Embed Size (px)

Citation preview

#FreedomDrivesProgress

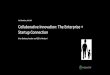

Cesar Grajales was born in Colombia and moved to

Miami at the age of 17. His professional background

covers different fields, from the music business industry

and Hispanic entertainment to the stock market. His

unwavering commitment to the preservation of economic

freedom in the United States led him to join LIBRE’s

cause from its beginning; first as a volunteer, then as a

writer for Fox News Latino on political and economic

issues, later as Field Representative and as a Field

Director in LIBRE’s office in South Florida and currently

as Florida State Director. Grajales has successfully

promoted de principles of economic freedom amongst

the growing Hispanic community in Florida. In his current

role, he coordinates events at a state level, and

represents the organization at fairs, forums and

conferences promoting LIBRE’s cause among fellow

Floridians. Grajales has a vast experience in business

administration, management, political campaign

operations and grassroots operations.

CESAR GRAJALES

Florida State Director

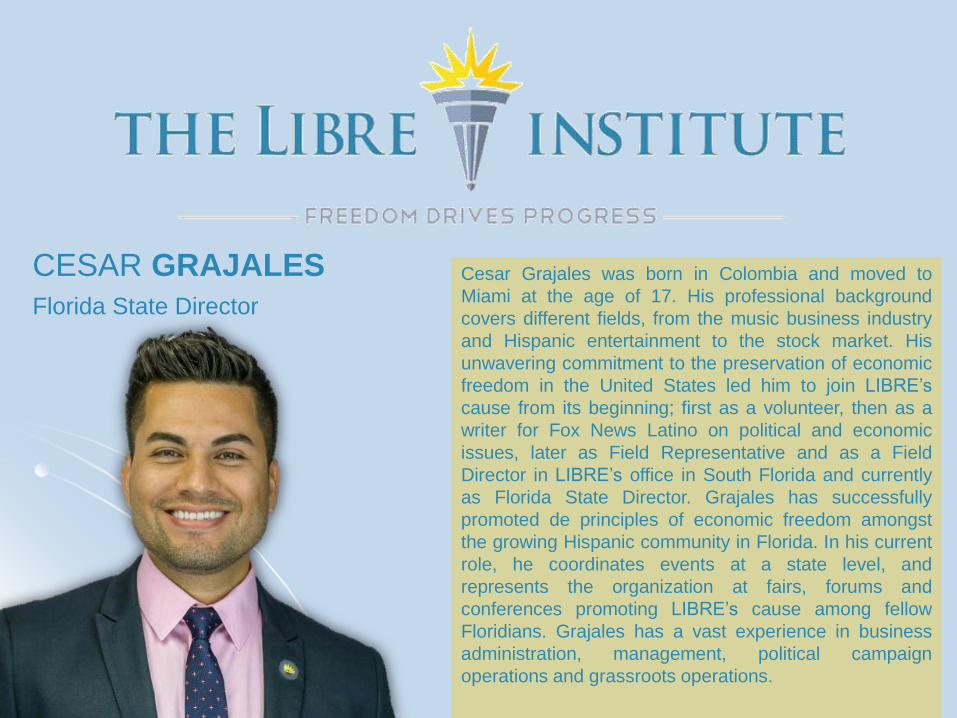

Mr. Barrera is a recognized national leader in the

business and Hispanic community. He is an attorney

with over 30 years of business, legal, non-profit and

government experience and he serves as National

Manager of Economic Prosperity for The LIBRE

Institute. Mr. Barrera previously served as President

of the Business Information Clearinghouse (BIC) Mr.

Barrera also served as President and CEO of the

United States Hispanic Chamber of Commerce

(USHCC). Mr. Barrera received his law degree from

the University of Texas School Of Law in 1989 and a

bachelor’s degree from Kansas State University in

1982. He was also educated at Harvard Business

School and the Marshall School of Business at USC.

He has previously been named one of the Top 100

Hispanics in Business as well as one of the Top

Diversity Advocates in America. He currently lives in

Kansas City, MO.

MICHAEL BARRERA

National Manager Economic Prosperity

Hispanic Financial Planning

Michael BarreraNational Manager Economic Prosperity

The LIBRE Institutewww.thelibreinstitute.org

The LIBRE Institute is a non-profit, non-partisan C3 organization. It is committed to strengthening America and building prosperous Hispanic communities through Our Four Pillars that focus on Economic Prosperity, Education, Faith, and Family

Surveys indicate that Hispanics want more information on personal finances and entrepreneurship.

Economic Prosperity Pillar seeks to increase the level of independence within the U.S. Hispanic community by further educating the community on Financial Wellness and Entrepreneurship.

Independence and self-sufficiency create Freedom and Freedom Drives Progress

The LIBRE Institute

What is the Institute?

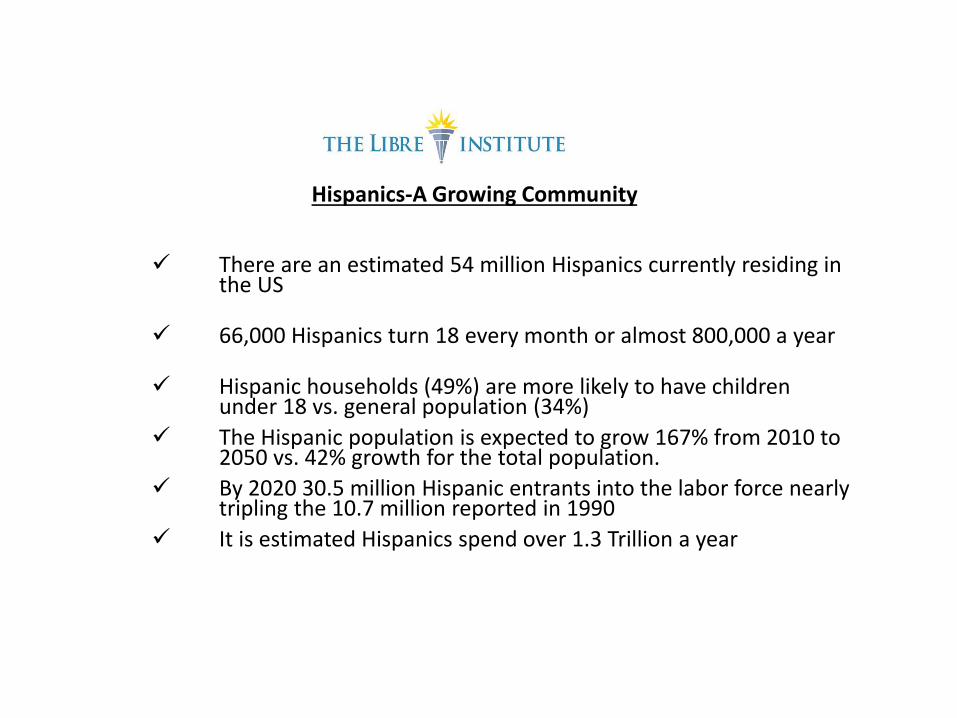

There are an estimated 54 million Hispanics currently residing in the US

66,000 Hispanics turn 18 every month or almost 800,000 a year

Hispanic households (49%) are more likely to have children under 18 vs. general population (34%)

The Hispanic population is expected to grow 167% from 2010 to 2050 vs. 42% growth for the total population.

By 2020 30.5 million Hispanic entrants into the labor force nearly tripling the 10.7 million reported in 1990

It is estimated Hispanics spend over 1.3 Trillion a year

Hispanics-A Growing Community

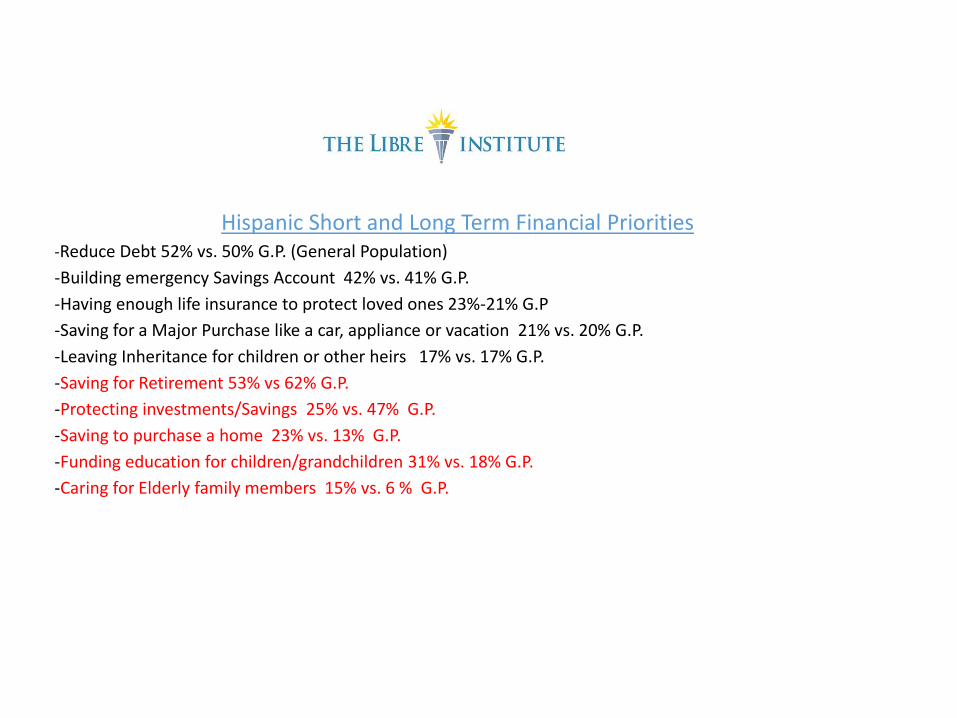

Hispanic Short and Long Term Financial Priorities-Reduce Debt 52% vs. 50% G.P. (General Population)

-Building emergency Savings Account 42% vs. 41% G.P.

-Having enough life insurance to protect loved ones 23%-21% G.P

-Saving for a Major Purchase like a car, appliance or vacation 21% vs. 20% G.P.

-Leaving Inheritance for children or other heirs 17% vs. 17% G.P.

-Saving for Retirement 53% vs 62% G.P.

-Protecting investments/Savings 25% vs. 47% G.P.

-Saving to purchase a home 23% vs. 13% G.P.

-Funding education for children/grandchildren 31% vs. 18% G.P.

-Caring for Elderly family members 15% vs. 6 % G.P.

Hispanic Financial Stats

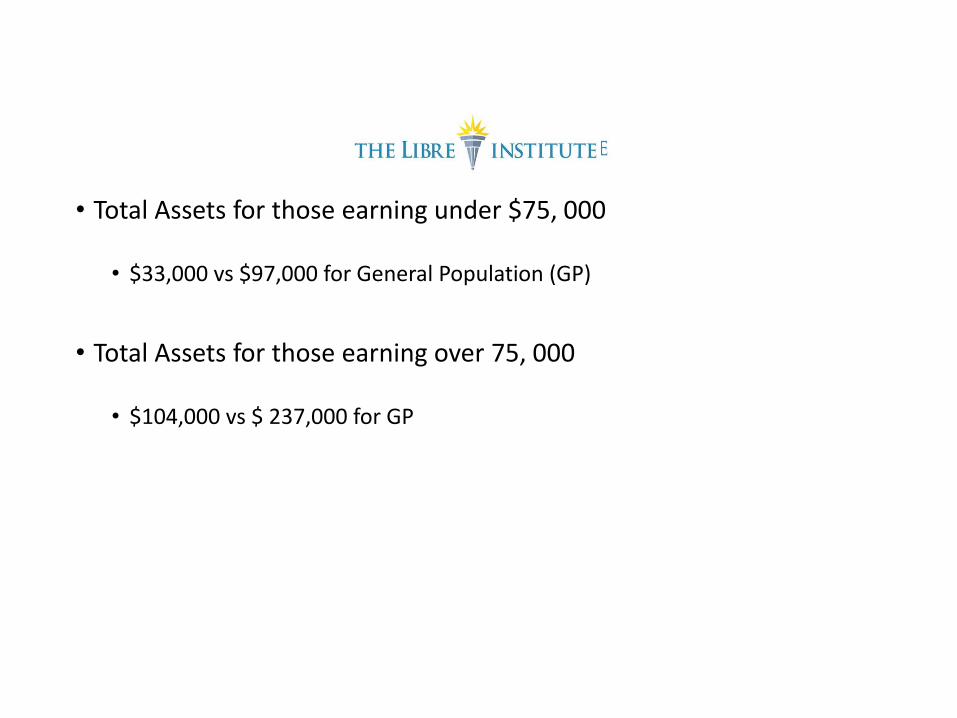

• Total Assets for those earning under $75, 000

• $33,000 vs $97,000 for General Population (GP)

