Embed Size (px)

DESCRIPTION

Slides from an APPG on Social Care public debate, in association with the Strategic Society Centre. Date and time: 16.30-18.30, June 26th 2012 Location: Committee Room 18, House of Commons Speakers at this event comprised: James Lloyd, Director, The Strategic Society Centre Paul Johnson, Director, IFS Anita Charlesworth, Chief Economist, Nuffield Trust and former Director of Public Spending, HM Treasury Caroline Abrahams, Director of External Affairs, Age UK

Citation preview

Can the Treasury combine deficit reduction and reform of social care funding? !!James Lloyd!Director, The Strategic Society Centre!!Tuesday June 26th, 2012!

!!

The Strategic Society Centre is a London-based public policy think-tank, founded in 2010.

The Centre has a simple mission: to examine the big, strategic challenges facing policymakers and society. All our work is independent, objective and free of partisan association.

Various publications on long-term care funding: Immediate Needs Annuities: Their role in funding care Inheritance Tax: Could it be used to fund long-term care ? Politics and the Care Conundrum: Why does England have a problem funding care? Cash Convergence: Enabling choice and independence through disability benefits and social care Stepping Stones: A strategy for reforming long-term care funding Delivering a National Care Fund: How would a public private partnership work? Gone for Good? Pre-funded insurance for long-term care

‘The Roadmap: England’s choices for the care crisis’ Published May 17th, 2012 Download at www.strategicsociety.org.uk

Unprecedented fiscal crisis Government borrowing up £2.7 billion in one year Double-dip recession Unknowable eurozone uncertainties …and the social care system at breaking point. Can the Treasury combine deficit reduction and reform of social care funding?

To start off: what are the decisions that policymakers have to take? What is the cost of reforming social care in England going to be?

Spending Decision!What will the state spend on care and

support in future and how will this money

be spent?!

Spending Decision!What will the state spend on care and

support in future and how will this money

be spent?!

Funding Decision!Where will the

money come from to fund spending

on care?!

Spending Decision!What will the state spend on care and

support in future and how will this money

be spent?!

Funding Decision!Where will the

money come from to fund spending

on care?!

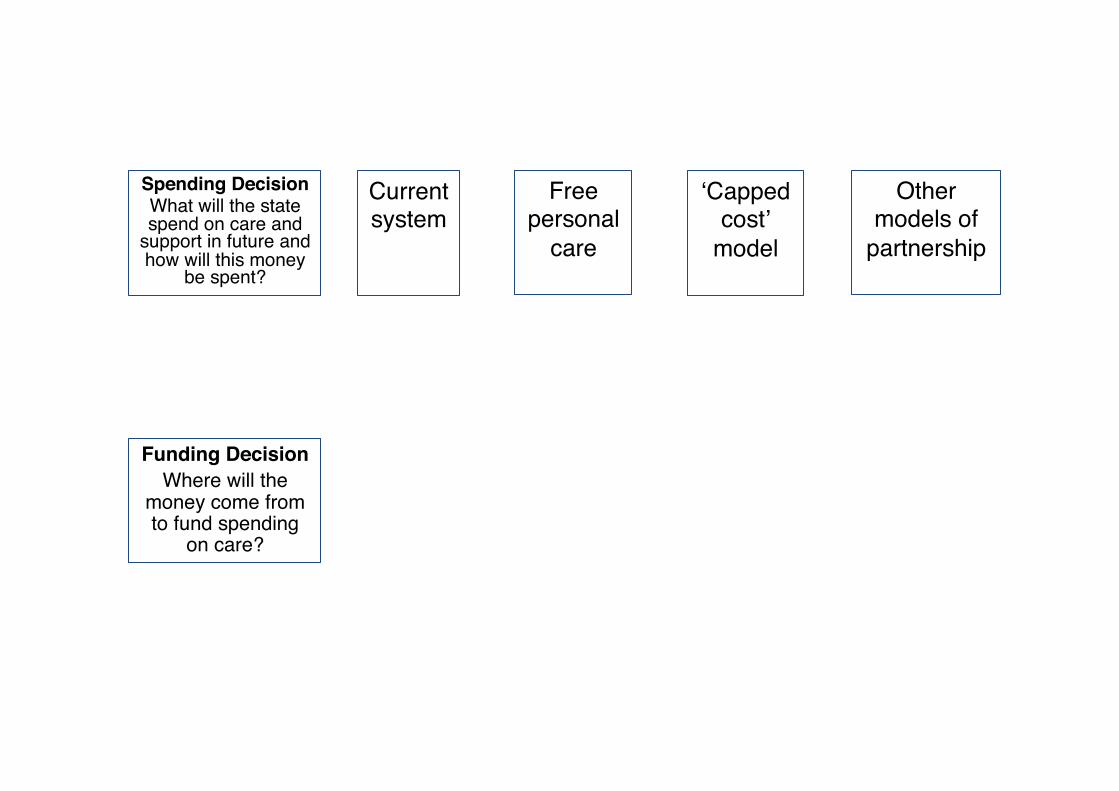

Current system!

