Embed Size (px)

Citation preview

CHALLENGES FACED BY MODERN INDIAN RETAILERS

By

SRIRAM S

YAMINI ASP

YUVASRI G

PROJECT GUIDE

Dr. P. MOHAN SUYAMBURAJPROFESSOR

THIAGARAJAR SCHOOL OF MANAGEMENTMADURAI-625005

TABLE OF CONTENTS

CH.NO.

CONTENTSPAGENO.

1 INTRODUCTION 32 CURRENT SCENARIO OF INDIAN RETAIL MARKET 43 IMPACT ON MANUFACTURERS 44 THE RELATIONSHIP BETWEEN RETAILERS AND SUPPLIERS 5

4.1 WHAT IS BUYER POWER? 54.2 ABUSES OF BUYER POWER 64.3 WHAT DO THESE ABUSES IMPLY FOR SUPPLIERS? 7

4.3.1 THE RISE OF RETAILERS’ OWN BRANDS AND THE LOSS OF INDEPENDENT BRANDS 84.3.2 LOW PRICES, UNCERTAINTY AND SUSTAINABILITY OF SUPPLY 10

4.4 WHAT DO THESE ABUSES IMPLY FOR CONSUMERS? 134.4.1 THE CONSUMER BENEFITS OF SUPERMARKETS 134.4.2 DETRIMENTS TO CONSUMERS 13

5 CHALLENGES IN RETAIL LOGISTICS 145.1 LOGISTIC TASK 165.2 CARELESSNESS AT MOTHERCARE LEAVES CUPBOARD BARE 175.3 FUTURE CHALLENGES 195.4 TESCO.COM: DELIVERING HOME SHOPPING 21

6 RETAIL LOGISTICS 226.1 LOGISTICS FUNCTIONS 236.2 OVERCOMING OBSTACLES WITH DROP SHIPPING 24

6.2.1 B2B TO INTEGRATION 256.2.2 DATA, BUSINESS, INTEGRATION FLOW 266.2.3 COLLABORATORS NOT CUSTOMERS 26

6.3 FOUNDATIONAL FACTORS 286.4 FOCUS ON THE CONSUMER 29

7 CONCLUSION 298 REFERENCES 30

2

1. INTRODUCTION

India is the second fastest growing economy in the world. It is third largest economy in

the world in terms of GDP and fourth largest economy in terms of Purchasing Power Parity.

India presents a huge opportunity to the world at age, to use as a hub. Standing on the threshold

of a retail revolution and witnessing a fast changing retail landscape, India is all set to experience

the phenomenon of global village. India is the “promised land” for global brands and Indian

retailers A “Vibrant economy”. India tops in the list of emerging market for global retailer and

India’s retail sector is expanding and modernizing rapidly in line with India’s economic growth.

The future is promising; the market is growing, government policies are becoming more

favorable and emerging technologies are facilitating operations.

Retailing in India is gradually inching its way toward becoming the next boom industry.

The whole concept of shopping has altered in terms of format and consumer buying behavior,

ushering in a revolution in shopping in India. Modern retail has entered India as seen in

sprawling shopping centers, multi-storied malls and huge complexes offer shopping,

entertainment and food all under one roof. The Indian retailing sector is at an inflexion point

where the growth of organized retailing and growth in the consumption by the Indian population

is going to take a higher growth trajectory. The Indian population is witnessing a significant

change in its demographics. A large young working population with median age of 24 years,

nuclear families in urban areas, along with increasing working-women population and emerging

opportunities in the services sector are going to be the key growth drivers of the retail sector in

India. Retailing in India is evolving rapidly, with consumer spending growing by unprecedented

rates and with increasing no of global players investing in this sector. Organized retail in India is

undergoing a metamorphosis and is expected to scale up to meet global standards over the next

five years.

India’s retail market has experienced enormous growth over the past decade. The most

significant period of growth for the sector was between year 2000 & 2006, when the sector

revenues increased by about 93.5% translating to an average annual growth of 13.3%.The sectors

growth was partly a reflection of the impressive Indian economic growth and overall rise in

income level of consumers. Apparels and consumer durables are the fastest growing vertical in

the retail sector.

3

Mobile phone as a product category has witnessed the highest growth in the consumer

demand amongst all retail products offering, with increasing penetration of telecommunication in

towns and villages. The telecommunication sector has been adding on an average 5 million new

users every month. The other product categories are gaining traction predominantly in the urban

areas and emerging cities, with increasing average income and spending power of young urban

India.

India remained as the most attractive market for third year in a row in an index prepared

by At Kearney. Retail sector is the largest contributing sector to country’s GDP.

2. CURRENT SCENARIO OF INDIAN RETAIL MARKET

The size of Indian retail industry is more than US $350 billion but it is highly

unorganized. The organized sector has started developing in the past few years. Many

International brands have entered the market. With the growth in organized retailing,

unorganized retailers are fast changing their business models. According to study conducted by

ICRIER, total retail business in India will grow at 13% annually, from US $322 billion in 2006-

07 to US $590 billion in 2011-12 and further US $1 trillion by 2016-17.

3. IMPACT ON MANUFACTURERS

The impact on manufacturers are:

(i) Large manufacturers have started feeling the competitive impact of organized retail through

price and payment pressures.

(ii) Entry of organized retail is transforming the logistics industry. This will create significant

positive externalities across the economy.

(iii) Manufacturers have started building and responding their brand strength and set up

dedicated teams to deal with modern retailers.

Thus, the overall impact of organized sector on other sectors is positive. According to a

report prepared by FCRIER, unorganized retailers in the vicinity of organized retailers

experienced a decline in sales and profit in initial years of the entry of organized sectors. The

adverse impact, however, weakens over time.

4

4. THE RELATIONSHIP BETWEEN RETAILERS AND SUPPLIERS

4.1 WHAT IS BUYER POWER?

Buyer power is essentially the ability of a buyer to obtain more favorable buying terms

than would be possible in a fully-competitive market. Most people will understand that, in most

traded goods markets, bigger buying volumes command better buying prices, but what explains

the ability of large supermarkets to go on extracting better terms from suppliers after economies

of scale have been exhausted? The explanation is abuse of buyer power. Supermarkets’ buyer

power arises from their retailer power: often commanding upwards of 60 percent of domestic

grocery sales,1 supermarkets collectively are of an importance to suppliers which enables them

effectively to determine what will – and will not – be stocked, and on what terms: sources,

quantity, quality, delivery schedules, packaging, returns policy, and above all, price and payment

conditions.

There are, of course, other actors in grocery supply chains, some very large, such as

Procter & Gamble, Nestlé, and Unilever. But even for these, the dominance of supermarkets is

daunting, and the imbalance of bargaining power striking. Except through supermarkets, brand

owners large or small have only limited access to end consumers. Producers of non-branded

goods, most notably agricultural producers, have even less access and less ability to bargain for

