Embed Size (px)

Citation preview

BOWMAN’S STRATEGY CLOCK PERSONAL CARE

KESHAV BAGRI [H006] ASHWINI DESHPANDE [H012] AKSHAY MATHUR [H035] ROSHAN P R [H045] RISHI SAMPAT [H049] KSHIPRA SINGH [H060]

GROUP 8

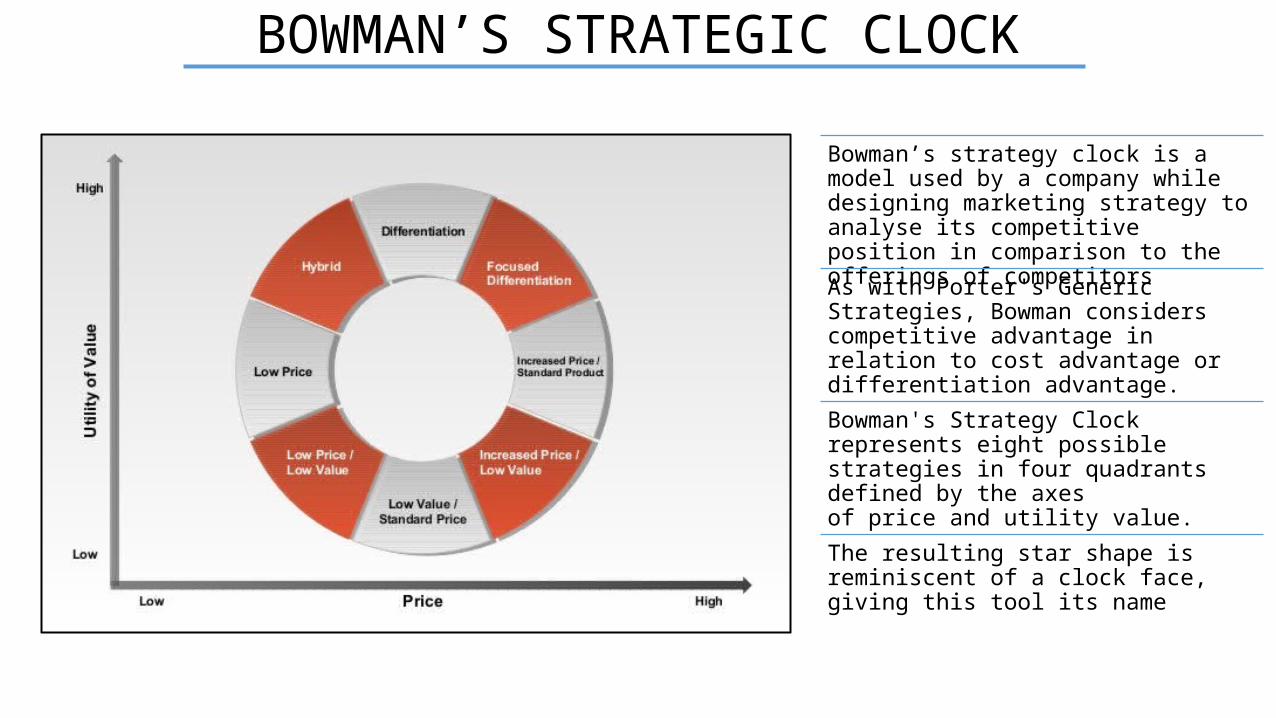

BOWMAN’S STRATEGIC CLOCKBowman’s strategy clock is a model used by a company while designing marketing strategy to analyse its competitive position in comparison to the offerings of competitors

As with Porter's Generic Strategies, Bowman considers competitive advantage in relation to cost advantage or differentiation advantage.

Bowman's Strategy Clock represents eight possible strategies in four quadrants defined by the axes of price and utility value.

The resulting star shape is reminiscent of a clock face, giving this tool its name