• Total Assets for those earning over 75, 000

• $104,000 vs $ 237,000 for GP

National Debt

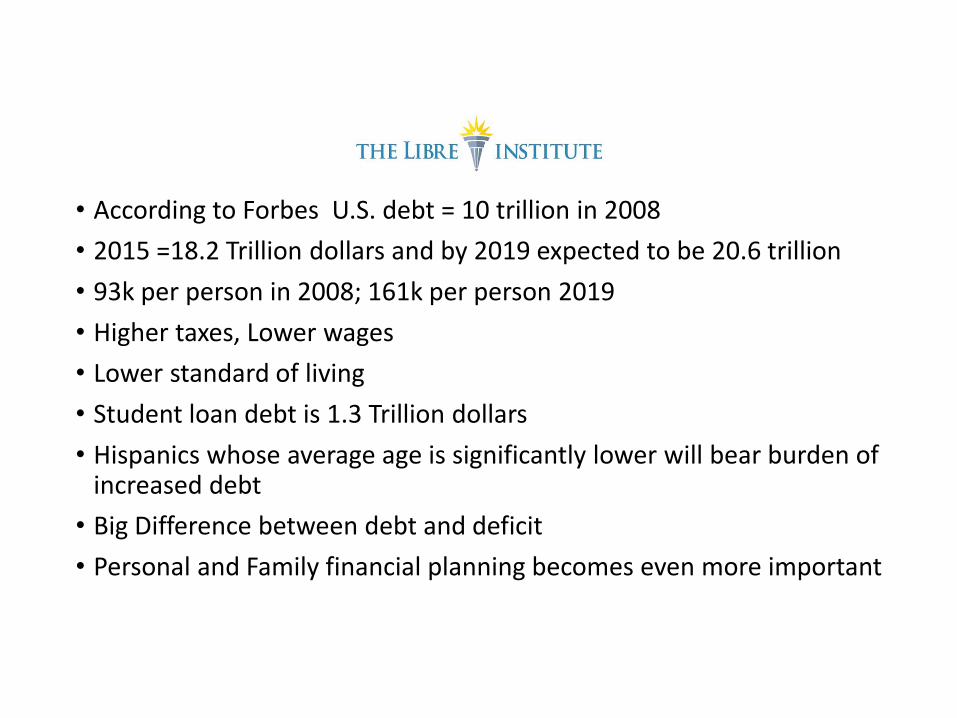

• According to Forbes U.S. debt = 10 trillion in 2008

• 2015 =18.2 Trillion dollars and by 2019 expected to be 20.6 trillion

• 93k per person in 2008; 161k per person 2019

• Higher taxes, Lower wages

• Lower standard of living

• Student loan debt is 1.3 Trillion dollars

• Hispanics whose average age is significantly lower will bear burden of increased debt

• Big Difference between debt and deficit

• Personal and Family financial planning becomes even more important

Other Financial Considerations

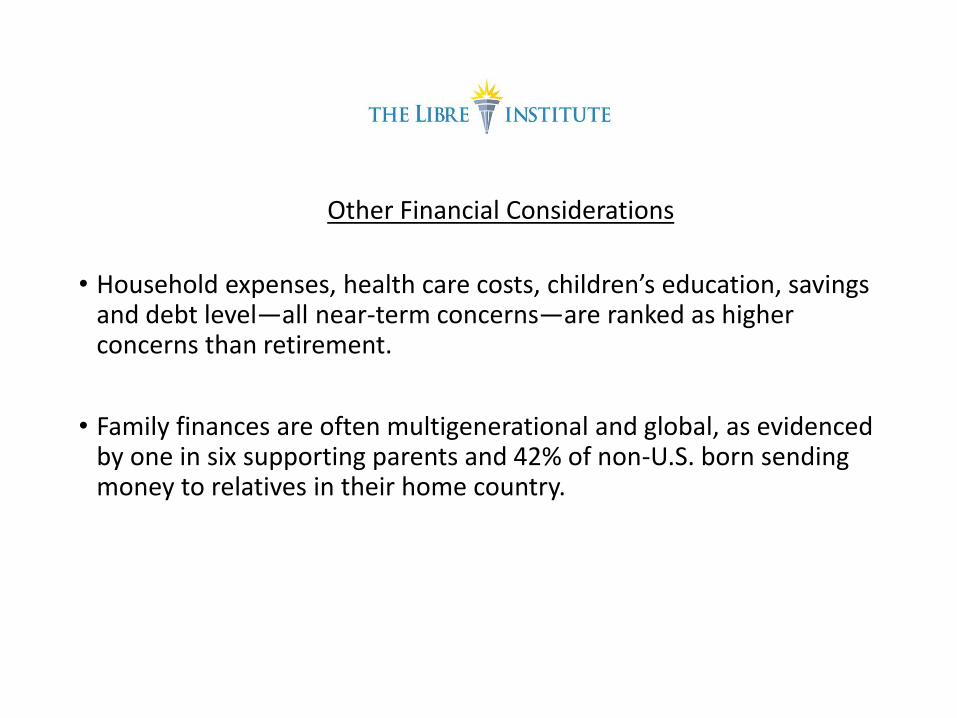

• Household expenses, health care costs, children’s education, savings and debt level—all near-term concerns—are ranked as higher concerns than retirement.

• Family finances are often multigenerational and global, as evidenced by one in six supporting parents and 42% of non-U.S. born sending money to relatives in their home country.

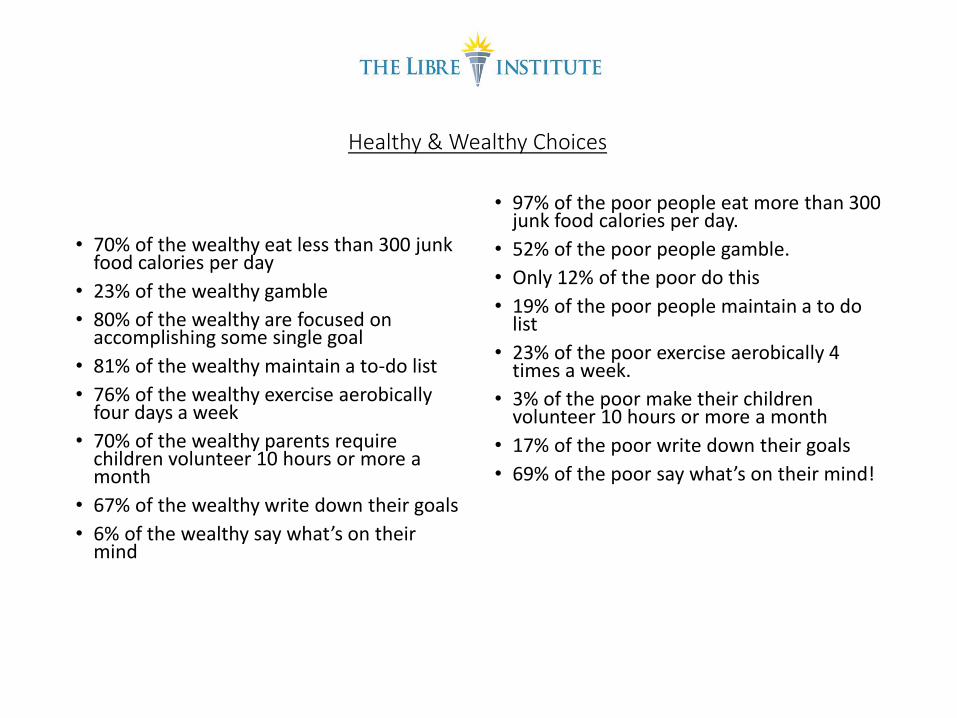

Healthy & Wealthy Choices

• 70% of the wealthy eat less than 300 junk food calories per day

• 23% of the wealthy gamble

• 80% of the wealthy are focused on accomplishing some single goal

• 81% of the wealthy maintain a to-do list

• 76% of the wealthy exercise aerobically four days a week

• 70% of the wealthy parents require children volunteer 10 hours or more a month

• 67% of the wealthy write down their goals

• 6% of the wealthy say what’s on their mind

• 97% of the poor people eat more than 300 junk food calories per day.

• 52% of the poor people gamble.

• Only 12% of the poor do this

• 19% of the poor people maintain a to do list

• 23% of the poor exercise aerobically 4 times a week.

• 3% of the poor make their children volunteer 10 hours or more a month

• 17% of the poor write down their goals

• 69% of the poor say what’s on their mind!

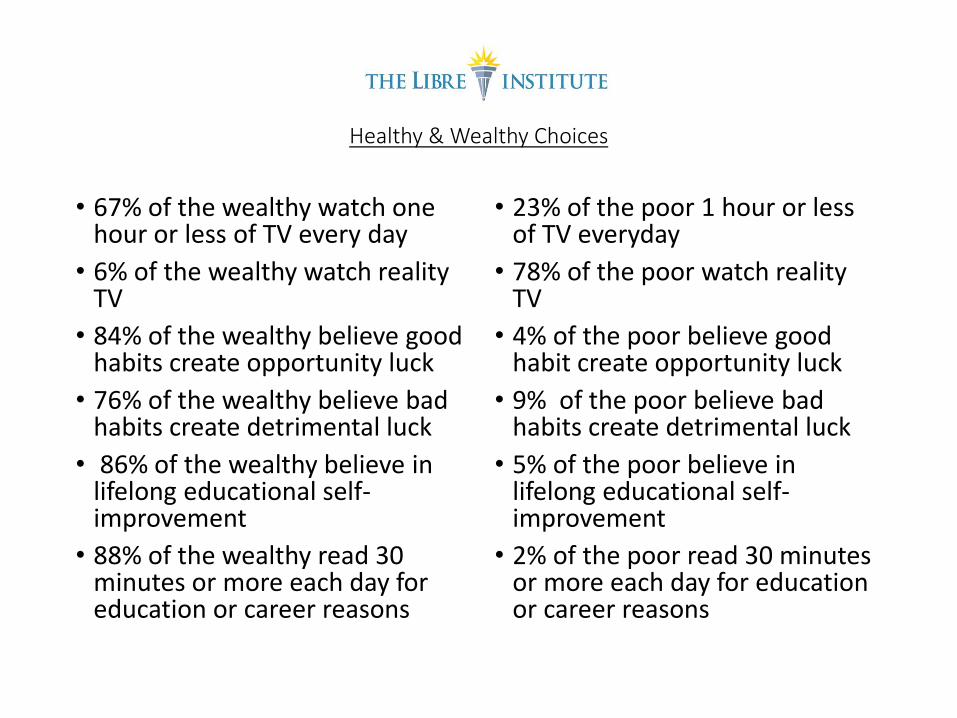

Healthy & Wealthy Choices

• 67% of the wealthy watch one hour or less of TV every day

• 6% of the wealthy watch reality TV

• 84% of the wealthy believe good habits create opportunity luck

• 76% of the wealthy believe bad habits create detrimental luck

• 86% of the wealthy believe in lifelong educational self-improvement

• 88% of the wealthy read 30 minutes or more each day for education or career reasons

• 23% of the poor 1 hour or less of TV everyday

• 78% of the poor watch reality TV

• 4% of the poor believe good habit create opportunity luck

• 9% of the poor believe bad habits create detrimental luck

• 5% of the poor believe in lifelong educational self-improvement

• 2% of the poor read 30 minutes or more each day for education or career reasons

Mr. Dore-Bernhard earned his finance degree from

Florida International University. He then went on to

pursue his MBA at Nova Southeastern University. He

has held various investment, insurance and mortgage

licenses. His experience in financial planning expands

from bank telling, to having been the youngest

investment portfolio manager at one of the big four US

Banks at the early age of 24. In addition Mr. Bernhard

has been a private banker, a business owner in the

mortgage, insurance, and financial consulting areas, an

occasional writer and a contributor of financial topics

to newspapers and websites. He is committed to

excellence in his work and service, he is goal-oriented,

organized, disciplined, and he demonstrates leadership

based on principles and values. His favorite quote is:

“Change your focus, from making money to serving

more people. Serving more people makes the money

come in.” – Robert Kiyosaki..

