Embed Size (px)

Citation preview

WEBSHOPPERS 201634TH EDITION

www.ebit.com.br www.buscapecompany.com

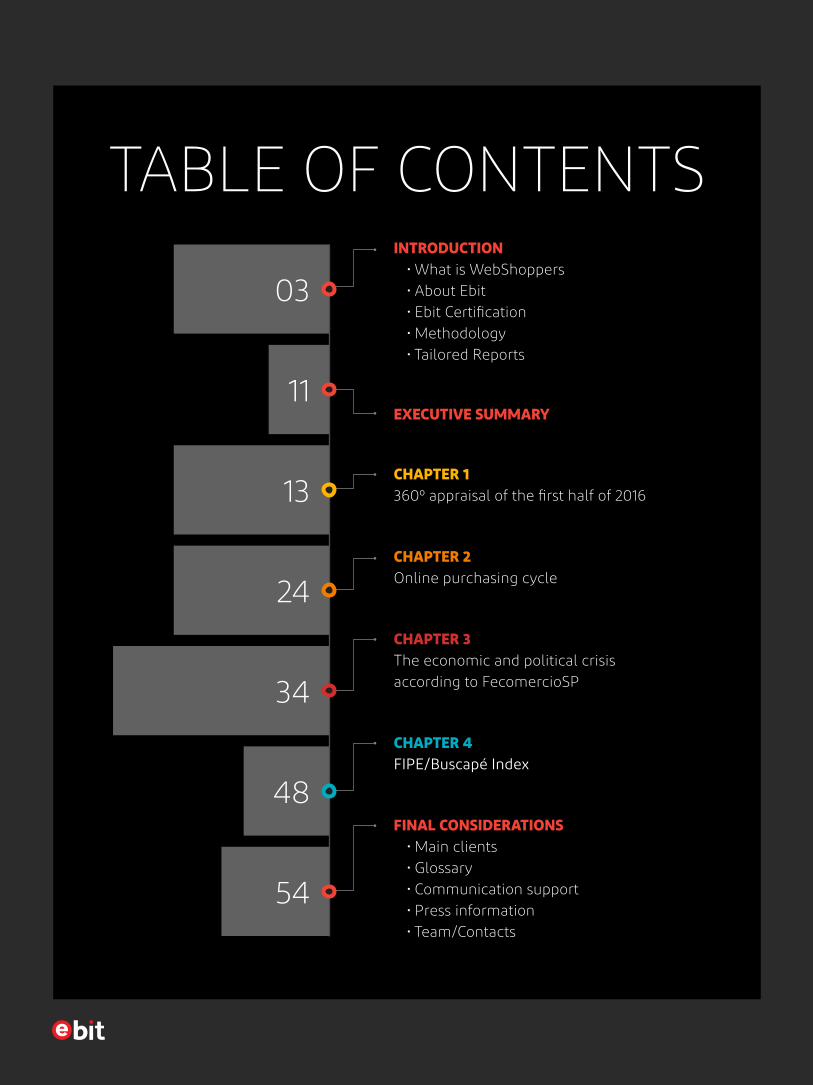

TABLE OF CONTENTSINTRODUCTION

• What is WebShoppers • About Ebit • Ebit Certification

• Methodology • Tailored Reports

EXECUTIVE SUMMARY

CHAPTER 1 360º appraisal of the first half of 2016

CHAPTER 2 Online purchasing cycle

CHAPTER 3 The economic and political crisis according to FecomercioSP

CHAPTER 4 FIPE/Buscapé Index

FINAL CONSIDERATIONS • Main clients • Glossary • Communication support

• Press information • Team/Contacts

03

24

11

34

13

48

54

INTRODUCTION

3

WHAT IS WEBSHOPPERSPerformed by Ebit since 2001, WebShoppers

is the highest credibility report on Brazilian e-commerce and it is considered the main reference for professionals in this segment.

In this study, we will show the current e-commerce market scenario,estimates for 2016, as well as changes in behavior and preferences of consumers.

Insights obtained in this research aim at outlining the online market direction and contributing to understand and develop the sector.

P resent in the Brazilian market since January 2000, Ebit has been following the evolution

of online retail in our country since its begin-ning, and it is a reference in this topic. Using a sophisticated system that collects data directly from the online buyer, Ebit generates detailed information on e-commerce.

On its website, Ebit ( www.ebit.com.br) pro-vides relevant information for purchase deci-sion-making processes, and it offers products and services to retailers. Ebit's store certifi-cation helps consumers build trust in online purchases. Through a classification by medals (Diamond, Gold, Silver, and Bronze), which cer-

tifies the quality of services provided by retail-ers, consumers find arguments that help them at the moment of decision.

For the executive, Ebit works as a source of knowledge on e-commerce in Brazil, contri- buting to the growth of business and of the sector in general. Learn more on Ebit and its main products below.

This edition of the WebShoppers report uses information deriving from the research carried out by Ebit with over 21,000 online stores already certified and with its consumer panel, as well as from ad hoc research and external information.

ABOUT EBIT

WEBSHOPPERS

TABLE OF CONTENTS

4

INTRODUCTION | WHAT IS WEBSHOPPERS / ABOUT EBIT

0976 8765 6543 0987

09 17

Pesquisa E-bit

DIAMOND BRONZESILVERGOLD

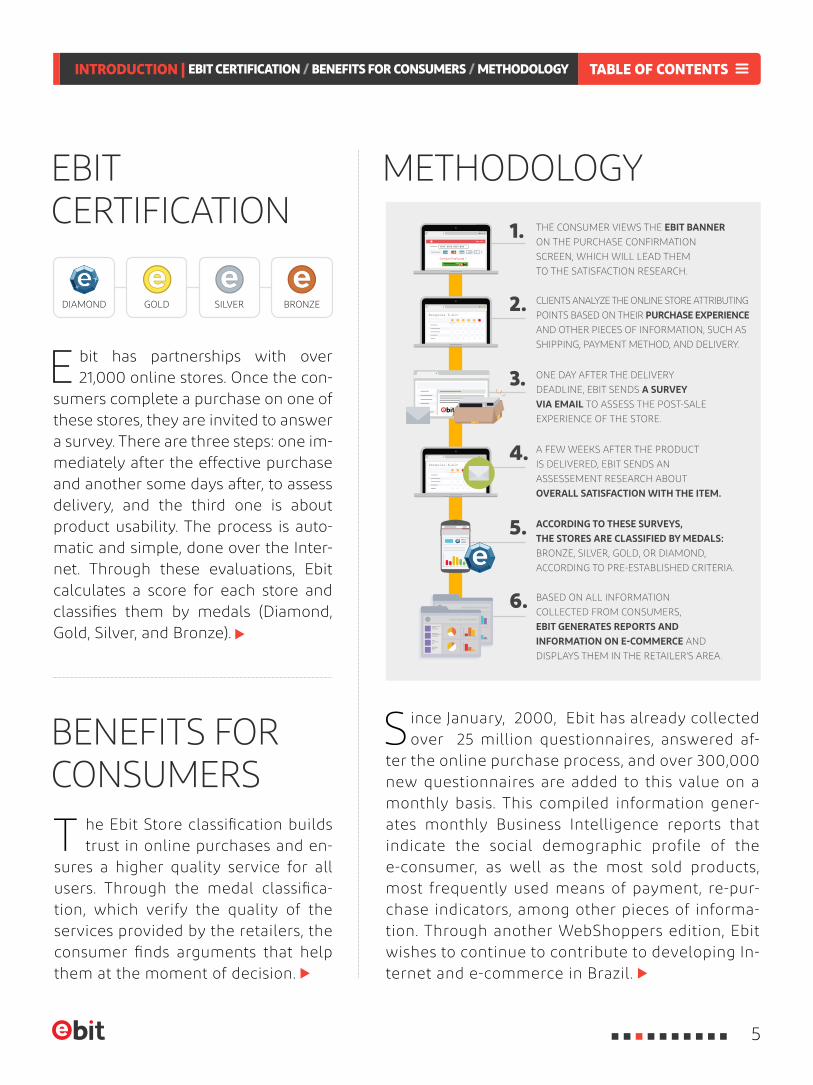

E bit has partnerships with over 21,000 online stores. Once the con-

sumers complete a purchase on one of these stores, they are invited to answer a survey. There are three steps: one im-mediately after the effective purchase and another some days after, to assess delivery, and the third one is about product usability. The process is auto-matic and simple, done over the Inter-net. Through these evaluations, Ebit calculates a score for each store and classifies them by medals (Diamond, Gold, Silver, and Bronze).

EBIT CERTIFICATION

METHODOLOGY

BENEFITS FOR CONSUMERS

S ince January, 2000, Ebit has already collected over 25 million questionnaires, answered af-

ter the online purchase process, and over 300,000 new questionnaires are added to this value on a monthly basis. This compiled information gener-ates monthly Business Intelligence reports that indicate the social demographic profile of the e-consumer, as well as the most sold products, most frequently used means of payment, re-pur-chase indicators, among other pieces of informa-tion. Through another WebShoppers edition, Ebit wishes to continue to contribute to developing In-ternet and e-commerce in Brazil.

T he Ebit Store classification builds trust in online purchases and en-

sures a higher quality service for all users. Through the medal classifica-tion, which verify the quality of the services provided by the retailers, the consumer finds arguments that help them at the moment of decision.

Pesquisa E-bit

THE CONSUMER VIEWS THE EBIT BANNER ON THE PURCHASE CONFIRMATION

SCREEN, WHICH WILL LEAD THEM

TO THE SATISFACTION RESEARCH.

ONE DAY AFTER THE DELIVERY

DEADLINE, EBIT SENDS A SURVEY VIA EMAIL TO ASSESS THE POST-SALE

EXPERIENCE OF THE STORE.

ACCORDING TO THESE SURVEYS, THE STORES ARE CLASSIFIED BY MEDALS: BRONZE, SILVER, GOLD, OR DIAMOND,

ACCORDING TO PRE-ESTABLISHED CRITERIA.

BASED ON ALL INFORMATION

COLLECTED FROM CONSUMERS, EBIT GENERATES REPORTS AND INFORMATION ON E-COMMERCE AND

DISPLAYS THEM IN THE RETAILER'S AREA.

CLIENTS ANALYZE THE ONLINE STORE ATTRIBUTING

POINTS BASED ON THEIR PURCHASE EXPERIENCE

AND OTHER PIECES OF INFORMATION, SUCH AS

SHIPPING, PAYMENT METHOD, AND DELIVERY.

A FEW WEEKS AFTER THE PRODUCT

IS DELIVERED, EBIT SENDS AN

ASSESSEMENT RESEARCH ABOUT

OVERALL SATISFACTION WITH THE ITEM.

1.

4.

2.

5.

6.

3.

TABLE OF CONTENTS

5

INTRODUCTION | EBIT CERTIFICATION / BENEFITS FOR CONSUMERS / METHODOLOGY

BI-YEARLY

MONTHLY

DAILY

6

1

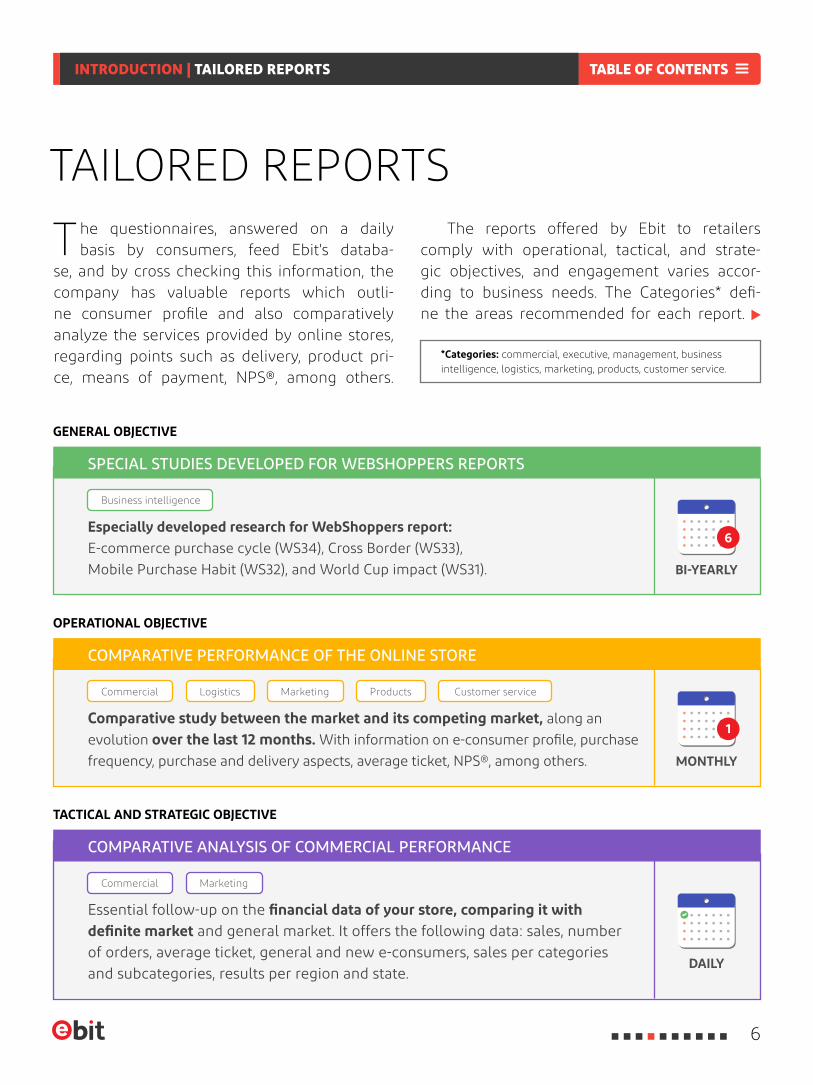

The questionnaires, answered on a daily basis by consumers, feed Ebit's databa-

se, and by cross checking this information, the company has valuable reports which outli-ne consumer profile and also comparatively analyze the services provided by online stores, regarding points such as delivery, product pri-ce, means of payment, NPS®, among others.

The reports offered by Ebit to retailers comply with operational, tactical, and strate-gic objectives, and engagement varies accor-ding to business needs. The Categories* defi-ne the areas recommended for each report.

TAILORED REPORTS

*Categories: commercial, executive, management, business intelligence, logistics, marketing, products, customer service.

SPECIAL STUDIES DEVELOPED FOR WEBSHOPPERS REPORTS

COMPARATIVE PERFORMANCE OF THE ONLINE STORE

COMPARATIVE ANALYSIS OF COMMERCIAL PERFORMANCE

Especially developed research for WebShoppers report: E-commerce purchase cycle (WS34), Cross Border (WS33),Mobile Purchase Habit (WS32), and World Cup impact (WS31).

Comparative study between the market and its competing market, along an evolution over the last 12 months. With information on e-consumer profile, purchase frequency, purchase and delivery aspects, average ticket, NPS®, among others.

Essential follow-up on the financial data of your store, comparing it with definite market and general market. It offers the following data: sales, number of orders, average ticket, general and new e-consumers, sales per categories and subcategories, results per region and state.

GENERAL OBJECTIVE

OPERATIONAL OBJECTIVE

TACTICAL AND STRATEGIC OBJECTIVE

Business intelligence

Commercial

Commercial

Logistics Marketing

Marketing

Products Customer service

TABLE OF CONTENTS

6

INTRODUCTION | TAILORED REPORTS

PRODUCTS THAT GENERATED MORE VISITS TO THE STORES PRESENT ON BUSCAPÉ

DAILY

MONTHLY

REAL TIME

WEEKLY

MONTHLY

1

1

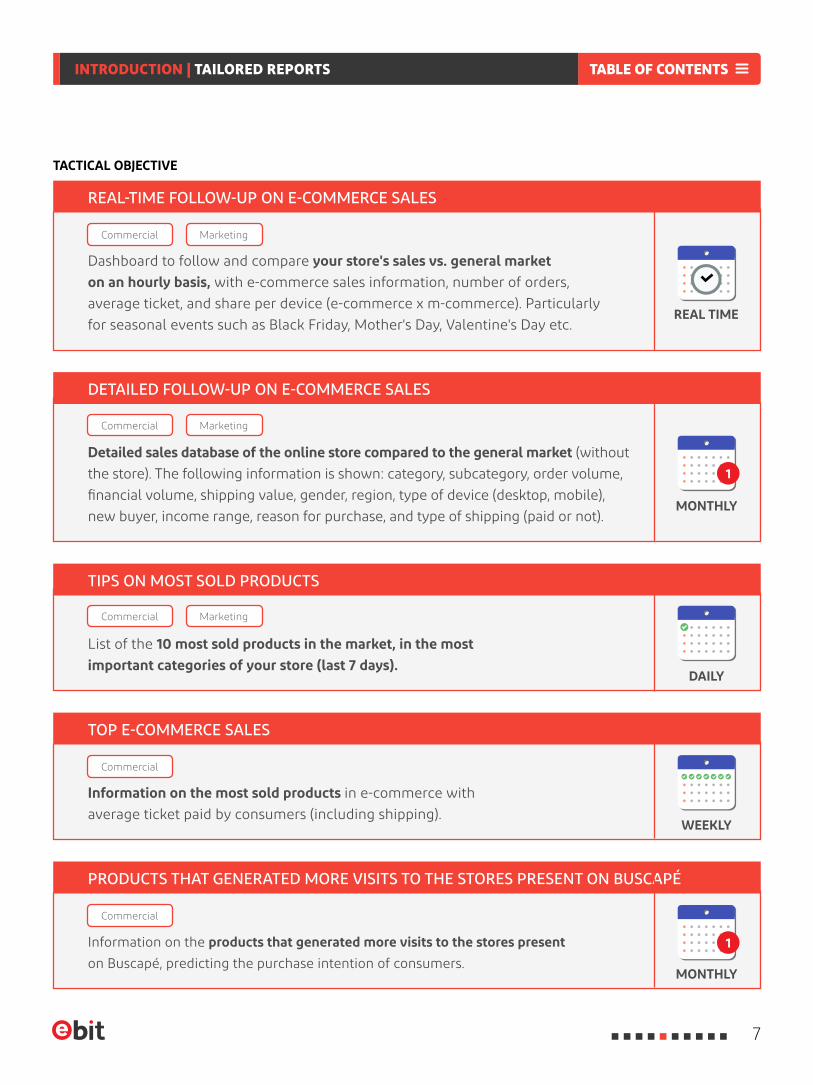

REAL-TIME FOLLOW-UP ON E-COMMERCE SALES

DETAILED FOLLOW-UP ON E-COMMERCE SALES

TIPS ON MOST SOLD PRODUCTS

TOP E-COMMERCE SALES

Dashboard to follow and compare your store's sales vs. general market on an hourly basis, with e-commerce sales information, number of orders, average ticket, and share per device (e-commerce x m-commerce). Particularly for seasonal events such as Black Friday, Mother's Day, Valentine's Day etc.

Detailed sales database of the online store compared to the general market (without the store). The following information is shown: category, subcategory, order volume, financial volume, shipping value, gender, region, type of device (desktop, mobile), new buyer, income range, reason for purchase, and type of shipping (paid or not).

List of the 10 most sold products in the market, in the most important categories of your store (last 7 days).

Information on the most sold products in e-commerce with average ticket paid by consumers (including shipping).

Information on the products that generated more visits to the stores present on Buscapé, predicting the purchase intention of consumers.

TACTICAL OBJECTIVE

Commercial

Commercial

Commercial

Commercial

Commercial

Marketing

Marketing

Marketing

TABLE OF CONTENTS

7

INTRODUCTION | TAILORED REPORTS

REAL TIME

DAILY

DAILY

DAILY

WEEKLY

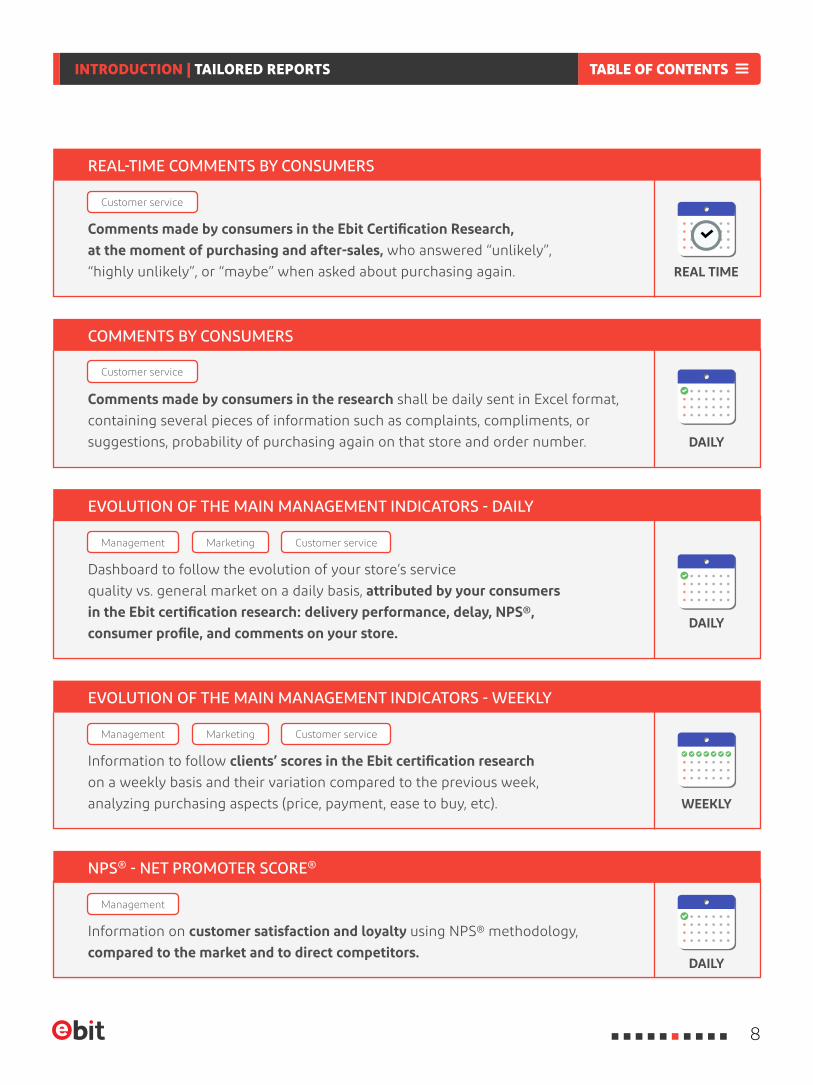

REAL-TIME COMMENTS BY CONSUMERS

COMMENTS BY CONSUMERS

EVOLUTION OF THE MAIN MANAGEMENT INDICATORS - DAILY

Comments made by consumers in the Ebit Certification Research, at the moment of purchasing and after-sales, who answered “unlikely”, “highly unlikely”, or “maybe” when asked about purchasing again.