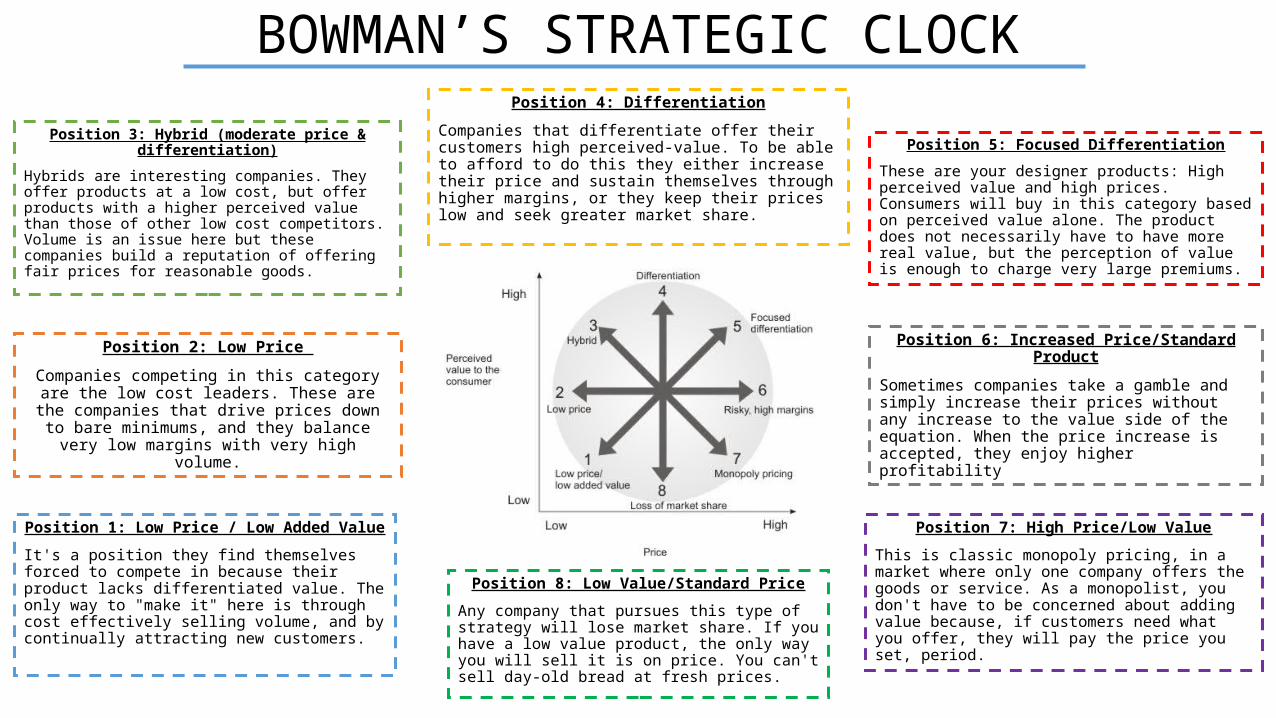

BOWMAN’S STRATEGIC CLOCK

Position 1: Low Price / Low Added Value

It's a position they find themselves forced to compete in because their product lacks differentiated value. The only way to "make it" here is through cost effectively selling volume, and by continually attracting new customers.

Position 2: Low Price

Companies competing in this category are the low cost leaders. These are the companies that drive prices down to bare minimums, and they

balance very low margins with very high volume.

Position 3: Hybrid (moderate price & differentiation)

Hybrids are interesting companies. They offer products at a low cost, but offer products with a higher perceived value than those of other low cost competitors. Volume is an issue here but these companies build a reputation of offering fair prices for reasonable goods.

Position 8: Low Value/Standard Price

Any company that pursues this type of strategy will lose market share. If you have a low value product, the only way you will sell it is on price. You can't sell day-old bread at fresh prices.

Position 7: High Price/Low Value

This is classic monopoly pricing, in a market where only one company offers the goods or service. As a monopolist, you don't have to be concerned about adding value because, if customers need what you offer, they will pay the price you set, period.

Position 6: Increased Price/Standard Product

Sometimes companies take a gamble and simply increase their prices without any increase to the value side of the equation. When the price increase is accepted, they enjoy higher profitability

Position 4: Differentiation

Companies that differentiate offer their customers high perceived-value. To be able to afford to do this they either increase their price and sustain themselves through higher margins, or they keep their prices low and seek greater market share.

Position 5: Focused Differentiation

These are your designer products: High perceived value and high prices. Consumers will buy in this category based on perceived value alone. The product does not necessarily have to have more real value, but the perception of value is enough to charge very large premiums.

