Embed Size (px)

DESCRIPTION

Views from Brussels and national capitals across Europe on the implications for businesses, focusing on the financial services, energy and technology, media and telecommunications sectors.

Citation preview

Brunswick Group 26 May 2014

Talking Politics

No watershed moment, but not quite business as

usual for Brussels

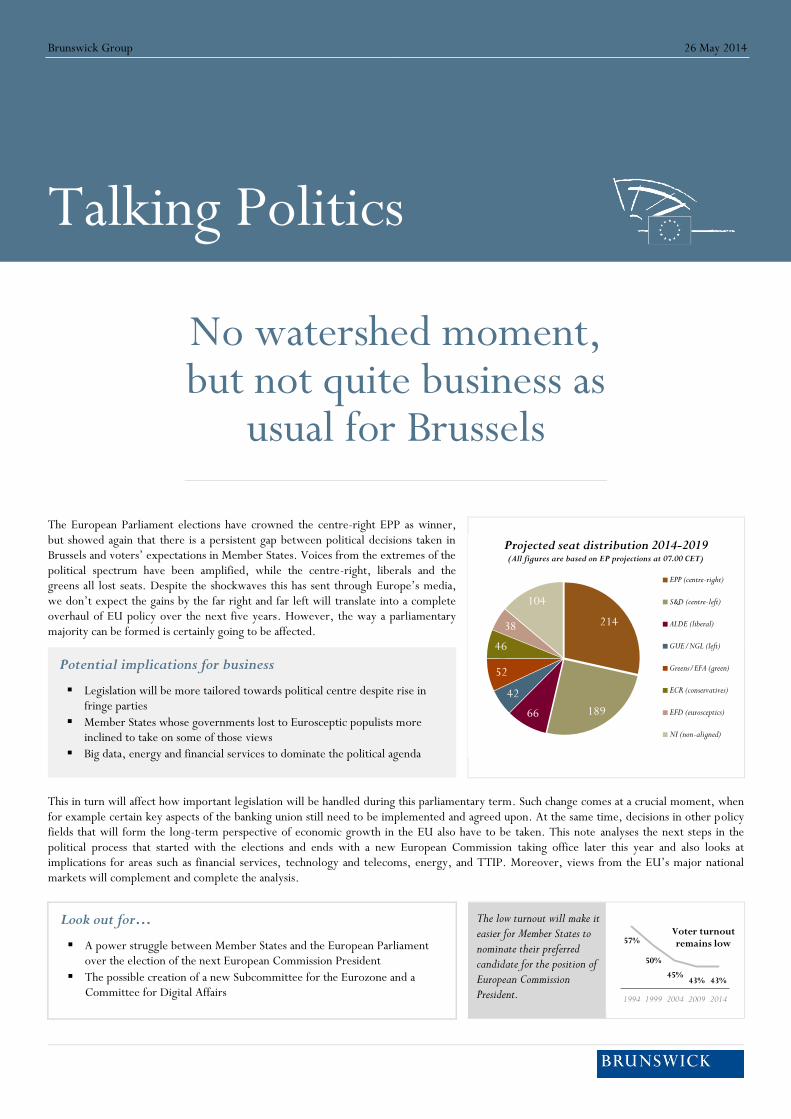

The European Parliament elections have crowned the centre-right EPP as winner, but showed again that there is a persistent gap between political decisions taken in Brussels and voters’ expectations in Member States. Voices from the extremes of the political spectrum have been amplified, while the centre-right, liberals and the greens all lost seats. Despite the shockwaves this has sent through Europe’s media, we don’t expect the gains by the far right and far left will translate into a complete overhaul of EU policy over the next five years. However, the way a parliamentary majority can be formed is certainly going to be affected.

Potential implications for business

Legislation will be more tailored towards political centre despite rise in fringe parties

Member States whose governments lost to Eurosceptic populists more inclined to take on some of those views

Big data, energy and financial services to dominate the political agenda

This in turn will affect how important legislation will be handled during this parliamentary term. Such change comes at a crucial moment, when for example certain key aspects of the banking union still need to be implemented and agreed upon. At the same time, decisions in other policy fields that will form the long-term perspective of economic growth in the EU also have to be taken. This note analyses the next steps in the political process that started with the elections and ends with a new European Commission taking office later this year and also looks at implications for areas such as financial services, technology and telecoms, energy, and TTIP. Moreover, views from the EU’s major national markets will complement and complete the analysis.

