Embed Size (px)

Citation preview

Consult Construction is a consulting firm with all governance, compliance and IT related services related to the construction sector under one roof.

Focus Areas :-

Corporate GovernanceManagement AuditProject Budgeting and MonitoringIndirect Tax CompliancesCorporate TrainingInformation Technology and Allied ServicesISO Implementation

Core Team

Mr.Sandesh Mundra - Indirect Tax & Management AuditMr.S N Mundra - CompliancesMr.Samir Siddhpuria - VAT Mr.Philip Fernandes - Excise Mr.Dinesh Kavi - Labour LawsMs.Suman Mundra - Management AuditMr.Sanjay Christian - Management AuditMs Pooja Jajwani - IndirectTax Consulting

Authored - Technical Guide on “Business Controls, Monitoring and Internal Audit of Construction Sector”

Authored the technical Guide on “Business Controls, Monitoring and Internal Audit of Construction Sector” issued by ICAI in 2011.

One of our team members has been appointed to the three member National level Direct and Indirect Committee of Builder’s Association of India (BAI) for year 2014. Successful representation to the Ministry of Finance on service tax related issues on behalf of BAI.

Paper on “Accounting Controls in Construction Sector” chosen for publication in January, 2013 issue of National Journal of ICAI.

Paper on "Budgeting Challenges for construction sector" chosen for publication in August 2013 issue of National Journal of ICAI.

Our team members have acted as a speaker on various topics in seminars and study circle meets organised at Mumbai, Ahmedabad, Gandhinagar, Navsari, Jamnagar, Rajkot and Nadiad Branches and study circles of ICAI.

Our team members are Regular Column writers for Indian Construction (Journal of Builder’s association of India), CA Associaton Ahmedabad & web portals like Consult Construction.com & Consolidation of accounts.com

Our Team Achievements

We have pan India Network of VAT Consultants at following locations

CREDIT MAPPING & OPTIMISATION

In terms of the indirect tax provisions (service tax, VAT and excise) a manufacturer or service provider is eligible to claim input tax credit of tax paid on goods and services. The said credit can be utilized for payment of indirect tax liability. Thus the input tax credit is akin to cash on hand which can be used for making tax payments. It is essential that a manufacturer or service provider avails all the eligible input tax credit in terms of the applicable input tax credit provisions and optimizes the same.

• Credit mapping and optimisation cover the following:• Identifying expenses on which tax is paid.• Evaluate expenses on which input tax credit has not been availed.• Evaluate the eligibility in terms of applicable input tax credit provisions.• Put a system in place to ensure optimum input tax credit availment.

STRUCTURING & PLANNING

Setting up a new business or expanding an existing one attracts various indirect taxes. It is observed that indirect tax planning is generally done post execution of the arrangement; thus leading to loss of indirect tax benefits or credit, higher payment of taxes, inefficient indirect tax structure. Therefore it is essential that the transaction is evaluated, structured and planned specifically considering the indirect tax impact:-

• Structuring & Planning would broadly cover the following:• indirect tax analysis on proposed transactions.• Tax neutralization / optimisation advice.• Agreement review/ drafting.• Advice on setting up business in tax efficient manner.• Identify mechanics to optimize tax credits and reduce cascading of

taxes.

MANAGEMENT OF SUB-CONTRACTOR

• We help plan proper contracting arrangement with the sub-contractor, taking care of tax, legal and several control related issues. We also ensure regular reporting formats/ MIS on daily and monthly basis.

PLANNING FOR WITHHOLDING TAXES

• WCT deduction is a very critical issue. It can be planned keeping in mind the relevant provisions of relevant VAT law in mind.

MULTI STATE VAT

• VAT / Sales tax in India is a state level tax• Difficult for a business man to learn and keep track of all statues

applicable under different states • Continuous amendments in the state laws make it very difficult for

multi locational companies to comply within time bound manner with optimum utilizations of available benefits.