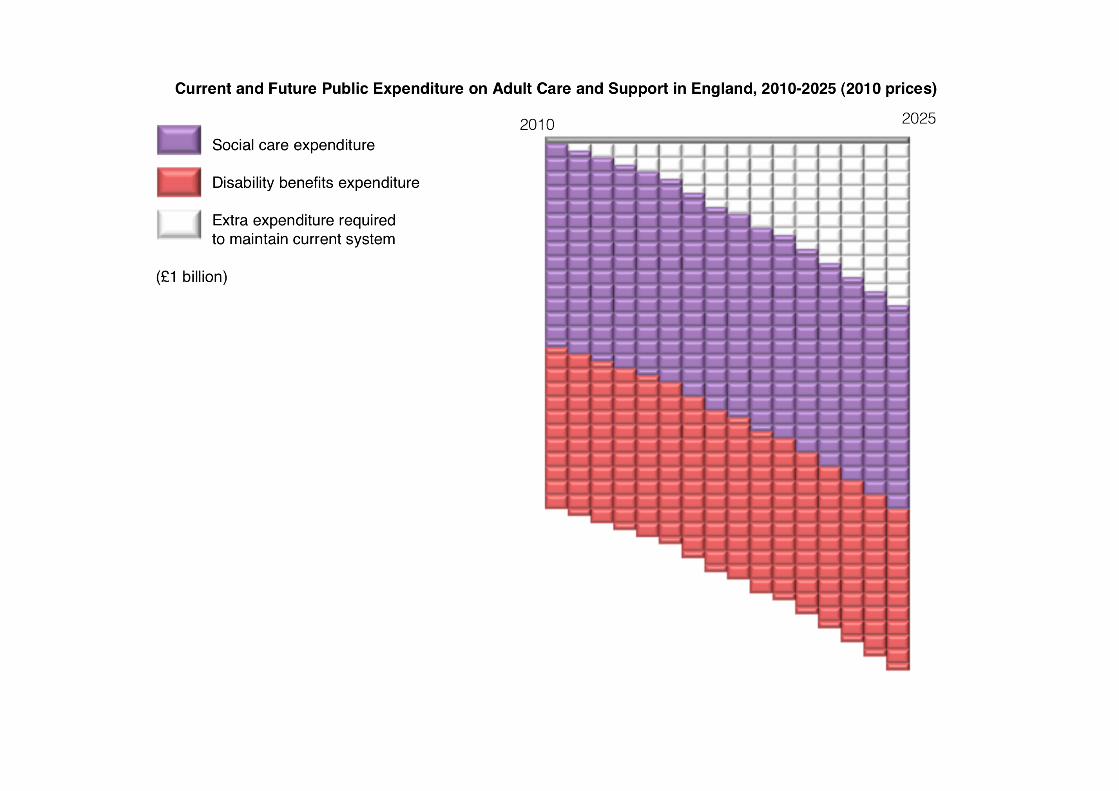

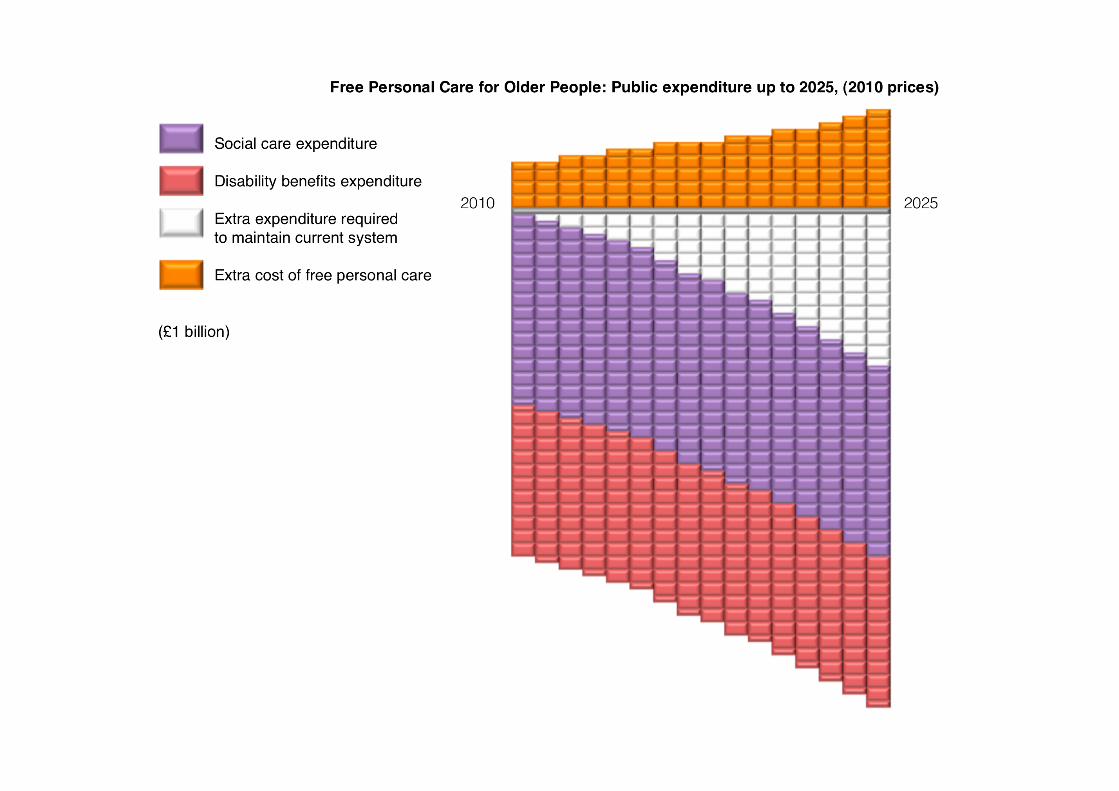

Key point: just to maintain current system, the Treasury is going to have to find billions of pounds in future. Risk: reforming the system makes this challenge even bigger. Opportunity: Treasury will have face up to these difficult questions anyway. Public may be more likely to accept tough decisions if linked to reform of care system. So what are the options for reform?

Spending Decision!What will the state spend on care and

support in future and how will this money

be spent?!

Funding Decision!Where will the

money come from to fund spending

on care?!

Current system!

Free personal

care!

Spending Decision!What will the state spend on care and

support in future and how will this money

be spent?!

Funding Decision!Where will the

money come from to fund spending

on care?!

Current system!

Free personal

care!

ʻCapped costʼ

model!