Look out for…

A power struggle between Member States and the European Parliament over the election of the next European Commission President

The possible creation of a new Subcommittee for the Eurozone and a Committee for Digital Affairs

The low turnout will make it easier for Member States to nominate their preferred candidate for the position of European Commission President.

214

189 66

42

52

46

38

104

Projected seat distribution 2014-2019 (All figures are based on EP projections at 07.00 CET)

EPP (centre-right)

S&D (centre-left)

ALDE (liberal)

GUE/NGL (left)

Greens/EFA (green)

ECR (conservatives)

EFD (eurosceptics)

NI (non-aligned)

57%

50%

45% 43% 43%

1994 1999 2004 2009 2014

Voter turnout remains low

Following the groups’ formation, MEPs will then

decide on their new President, Vice-Presidents,

and Committee Chairs. Expect a lot of horse trading

and backroom deals.

What is Next?

Shifts in the balance of power will lead to informal grand coalition

The overall balance of power in the new European Parliament remains largely unaffected, but the political centre still lost out to fringe parties. However, the likely formation of an informal “grand coalition” between the centre-right EPP and the centre-left S&D groups will bring more substantive change to the way the European Parliament works. Unlike in the previous Parliament, there are no other possible constellations of either centre-left or centre-right groups that can gather enough MEPs to adopt legislation. As a consequence, the kingmaker role of the liberal ALDE group is significantly reduced.

A second major change will most likely be the formation of a political group of far right parties. While this would increase their public profile considerably, the different political views within such a group are too heterogeneous to make any real impact on the policy formulation process. However, their increased presence will be felt in the Council, as national governments attempt to counter the raising influence of these fringe parties back in their home countries.

Formation of political groups

The national parties will convene over the next five weeks to form their political groups. Several old and new delegations will have to make a difficult choice where to sit. For example, the future affiliation of Germany’s Eurosceptic AfD, Italy’s populist Five Star Movement, and Belgium’s N-VA are still unclear. The future of the ECR and the EFD might also be called into question, as both of them more or less depend on the British delegations and their decisions.

Election of European Commission President

The big unknown is still how the Member States and the European Parliament will agree on a new Commission President. The EPP’s main candidate Jean-Claude Juncker already stated he expects to be the next Commission President, but Member States are eager to retain their prerogative in nominating the candidate. Leaders of the old European Parliament will gather this week to analyse the outcome of the elections, as will national heads of state and/or government. Member States are expected to give a mandate to the European Council President Herman van Rompuy to start consultations with the Parliament. A power struggle between the Parliament and the Member States is likely to derail the ordinary timetable of electing the new Commission.

Summer Timeline

Financial Services Attempts to regulate financial markets have made the Economic and Monetary Affairs Committee (ECON) the linchpin of parliamentary work over the last five years. We are now seeing a gradual slowing down of new legislative proposals by the European Commission. The banking union is nearing completion with a Single Supervisory Mechanism (SSM), a Single Resolution Mechanism (SRM) and a Deposit Guarantee Scheme (DGS) already decided. The only major policy proposal still at an early stage is the restructuring of the banking sector.

Therefore, over the next five years, we predict more ‘business as usual’ for the ECON Committee. Yet major technical and political decisions still need to be taken by the European institutions and authorities. The focus will shift to reviews of current legislation as well as level 2 implementing decisions.

All this will have to be done under a new leadership, as ECON Chair Sharon Bowles (ALDE, UK) did not stand for re-election. Candidates for the position of ECON chair include a small number of key MEPs from Germany, the UK and France, who have served on the ECON Committee in the past and possess the necessary experience for the job. Othmar Karas MEP (EPP, AT), despite being from a small Member State, would also be such a potential candidate.

Another key development to look out for will be the possible creation of a new Eurozone Subcommittee. MEPs discussed such a possibility during the end of their last term, but ended up not taking a decision, effectively leaving the question for the new EP. MEPs have been looking for a way to counter the growing influence of the Member States in financial legislation, and the instalment of a Euro Subcommittee might be a feasible response.

Contact Brunswick Brussels

Address

27 Avenue Des Arts

1040 Brussels Belgium

Tel.+32 2 235 6510

Fax+32 2 235 6522

Email [email protected]

Technology & Telecoms

Big Data

The transformative power of internet and big data has been a part of the European electoral campaign itself, evidenced by a frenzy of social media activities by all sorts of candidates, EU institutions and stakeholders alike. For businesses of all background, big data is becoming more and more essential to their core business activities, rather than something that is confined to their IT departments. This debate on big data has only just begun, and it will determine the work programme of the new European Parliament in the years to come.