Comments made by consumers in the research shall be daily sent in Excel format, containing several pieces of information such as complaints, compliments, or suggestions, probability of purchasing again on that store and order number.

Dashboard to follow the evolution of your store’s service quality vs. general market on a daily basis, attributed by your consumers in the Ebit certification research: delivery performance, delay, NPS®, consumer profile, and comments on your store.

Customer service

Customer service

Management

Management

Management

Customer service

Customer service

Marketing

Marketing

NPS® - NET PROMOTER SCORE®

Information on customer satisfaction and loyalty using NPS® methodology, compared to the market and to direct competitors.

EVOLUTION OF THE MAIN MANAGEMENT INDICATORS - WEEKLY

Information to follow clients’ scores in the Ebit certification research on a weekly basis and their variation compared to the previous week, analyzing purchasing aspects (price, payment, ease to buy, etc).

TABLE OF CONTENTS

8

INTRODUCTION | TAILORED REPORTS

DAILY

MONTHLY

1

MONTHLY

1

QUARTERLY

3

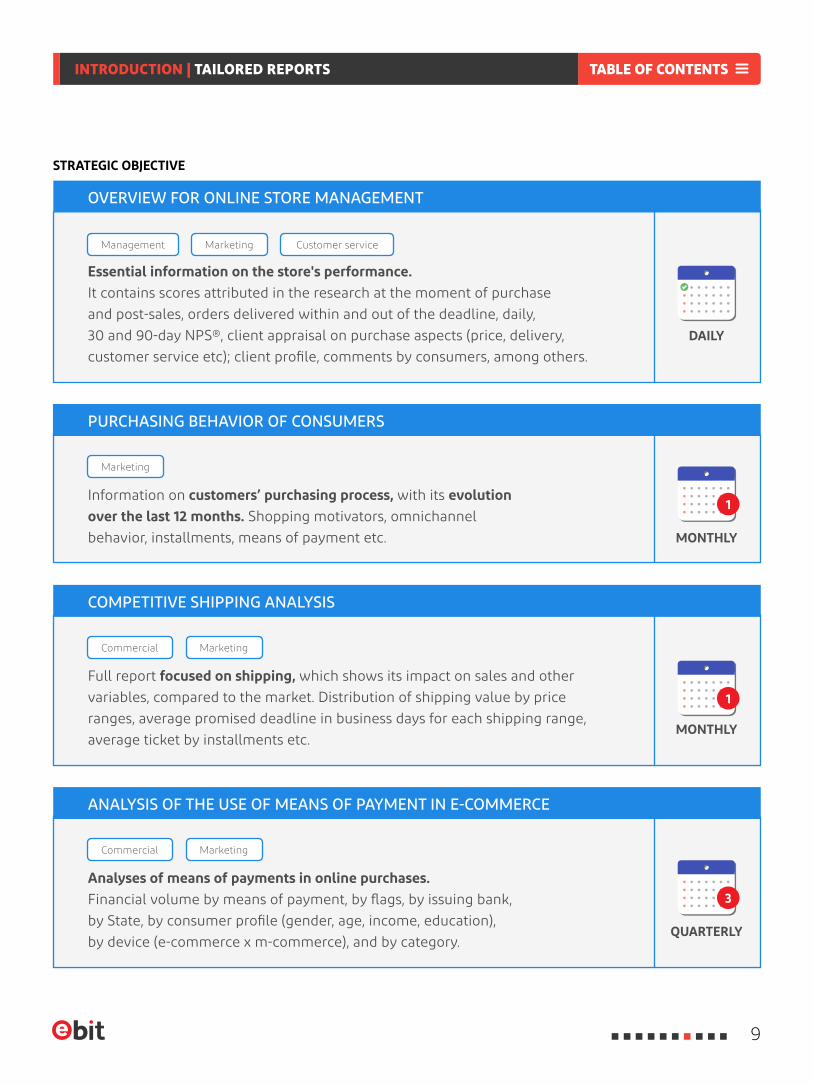

OVERVIEW FOR ONLINE STORE MANAGEMENT

COMPETITIVE SHIPPING ANALYSIS

ANALYSIS OF THE USE OF MEANS OF PAYMENT IN E-COMMERCE

PURCHASING BEHAVIOR OF CONSUMERS

Essential information on the store's performance.It contains scores attributed in the research at the moment of purchase and post-sales, orders delivered within and out of the deadline, daily, 30 and 90-day NPS®, client appraisal on purchase aspects (price, delivery, customer service etc); client profile, comments by consumers, among others.

Full report focused on shipping, which shows its impact on sales and other variables, compared to the market. Distribution of shipping value by price ranges, average promised deadline in business days for each shipping range, average ticket by installments etc.

Analyses of means of payments in online purchases.Financial volume by means of payment, by flags, by issuing bank, by State, by consumer profile (gender, age, income, education),by device (e-commerce x m-commerce), and by category.

Information on customers’ purchasing process, with its evolution over the last 12 months. Shopping motivators, omnichannel behavior, installments, means of payment etc.

STRATEGIC OBJECTIVE

Management Customer serviceMarketing

Marketing

Commercial

Commercial

Marketing

Marketing

TABLE OF CONTENTS

9

INTRODUCTION | TAILORED REPORTS

MONTHLY

MONTHLY

1

1

TAILORED REPORTS

Is any data or information which you need and not listed here?We can tailor it for you.

Contact [email protected]

and let's talk about it!

EXECUTIVE PRESENTATION BY EBIT SPECIALISTS

Executive presentation by Ebit e-commerce specialistswith a detailed analysis of the online store's comparative performance report x competing market, together with market insightsin the period and specific recommendations.

RELATIONSHIP WITH THE FINANCIAL MARKET

• Presence of Ebit e-commerce specialists at meetings, lectures, and events held by your company• Invite your clients, partners, and investors to pre-launching events of WebShoppers reports at Ebit• Monthly access to the most important financial and metric e-commerce information• Anticipated access to forecast of growth estimates (2 years) – December.

Commercial

Executives

Marketing

TABLE OF CONTENTS

10

INTRODUCTION | TAILORED REPORTS

T the current economic and political moment in Bra-

zil has posed several obsta-cles to the growth trajectory observed over the last years, with clear impacts on the pro-ductive activity and on em-ployment levels throughout national territory. After the adoption of a comprehensive tax policy between 2009 and 2014, Brazilian public deficit

EXECUTIVE SUMMARYges in the Government. The last two months of the first half of 2016 signaled a react- ion regarding sales recovery, which caused e-commerce market to reach a nominal growth of 5.2% in the period, with R$ 19.6 billion in sales.

The main e-commerce high-lights of the first half of the year are outlined on the next page.

increased substantially, espe-cially in 2015, thus generating several obstacles and a lack of optimism by retail consumers in the country.

Following this unfavorable scenario, Brazilian e-commer- ce did not show any growth in the first months of the year, when it started to show some reaction after a few chan-

TABLE OF CONTENTS

11

INTRODUCTION | EXECUTIVE SUMMARY

MAJOR HIGHLIGHTS OF BRAZILIAN E-COMMERCE IN THE FIRST HALF OF 2016

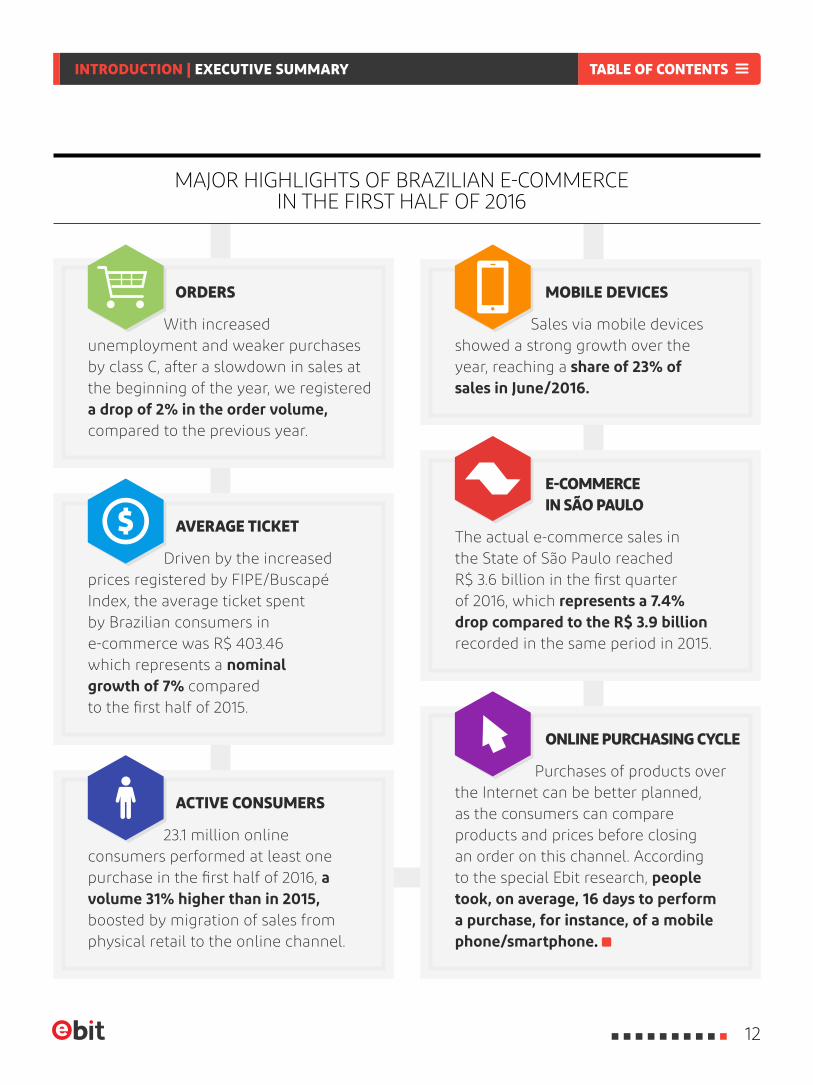

Driven by the increased prices registered by FIPE/Buscapé Index, the average ticket spent by Brazilian consumers in e-commerce was R$ 403.46 which represents a nominal growth of 7% compared to the first half of 2015.

23.1 million online consumers performed at least one purchase in the first half of 2016, a volume 31% higher than in 2015, boosted by migration of sales from physical retail to the online channel.

ORDERS

AVERAGE TICKET

ACTIVE CONSUMERS

With increased unemployment and weaker purchases by class C, after a slowdown in sales at the beginning of the year, we registered a drop of 2% in the order volume, compared to the previous year.

The actual e-commerce sales in the State of São Paulo reached R$ 3.6 billion in the first quarter of 2016, which represents a 7.4% drop compared to the R$ 3.9 billion recorded in the same period in 2015.

Sales via mobile devices showed a strong growth over the year, reaching a share of 23% of sales in June/2016.

E-COMMERCE IN SÃO PAULO

MOBILE DEVICES

ONLINE PURCHASING CYCLE

Purchases of products over the Internet can be better planned, as the consumers can compare products and prices before closing an order on this channel. According to the special Ebit research, people took, on average, 16 days to perform a purchase, for instance, of a mobile phone/smartphone.

TABLE OF CONTENTS

12

INTRODUCTION | EXECUTIVE SUMMARY

CHAPTER 1

13

360º APPRAISAL OF THE FIRST

HALF OF 2016

360º APPRAISAL OF THE FIRST HALF OF 2016

I n addition to the challenges of the macro-economic moment of the country, online re-tail was affected in the first half of 2016 by

increased product prices, as registered by the FIPE/Buscapé Index (chapter IV), changes in the ICMS billing model, and also by the downfall if

AMIDST A TROUBLED POLITICAL AND ECONOMIC MOMENT IN BRAZIL, E-COMMERCE IN THE FIRST HALF OF THE YEAR WAS MARKED BY THE FACT THAT

MANY COMPANIES IN THE SECTOR HAD TO RETHINK THEIR STRATEGIES AND REVIEW THEIR EXPENSES IN SEARCH FOR SURVIVAL AND GROWTH

the “Good Law”, which ensured a zero PIS/Cofins aliquot for computing and telecom products (In summary increasing taxes).

In this scenario, the solution for companies in the sector was to improve online consumer

TABLE OF CONTENTSCHAPTER 1 | 360º APPRAISAL OF THE FIRST HALF OF 2016

14

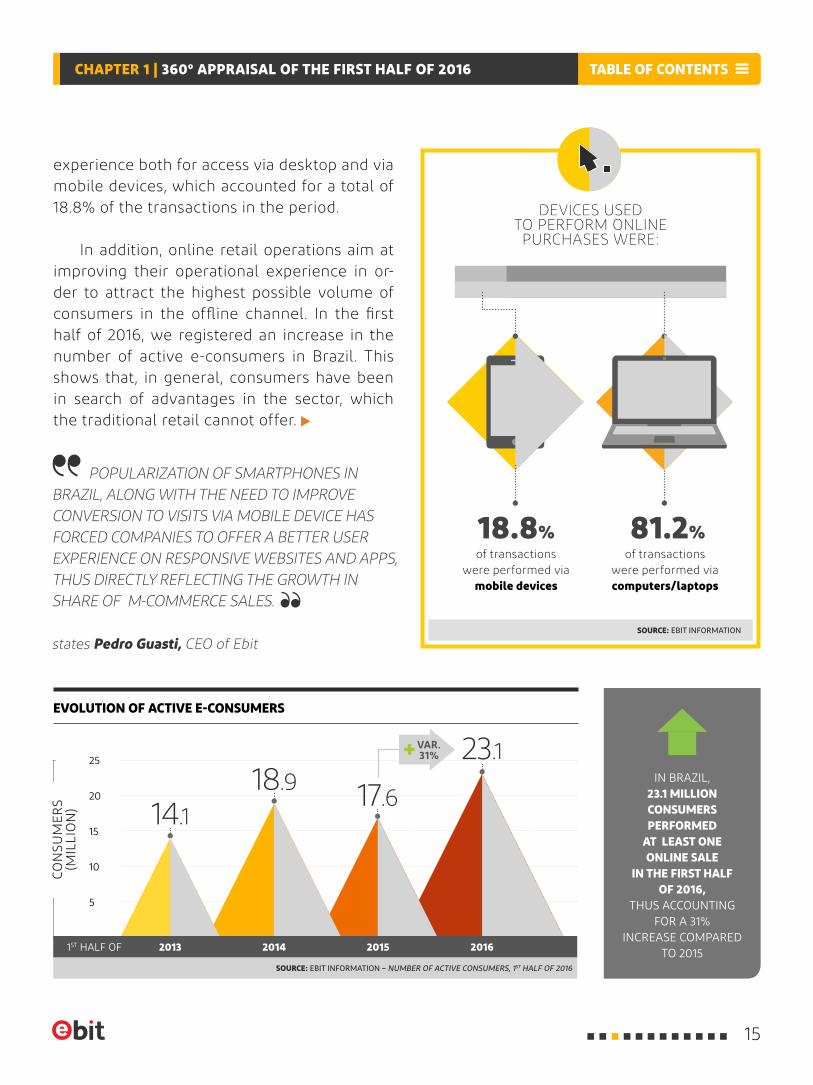

experience both for access via desktop and via mobile devices, which accounted for a total of 18.8% of the transactions in the period.

In addition, online retail operations aim at improving their operational experience in or-der to attract the highest possible volume of consumers in the offline channel. In the first half of 2016, we registered an increase in the number of active e-consumers in Brazil. This shows that, in general, consumers have been in search of advantages in the sector, which the traditional retail cannot offer.

POPULARIZATION OF SMARTPHONES IN BRAZIL, ALONG WITH THE NEED TO IMPROVECONVERSION TO VISITS VIA MOBILE DEVICE HAS FORCED COMPANIES TO OFFER A BETTER USER EXPERIENCE ON RESPONSIVE WEBSITES AND APPS, THUS DIRECTLY REFLECTING THE GROWTH IN SHARE OF M-COMMERCE SALES.

states Pedro Guasti, CEO of Ebit

IN BRAZIL, 23.1 MILLION CONSUMERS PERFORMED

AT LEAST ONE ONLINE SALE

IN THE FIRST HALF OF 2016,

THUS ACCOUNTING FOR A 31%

INCREASE COMPARED TO 2015

of transactionswere performed via

mobile devices

of transactionswere performed via computers/laptops

DEVICES USED TO PERFORM ONLINE

PURCHASES WERE:

81.2%18.8%

EVOLUTION OF ACTIVE E-CONSUMERS

SOURCE: EBIT INFORMATION – NUMBER OF ACTIVE CONSUMERS, 1ST HALF OF 2016

10

15

5

20

25

CON

SUM

ERS

(MIL

LIO

N)

VAR. 31%

20131ST HALF OF 2014 2015 2016

14.118.9 17.6

23.1

SOURCE: EBIT INFORMATION

TABLE OF CONTENTSCHAPTER 1 | 360º APPRAISAL OF THE FIRST HALF OF 2016

15

CONSUMER PROFILE IN THE 1ST HALF OF 2016

SOURCE: EBIT INFORMATION

REGION

WOMAN

1S/2016

1S/ 2015

1S/ 2016

1S/2015

MEN

49.99%50.01%

48.13%51.87%

TO 24 YEARS

OLD

BETWEEN 25 AND 34 YEARS OLD

ABOVE 50 YEARS

OLD

AVERAGE AGE

(YEARS OLD)

BETWEEN 35 AND 49 YEARS OLD

8%

8%

22%

23%

37%

37%

33%

32%

43.1

42.8

FAMILYAVERAGEINCOME

THE AVERAGE INCOME

OF ONLINE CONSUMERS INCREASED

BY 11%, BOOSTED BY A WEAKER CLASS C

IN E-COMMERCE PURCHASES

THE AVERAGE AGE OF THE BRAZILIAN CONSUMER IS STILL 43 YEARS OLD.

DUE TO THE INTRODUCTION OF NEW, YOUNGER CONSUMERS

LESS THAN R$ 3,000

BETWEEN R$ 3,001 AND R$ 5,000

ABOVE R$ 8.001

I’D RATHER NOTANSWER

BETWEEN R$ 5.001 AND R$ 8.000

SOUTHEAST

SOUTH

NORTHEAST

MID-WEST

NORTH

FAMILY INCOME

SOUTHERN AND

MID-WESTERN

REGIONS HAVE

GAINED A LARGER

SHARE IN

E-COMMERCE

SALES

IN THE FIRST

HALF OF 2016,

THE SHARE OF

WOMEN WAS

HIGHER IN

E-COMMERCE THERE

WERE 828,655 MORE

WOMEN THAN MEN

GENDER

1S/2015 1S/2016

AGE GROUP

64.5%

13.7%

12.9%

6.1%

2.8%

63.8%

14.5%

12.5%

6.6%

2.6%

1S/2015

R$ 4.658

40,35%

21,99%

15,30%

15,09%

7,27%

1S/2016

R$ 5.174

34,70%

21,97%

16,51%

19,24%

7,58%

TABLE OF CONTENTSCHAPTER 1 | 360º APPRAISAL OF THE FIRST HALF OF 2016

16

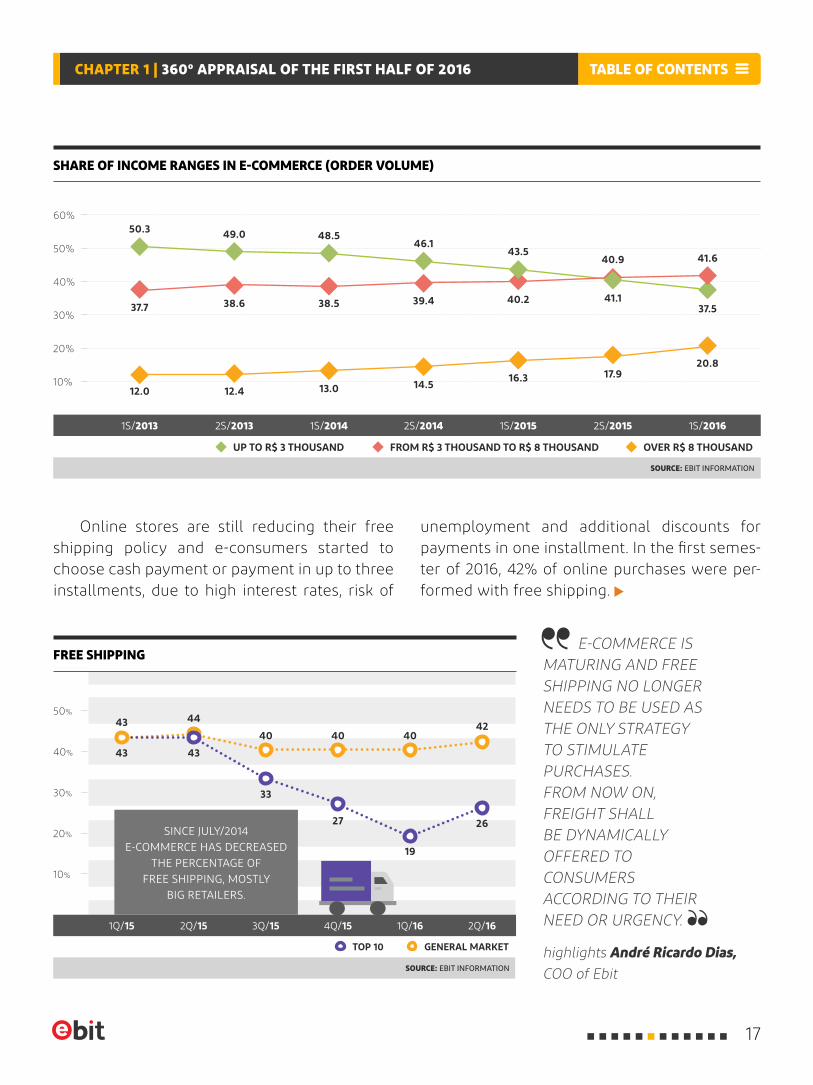

unemployment and additional discounts for payments in one installment. In the first semes-ter of 2016, 42% of online purchases were per-formed with free shipping.