• We have dedicated team of experts and proper infrastructure facilities to provide one stop solutions to comply with VAT law across the country. It obviates need to appoint consultant separately for each of the states. It would reduce communication gap, provide expert hand and save time & cost with optimum productivity. Ultimately bringing peace of mind to your taxation department.

HANDLING APPELLATE PROCEEDINGS

Our services cover the following :-

• Representation before all adjudicating Authorities including CESTAT.

• Representation before Advance Ruling Authority.• Representation before Ministry of Finance.• Representation before Settlement Commission for

settlement of cases.• Day-to-day litigation support on notices, summons

etc. received from tax authorities.

Subscribe to our E-Bulletin

email - [email protected]

• VAT and Service Tax updates for the construction / Project sector companies.

• Legislative changes and major case laws under the State VAT Laws and under Service Tax law affecting the construction /Project Sector.

• In addition our brief analysis and comments on the various developments.

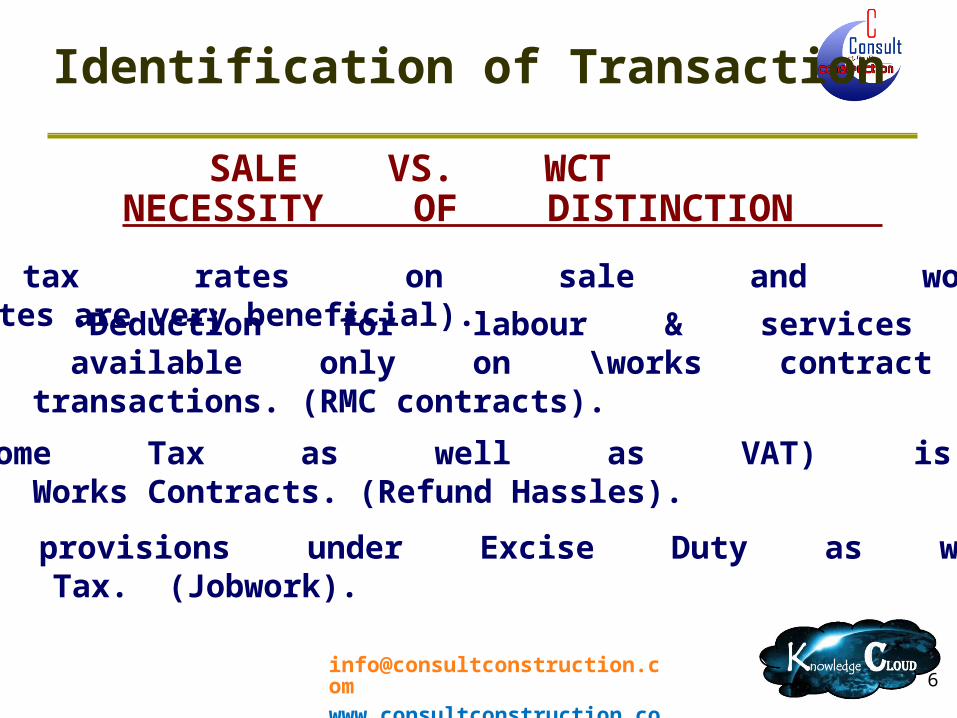

SALE VS. WCT NECESSITY OF DISTINCTION

• Different tax rates on sale and works contract. (At times the rates are very beneficial). •Deduction for labour & services available only on \

works contract transactions. (RMC contracts).

• TDS (Income Tax as well as VAT) is deducted only on Works Contracts. (Refund Hassles).

• Different provisions under Excise Duty as well as Service Tax. (Jobwork).