MARIO DORE-BERNHARDFinancial Advisor

ClearPoint’s Hispanic Center for

Financial Excellence (HCFE)

ClearPointCCS.org

ClearPointSurviving on a Limited Budget

Mario Dore-Bernhard

Financial Advisor

305.592.9298 - Ext. 2135

ClearPointCCS.org

Objectives

Create a spending plan to help you get

back to basics

Identify ways to increase income and

help you survive on a limited budget

Identify ways to reduce financial stress

and handle your financial situation

ClearPointCCS.org

How Can I Succeed On a Limited Budget?

ClearPointCCS.org

Step 1: Create a Priority Spending Plan

List your current income and expenses

ClearPointCCS.org

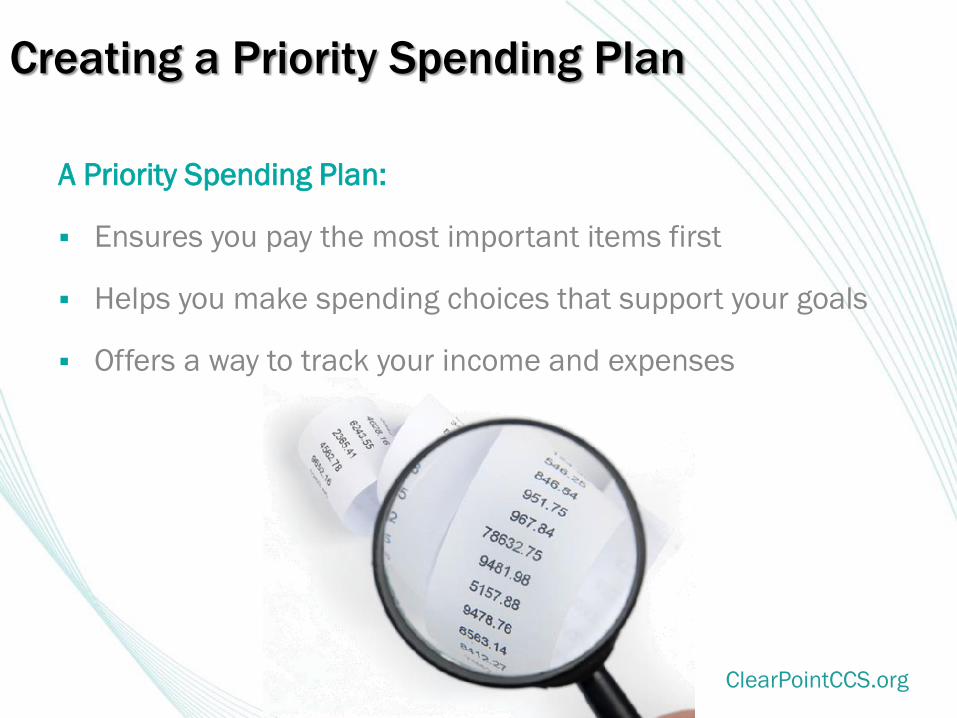

Creating a Priority Spending Plan

A Priority Spending Plan:

Ensures you pay the most important items first

Helps you make spending choices that support your goals

Offers a way to track your income and expenses

ClearPointCCS.org

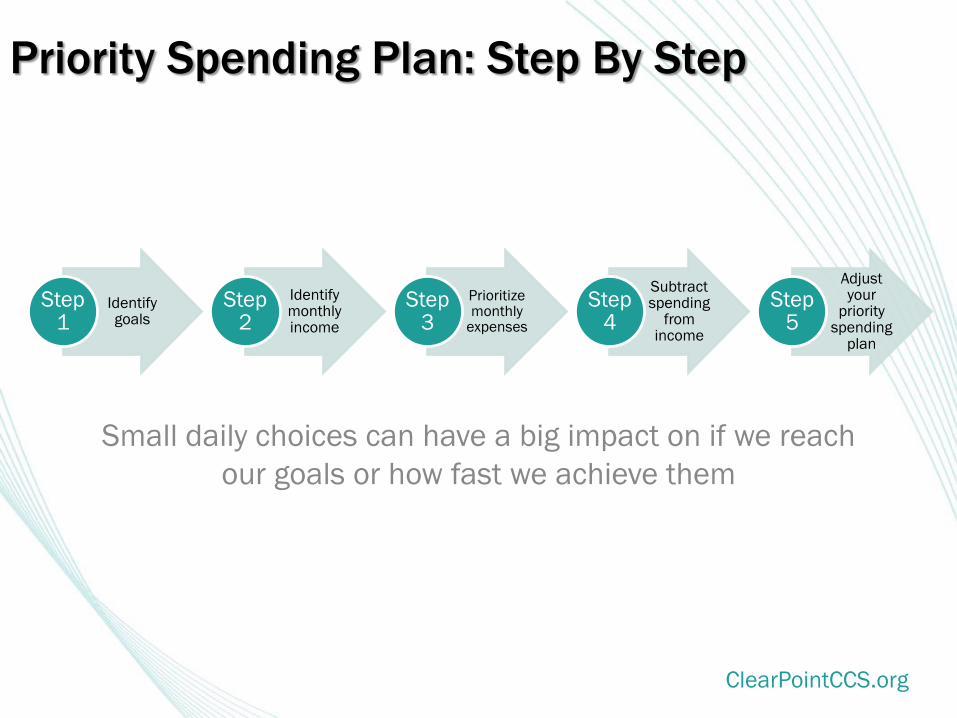

Priority Spending Plan: Step By Step

Identify goals

Step 1

Identify monthly income

Step 2

Prioritize monthly

expenses

Step 3

Subtract spending

from income

Step 4

Adjust your

priority spending

plan

Step 5

Small daily choices can have a big impact on if we reach

our goals or how fast we achieve them

ClearPointCCS.org

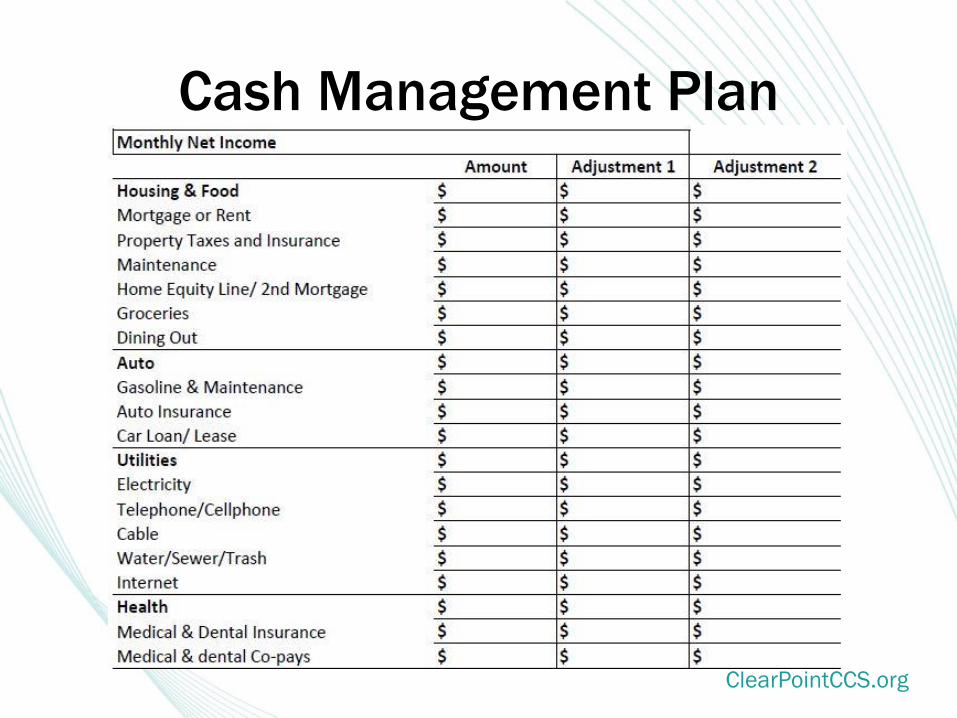

Cash Management Plan

ClearPointCCS.org

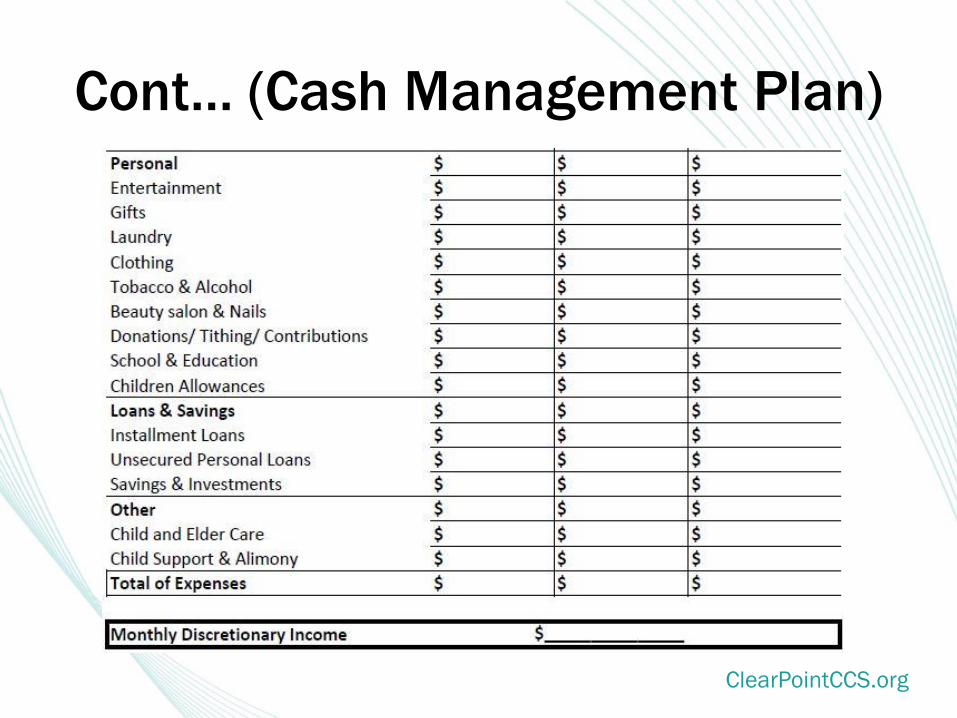

Cont… (Cash Management Plan)

ClearPointCCS.org

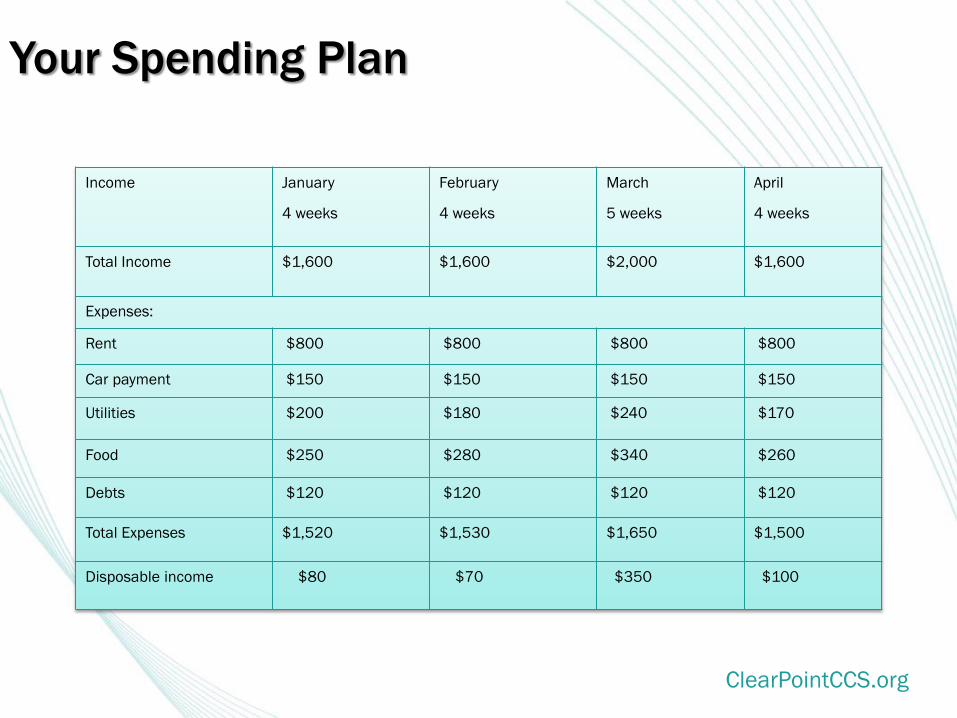

Your Spending Plan

Income January

4 weeks

February

4 weeks

March

5 weeks

April

4 weeks

Total Income $1,600 $1,600 $2,000 $1,600

Expenses:

Rent $800 $800 $800 $800

Car payment $150 $150 $150 $150

Utilities $200 $180 $240 $170

Food $250 $280 $340 $260

Debts $120 $120 $120 $120

Total Expenses $1,520 $1,530 $1,650 $1,500

Disposable income $80 $70 $350 $100

ClearPointCCS.org

Where Does Your Money Go?