E-COMMERCE IS MATURING AND FREE SHIPPING NO LONGER NEEDS TO BE USED AS THE ONLY STRATEGY TO STIMULATE PURCHASES. FROM NOW ON, FREIGHT SHALL BE DYNAMICALLY OFFERED TO CONSUMERS ACCORDING TO THEIR NEED OR URGENCY.

Online stores are still reducing their free shipping policy and e-consumers started to choose cash payment or payment in up to three installments, due to high interest rates, risk of

highlights André Ricardo Dias, COO of Ebit

SHARE OF INCOME RANGES IN E-COMMERCE (ORDER VOLUME)

SOURCE: EBIT INFORMATION

TOP 10 GENERAL MARKET

30%

50%

20%

10%

40% 43

33

19

43

27 26

4340 40

44

4042

1Q/15 3Q/152Q/15 4Q/15 2Q/161Q/16

SOURCE: EBIT INFORMATION

UP TO R$ 3 THOUSAND FROM R$ 3 THOUSAND TO R$ 8 THOUSAND OVER R$ 8 THOUSAND

1S/2013 1S/20162S/20151S/20152S/20141S/20142S/2013

FREE SHIPPING

10%

30%

50%

20%

40%

60%

SINCE JULY/2014 E-COMMERCE HAS DECREASED

THE PERCENTAGE OF FREE SHIPPING, MOSTLY

BIG RETAILERS.

50.348.5

43.5

49.046.1

41.1

41.6

38.5 40.238.6 39.4

40.9

37.537.7

12.0 12.4 13.0 14.516.3 17.9

20.8

TABLE OF CONTENTSCHAPTER 1 | 360º APPRAISAL OF THE FIRST HALF OF 2016

17

SOURCE: EBIT INFORMATION

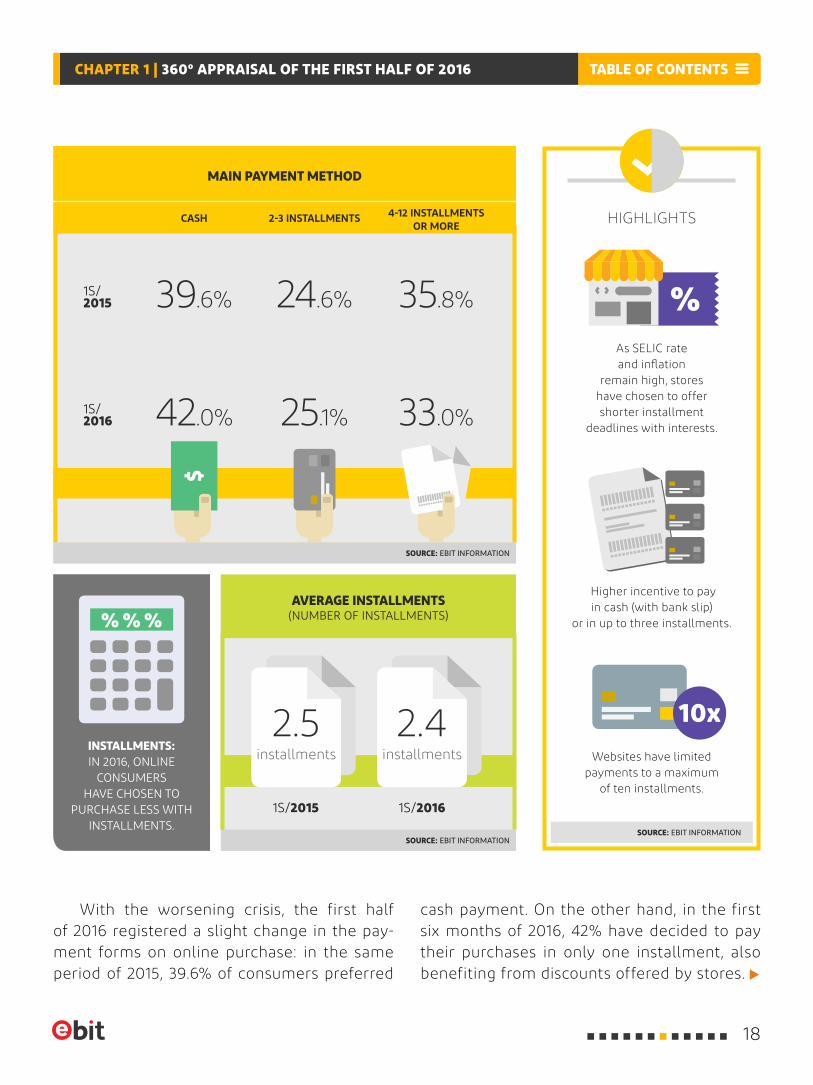

With the worsening crisis, the first half of 2016 registered a slight change in the pay-ment forms on online purchase: in the same period of 2015, 39.6% of consumers preferred

cash payment. On the other hand, in the first six months of 2016, 42% have decided to pay their purchases in only one installment, also benefiting from discounts offered by stores.

HIGHLIGHTS

As SELIC rate and inflation

remain high, stores have chosen to offer shorter installment

deadlines with interests.

Higher incentive to pay in cash (with bank slip)

or in up to three installments.

Websites have limited payments to a maximum

of ten installments.

SOURCE: EBIT INFORMATION

INSTALLMENTS:IN 2016, ONLINE

CONSUMERS HAVE CHOSEN TO

PURCHASE LESS WITH INSTALLMENTS.

AVERAGE INSTALLMENTS(NUMBER OF INSTALLMENTS)

MAIN PAYMENT METHOD

CASH 2-3 INSTALLMENTS 4-12 INSTALLMENTS OR MORE

2.5installments

2.4installments

39.6%

42.0%

24.6%

25.1%

35.8%

33.0%

1S/2015 1S/2016

1S/2015

1S/2016

SOURCE: EBIT INFORMATION

TABLE OF CONTENTSCHAPTER 1 | 360º APPRAISAL OF THE FIRST HALF OF 2016

18

FINANCIAL DATA: ORDERS, SALES, AND AVERAGE TICKET

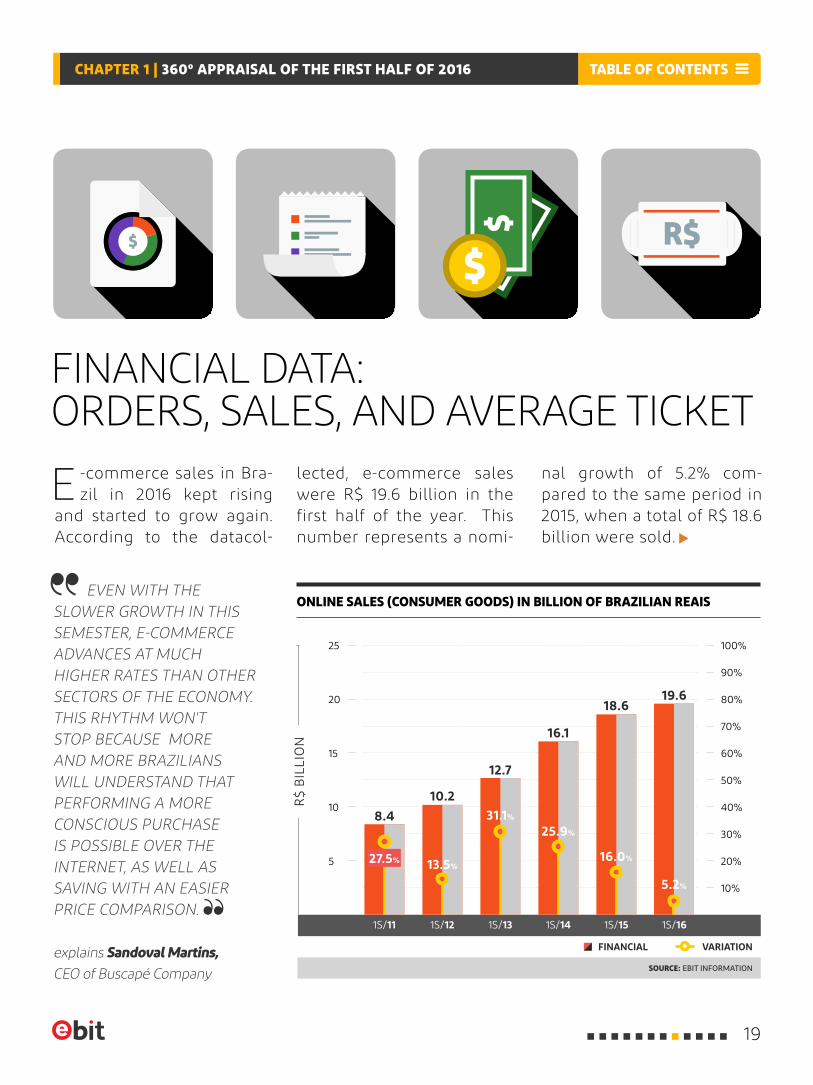

E -commerce sales in Bra-zil in 2016 kept rising

and started to grow again. According to the datacol-

EVEN WITH THE SLOWER GROWTH IN THIS SEMESTER, E-COMMERCE ADVANCES AT MUCH HIGHER RATES THAN OTHER SECTORS OF THE ECONOMY. THIS RHYTHM WON'T STOP BECAUSE MORE AND MORE BRAZILIANS WILL UNDERSTAND THAT PERFORMING A MORE CONSCIOUS PURCHASE IS POSSIBLE OVER THE INTERNET, AS WELL AS SAVING WITH AN EASIER PRICE COMPARISON.

explains Sandoval Martins, CEO of Buscapé Company

lected, e-commerce sales were R$ 19.6 billion in the first half of the year. This number represents a nomi-

nal growth of 5.2% com-pared to the same period in 2015, when a total of R$ 18.6 billion were sold.

ONLINE SALES (CONSUMER GOODS) IN BILLION OF BRAZILIAN REAIS

SOURCE: EBIT INFORMATION

FINANCIAL VARIATION

10

30%

20

70%

60%

40%

80%

5 20%

10%

15

50%

25

90%

100%

R$

BIL

LIO

N

1S/11 1S/141S/13 1S/161S/12 1S/15

27.5%

8.4

12.7

18.6

10.2

16.1

19.6

31.1%

16.0%13.5%

25.9%

5.2%

TABLE OF CONTENTSCHAPTER 1 | 360º APPRAISAL OF THE FIRST HALF OF 2016

19

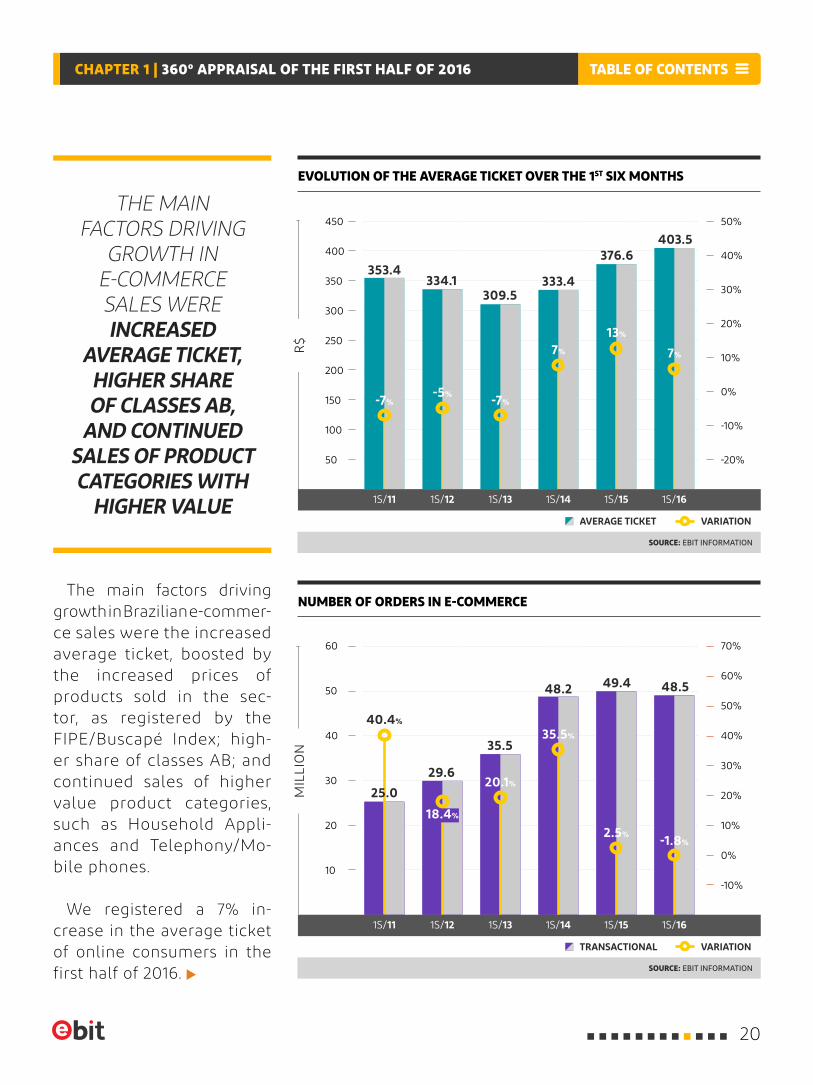

The main factors driving growth in Brazilian e-commer- ce sales were the increased average ticket, boosted by the increased prices of products sold in the sec-tor, as registered by the FIPE/Buscapé Index; high-er share of classes AB; and continued sales of higher value product categories, such as Household Appli-ances and Telephony/Mo-bile phones.

We registered a 7% in-crease in the average ticket of online consumers in the first half of 2016.

THE MAIN FACTORS DRIVING

GROWTH IN E-COMMERCE SALES WERE INCREASED

AVERAGE TICKET, HIGHER SHARE OF CLASSES AB,

AND CONTINUED SALES OF PRODUCT CATEGORIES WITH

HIGHER VALUE

EVOLUTION OF THE AVERAGE TICKET OVER THE 1ST SIX MONTHS

NUMBER OF ORDERS IN E-COMMERCE

SOURCE: EBIT INFORMATION

SOURCE: EBIT INFORMATION

AVERAGE TICKET

TRANSACTIONAL

VARIATION

-20%

-10%

20%

30%

10%

20%

-10%

0%

30%

40%

0%

10%

450

60

350

40

250

20

150

50

400

50

300

30

200

10

100

40%

50%

50%

60%

70%

R$

MIL

LIO

N

VARIATION

353.4

309.5

376.6

334.1 333.4

403.5

25.0

35.5

49.4

29.6

48.2 48.5

40.4%

1S/11 1S/141S/13 1S/161S/12 1S/15

18.4%

-5% -7%

7%

13%

7%

-7%

20.1%

35.5%

2.5% -1.8%

1S/11 1S/141S/13 1S/161S/12 1S/15

TABLE OF CONTENTSCHAPTER 1 | 360º APPRAISAL OF THE FIRST HALF OF 2016

20

HIGHLIGHTS

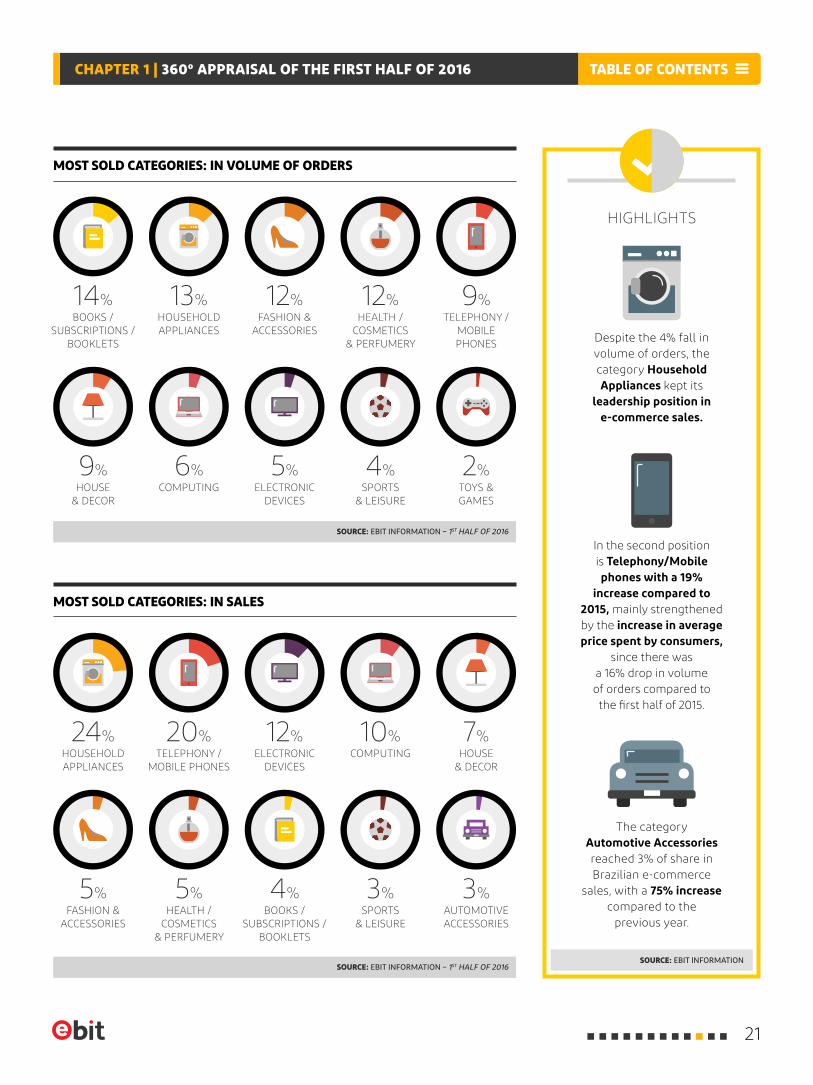

MOST SOLD CATEGORIES: IN VOLUME OF ORDERS

MOST SOLD CATEGORIES: IN SALES

SOURCE: EBIT INFORMATION – 1ST HALF OF 2016

BOOKS /SUBSCRIPTIONS /

BOOKLETS

FASHION & ACCESSORIES

HOUSE & DECOR

HOUSEHOLD APPLIANCES

FASHION & ACCESSORIES

BOOKS /SUBSCRIPTIONS /

BOOKLETS

ELECTRONIC DEVICES

ELECTRONIC DEVICES

HOUSEHOLD APPLIANCES

HEALTH / COSMETICS

& PERFUMERY

COMPUTING

TELEPHONY / MOBILE PHONES

HEALTH / COSMETICS

& PERFUMERY

SPORTS& LEISURE

SPORTS& LEISURE

COMPUTING

TELEPHONY / MOBILE PHONES

AUTOMOTIVEACCESSORIES

TOYS & GAMES

HOUSE & DECOR

14%

5%

9%

24%

12%

4%

5%

12%

13%

5%

6%

20%

12%

3%

4%

10%

9%

3%

2%

7%

SOURCE: EBIT INFORMATION – 1ST HALF OF 2016

Despite the 4% fall in volume of orders, the category Household Appliances kept its

leadership position in e-commerce sales.

In the second position is Telephony/Mobile phones with a 19%

increase compared to 2015, mainly strengthened by the increase in average price spent by consumers,

since there was a 16% drop in volume of orders compared to the first half of 2015.

The category Automotive Accessories reached 3% of share in Brazilian e-commerce

sales, with a 75% increase compared to the

previous year.