The General Data Protection Regulation still needs to be negotiated between the European Parliament and the Member States, who themselves have yet to agree on a compromise that satisfies both data protection and privacy concerns as well as the well-being of the wider economy that is dependent on the free flows of information.

Related to this legislative dossier are a range of other policy fields where the EU has been active or initiated legislation. Completing the digital single market, cloud computing, intellectual property and copyright reform, and the question of government surveillance are all connected to each other in the sense that big data plays a role in all of them. The upcoming Commission “Communication on a data-driven economy” will be one of the first dossiers to look at for the new Parliament. The Civil Liberties, Justice and Home Affairs Committee (LIBE) will therefore see an uptake in external interest and legislative activities, meaning that new and returning MEPs in this Committee will quickly find them at the centre of one of the most important political debates in the EU. Some MEPs have also suggested the establishment of a new ‘Digital Affairs’ Committee dedicated entirely to digital issues.

Telecommunications

The European telecommunications sector is looking at a new wave of consolidation and M&A activities. German Chancellor Angela Merkel recently stated she is in favour of further consolidation in the sector. Therefore, we expect the issue to remain high on the radar of EU public officials. When the hearings with nominees for the next European Commission take place in the European Parliament, we expect the new Competition Commissioner to be grilled on his or her views on past merger and consolidation cases in the telecommunications sector.

Energy

Developments in the Ukraine and the European Commission’s proposals for a 2030 framework on energy and climate policies have brought the ‘energy question’ back on the European agenda. The upcoming Italian Council Presidency is committed to reaching an agreement on the 2030 framework and bridging the existing gap among Member States.

In addition, the European Commission will present its in-depth analysis and action plan on how to reduce the EU’s dependency on Russian gas imports this week, and the question is sure to be picked up by the new European Parliament, most likely in the form of non-binding resolutions or an own-initiative report until a formal legislative proposal is presented.

It is worth noting that in East European Member States parties with a strong anti-Russian stance have managed to gain considerable support over the last couple of months, with the best example being the Civic Platform of Polish Prime Minister Donald Tusk, which came in first in Poland after having trailed the oppositional Law and Justice Party in polls for over a year. The Polish government will take this result as an encouragement to continue pushing forward with its plan for an ‘Energy Union’, which asks for joint gas purchasing by the EU. Also look for Poland to make a push to ensure the Energy or Foreign Affairs portfolio for their next EU Commissioner.

It is also significant that in two key Eastern European Member States national elections will take place in 2014/2015: Poland will hold presidential and parliamentary elections in 2015, and Latvia, which will take over the Council Presidency from Italy in the first half of 2015, is set to hold its general election in October 2014.

The upcoming international climate change conference in Paris is expected for 2015, where countries will try to negotiate a legally binding and universal agreement replacing the Kyoto protocol. An improving economic outlook might lead to more openness by European leaders for a comprehensive deal, a policy that the European Parliament is likely to pursue as well.

TTIP

The outcome of the elections could also have an impact on the negotiations surrounding the Trans-Atlantic free trade agreement TTIP. This will need to be approved by the European Parliament and Member states before ratification (probably in late 2015). Marine Le Pen of the French National Front has been clear that she would oppose the agreement. The EU Greens (in conjunction with their US counterparts) have already stated that the agreement is a threat to democracy, and many of the Socialist and some EPP MEPs in the last Parliament have expressed concerns about the investment protection aspects of the agreement, which they see as potentially overturning decisions by national governments. The make-up of the new Parliament is likely to reinforce these views. The largest UK party, UKIP, has not taken a definitive stance – on the one hand, they want free trade with non-EU countries, on the other do not want the EU negotiating this for them.

