Embed Size (px)

DESCRIPTION

An introductory ebook on IFRS covering the following topics: What if IFRS? Why do we need it? What's in it for us? Comparison between IFRS and GAAP How can you prepare IFRS compliant Balance Sheets

Citation preview

Prepare Balance Sheets and Profit & Loss A/C in IFRSformat

IFRS refers to International

Financial Reporting Standards which are applied while preparing the Balance Sheet and other Profitability Statements of a Company and are developed by IASB. These have already been applied in more than 100 countries and would soon be used across the globe.

It defines how particular types of transactions and other events should be reported in financial statements globally in a single format.

What is IFRS?

Reference: www.charteredclub.com

Why do you need it?Different countries employ different Accounting Standards while preparing balance sheets and computing profits of a company. Computation of profits in different currencies always yield different figures. IFRS format offers globally uniform standards of accounting so as to arrive at uniform profits across the globe. Adoption of

IFRS will reduce the costs involved in comparing investments thus increasing the quality of information. Your company will also be benefitted as a clear accounting structure would mean more investors willing to provide financing.

Reference: www.charteredclub.com

What’s in it for you?A consistent financial reporting basis would allow a multinational company to apply common accounting standards with its subsidiaries worldwide, which would improve internal communications, quality of reporting and group decision-making.

By adopting IFRS, you would be adopting a "global financial reporting" basis that will enable your company to be understood in a global marketplace. This helps in accessing world capital markets and promoting new business. It allows your company to be perceived as an international player.

In increasingly competitive markets, IFRS allows a company to benchmark itself against its peers throughout the world, and allows investors and others to compare the company's performance with competitors globally.

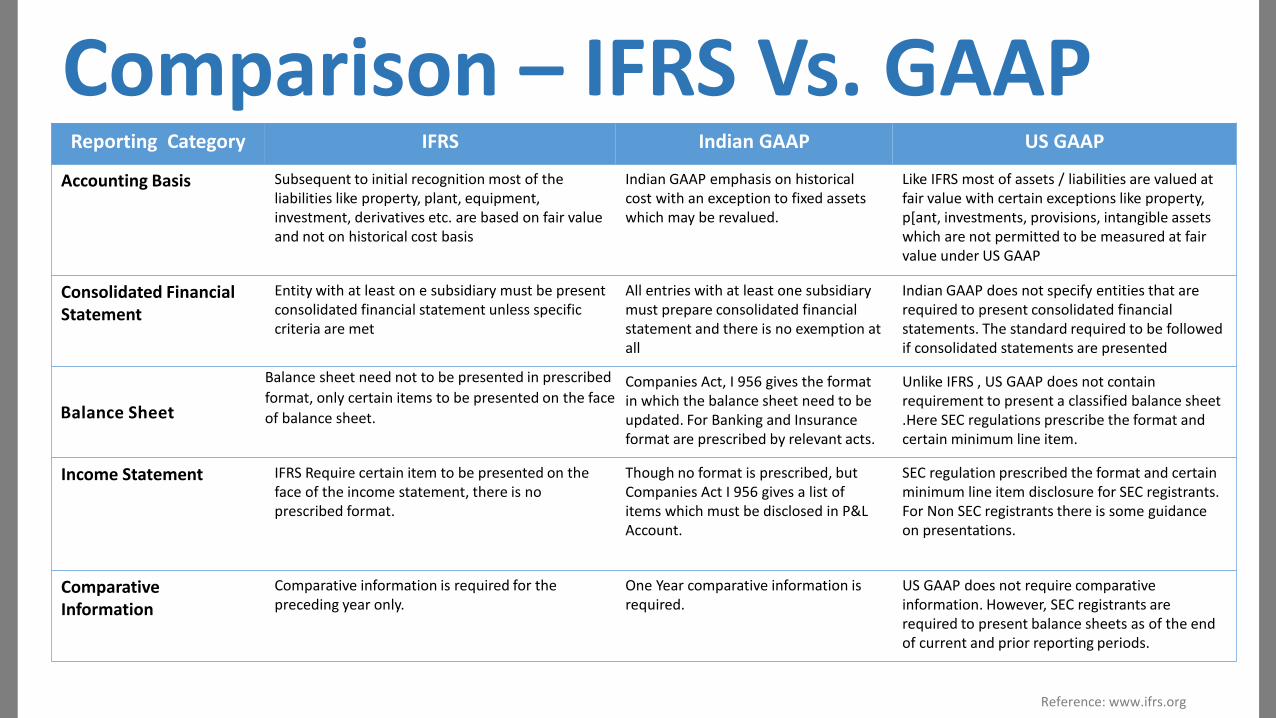

Reporting Category IFRS Indian GAAP US GAAP

Accounting Basis Subsequent to initial recognition most of the liabilities like property, plant, equipment, investment, derivatives etc. are based on fair value and not on historical cost basis

Indian GAAP emphasis on historical cost with an exception to fixed assets which may be revalued.

