Embed Size (px)

Citation preview

Investor Presentation

TSX-V:PLU FSE:QG1 OTC:PLUUF

Disclaimer

The particulars contained herein were obtained from sources which we believe reliable but are not guaranteed by us and may be incomplete. The opinions expressed are based upon our

analysis and interpretation and are not to be construed as a solicitation or offer to buy or sell the securities mentioned herein. This presentation includes certain forward-looking statements

concerning the future performance of Plateau Uranium's business, operations and financial performance and condition, as well as management's objectives, strategies, beliefs and intentions.

Forward-looking statements are frequently identified by such words as "may", "will", "plan", "expect", "anticipate", "estimate", "intend" and similar words referring to future events and results.

Forward-looking statements are based on the current opinions and expectations of management. Forward-looking statements and forward-looking information include, but are not limited to,

statements with respect to estimated production and mine life; the future price of uranium; the estimation of mineral reserves and resources; the realization of mineral resource and reserve

estimates; the timing and amount of estimated future production; costs of production; success of exploration activities; and currency exchange rate fluctuations. Except for statements of

historical fact relating to Plateau Uranium, certain information contained herein constitutes forward-looking statements. All forward-looking information is inherently uncertain and subject to a

variety of assumptions, risks and uncertainties, including the speculative nature of mineral exploration and development, fluctuating commodity prices, competitive risks, the availability of

financing, variations in grades or recovery rates, risks relating to international operations, fluctuating currency exchange rates, changes in project parameters, the possibility of project cost

overruns or unanticipated costs and expenses, labour disputes and other risks of the mining industry, failure of plant, equipment or processes to operate as anticipated, as described in more

detail in the Company's recent securities filings available at www.sedar.com. Actual events or results may differ materially from those projected in the forward-looking statements and

Macusani cautions against placing undue reliance thereon. Neither Plateau Uranium nor its management assume any obligation to revise or update these forward-looking statements.

Qualified Persons

The scientific and technical information contained in this document relating to preliminary economic assessment was prepared by or under the supervision of, or reviewed and approved by, Mr.

Michael Short, B.E., CEng., FIMMM and Dr Thomas Apelt, PhD, CEng., MAusIMM, of GBM Minerals Engineering Consultants, and/or Mr. Mark Mounde, BEng., CEng., MIMMM of Wardell

Armstrong International, who are independent technical consultants to the Company and "Qualified Persons" under NI 43-101 Standards of Disclosure for Mineral Projects.

The scientific and technical information contained in this document relating to the Mineral Resources was prepared under the supervision of, or reviewed and approved by Mr. David Young,

B.Sc. (Hons), FGSSA, FSAIMM, FAusIMM, Pr Sci Nat (No 400989/83) of The Mineral Corporation that is an independent technical consultant to the Company and a “Qualified Person” under NI

43-101 Standards of Disclosure for Mineral Projects.

2

Investment Highlights

• Consolidated Resource in Emerging Uranium District* • 52.9 M lbs U3O8 Measured & Indicated (248 ppm)

• 72.1 M lbs U3O8 Inferred (251 ppm)

• 75 ppm U cut-off

• Robust Resource at Higher Grade Cut-Off * • 32.8 M lbs U3O8 Measured & Indicated (445 ppm)

• 45.9 M lbs U3O8 Inferred (501 ppm)

• 200 ppm U cut-off

• Robust Project Economics** • NPV: $708 M / IRR: 47.5% (pre-tax)

• Large Scale: Proposed production of 5.2M lbs U3O8 /year during the first 5 years

• Low Cost: <$21/lb estimated cash production cost

• Updated PEA using $50/lb U3O8 price expected Q1/16: Revised to incorporate the new consolidated resource

• Excellent Infrastructure - Roads, inexpensive power, water, etc.

• Mining Friendly Jurisdiction - Peru

Well-positioned for Uranium sector recovery* See Slide 21 & 22 for resource details from May 2015 news release. ** Jan 2014 Preliminary Economic Assessment – see slides 9 & 10 for details. 3

Management & Board of Directors

4

Ian StalkerChairman

Over 30 years experience in mining development and operations in Europe, Africa, and Australia. Former CEO of UraMin Inc. until its acquisition by Areva in 2007 for US$2.5 billion. Former VP Exploration of Gold Fields Ltd., the fourth largest gold producer in the world at that time.