Views from the Capitals

Germany

96 MEPs

72 MEPs ran

66 MEPs re-elected

30 Newcomers

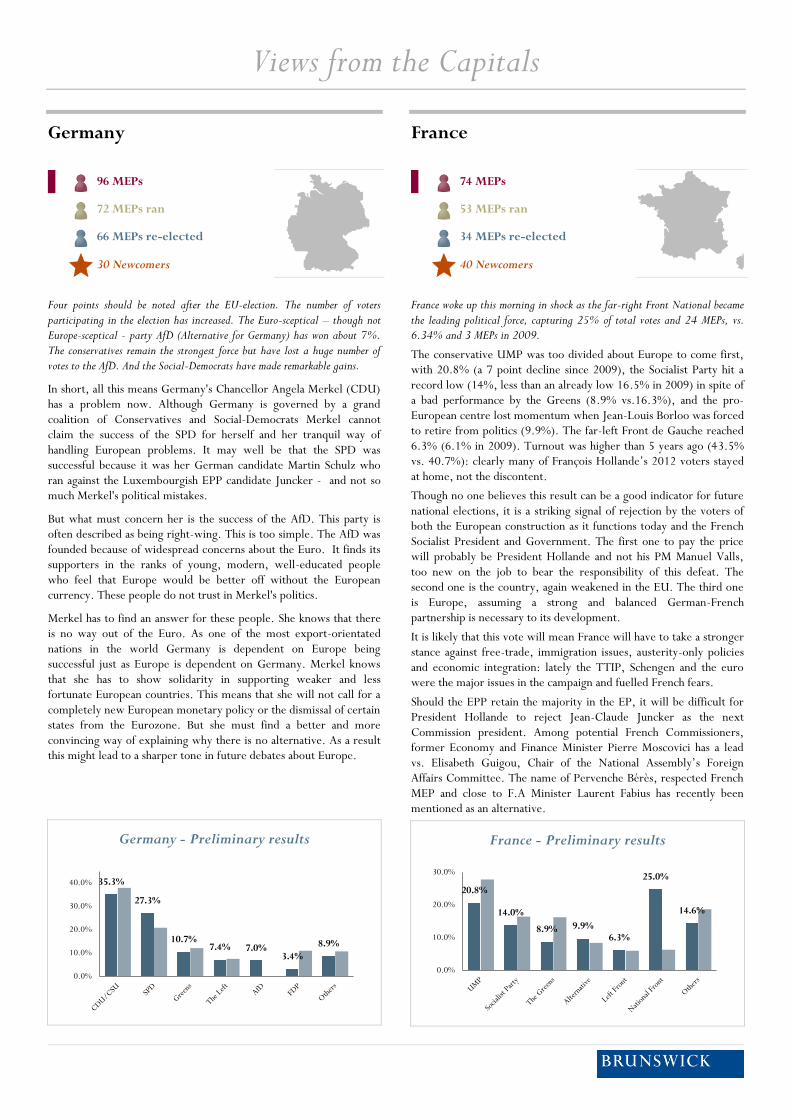

Four points should be noted after the EU-election. The number of voters participating in the election has increased. The Euro-sceptical – though not Europe-sceptical - party AfD (Alternative for Germany) has won about 7%. The conservatives remain the strongest force but have lost a huge number of votes to the AfD. And the Social-Democrats have made remarkable gains.

In short, all this means Germany's Chancellor Angela Merkel (CDU) has a problem now. Although Germany is governed by a grand coalition of Conservatives and Social-Democrats Merkel cannot claim the success of the SPD for herself and her tranquil way of handling European problems. It may well be that the SPD was successful because it was her German candidate Martin Schulz who ran against the Luxembourgish EPP candidate Juncker - and not so much Merkel's political mistakes.

But what must concern her is the success of the AfD. This party is often described as being right-wing. This is too simple. The AfD was founded because of widespread concerns about the Euro. It finds its supporters in the ranks of young, modern, well-educated people who feel that Europe would be better off without the European currency. These people do not trust in Merkel's politics.

Merkel has to find an answer for these people. She knows that there is no way out of the Euro. As one of the most export-orientated nations in the world Germany is dependent on Europe being successful just as Europe is dependent on Germany. Merkel knows that she has to show solidarity in supporting weaker and less fortunate European countries. This means that she will not call for a completely new European monetary policy or the dismissal of certain states from the Eurozone. But she must find a better and more convincing way of explaining why there is no alternative. As a result this might lead to a sharper tone in future debates about Europe.

Germany - Preliminary results

France

74 MEPs

53 MEPs ran

34 MEPs re-elected

40 Newcomers

France woke up this morning in shock as the far-right Front National became the leading political force, capturing 25% of total votes and 24 MEPs, vs. 6.34% and 3 MEPs in 2009.

The conservative UMP was too divided about Europe to come first, with 20.8% (a 7 point decline since 2009), the Socialist Party hit a record low (14%, less than an already low 16.5% in 2009) in spite of a bad performance by the Greens (8.9% vs.16.3%), and the pro-European centre lost momentum when Jean-Louis Borloo was forced to retire from politics (9.9%). The far-left Front de Gauche reached 6.3% (6.1% in 2009). Turnout was higher than 5 years ago (43.5% vs. 40.7%): clearly many of François Hollande’s 2012 voters stayed at home, not the discontent.