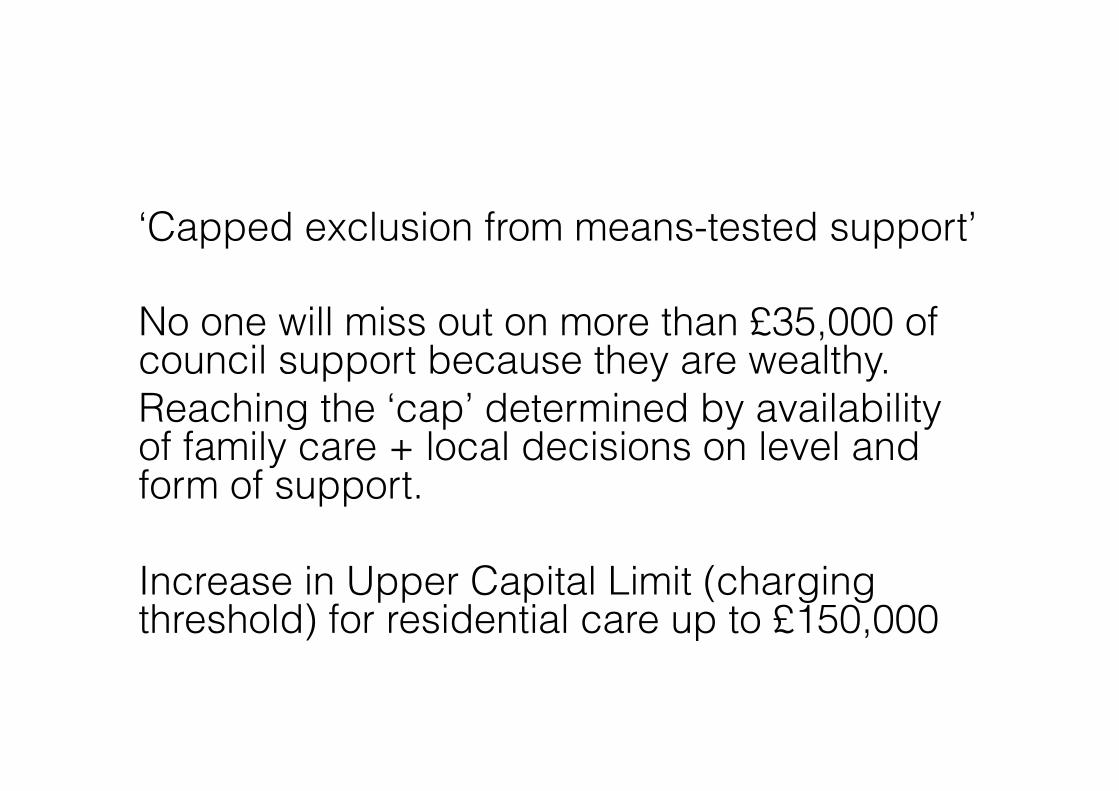

‘Capped exclusion from means-tested support’ No one will miss out on more than £35,000 of council support because they are wealthy. Reaching the ‘cap’ determined by availability of family care + local decisions on level and form of support. Increase in Upper Capital Limit (charging threshold) for residential care up to £150,000

Spending Decision!What will the state spend on care and

support in future and how will this money

be spent?!

Funding Decision!Where will the

money come from to fund spending

on care?!

Current system!

Free personal

care!

ʻCapped costʼ

model!

Other models of

partnership!

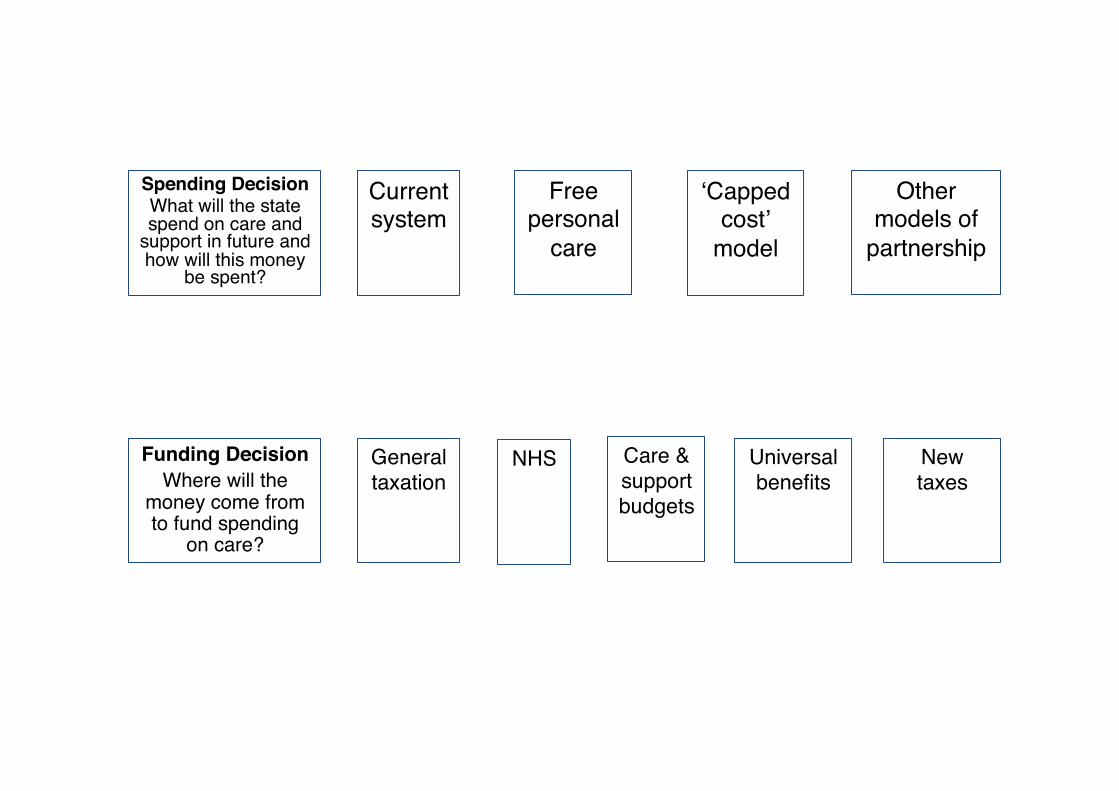

So, different ‘spending proposals’ for reshaping the care system. But all ultimately depends on the Funding Question…

The Funding Question… …Where will the money come from to fund spending on care and support? = Costs of current baseline system going forward + cost of new ‘partnership’ Can the Treasury combine these costs of reform with deficit reduction?