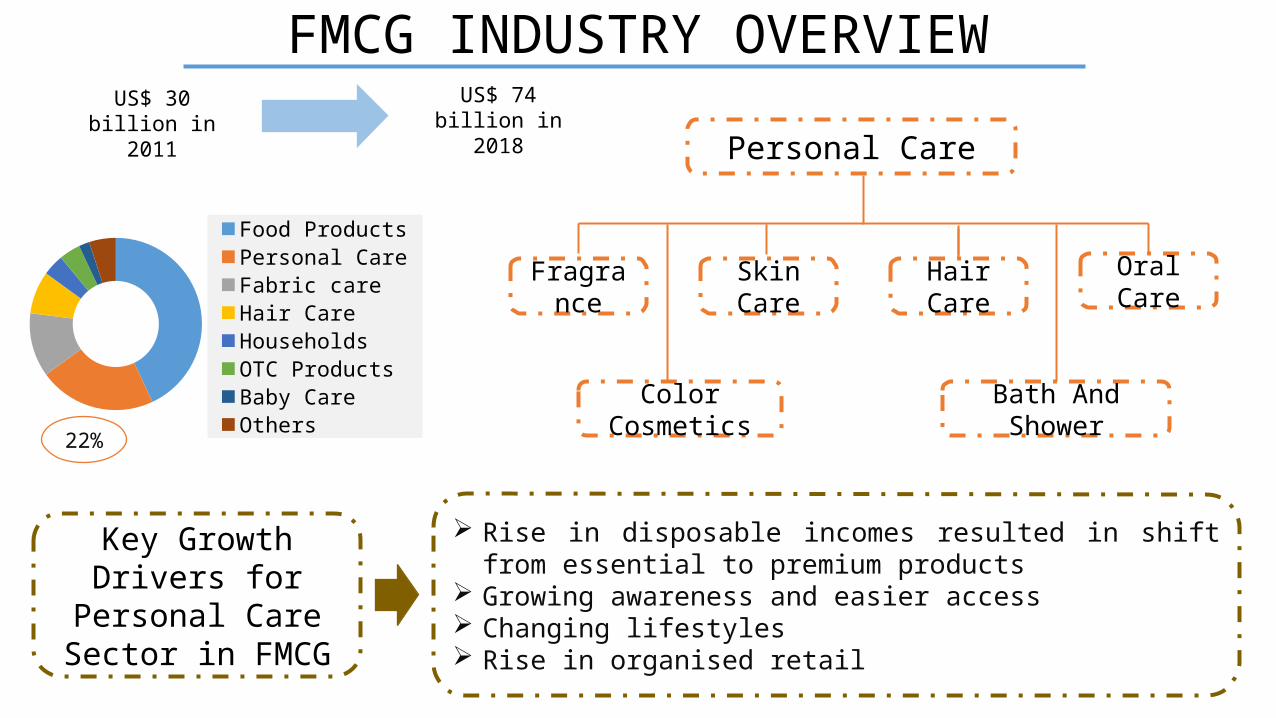

FMCG INDUSTRY OVERVIEW

Food ProductsPersonal CareFabric careHair CareHouseholdsOTC ProductsBaby CareOthers