Ted O’ConnorCEO, Director

Over 22 years of experience in the exploration industry, most recent as Director of Corporate Development at Cameco. In that role, he was responsible for evaluating, directing and exploring for uranium deposits worldwide. Mr. O’Connor has successfully led new project generation and acquisitions from early exploration through to discovery and delineation on multiple uranium projects globally. CEO & President of Azincourt Uranium for the past 24 months.

Laurence StefanPresident & COO, Director

Founder of Plateau Uranium (formerly Macusani Yellowcake), serving as Managing Director in Peru since Oct. 2007. Dr. Stefan previously worked at Gold Fields of South Africa and JCI (Pty) Ltd. with recent years spent mainly on South American projects.

Alan FerryDirector

Over 25 years of experience in the investment industry following a career as a geologist, mainly in uranium exploration. Significant experience in mining analysis, mineral economics and corporate finance. Current Lead Director of Guyana Goldfields Inc. and director of Avalon Rare Metals Inc and GPM Metals Inc

Marc Henderson Director

Over 20 years of CEO experience. Currently President & CEO of Laramide Resources Ltd. Mr. Henderson previously served as President of Aquiline Resources Inc., prior to being acquired by Pan American Silver in Jan. 2010. Mr. Henderson is a Chartered Financial Analyst, and holds an economics degree from the University of Colorado.

Richard PatricioDirector

Current VP Legal & Corporate Affairs at Pinetree Capital Ltd. Mr. Patricio is responsible for merger and acquisition activity, corporate transactions, compliance, corporate governance and the administration of Pinetree. Mr. Patricio received his law degree from Osgoode Hall and was called to the Ontario bar in 2000.

Engin ÖzberkDirector

Currently Executive Director & Senior Technical Advisor and Mitacs Industry Executive in Residence – Minerals, with the International Minerals Innovation Institute. Prior to his current role, Engin spent 16 years with Cameco Corporation, most recently as Vice President, Technology and Innovation.

Dennis HiggsDirector

Over 30 years of experience with financial and venture capital markets in the United States, Canada and Europe. Currently serves on the board of Energy Fuels Inc., an integrated uranium producer focused in the United States, following its acquisition of Uranerz, where Mr. Higgs was Executive Chairman for 9 years.

Experienced, proven and committed

Capital Structure

5

Shares 40.6 M

Warrants @ $0.80Warrants @ $0.60

4.0 M3.7 M

Options 1.7 M

Fully Diluted 50.0 M

Market Capitalization (as of 15 Jan 2016) CAD $15.6 M

TSX-V: PLU FSE:QG1

Consolidating An Emerging Uranium District

6

PlateauUranium

• Plateau Uranium controls one of the largest undeveloped uranium districts in the world

• Located on the Macusani Plateau, Puno, Southern Peru: concessions cover > 1,000 km2

• District offers exceptional exploration prospects & development potential

• Excellent infrastructure: • Access to labour, water and inexpensive

hydro-electric power• Transport (major highway runs past

properties)• Plentiful supply of sulfuric acid

• History of mining in the region• Minsur – San Rafael Tin Mine• Minera IRL – Ollachea Gold project