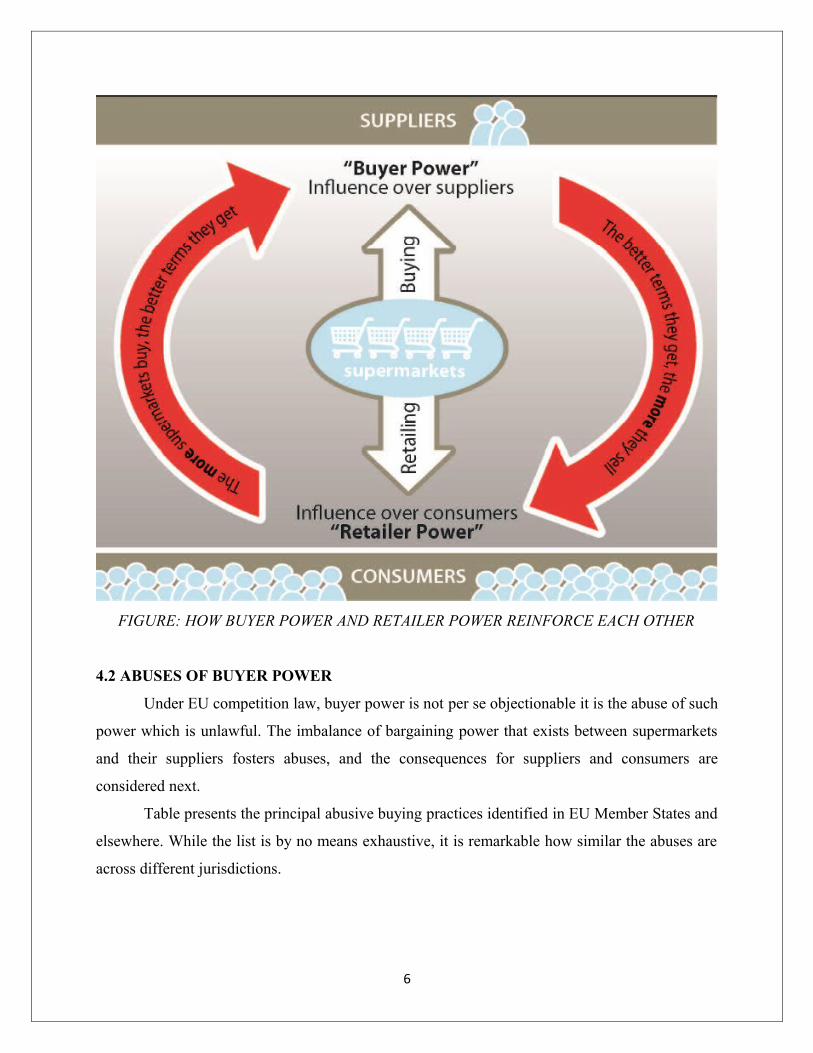

it. Supermarkets’ buyer power and retailer power are now mutually reinforcing. As their retail

market share increases, they are able to secure ever better deals from their suppliers. And, as

buying prices fall, retail prices fall too, giving them yet more market share. Buyer power would

not exist without retailer power, and vice versa. Figure below illustrates the circular relationship.

5

FIGURE: HOW BUYER POWER AND RETAILER POWER REINFORCE EACH OTHER

4.2 ABUSES OF BUYER POWER

Under EU competition law, buyer power is not per se objectionable it is the abuse of such

power which is unlawful. The imbalance of bargaining power that exists between supermarkets

and their suppliers fosters abuses, and the consequences for suppliers and consumers are

considered next.

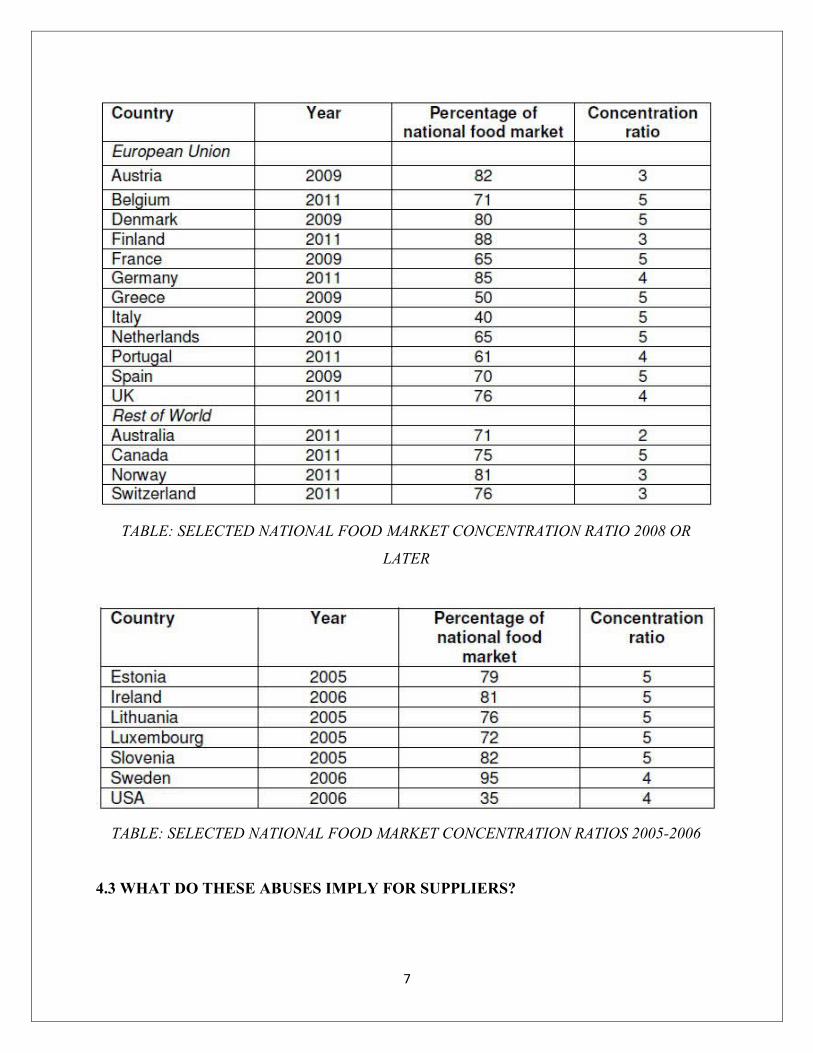

Table presents the principal abusive buying practices identified in EU Member States and

elsewhere. While the list is by no means exhaustive, it is remarkable how similar the abuses are

across different jurisdictions.

6

TABLE: SELECTED NATIONAL FOOD MARKET CONCENTRATION RATIO 2008 OR

LATER

TABLE: SELECTED NATIONAL FOOD MARKET CONCENTRATION RATIOS 2005-2006

4.3 WHAT DO THESE ABUSES IMPLY FOR SUPPLIERS?

7

It would not of course be reasonable to assert that supermarkets have inflicted only abuse

on suppliers: there have been benefits too. The principal gain that supermarkets have brought to

suppliers is volume.

Also, there can be no question that the demands of supermarkets have in several respects

forced suppliers to raise their game: the quality of their output, the variety of what they produce,

and the condition in which it reaches the end user. However, as expenditure by consumers on

food has increased, so has the share of that expenditure taken by supermarkets. Nor is it

reasonable to suggest that only supermarkets exert buyer power: the largest brand owners,

themselves multi-national corporations, almost certainly possess buyer power, as do a number of

very large European buying groups which act on behalf of major grocery retailers. But what

makes supermarkets distinctive in the exercise of buyer power is the power they also exercise as

retailers.

The question that this paper considers is not whether supermarkets are a good thing or not

but whether, as gate-keepers controlling both suppliers and consumers, they misuse their power

over both groups. The conclusion drawn here is not only that they can, but that they do.

4.3.1 THE RISE OF RETAILERS’ OWN BRANDS AND THE LOSS OF INDEPENDENT

BRANDS

It is unsurprising that, as supermarkets acquired increasing presence in the minds of

consumers and economic power in grocery markets, they began to develop their own brands as a

means of bolstering market share and profits. This has given retailers a new role – in addition to

their traditional role as purchasers, they have become direct competitors to their suppliers.

To begin with, retailers’ own brand goods6 were generally low-price, basic versions of

commodities such as (in the case of food) cereals or tinned vegetables. The rather crude

packaging applied to the early retailers’ own brands served to emphasize the cheap and cheerful

nature of the products. Over time, however, own brands have extended outwards to cover a much