Track your expenses for 30 days

Total all columns and expenses

Review your overall expenses

ClearPointCCS.org

Where Does Your Money Go?

Fixed expenses:

The same each month

Variable expenses:

Different each month

Periodic expenses:

Due once or twice a year

ClearPointCCS.org

What Are Your Spending Habits?

Observe how you feel when you need to spend

Avoid going to stores when you feel the need to spend

Substitute the need to spend with something different

Leave your credit cards at home whenever possible

ClearPointCCS.org

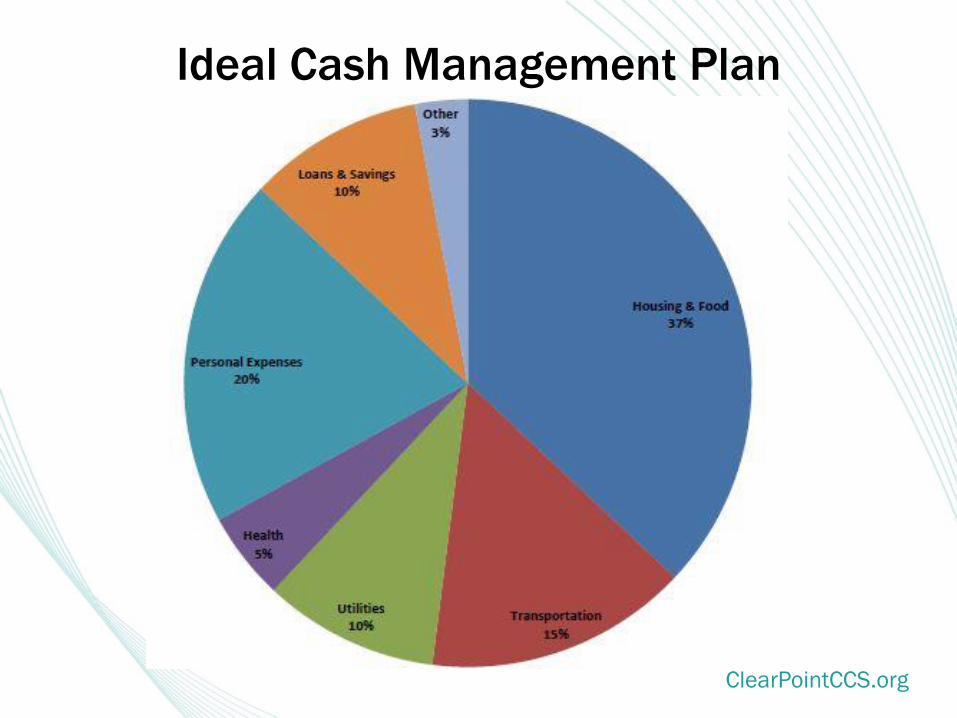

Ideal Cash Management Plan

ClearPointCCS.org

Step 2: Differentiate Between Wants and Needs

If expenses exceed income, adjust

your spending plan

ClearPointCCS.org

Essential Needs

• Housing

• Food

• Utilities

• Transportation

ClearPointCCS.org

Step 3: Identify ways to

increase income

• Part-time job / freelance work

• Ask family members for help (e.g. rent contribution, child care)

• Small business

• Public assistance

• Roommate

• Garage sale / online sales (e.g. eBay)

• Cut costs / reduce unnecessary expenses (e.g. gym, cel phone, cable)

ClearPointCCS.org

How Can You Save?

Take lunch to work and eat at

home more

Use coupons, buy store brands

or buy in bulk at club stores

Give handmade cards and gifts

Consolidate plans and services

Utilize free resources at the

library and online

ClearPointCCS.org

Saving to Reach Your Goals

Determine the amount

you can save each month

after expenses

Assign those savings to

each goal

Modify the term to reach

your goals accordingly

Adjust as necessary

ClearPointCCS.org

Reduce Financial Stress

Develop a priority spending plan and debt reduction plan

De-clutter your home

Communicate with your family and

set realistic expectations

Shop with a purpose

Adopt a ‘less is more’ attitude

Eliminate barriers to your success

ClearPointCCS.org

Reduce Emotional Stress

Develop a healthy living plan

Exercise regularly

Get proper nutrition

Maintain relationships with

friends and family

ClearPointCCS.org

Monitor your Progress

ClearPointCCS.org

Succeeding on a Limited Budget!

ClearPointCCS.org

ClearPoint

Thank You for Attending

For more information, visit our website

www.ClearPointCCS.org/HCFE

To set up a counseling appointment,

call us at 305.592.9298 - Ext. 2135

Mario Dore-Bernhard

Financial Advisor

ClearPointCCS.org

ClearPoint

How Do I Get Out of Debt?

Mario Dore-Bernhard

Financial Advisor

305.592.9298 - Ext. 2135ClearPointCCS.org

ClearPointCCS.org

Objectives

Understand the difference between

good debt and bad debt

Identify how small costs add up

Build a workable plan to pay down

debts

ClearPointCCS.org

What Would Your Life Be Like Without Debt?

How much money would you save each month to achieve

your dreams and goals?

ClearPointCCS.org

Good Debt vs. Bad Debt

ClearPointCCS.org

Unexpected Emergencies

ClearPointCCS.org

Understand Why You Are In Debt

Understand why you are

in debt

Observe how you feel

Give each dollar a

purpose

ClearPointCCS.org

Always Spend Less Than You Make

EXPENSES

INCOME

ClearPointCCS.org

Small Costs Add Up

Car Repair

Movies

Coffee

Prescriptions Dining

ClearPointCCS.org

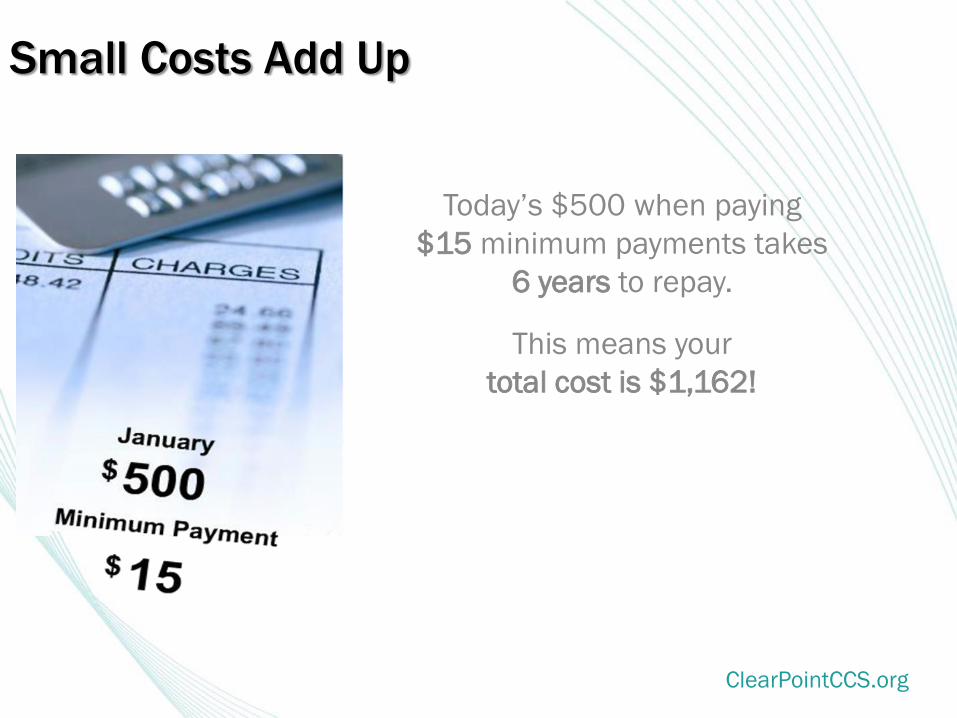

Small Costs Add Up

Today’s $500 when paying

$15 minimum payments takes

6 years to repay.

This means your

total cost is $1,162!