Identification of Transaction

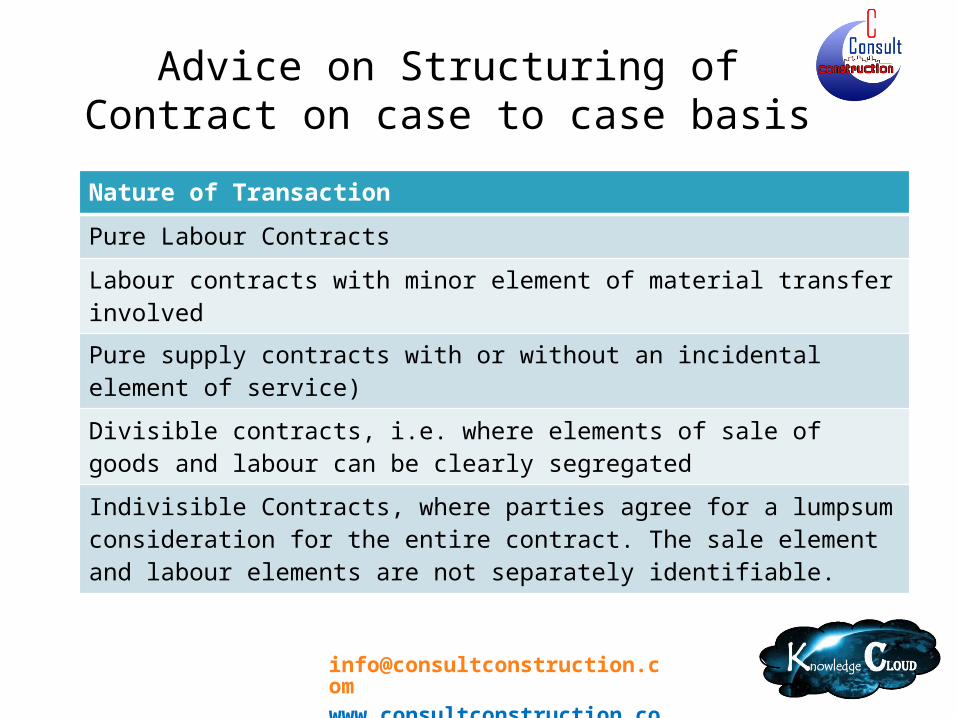

Advice on Structuring of Contract on case to case basis

Nature of Transaction

Pure Labour Contracts

Labour contracts with minor element of material transfer involved

Pure supply contracts with or without an incidental element of service)

Divisible contracts, i.e. where elements of sale of goods and labour can be clearly segregated

Indivisible Contracts, where parties agree for a lumpsum consideration for the entire contract. The sale element and labour elements are not separately identifiable.