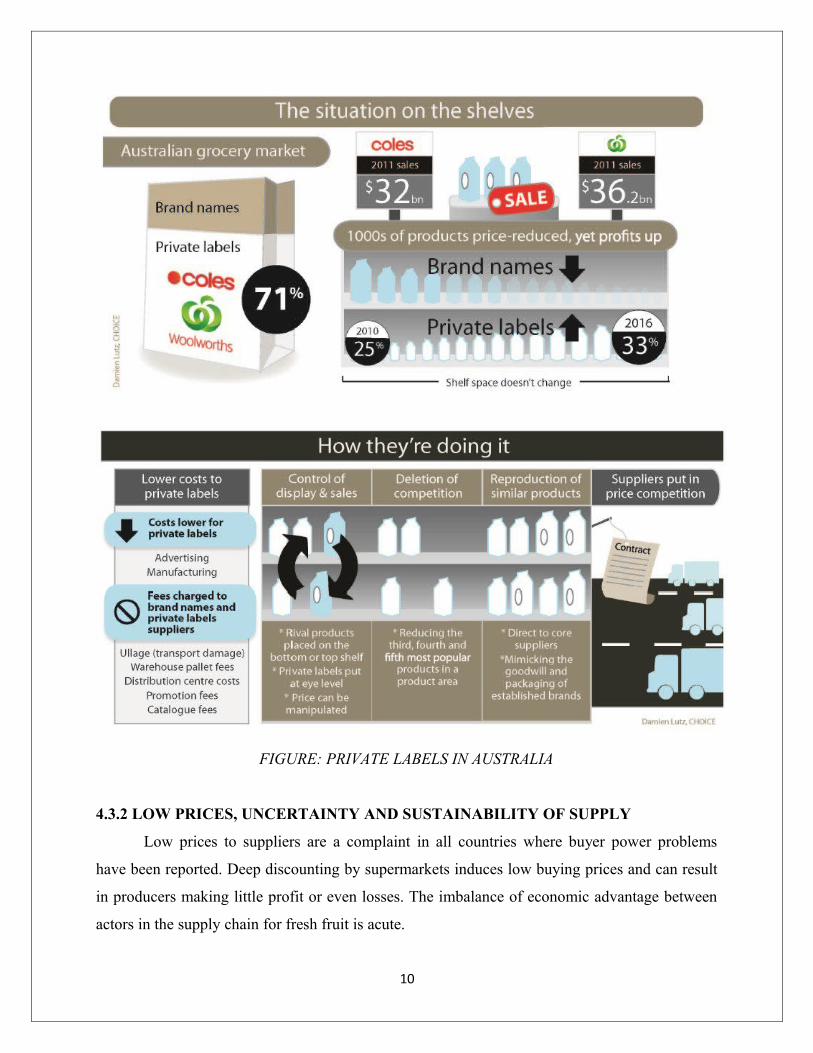

wider range of goods, and upwards into premium segments. In Australia, the share of

supermarket food sales occupied by retailers’ own brands is now estimated at 25%. In the UK, it

is estimated by the British Brands Group as double that.

Given that shelf space is finite, branded goods are being increasingly squeezed out by

retailers’ own brands. It is profitable twice over for the supermarkets to do this. First, the

8

promotion of their own brand products can be carried as part of their corporate promotional

overhead, which implies substantial savings of indirect cost.

Second, the closer control that supermarkets have over their own brand suppliers means

that they can often achieve lower direct product costs too. Yet, as retailers’ own brands have

moved up market into premium and prepared foods, the prices they can command are often not

far below those of independent, established brand owners.

In Australia, the loss of brands and rise of retailers’ own brands has been

comprehensively documented by CHOICE, a leading consumer watchdog. The evidence that

CHOICE provides suggests that the removal of branded goods from supermarket shelves and

their replacement by retailers’ own brands is driven by the commercial interests of supermarkets

rather than consumer choice:

“Many small suppliers – and even large ones such as Heinz and Coca Cola – are concerned

about the pressure they face in the fight for [this] finite shelf space. Kevin [a branded goods

manufacturer] argues his product was cut not because he wasn’t innovating, but because Coles

set him up to fail. “Coles told us it’s because our sales weren’t achieving targets. But that’s

because they wouldn’t put us in catalogues, we got no shelf space, we were hidden behind a

column and they refused to let us have promotions, and that made it impossible for us to compete

with the big boys. We suspect what they were really doing was targeting the products they

wanted to delete so that it would be easier to justify in six to eight months’ time.”

Over at Woolworths, brands are also being cut. Mark [another branded goods

manufacturer] had his organic product deleted directly after Woolworths acquired the Macro

label. Following steady sales for three years, Woolworths’ category buyer told him there was

only room for one organic label – Macro, its own. This decision saw his yearly sales halved.

Potentially more damaging is the practice by supermarkets of demanding to know the

future product plans of branded suppliers. When these are shared with retailers’ own brand

manufacturers in order that retailers may launch own brand products simultaneously with or

ahead of the branded goods, it undermines the IP rights of the branded suppliers and damages

their profitability. The consumer interest in retailer own brands is considered later in this paper.

9

FIGURE: PRIVATE LABELS IN AUSTRALIA

4.3.2 LOW PRICES, UNCERTAINTY AND SUSTAINABILITY OF SUPPLY

Low prices to suppliers are a complaint in all countries where buyer power problems

have been reported. Deep discounting by supermarkets induces low buying prices and can result

in producers making little profit or even losses. The imbalance of economic advantage between

actors in the supply chain for fresh fruit is acute.

10

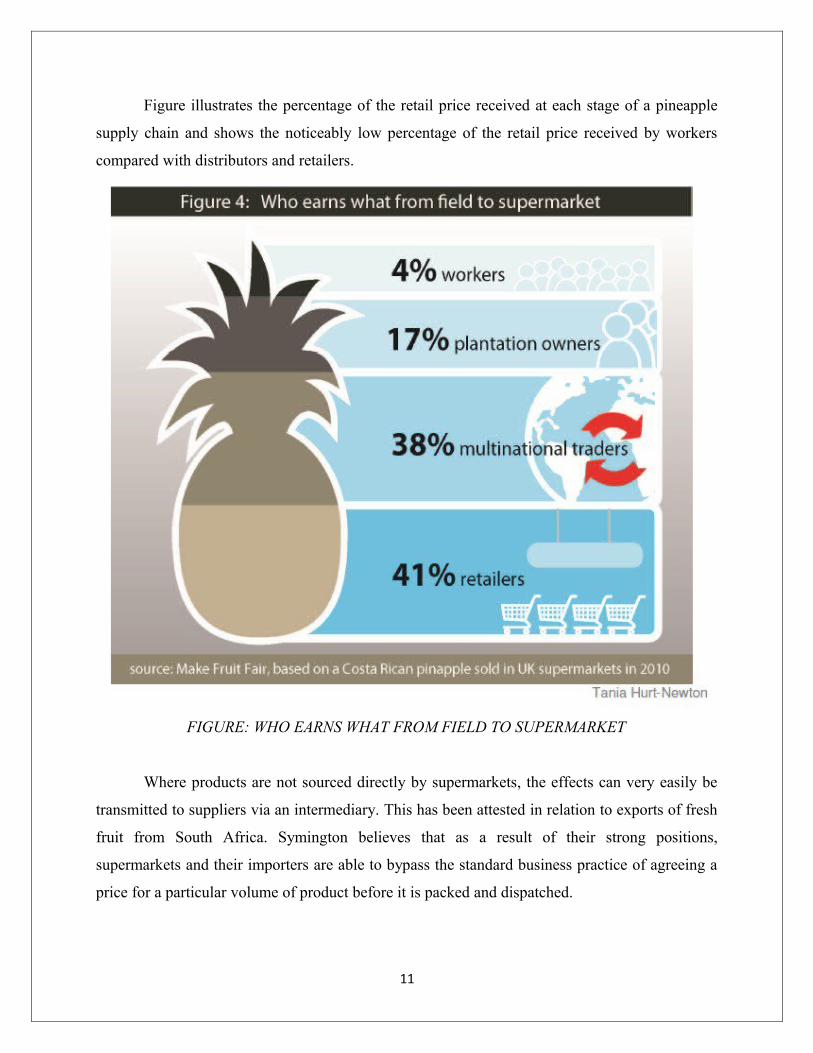

Figure illustrates the percentage of the retail price received at each stage of a pineapple

supply chain and shows the noticeably low percentage of the retail price received by workers

compared with distributors and retailers.

FIGURE: WHO EARNS WHAT FROM FIELD TO SUPERMARKET

Where products are not sourced directly by supermarkets, the effects can very easily be

transmitted to suppliers via an intermediary. This has been attested in relation to exports of fresh

fruit from South Africa. Symington believes that as a result of their strong positions,

supermarkets and their importers are able to bypass the standard business practice of agreeing a

price for a particular volume of product before it is packed and dispatched.

11

Instead the risk is passed on to the supplier (who might not find out what price has been

achieved until after the product is sold) and the supermarket has the flexibility to pursue price

wars and unscheduled promotions without having to bear the cost itself.

Over-procurement to ensure that shelves are covered is described as common, as are

complaints about quality. And it is the supplier, not the supermarket, which will pay the price of

offloading excess supply of a perishable product. In Symington’s view, 11 suppliers cannot

tolerate these practices indefinitely:

Practices that have the potential to create increased uncertainty for suppliers were

identified as particularly significant by the UK Competition Commission in its 2008

report already cited.

Twenty six such practices were described, often involving the transfer of retrospective

(and therefore unexpected) cost and excessive risk to suppliers, undermining their ability

to plan, invest and innovate, ultimately to the detriment of the consumer.