ClearPointCCS.org

Find Additional Dollars

Take lunch to work and cook meals at home

Use grocery coupons and buy store brands

Unplug computers, TVs and other utilities

Bundle services for possible discounts

Buy in bulk at club stores

Utilize websites and online resources

Check out books from the library

Look for ways to generate income

ClearPointCCS.org

Build a Workable Plan to Pay Down Debts

ClearPointCCS.org

Maria and Juan

Wanted to save for a down

payment on a home

5 credit cards combined

$8,000 total debt

ClearPointCCS.org

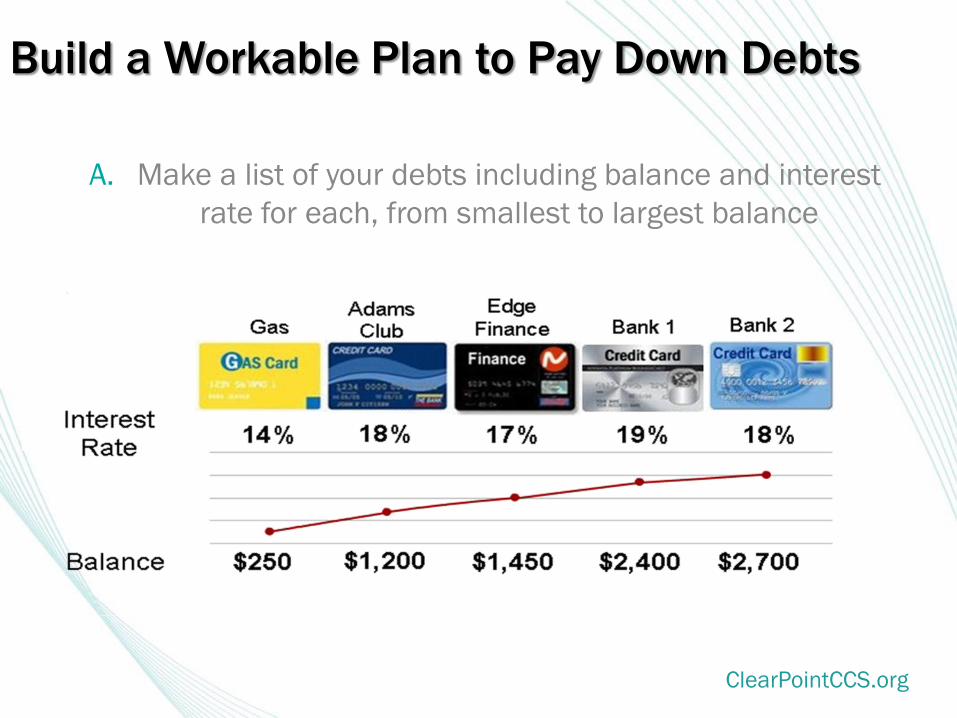

Build a Workable Plan to Pay Down Debts

A. Make a list of your debts including balance and interest

rate for each, from smallest to largest balance

ClearPointCCS.org

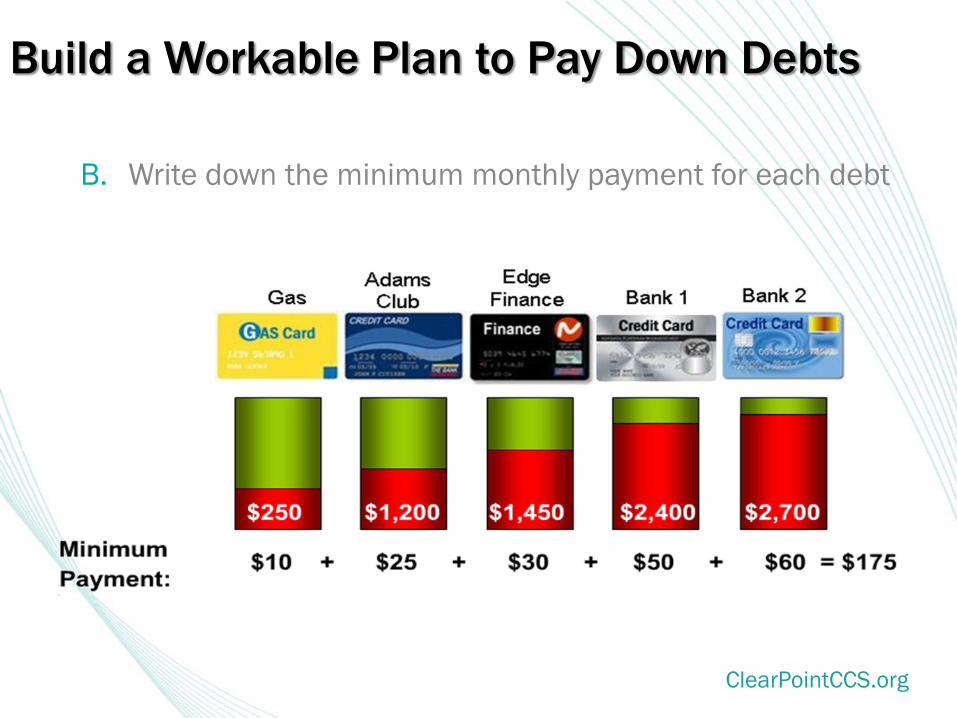

Build a Workable Plan to Pay Down Debts

B. Write down the minimum monthly payment for each debt

ClearPointCCS.org

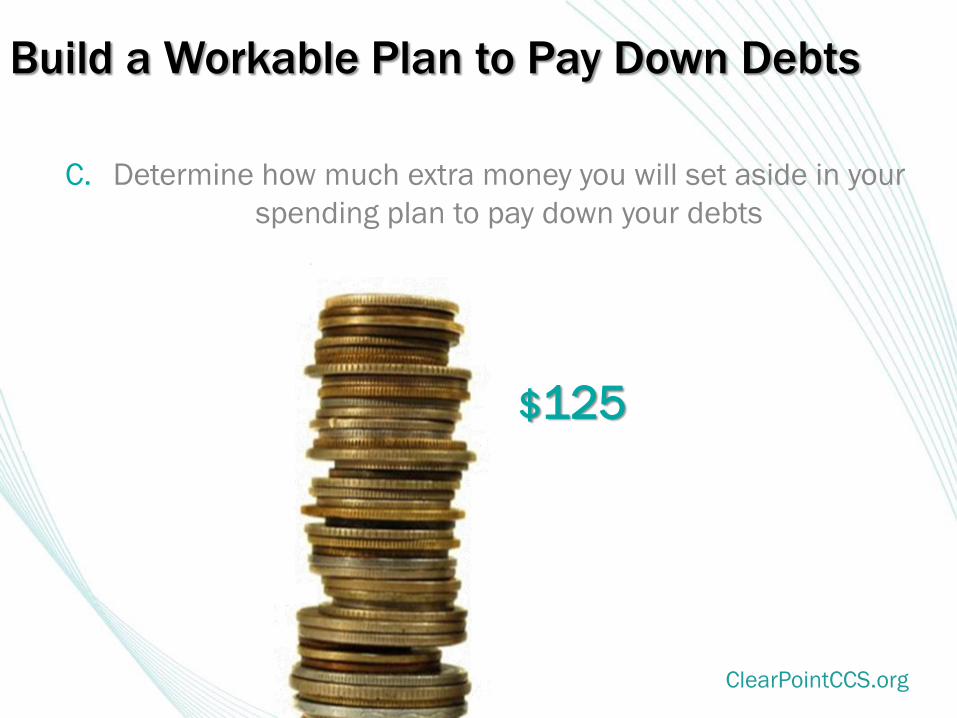

Build a Workable Plan to Pay Down Debts

C. Determine how much extra money you will set aside in your

spending plan to pay down your debts

$125

ClearPointCCS.org

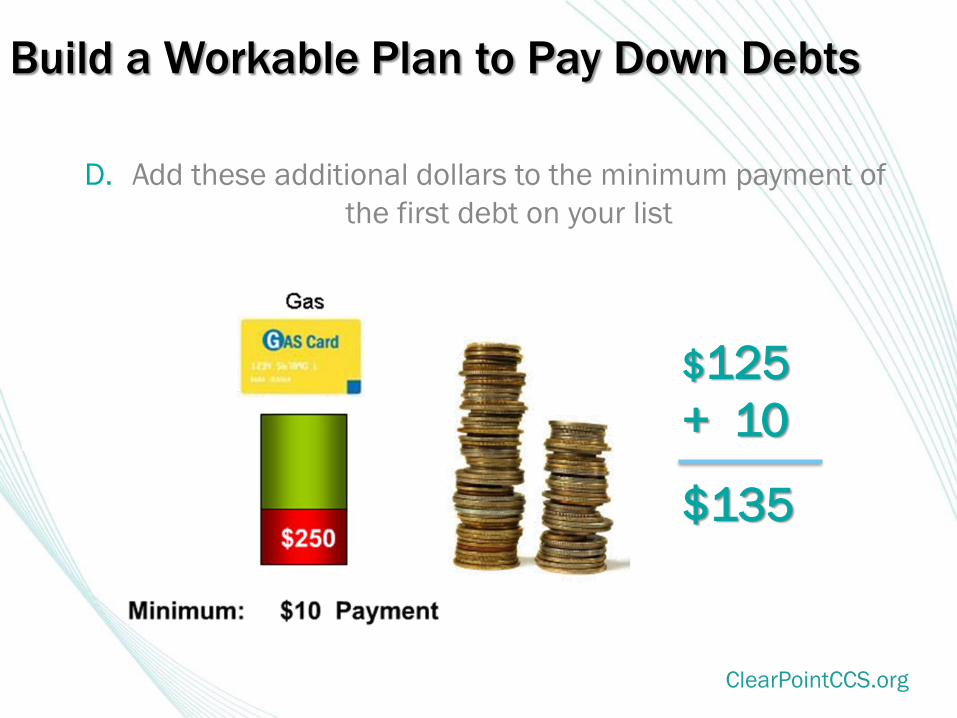

Build a Workable Plan to Pay Down Debts

D. Add these additional dollars to the minimum payment of

the first debt on your list

$125

+ 10

$135

ClearPointCCS.org

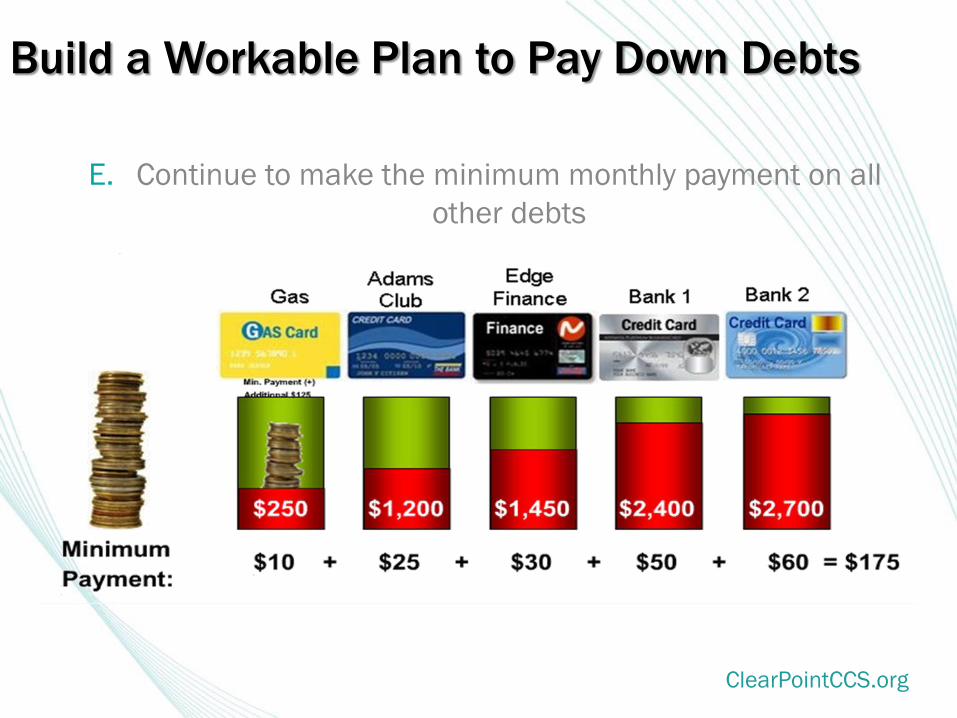

Build a Workable Plan to Pay Down Debts

E. Continue to make the minimum monthly payment on all

other debts

ClearPointCCS.org

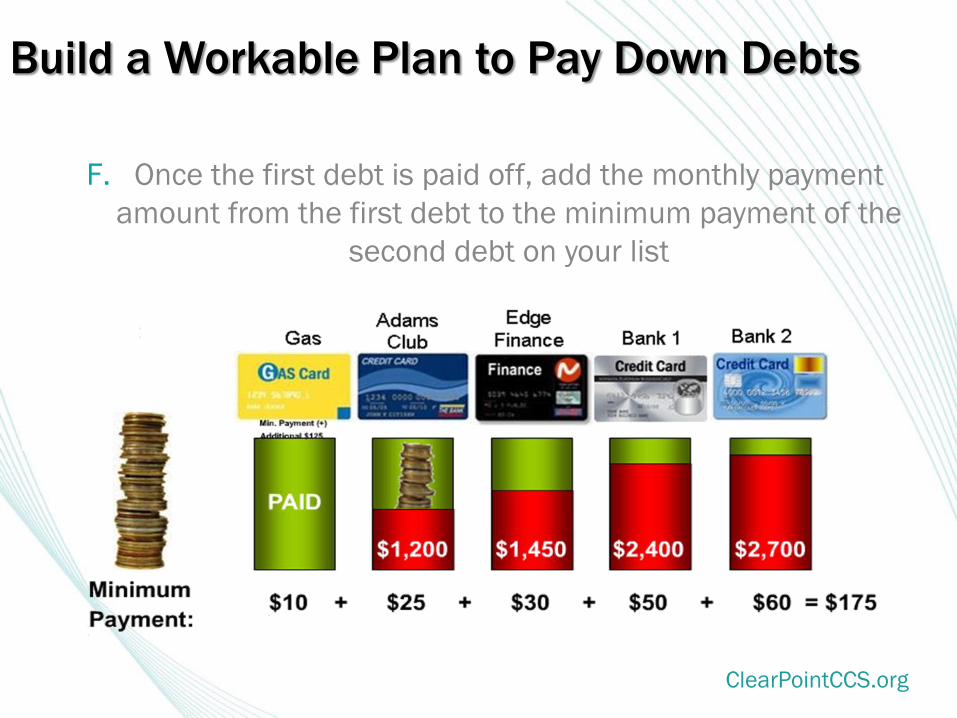

Build a Workable Plan to Pay Down Debts

F. Once the first debt is paid off, add the monthly payment

amount from the first debt to the minimum payment of the

second debt on your list

ClearPointCCS.org

Build a Workable Plan to Pay Down Debts

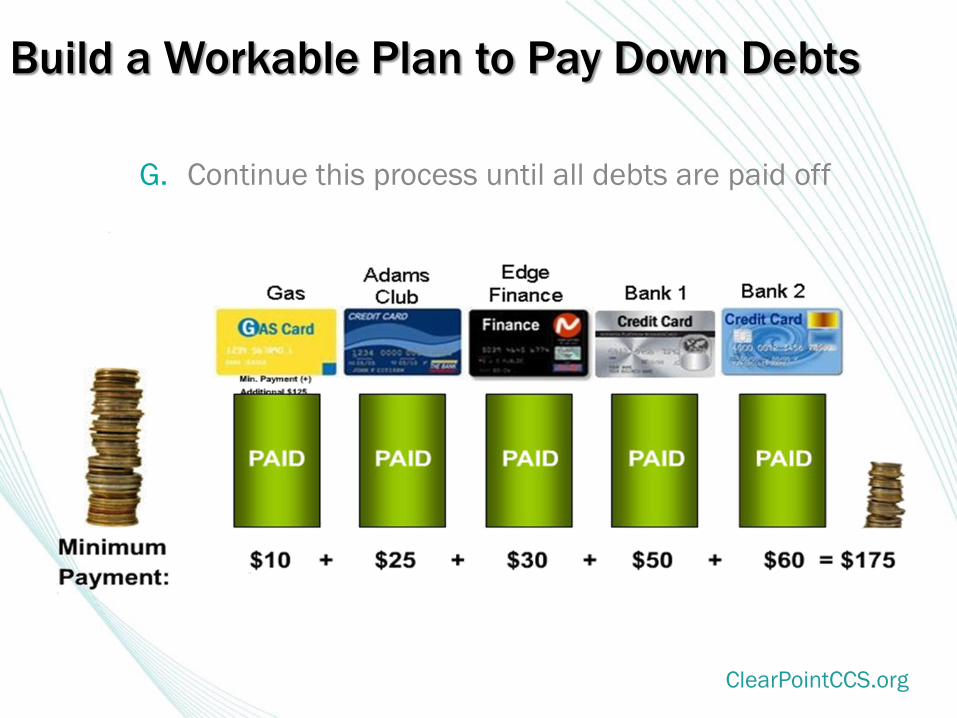

G. Continue this process until all debts are paid off

ClearPointCCS.org

Build a Workable Plan to Pay Down Debts

H. Use any additional income you receive as additional money

to pay down your debts

ClearPointCCS.org

Build a Workable Plan to Pay Down Debts

Do not put more debt on any of these credit cards while they

are being paid off

ClearPointCCS.org

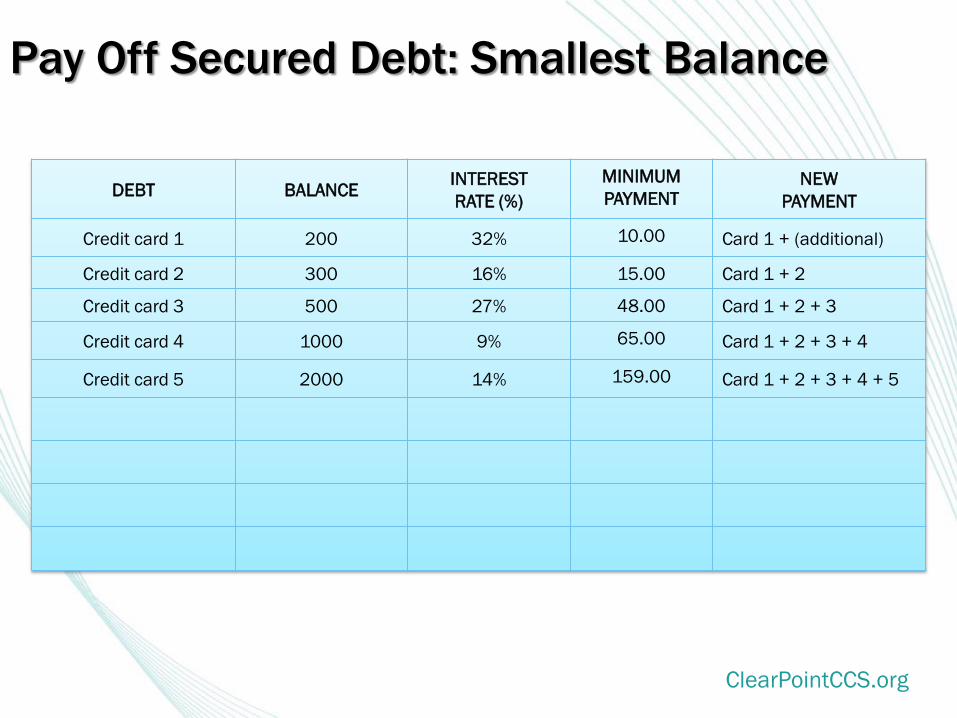

Pay Off Secured Debt: Smallest Balance

DEBT BALANCEINTEREST

RATE (%)

MINIMUM

PAYMENTNEW

PAYMENT

Credit card 1 200 32% 10.00 Card 1 + (additional)

Credit card 2 300 16% 15.00 Card 1 + 2

Credit card 3 500 27% 48.00 Card 1 + 2 + 3

Credit card 4 1000 9% 65.00 Card 1 + 2 + 3 + 4

Credit card 5 2000 14% 159.00 Card 1 + 2 + 3 + 4 + 5

ClearPointCCS.org

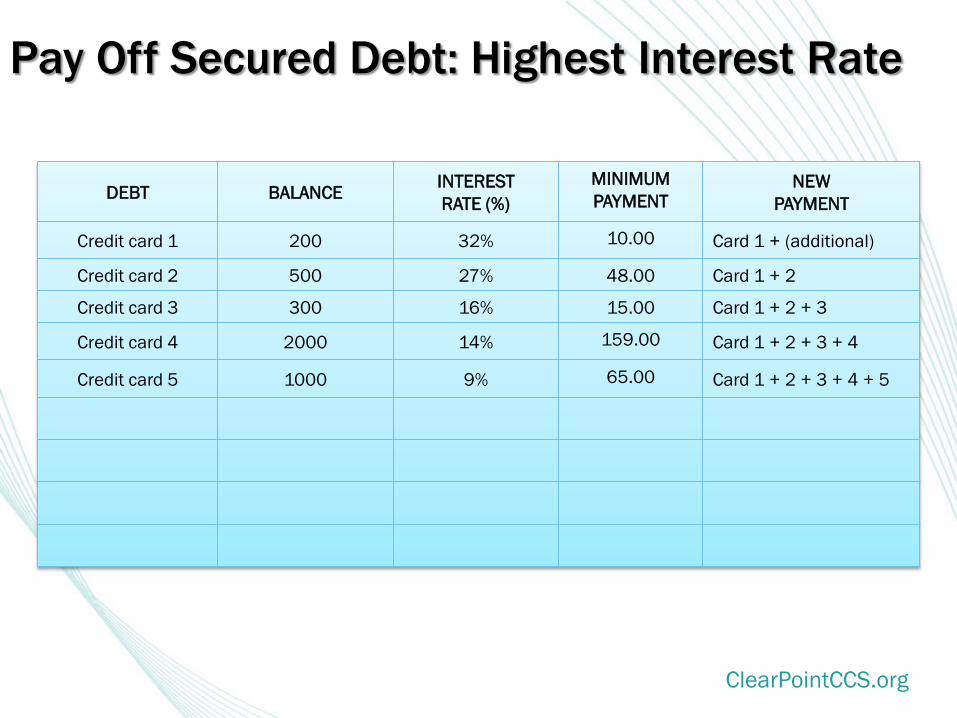

Pay Off Secured Debt: Highest Interest Rate

DEBT BALANCEINTEREST

RATE (%)

MINIMUM

PAYMENTNEW

PAYMENT

Credit card 1 200 32% 10.00 Card 1 + (additional)

Credit card 2 500 27% 48.00 Card 1 + 2

Credit card 3 300 16% 15.00 Card 1 + 2 + 3

Credit card 4 2000 14% 159.00 Card 1 + 2 + 3 + 4

Credit card 5 1000 9% 65.00 Card 1 + 2 + 3 + 4 + 5

ClearPointCCS.org

After Unsecured Debt is Paid Off

Consider paying off

secured debt

Build up savings or

retirement accounts

Pay off new debts

ClearPointCCS.org

Pay Off Secured Debt

If you are unable to build a workable

plan to pay down your debts, contact