SOURCE: EBIT INFORMATION

TABLE OF CONTENTSCHAPTER 1 | 360º APPRAISAL OF THE FIRST HALF OF 2016

21

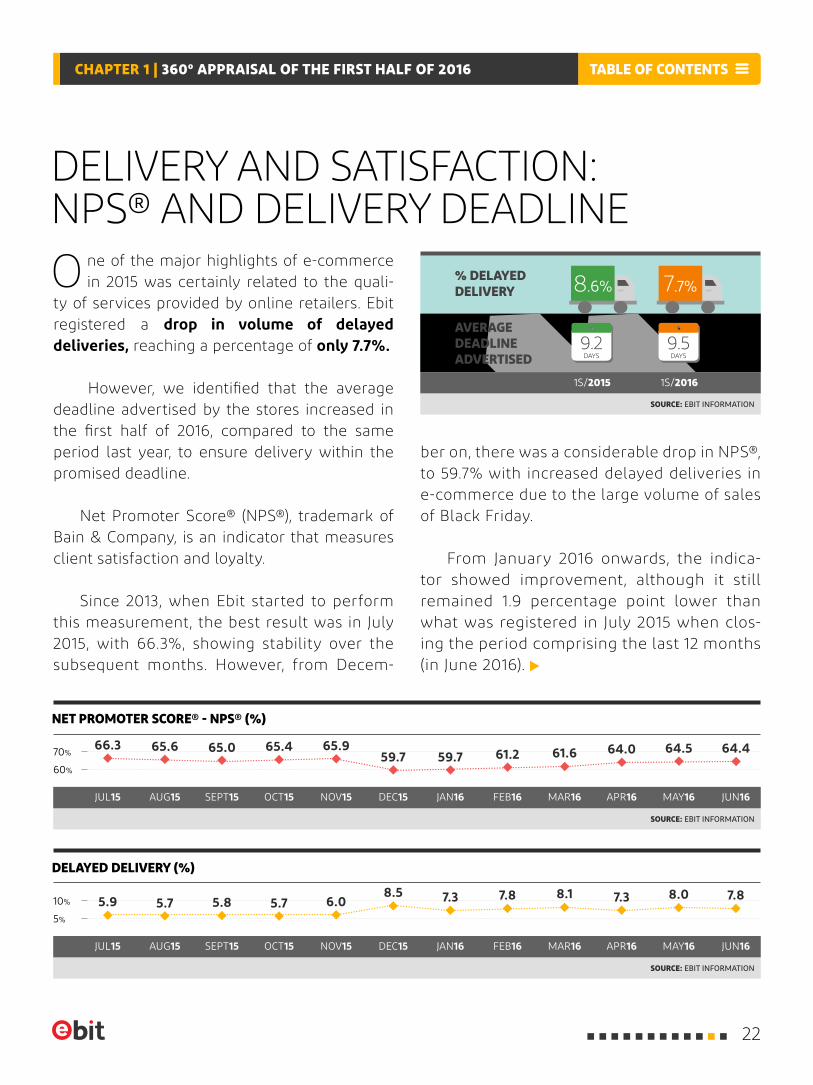

DELIVERY AND SATISFACTION: NPS® AND DELIVERY DEADLINE

O ne of the major highlights of e-commerce in 2015 was certainly related to the quali-

ty of services provided by online retailers. Ebit registered a drop in volume of delayed deliveries, reaching a percentage of only 7.7%.

However, we identified that the average deadline advertised by the stores increased in the first half of 2016, compared to the same period last year, to ensure delivery within the promised deadline.

Net Promoter Score® (NPS®), trademark of Bain & Company, is an indicator that measures client satisfaction and loyalty.

Since 2013, when Ebit started to perform this measurement, the best result was in July 2015, with 66.3%, showing stability over the subsequent months. However, from Decem-

ber on, there was a considerable drop in NPS®, to 59.7% with increased delayed deliveries in e-commerce due to the large volume of sales of Black Friday.

From January 2016 onwards, the indica-tor showed improvement, although it still remained 1.9 percentage point lower than what was registered in July 2015 when clos-ing the period comprising the last 12 months (in June 2016).

10%

70%

5%

60%

NET PROMOTER SCORE® - NPS® (%)

DELAYED DELIVERY (%)

SOURCE: EBIT INFORMATION

SOURCE: EBIT INFORMATION

SOURCE: EBIT INFORMATION

JAN16

JAN16

JUL15

JUL15

APR16

APR16

OCT15

OCT15

FEB16

FEB16

AUG15

AUG15

MAY16

MAY16

NOV15

NOV15

MAR16

MAR16

SEPT15

SEPT15

JUN16

JUN16

DEC15

DEC15

1S/2015 1S/2016

% DELAYED DELIVERY

AVERAGE DEADLINE ADVERTISED

65.0

5.8

65.4

5.7

59.7

7.3

61.2

7.8

66.3

5.9

65.6

5.7

65.9

6.0

59.7

8.5

61.6

8.1

64.0

7.3

64.4

7.8

64.5

8.0

8.6% 7.7%

9.5DAYS

9.2DAYS

TABLE OF CONTENTSCHAPTER 1 | 360º APPRAISAL OF THE FIRST HALF OF 2016

22

PROJECTION FOR 2016

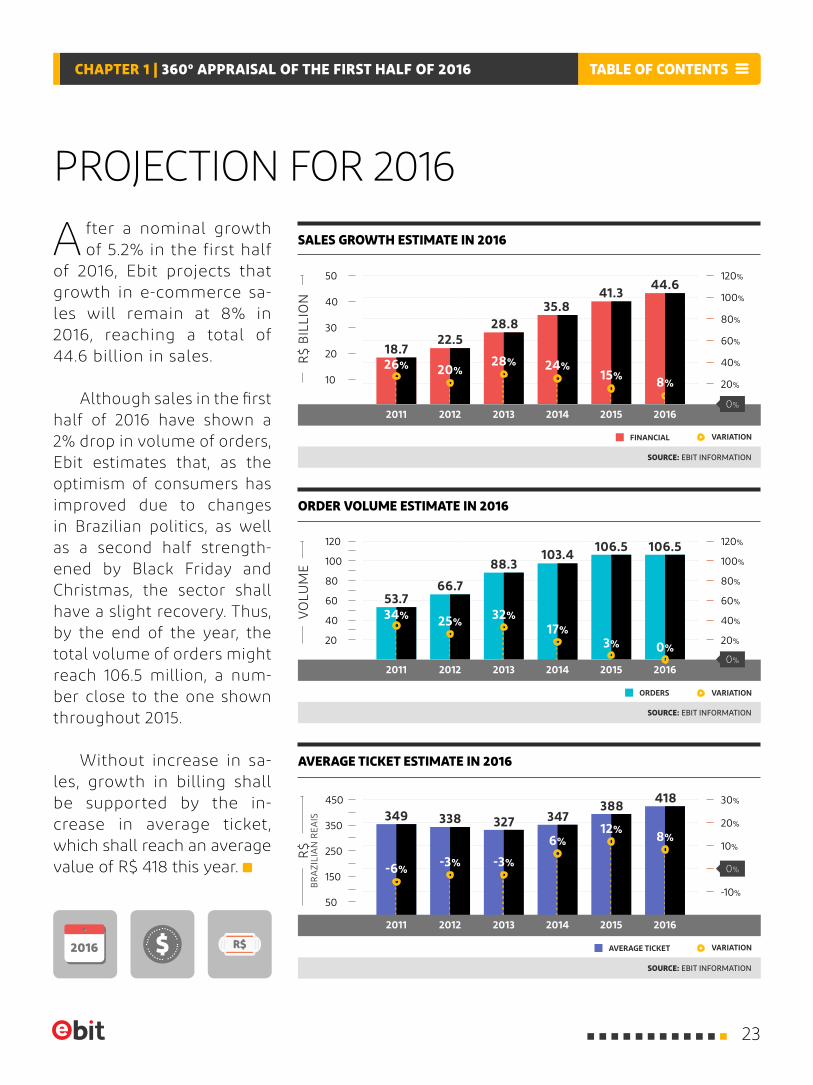

A fter a nominal growth of 5.2% in the first half

of 2016, Ebit projects that growth in e-commerce sa-les will remain at 8% in 2016, reaching a total of 44.6 billion in sales.

Although sales in the first half of 2016 have shown a 2% drop in volume of orders, Ebit estimates that, as the optimism of consumers has improved due to changes in Brazilian politics, as well as a second half strength- ened by Black Friday and Christmas, the sector shall have a slight recovery. Thus, by the end of the year, the total volume of orders might reach 106.5 million, a num-ber close to the one shown throughout 2015.

Without increase in sa-les, growth in billing shall be supported by the in-crease in average ticket, which shall reach an average value of R$ 418 this year.

AVERAGE TICKET ESTIMATE IN 2016

ORDER VOLUME ESTIMATE IN 2016

SALES GROWTH ESTIMATE IN 2016

SOURCE: EBIT INFORMATION

SOURCE: EBIT INFORMATION

SOURCE: EBIT INFORMATION

450

350

250

150

50

50

40

30

20

10

30%

120%120

120%

10%

80%80

80%

20%

100%100

100%

-10%

40%40

40%

60%60

60%

20%20

20%

R$

R$

BIL

LIO

NV

OLU

ME

0%

BR

AZI

LIA

N R

EAIS

AVERAGE TICKET

ORDERS

FINANCIAL

VARIATION

VARIATION

VARIATION

2011 20142013 20162012 20150%

2011 20142013 20162012 2015

2011 20142013 20162012 20150%

18.7

53.7

349 338 327 347388 418

66.7

88.3103.4 106.5 106.5

22.528.8

35.841.3

44.6

26%

34%

-6%-3% -3%

6%12% 8%

17%25%

3%

32%

0%

20%28% 24%

15% 8%

2016

TABLE OF CONTENTSCHAPTER 1 | 360º APPRAISAL OF THE FIRST HALF OF 2016

23

ONLINE PURCHASING

CYCLE

CHAPTER 2

24

I t has become increasingly important for e-commer- ce companies to un-

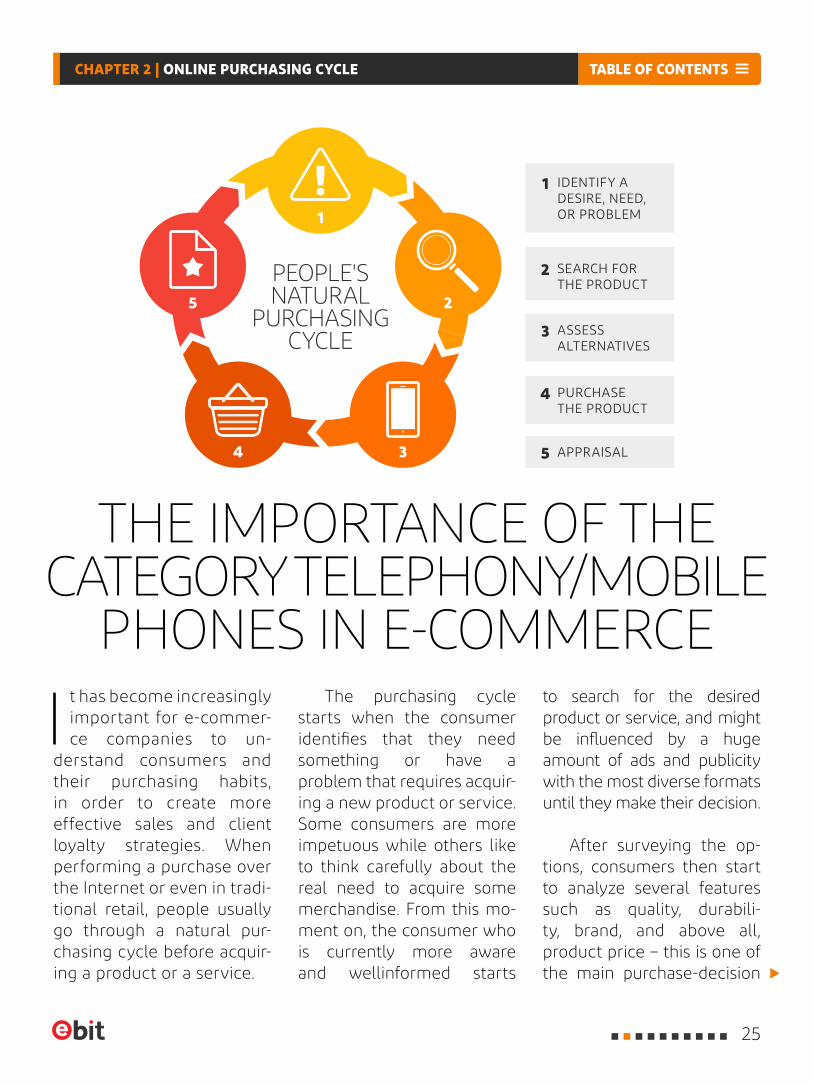

derstand consumers and their purchasing habits, in order to create more effective sales and client loyalty strategies. When performing a purchase over the Internet or even in tradi-tional retail, people usually go through a natural pur-chasing cycle before acquir-ing a product or a service.

THE IMPORTANCE OF THE CATEGORY TELEPHONY/MOBILE

PHONES IN E-COMMERCEThe purchasing cycle

starts when the consumer identifies that they need something or have a problem that requires acquir-ing a new product or service. Some consumers are more impetuous while others like to think carefully about the real need to acquire some merchandise. From this mo-ment on, the consumer who is currently more aware and wellinformed starts

to search for the desired product or service, and might be influenced by a huge amount of ads and publicity with the most diverse formats until they make their decision.

After surveying the op-tions, consumers then start to analyze several features such as quality, durabili-ty, brand, and above all, product price – this is one of the main purchase-decision

IDENTIFY A DESIRE, NEED, OR PROBLEM

1

SEARCH FOR THE PRODUCT

2

APPRAISAL5

ASSESS ALTERNATIVES

3

PURCHASE THE PRODUCT

4

1

2

34

5

PEOPLE'S NATURAL

PURCHASING CYCLE

TABLE OF CONTENTSCHAPTER 2 | ONLINE PURCHASING CYCLE

25

factors. After making their decision, having weighed up all benefits as well as negative points, con-sumers decide to buy the product with the best cost-benefit ratio.

In this scenario, the question posed by many companies in the sector is: "What is the process and time to purchase a product in different categories by e-commerce websites?"

We know that the cate-gory Telephony and Mobile phones has been gaining rel-evance with online practices over the last years, with in-creasing share in the nation-al e-commerce market. In 2013, this category occupied the sixth position in volume of orders, with a 6% share of sales; in 2014, it rose to the fourth position with 8% of share in online purchases. In 2015, the category rose again, reaching the third position in the ranking of most sold cate-gories in the Brazilian e-com-merce, with a total of 11% of sales in volume of orders.

Having increasingly be-come an object of desire and a need for Brazilians, who

used to having smartphones for personal and professional use several times a day, this category reached the sec-ond position in e-commerce sales in Brazil, with an aver-age price of R$ 867 in the first half of 2016. In the first six months of 2016 alone, Ebit

estimates that approxima- tely 3.98 million smart-phones were sold in the Brazilian e-commerce. This high sales volume makes Brazil a large market for manufacturers and Telecom operators, whose mission is to broaden the installed 3G and 4G base over the next years. By crossing check-ing information obtained by PNAD survey with data from Teleco/Anatel, Ebit estimates there are approximately 100 million users who have some type of mobile phone with Internet connection.

An article in portal Ex-ame.com in 2015 estimat-ed that Brazilians like to ex-change mobile phones, on average, every year and one month, thus generating a po-tential market/year of 100 million new devices in Brazil.

The increasing use of smartphones and mobile phones has been largely de-bated and displayed in the last Ebit Webshoppers re-ports. The share of online purchases via mobile devices, which was practically non-exis-tent in June 2011 (0.3%), has risen to 23% in five years, a 6,300% growth over the period.

THE INTERNET HAS SIGNIFICANTLY

CHANGED THE WAY HOW

PEOPE ACQUIRE A PRODUCT OR SERVICE

AS THE RULE IS NO LONGER HOW

TO FIND YOUR CLIENTS BUT HOW TO BE FOUND

BY THEM IN A NON-INVASIVE MANNER AND

WITH CREDIBILITY.

says André Ricardo Dias,COO of Ebit

TABLE OF CONTENTSCHAPTER 2 | ONLINE PURCHASING CYCLE

26

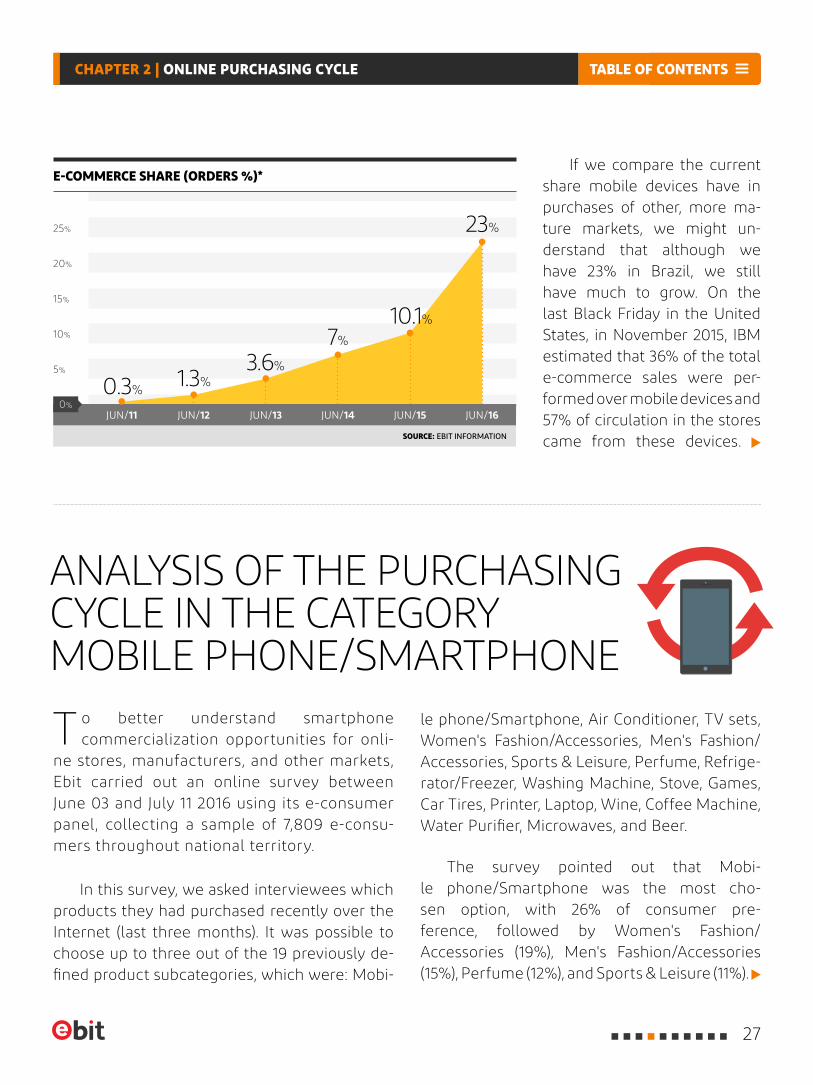

ANALYSIS OF THE PURCHASING CYCLE IN THE CATEGORY MOBILE PHONE/SMARTPHONE

T o better understand smartphone commercialization opportunities for onli-

ne stores, manufacturers, and other markets, Ebit carried out an online survey between June 03 and July 11 2016 using its e-consumer panel, collecting a sample of 7,809 e-consu-mers throughout national territory.

In this survey, we asked interviewees which products they had purchased recently over the Internet (last three months). It was possible to choose up to three out of the 19 previously de-fined product subcategories, which were: Mobi-

le phone/Smartphone, Air Conditioner, TV sets, Women's Fashion/Accessories, Men's Fashion/Accessories, Sports & Leisure, Perfume, Refrige-rator/Freezer, Washing Machine, Stove, Games, Car Tires, Printer, Laptop, Wine, Coffee Machine, Water Purifier, Microwaves, and Beer.

The survey pointed out that Mobi-le phone/Smartphone was the most cho-sen option, with 26% of consumer pre-ference, followed by Women's Fashion/ Accessories (19%), Men's Fashion/Accessories (15%), Perfume (12%), and Sports & Leisure (11%).

If we compare the current share mobile devices have in purchases of other, more ma-ture markets, we might un-derstand that although we have 23% in Brazil, we still have much to grow. On the last Black Friday in the United States, in November 2015, IBM estimated that 36% of the total e-commerce sales were per-formed over mobile devices and 57% of circulation in the stores came from these devices.