• Good government and local community relations

Consolidated Land Position

7

Over 1,000 km2 of claims holding all known resources in the region

• Azincourt acquisition resulted in consolidated >1,000 km2 land package

• One of the largest uranium districts in the world

• All deposits within 7.5-10 km radius

• Plateau controls all known uranium resources in Peru

• Significant exploration potential exists throughout district

7.5 km radius

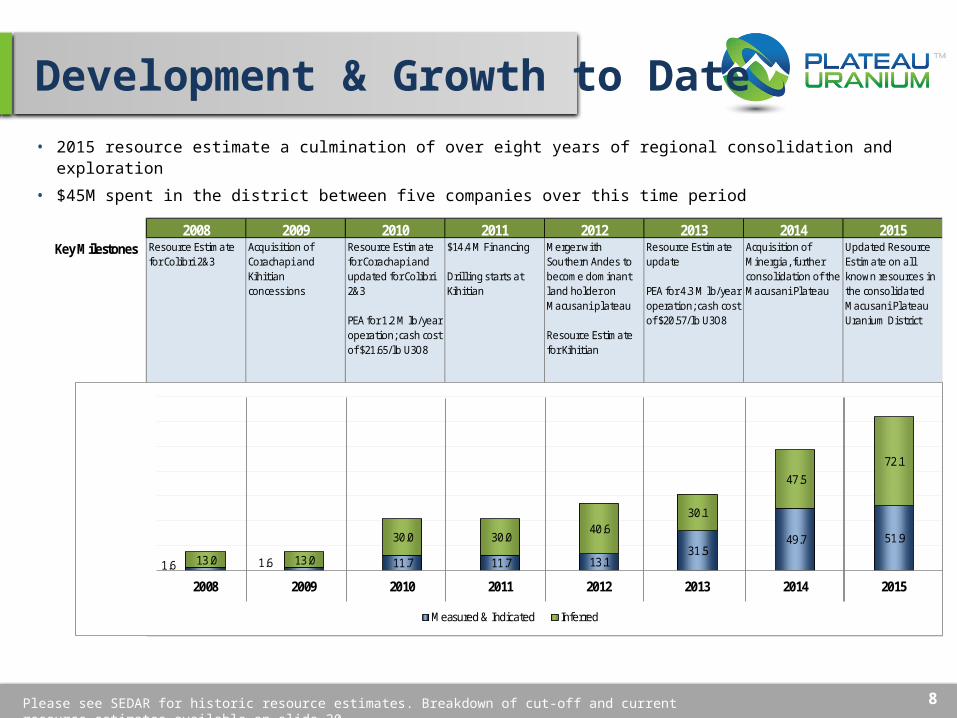

Development & Growth to Date

8

2015 resource estimate a culmination of over eight years of regional consolidation and exploration

Please see SEDAR for historic resource estimates. Breakdown of cut-off and current resource estimates available on slide 20.

2008 2009 2010 2011 2012 2013 2014 2015Key Milestones Res ource Es timate

for Col ibri 2&3Acquis ition of Corachapi and Ki hitian conces s ions

Resource Esti mate for Corachapi and updated for Col ibri 2&3

PEA for 1.2 M lb/year operation; cash cos t of $21.65/lb U3O8

$14.4 M Financing

Dri l l ing starts a t Kihitian

Merger with Southern Andes to become domi nant land holder on Macus ani pla teau

Res ource Es timate for Kihiti an

Res ource Es timate update

PEA for 4.3 M lb/year operation; cash cos t of $20.57/lb U3O8

Acquis ition of Minergia , further cons ol idati on of the Macus ani Plateau

Updated Resource Es timate on a l l known resources in the consol idated Macus ani Pla teau Uranium Distri ct

2008 2009 2010 2011 2012 2013 2014 2015

1.6 1.6 11.7 11.7 13.1 31.5

49.7 51.9

13.0 13.0

30.0 30.0 40.6

30.1

47.5 72.1

2008 2009 2010 2011 2012 2013 2014 2015

Measured & Indicated Inferred

• 2015 resource estimate a culmination of over eight years of regional consolidation and exploration