The Funding Question… So what are the options?

Spending Decision!What will the state spend on care and

support in future and how will this money

be spent?!

Funding Decision!Where will the

money come from to fund spending

on care?!

Current system!

Free personal

care!

ʻCapped costʼ

model!

Other models of

partnership!

Spending Decision!What will the state spend on care and

support in future and how will this money

be spent?!

Funding Decision!Where will the

money come from to fund spending

on care?!

Current system!

Free personal

care!

ʻCapped costʼ

model!

Other models of

partnership!

General taxation!

NHS! Care & support budgets!

Universal benefits!

New taxes!

So how should policymakers think about these choices?

Treasury will have face up to these difficult questions anyway. Public may be more likely to accept tough decisions if linked to reform.

Key principle: those who benefit from reform should pay for reform. Essential for intergenerational fairness. Even more important in context of deficit reduction, and reduced spending on younger cohorts.

Competing policy objectives: care is not the only issue for the older population requiring reform. For example: 27,000 excess winter deaths among the elderly each year. A competing use for expenditure on Winter Fuel Payments?

Understand what works: practical constraints. For example, means testing system for Pension Credit doesn’t work. Only reaches 2 in 3 of target group.

Understand public attitudes: economic crisis has changed attitudes among older people. Greater acceptance of benefit cuts or new taxes?

Understand outcomes and costs to the public purse: For example, prevention can be cheaper. Subsidised transport for the elderly: a form of prevention?

So, can the Treasury combine deficit reduction and reform of social care funding? Yes. There is money in older households, especially housing wealth. There are potential ‘tax and spending’ changes. Older people more likely to accept tough decisions if linked to reform. Government and care sector can work together to prepare public opinion.

© Institute for Fiscal Studies

Paying for Dilnot

James Browne and Paul Johnson

June 26, 2012

Paying for the Dilnot commission proposals

• Overall question: – Are there coherent ways of ensuring that better off pensioners as a

group pay for more generous social care funding?

• What does the pensioner income distribution look like? – And how has it evolved over time?

• What elements of the current tax and benefit system look less than coherent – And how could they be reformed

• What options exist to raise money while enhancing coherence?