Like IFRS most of assets / liabilities are valued at fair value with certain exceptions like property, p[ant, investments, provisions, intangible assets which are not permitted to be measured at fair value under US GAAP

Consolidated Financial Statement

Entity with at least on e subsidiary must be present consolidated financial statement unless specific criteria are met

All entries with at least one subsidiary must prepare consolidated financial statement and there is no exemption at all

Indian GAAP does not specify entities that are required to present consolidated financial statements. The standard required to be followed if consolidated statements are presented

Balance Sheet

Balance sheet need not to be presented in prescribed

format, only certain items to be presented on the face

of balance sheet.

Companies Act, I 956 gives the format in which the balance sheet need to be updated. For Banking and Insurance format are prescribed by relevant acts.

Unlike IFRS , US GAAP does not contain requirement to present a classified balance sheet .Here SEC regulations prescribe the format and certain minimum line item.

Income Statement IFRS Require certain item to be presented on the face of the income statement, there is no prescribed format.

Though no format is prescribed, but Companies Act I 956 gives a list of items which must be disclosed in P&L Account.

SEC regulation prescribed the format and certain minimum line item disclosure for SEC registrants.For Non SEC registrants there is some guidance on presentations.

Comparative Information

Comparative information is required for the preceding year only.

One Year comparative information is required.

US GAAP does not require comparative information. However, SEC registrants are required to present balance sheets as of the end of current and prior reporting periods.

Comparison – IFRS Vs. GAAP

Reference: www.ifrs.org

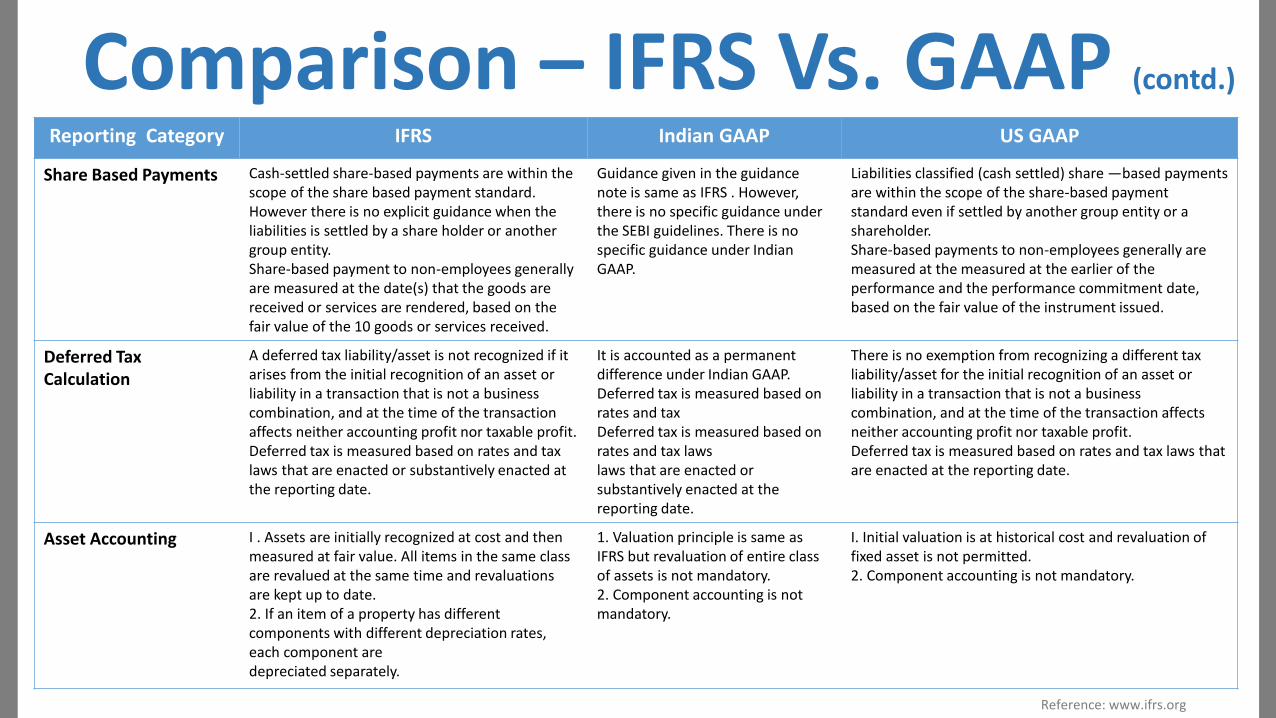

Reporting Category IFRS Indian GAAP US GAAP

Minority Interest Minority interests are classified as equity in balance Minority Interest sheet but are presented separately from shareholders equity.