Again, it is important to note that supermarkets are not the only type of organization to be

able to exert buyer power: brand owners, to differing degrees, and major buying groups also

enjoy buyer power. But, to re-emphasize a point already made, supermarkets are distinctive

because of the retailer power that they exert.

There are signs of recognition by retailers and large manufacturers of the need for more

responsible commercial practices – if only to ensure the sustainability of their supply and to

respond to public pressure in domestic markets. An example of a supermarket response is the

Tesco Sustainable Dairy Group, which aims to address issues such as price, uncertainty and the

cost to UK dairy farmers of implementing standards. Although other retailers have also taken

action to address these issues in this industry and elsewhere, what is significant about this

initiative is the inclusion of a price guarantee. The initiative only applies to liquid milk, however,

and there is a long way to go before supermarkets apply these principles throughout their supply

base.

12

4.4 WHAT DO THESE ABUSES IMPLY FOR CONSUMERS?

4.4.1 THE CONSUMER BENEFITS OF SUPERMARKETS

As with suppliers, so with consumers, there is no suggestion that the record of

supermarkets merits only criticism. For several decades past, supermarkets have fuelled, and

have been fuelled by, profound social and demographic changes. For the vast majority of people

in developed market economies it is impossible to imagine modern life without supermarkets:

the convenience of buying substantially all one’s grocery needs under one roof in clean and

pleasant surroundings, from early in the morning to late at night, with ancillary services such as

toilets and cafés, adjacent car parking and/or public transport is irreplaceable. One might argue

that for many the true convenience store is in fact a supermarket.

Supermarkets also claim – though the evidence is mixed – that over the long term they

have reduced the real (i.e. inflation-adjusted) prices of food. Yet, as the market power of

supermarkets has increased, so have the numbers of those who feel that they are not well served

by them: those in rural areas and/or without a car, the old, and, increasingly, those who dislike

the damaging environmental impacts of out-of-town hypermarkets. The British Brands Group

(BBG) 15 submission to the UK Competition Commission’s inquiry of 2006-2008 reported

survey findings that showed that some 26 per cent of the population and 33 per cent of people

older than 16 were not well served by supermarkets. It is unlikely that the UK’s position in these

respects is radically different from those of other large EU Member States: indeed, where the

population density is lower, as it is in France, Germany, Spain and Italy, the prevalence of

problems for people in rural areas may already be worse.

4.4.2 DETRIMENTS TO CONSUMERS

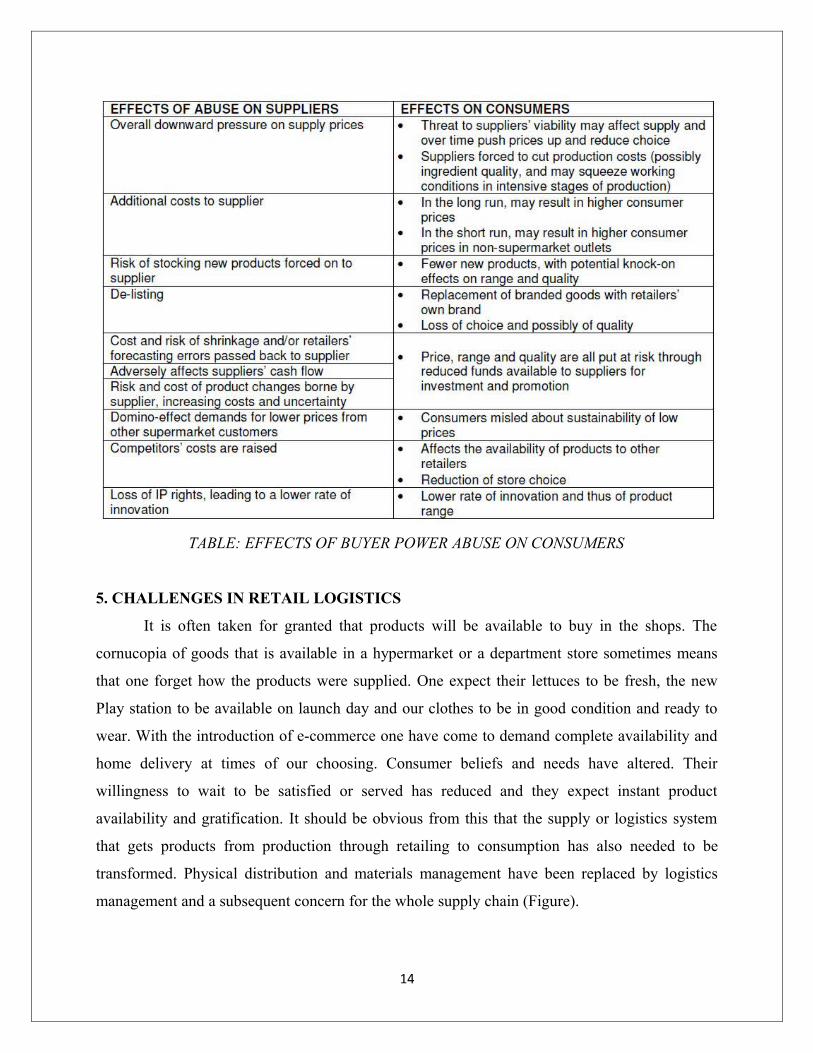

The effects of abuse on suppliers identified in Table are summarized and the subsequent

effects of these on consumers are assessed in Table below. This is followed by a commentary on

the principal issues arising.

13

TABLE: EFFECTS OF BUYER POWER ABUSE ON CONSUMERS

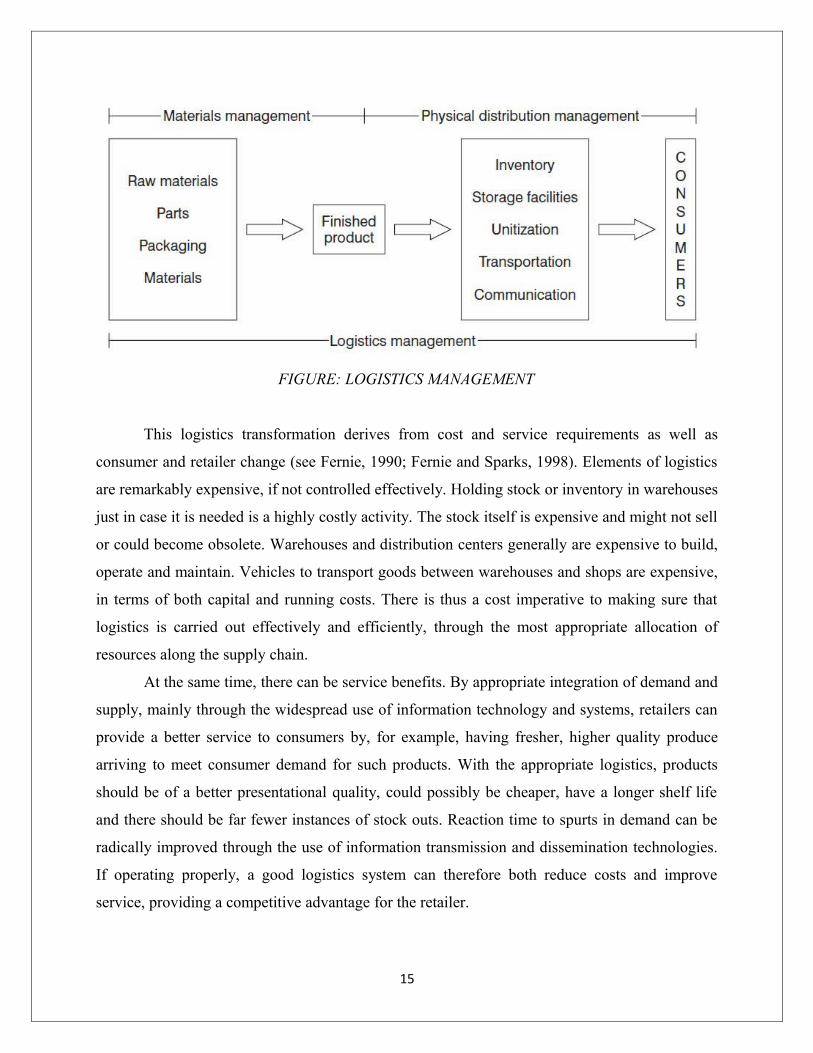

5. CHALLENGES IN RETAIL LOGISTICS

It is often taken for granted that products will be available to buy in the shops. The

cornucopia of goods that is available in a hypermarket or a department store sometimes means

that one forget how the products were supplied. One expect their lettuces to be fresh, the new

Play station to be available on launch day and our clothes to be in good condition and ready to

wear. With the introduction of e-commerce one have come to demand complete availability and

home delivery at times of our choosing. Consumer beliefs and needs have altered. Their

willingness to wait to be satisfied or served has reduced and they expect instant product

availability and gratification. It should be obvious from this that the supply or logistics system

that gets products from production through retailing to consumption has also needed to be

transformed. Physical distribution and materials management have been replaced by logistics

management and a subsequent concern for the whole supply chain (Figure).