© Institute for Fiscal Studies

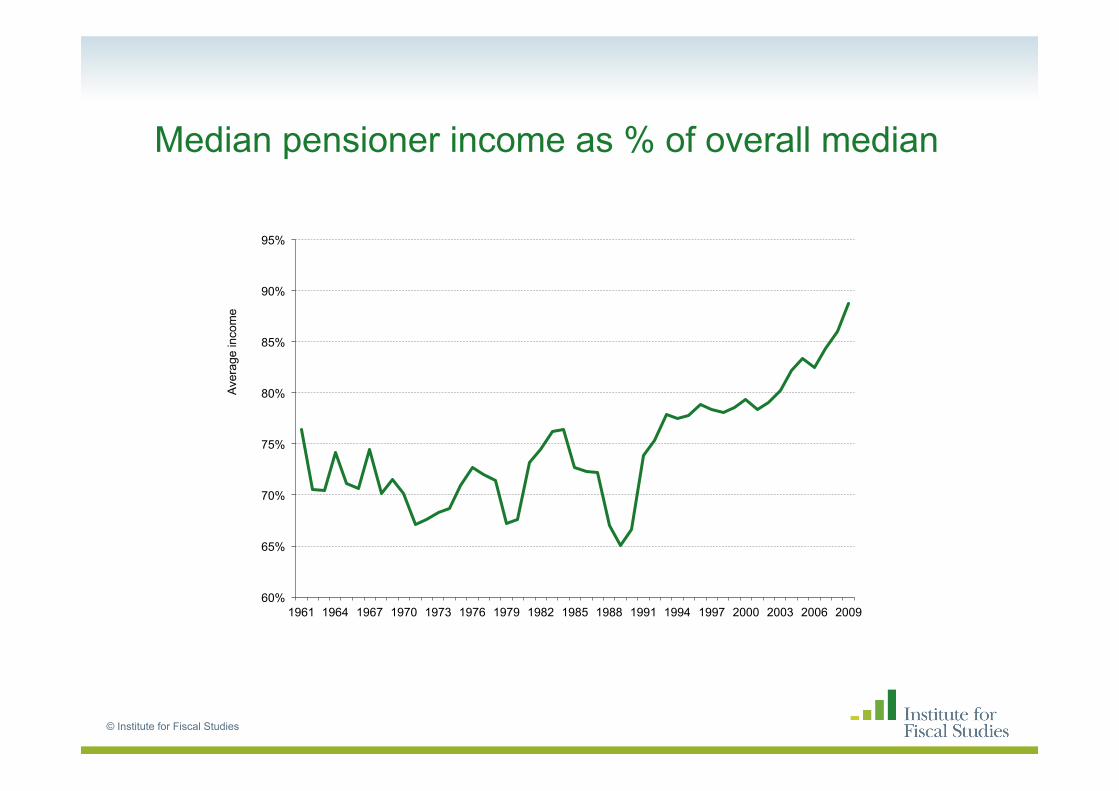

Pensioners

• Have moved up the income distribution over time

© Institute for Fiscal Studies

Median pensioner income as % of overall median

© Institute for Fiscal Studies

60%

65%

70%

75%

80%

85%

90%

95%

1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009

Ave

rage

inco

me

Pensioners

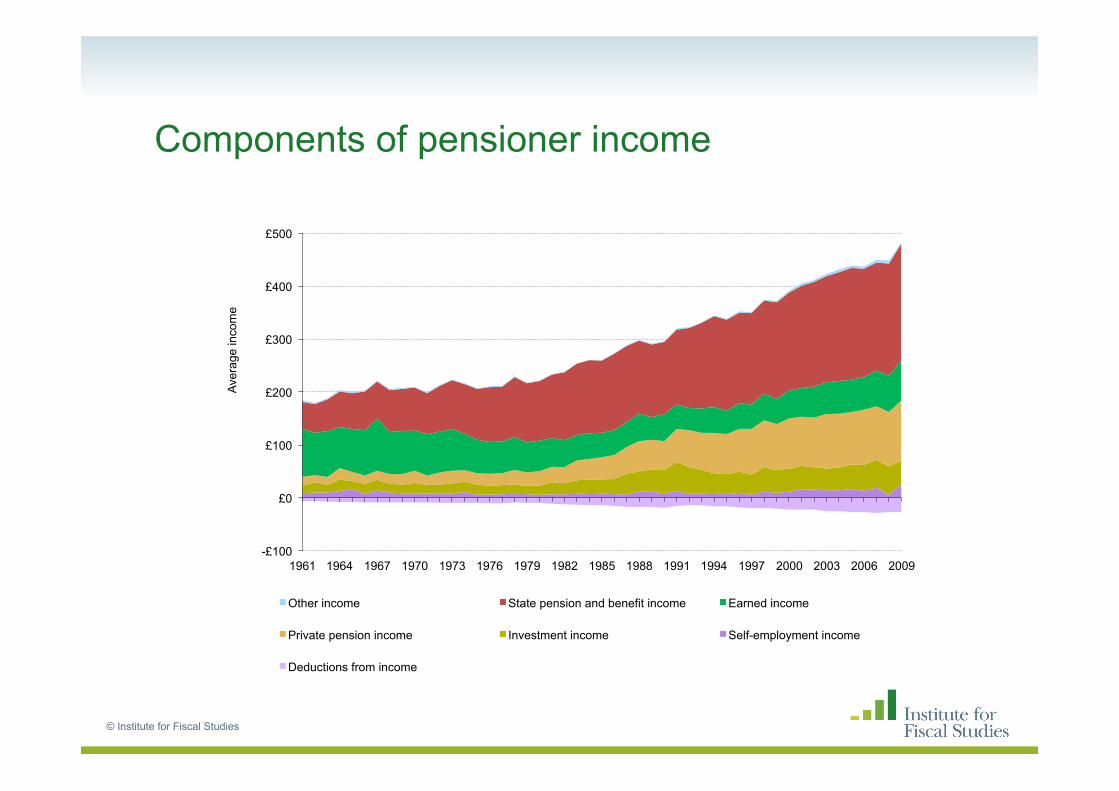

• Have moved up the income distribution over time • Getting better off as incomes from state and private sources

have increased

© Institute for Fiscal Studies

Components of pensioner income

© Institute for Fiscal Studies

-£100

£0

£100

£200

£300

£400

£500

1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009

Aver

age

inco

me

Other income State pension and benefit income Earned income

Private pension income Investment income Self-employment income

Deductions from income

Pensioners

• Have moved up the income distribution over time • Getting better off as incomes from state and private sources

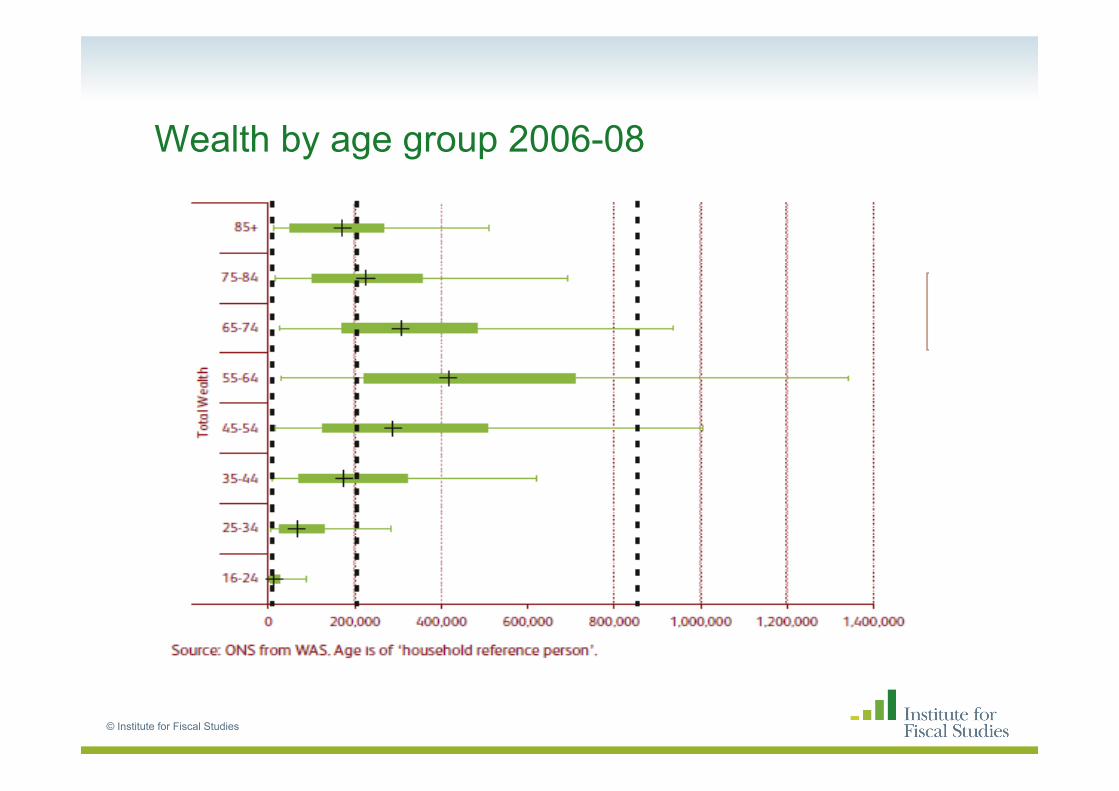

have increased • Wealth levels are also higher among older groups

© Institute for Fiscal Studies

Wealth by age group 2006-08

© Institute for Fiscal Studies

Pensioners

• Have moved up the income distribution over time • Getting better off as incomes from state and private sources

