Embed Size (px)

DESCRIPTION

This presentation by Ken Warren was made at the 14th Annual OECD Public Sector Accruals Symposium, Paris 3-4 March 2014. Find out more at http://www.oecd.org/gov/budgeting/14thannualoecdpublicsectoraccrualssymposiumparis3-4march2014.htm

Citation preview

© The Treasury

TIME TO LOOK AGAIN AT ACCRUAL BUDGETING

Ken Warren

Chief Accounting Advisor New Zealand Treasury

© The Treasury

© The Treasury

© The Treasury

Designed for decision-making

• Generally Accepted Accounting Principles (GAAP)

• Principles for the faithful representation of financial results for accountability purposes and to provide relevant information for decision-making purposes.

© The Treasury

Arguments to use GAAP in budgets:

• More consistency • Greater relevance • Better accountability • Greater Coverage

© The Treasury

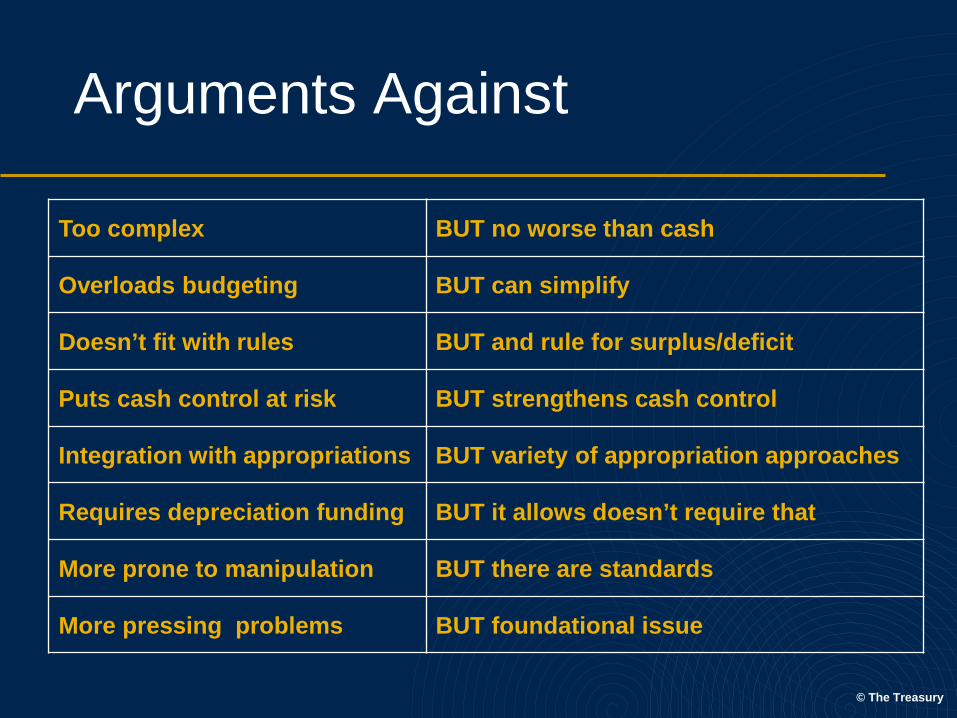

Arguments Against

Too complex BUT no worse than cash

Overloads budgeting BUT can simplify

Doesn’t fit with rules BUT and rule for surplus/deficit

Puts cash control at risk BUT strengthens cash control

Integration with appropriations BUT variety of appropriation approaches

Requires depreciation funding BUT it allows doesn’t require that

More prone to manipulation BUT there are standards

More pressing problems BUT foundational issue

© The Treasury

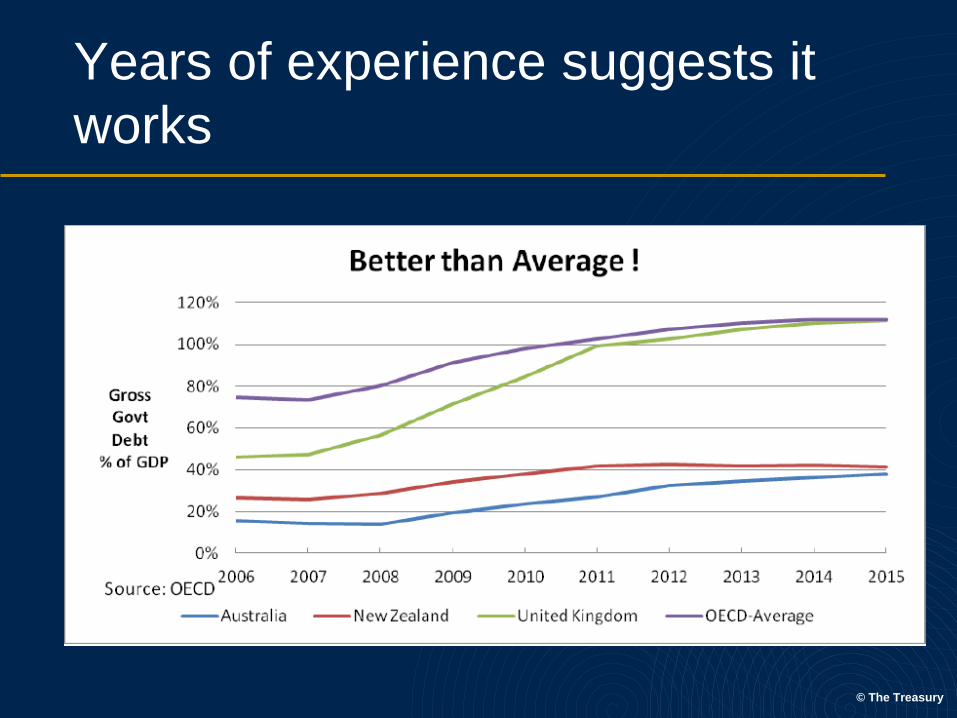

Years of experience suggests it works

© The Treasury

© The Treasury

© The Treasury

© The Treasury

© The Treasury

© The Treasury

© The Treasury

© The Treasury

© The Treasury

© The Treasury

TIME TO LOOK AGAIN AT ACCRUAL BUDGETING

Ken Warren

Chief Accounting Advisor New Zealand Treasury