ClearPoint to help you by implementing

a debt management plan.

ClearPointCCS.org

Summary

Understand the difference between

good debt and bad debt

Identify how small costs add up

Build a workable plan to pay down

debts

ClearPointCCS.org

ClearPoint

Thank You for Attending

For more information, visit our website

www.ClearPointCCS.org/HCFE

To set up a counseling appointment,

call us at 305.592.9298 - Ext. 2135

Mario Dore-Bernhard

Financial Advisor

ClearPointCCS.org

ClearPoint

Financial Success Starts Here

Mario Dore-Bernhard

Financial Advisor

305.592.9298 - Ext. 2135

ClearPointCCS.org

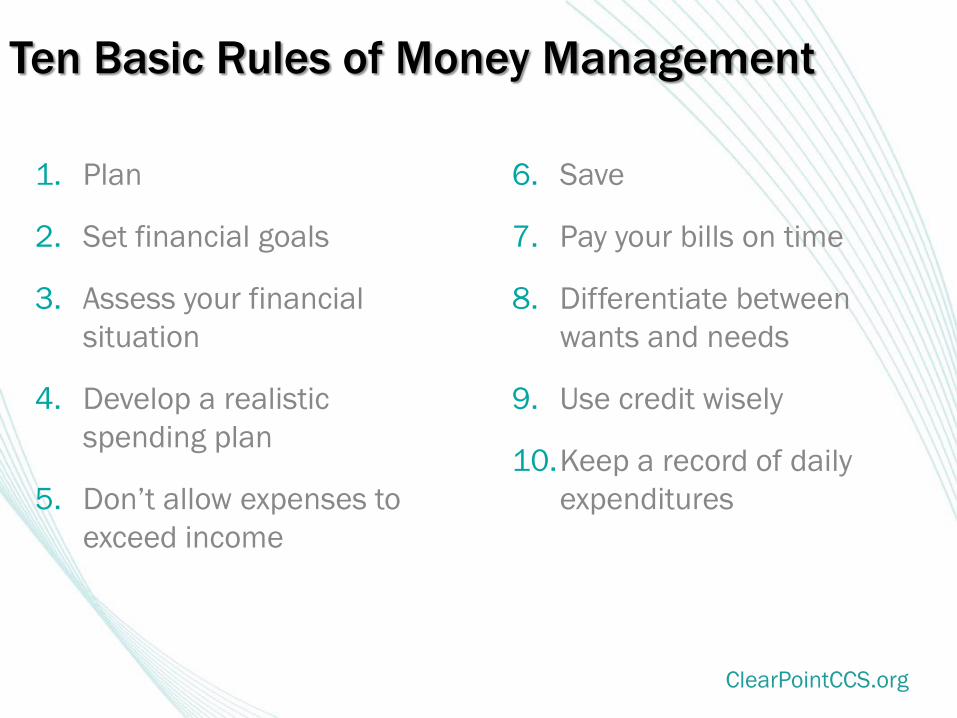

Ten Basic Rules of Money Management

1. Plan

2. Set financial goals

3. Assess your financial

situation

4. Develop a realistic

spending plan

5. Don’t allow expenses to

exceed income

6. Save

7. Pay your bills on time

8. Differentiate between

wants and needs

9. Use credit wisely

10.Keep a record of daily

expenditures

ClearPointCCS.org

What Are Your Dreams?

Car

House

Vacation

Education

ClearPointCCS.org

Can Your Dreams Become Financial Goals?

Goals are statements about things you would like to do or

accomplish. To create goals:

Start with the end in mind

Write your goals down

Make goals specific

ClearPointCCS.org

Can Your Dreams Become Financial Goals?

Set a timeline and budget to accomplish your goals

Measure your progress from time to time

Make adjustments as necessary

ClearPointCCS.org

When Will You Reach Your Goals?

•Can be accomplished within in one year

Short-term goals

•Can be accomplished in 2 to 4 years

Mid-range goals

•Can be accomplished in 5 years or more

Long-term goals

ClearPointCCS.org

If you had $5,000 what would you do with it?

Where Do You Want To Be In 5 Years?

ClearPointCCS.org

Start with the end in mind

Write down your goals

Adjust your goals as necessary

Setting Goals In 3 Simple Steps

ClearPointCCS.org

Adjust Your Goals as Necessary

ClearPointCCS.org

Financial Stability

Reserves

Insurance

Fixed assets

Variable assets

ClearPointCCS.org

Ten Basic Rules of Money Management

1. Plan

2. Set financial goals

3. Assess your financial

situation

4. Develop a realistic

spending plan

5. Don’t allow expenses to

exceed income

6. Save

7. Pay your bills on time

8. Differentiate between

wants and needs

9. Use credit wisely

10.Keep a record of daily

expenditures

ClearPointCCS.org

ClearPoint

Thank You for Attending

For more information, visit our website

www.ClearPointCCS.org/HCFE

To set up a counseling appointment,

call us at 305.592.9298 - Ext. 2135

Mario Dore-Bernhard

Financial Advisor

Ms. Sega is a self-motivated and highly

qualified professional with experience

expanding in financial planning, tax

preparation and banking. She is currently

the President of International Marketing

Agency Inc., located in Miami, Florida. She

earned her Master’s in Business

Administration at Florida International

University. She also possesses a Bachelor

of Economy and a Computer Associate

degree. Ms. Sega has served as a loan

officer for Bank of America and JP Morgan

Chase. In addition she has and continues to

serve as the President of the Peruvian

American Chamber of Commerce.