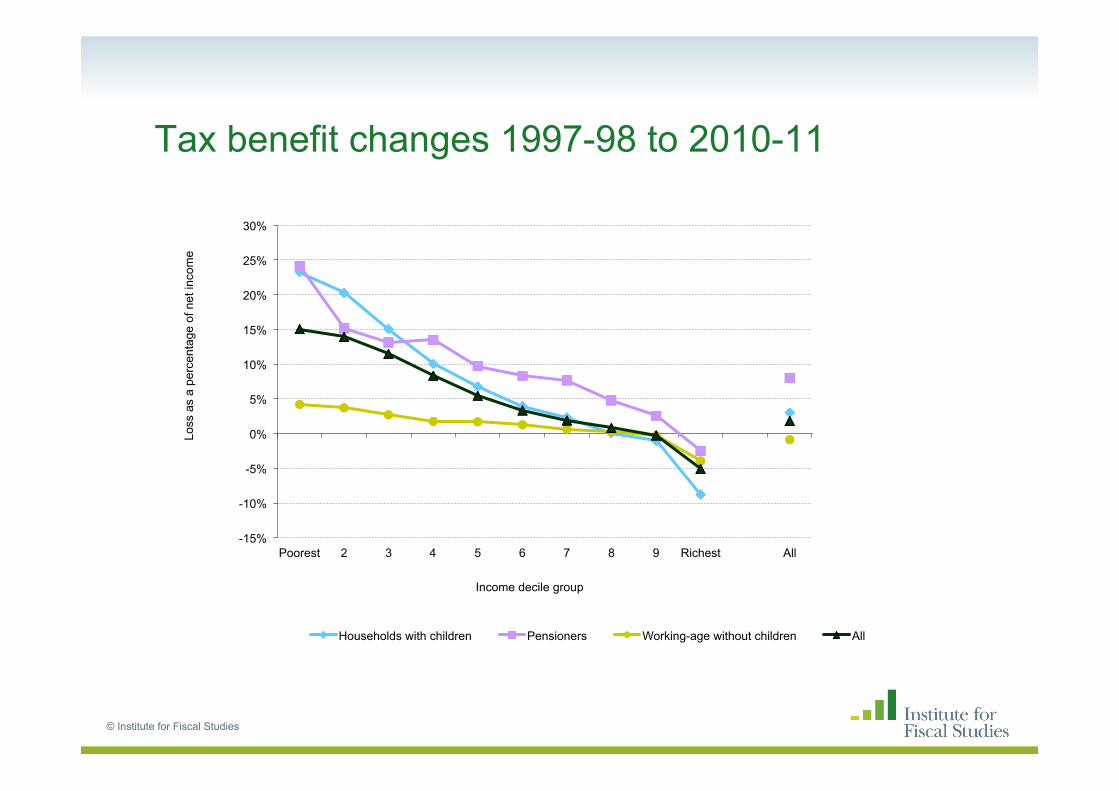

have increased • Wealth levels are also higher among older groups • They did well from Labour’s tax and benefit reforms

– Though it was mostly those on lower incomes who benefited

© Institute for Fiscal Studies

Tax benefit changes 1997-98 to 2010-11

© Institute for Fiscal Studies

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Poorest 2 3 4 5 6 7 8 9 Richest All

Loss

as

a pe

rcen

tage

of n

et in

com

e

Income decile group

Households with children Pensioners Working-age without children All

Pensioners

• Have moved up the income distribution over time • Getting better off as incomes from state and private sources

have increased • Wealth levels are also higher among older groups • They did well from Labour’s tax and benefit reforms