E-COMMERCE SHARE (ORDERS %)*

SOURCE: EBIT INFORMATION

20%

25%

15%

5%

10%

JUN/13JUN/11 JUN/12 JUN/14 JUN/16JUN/15

0.3%

7%

1.3%

10.1%

3.6%

23%

0%

TABLE OF CONTENTSCHAPTER 2 | ONLINE PURCHASING CYCLE

27

ONLINE CONSUMER PROFILE: MOBILE PHONE/SMARTPHONE

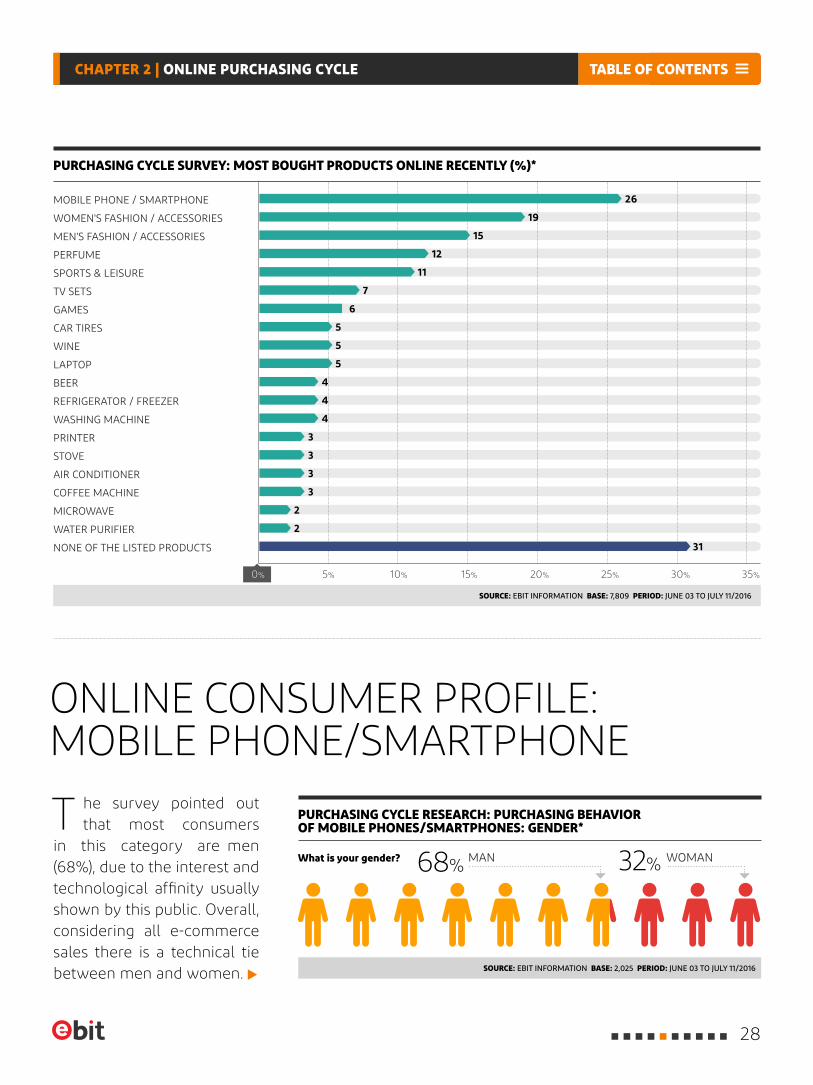

T he survey pointed out that most consumers

in this category are men (68%), due to the interest and technological affinity usually shown by this public. Overall, considering all e-commerce sales there is a technical tie between men and women.

PURCHASING CYCLE SURVEY: MOST BOUGHT PRODUCTS ONLINE RECENTLY (%)*

SOURCE: EBIT INFORMATION BASE: 7,809 PERIOD: JUNE 03 TO JULY 11/2016

What is your gender?

SOURCE: EBIT INFORMATION BASE: 2,025 PERIOD: JUNE 03 TO JULY 11/2016

PURCHASING CYCLE RESEARCH: PURCHASING BEHAVIOR OF MOBILE PHONES/SMARTPHONES: GENDER*

PERFUME

CAR TIRES

REFRIGERATOR / FREEZER

PRINTER

WOMEN'S FASHION / ACCESSORIES

TV SETS

LAPTOP

AIR CONDITIONER

STOVE

WATER PURIFIER

MOBILE PHONE / SMARTPHONE

SPORTS & LEISURE

WINE

WASHING MACHINE

COFFEE MACHINE

MEN'S FASHION / ACCESSORIES

GAMES

BEER

MICROWAVE

NONE OF THE LISTED PRODUCTS

0% 5% 15% 25% 35%10% 20% 30%

MAN WOMAN32%68%

26

6

4

15

5

3

11

4

3

2

19

5

3

12

5

3

7

4

2

31

TABLE OF CONTENTSCHAPTER 2 | ONLINE PURCHASING CYCLE

28

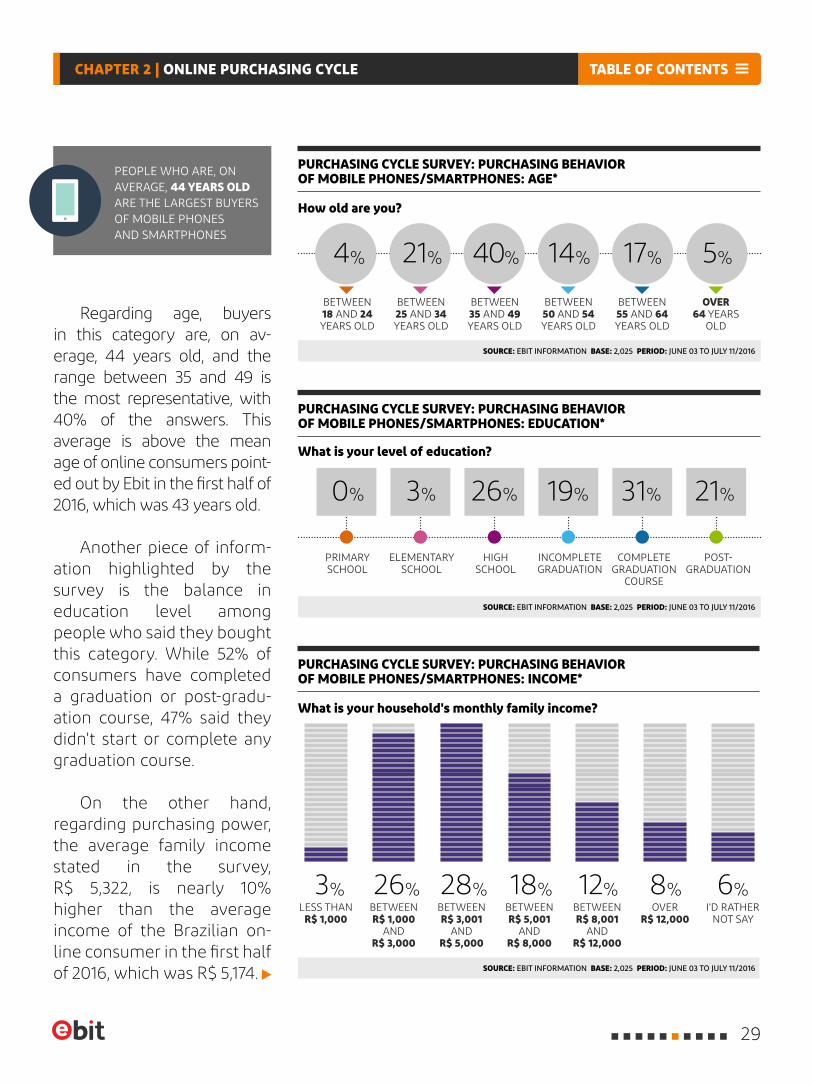

Regarding age, buyers in this category are, on av-erage, 44 years old, and the range between 35 and 49 is the most representative, with 40% of the answers. This average is above the mean age of online consumers point-ed out by Ebit in the first half of 2016, which was 43 years old.

Another piece of inform- ation highlighted by the survey is the balance in education level among people who said they bought this category. While 52% of consumers have completed a graduation or post-gradu-ation course, 47% said they didn't start or complete any graduation course.

On the other hand, regarding purchasing power, the average family income stated in the survey, R$ 5,322, is nearly 10% higher than the average income of the Brazilian on-line consumer in the first half of 2016, which was R$ 5,174.

PEOPLE WHO ARE, ON AVERAGE, 44 YEARS OLD ARE THE LARGEST BUYERS OF MOBILE PHONES AND SMARTPHONES

SOURCE: EBIT INFORMATION BASE: 2,025 PERIOD: JUNE 03 TO JULY 11/2016

SOURCE: EBIT INFORMATION BASE: 2,025 PERIOD: JUNE 03 TO JULY 11/2016

SOURCE: EBIT INFORMATION BASE: 2,025 PERIOD: JUNE 03 TO JULY 11/2016

BETWEEN18 AND 24 YEARS OLD

PRIMARY SCHOOL

ELEMENTARY SCHOOL

HIGH SCHOOL

INCOMPLETE GRADUATION

COMPLETE GRADUATION

COURSE

POST-GRADUATION

LESS THAN R$ 1,000

BETWEEN R$ 3,001

AND R$ 5,000

OVER R$ 12,000

BETWEEN R$ 1,000

AND R$ 3,000

BETWEEN R$ 8,001

AND R$ 12,000

BETWEEN R$ 5,001

AND R$ 8,000

I'D RATHER NOT SAY

BETWEEN 55 AND 64 YEARS OLD

OVER 64 YEARS

OLD

BETWEEN 35 AND 49 YEARS OLD

BETWEEN 25 AND 34 YEARS OLD

BETWEEN 50 AND 54 YEARS OLD

How old are you?

What is your level of education?

What is your household's monthly family income?

40% 17%21% 14% 5%4%

0% 21%31%26% 19%3%

3% 28% 8%26% 12%18% 6%

PURCHASING CYCLE SURVEY: PURCHASING BEHAVIOR OF MOBILE PHONES/SMARTPHONES: INCOME*

PURCHASING CYCLE SURVEY: PURCHASING BEHAVIOR OF MOBILE PHONES/SMARTPHONES: AGE*

PURCHASING CYCLE SURVEY: PURCHASING BEHAVIOR OF MOBILE PHONES/SMARTPHONES: EDUCATION*

TABLE OF CONTENTSCHAPTER 2 | ONLINE PURCHASING CYCLE

29

PURCHASING BEHAVIOR: MOBILE PHONE/SMARTPHONE

T he higher the added value of the acquired product, the higher the need

for researching and searching for the best cost-benefit ratio, mainly when the product belongs to a category that will be part of the consumer's daily life, which is practi-cally 24 hours connected a day.

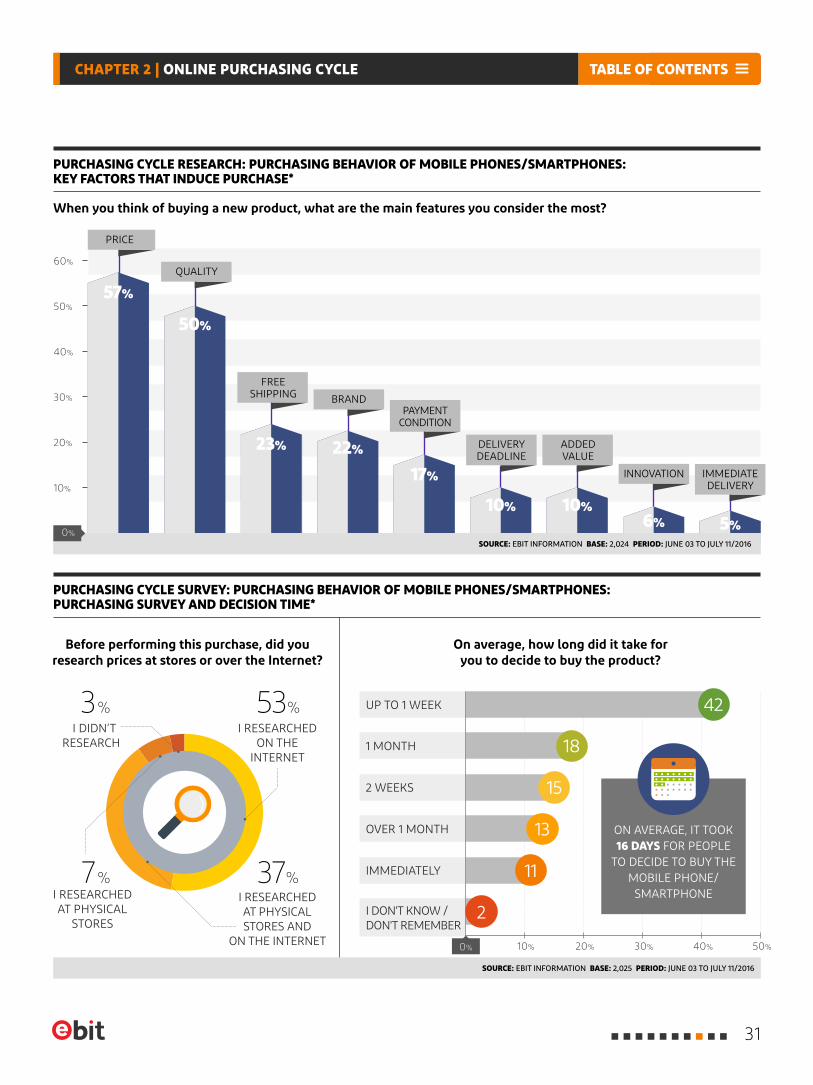

Only 3% of consumers said they did not research product prices, whereas 53% search- ed for this piece of information only over the Internet, and 37% used both digital media and physical stores for that purpose. The use of mobile devices positively helps with this challenge. One of the leaders in launching apps was Buscapé, with over 8 million downloads, which represents an extreme change in the behavior of consumers, who usually use this resource over the weekend at shopping centers and street stores.

Through another question, we under- stood the relevance of the main attributes that directly influence the purchase-decision making process. When buying a mobile pho-

ne/smartphone, 57% chose price as the main decision factor, while 50% chose quality, 23% chose free shipping, and 22% chose product brand as the most important aspect.

Therefore, choosing a product might take longer than people think. The survey indica-ted that only 15% of consumers immediately chose the purchased item, while for 42%, it took up to a week to choose the ideal item, and over two weeks for another 42%.

BUSCAPÉ’S APP IS PART OF CONSUMER BEHAVIOR HABITS, AS IT MAKES THIS ROUTINE MORE PRACTICAL AND PROVIDES A DIFFERENTIAL EXPERIENCE ANYWHERE CONSUMERS GO BY TURNING THE COMPARISON OF PRICES AND PRODUCTS ON THE BEST E-COMMERCE STORES IN BRAZIL A SIMPLE PROCESS.

says Fábio Sakae, Marketing Director of Buscapé

TABLE OF CONTENTSCHAPTER 2 | ONLINE PURCHASING CYCLE

30

PURCHASING CYCLE RESEARCH: PURCHASING BEHAVIOR OF MOBILE PHONES/SMARTPHONES: KEY FACTORS THAT INDUCE PURCHASE*

PURCHASING CYCLE SURVEY: PURCHASING BEHAVIOR OF MOBILE PHONES/SMARTPHONES: PURCHASING SURVEY AND DECISION TIME*

SOURCE: EBIT INFORMATION BASE: 2,025 PERIOD: JUNE 03 TO JULY 11/2016

Before performing this purchase, did youresearch prices at stores or over the Internet?

When you think of buying a new product, what are the main features you consider the most?

On average, how long did it take foryou to decide to buy the product?

20%

60%

50%

40%

10%

30%

I DON'T KNOW / DON'T REMEMBER

UP TO 1 WEEK

1 MONTH

2 WEEKS

OVER 1 MONTH

IMMEDIATELY

40% 50%10% 20% 30%0%

57%

17%

23%

10%

50%

10%

22%

6% 5%

7

3%

% 37%

%53

0% SOURCE: EBIT INFORMATION BASE: 2,024 PERIOD: JUNE 03 TO JULY 11/2016

PRICE

QUALITY

IMMEDIATE DELIVERY

INNOVATION

ADDED VALUE

DELIVERY DEADLINE

PAYMENT CONDITION

BRAND

FREE SHIPPING

18

15

13

11

2

I RESEARCHED ON THE

INTERNET

I DIDN’T RESEARCH

I RESEARCHEDAT PHYSICAL STORES AND

ON THE INTERNET

I RESEARCHEDAT PHYSICAL

STORES

42

ON AVERAGE, IT TOOK 16 DAYS FOR PEOPLE

TO DECIDE TO BUY THE MOBILE PHONE/

SMARTPHONE

TABLE OF CONTENTSCHAPTER 2 | ONLINE PURCHASING CYCLE

31

PURCHASING FREQUENCY OF MOBILE PHONE/SMARTPHONE

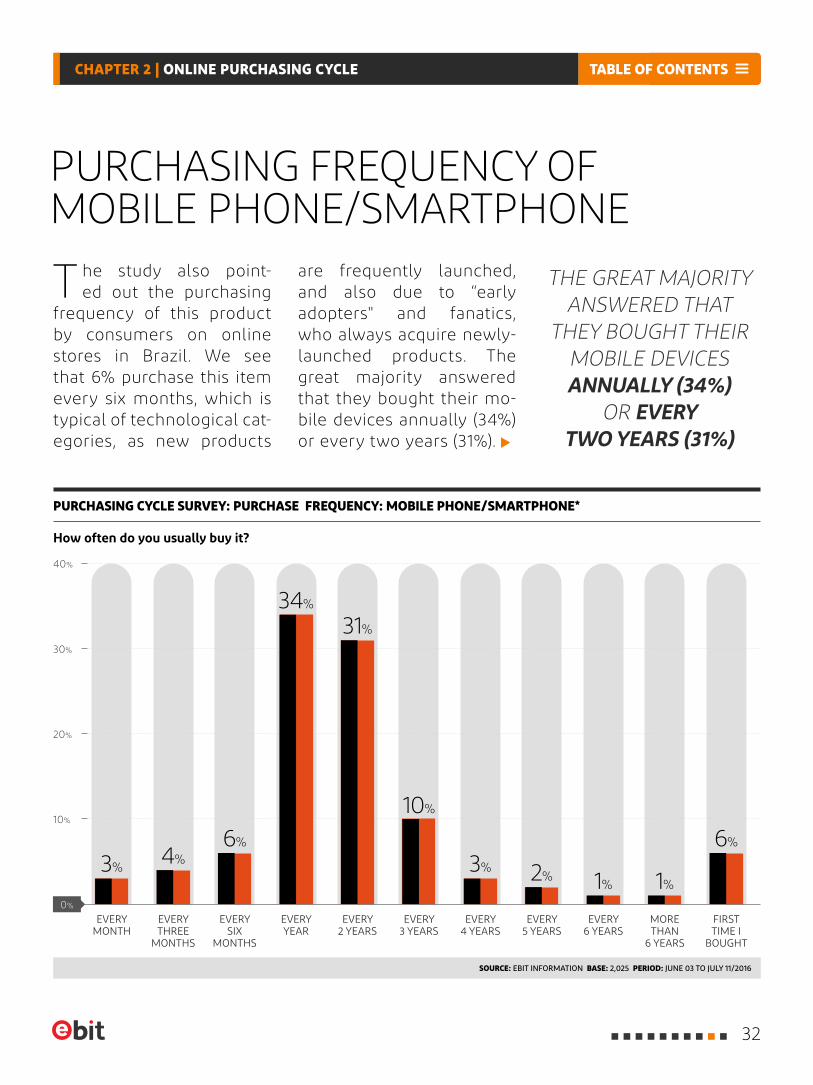

T he study also point-ed out the purchasing

frequency of this product by consumers on online stores in Brazil. We see that 6% purchase this item every six months, which is typical of technological cat-egories, as new products

THE GREAT MAJORITY ANSWERED THAT

THEY BOUGHT THEIR MOBILE DEVICES ANNUALLY (34%)

OR EVERY TWO YEARS (31%)

are frequently launched, and also due to “early adopters" and fanatics, who always acquire newly- launched products. The great majority answered that they bought their mo-bile devices annually (34%) or every two years (31%).

PURCHASING CYCLE SURVEY: PURCHASE FREQUENCY: MOBILE PHONE/SMARTPHONE*

How often do you usually buy it?

SOURCE: EBIT INFORMATION BASE: 2,025 PERIOD: JUNE 03 TO JULY 11/2016

EVERY MONTH

EVERY 2 YEARS

EVERY 3 YEARS

EVERY SIX

MONTHS

EVERY 5 YEARS

MORE THAN

6 YEARS

EVERY THREE

MONTHS

EVERY 4 YEARS

EVERY YEAR

EVERY 6 YEARS

FIRST TIME I

BOUGHT

20%

40%

10%

30%

0%

3%

31%

1%

6%

3%

6%4%

10%

1%

34%

2%

TABLE OF CONTENTSCHAPTER 2 | ONLINE PURCHASING CYCLE

32

*IN QUESTIONS THAT USE SELECTION BOXES, THE TOTAL NUMBER OF ANSWERS MIGHT BE HIGHER THAN THE NUMBERS OF INTERVIEWEES. THIS MIGHT CAUSE THE TOTAL PERCENTAGES OF THE ANSWER TO EXCEED 100%.