• $45M spent in the district between five companies over this time period

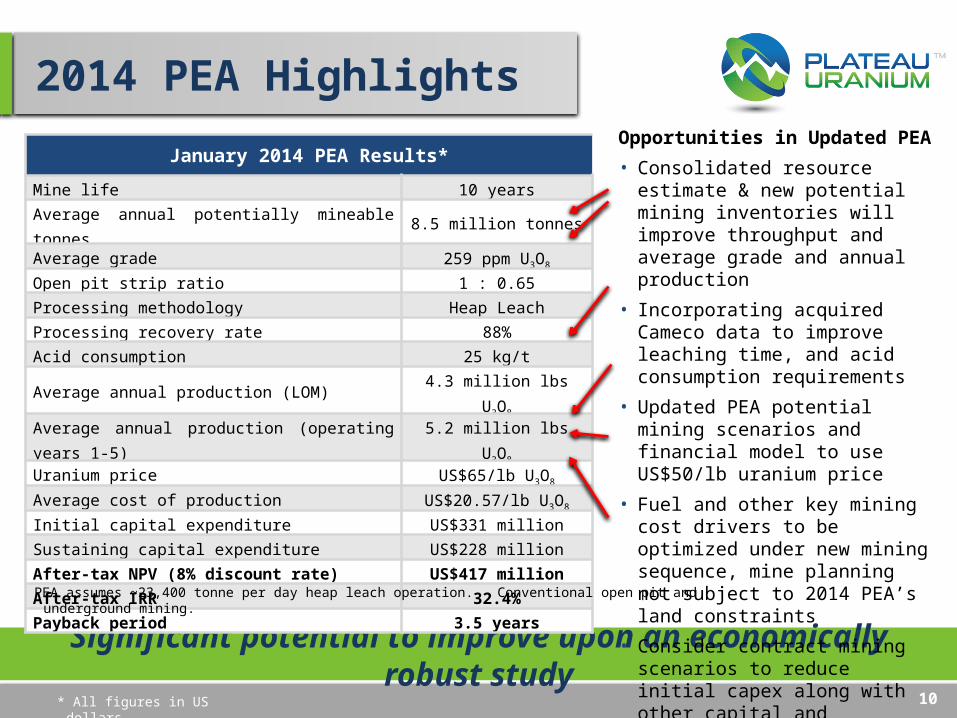

2014 PEA Highlights

• Robust financials• Low cash costs• Large-scale production• Manageable CAPEX• Resource expansion potential• Prepared by GBM Minerals Engineering Consultants,

The Mineral Corp. & Wardell Armstrong International

Paves the way for PEA update in Q3 2015 on road to PFS9

Significant potential to improve upon an economically robust study

2014 PEA Highlights

10* All figures in US dollars

January 2014 PEA Results*

Mine life 10 yearsAverage annual potentially mineable tonnes 8.5 million tonnesAverage grade 259 ppm U3O8

Open pit strip ratio 1 : 0.65Processing methodology Heap LeachProcessing recovery rate 88%Acid consumption 25 kg/tAverage annual production (LOM) 4.3 million lbs U3O8

Average annual production (operating years 1-5) 5.2 million lbs U3O8

Uranium price US$65/lb U3O8

Average cost of production US$20.57/lb U3O8

Initial capital expenditure US$331 millionSustaining capital expenditure US$228 millionAfter-tax NPV (8% discount rate) US$417 millionAfter-tax IRR 32.4%Payback period 3.5 years

PEA assumes ~23,400 tonne per day heap leach operation. Conventional open pit and underground mining.

Opportunities in Updated PEA• Consolidated resource estimate & new

potential mining inventories will improve throughput and average grade and annual production

• Incorporating acquired Cameco data to improve leaching time, and acid consumption requirements

• Updated PEA potential mining scenarios and financial model to use US$50/lb uranium price

• Fuel and other key mining cost drivers to be optimized under new mining sequence, mine planning not subject to 2014 PEA’s land constraints

• Consider contract mining scenarios to reduce initial capex along with other capital and operating improvements

• Study to be completed in Q1/2016

Low Valuation vs Developer Peers

11Source: Company Reports and Technical Reports. As of May 5th, 2015.

Attractive investment opportunity vs peers

Mkt Cap (C$M) Location Stage M&I Res.

(Mlbs)Inf Res. (Mlbs) Study Date

Ann. Prod

(Mlbs)Mine

Life (yrs)LoM Op.

Cash Cost (US$/lb)

Capital Intensity*

Fission Uranium $300M Sask. Scoping 79.6M 25.9M PEA: Sept 2015 7.2M 12 yrs $14 $152

Toro Energy $140M Australia Feasibility 61.2M 21.9M PEA: Jan 2014 1.9M 16 yrs $31 $138

Vimy Resources $75M Australia Feasibility 23.5M 49.2M PFS: Nov 2015 3.0M 16 yrs $29 $100

Berkeley $40M Spain Feasibility 33.5M 54.8M PFS: Sep 2013 2.7M 11 yrs $25 $63

Forsys Metals $30M Namibia Feasibility 115.0M 11.0M FS: Mar 2015 5.2M 15 yrs $35 $83

Deep Yellow $22M Namibia Scoping 45.0M 46.1M PEA: Jun 2014 2.5-3.5M 10-14 yrs N/A N/A

Mantra Acq. (Mar 2011) $920M Tanzania Feasibility 65.5M 41.2M PFS: Feb 2010 3.7M 12 yrs $25 $81

Extract Acq. (Dec 2011) $2,300M Namibia Feasibility 358.1M 154.9M FS: Apr 2011 12.4M 16 yrs $32 $134

Plateau $11M Peru Scoping 51.9M 72.1

MPEA: Dec

2013 4.3M 10 yrs $21 $77

*Capital Intensity calculated as Initial Capex (US$M) divided by LoM average annual U3O8 production.