Though no one believes this result can be a good indicator for future national elections, it is a striking signal of rejection by the voters of both the European construction as it functions today and the French Socialist President and Government. The first one to pay the price will probably be President Hollande and not his PM Manuel Valls, too new on the job to bear the responsibility of this defeat. The second one is the country, again weakened in the EU. The third one is Europe, assuming a strong and balanced German-French partnership is necessary to its development.

It is likely that this vote will mean France will have to take a stronger stance against free-trade, immigration issues, austerity-only policies and economic integration: lately the TTIP, Schengen and the euro were the major issues in the campaign and fuelled French fears.

Should the EPP retain the majority in the EP, it will be difficult for President Hollande to reject Jean-Claude Juncker as the next Commission president. Among potential French Commissioners, former Economy and Finance Minister Pierre Moscovici has a lead vs. Elisabeth Guigou, Chair of the National Assembly’s Foreign Affairs Committee. The name of Pervenche Bérès, respected French MEP and close to F.A Minister Laurent Fabius has recently been mentioned as an alternative.

France - Preliminary results

35.3%

27.3%

10.7% 7.4% 7.0%

3.4%

8.9%

0.0%

10.0%

20.0%

30.0%

40.0%20.8%

14.0%

8.9% 9.9% 6.3%

25.0%

14.6%

0.0%

10.0%

20.0%

30.0%

United Kingdom

73 MEPs

In the United Kingdom, the European election campaign has been essentially inward looking, with little or no focus on the question of Europe, and a disproportionate amount of coverage of the rise of UKIP and the major political parties’ increasingly desperate efforts to counter their surge.

This bitter debate has been typified by an ongoing polemic on whether UKIP is a ‘racist’ party, which their leader Nigel Farage has robustly rejected in a series of high profile media interviews.

The results of this acrimonious campaign suggest that these efforts have been in vain, with UKIP now the largest party in the British caucus, having achieved a record 27.5% share of the vote – ahead of the Labour Party on 25.4% and the Conservatives on 23.9%. Though perhaps not the slam-dunk result for the eurosceptic party that some predicted, they are declaring it as a major victory, and Mr Farage has stated that the “UKIP fox is in the Westminster hen house”.

This result can only make life more difficult for British business. Looking back 15 years, the British caucus, while divided along party lines, was cohesive and influential with several key committees in the European Parliament chaired by UK MEPs. Following the Conservative party’s exit from the largest EPP party block in 2009 and with UKIP ideologically opposed to any kind of constructive engagement, these key roles will now largely be filled by MEPs from other countries. This begs the question, who will help British business engage in the policy debate and input into the formation of legislation?

Whether the strong UKIP performance will carry through into the General Election in May 2015 is hotly debated. Traditionally however, parties which have benefitted from a protest vote at mid-term elections have not experienced the same success in national elections, partly as a result of the ‘First Past the Post’ electoral system and partly as traditional supporters turn back toward the more familiar parties.

UK - Preliminary results

Italy

73 MEPs

While eurosceptic forces also gained support in Italy, the first national election ever faced by the 39-year-old new Prime Minister Matteo Renzi turned out as a triumph for the 80-day-old Italian Government.

According to the almost final results (ballots in Italy closed at 11pm), the Democratic Party (PD) - led by the unelected Prime Minister - gained almost 41% of the votes, the best results ever.

The anti-establishment movement led by the former comedian Beppe Grillo, which stunned Europe by winning 25% of the vote in last year's general election, came in second place with only about 21% - or half of the votes of the Democratic Party.

More than being a vote about Europe, yesterday’s elections in Italy were also a test of Renzi’s political legitimacy and his ability to meet the challenge posed by Grillo's proven appeal to an angry electorate disillusioned by recession, unemployment and rampant political corruption.

With Italy facing the risk of a return to recession after its economy contracted in the first quarter, these unexpected results will probably translate into more support for the ambitious economic and constitutional reforms the premier has promised, but so far has only partially delivered.