RELATIONSHIP BRAND x PRICE IN DECIDING TO PURCHASE A MOBILE PHONE/SMARTPHONE

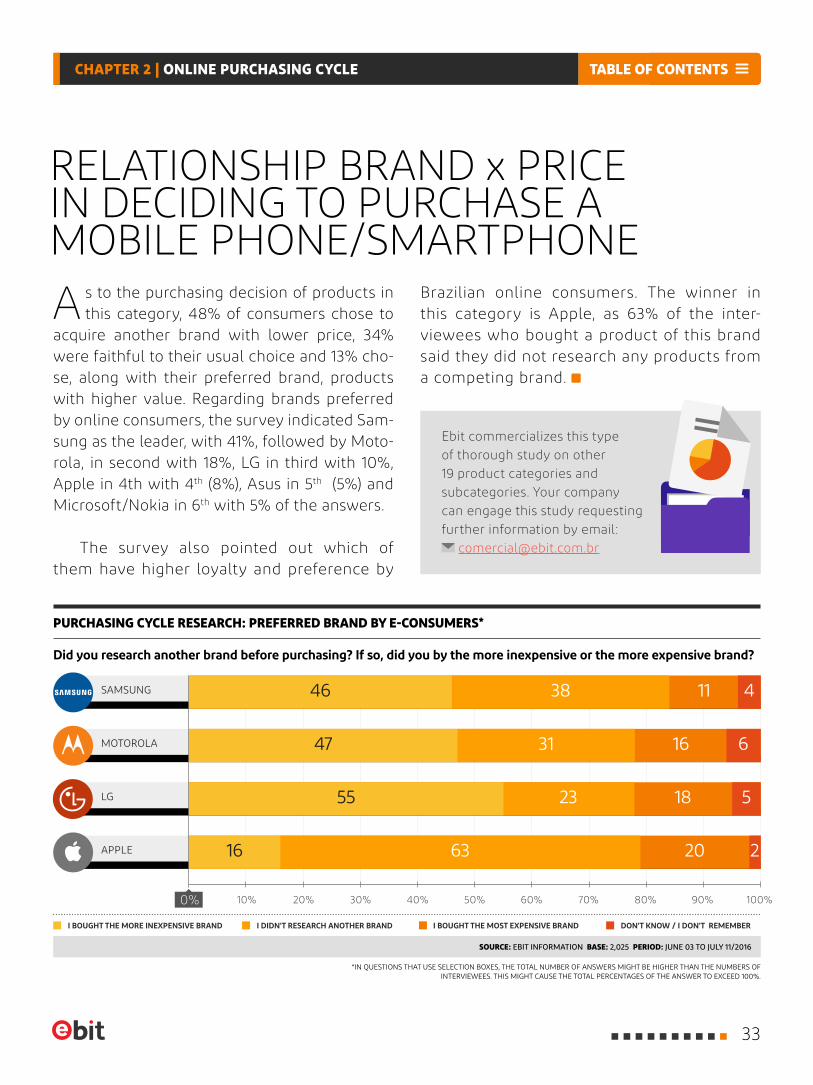

A s to the purchasing decision of products in this category, 48% of consumers chose to

acquire another brand with lower price, 34% were faithful to their usual choice and 13% cho-se, along with their preferred brand, products with higher value. Regarding brands preferred by online consumers, the survey indicated Sam-sung as the leader, with 41%, followed by Moto-rola, in second with 18%, LG in third with 10%, Apple in 4th with 4th (8%), Asus in 5th (5%) and Microsoft/Nokia in 6th with 5% of the answers.

The survey also pointed out which of them have higher loyalty and preference by

Brazilian online consumers. The winner in this category is Apple, as 63% of the inter-viewees who bought a product of this brand said they did not research any products from a competing brand.

Ebit commercializes this type of thorough study on other 19 product categories and subcategories. Your company can engage this study requesting further information by email:

SOURCE: EBIT INFORMATION BASE: 2,025 PERIOD: JUNE 03 TO JULY 11/2016

Did you research another brand before purchasing? If so, did you by the more inexpensive or the more expensive brand?

PURCHASING CYCLE RESEARCH: PREFERRED BRAND BY E-CONSUMERS*

0% 50% 100%10% 60%20% 70%40% 90%30% 80%

I BOUGHT THE MORE INEXPENSIVE BRAND I DIDN'T RESEARCH ANOTHER BRAND I BOUGHT THE MOST EXPENSIVE BRAND DON'T KNOW / I DON'T REMEMBER

SAMSUNG

MOTOROLA

APPLE

LG

216 2063

5182355

4113846

6163147

TABLE OF CONTENTSCHAPTER 2 | ONLINE PURCHASING CYCLE

33

THE ECONOMIC AND POLITICAL

CRISIS,according to FecomercioSP

34

CHAPTER 3

B razil is probably experiencing the great-est crisis of its history. GDP (Gross Domes-tic Product) shall decrease approximately

3.5% in 2016, after having registered a 3.8% drop last year. It will be the first time since the 1930's that the Brazilian economy registers a retraction for two consecutive years. The per capita income shall drop for the third consecutive year and re-tail sales in São Paulo, which dropped 3% in 2014 and 6% in 2015, shall remain unchanged in 2016 in an optimistic scenario, according to data and

projections by the Federation of Goods, Services, and Tourism of the State of São Paulo – Fecomer-cioSP. Consequently, unemployment rate has exceeded 11%. Over 100 thousand formal job vacancies have been eliminated per month in our country. In the trade in goods and services of the State of São Paulo, over 260 thousand job positions have already been extinguished in one year, according to the survey conducted by the federation based on data of the General Regis-try of Employed and Unemployed – CAGED.

THE ECONOMIC AND POLITICAL CRISIS,

ACCORDING TO FECOMERCIOSP

TABLE OF CONTENTSCHAPTER 3 | THE ECONOMIC AND POLITICAL CRISIS, according to FecomercioSP

35

DESPITE THE DEPRESSION IN THE ECONOMIC ACTIVITY

AND THE CONSEQUENT INCREASE IN UNEMPLOYMENT, INFLATION

REMAINS HIGH – ALTHOUGHTHE LAST DATA HAVE

INDICATED A SLOWDOWN – AND INTERESTS ARE ALSO HIGH

Despite the declining economic activi-ty and the consequent increased unemploy-ment, inflation remains high – although the latest data have indicated a slowdown – and interests are also high; banks are not willing to lend; companies are postponing or cutting down investments, while families, who work more and more on a tight budget, are cutting expenses and avoiding to take on debts.

The characteristics of the current re-cession, however, are quite different from conventional recessions, which usually oc-cur within economic cycles, resulting, for instance, from periods of euphoria and excessive investments or as a reflection of external shocks. The Brazilian crisis is above all a confidence crisis. Evidence of that is the pessimism of executives and consumers, indicated in confidence indicators calculated by FecomercioSP, which have reached the lowest levels in history throughout 2015 and 2016.

It is difficult to pinpoint the exact begin-ning of a crisis, which typically results of a combination of factors; however, the fact is that incorrect interventions performed by the Government from 2012 on have under-mined key sectors such as the energy sec-tor, while subsidies to specific groups have resulted in market concentration and inef-ficiency. Structural problems, such as in-creased Social Security expenses, have been left aside throughout the last decade, some-what overcast by a favorable international scenario for Brazil.

However, the international situation has changed. Misguided governmental

actions have made investors lose confidence. Despite the decrease in revenue deriving from a weaker economic activity, the Government continued to expand costs, which resulted in deficit in government accounts in 2014 and 2015. The country ended up having its invest-ment grade lowered by the main international risk assessment agencies.

While the crisis worsened, the Govern-ment didn't seem confident in the diagnosis shown by the main Brazilian executives and economists, and did not submit proposals or show any ability for political articulation to overcome the problem. Thus, it lost popula-tion and Congress support.

TABLE OF CONTENTSCHAPTER 3 | THE ECONOMIC AND POLITICAL CRISIS, according to FecomercioSP

36

THE CRISIS AND RETAIL IN SÃO PAULO

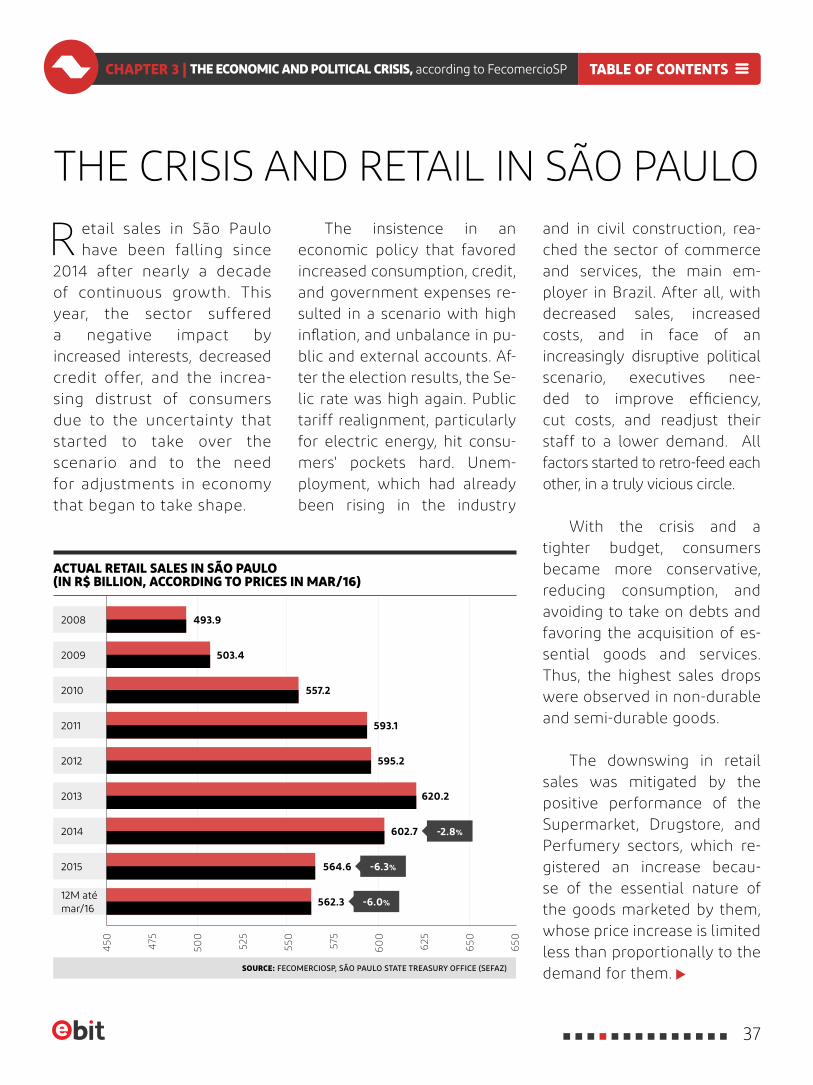

R etail sales in São Paulo have been falling since

2014 after nearly a decade of continuous growth. This year, the sector suffered a negative impact by increased interests, decreased credit offer, and the increa-sing distrust of consumers due to the uncertainty that started to take over the scenario and to the need for adjustments in economy that began to take shape.

The insistence in an economic policy that favored increased consumption, credit, and government expenses re-sulted in a scenario with high inflation, and unbalance in pu-blic and external accounts. Af-ter the election results, the Se-lic rate was high again. Public tariff realignment, particularly for electric energy, hit consu-mers' pockets hard. Unem-ployment, which had already been rising in the industry

and in civil construction, rea-ched the sector of commerce and services, the main em-ployer in Brazil. After all, with decreased sales, increased costs, and in face of an increasingly disruptive political scenario, executives nee-ded to improve efficiency, cut costs, and readjust their staff to a lower demand. All factors started to retro-feed each other, in a truly vicious circle.

With the crisis and a tighter budget, consumers became more conservative, reducing consumption, and avoiding to take on debts and favoring the acquisition of es-sential goods and services. Thus, the highest sales drops were observed in non-durable and semi-durable goods.

The downswing in retail sales was mitigated by the positive performance of the Supermarket, Drugstore, and Perfumery sectors, which re-gistered an increase becau-se of the essential nature of the goods marketed by them, whose price increase is limited less than proportionally to the demand for them.

ACTUAL RETAIL SALES IN SÃO PAULO (IN R$ BILLION, ACCORDING TO PRICES IN MAR/16)

SOURCE: FECOMERCIOSP, SÃO PAULO STATE TREASURY OFFICE (SEFAZ)

2008

2012

2010

2014

2009

2013

2011

2015

12M até mar/16

525

625475

575

450 55

0

650

650

500

60

0

493.9

503.4

557.2

593.1

595.2

620.2

602.7

564.6

562.3

-2.8%

-6.3%

-6.0%

TABLE OF CONTENTSCHAPTER 3 | THE ECONOMIC AND POLITICAL CRISIS, according to FecomercioSP

37

F rom 2015 on, with the launching of the E-commerce Conjunctural Research (PCCE),

FecomercioSP, in partnership with Ebit, start-ed to systematically investigate the behavior of sales performed over the Internet, the so-called e-commerce. This was due to the acknowledg-ment of the increasing and undeniable relevance this segment has been gaining in the Brazilian retail in general and in São Paulo, particularly.

The process of monthly monitoring e-commerce required the elaboration of an exclusive methodology, which, in turn, allowed

E-COMMERCE IN SÃO PAULO

(FECOMERCIOSP/EBIT SURVEY)

ENABLED THE KNOWLEDGE OF E-COMMERCE

SHARE IN RETAIL SALES, AS WELL AS THE INDICATOR

BEHAVIOR OVER TIME

for surveying unprecedented information on commerce in São Paulo and for elaborating, for instance, comparisons between the volume negotiated in e-commerce and monthly sales of physical stores in the State of São Paulo, divided in the 16 regions defined by the Regional Tax Offices of the São Paulo State Treasury Office (Sefaz). This enabled knowledge of the e-commerce share in retail sales in each one of these regions, as well as the indicator behavior over time.

In addition, in the exclusive context of e-commerce, unprecedented monthly data start-ed to be provided on number of orders, average ticket, and the actual sales variation in this segment.

It is thus another important source of information for the monitoring of the situation of commerce in a segment of in-creasing importance in the economy, which can be a valuable instrument for executives to define their strategies and also a guidance element for public policies directed to safety and improvement of transactions performed in the world of e-commerce.

TABLE OF CONTENTSCHAPTER 3 | THE ECONOMIC AND POLITICAL CRISIS, according to FecomercioSP

38

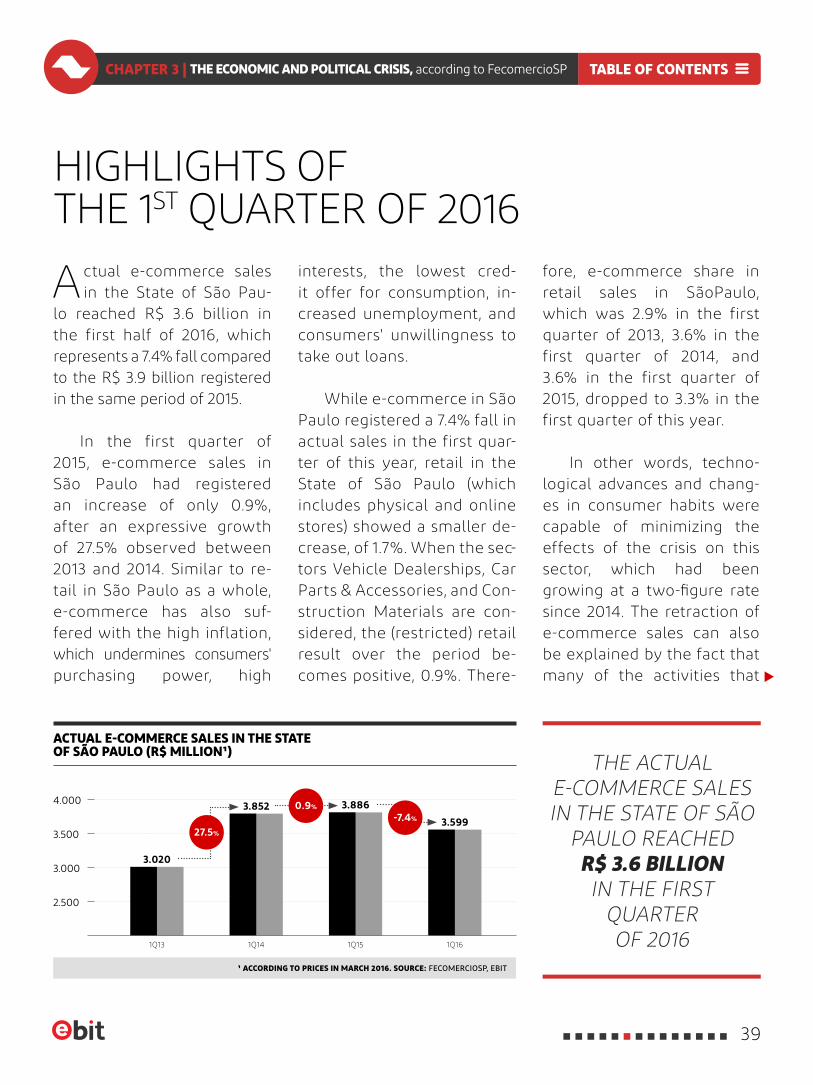

A ctual e-commerce sales in the State of São Pau-

lo reached R$ 3.6 billion in the first half of 2016, which represents a 7.4% fall compared to the R$ 3.9 billion registered in the same period of 2015.

In the first quarter of 2015, e-commerce sales in São Paulo had registered an increase of only 0.9%, after an expressive growth of 27.5% observed between 2013 and 2014. Similar to re-tail in São Paulo as a whole, e-commerce has also suf-fered with the high inflation, which undermines consumers' purchasing power, high

HIGHLIGHTS OF THE 1ST QUARTER OF 2016

fore, e-commerce share in retail sales in SãoPaulo, which was 2.9% in the first quarter of 2013, 3.6% in the first quarter of 2014, and 3.6% in the first quarter of 2015, dropped to 3.3% in the first quarter of this year.

In other words, techno-logical advances and chang-es in consumer habits were capable of minimizing the effects of the crisis on this sector, which had been growing at a two-figure rate since 2014. The retraction of e-commerce sales can also be explained by the fact that many of the activities that

interests, the lowest cred-it offer for consumption, in-creased unemployment, and consumers' unwillingness to take out loans.

While e-commerce in São Paulo registered a 7.4% fall in actual sales in the first quar-ter of this year, retail in the State of São Paulo (which includes physical and online stores) showed a smaller de-crease, of 1.7%. When the sec-tors Vehicle Dealerships, Car Parts & Accessories, and Con-struction Materials are con-sidered, the (restricted) retail result over the period be-comes positive, 0.9%. There-

THE ACTUAL E-COMMERCE SALES IN THE STATE OF SÃO

PAULO REACHEDR$ 3.6 BILLION IN THE FIRST

QUARTEROF 2016

ACTUAL E-COMMERCE SALES IN THE STATE OF SÃO PAULO (R$ MILLION¹)

¹ ACCORDING TO PRICES IN MARCH 2016. SOURCE: FECOMERCIOSP, EBIT

1Q13 1Q151Q14 1Q16

4.000

3.000

3.500

2.500

3.020

3.852 3.886

3.59927.5%

0.9%

-7.4%

TABLE OF CONTENTSCHAPTER 3 | THE ECONOMIC AND POLITICAL CRISIS, according to FecomercioSP

39

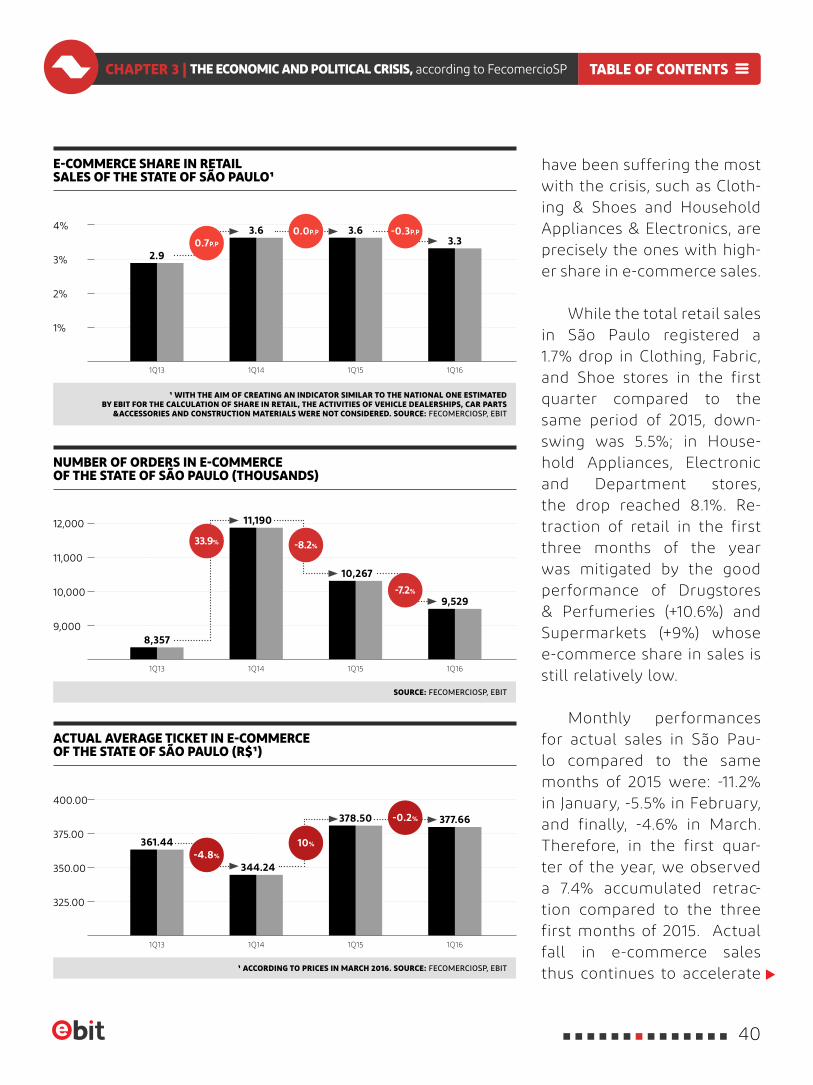

have been suffering the most with the crisis, such as Cloth-ing & Shoes and Household Appliances & Electronics, are precisely the ones with high-er share in e-commerce sales.

While the total retail sales in São Paulo registered a 1.7% drop in Clothing, Fabric, and Shoe stores in the first quarter compared to the same period of 2015, down-swing was 5.5%; in House-hold Appliances, Electronic and Department stores, the drop reached 8.1%. Re-traction of retail in the first three months of the year was mitigated by the good performance of Drugstores & Perfumeries (+10.6%) and Supermarkets (+9%) whose e-commerce share in sales is still relatively low.