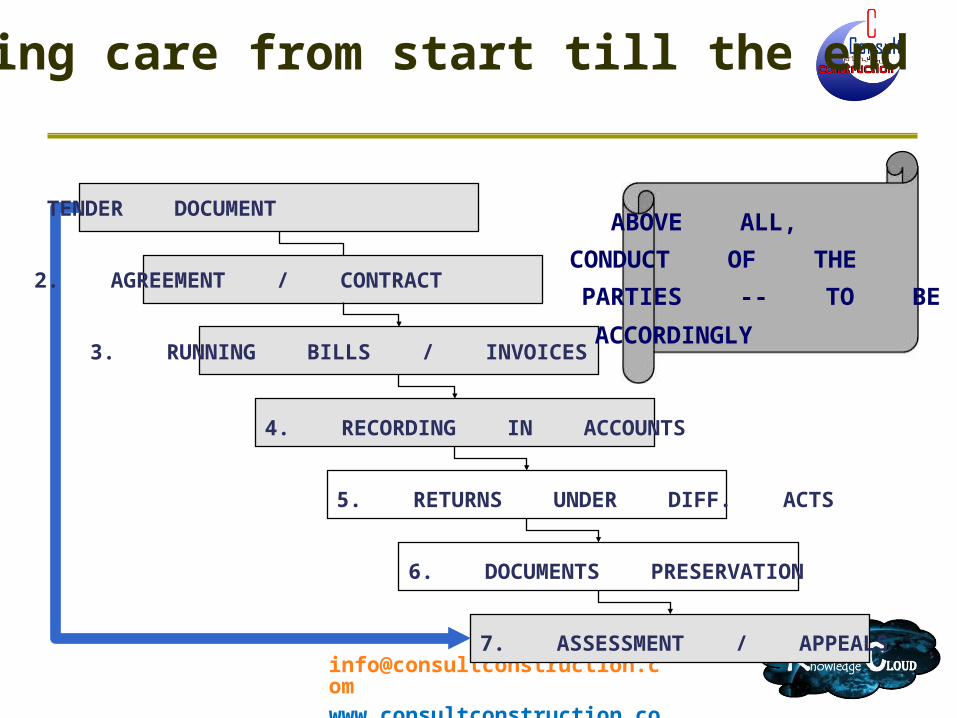

Taking care from start till the end

1. TENDER DOCUMENT

2. AGREEMENT / CONTRACT

3. RUNNING BILLS / INVOICES

4. RECORDING IN ACCOUNTS

5. RETURNS UNDER DIFF. ACTS

6. DOCUMENTS PRESERVATION

7. ASSESSMENT / APPEALS

4

ABOVE ALL,

CONDUCT OF THE

PARTIES - TO BE ‐

ACCORDINGLY

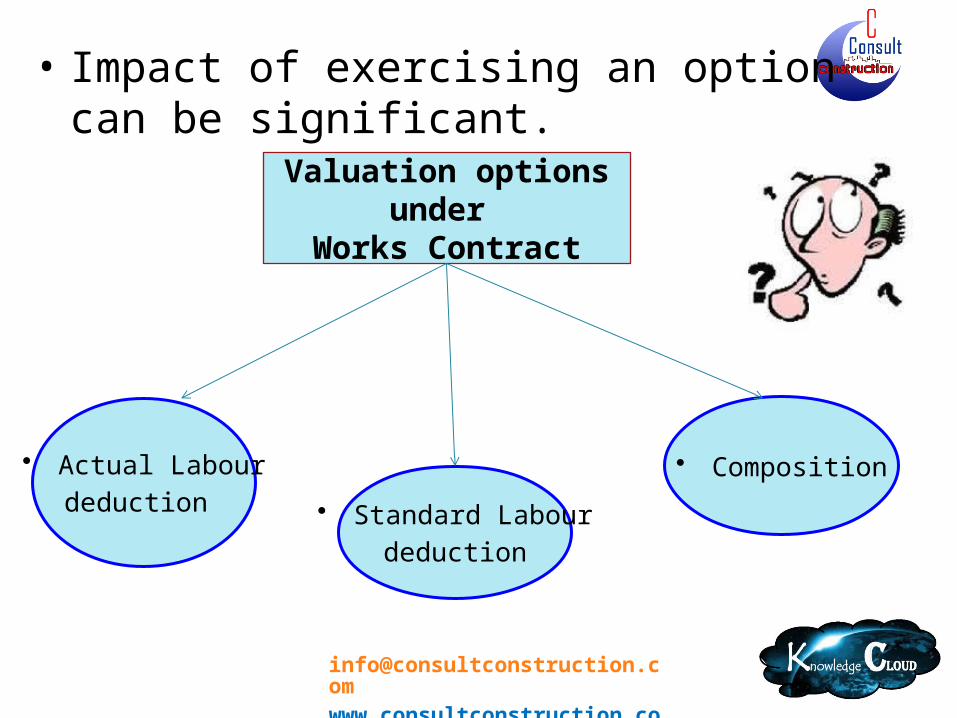

Valuation options under Works Contract

• Actual Labour

deduction • Standard Labour

deduction

• Composition

• Impact of exercising an option can be significant.