14

FIGURE: LOGISTICS MANAGEMENT

This logistics transformation derives from cost and service requirements as well as

consumer and retailer change (see Fernie, 1990; Fernie and Sparks, 1998). Elements of logistics

are remarkably expensive, if not controlled effectively. Holding stock or inventory in warehouses

just in case it is needed is a highly costly activity. The stock itself is expensive and might not sell

or could become obsolete. Warehouses and distribution centers generally are expensive to build,

operate and maintain. Vehicles to transport goods between warehouses and shops are expensive,

in terms of both capital and running costs. There is thus a cost imperative to making sure that

logistics is carried out effectively and efficiently, through the most appropriate allocation of

resources along the supply chain.

At the same time, there can be service benefits. By appropriate integration of demand and

supply, mainly through the widespread use of information technology and systems, retailers can

provide a better service to consumers by, for example, having fresher, higher quality produce

arriving to meet consumer demand for such products. With the appropriate logistics, products

should be of a better presentational quality, could possibly be cheaper, have a longer shelf life

and there should be far fewer instances of stock outs. Reaction time to spurts in demand can be

radically improved through the use of information transmission and dissemination technologies.

If operating properly, a good logistics system can therefore both reduce costs and improve

service, providing a competitive advantage for the retailer.

15

5.1 LOGISTIC TASK

The logistics management task is therefore initially concerned with managing the

components of the ‘logistics mix’. One can identify five components:

Storage facilities

These might be warehouses or distribution centers or simply the stock rooms of retail

stores. Retailers manage these facilities to enable them to keep stock in anticipation of or to react

to, demand for products.

Inventory

All retailers hold stock to some extent. The question for retailers is the amount of stock or

inventory (finished products and/or component parts) that has to be held for each product, and

the location of this stock to meet demand changes.

Transportation

Most products have to be transported in some way at some stage of their journey from

production to consumption. Retailers therefore have to manage a transport operation that might

involve different forms of transport, different sizes of containers and vehicles and the scheduling

and availability of drivers and vehicles.

Unitization and packaging

Consumers generally buy products in small quantities. They sometimes make purchase

decisions based on product presentation and packaging. Retailers are concerned to develop

products that are easy to handle in logistics terms, do not cost too much to package or handle, yet

retain their selling ability on the shelves.

Communications

To get products to where retailers need them, it is necessary to have information, not only

about demand and supply, but also about volumes, stock, prices and movements. Retailers have

thus become increasingly concerned with being able to capture data at appropriate points in the

system and to use that information to have a more efficient and effective logistics operation.

16

5.2 CARELESSNESS AT MOTHERCARE LEAVES CUPBOARD BARE

Sales at Mothercare dived by 6 per cent in three weeks after its move to a new hi-tech

distribution centre caused problems. The children's wear retailer admitted that staff shortcomings

meant its heralded autumn/winter clothing range had languished at the new Northampton shire

warehouse, causing huge stock shortages in its stores.

Chief Executive Chris Martin, who was recruited to turn around the chain, admitted the

setback was ‘exceptionally frustrating’ given that like-for-like sales until this period had been up

about 10 per cent, and that the new range had been well received.

It was doubly frustrating, he said, as management of the Daventry warehouse was sub-

contracted to a third party, Tibbett & Britten. ‘Some of their staff just weren’t doing their job’,

said a source. Tibbett responded by placing a senior director at the building to sort out the

problems and establish a proper flow of stock to the stores.

Asked if he was considering legal action, Mr. Martin said: ‘This is a five year

relationship. We are working it through together.’ He added that a fifth less stock than usual had

been in the shops but stressed that it was ‘now coming through’. In a trading statement Mr.

Martin revealed that sales rose by 9.6 per cent for the 26 weeks to 28 September 2001, with like-

for-like sales up by 7.6 per cent. Brokers at Charterhouse Securities cut their recommendation

from hold to sell after the news, but Seymour Pierce retail analyst Richard Ratner said, ‘If they

sort the warehouse problems out in the next few weeks I won’t be unduly concerned, particularly

as the 2.1 percentage point improvement in margin was better than expected.’ Mothercare

planned to continue with the roll-out of its larger Mothercare World format after Christmas 2001.

Source: Helen Slingsby, Guardian, Tuesday 9 October 2001

It should be clear that all of these elements are interlinked. In the past they were often

managed as functional areas or ‘silos’, and while potentially optimal within each function, the

business as a whole was sub-optimal in logistics terms. More recently the management approach

has been to integrate these logistics tasks and reduce the functional barriers. So, if a retailer gets

good sales data from the checkout system, this can be used in scheduling transport and deciding

levels and locations of stock holding. If the level of inventory can be reduced, perhaps fewer

warehouses are needed.

17

If communications and transport can be linked effectively, a retailer can move from

keeping stock in a warehouse to running a distribution centre which sorts products for immediate

store delivery: that is, approaching a ‘Just-In-Time’ system. Internal integration has therefore

been a major concern.

It should also be clear, however, that retailers are but one part of the supply system.

Retailers are involved in the selling of goods and services to the consumer. For this they draw

upon manufacturers to provide the necessary products. They may outsource certain functions

such as transport and warehousing to specialist logistics services providers.

Retailers therefore have a direct interest in the logistics systems of their suppliers and

other intermediaries. If a retailer is effective, but its suppliers are not, errors and delays in supply

from the manufacturer or logistics services provider will impact the retailer and the retailer ’s

consumers, in terms of either higher prices or stock-outs (no products available on the store

shelves). This was the essence of the problem in the Mothercare example (page 3). If a retailer

can integrate effectively its logistics system with that of its suppliers, such problems may be

minimized.

Much more importantly, however, the entire supply chain can then be optimized and

managed as a single entity. This brings potential advantages of cost reduction and service

enhancement, not only for the retailer, but also for the supplier. It should also mean that products

reach the stores more rapidly, thus better meeting sometimes transient customer demand. In

some instances it may mean the production of products in merchandisable ready units, which

flow through the distribution systems from production to the shop floor without the need for

assembly or disassembly. Such developments clearly require supply chain co-operation and

coordination. We may be describing highly complex and advanced operations here. Retail

suppliers are increasingly spread across the world.

A retailer may have thousands of stores in a number of countries, with tens of thousands

of individual product lines. They may make millions of individual sales per day. Utilizing data to

ensure effective operation amongst retailers, manufacturers, suppliers, logistics services

providers, head office, shops and distribution centers is not straightforward. There is thus always

a tension between overall complexity and the desire for the simplest possible process.