US$ 30 billion in 2011

US$ 74 billion in 2018

22%

Personal Care

Skin Care

Bath And ShowerColor Cosmetics

Hair Care Oral CareFragrance

Key Growth Drivers for Personal Care Sector in FMCG

Rise in disposable incomes resulted in shift from essential to premium products

Growing awareness and easier access Changing lifestyles Rise in organised retail

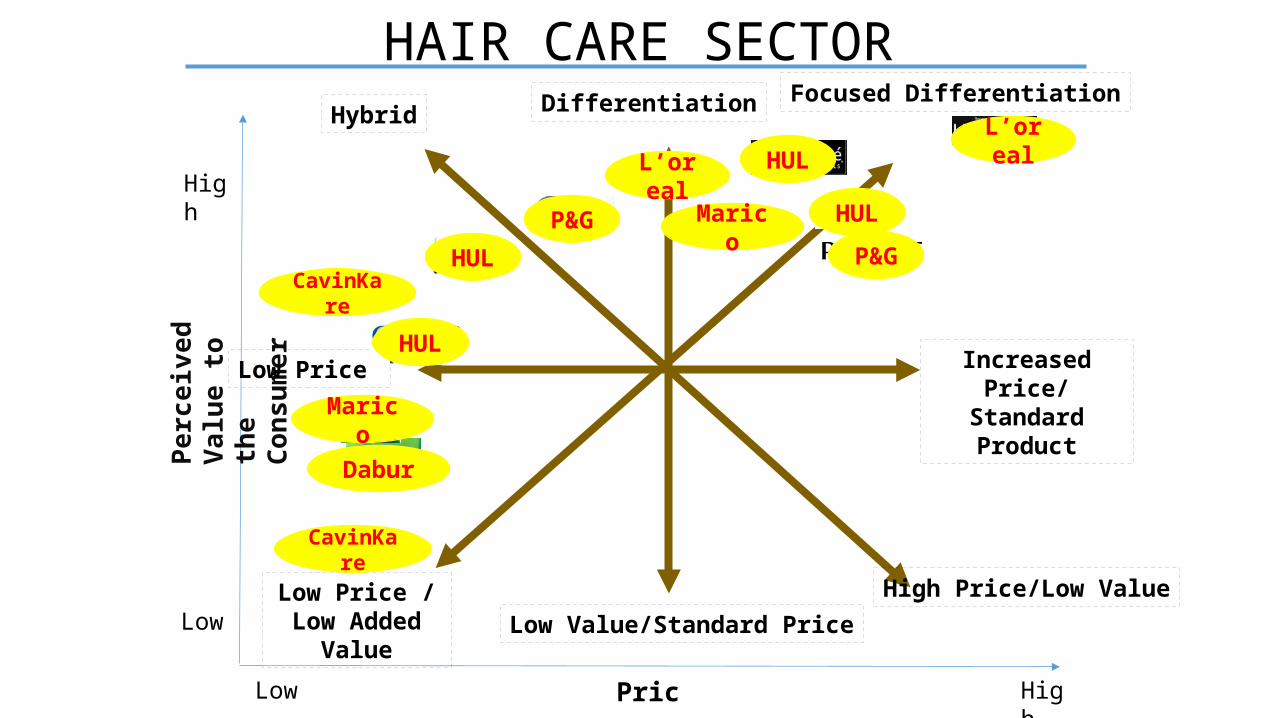

HAIR CARE SECTOR

Low

Low

High

High

Perc

eive

d Va

lue

to th

e Co

nsum

er

Price

Low Price / Low Added Value

Low Price

Hybrid Differentiation Focused Differentiation

Increased Price/ Standard Product

High Price/Low ValueLow Value/Standard Price

HUL

HUL

HUL

P&GP&G

Marico

Dabur

CavinKare

CavinKare

Marico

HUL

L’orealL’oreal

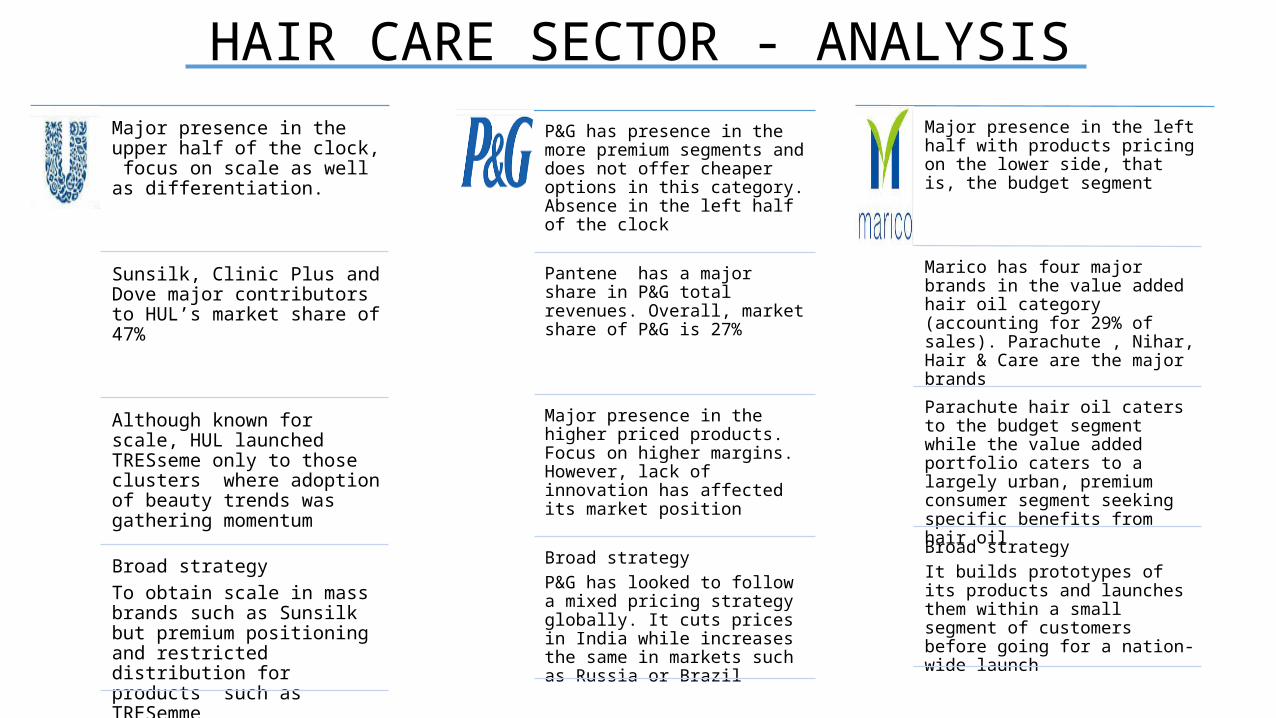

HAIR CARE SECTOR - ANALYSISMajor presence in the upper half of the clock, focus on scale as well as differentiation.