MARICARMEN SEGAPresident, International

Marketing Agency, Inc.

Video link

MARICARMEN SEGAPresident, International

Marketing Agency, Inc.

MARICARMEN SEGA

TAX & ACCOUNTING

(786) 290-2899

INTERNATIONAL MARKETING AGENCY INC.

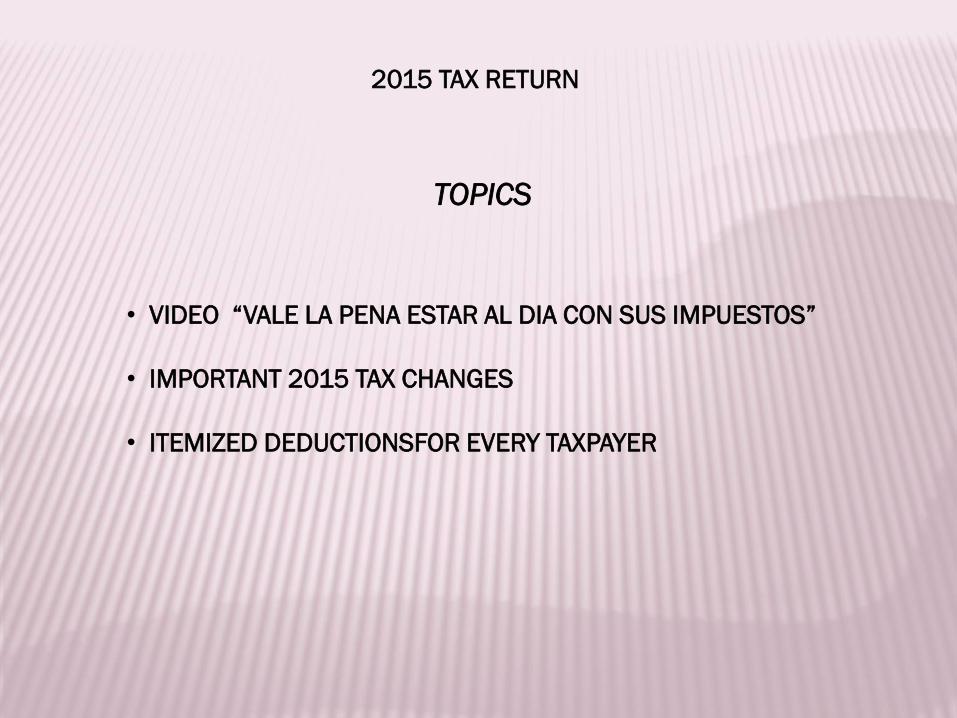

2015 TAX RETURN

TOPICS

• VIDEO “VALE LA PENA ESTAR AL DIA CON SUS IMPUESTOS”

• IMPORTANT 2015 TAX CHANGES

• ITEMIZED DEDUCTIONSFOR EVERY TAXPAYER

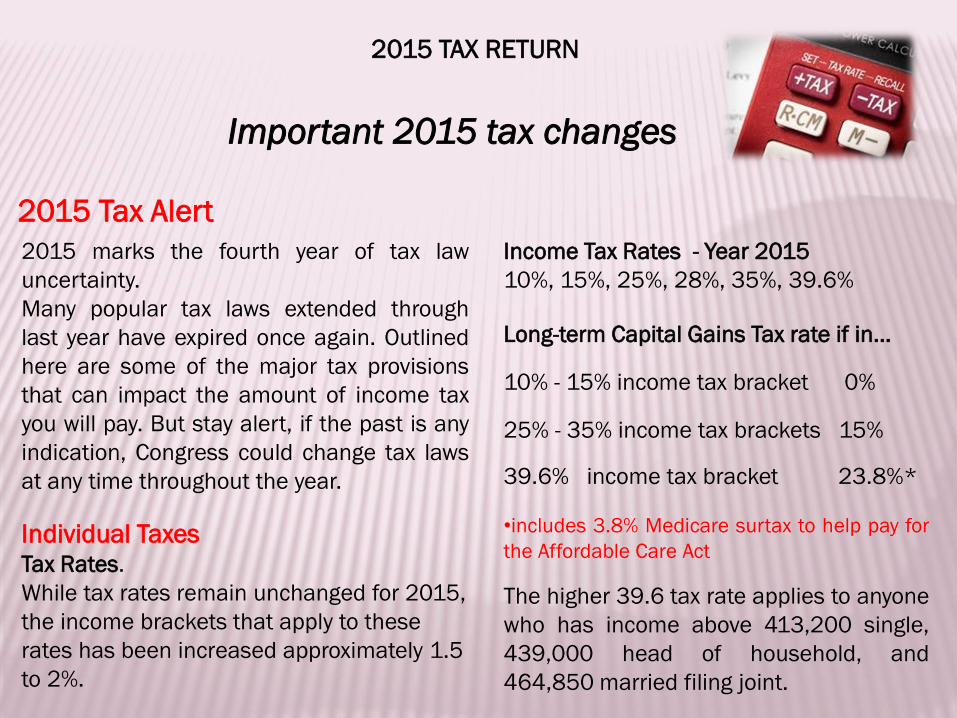

2015 marks the fourth year of tax law

uncertainty.

Many popular tax laws extended through

last year have expired once again. Outlined

here are some of the major tax provisions

that can impact the amount of income tax

you will pay. But stay alert, if the past is any

indication, Congress could change tax laws

at any time throughout the year.

Individual TaxesTax Rates.

While tax rates remain unchanged for 2015,

the income brackets that apply to these

rates has been increased approximately 1.5

to 2%.

Income Tax Rates - Year 2015

10%, 15%, 25%, 28%, 35%, 39.6%

Long-term Capital Gains Tax rate if in…

10% - 15% income tax bracket 0%

25% - 35% income tax brackets 15%

39.6% income tax bracket 23.8%*

•includes 3.8% Medicare surtax to help pay for

the Affordable Care Act

The higher 39.6 tax rate applies to anyone

who has income above 413,200 single,

439,000 head of household, and

464,850 married filing joint.

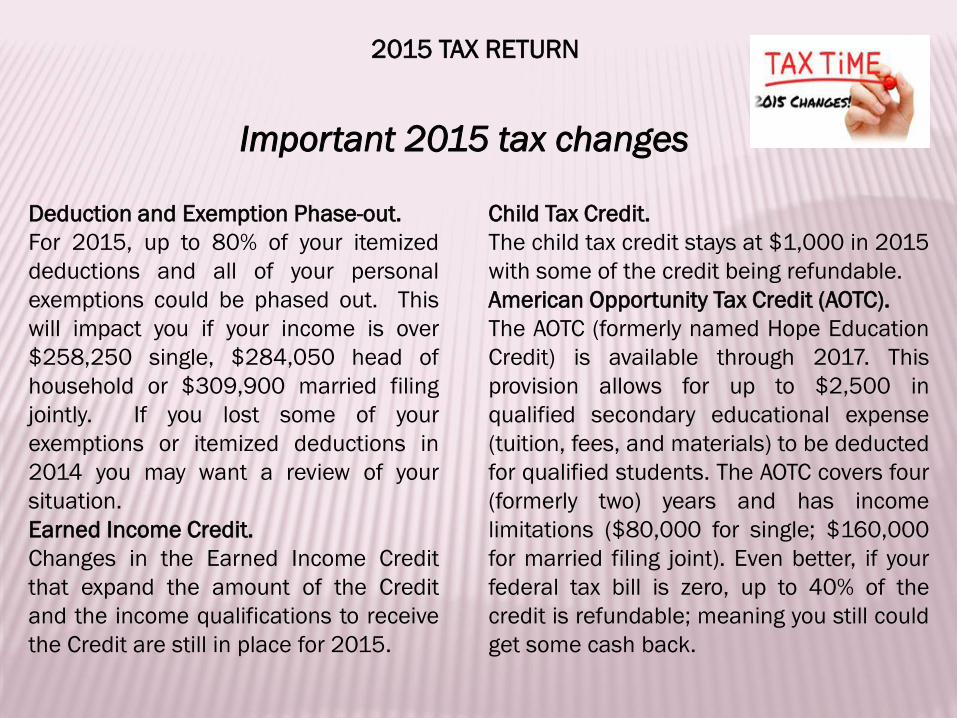

Important 2015 tax changes

2015 TAX RETURN

2015 Tax Alert

Deduction and Exemption Phase-out.

For 2015, up to 80% of your itemized

deductions and all of your personal

exemptions could be phased out. This

will impact you if your income is over

$258,250 single, $284,050 head of

household or $309,900 married filing

jointly. If you lost some of your

exemptions or itemized deductions in

2014 you may want a review of your

situation.

Earned Income Credit.

Changes in the Earned Income Credit

that expand the amount of the Credit

and the income qualifications to receive

the Credit are still in place for 2015.

Child Tax Credit.

The child tax credit stays at $1,000 in 2015

with some of the credit being refundable.

American Opportunity Tax Credit (AOTC).

The AOTC (formerly named Hope Education

Credit) is available through 2017. This

provision allows for up to $2,500 in

qualified secondary educational expense

(tuition, fees, and materials) to be deducted

for qualified students. The AOTC covers four

(formerly two) years and has income

limitations ($80,000 for single; $160,000

for married filing joint). Even better, if your

federal tax bill is zero, up to 40% of the

credit is refundable; meaning you still could

get some cash back.

Important 2015 tax changes

2015 TAX RETURN

Health Care Savings Accounts.

The Health Care Savings Account (HSA)

annual contribution limits for those in

qualified high deductible health

insurance plans is $3,350 for a single

taxpayer and $6,650 for a family. If you

are age 55 or over the amount increases

by $1,000.

Social Security Limits.

In 2015, income subject to Social

Security tax will increase from $117,000

to $118,500 with the employee portion

taxed at 6.2%.

Key Tax Laws Extended

A number of popular tax deductions have

not had their provisions made permanent

within the tax code. These on-again, off-

again tax provisions ARE NOT available in

2015. This may change so please keep

required documentation in case Congress

changes their minds once again. Key

among them are:

The $250 “above-the-line” deduction

for unreimbursed classroom expenses

for qualified elementary and secondary

school teachers.

Important 2015 tax changes

2015 TAX RETURN

The $250 “above-the-line” deduction for

unreimbursed classroom expenses for

qualified elementary and secondary

school teachers.

The option to use general sales tax as

an itemized deduction option in lieu of

taking a state income tax deduction.

The deduction for qualified tuition and

educational expenses.

Deductibility of mortgage insurance

premiums as an itemized deduction.

Tax beneficial treatment of direct

charitable contributions from a

qualifying senior’s IRA.

50% Bonus Depreciation for assets

placed in service during the tax year.

Other Key 2015 Tax LawsEstate Taxes. In 2015, the maximum estate

tax is 40%. Up to $5,430,000 in assets are

sheltered from this tax. In addition, the

ability to transfer unused portions of your

estate tax exclusion to your spouse are now

a permanent part of the tax code.

Gift Taxes. The gift tax rates are re-unified

with estate taxes. This means the gift tax

exclusion amount for 2015 is $5.43 million

with a top gift tax rate of 40%. The annual

gift exclusion amount is $14,000 ($28,000

per couple).

Health Care Provisions. In 2015 there are

two Affordable Care Act tax provisions worth

noting.

Important 2015 tax changes

2015 TAX RETURN.

1. Shared Responsibility Payment. If you

do not have qualified health insurance

for yourself and your dependents you

will need to pay a fee. In 2015 the fee

is the higher of; 2% of your yearly

household income (1% in 2014) up to

the cost of the average qualifying

insurance premium OR $325 per

person ($162.59 per child under 18)

with a family maximum of $975 ($285

maximum in 2014). There are

exceptions to this fee if you meet

certain requirements including low

income and lack of affordable

insurance options.