18

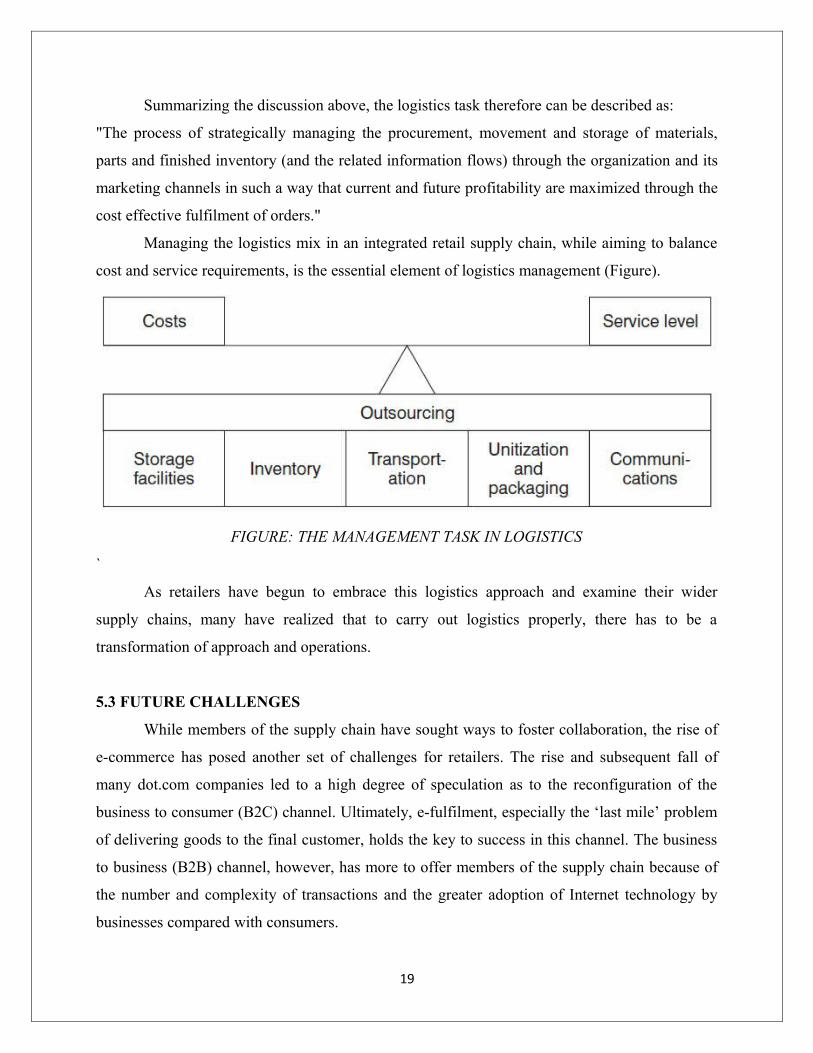

Summarizing the discussion above, the logistics task therefore can be described as:

"The process of strategically managing the procurement, movement and storage of materials,

parts and finished inventory (and the related information flows) through the organization and its

marketing channels in such a way that current and future profitability are maximized through the

cost effective fulfilment of orders."

Managing the logistics mix in an integrated retail supply chain, while aiming to balance

cost and service requirements, is the essential element of logistics management (Figure).

FIGURE: THE MANAGEMENT TASK IN LOGISTICS

`

As retailers have begun to embrace this logistics approach and examine their wider

supply chains, many have realized that to carry out logistics properly, there has to be a

transformation of approach and operations.

5.3 FUTURE CHALLENGES

While members of the supply chain have sought ways to foster collaboration, the rise of

e-commerce has posed another set of challenges for retailers. The rise and subsequent fall of

many dot.com companies led to a high degree of speculation as to the reconfiguration of the

business to consumer (B2C) channel. Ultimately, e-fulfilment, especially the ‘last mile’ problem

of delivering goods to the final customer, holds the key to success in this channel. The business

to business (B2B) channel, however, has more to offer members of the supply chain because of

the number and complexity of transactions and the greater adoption of Internet technology by

businesses compared with consumers.

19

There have been numerous B2B exchange marketplaces created since the late 1990s, with

most of these exchanges being created in highly concentrated global market sectors with a

‘streamlined’ number of buyers and sellers, for example in the automobile, chemical and steel

industries.

The more proactive retailers developed B2B Internet exchanges as an extension of the

EDI platforms created a decade earlier. This has enabled companies such as Tesco, Sainsbury

and Wal-Mart to establish their own private exchanges with suppliers to share data on sales,

product forecasting, promotion tracking and production planning. There are major benefits to be

derived from pooling EDI efforts into a smaller number of B2B platforms. For example it is

easier to standardize processes for communication, reduce development costs and give members

access to a larger customer base.

In 2000 several Internet trading exchanges were created, promising a revolution in

product procurement. The two major exchanges, GlobalNet Xchange (GNX) and World Wide

Retail Exchange (WWRE), have made some progress. Although the Global Commerce Initiative

established draft standards for global Internet trading, many issues need to be resolved to ensure

the seamless flow of data across the supply chain. The complexity of dealing with thousands of

stock-keeping units (SKUs) has meant that retailers have had to be selective in the projects that

can be routed through their private exchanges compared with these global exchanges. To date the

focus of the GNX exchange has been on special promotions, perishables and own-label products:

for example, 600 out of potential 2,000 suppliers of Sainsbury’s retail brand products are on

GNX.

In the business to consumer (B2C) channel, the rise and fall of Internet retailers has

brought a touch of realism to the evolving market potential of online shopping. In Europe,

grocery retailers are powerful ‘bricks and mortar’ companies and the approach to Internet

retailing has been reactive rather than proactive. Most Internet operations have been small, and

few pure players have entered the market to challenge the conventional supermarket chains.

Tesco is one of the few success stories in egrocery, having adopted an unconventional model.

20

5.4 TESCO.COM: DELIVERING HOME SHOPPING

Tesco.com has become the world’s largest Internet grocery system in a very short time.

Unlike many of its competitors, it has opted for an in store picking and home delivery operation,

rather than starting with a dedicated distribution centre system. This choice came about for three

reasons:

Warehouse-based picking and delivery was not believed to be economic due to low

penetration levels and drive times for vehicles being high

Customers confirmed that they did not want a reduced offer online as this destroyed the

point of shopping at Tesco for them

Outside of London, the penetration rates possible did not make a warehouse a valid

option, even if other costs (such as picking) were solved

Since introduction there has been a very rapid roll-out to effectively cover the UK

through the network of stores. Each store involved has dedicated local delivery vehicles. The

system in operation has thrown up a few surprises:

Fresh food has been a big seller online, whereas people had initially expected big, bulky

replenishment items to be the most popular

People plan their online order better than their in-store trip (aided by the Clubcard and

Internet item recall availability), so a higher proportion of spend is made with Tesco

The non-food item offer can be more extensive online than in-store so sales in this area

can be expanded

Knowledge is gained from the online shopping process of what items customers wanted

to buy, that were not actually in stock. This helps enhance the supply system

Source: adapted from Jones, 2001

21

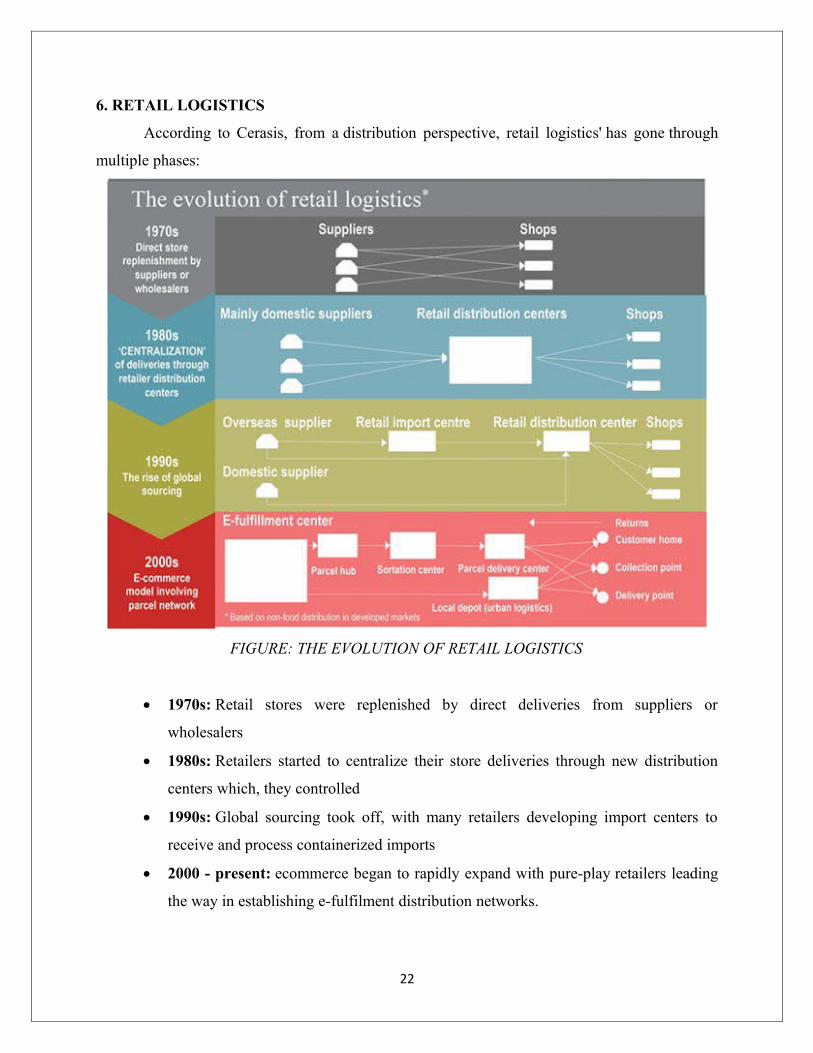

6. RETAIL LOGISTICS

According to Cerasis, from a distribution perspective, retail logistics' has gone through

multiple phases:

FIGURE: THE EVOLUTION OF RETAIL LOGISTICS

1970s: Retail stores were replenished by direct deliveries from suppliers or

wholesalers

1980s: Retailers started to centralize their store deliveries through new distribution

centers which, they controlled

1990s: Global sourcing took off, with many retailers developing import centers to

receive and process containerized imports

2000 - present: ecommerce began to rapidly expand with pure-play retailers leading

the way in establishing e-fulfilment distribution networks.