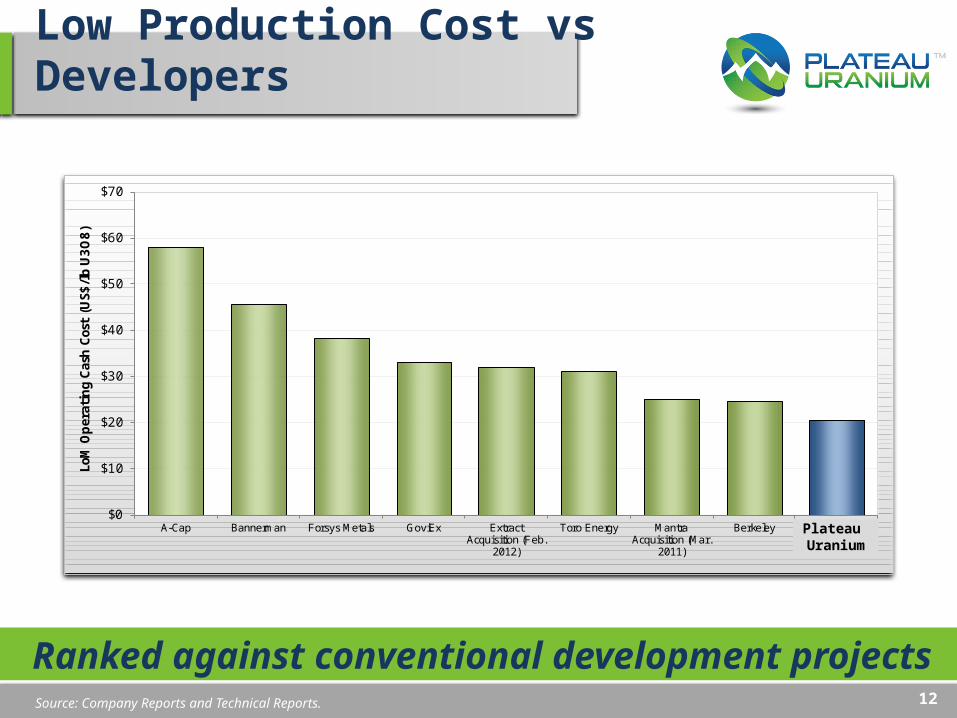

Low Production Cost vs Developers

12Source: Company Reports and Technical Reports.

$0

$10

$20

$30

$40

$50

$60

$70

A-Cap Bannerman Forsys Metals GoviEx ExtractAcquisition (Feb.

2012)

Toro Energy MantraAcquisition (Mar.

2011)

Berkeley Macusani

LoM

Oper

atin

g Ca

sh C

ost (

US$/

lb U

3O8)

Plateau Uranium

Ranked against conventional development projects

Gold Heap Leach Comparison

13Source: Company Reports and Technical Reports.

~175kozpa AuEq developer at US$505/oz cash cost*

• Strong history of heap leach gold production in Peru, including Tahoe’s (previously Rio Alto’s) La Arena gold mine and Shahuindo gold development project

• On a gold equivalent* basis, Plateau’s updated resource at 75 ppm U cut-off (0.2 g/t AuEq cut-off) is equal to:

• M&I resource of 2.1Moz AuEq at 0.69 g/t AuEq• Inferred resource of 2.9Moz AuEq at 0.70 g/t AuEq

• At the higher 200 ppm U cut-off, Plateau’s updated resource is equal to:• M&I resource of 1.3Moz AuEq at 1.24 g/t AuEq• Inferred resource of 1.9Moz AuEq at 1.40 g/t AuEq

• For comparison, Rio Alto acquired Sulliden Gold in May 2014 for approximately $300M; Sulliden’s Shahuindo development project had a resource consisting of:

• M&I resource of 2.4Moz Au at 0.52 g/t Au**• Inferred resource of 1.6Moz Au at 0.71 g/t Au**• Sulliden’s Sept 2012 Feasibility Study estimated avg. annual production of 87kozpa