2. Premium Tax Credit. If you purchase your

health insurance through a Marketplace

Exchange you could be eligible to receive

a credit to help cover the cost of your

insurance premium. The credit varies

depending on your location, your income,

number of dependents, and your health

plan classification. It is important to

accurately reflect your current situation

when you apply for this coverage through

the exchange. It is also important to

review your Form 1095-A for accuracy at

the end of each year. Making errors in

this area could result in unpleasant tax

surprises at the end of the year.

Important 2015 tax changes

2015 TAX RETURN

This limit is reduced by total purchases of

qualified property in excess of $200,000

($2 million in 2014). Section 179 allows

small business owners to expense versus

depreciate qualified property up to the

published limits.

Please remember that business

depreciation related provisions only

impact the timing of when you expense

your depreciation and not the total

amount of depreciation you may expense

over the life of the assets purchased.

Important 2015 tax changes

2015 TAX RETURN

Mileage Rates. The amount available for

qualified deduction of automobile use is:

Mileage Rates (per mile)

Item 2015 2014

Business 57.5¢ 56.0¢

Medical / Moving 23.0¢ 23.5¢

Charitable 14.0¢ 14.0¢

Business TaxesSection 179 Limits. The maximum

section 179 deduction for property

placed in service in 2015 is currently

$25,000 ($500,000 in 2014).

Home Office Safe Harbor Calculation.

Remember there is a simplified way to

take a home office expense for a portion

of your home. The expense is up to

$1,500 and replaces the cumbersome

allocation of valid home expenses

allocated by a percent of the home used

for business.

Common Business Credits Expire. A

number of other business tax provisions

expired and are no longer available in

2015. Some of the more common:

15-year straight line depreciation for

qualified leasehold improvements,

restaurant and retail improvements

Important 2015 tax changes

2015 TAX RETURN.

Research and Experimentation Tax Credit

New markets tax credit

Empowerment zone incentives

Work Opportunity Tax Credit

Biodiesel and alternative fuels incentives.

Special charitable deduction rules for

food inventory.

This is a brief summary of some of the most

broadly applicable tax changes in 2015.

There are also many other pre-programmed

changes built into the tax code. Should you

have any questions regarding your situation,

please call.

Itemized Deductions

Once all your income is reported it is time to focus on capturing ALL your allowable

deductions.

And while the IRS is getting very good at automatically notifying you if you under-report

your income, taxpayers are rarely given the same courtesy should they omit a valid

deduction.

How do you make sure you gather and retain the correct information? Provided here is a

list of the most common allowable itemized deductions.

Also included are tips to ensure you are given proper credit for all your valid deductions.

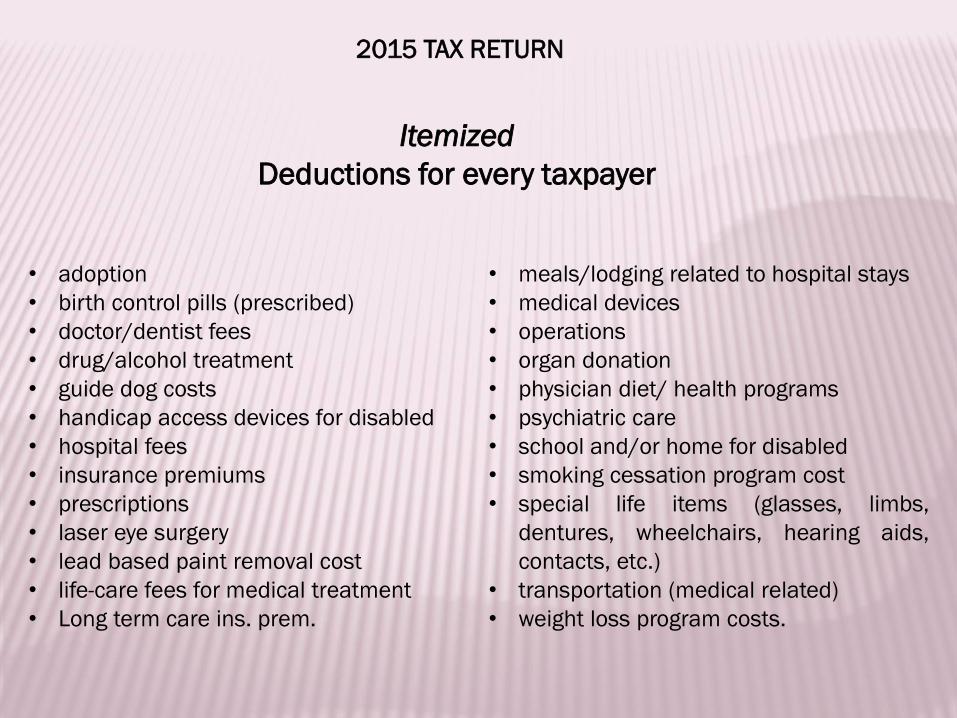

Medical & Dental CostsMedical and Dental expenses are generally deductible to the extent they exceed 10% of

your income (7.5% if age 65 or older). Some of the more common expenses:

2015 TAX RETURN

Itemized

Deductions for every taxpayer

• adoption

• birth control pills (prescribed)

• doctor/dentist fees

• drug/alcohol treatment

• guide dog costs

• handicap access devices for disabled

• hospital fees

• insurance premiums

• prescriptions

• laser eye surgery

• lead based paint removal cost

• life-care fees for medical treatment

• Long term care ins. prem.

• meals/lodging related to hospital stays

• medical devices

• operations

• organ donation

• physician diet/ health programs

• psychiatric care

• school and/or home for disabled

• smoking cessation program cost

• special life items (glasses, limbs,

dentures, wheelchairs, hearing aids,

contacts, etc.)

• transportation (medical related)

• weight loss program costs.

Itemized

Deductions for every taxpayer

2015 TAX RETURN

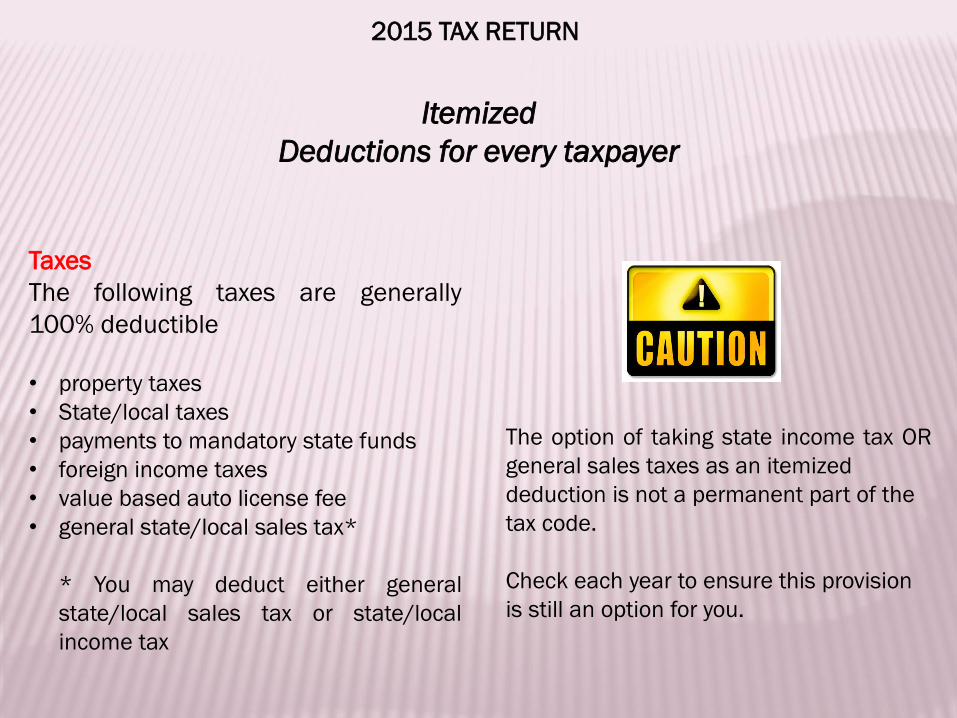

Taxes

The following taxes are generally

100% deductible

• property taxes

• State/local taxes

• payments to mandatory state funds

• foreign income taxes

• value based auto license fee

• general state/local sales tax*

* You may deduct either general

state/local sales tax or state/local

income tax

The option of taking state income tax OR

general sales taxes as an itemized

deduction is not a permanent part of the

tax code.

Check each year to ensure this provision

is still an option for you.

2015 TAX RETURN

Itemized

Deductions for every taxpayer

Charitable ContributionsBoth cash and property are generally

deductible if donated to qualified

organizations as:

• Churches

• non-profit schools

• non-profit hospitals

• public parks

• boy & girl scouts

• war/veterans groups

• YMCA/YWCA

• environmental/conservation groups.

• agencies such as:

o Red Cross,

o Salvation Army,

o Goodwill, CARE,

o United Way, etc.

2015 TAX RETURN

TIPS: All cash donations now require a

bank record or receipt.

Make sure you keep track of your

mileage to and from the charity. It is

also deductible.

Only donate your vehicle to a

qualified charity that uses, improves

or sells the vehicle at full market

value. If the charity sells your vehicle

without using or improving the

vehicle, your deduction is limited to

the gross proceeds from the sale

and not what could be a higher “fair

market value”.

Make sure donated clothing is in

good or better condition.

Itemized

Deductions for every taxpayer

Casualty & Theft Losses

Casualty and Theft losses are generally deductible to the extent they exceed

10% of your adjusted gross income, are not reimbursable via insurance, and

each event exceeds $500.

Examples include:

• fire

• theft

• natural loss: tornado, hurricane, flood, etc.

• car accident

• vandalism

• other accidents.

Itemized

Deductions for every taxpayer

2015 TAX RETURN

Most miscellaneous deductions are

only deductible to the extent they

exceed 2% of your adjusted gross

income. Items with an “*” are usually

not subject to this income threshold.

• gambling losses to offset gains*

• handicapped job related expenses*

• work uniforms

• un-recovered annuity costs*

• job hunting expenses

• safe deposit box cost

• tax prep fees

• employee business expenses

• IRA/KEOGH administration fees

• business use depreciation

• certain legal fees

• trust administration fees

• hobby expense to offset gains

• 50% of business related meals;

entertainment

• classroom material expense for teachers

• repayments of income*

• repayments of Social Security

• investment related expenses

• in-home office expenses

• job required medical exam

• job required education expenses

2015 TAX RETURN

Miscellaneous Deductions

Itemized

Deductions for every taxpayer

The following are common non-deductible

items:

• accidental damage

• blood donation

• club dues

• commuting expenses

• cosmetic surgery

• drought losses

• estate/gift taxes

• funeral expenses

• gifts to foreign organizations

• gifts to “for profit” groups

• gifts to individuals

• home repairs

• labor union donations

• license fees

• life insurance premiums

• lost property

• non-essential education

• non-health related household help

• health club dues

• PAC donations

• political donations

• property assessments

• raffle tickets

• sales taxes (unless in lieu of state

income taxes)

• Soc. Sec./Medicare

• tax penalties

• termite/insect damage

• tickets and fines

Itemized

Deductions for every taxpayer

2015 TAX RETURN

Non-deductible Expenses

TIPS: Expense Shifting Whenever possible shift

expenses into categories of itemized

deductions to surpass the IRS thresholds

in a given year

Miles, Miles, Miles Capture all your mileage

for business travel, charitable travel and

medical travel. Keep a log book in your car

and note the miles to and from the doctor.

Track the miles to drop off charitable

donations. This area of deductible expense

is often not taken or is poorly captured.

Missing a few things What is deductible?

What is not? When in doubt save the

canceled check, the proof of payment, and

receipt. Without the proof, the expense

cannot be taken.

No cash donations How many times

have you dropped off a bag of clothes

or a lamp and not keep a record of the

gift? Keep a list of items you plan to

give away. Put the list next to or inside

the bag. The required itemization of

items donated can be prepared when

the bag is ready to be dropped off at

your favorite charity.

Donation Traps You must now have a

bank statement, canceled check, or

receipt for all cash donations. So, write

checks to your church versus cash.

Send in a check to the Salvation Army

or favor charity instead of putting cash

in the kettle.

Itemized

Deductions for every taxpayer

2015 TAX RETURN

#FreedomDrivesProgress