Embed Size (px)

Citation preview

Insurance, what’s next?June 2015

Agenda

2

1. Introduction

2. Move to digital

3. Broker social

4. The challenges

5. More than price

6. Innovation

7. Roadmap

3

Introduction

4

HeathWallace

Creative and user centric cross channel solutions

Effective use of technology to empower clients

Highly scalable and robust delivery methods

Expertise in financial services

______________________

Founded in 2001

Create solutions that offer their customers an immersive, rich and rewarding experience

Joined WPP in 2008

150 people, 8 offices, £12.5million annual turnover

4

5

Move to digital

Share of individuals who purchased insurance policiesor shares online in Great Britain in 2014, by age and gender

Source: Office for National Statistics (UK)

Men

Women

16-24

25-34

35-44

45-54

55-64

65+

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0%

25%

18%

13%

28%

29%

28%

21%

9%

Share of respondents

6

7

Move to digital

• By 2020 Millennials will be the majority generation in the workforce.

• They are incredibly digital averaging 96 hours per week online.

• “Why can’t I just do this online.”

• The challenge will be moving them from the research phase (browsing) into purchase.

• Millennials are prepared to be involved and make an experience work better for them.

8

Leading Sources that Influence Insurance Purchasing Decisions Among UK Millennial Internet Users, March 2015

Note: ages 18-34 who have purchased or plan to purchase insurance Source: Pegasystems and Capgemini, ‘’Born Yesterday: Will Millennials Disrupt the Insurance Industry?’’ conducted by Decode, May 14, 2015

Comparison website

Searching online

Word-of-mouth from friends

Parents' recommendations

51%

48%

27%

24%

% of respondents

9

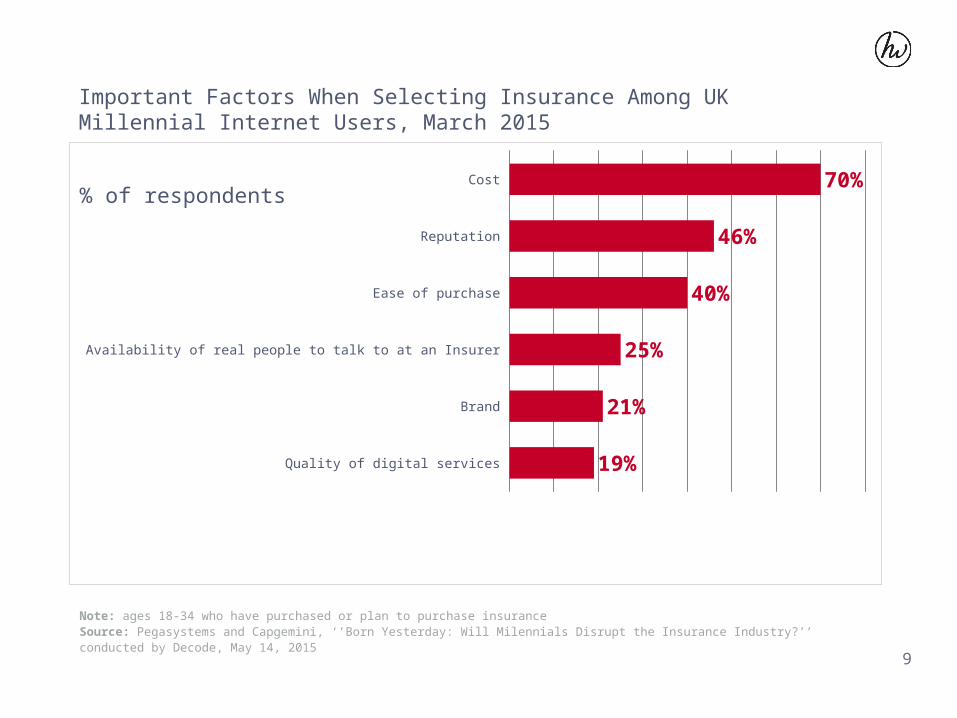

Important Factors When Selecting Insurance Among UKMillennial Internet Users, March 2015

Note: ages 18-34 who have purchased or plan to purchase insurance Source: Pegasystems and Capgemini, ‘’Born Yesterday: Will Milennials Disrupt the Insurance Industry?’’ conducted by Decode, May 14, 2015

Cost

Reputation

Ease of purchase

Availability of real people to talk to at an Insurer

Brand

Quality of digital services

70%

46%

40%

25%

21%

19%

% of respondents

Thank you

www.heathwallace.comp @heathwallace