AuEq at US$552/oz cash cost * AuEq calculated using current uranium term price of US$49/lb U3O8 and current gold price of $1,200/oz Au, implying and Au/U3O8 ratio of 24.5x**Resource calculated at a 0.20 g/t AuEq cut-off for oxide resources, 0.35 g/t AuEq cut-off for mixed resources, and 0.50 g/t AuEq cut-off for sulphide resources

Uranium Supply and Demand

14* World Nuclear Association

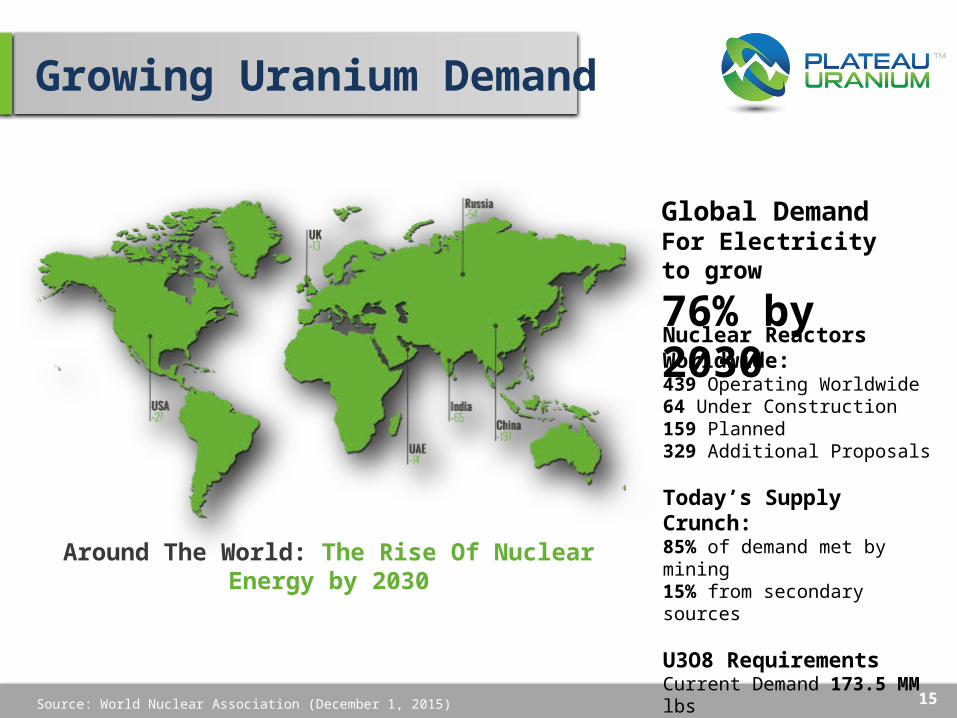

Growing Uranium Demand

15Source: World Nuclear Association (December 1, 2015)

Global Demand For Electricity to grow

76% by 2030Nuclear Reactors Worldwide:439 Operating Worldwide64 Under Construction159 Planned329 Additional Proposals

Today’s Supply Crunch:85% of demand met by mining15% from secondary sources

U3O8 RequirementsCurrent Demand 173.5 MM lbsReference Demand 270 MM lbs by 2030

Around The World: The Rise Of Nuclear Energy by 2030

U Price & Uncovered Demand

16* Source: Dundee Capital Markets, Company Reports, UxC (uxc.com)

Utilities contract 2-4 years ahead

Uranium Inducement Price

17Source: JPMorgan Research, July 28th, 2014. Plateau Uranium data based on 2013 PEA.

$0

$20

$40

$60

$80

$100

$120

$140

$160

U3O8

Pric

e Re

quire

d

INDUCEMENT PRICE FOR NEW PRODUCTION (15% IRR)Plat

eau Uranium

Ranked against Global competitor projects

Near-Term Milestones

Except for statements of historical fact relating to Plateau Uranium, certain information contained herein constitutes forward-looking statements. All forward-looking information is inherently uncertain and subject to a variety of assumptions, risks and uncertainties, including the speculative nature of mineral exploration and development, fluctuating commodity prices, competitive risks, the availability of financing, variations in grades or recovery rates, risks relating to international operations, fluctuating currency exchange rates, changes in project parameters, the possibility of project cost overruns or unanticipated costs and expenses, labour disputes and other risks of the mining industry, failure of plant, equipment or processes to operate as anticipated.