Monthly performances for actual sales in São Pau-lo compared to the same months of 2015 were: -11.2% in January, -5.5% in February, and finally, -4.6% in March. Therefore, in the first quar-ter of the year, we observed a 7.4% accumulated retrac-tion compared to the three first months of 2015. Actual fall in e-commerce sales thus continues to accelerate

¹ WITH THE AIM OF CREATING AN INDICATOR SIMILAR TO THE NATIONAL ONE ESTIMATED BY EBIT FOR THE CALCULATION OF SHARE IN RETAIL, THE ACTIVITIES OF VEHICLE DEALERSHIPS, CAR PARTS

&ACCESSORIES AND CONSTRUCTION MATERIALS WERE NOT CONSIDERED. SOURCE: FECOMERCIOSP, EBIT

ACTUAL AVERAGE TICKET IN E-COMMERCE OF THE STATE OF SÃO PAULO (R$¹)

NUMBER OF ORDERS IN E-COMMERCE OF THE STATE OF SÃO PAULO (THOUSANDS)

E-COMMERCE SHARE IN RETAIL SALES OF THE STATE OF SÃO PAULO¹

¹ ACCORDING TO PRICES IN MARCH 2016. SOURCE: FECOMERCIOSP, EBIT

SOURCE: FECOMERCIOSP, EBIT

400.00

350.00

375.00

325.00

4%

2%

3%

1%

12,000

10,000

11,000

9,000

1Q13

1Q13

1Q13

1Q15

1Q15

1Q15

1Q14

1Q14

1Q14

1Q16

1Q16

1Q16

361.44

8,357

2.9

344.24

11,190

3.6

378.50

10,267

3.6

377.66

9,529

3.3

-4.8%

33.9%

0.7P.P

10%

-8.2%

0.0P.P

-0.2%

-7.2%

-0.3P.P

TABLE OF CONTENTSCHAPTER 3 | THE ECONOMIC AND POLITICAL CRISIS, according to FecomercioSP

40

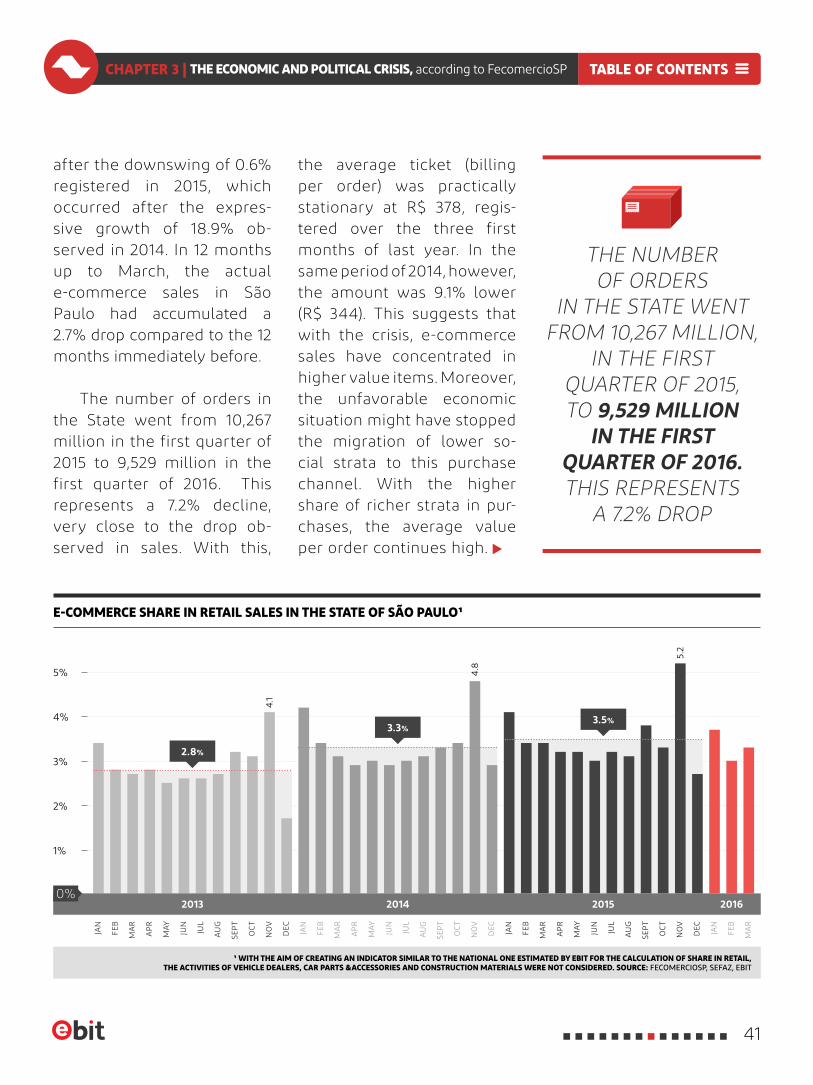

THE NUMBER OF ORDERS

IN THE STATE WENT FROM 10,267 MILLION,

IN THE FIRSTQUARTER OF 2015,TO 9,529 MILLION

IN THE FIRST QUARTER OF 2016. THIS REPRESENTS

A 7.2% DROP

after the downswing of 0.6% registered in 2015, which occurred after the expres-sive growth of 18.9% ob-served in 2014. In 12 months up to March, the actual e-commerce sales in São Paulo had accumulated a 2.7% drop compared to the 12 months immediately before.

The number of orders in the State went from 10,267 million in the first quarter of 2015 to 9,529 million in the first quarter of 2016. This represents a 7.2% decline, very close to the drop ob-served in sales. With this,

the average ticket (billing per order) was practically stationary at R$ 378, regis- tered over the three first months of last year. In the same period of 2014, however, the amount was 9.1% lower (R$ 344). This suggests that with the crisis, e-commerce sales have concentrated in higher value items. Moreover, the unfavorable economic situation might have stopped the migration of lower so-cial strata to this purchase channel. With the higher share of richer strata in pur-chases, the average value per order continues high.

E-COMMERCE SHARE IN RETAIL SALES IN THE STATE OF SÃO PAULO¹

¹ WITH THE AIM OF CREATING AN INDICATOR SIMILAR TO THE NATIONAL ONE ESTIMATED BY EBIT FOR THE CALCULATION OF SHARE IN RETAIL, THE ACTIVITIES OF VEHICLE DEALERS, CAR PARTS &ACCESSORIES AND CONSTRUCTION MATERIALS WERE NOT CONSIDERED. SOURCE: FECOMERCIOSP, SEFAZ, EBIT

4.1

4.8

5.2

5%

4%

3%

2%

1%

FEB

MA

R

JAN

FEB

JUN

OC

T

AP

R

AU

G

DEC

MA

R

JUL

NO

V

MA

Y

SEP

T

JAN

FEB

MA

R

JAN

JUN

JUL

OC

T

AP

R

AU

G

DEC

NO

V

MA

Y

SEP

T

DEC

FEB

JUN

AP

R

AU

G

MA

R

JUL

NO

V

OC

T

MA

Y

SEP

T

JAN

2013 2014 20162015

2.8%

3.3%3.5%

0%

TABLE OF CONTENTSCHAPTER 3 | THE ECONOMIC AND POLITICAL CRISIS, according to FecomercioSP

41

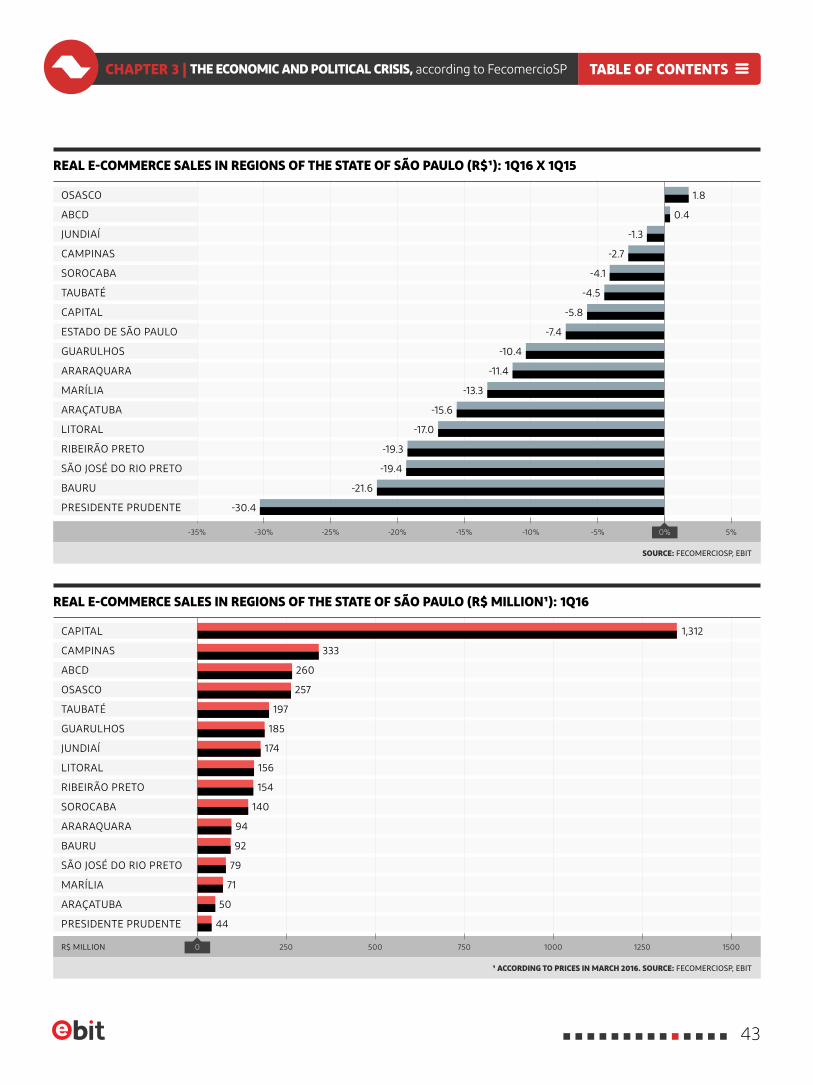

APPRAISAL OF REGIONAL DATA FROM THE STATE OF SÃO PAULO

A mong the 16 regions appraised by PCCE, considering the accumulated billion in

the first quarter of 2016, only two registered a positive variation compared to the same pe-riod in 2015: ABCD (0.4%) and Osasco (1.8%). On the other hand, the highest falls were ob-served in the regions of Presidente Prudente (-30.4%), Bauru (-21.6%), and São José do Rio Preto (19.4%).

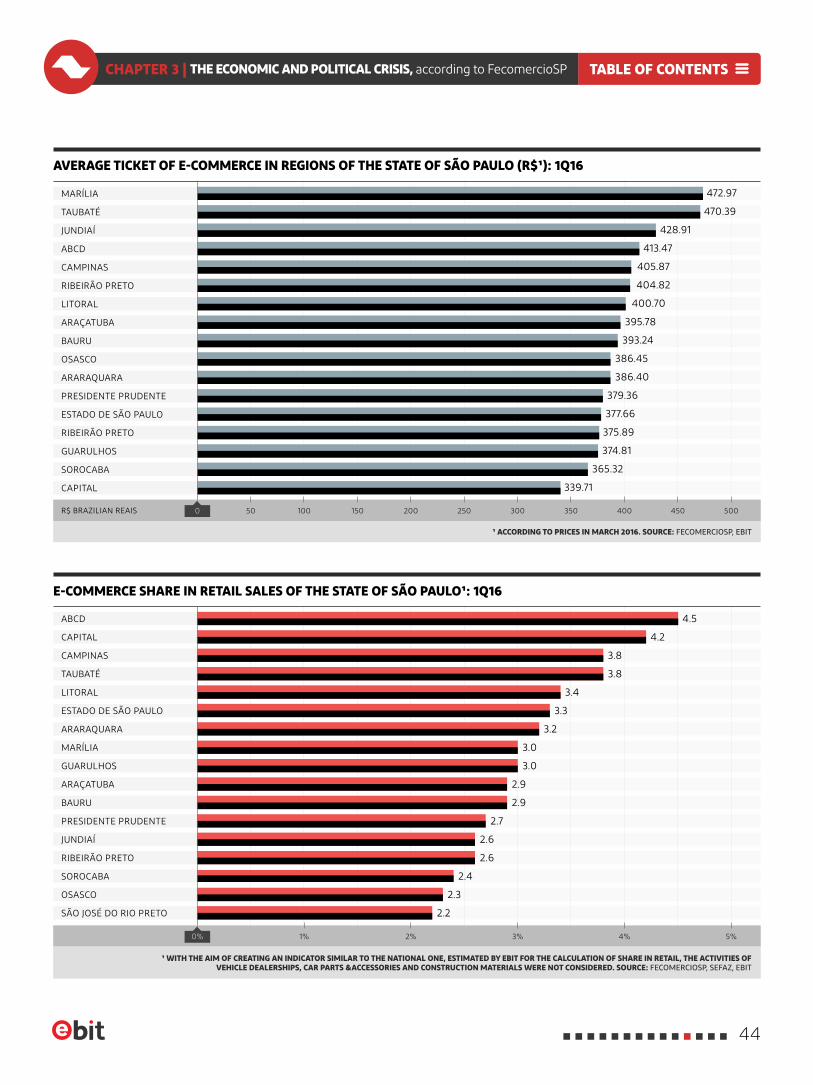

The average ticket in São Paulo was R$ 377.66 in the first quarter. The regions that registered the highest average tickets were Marília (R$ 472.97), Taubaté (R$ 470.39), and Jundiaí (R$ 428.91). At the other end, the capi-tal has the lowest average ticket, of R$ 339.71.

However, the region accounts for over 40% of the total orders and for over 36% of actual e-commerce sales; therefore, the average tick-et is naturally lower than in the other locations.

In the State of São Paulo, e-commerce share in retail (excluding the sectors Vehicle Dealerships, Car parts & Accessories, and Fur-niture & Decor) was 3.3% in the first quarter, lower than the 3.6% registered in the same pe-riod of 2015 and the 3.7% of the last quarter of 2015, when the result was influenced by the good sales performance of November in the sector due to Black Friday. In the ABCD region, share reached 4.5% in the first quarter of 2016. In the capital, it reached 4.2%.

TABLE OF CONTENTSCHAPTER 3 | THE ECONOMIC AND POLITICAL CRISIS, according to FecomercioSP

42

¹ ACCORDING TO PRICES IN MARCH 2016. SOURCE: FECOMERCIOSP, EBIT

SOURCE: FECOMERCIOSP, EBIT

REAL E-COMMERCE SALES IN REGIONS OF THE STATE OF SÃO PAULO (R$ MILLION¹): 1Q16

REAL E-COMMERCE SALES IN REGIONS OF THE STATE OF SÃO PAULO (R$¹): 1Q16 X 1Q15

BAURU

ARAÇATUBA

RIBEIRÃO PRETO

GUARULHOS

GUARULHOS

TAUBATÉ

ARAÇATUBA

BAURU

ARARAQUARA

MARÍLIA

LITORAL

ESTADO DE SÃO PAULO

TAUBATÉ

SOROCABA

CAMPINAS

ABCD

PRESIDENTE PRUDENTE

PRESIDENTE PRUDENTE

R$ MILLION

MARÍLIA

RIBEIRÃO PRETO

SÃO JOSÉ DO RIO PRETO

SÃO JOSÉ DO RIO PRETO

LITORAL

SOROCABA

ARARAQUARA

JUNDIAÍ

CAPITAL

OSASCO

CAMPINAS

CAPITAL

OSASCO

ABCD

JUNDIAÍ

250

-25%-30%-35%

750

-15%

1250

-5%

500

-20%

1000

-10%

1500

5%

0

0%

1,312

197

154

79

260

174

94

50

333

185

140

71

257

156

92

44

1.8

0.4

-4.1

-10.4

-17.0

-1.3

-5.8

-13.3

-19.4

-4.5

-11.4

-19.3

-2.7

-7.4

-15.6

-21.6

-30.4

TABLE OF CONTENTSCHAPTER 3 | THE ECONOMIC AND POLITICAL CRISIS, according to FecomercioSP

43

¹ WITH THE AIM OF CREATING AN INDICATOR SIMILAR TO THE NATIONAL ONE, ESTIMATED BY EBIT FOR THE CALCULATION OF SHARE IN RETAIL, THE ACTIVITIES OF VEHICLE DEALERSHIPS, CAR PARTS &ACCESSORIES AND CONSTRUCTION MATERIALS WERE NOT CONSIDERED. SOURCE: FECOMERCIOSP, SEFAZ, EBIT

¹ ACCORDING TO PRICES IN MARCH 2016. SOURCE: FECOMERCIOSP, EBIT

AVERAGE TICKET OF E-COMMERCE IN REGIONS OF THE STATE OF SÃO PAULO (R$¹): 1Q16

E-COMMERCE SHARE IN RETAIL SALES OF THE STATE OF SÃO PAULO¹: 1Q16

PRESIDENTE PRUDENTE

PRESIDENTE PRUDENTE

GUARULHOS

BAURU

ESTADO DE SÃO PAULO

RIBEIRÃO PRETO

SÃO JOSÉ DO RIO PRETO

CAPITAL

SOROCABA

GUARULHOS

BAURU

ARARAQUARA

MARÍLIA

ARAÇATUBA

LITORAL

CAMPINAS

CAPITAL

TAUBATÉ

OSASCO

SOROCABA

RIBEIRÃO PRETO

RIBEIRÃO PRETO

JUNDIAÍ

ESTADO DE SÃO PAULO

ARAÇATUBA

OSASCO

ARARAQUARA

LITORAL

TAUBATÉ

ABCD

CAMPINAS

JUNDIAÍ

R$ BRAZILIAN REAIS

MARÍLIA

ABCD

1%

10050

3%

200

5%

300 350 400 450

2%

150

4%

250 500

0%

0

472.97

405.87

393.24

377.66

428.91

400.70

386.40

374.81

470.39

404.82

386.45

375.89

413.47

395.78

379.36

365.32

339.71

4.5

3.4

3.0

2.6

3.8

3.2

2.9

2.4

4.2

3.3

2.9

2.6

3.8

3.0

2.7

2.3

2.2

TABLE OF CONTENTSCHAPTER 3 | THE ECONOMIC AND POLITICAL CRISIS, according to FecomercioSP

44

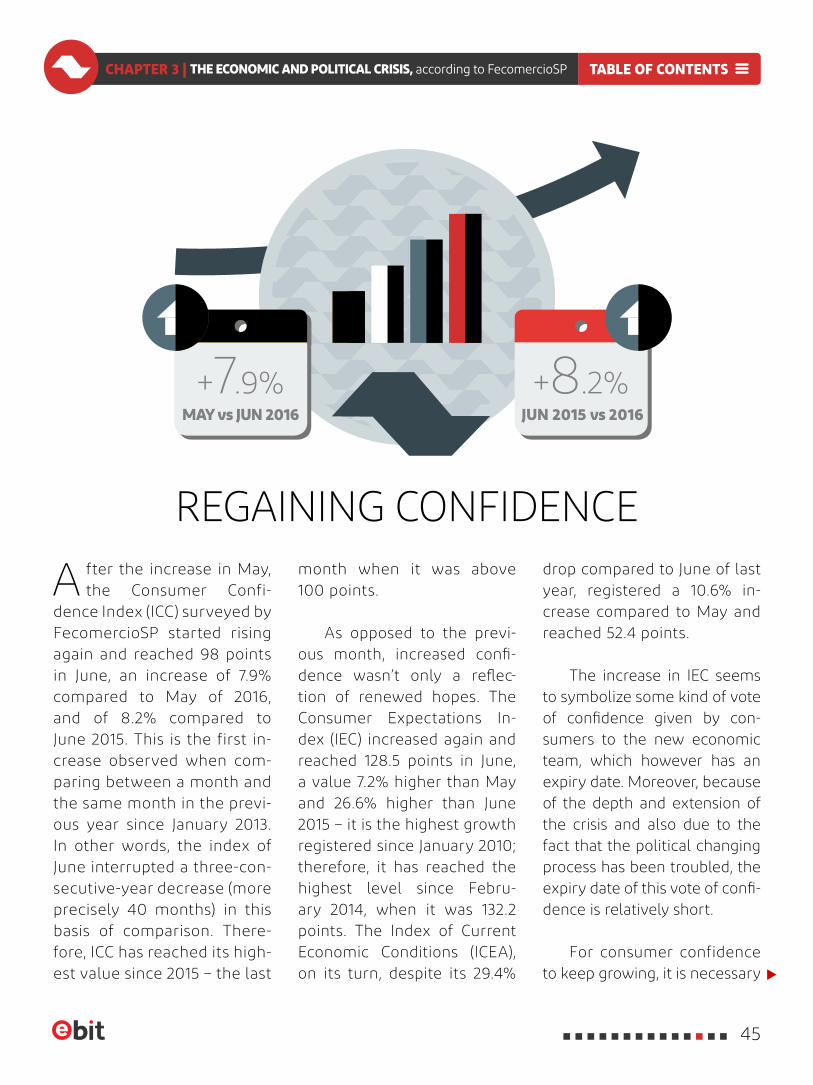

A fter the increase in May, the Consumer Confi-

dence Index (ICC) surveyed by FecomercioSP started rising again and reached 98 points in June, an increase of 7.9% compared to May of 2016, and of 8.2% compared to June 2015. This is the first in-crease observed when com-paring between a month and the same month in the previ-ous year since January 2013. In other words, the index of June interrupted a three-con-secutive-year decrease (more precisely 40 months) in this basis of comparison. There-fore, ICC has reached its high-est value since 2015 – the last

month when it was above 100 points.