Disclosed separately from liability and equity of the parent shareholders.

It's presented as long term liability or under equity in Balance Sheet.

Cash Flow Statement An entity having a subsidiary must present CFS unless specific criteria are met.Separate Financial statements of parent that represent CFS are not required

There is no mandatory requirement under Companies Act. I 956 for an entity to present CFS. Accounting Standard also Do not mandate.

There is no exemption from preparing CFS for parent entity. An entity must prepare CFS when it had at least one subsidiary at any time during current reporting period.

Revenue Recognition I .Revenue recognition is based on one single standard which contains general principles that are applied to different types of transactions.2. In a sale of good transaction, revenue is recognized when the seller transfers the significant risk and rewards of ownership to the buyer.

1. Revenue recognition is based on one single standard which contains general principles that are applied to different types of transactions. 2. In a sale of good transaction, Indian GAAP recognizes revenue when the seller transfers the property in goods to the buyer. There are some subtle differences in application.

1. Extensive guidance on revenue recognition specific to industry and transactions are available.2. Same as IFRS, however detailed criteria underlying these principles are different in U.S GAAP.

True and Fair Presentation The overriding requirement of IFRS is for financialstatements to give a fair presentation.

The Companies Act 1985 requires Financial Statement to give true and fair view of state of affairs and its P& L Account. The Act also requires compliance with Accounting Standards

The objective of U.S GAAP is fair presentation in accordance with U.S GAAP, which is more restrictive than the requirement under IFRS.

Foreign Currency Measures assets, liabilities, expenses and incomes at functional currency. Functional currency is different from local currency and it is the currency of the primary economic environment in which the entity operates.

No concept of functional currency and entities has to report their financial statements in Indian rupees.

Same as IFRS

Comparison – IFRS Vs. GAAP (contd.)

Reference: www.ifrs.org

Reporting Category IFRS Indian GAAP US GAAP

Share Based Payments Cash-settled share-based payments are within the scope of the share based payment standard. However there is no explicit guidance when the liabilities is settled by a share holder or another group entity.Share-based payment to non-employees generally are measured at the date(s) that the goods are received or services are rendered, based on the fair value of the 10 goods or services received.

Guidance given in the guidance note is same as IFRS . However, there is no specific guidance under the SEBI guidelines. There is no specific guidance under Indian GAAP.

Liabilities classified (cash settled) share —based payments are within the scope of the share-based payment standard even if settled by another group entity or a shareholder.Share-based payments to non-employees generally aremeasured at the measured at the earlier of theperformance and the performance commitment date,based on the fair value of the instrument issued.

Deferred TaxCalculation

A deferred tax liability/asset is not recognized if it arises from the initial recognition of an asset or liability in a transaction that is not a business combination, and at the time of the transaction affects neither accounting profit nor taxable profit. Deferred tax is measured based on rates and tax laws that are enacted or substantively enacted at the reporting date.

It is accounted as a permanent difference under Indian GAAP. Deferred tax is measured based on rates and taxDeferred tax is measured based on rates and tax lawslaws that are enacted or substantively enacted at the reporting date.

There is no exemption from recognizing a different tax liability/asset for the initial recognition of an asset or liability in a transaction that is not a business combination, and at the time of the transaction affects neither accounting profit nor taxable profit.Deferred tax is measured based on rates and tax laws that are enacted at the reporting date.

Asset Accounting I . Assets are initially recognized at cost and then measured at fair value. All items in the same class are revalued at the same time and revaluations are kept up to date.2. If an item of a property has different components with different depreciation rates, each component aredepreciated separately.

1. Valuation principle is same as IFRS but revaluation of entire class of assets is not mandatory.2. Component accounting is not mandatory.

I. Initial valuation is at historical cost and revaluation of fixed asset is not permitted.2. Component accounting is not mandatory.

Comparison – IFRS Vs. GAAP (contd.)

Reference: www.ifrs.org

How can you prepare Balance sheets in IFRS format?BUSY 14 provides you the flexibility to generate balance sheet in any format including Schedule VI and IFRS. You can configure both Balance Sheet and Profit & Loss Account. There’re also pre-defined formats for IFRS compliant financial statements.