18

Q1/Q2 - 2015 2016+

• Completed resource integration & initiated revised PEA incorporating entire portfolio initiated

• Initiated prospecting & sampling on unexplored land and prioritize known un-drilled prospects

• Further metallurgical testwork planned

• Community Agreements & Environmental Permits in place

• Pre-Feasibility Study• Bankable Feasibility

Study• Project financing• Commence

construction• Production Visibility –

2018 at the earliest

• Revised PEA completion• Environmental studies• Drilling for new discovery

& to convert inferred to measured and indicated

• Advance uranium permitting discussions with government

Q3/Q4 - 2015

Budget to PFS (end of 2016):

$3-5M

Budget to Complete BFS and Permitting:

$5-8M

Permitting Environment in Peru

19

• No current uranium production in the country

• Established specific uranium exploration regulations

• Working committee formed to advance uranium production permitting regulations:

• Plateau Uranium representatives• INGEMMET (Institute of Geology, Mining & Metallurgy)• MEM (Ministry of Mines & Energy)• IPEN (Peruvian Nuclear Energy Institute)

• International Atomic Energy Agency (IAEA)• “Red Book” resource reporting• Potential scientific & regulatory assistance

Contact Information

20

Ted O’ConnorChief Executive Officer & [email protected]

OR

Laurence StefanPresident & Chief Operating [email protected]

www.plateauuranium.com

Head Office 141 Adelaide St. W., Suite 1200Toronto, Ontario M5H 3L5

NI 43-101 Compliant Resources

21

All Resources stated at 75 ppm U cutoff(1) Kihitian Complex includes the Chilcuno Chico, Quebrada Blanca, Tuturumani and Tantamaco deposits updated, May 6, 2015(2) Isivilla Complex includes the Isivilla, Calvario Real, Puncopata and Calvario I deposits, updated May 6, 2015(3) Corani Complex includes the Calvario II, Calvario III and Nueva Corani deposits, updated May 6, 2015(4) Colibri II-III and Tupuramani remain unchanged, last updated August 14, 2013(5) Corachapi remains unchanged, last updated September 8, 2010

Resources at 75 ppm cut-off

Measured & Indicated Inferred

Tonnes(Mt)

Grade(ppm U3O8)

Contained lbs(Mlbs U3O8)

Tonnes(Mt)

Grade(ppm U3O8)

Contained lbs(Mlbs U3O8)

Kihitian Complex(1) 47.7 Mt 261 ppm

(0.575 lbs/t) 27.4 Mlbs 83.6 Mt 273 ppm(0.60 lbs/t) 50.3 Mlbs

Isivilla Complex(2) 4.6 Mt 350 ppm

(0.77 lbs/t) 3.5 Mlbs 16.1 Mt 293 ppm(0.645 lbs/t) 10.4 Mlbs

Corani Complex(3) 3.4 Mt 166 ppm

(.366 lbs/t) 1.3 Mlbs 6.1 Mt 131 ppm(0.288 lbs/t) 1.8 Mlbs

Colibri 2 & 3 / Tupuramani(4) 27.9 Mt 240 ppm

(0.529 lbs/t) 14.7 Mlbs 20.4 Mt 170 ppm(0.374 lbs/t) 7.7 Mlbs

Corachapi(5) 11.6 Mt 195 ppm(0.43 lbs/t) 5.0 Mlbs 3.8 Mt 230 ppm

(0.507 lbs/t) 1.91 Mlbs

Total 95.2 Mt 248 ppm(0.546 lbs/t) 51.9 Mlbs 130.0 Mt 251 ppm

(0.553 lbs/t) 72.1 Mlbs

NI 43-101 Compliant Resources

22

All Resources stated at 200 ppm U cutoff(1) Kihitian Complex includes the Chilcuno Chico, Quebrada Blanca, Tuturumani and Tantamaco deposits updated, May 6, 2015(2) Isivilla Complex includes the Isivilla, Calvario Real, Puncopata and Calvario I deposits, updated May 6, 2015(3) Corani Complex includes the Calvario II, Calvario III and Nueva Corani deposits, updated May 6, 2015(4) Colibri II-III and Tupuramani remain unchanged, last updated August 14, 2013(5) Corachapi remains unchanged, last updated September 8, 2010