Forza Italia, led by the former Prime Minister Silvio Berlusconi - weakened by party infighting and forced to serve a community service order for tax fraud that requires him to spend four hours a week at a home for Alzheimer's patients - only got around 16 per cent of the votes. It is now unclear if Berlusconi will keep supporting the efforts of the government to change the ineffective Italian electoral laws. But yesterday's vote showed very strong popular support for Mr Renzi’s ambitious program of tax cuts, labour reforms and sweeping changes to the system of government on the eve of the Italian Presidency of the EU starting on 1st of July.

Italy - Preliminary results

23.9% 25.4% 27.5%

6.9% 7.9%

2.4% 6.0%

0.0%

10.0%

20.0%

30.0%40.9%

21.1% 16.7%

6.2% 4.4% 4.0% 6.7%

0.0%

10.0%

20.0%

30.0%

40.0%

Austria

18 MEPs

13 MEPs ran

10 MEPs re-elected

8 Newcomers

Despite a loss of votes, EU parliament Vice-President Othmar Karas has led his personality election under the banner “O.K.” to a successful conclusion for him and the Austrian People’s Party and managed to maintain the first position (27.4%).

The Austrian Social Democratic Party with its independent top candidate could only increase its vote marginally and clearly stays in second place (23.8%). The right-wing National Freedom Party (19.5%) and the Green Party (15.1%) posted increases, the new liberals Neos (7.9%) immediately succeeded in getting into the EU parliament. The turnout was 45.7%.

The results come as a relief for the governing grand coalition of Chancellor Werner Faymann (Social Democrats) and Vice Chancellor Michael Spindelegger (Christian Democrats). Especially for Spindelegger another electoral defeat would have spelled problems, as his position as leader of his party has been questioned in the past.

The Freedom party, Austria’s biggest opposition party and one of the potential national delegations for a new far right group, are the evening’s big winners, doubling their number of MEPs from two to four. This has not so much to do with discontent over the ruling parties, but more with the fact that Hans-Peter Martin, who won more than 17% of votes in 2009, and tried to make a name for himself as a crusader for transparency and against lobbyists in the old Parliament, did not stand for re-election.

Two smaller opposition parties, the Greens and the newly formed liberal party NEOS, also put in strong results. The Greens managed to secure their third mandate, and NEOS, who last year entered Austria’s Nationalrat for the first time, gained 7.9% and will send one MEP to the Liberal ALDE group.

A number of smaller, mostly anti-European and far right parties did not manage to pass the threshold for election.

Austria - Preliminary results

Sweden

20 MEPs

14 MEPs ran

12 MEPs re-elected

8 Newcomers

In Sweden, voter turnout exceeded that of 2009, increasing from 45.5 % to 48.5 %. This is partly explained by the upcoming Swedish parliamentary election in September, which raised the general ‘political temperature’ and makes the campaign for the European elections a lead-in for the national one.

The result of the election is a setback for the largest party in the centre-right government, the Moderate Party (Moderaterna). The party of Prime Minister Reinfeldt failed to improve on its meagre result in the last European election and lost one seat. One of its coalition partners - the Liberal People’s Party (Folkpartiet Liberalerna) – saw a decrease in support compared to its strong performance in 2009, causing it to lose one of its three seats. The other members of the Government coalition, the Centre Party (Centerpartiet) and Christian Democrats (Kristdemokraterna), both performed in line with expectations and retained their respective mandate.

The centre-left Social Democrats (Socialdemokraterna) remain the biggest national delegation with six seats. This bodes well for the opposition in the upcoming national elections due to the strong performance of the Greens (Miljöpartiet de gröna) – who came in second and grabbed one additional seat. This was also the first election for the leader of the opposition, Stefan Löfven, since he took over the Social Democratic Party. The strong showing of his party will strengthen his position ahead of the general elections in autumn.

The election also saw the entrance of two new parties. The far-right populist Swedish Democrats (Sverigedemokratena) captured two mandates, and the Feminist Initiative (Feministiskt initiativ) one. It remains to be seen which political group these newcomers will join. The Swedish Democrats have expressed a will to join the Eurosceptic Europe of freedom and democracy (EFD) group, but it might not be welcomed there by the UK Independence Party, which does not want to be associated with the Swedish Democrats. Another option for the Swedish Democrats would be to join the potential new far right group that is likely to form as a result of the elections.

Sweden - Preliminary results

27.3% 24.2%

20.5%

13.9%

7.6% 6.5%

0.0%

10.0%

20.0%

30.0%

13.6% 10.0%

6.5% 6.0%

24.4%

6.3%

15.3%

9.7%

5.3% 2.9%

0.0%

10.0%

20.0%