You can easily restructure your data in BUSY to meet the IFRS requirements. You can change captions of your balance sheets and even the sequence in which they occur so that it fits your requirement easily. Given below are steps depicting how can you start using this feature in BUSY 14:

Configuring IFRS in BUSY 14

Go to AdministrationFinal Results Configuration

Add a Format Click on Configure to select theformat type

Here, select the format type in which you want to configure your Balance sheet by clicking on the option available

You would need to go to the “Administration” option in BUSY 14 main window where you open a company. Then by clicking on “Final Results Configuration” select the option of adding a format. After this you should click on the option to select the format type. The next window will appear (Fig. 1), which will ask you to define the format for your balance sheet or your Profit & Loss Account. You can select the standard format which BUSY provides or you can select the IFRS format.

Fig 1

Steps to configure IFRS in BUSY 14

Once you select IFRS format, you will be presented with this screenshot (Fig 2). Here you have the option of changing any caption and making it IFRS compliant. In the second column you can choose the level of the entered caption. It can be a sub caption like L2 or even a new caption like “Liabilities and Equity”. In the next column you can define the type of value you want to assign to a particular caption and from where the value should be sourced. The value can be sourced from the following options:

Group (All A/c): All accounts under the selected group will be picked.Group (Direct): All accounts directly tagged under the selected group will be picked.Account: Any selected account will be picked.Sub total down/up: It will do a total of the head which are below or upwards in the hierarchy defined in the “Levels” column.Derived Value: Any combination of any head within the same format.Payable/Receivable: Value of Trade Receivable or Payable.Net Profit: Current year profit up to a specific date.Value: Reflection of selected value typePercentage: % of value to be derived under the “value” column.

Fig 2

You can configure the Profit & Loss account in a similar manner. All the balance sheets in BUSY 14 are fully configurable. Apart from IFRS compliant, you can prepare balance sheets in a format of your choice or standard being followed in your country.

Go to Display Final Results

Select Balance Sheet or Profit & Loss A/Cclick on Vertical (configurable)

Select the format name

You can view the report by clicking on display then selecting the final result. Select the report that you want to see. It can either be a balance sheet or a profit & loss A/C. Select the “Vertical(configurable)” option and then choose whether you want the balance sheet date wise or month wise.

Fig 3

For viewing the report

FAQsIs reconfiguration possible once the IFRS compliant balance sheet is made? Is it a static report or a dynamic report?Yes, you can reconfigure the report as many times as you want and in different formats. BUSY 14 allows you to configure and reconfigure the report in the format of your choice.

Which version of BUSY is this feature available?This feature is available in Standard and Enterprise editions of BUSY 14. To know more about different features in BUSY 14, you can log on to www.busy14.busy.in for more details.

Can we make multiple formats of final accounts?Yes, you can design any number of formats to meet your different needs.

After making the report, can we print it directly from BUSY?No, you will have to export the report in excel or pdf to get a printout.

If there exists multiple companies in BUSY, then can you transfer one balance sheet or Profit & Loss to another company?Yes, you can transfer it to another company created in BUSY.

Is the configurable report available in both horizontal and vertical format?No, the report is available only in vertical format.

Why BUSY 14?In today's dynamic business scenario, its imperative to maximize your business potential by making the most of man, machine & material. Here is an all encompassing business accounting software that enables you to achieve the above. Unveiling the all new BUSY 14 - The complete Business Accounting Software designed especially for SMEs like you. BUSY 14 goes beyond Accounting, Inventory & Taxation, and helps you take full charge of your business anytime anywhere through any device. With host of new features like Web-based Reporting, Payroll, Job Work, & Configurable Balance Sheet, BUSY 14 is here to deliver everything you wanted at a click of a button.

Web-based Reporting

Stay connected with your business

anytime anywhere through any

device. All you need to do is access

your business data using BUSY 14

secured Web-based Reporting facility

via your laptop, tablet, PC or Smart

phone. Now be in the driving seat

wherever you are and wherever your

business takes you.

Smart Payroll Management

Human capital is the greatest asset

of an organization and to keep it

ticking you need to put in place a

flawless and seamless payroll

process. Loaded with

comprehensive payroll management

capabilities, BUSY 14 is rightly

suited to simplify payroll process of

your organization.

Job Work Management

Outsourcing is the best way to cut

costs and get specialized personnel

to work on your product. But many a

times, keeping tab on outsourced

work proves to be cumbersome. With

Job Work module in BUSY 14, you

can keep track of all outsourced

work, raw material and finished

product at a click of a button.

Find out how more than 600,000 users across 25 countries are managing there business in a hassle free manner. Click here to download a FREE Trial Version and go easy in managing your business.

www.busy.in

For further queries, you can write to us : [email protected] call us @ +91-011-27372704/05