Sunsilk, Clinic Plus and Dove major contributors to HUL’s market share of 47%

Although known for scale, HUL launched TRESseme only to those clusters where adoption of beauty trends was gathering momentum

Broad strategyTo obtain scale in mass brands such as Sunsilk but premium positioning and restricted distribution for products such as TRESemme

P&G has presence in the more premium segments and does not offer cheaper options in this category. Absence in the left half of the clock

Pantene has a major share in P&G total revenues. Overall, market share of P&G is 27%

Major presence in the higher priced products. Focus on higher margins. However, lack of innovation has affected its market position

Broad strategyP&G has looked to follow a mixed pricing strategy globally. It cuts prices in India while increases the same in markets such as Russia or Brazil

Major presence in the left half with products pricing on the lower side, that is, the budget segment

Marico has four major brands in the value added hair oil category (accounting for 29% of sales). Parachute , Nihar, Hair & Care are the major brands

Parachute hair oil caters to the budget segment while the value added portfolio caters to a largely urban, premium consumer segment seeking specific benefits from hair oil

Broad strategyIt builds prototypes of its products and launches them within a small segment of customers before going for a nation-wide launch

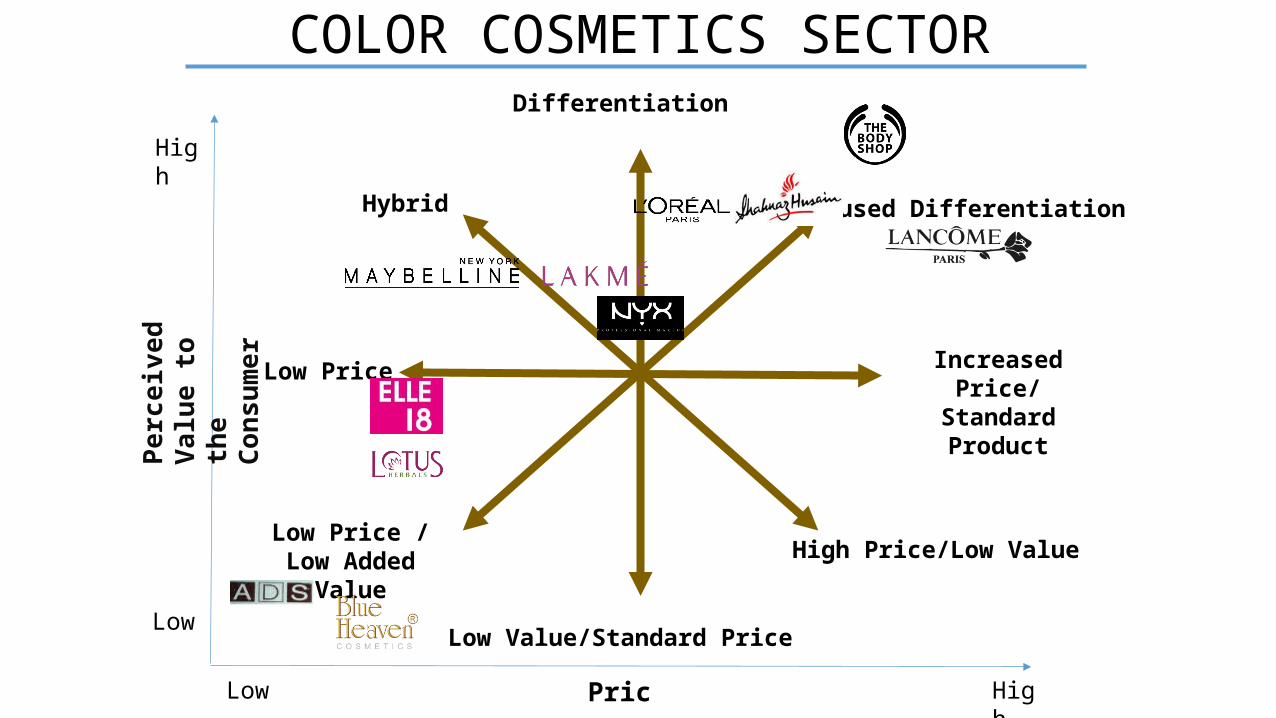

COLOR COSMETICS SECTOR

Low

Low

High

High

Perc

eive

d Va

lue

to th

e Co

nsum

er

Price

Low Price / Low Added Value

Low Price

Hybrid

Differentiation

Focused Differentiation

Increased Price/ Standard Product

High Price/Low Value

Low Value/Standard Price

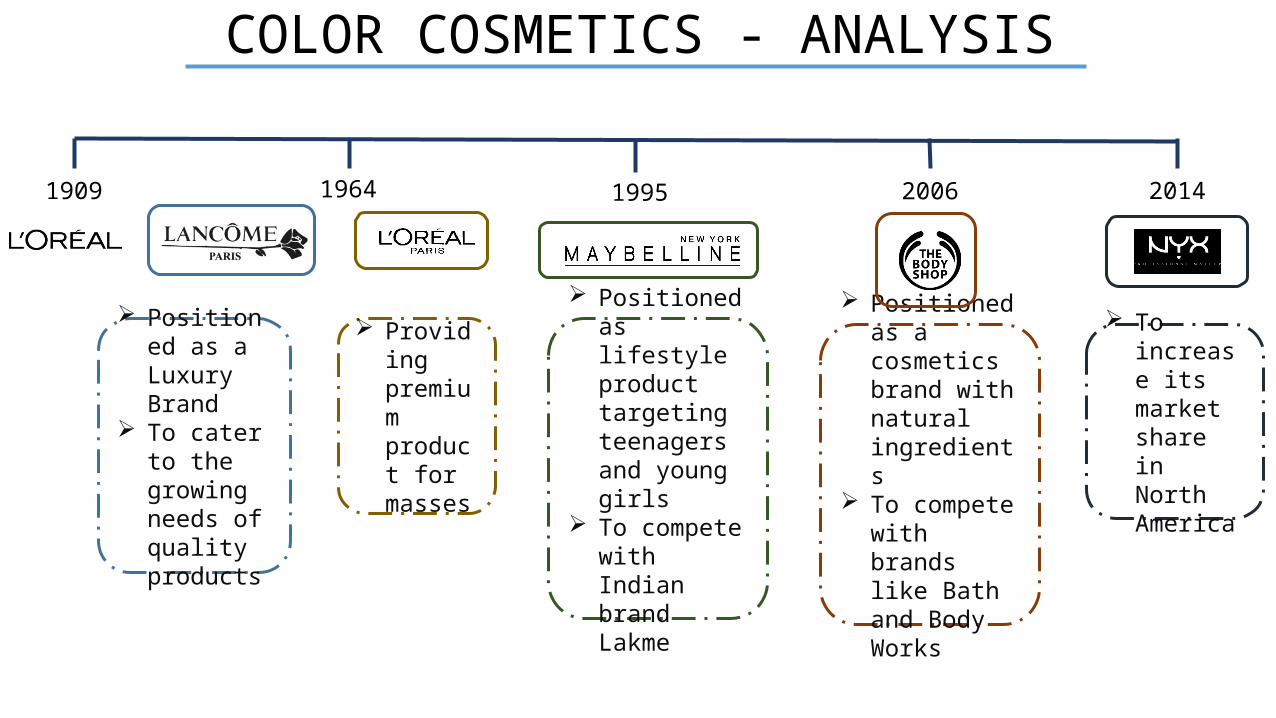