Resources at 200 ppm cut-off

Measured & Indicated Inferred

Tonnes(Mt)

Grade(ppm U3O8)

Contained lbs(Mlbs U3O8)

Tonnes(Mt)

Grade(ppm U3O8)

Contained lbs(Mlbs U3O8)

Kihitian Complex(1) 16.23 Mt 505 ppm

(1.11 lbs/t) 18.05 Mlbs 29.78 Mt 520 ppm(1.15 lbs/t) 34.1 Mlbs

Isivilla Complex(2) 2.87 Mt 465 ppp

(1.02 lbs/t) 2.94 Mlbs 7.21 Mt 500 ppm(1.10 lbs/t) 7.96 Mlbs

Corani Complex(3) 0.42 Mt 342 ppm

(0.75 lbs/t) 0.31 Mlbs 0.19 Mt 294 ppm(0.648 lbs/t) 0.12 Mlbs

Colibri 2 & 3 / Tupuramani(4) 11.0 Mt 376 ppm

(0.828 lbs/t) 9.12 Mlbs 3.29 Mt 363 ppm(0.8 lbs/t) 2.64 Mlbs

Corachapi(5) 2.94 Mt 372 ppm(0.819 lbs/t) 2.41 Mlbs 1.14 Mt 443 ppm

(0.98 lbs/t) 0.89 Mlbs

Total 33.47 Mt 445 ppm(0.98 lbs/t) 32.8 Mlbs 41.62 Mt 501 ppm

(1.10 lbs/t) 45.9 Mlbs

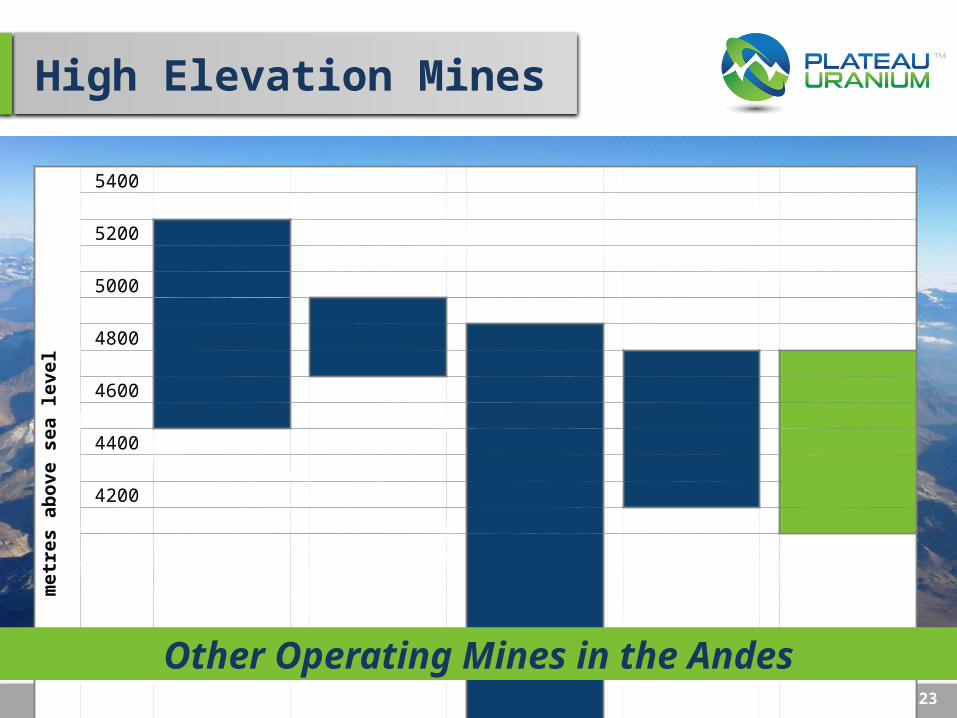

High Elevation Mines

metres

above sea level

5400

5200

5000

4800

4600

4400

4200

4000

Minsur - San Rafael Tin Mine

Chinalco - Toromocho

Copper Mine

Collahuasi - Copper Mine

Antamina - Copper / Zinc Mine

PlateauUranium

Other Operating Mines in the Andes23