– Though it was mostly those on lower incomes who benefited

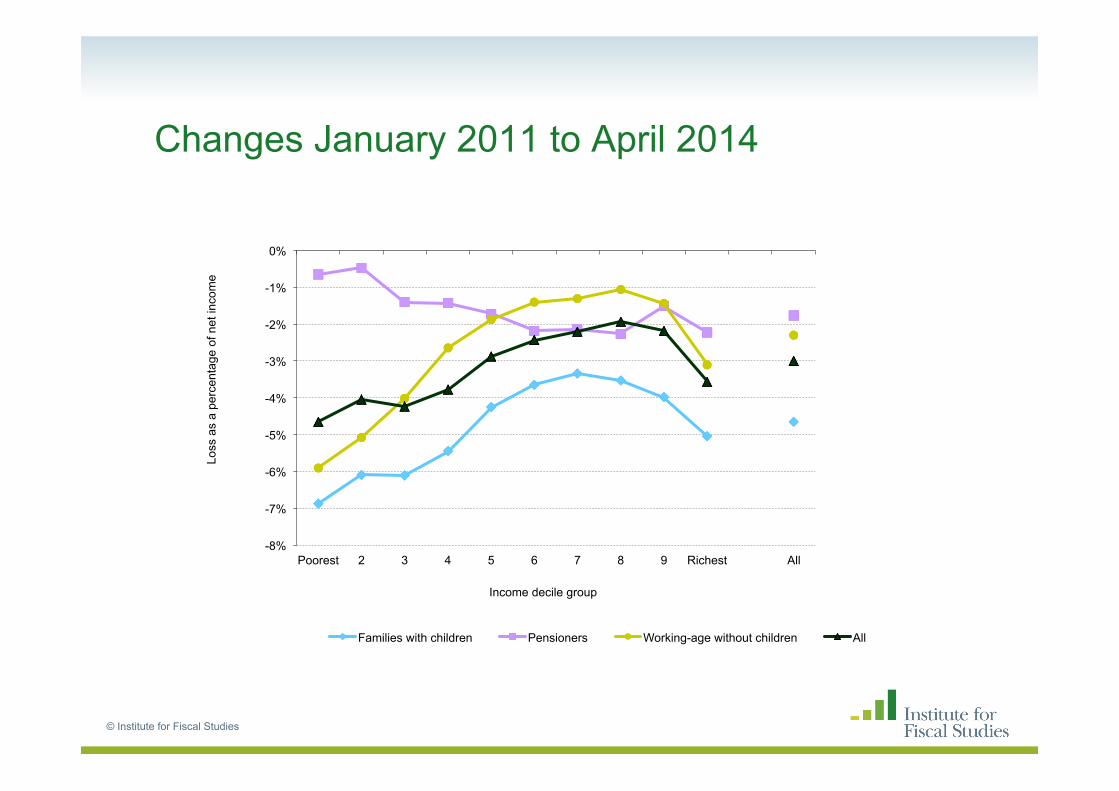

• And are relatively protected in recent changes

© Institute for Fiscal Studies

Changes January 2011 to April 2014

© Institute for Fiscal Studies

-8%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

Poorest 2 3 4 5 6 7 8 9 Richest All

Loss

as

a pe

rcen

tage

of n

et in

com

e

Income decile group

Families with children Pensioners Working-age without children All

Promises to protect pensioners

• Triple lock on state pensions helps them all – Most valuable to those not on means tested benefits

• Protection of specific benefits like winter fuel allowance also protects all

• They are the only group protected from cuts to Council Tax Benefit in England – That helps only poorer pensioners

© Institute for Fiscal Studies

Promises to protect pensioners

• Triple lock on state pensions helps them all – Most valuable to those not on means tested benefits

• Protection of specific benefits like winter fuel allowance also protects all

• They are the only group protected from cuts to Council Tax Benefit in England – That helps only poorer pensioners

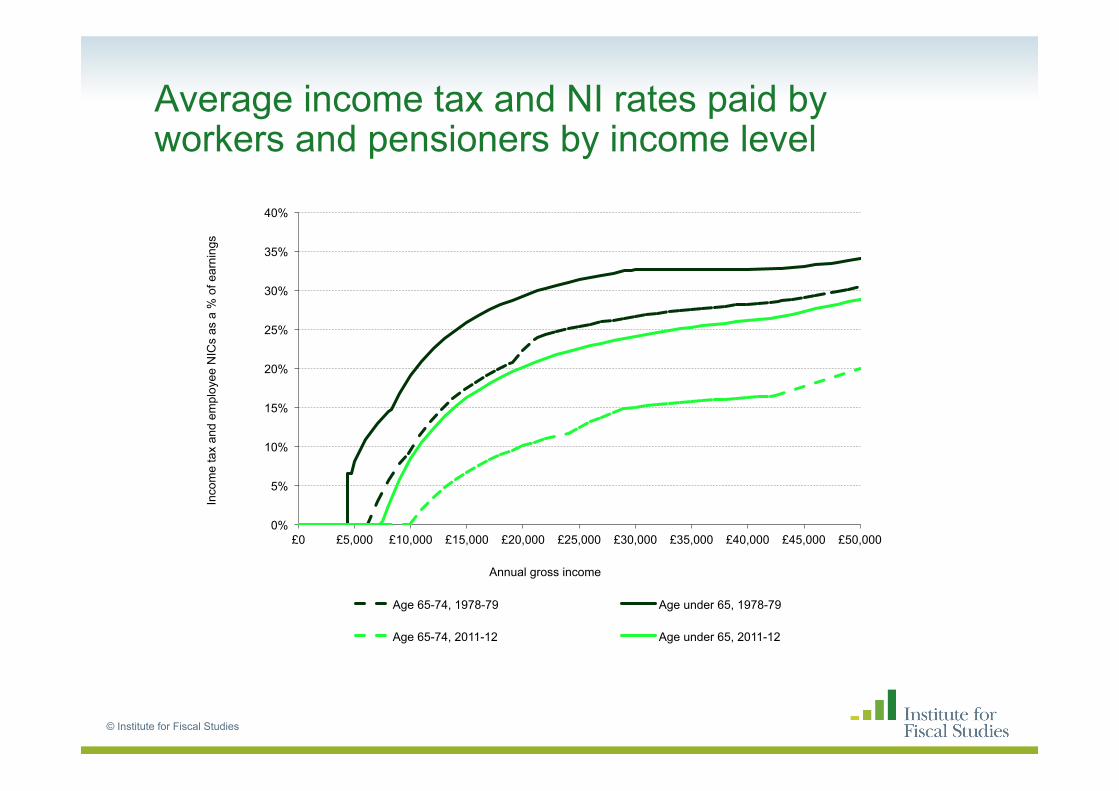

• Over a longer period movement from income tax to NI has been very beneficial for pensioners

© Institute for Fiscal Studies

Average income tax and NI rates paid by workers and pensioners by income level

© Institute for Fiscal Studies

0%

5%

10%

15%

20%

25%

30%

35%

40%

£0 £5,000 £10,000 £15,000 £20,000 £25,000 £30,000 £35,000 £40,000 £45,000 £50,000