COLOR COSMETICS - ANALYSIS

1909 20141964 1995 2006

To increase its market share in North America

Positioned as a Luxury Brand

To cater to the growing needs of quality products

Providing premium product for masses

Positioned as lifestyle product targeting teenagers and young girls

To compete with Indian brand Lakme

Positioned as a cosmetics brand with natural ingredients

To compete with brands like Bath and Body Works

Low

HighPe

rcei

ved

Valu

e to

the

Cons

umer

Low Price / Low Added Value

Low Price

Hybrid

Differentiation

Focused Differentiation

Increased Price/ Standard Product

High Price/Low Value

Low Value/Standard Price

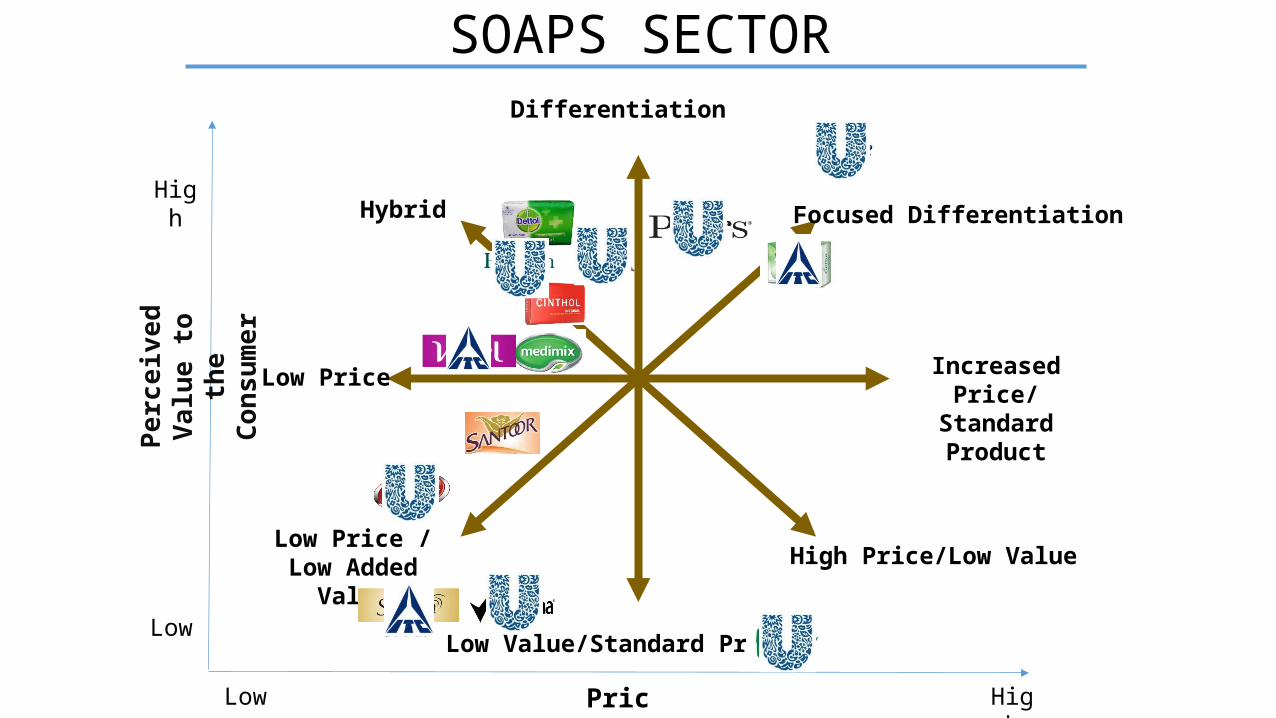

SOAPS SECTOR

Low HighPrice

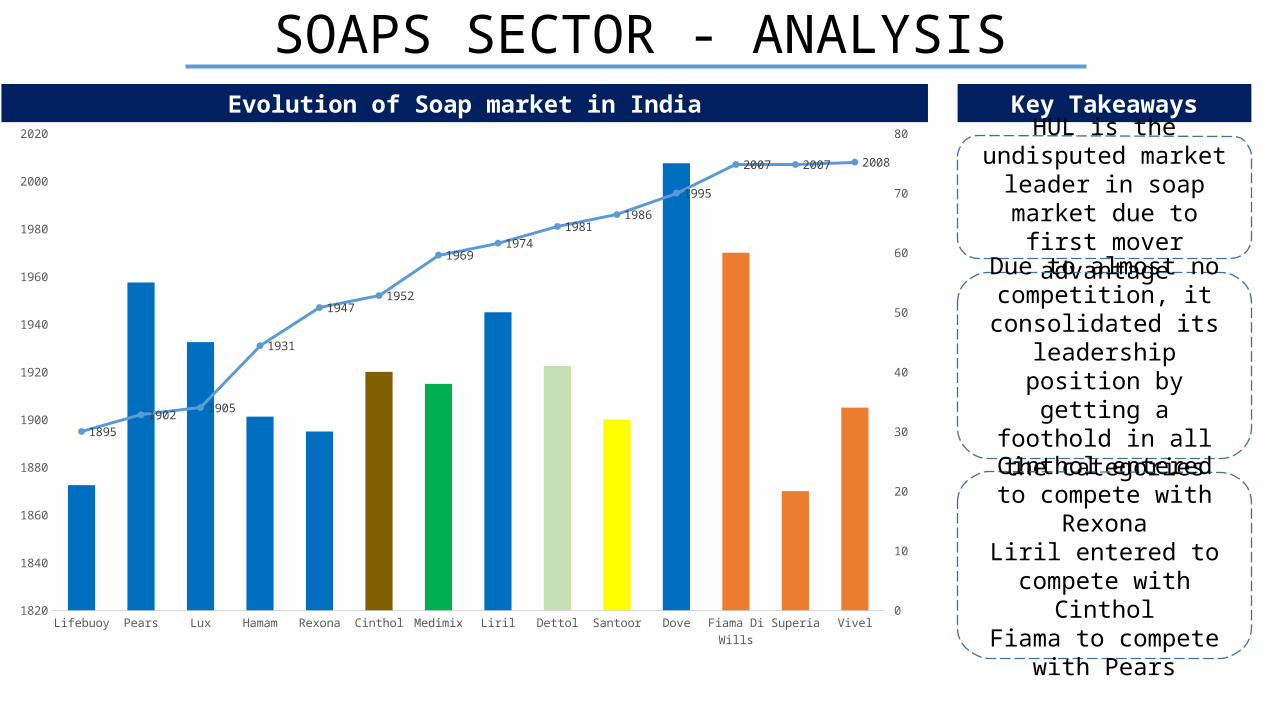

SOAPS SECTOR - ANALYSIS

Lifebuoy Pears Lux Hamam Rexona Cinthol Medimix Liril Dettol Santoor Dove Fiama Di Wills