22

6.1 LOGISTICS FUNCTIONS

1. Mega e-fulfillment Centers: merchandise is stocked and chosen at item level. These

facilities, which are either operated by the retailer or a logistics service provider, are

typically 500,000 sq ft to one million sq ft in size, or larger. They often operate 24 hours

a day, 7 days a week

2. Parcel Hubs / Sorting Centers: sorts orders according to geographical location -- often

by zip or post code, so deliveries are relevant to parcel delivery center, customer’s home

or designated collection point

3. Parcel Delivery Centers: handles the ‘last mile’ delivery to the customer

4. Seamlessly Integrated Technology: shopping carts connect via API or web xml to a

transportation management system, so shoppers get the exact price quote of shipping of

larger items. Quotes are often more suited for less than truckload modes, as these

technology products for logistics, such as a TMS, must accomplish along with the

shopping cart for better management:

Ability to organize and track shipment no matter what mode

Online order status and documentation

Online dispatch documentation and invoice, such as a bill of lading and freight

invoice

Auto reminder for payments

Seamless interface with existing SCM or ERP system

Online alerts for critical information via text or mobile

Information systems reports on past data analysis or delivery history

Types of ecommerce logistics systems ensure the following benefits to shippers,

customers, and 3PL service providers:

Improved communication

Transparency into the supply chain

Improved customer satisfaction

Cost reduction

Improvement in efficiency

23

On-time delivery

As a result, the logistic facilities will encourage some retailers to set up their own

networks of local depots -- either to cross-dock items shipped from larger e-fulfillment centers or

to ship certain ‘fast moving’ products direct to customers. In this emerging model, e-fulfillment

blends with urban logistics, as these facilities will be mainly based around the major population

centers where online sales densities are highest.

For example, in the U.S., Amazon opened smaller scale distribution facilities to offer

same-day delivery services. In the UK, Amazon has a current requirement for some 20 smaller

distribution facilities around major urban areas. By contrast, in France, Amazon’s demand

remains focused on very large units, with the last kilometer delivery being operated by third

party providers.

Omni-channel retailers are now managing their channels in an integrated way that offers

customers a seamless experience, however they choose to shop. With Omni-channel, a retailer

may fulfill orders from stores or warehouses, ultimately blurring the distinction between the two

e-fulfillment centers.

Fulfillment technologies have also helped integrate the front-end and back-end of online

retail. The back-end process is now a collaborative effect thanks to automated software and real-

time fulfillment date. The alignment of important touch-points in the supply chain has reduced

inefficiencies and has helped identify redundant processes. There are even robots that will pick

inventory for customers and move it around the warehouse!

6.2 OVERCOMING OBSTACLES WITH DROP SHIPPING

As with many things, drop shipping presents both advantages and disadvantages to

retailers and suppliers. Many retailers today have tried drop shipping and unfortunately failed.

According to Commerce Hub, “The lack of intercompany system integration is even more

problematic in the drop ship fulfilment model, because record keeping and track-ability become

even more critical as thousands of orders are sourced through hundreds of suppliers. In drop ship

fulfilment, thousands of orders are being shipped to thousands of locations.

The choreography of this is much more complex than single orders with thousands of line

items being shipped in a few warehouses.”

24

This may lead retailers to experience a loss of control, as they now rely on their suppliers

to ship promptly and skilfully. If a supplier fails to execute an order properly, the customer

service wing may get hit. Or worse, it could result in back orders, complicated returns, and

branding problems with packaging.

Though, there are many challenges that suppliers face too. Picking, packing, and shipping

consumer orders is much different than shipping pallets to a retailer or distribution center. Drop

shipping can require updates to warehousing, fulfilment, and invoicing systems, as well as

changes to processes and channel policies. This all contributes to an added degree of inventory

risk for the supplier.

One of the greatest challenges faced by retailers and suppliers is system-to-system

integrations with trading partners. As well as, automating drop shipping processes and the lack of

any kind of standard for performing and maintaining those integrations. I know, it may appear

complicated and at this point even impossible. However, the one key ingredient that will make

drop shipping successful as an ecommerce supply chain management technique is building and

maintaining your relationships.

6.2.1 B2B TO INTEGRATION

With drop shipping, you replace the B2B discussion -- when a retailer negotiates with a

vendor to purchase inventory at wholesale prices, then resells -- with an integration discussion --

where both sides need to understand the virtual part of the relationship and work alongside one

another to designate resources to handle different business processes and new technology

requirements.

25

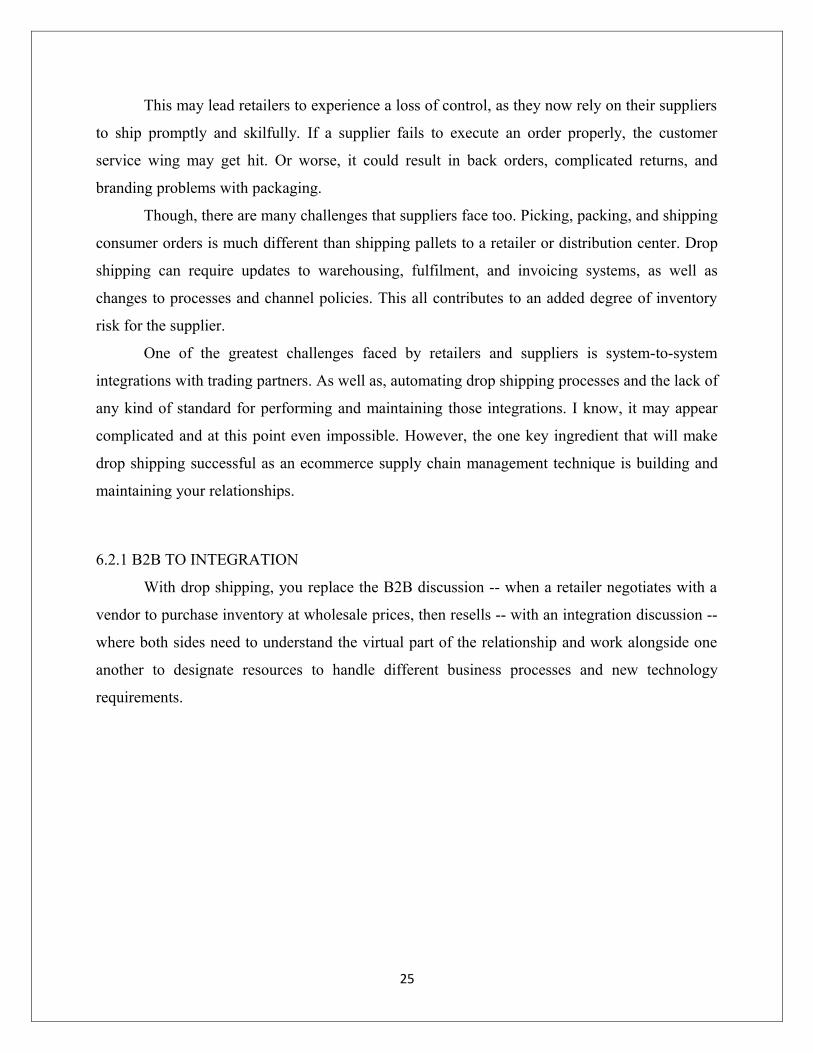

6.2.2 DATA, BUSINESS, INTEGRATION FLOW

FIGURE: DATA, BUSINESS, INTEGRATION FLOW

This commit-to-integrate discussion, and how each relationship accesses it, is the key

ingredient that will facilitate drop shipping success, or guarantee failure. Extensive, coordinated

expectations between the retailer and supplier are crucial.