Inco

me

tax

and

empl

oyee

NIC

s as

a %

of e

arni

ngs

Annual gross income

Age 65-74, 1978-79 Age under 65, 1978-79

Age 65-74, 2011-12 Age under 65, 2011-12

But the future may not be so rosy

• Much of the increase in incomes is down to more generous state and private pension arrangements – SERPS and S2P are becoming less generous for higher earners

– Private sector DB schemes are disappearing

• Interest rates are at historically low levels

• Annuity rates may remain low

• Loss of additional personal allowance may be prelude to other changes

© Institute for Fiscal Studies

Principles for reform

• Look for where the current system deviates from a coherent structure for supporting pensioners

• Basic and earnings related pensions and pension credit represent a coherent system of support by themselves

• Other additional benefits and tax reliefs need to be justified

© Institute for Fiscal Studies

Additional benefits

• Winter fuel allowance – Goes to all pensioners, not taxed or means-tested

– Cost: £2.2 billion

• Free bus passes – Total cost of concessionary bus travel £1 billion

– (Not all of this is for pensioners)

• Free TV licences (for over 75s) – Cost: £600 million

© Institute for Fiscal Studies

Also look at coherence of the tax system

• No NICs on earnings after state pension age – cost £800 million – this is a separate issue from the general shift from income tax to NI

• Higher income tax personal allowances – Being phased out

• Single person discount for Council Tax – Particularly valuable to pensioners

• CGT is forgiven at death – cost £600 million – And IHT is probably in need of reform

© Institute for Fiscal Studies

Taxation of pensions

• Tax neutral treatment of saving generally appropriate – Want more generous treatment for pensions

– Current treatment is more generous in various ways, but maybe excessive and not the most efficient ways

• Tax free lump sum costs £2.5 billion – Limiting to higher rate threshold would save £500 million

• Employer pension contributions not subject to NI at any point – Which is both distorting/unfair relative to those whose employer

does not contribute and extraordinarily generous

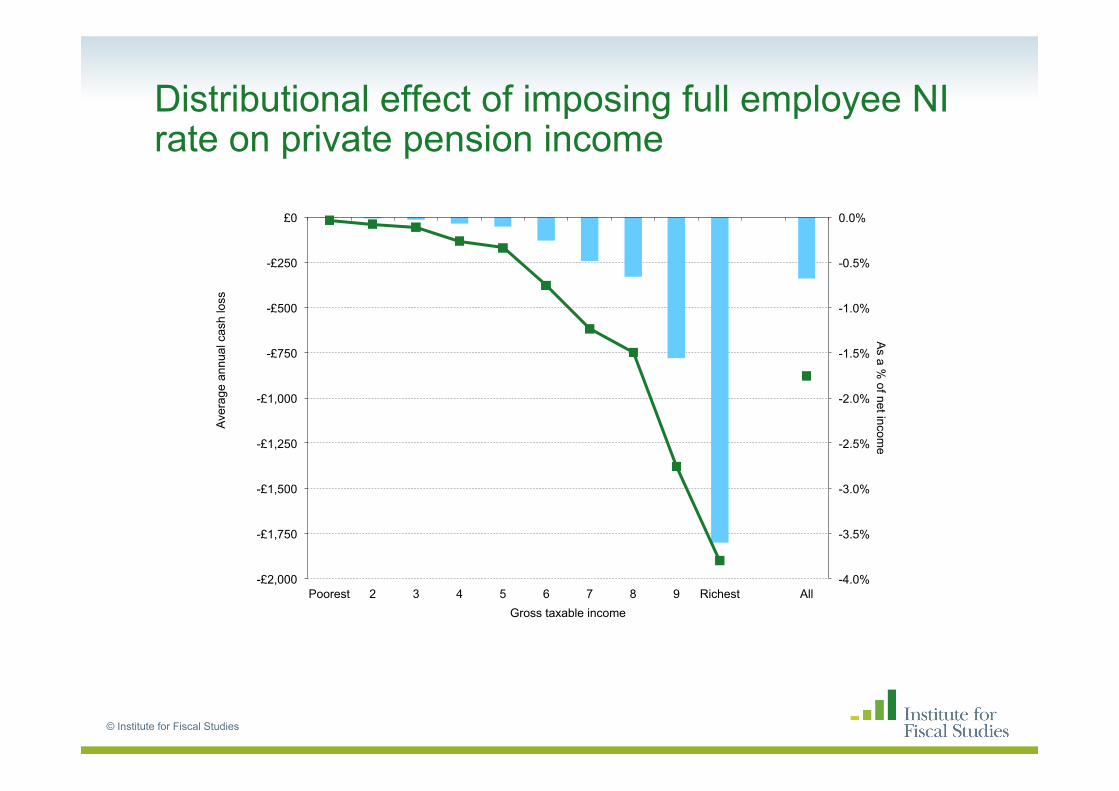

• Imposing NI on private pensions in payment could raise £350 million per 1p – Any such change would need to be phased in

© Institute for Fiscal Studies

Distributional effect of imposing full employee NI rate on private pension income

© Institute for Fiscal Studies

-4.0%

-3.5%

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

-£2,000

-£1,750

-£1,500

-£1,250

-£1,000

-£750

-£500

-£250

£0

Poorest 2 3 4 5 6 7 8 9 Richest All

As a %

of net income

Ave

rage

ann

ual c

ash

loss

Gross taxable income

Conclusions

• The “Dilnot reforms” would benefit better off pensioners

• As a group pensioners have done relatively well in recent years – Though their incomes are still below those of working age on

average

• The current tax and benefit system is not wholly rational in its treatment of pensioners – If one wanted to find money from better off pensioners to fund the

Dilnot proposals one could

• Universal benefits like winter fuel allowances and free TV licences could be means-tested, abolished, or consolidated into the pension

• CGT at death, NICs and tax treatment of pensions could all be reformed to increase coherence

© Institute for Fiscal Studies