Superia Vivel1820

1840

1860

1880

1900

1920

1940

1960

1980

2000

2020

0

10

20

30

40

50

60

70

80

18951902 1905

1931

19471952

19691974

19811986

1995

2007 2007 2008

Evolution of Soap market in India Key Takeaways

HUL is the undisputed market leader in soap

market due to first mover advantage

Due to almost no competition, it consolidated its

leadership position by getting a foothold in all

the categories

Cinthol entered to compete with Rexona

Liril entered to compete with Cinthol

Fiama to compete with Pears

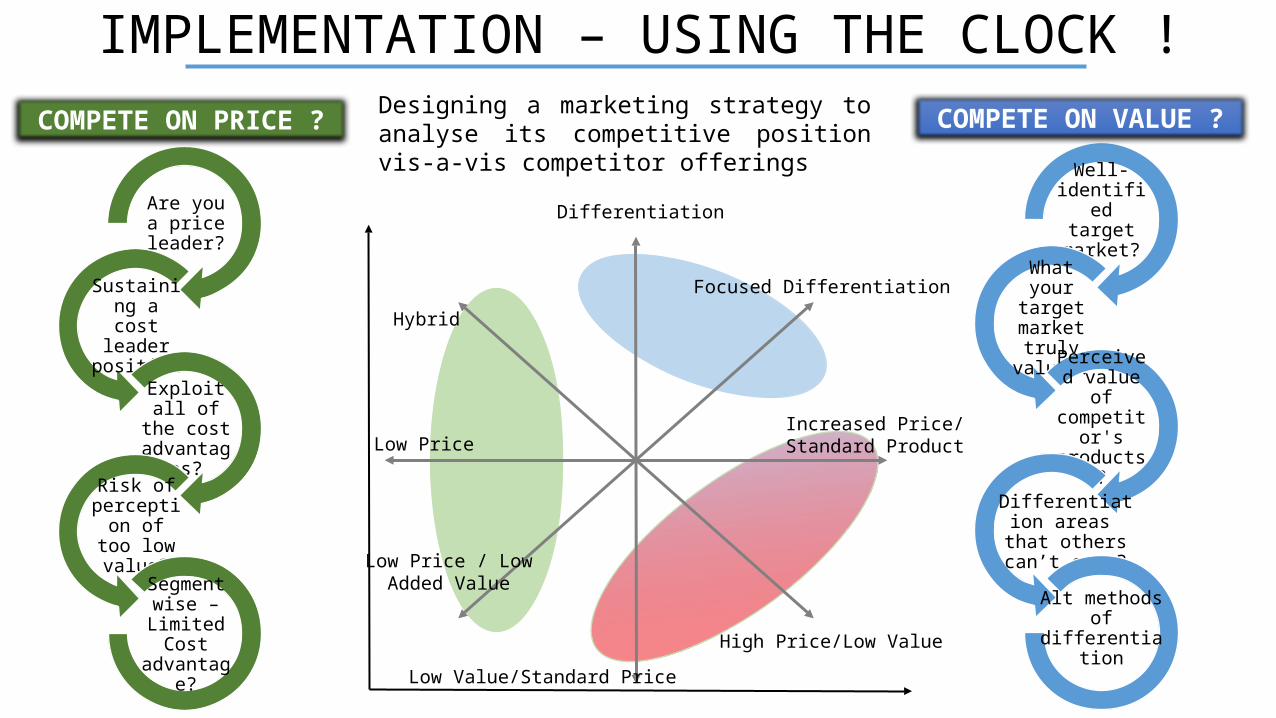

IMPLEMENTATION – USING THE CLOCK !

Are you a price

leader?

Sustaining a cost leader

position

Exploit all of the cost

advantages?

Risk of perception of too low

value?

Segment wise –

Limited Cost advantage?

Well-identified

target market?

What your target

market truly values?

Perceived value of

competitor's products?

Differentiation areas that others

can’t copy?

Alt methods of differentiation

COMPETE ON PRICE ? COMPETE ON VALUE ?Designing a marketing strategy to analyse its competitive position vis-a-vis competitor offerings

Low Price / Low Added Value

Low Price

Hybrid

Differentiation

Focused Differentiation

Increased Price/ Standard Product

High Price/Low Value

Low Value/Standard Price