6.2.3 COLLABORATORS NOT CUSTOMERS

Conventional supply chain relationships and business processes don’t necessarily fit into

our newly adopted economic world. When a retailer decides to modify their supply chain to a

drop ship or inventory-less fulfilment model, there are significant factors that should to be

discussed.

Drop shipping is not just another fulfilment model. The financial equation is altered, so

the vendor-retailer relationship is altered as well. While not having to actually purchase the

inventory is financially beneficial to a retailer, it actually reduces the amount of leverage the

retailer has over the vendor’s behaviour. In return for the opportunity to market more products

26

through the retailer’s channel, the vendor takes on all of the financial risk, while having far less

up-front financial security.

In conventional fulfilment models, the retailer usually controls the process and technical

requirements, while the vendor performs the cost/benefit analysis. Since financial negotiation has

already occurred between the merchant and vendor, it makes sense for the technical discussion to

be conducted separately from the retailer’s organization.

FIGURE: VENDOR DEALER RELATIONSHIP

With the drop shipping fulfilment model, conversations intersect much more frequently.

Retailers will often ask the vendor to spend time and money to work with them on the premise of

revenue. However, vendors are much more resistant to additional technical and process demands.

Vendors have less desire to add costs to participate in a drop shipping program, because of the

lower revenue per order normally associated with consumer-driven orders. The following factors

complicate things for retailers, as it makes it difficult to leverage existing partner on-boarding

processes or outsourced vendor management systems. It’s also generally very difficult for a third

party vendor to properly represent the retailer during these discussions.

27

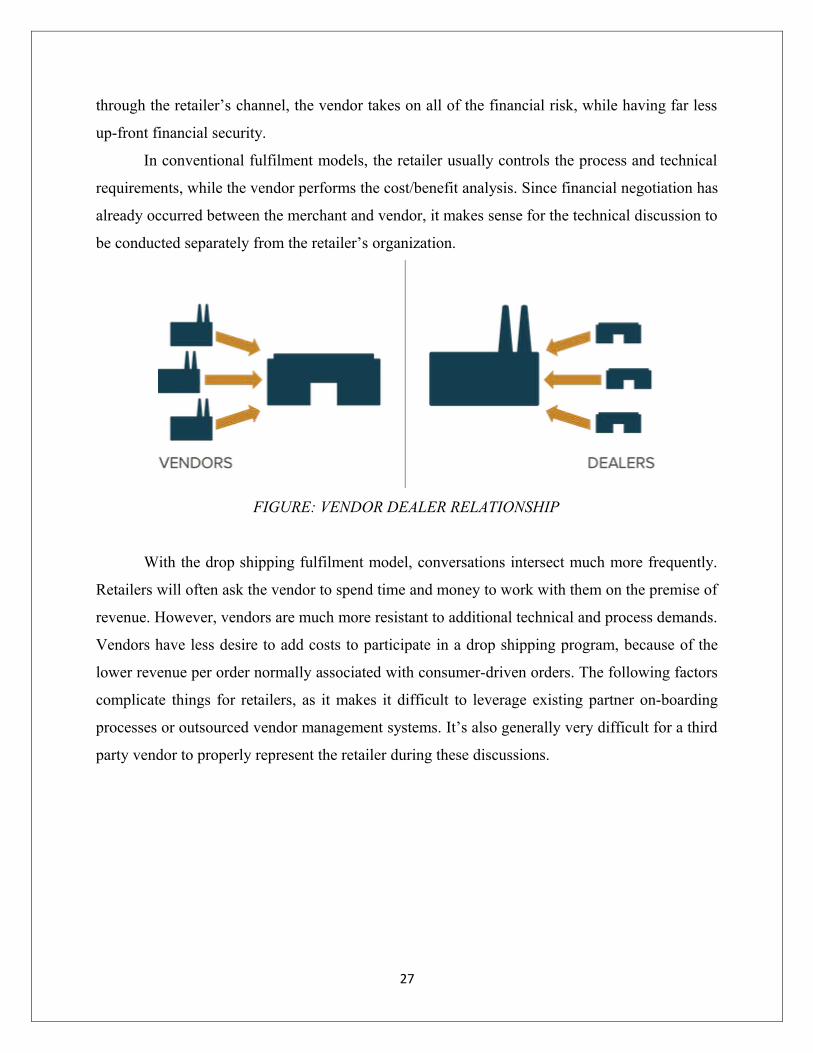

FIGURE: CONVERSATIONS INTERSECTING

With drop shipping as your main strategy, everyone is partners, which requires critical

alignment.

6.3 FOUNDATIONAL FACTORS

Determining and utilizing partners for a drop ship or endless aisle program is different

than for a conventional order fulfilment method. While there is no commitment to buy, retailers

have the opportunity to choose from multiple supply partners. However, this lack of financial

incentive can affect the willingness of the supplier to spend time and money to meet a retailer’s

compliance needs. Finally, because of the distributed nature of drop shipping, some component

of electronic data exchange cannot be optional for the supplier.

Two foundational factors that should be considered:

Logistics Efficiencies: When choosing a supplier to participate in a drop shipping

initiative, retailers must ensure that the supplier can do single-item fulfilment, and

that its ability to do this matches the retailer’s needs -- such as, shipping times and

expedited options. The capacity for suppliers to select individual items in their

warehouse or fulfilment center is a prerequisite for drop shipping. Retailers can gauge

this ability if the supplier offers direct-to-consumer fulfilment via its own ecommerce

28

site. Many suppliers underestimate the costs of switching to a single item fulfilment

model, so be cautious of those who promise to make the switch on your behalf.

Technology Opportunities: Both sides will need to commit time and resources to drop

shipping. With that said, you’re not committing to a specific revenue number, but

minimizing the technical excuses for not participating. This means providing multiple

options to exchange data at no or little cost. Options will range from partners with

very minimal technical expertise, to those with a mature and robust ecommerce

infrastructure. Typical data-exchange options:

o Self-service, manual portal

o Non-integrated batch process

o Automated, filed based integration option

o Web services (API, XML) automated option

6.4 FOCUS ON THE CONSUMER

The good news is that there is a strong alignment with all of these issues: the consumer.

Today, brands and suppliers are selling directly to the consumer. This positions the supply side

of the equation directly with the retail side: the consumer experience drives everything.

Consumers need descriptive product data, trust in inventory certainty, a consumer-friendly

ordering process, and item-level logistics that are track able and returnable.

The world is positioning its efforts on the consumer, and that is driving new relationships

in the supply chain, and especially partnerships between those that would like to be on one side

or the other of drop shipping, to flourish and find success.

7. CONCLUSION

Retailing in India is gradually inching its way toward becoming the next boom industry.

The whole concept of shopping has altered in terms of format and consumer buying behavior,

ushering in a revolution in shopping in India. Modern retail has entered India as seen in

sprawling shopping centers, multi-storied malls and huge complexes offer shopping,

entertainment and food all under one roof. The organized players has started developing in the

past few years. The growth potential for modern retailers are enormous in India. They may seem

to face lots of challenges. But that is because they are exploring a market which has been

unorganized and unstructured for decades. Modern retailers are coming out with best solutions

29

and alternatives and if they go down this path at the current pace, modern retail will be a great

success in India within ten years.

8. REFERENCES

https://www.academia.edu/2688921/Retail_logistics_changes_and_challenges

http://www.sciencedirect.com/science/article/pii/S0970389613000591

http://thejibe.com/blog/15/01/ecommerce-logistics-transformation-part-1

http://thejibe.com/blog/15/01/ecommerce-logistics-developed-markets-part-2

http://thejibe.com/blog/15/02/ecommerce-logistics-suppliers-and-retailers-part-3

http://www.consumersinternational.org/media/1035307/summary,%20the

%20relationship%20between%20supermarkets%20and%20suppliers.pdf

http://www.sclgme.org/shopcart/Documents/Retail%20Logistics%20-%20Change

%20and%20Challenges.pdf

30