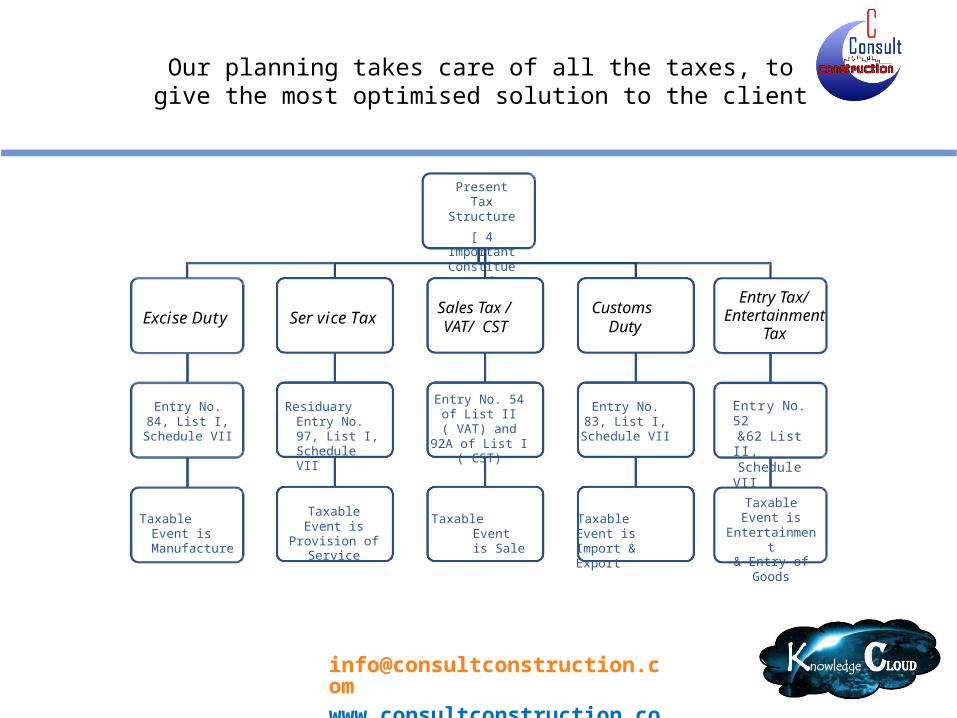

Our planning takes care of all the taxes, to give the most optimised solution to the client

Present Tax Structure

[ 4 Important Constituents]

Excise Duty

Entry No. 84, List I, Schedule

VII

Taxable Event is Manufacture

Ser vice Tax

Residuary Entry No. 97, List I, Schedule VII

Taxable Event is Provision of

Service

Sales Tax / VAT/ CST

Entry No. 54 of List II ( VAT) and

92A of List I( CST)

Taxable Event is Sale

Customs Duty

Entry No. 83, List I, Schedule

VII

Taxable Event is Import & Export

Entry Tax/ Entertainment

Tax

Entry No. 52&62 List II,Schedule

VII

Taxable Event is Entertainment

& Entry ofGoods

Checklist to understand VAT on Works Contract

We have state specific VAT checklists which help us in giving instant replies to client on any works contract related issues related to

