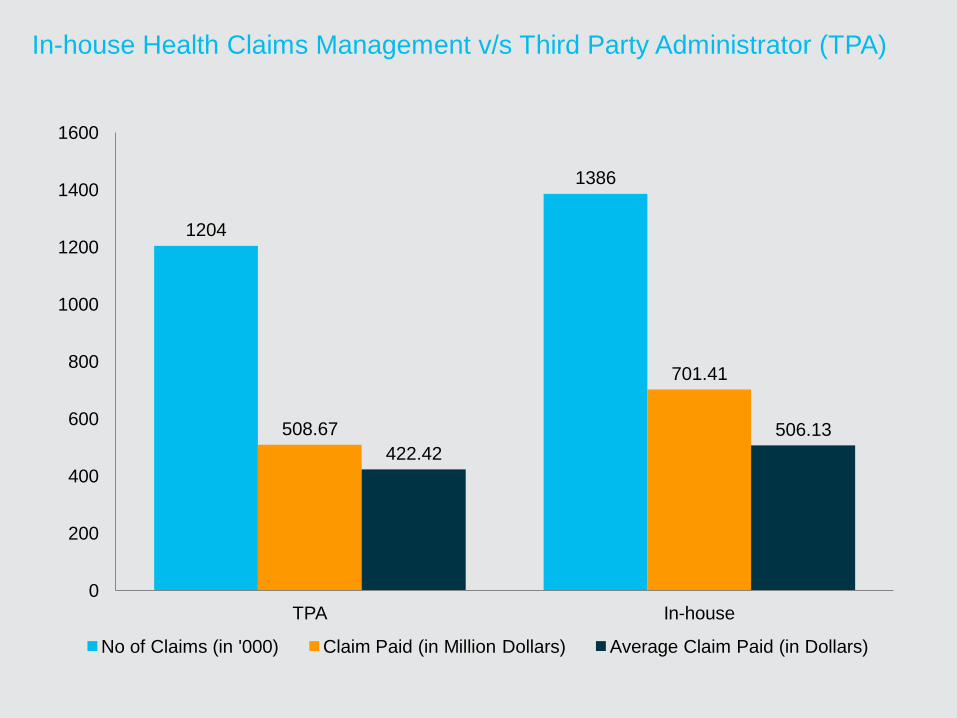

In-house Health Claims Management v/s Third Party Administrator (TPA)

1204

1386

508.67

701.41

422.42

506.13

0

200

400

600

800

1000

1200

1400

1600

TPA In-house

No of Claims (in '000) Claim Paid (in Million Dollars) Average Claim Paid (in Dollars)

Preventive Health Care Approach – Spreading awareness

Limit your salt intake

Don't load up on high protein foods such as meat & steaks

Keep your blood pressure at 130/80 or lower

Keep your blood sugar below 120 mg/dl

Drink 8 glasses of water a day

Watch your intake of pain relievers & other drugs

Be careful with tests & procedures using contrast dyes

Don't drink too much Vitamin C

Don't rely on food supplements to protect your kidneys

Get a kidney check-up

Example: 10 ways to protect your Kidney…

Distribution Mix - Channel wise contribution in health insurance

Health indeminity

(Top Up, HNI) 87%

Hospi Cash & CI

13%

Health Products Share

The profitability of the Health insurance industry - gradually improving

Standalone health insurers seem to have lower claims ratios, showing better pricing

► Net Claims Ratio for the PSU

insurers exceeded 100% largely

due to group health policies

► Since Jan 2007, post-

detariffication, health premiums

have been increasing faster

than the rest of the non-life

insurance markets

Group Segment

► Historically unprofitable segment

► Claims Ratio’s exceed 100% due

to uncompetitive premium rates

and waiver of key policy

exclusions

► Although, claims ratios are more

favorable

► Effective claims management,

strong underwriting and efficient

distribution could lead to lower

claims and distribution expenses

► Individual business can be written

more profitably

Individual Segment Premiums and Claims

Source: IRDAI Annual report and Journals

Claims ratios

Source: Company annual reports

Performance of a 5 years old Standalone Health Insurer - showing

gradual move towards profitability

Financial Performance of one of the Key Standalone Health Insurers (Figures in million USD)

-14.67 -10.17 -4.33 -9.50 -3.67 -13.17 -7.83 -1.67 -6.00 -1.00

62.33

76.67

85.67

93.83 100.33

-

20.00

40.00

60.00

80.00

100.00

120.00

-16.00

-14.00

-12.00

-10.00

-8.00

-6.00

-4.00

-2.00

-

FY11 FY12 FY13 FY14 FY15

Technical Result PBT Capital Infusion