As opposed to the previ-ous month, increased confi-dence wasn’t only a reflec-tion of renewed hopes. The Consumer Expectations In-dex (IEC) increased again and reached 128.5 points in June, a value 7.2% higher than May and 26.6% higher than June 2015 – it is the highest growth registered since January 2010; therefore, it has reached the highest level since Febru-ary 2014, when it was 132.2 points. The Index of Current Economic Conditions (ICEA), on its turn, despite its 29.4%

REGAINING CONFIDENCEdrop compared to June of last year, registered a 10.6% in-crease compared to May and reached 52.4 points.

The increase in IEC seems to symbolize some kind of vote of confidence given by con-sumers to the new economic team, which however has an expiry date. Moreover, because of the depth and extension of the crisis and also due to the fact that the political changing process has been troubled, the expiry date of this vote of confi-dence is relatively short.

For consumer confidence to keep growing, it is necessary

MAY vs JUN 2016

+7.9%JUN 2015 vs 2016

+8.2%

TABLE OF CONTENTSCHAPTER 3 | THE ECONOMIC AND POLITICAL CRISIS, according to FecomercioSP

45

THE HOUSEHOLD CONSUMPTION INTENTION (ICF),

CALCULATED MONTHLY BY

FECOMERCIOSP, HAS RENOVATED THE MINIMUM

HISTORICAL VALUE AND REACHED

63 POINTS IN JUNE, A 0.9% FALL

COMPARED TO MAY

that some kind of economic policy is effectively delivered by the Government, such as structural reforms, adjust-ments public accounts with cut in costs – and not with increased taxes –, and the approval of an expenditure ceiling in the public sector and privatizations.

The measures an-

nounced so far and the speed

with which they have been announced seem to have encouraged consumers. However, if this initial momentum is not confirmed by changes and effective approvals, consumers might be discouraged again, thus undermining the expected resumption of consumption.

Improved confidence, however, hasn't influenced overall retail sales in the State of São Paulo, yet; they registered a fall on Mother's Day (May) and Valentine's Day (June) – the two major commerce dates in the first half of the year. In fact, despite the growth in the expectation indicator, consumers are still struggling with high inflation, high interests, and increased unemployment, which affect their financial situation, and consequently, their perception of current conditions. Therefore, the household consumption intention (ICF), monthly calculated by FecomercioSP, repeated the minimum historical value and reached 63 points in June, 0.9% lower than May and 22.9% lower than June 2015.

The assessment of the level of "current consumption", one of the seven items that

comprise ICF, remained at 35.2 points, the same value of May, the lowest level in the historical series. Compared to June 2015, this value is 37.4% lower. It also is the item with the lowest score among the seven items researched. The decrease in consumption level has directly reflected in retail sales, which have an accumulated fall of 6% over a year in the State of São Paulo. There are still no indications of a recovery of the sector in the short term: the intention to take on debts is still low – despite the slight increase in June – and the analysis of this moment for durable items, another component of ICF, repeated the historical minimum value in June by reaching 38.2 points, 4.2% lower than May and 32.1% lower than June 2015. It is the item with the second lowest score among the seven items researched.

Items "current revenue" and "credit access" also re-peated their minimum values in June. The former reached 69.6 points – a drop of 4.7% compared to May 2016 and of 28.7% compared to June 2015 – while the latter remained at 62.3 points – 3.5% lower than May 2016 and 28.7% lower than June 2015.

TABLE OF CONTENTSCHAPTER 3 | THE ECONOMIC AND POLITICAL CRISIS, according to FecomercioSP

46

THE END OF THE YEAR MIGHT BE BETTER

FOR RETAIL THAN ITS BEGINNING, WITH

BETTER SALES IN CHRISTMAS COMPARED

TO THIS DATE IN 2015

BETTER PERSPECTIVES

T he perception of consumers regarding current jobs has reached 87.6 points,

practically the same as May, when it was 87.4 points, but 17.4% lower than June 2015.

If the assessment of item "current jobs" was practically stable in the monthly comparison, the indicator of "professional perspective" increased 1.5% and reached 97.6 points. With improved "professional perspective", "consumption perspective" also improved: this item reached 50.4 points, 3.9% higher than May.

Data aren't as encouraging, yet, since they generally indicate dissatisfaction of households regarding consumption con-ditions. On the other hand, there was a visible improvement in perspectives, in line with ICC data. For expectations to turn into increased sales, however, consump-tion conditions must improve effectively, with price stability, labor market stability, and reduced interest rates, which will only come with an effective tax adjustment and the announcement of measures to stimulate private investments.

However, if the trend towards improving expectations is consolidated, the end of the year might be better for retail than its beginning, with better sales

in Christmas compared to this date in 2015. Still facing many uncertainties, consumers are conservative; however, they tend to gradually return to stores as a less pessimistic scenario unfolds. Consumers who only buy indispensable items today tend to resume their more ambitious plans for consumption when regaining confidence, in face of a less gloomy scenario. It is expected that from the second half of the year on, scenario will become clearer and measures for the rationalization of the public sector and the resumption of investments will reflate economy after the greatest economic crisis in the history of our country. Thence, the stakes on a Christmas that symbolizes this resumption of retail sales.

TABLE OF CONTENTSCHAPTER 3 | THE ECONOMIC AND POLITICAL CRISIS, according to FecomercioSP

47

FIPE/BUSCAPÉ INDEX

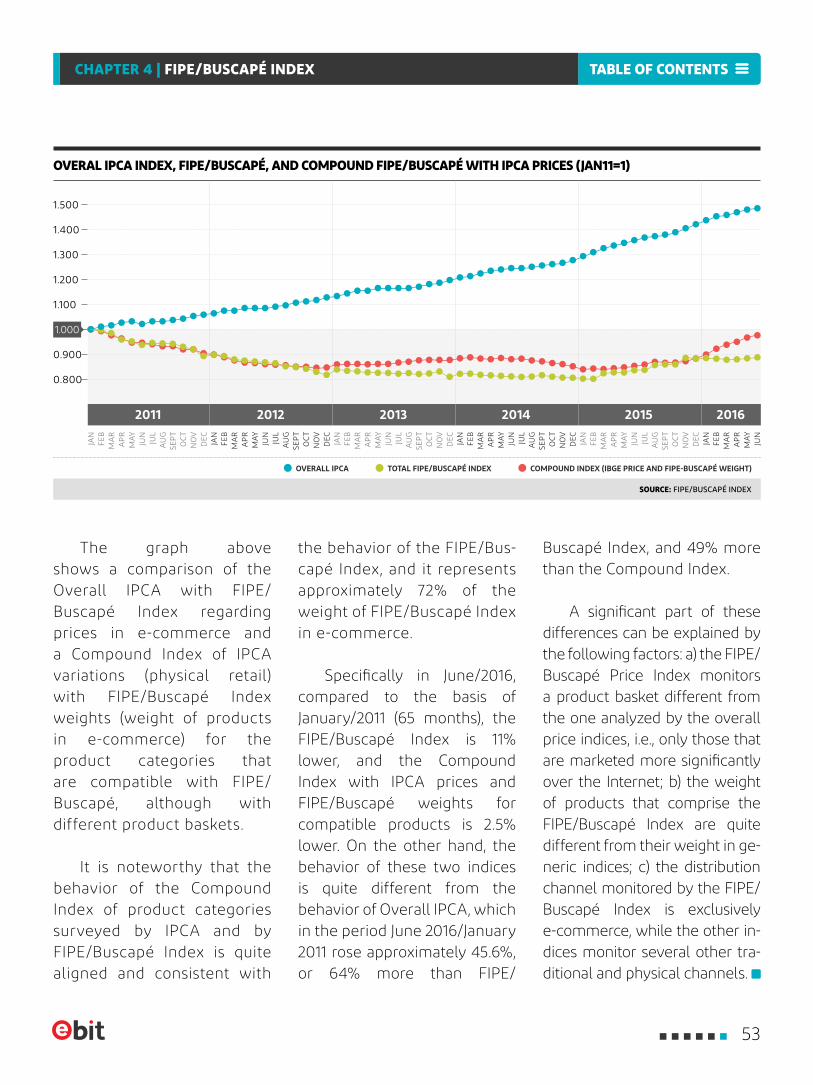

The FIPE/Buscape price index calculation is under the responsibility of the Economic

Researches Foundation Institute, represented by Prof. Sergio Crispim

CHAPTER 4

48

MONTHLY EVOLUTION OF THE FIPE/BUSCAPÉ INDEX

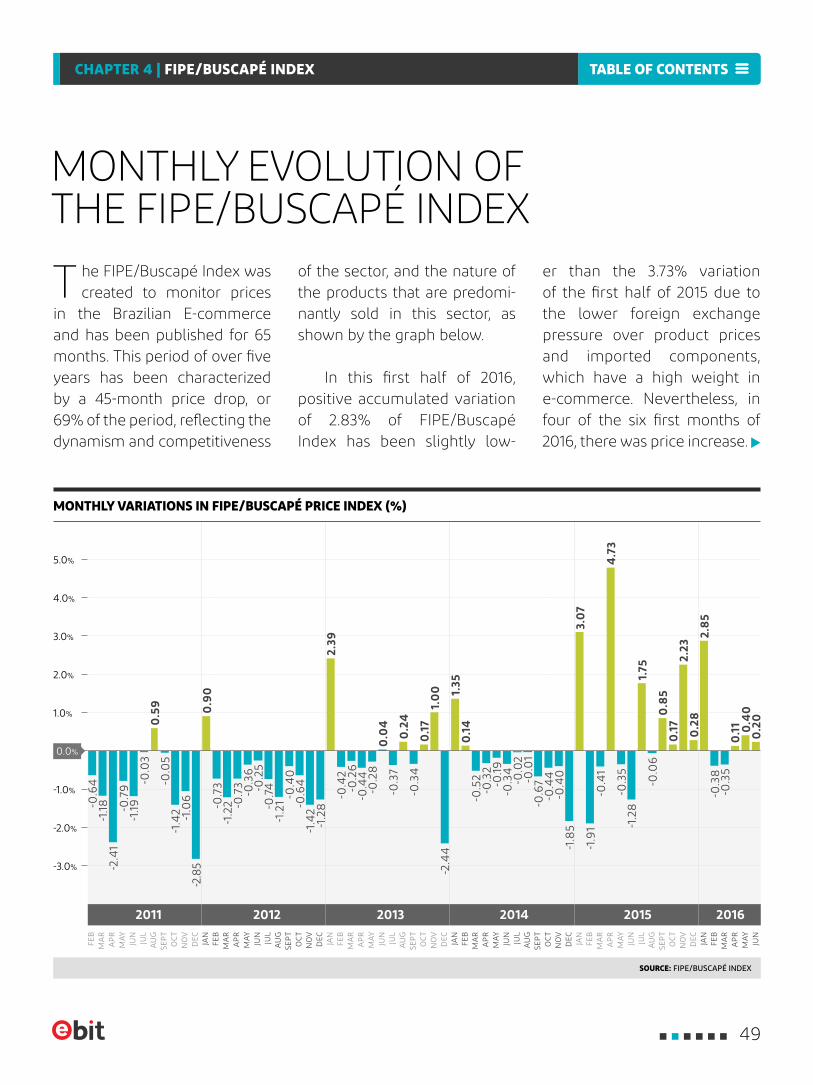

T he FIPE/Buscapé Index was created to monitor prices

in the Brazilian E-commerce and has been published for 65 months. This period of over five years has been characterized by a 45-month price drop, or 69% of the period, reflecting the dynamism and competitiveness

of the sector, and the nature of the products that are predomi- nantly sold in this sector, as shown by the graph below.

In this first half of 2016, positive accumulated variation of 2.83% of FIPE/Buscapé Index has been slightly low-

er than the 3.73% variation of the first half of 2015 due to the lower foreign exchange pressure over product prices and imported components, which have a high weight in e-commerce. Nevertheless, in four of the six first months of 2016, there was price increase.

MONTHLY VARIATIONS IN FIPE/BUSCAPÉ PRICE INDEX (%)

SOURCE: FIPE/BUSCAPÉ INDEX

-2.0%

-3.0%

0.0%

2.0%

5.0%

-1.0%

1.0%

4.0%

3.0%

DEC

FEB

JUN

AP

R

AU

G

MA

R

JUL

NO

VO

CT

MA

Y

SEP

T

JAN

FEB

MA

R

JAN

JUN

JUL

OC

T

AP

R

AU

G

DEC

NO

V

MA

Y

SEP

T

FEB

JUN

OC

T

AP

R

AU

G

DEC

MA

R

JUL

NO

V

MA

Y

SEP

T

JAN

FEB

JUN

AP

RM

AR

MA

Y

JAN

FEB

JUN

OC

T

AP

R

AU

G

DEC

MA

R

JUL

NO

V

MA

Y

SEP

T

JAN

FEB

JUN

OC

T

AP

R

AU

G

DEC

MA

R

JUL

NO

V

MA

Y

SEP

T

2011 2012 2013 2014 20162015

-0.6

4

-1.19

-0.3

6

-0.19

-0.2

8

-0.3

5

-2.4

1

-1.2

2 -0.5

2

-0.2

6

-0.4

1

-0.7

4 -0.0

2

-0.3

7

-1.18 -0

.73

-0.4

2

-1.9

1

-0.0

3

-0.2

5

-0.3

4

-1.2

8-0.7

9

-0.7

3 -0.3

2

-0.4

4-0.0

5

-1.2

1

-0.0

1

-0.0

6

-0.3

8-0

.35

-1.4

2

-0.4

0

-0.6

7

-0.3

4

-1.0

6 -0.6

4

-0.4

4

-2.8

5

-1.4

2

-0.4

0

-1.2

8

-1.8

5

-2.4

4

4.7

3

0.9

0 1.35

2.39

3.0

7

0.5

9

1.75

0.1

4

0.0

4

0.2

4 0.8

5

0.1

7

2.8

5

1.0

0

2.23

0.2

8

0.1

7

0.1

1 0.4

00

.20

TABLE OF CONTENTSCHAPTER 4 | FIPE/BUSCAPÉ INDEX

49

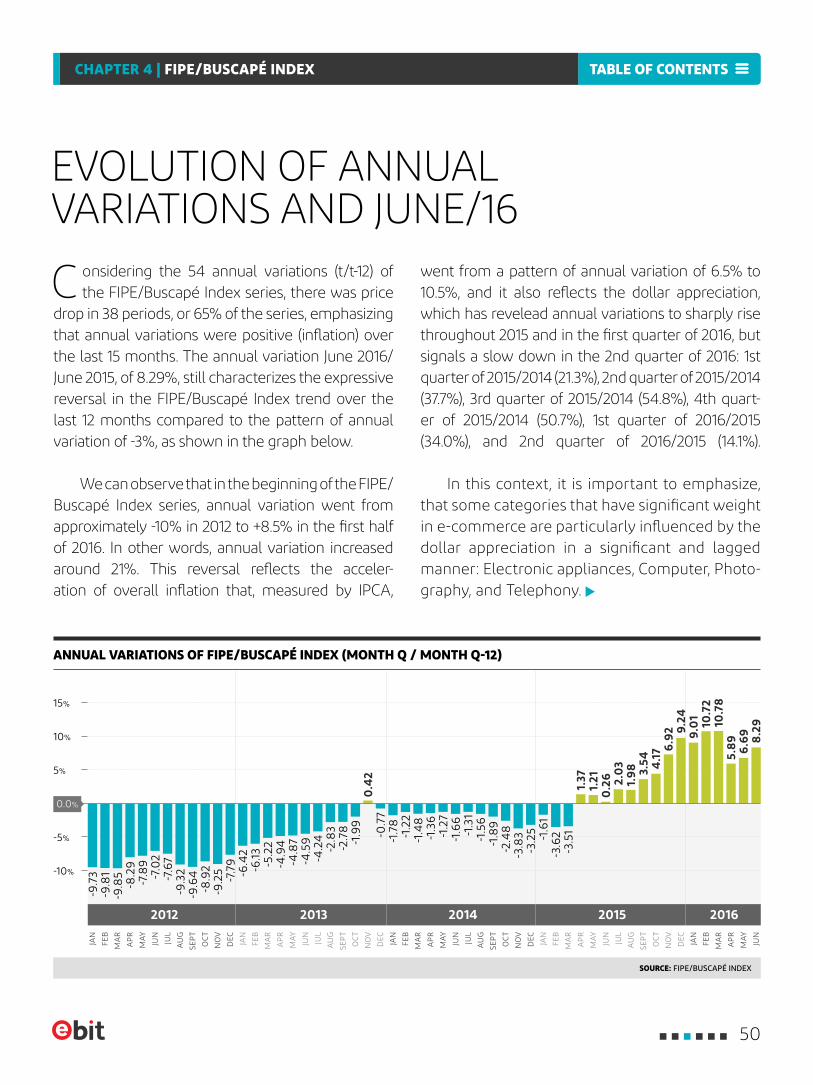

C onsidering the 54 annual variations (t/t-12) of the FIPE/Buscapé Index series, there was price

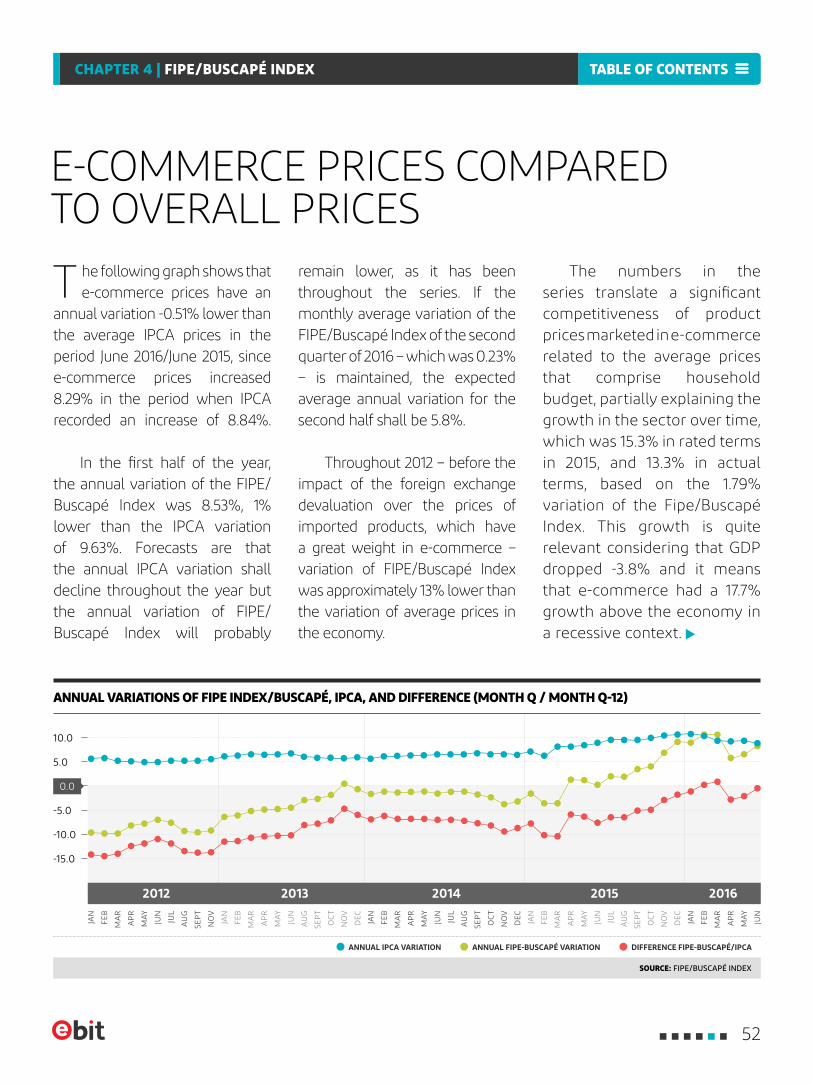

drop in 38 periods, or 65% of the series, emphasizing that annual variations were positive (inflation) over the last 15 months. The annual variation June 2016/June 2015, of 8.29%, still characterizes the expressive reversal in the FIPE/Buscapé Index trend over the last 12 months compared to the pattern of annual variation of -3%, as shown in the graph below.

We can observe that in the beginning of the FIPE/Buscapé Index series, annual variation went from approximately -10% in 2012 to +8.5% in the first half of 2016. In other words, annual variation increased around 21%. This reversal reflects the acceler- ation of overall inflation that, measured by IPCA,

went from a pattern of annual variation of 6.5% to 10.5%, and it also reflects the dollar appreciation, which has revelead annual variations to sharply rise throughout 2015 and in the first quarter of 2016, but signals a slow down in the 2nd quarter of 2016: 1st quarter of 2015/2014 (21.3%), 2nd quarter of 2015/2014 (37.7%), 3rd quarter of 2015/2014 (54.8%), 4th quart-er of 2015/2014 (50.7%), 1st quarter of 2016/2015 (34.0%), and 2nd quarter of 2016/2015 (14.1%).

In this context, it is important to emphasize, that some categories that have significant weight in e-commerce are particularly influenced by the dollar appreciation in a significant and lagged manner: Electronic appliances, Computer, Photo- graphy, and Telephony.

EVOLUTION OF ANNUAL VARIATIONS AND JUNE/16

ANNUAL VARIATIONS OF FIPE/BUSCAPÉ INDEX (MONTH Q / MONTH Q-12)

SOURCE: FIPE/BUSCAPÉ INDEX

-5%

-10%

10%

FEB

JUN

AP

R

MA

R

MA

Y

JAN

FEB

JUN

OC

T

AP

R

AU

G

DEC

MA

R

JUL

NO

V