any state of the country

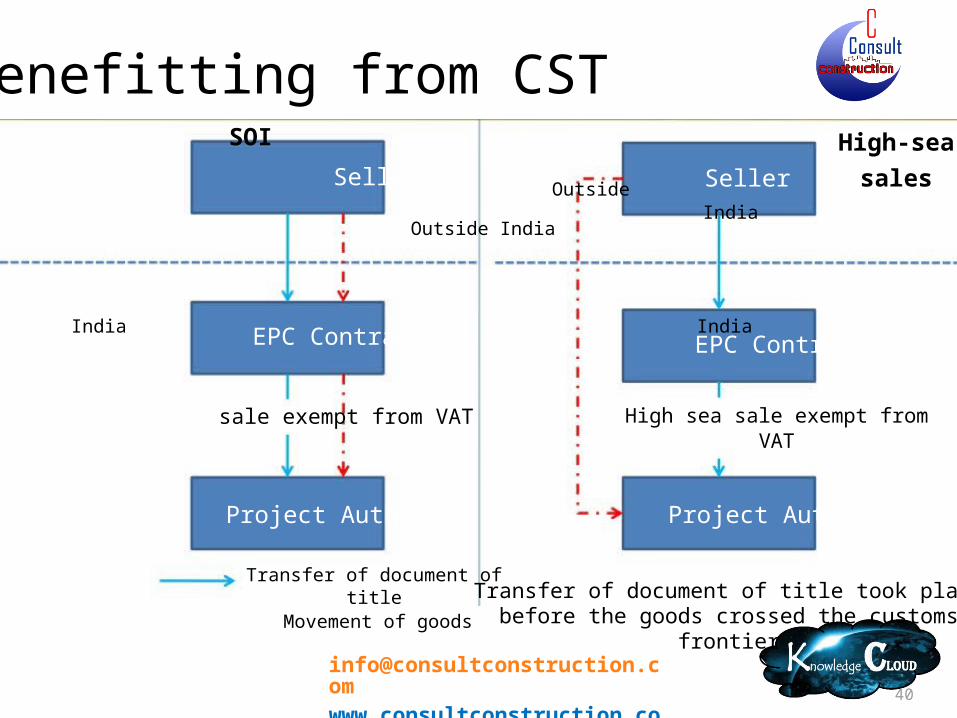

Benefitting from CSTSOI

Seller Outside

High-sea

Seller salesIndia

Outside India

India EPC Contractor

sale exempt from VAT

Project Authority

Transfer of document oftitle

Movement of goods

IndiaEPC Contractor

High sea sale exempt fromVAT

Project Authority

Transfer of document of title took placebefore the goods crossed the customs

frontier

40

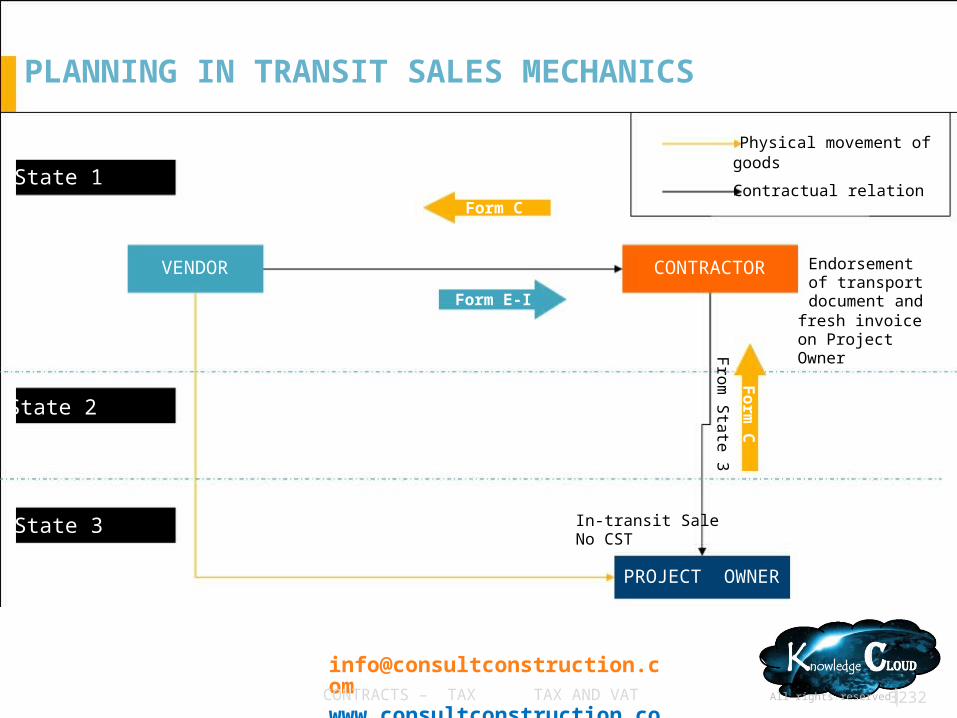

From

State 3

Form

C

All rights reserved| |3232CONTRACTS – TAX TAX AND VAT

State 3

VENDOR

In-transit SaleNo CST

PROJECT OWNER

CONTRACTOR

Form C

Form E-I

State 1

PLANNING IN TRANSIT SALES MECHANICS

Physical movement ofgoods

Contractual relation

Endorsementof transportdocument andfresh invoiceon ProjectOwner

State 2

We can help you cope up with the Expected Impact of GST by doing a prescrutiny of your

contracts and suggesting necessary modifications in your ERP

Some of the companies who have attended our workshops on Indirect Taxes